Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2017 - 2023 |

| Market Size (2025) | USD 1.79 Billion |

| Market Size (2030) | USD 2.31 Billion |

| Growth Rate (2025 - 2030) | 5.24% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Crop Protection Chemicals Market Analysis by Mordor Intelligence

The Canada Crop Protection Chemicals Market size is estimated at 1.79 billion USD in 2025, and is expected to reach 2.31 billion USD by 2030, growing at a CAGR of 5.24% during the forecast period (2025-2030).

Canada's agricultural sector continues to evolve, with significant expansions in cultivated areas driving the demand for crop protection chemicals. Between 2019 and 2022, the country's agricultural area increased by 785,700 hectares, reflecting the sector's robust growth trajectory. This expansion has been accompanied by intensified farming practices and diversification of crop portfolios, including major crops like wheat, canola, barley, and high-value fruits such as apples and blueberries. The agricultural sector's transformation has necessitated more sophisticated and efficient crop protection products, particularly in regions experiencing increased pest pressures and changing climate patterns.

The industry has witnessed substantial technological advancements and strategic collaborations in 2023, aimed at developing more effective and sustainable crop protection solutions. Notable developments include Bayer's partnership with Oerth Bio to develop next-generation crop protection products utilizing innovative protein degradation technology. Similarly, ADAMA's introduction of new products like Davai A Plus and Clearfield Broad-Spectrum Herbicide Solutions for imidazolinone-tolerant legumes demonstrates the industry's commitment to crop-specific protection solutions. These innovations reflect a broader industry shift toward more targeted and environmentally conscious pest management approaches.

Pest management challenges continue to significantly impact Canadian agriculture, with various crops facing substantial yield losses due to pest infestations. In Eastern Canada, failure to control weeds has led to a significant 10% potential yield loss in soybeans, amounting to approximately USD 32 million in economic impact. The Colorado potato beetle poses a particularly severe threat, capable of causing crop reductions ranging from 20% to 100% in potato yields, primarily through foliage damage. These challenges have spurred the development of more effective pest control strategies and integrated pest management approaches.

The industry is increasingly focusing on sustainable and precision agriculture practices, with companies developing innovative solutions that minimize environmental impact while maximizing efficacy. Syngenta's launch of Victrato, a new seed treatment technology in 2023, exemplifies this trend, offering protection against harmful nematodes and diseases across multiple crop types. The industry's emphasis on sustainability is reflected in the development of products with reduced environmental footprints, improved targeting capabilities, and enhanced resistance management properties. This shift aligns with growing regulatory scrutiny and increasing farmer awareness about the importance of sustainable agricultural practices.

Canada Crop Protection Chemicals Market Trends and Insights

Adoption of various sustainable agriculture practices and IPM techniques lead to a reduction in the consumption of pesticides for hectare

- Farmers in Canada are adopting integrated pest management (IPM) techniques, crop rotation, and other sustainable farming practices, which are reducing the reliance on chemical pesticides. Increased awareness and understanding of the environmental impact of pesticides led to a shift toward more eco-friendly alternatives. The country experienced a decrease in the consumption of pesticides, from 3.02 thousand metric ton per hectare to 2.5 thousand metric ton per hectare during 2017-2022.

- The Canadian government has instituted regulations and policies to foster responsible pesticide use, promote sustainable agriculture, and safeguard the environment, consequently influencing the pesticide market in the country. In 2020, the government introduced a sustainable agriculture plan to reduce pesticides in Québec over the next decade.

- Canada's organic industry emerged as one of the fastest-growing industries. Increased investment in this industry and governmental initiatives, such as providing subsidies and implementing favorable schemes, are projected to hinder the demand for synthetic pesticides. In 2022, the Canadian government allocated approximately USD 103,400 to the Organic Federation of Canada, facilitating a collaborative effort to foster sustainability and growth within the country's organic industry.

- However, rising temperatures and changing weather conditions may create more favorable environments for pests and diseases to thrive, leading to increased pressure on crops. In response to these challenges, farmers might need to use more pesticides to control pests and prevent the spread of diseases to protect their crops and ensure food security.

Growing demand and changes in import tariffs are significantly impacting the costs of active ingredients in the country

- Canada's agricultural industry depends considerably on agrochemicals to protect crops and boost yields. However, the country faces a significant dependence on the import of these pesticides. In 2021, Canada imported USD 1.85 billion in pesticides, establishing it as the fourth-largest global pesticide importer. As a result of this dependency on imports, pesticide prices are significantly impacted by currency exchange rates, import tariffs, and duties. These factors contribute to market fluctuations and instability.

- In 2022, cypermethrin was valued at USD 21.0 thousand per metric ton. Its widespread utilization in agriculture is due to its proficiency in managing diverse insect varieties, such as aphids, beetles, spotted bollworms, pink bollworms, and hairy caterpillars. Its proven efficacy has elevated its popularity among farmers aiming to protect their crops from pests and secure a fruitful yield.

- Atrazine, a systemic herbicide categorized as part of the chlorinated triazine family, is utilized to selectively target and control annual grasses and broadleaf weeds before germination. Formulations of herbicides containing atrazine are authorized for use on crops such as corn, sweet corn, sorghum, sugarcane, wheat, and guava. The recorded price for atrazine in 2022 stood at USD 13.8 thousand per metric ton.

- Malathion is an organophosphate insecticide used on a wide variety of food and feed crops to control many types of insects, such as aphids, fleas, leafhoppers, Japanese beetles, and other insect pests, on several crops. Five crops extensively grown in Canada that use malathion frequently are cherry tomato, broccoli, mulberry, cranberry, and fig. Malathion was valued at USD 12.5 thousand per metric ton in 2022.

Segment Analysis: Function

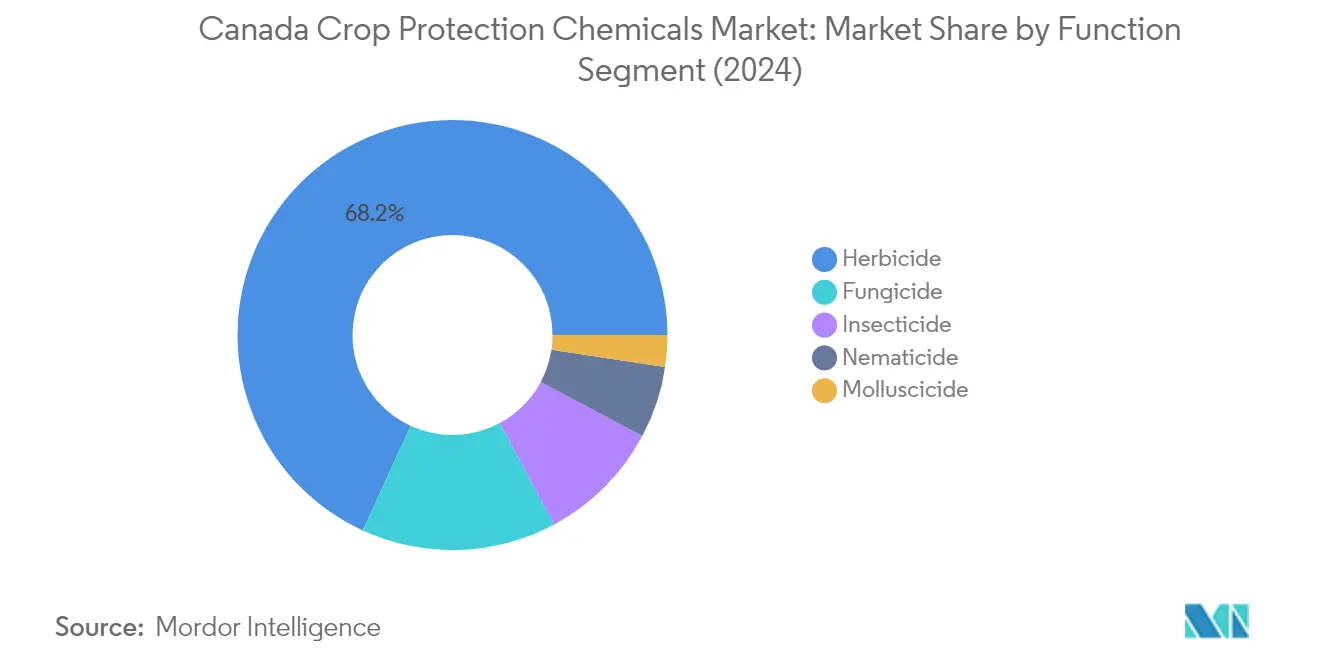

Herbicide Segment in Canada Crop Protection Chemicals Market

The herbicide segment dominates the Canadian crop protection chemicals market, commanding approximately 68% market share in 2024. This significant market position is driven by the critical need to control various devastating weeds that affect major crops in Canada. Canada thistle, wild mustard, kochia, and common lamb's quarters are among the primary weeds that pose substantial threats to crop production. In eastern Canada, weed interference leads to significant annual yield losses in soybeans, amounting to nearly USD 32 million. The situation is particularly critical in canola cultivation, which contributes an average of USD 29 billion to the economy annually, where weed interference during spring planting can result in potential financial losses reaching USD 2.14 billion. Soil treatment remains the most utilized method of herbicide application, accounting for a substantial portion of usage, as farmers proactively address weed issues through pre-emergent herbicides to enhance overall weed management effectiveness.

Herbicide Segment Growth in Canada Crop Protection Chemicals Market

The herbicide segment is projected to experience the strongest growth trajectory in the Canadian crop protection chemicals market, with an estimated growth rate of approximately 6.5% during 2024-2029. This robust growth is primarily driven by the increasing challenges posed by resistant weed species and the expanding agricultural activities across Canadian provinces. The substantial economic impact of weed interference on crop yields continues to motivate farmers to employ herbicides as an effective solution for weed control and productivity preservation. The segment's growth is further supported by ongoing developments in herbicide formulations that offer improved efficacy and environmental sustainability. The adoption of integrated weed management practices and the introduction of advanced herbicide technologies are expected to contribute significantly to this segment's expansion over the forecast period.

Remaining Segments in Function Segmentation

The Canadian crop protection chemicals market encompasses several other important segments, including fungicides, insecticides, molluscicides, and nematicides, each serving crucial roles in crop protection. Fungicides play a vital role in controlling various plant diseases, particularly in managing Fusarium head blight in wheat crops and other fungal infections affecting major Canadian crops. The insecticide segment addresses critical pest challenges, including the Colorado potato beetle and various other crop-damaging insects. Molluscicides are essential for controlling snails and slugs that pose threats to various crops, while nematicides help manage soil-borne pests that can significantly impact root health and overall crop productivity. These segments collectively provide farmers with a comprehensive toolkit for managing various crop threats and maintaining agricultural productivity.

Segment Analysis: Application Mode

Soil Treatment Segment in Canada Crop Protection Chemicals Market

Soil treatment has emerged as one of the dominant application methods in Canada's crop protection chemicals market, accounting for approximately 39% market share in 2024. This method involves the direct application of crop protection pesticides to the soil to combat soil-borne pests, diseases, and weeds, either before planting or after crop emergence. The segment's prominence is largely attributed to its effectiveness in applying pre-emergent herbicides, which specifically target weed seeds before crop sowing. Herbicides account for nearly 85% of soil treatment applications, demonstrating farmers' strong preference for this method in weed management. The method's popularity is further enhanced by its ability to provide comprehensive protection against various soil-borne pathogens while ensuring even distribution of active ingredients throughout the soil profile.

Soil Treatment Growth in Canada Crop Protection Chemicals Market

The soil treatment segment is projected to demonstrate robust growth in the Canadian crop protection chemicals market during 2024-2029, with an expected CAGR of approximately 6%. This growth trajectory is driven by several factors, including the method's proven effectiveness in controlling a wide range of soil-borne diseases, pests, and weed species. The increasing adoption of precision agriculture practices and the growing awareness among farmers about the benefits of preventive pest control measures are further propelling the segment's growth. Additionally, technological advancements in soil treatment equipment and formulations are making this application method more efficient and cost-effective for farmers, contributing to its expanding adoption across various crop types.

Remaining Segments in Application Mode

The other application methods in Canada's crop protection chemicals market include foliar application, chemigation, fumigation, and seed treatment, each serving specific purposes in crop protection. Foliar application offers precise delivery of pesticides directly to affected plant parts, while chemigation leverages irrigation systems for efficient pesticide distribution. Fumigation plays a crucial role in controlling soil-borne pathogens and pests through gaseous applications, particularly in high-value crops. Seed treatment provides targeted protection during the crucial early growth stages while minimizing environmental impact. These diverse application methods offer farmers flexibility in choosing the most appropriate approach based on their specific crop protection needs, environmental conditions, and operational requirements.

Segment Analysis: Crop Type

Grains & Cereals Segment in Canada Crop Protection Chemicals Market

The grains and cereals segment dominates the Canadian crop protection chemicals market, accounting for approximately 50% of the total market value in 2024. This significant market position is primarily driven by Canada's extensive cultivation of wheat, barley, and corn, especially in the Prairie province. The segment's prominence is further reinforced by the fact that wheat remains the main crop in Western Canada, accounting for approximately 60% of total grain production, with about 90% being exported. The segment's strong performance is supported by farmers' increasing adoption of crop protection products to combat various pathogens and pests that attack wheat, including Fusarium head blight (FHB), stripe rust, and leaf spots. Additionally, the segment demonstrates robust growth potential, with projections indicating it will maintain its market leadership position while expanding at a rate of around 6% during 2024-2029, driven by increasing agricultural yields and growing food security concerns that have encouraged farmers to adopt more sophisticated best crop protection practices.

Remaining Segments in Crop Type

The Canadian crop protection chemicals market encompasses several other important segments, including pulses & oilseeds, fruits & vegetables, commercial crops, and turf & ornamental applications. The pulses & oilseeds segment holds particular significance due to Canada's position as one of the largest suppliers of pulses globally, with farmers seeding an average of 3.5 million hectares annually. The fruits & vegetables segment plays a crucial role in crop protection, particularly in regions like Nova Scotia, Quebec, and Ontario, where diverse crops such as blueberries, apples, tender fruits, and various vegetables are cultivated. The commercial crops segment, though smaller, remains vital for specific cash crops, while the turf & ornamental segment serves specialized needs in the ornamental horticulture sector, particularly in Ontario, British Columbia, and Quebec, where floriculture represents a significant portion of total ornamental sales.

Competitive Landscape

Top Companies in Canada Crop Protection Chemicals Market

The Canadian crop protection company market is characterized by continuous product innovation and strategic partnerships among key players. Companies are actively investing in research and development to introduce novel active ingredients and formulations, particularly focusing on sustainable and environmentally friendly solutions. Strategic collaborations between major agrochemical companies have become increasingly common to share technologies, expand product portfolios, and strengthen market presence. Operational agility is demonstrated through investments in local manufacturing facilities and distribution networks to ensure reliable supply chains. Companies are also expanding their presence through acquisitions and partnerships with local distributors, while simultaneously developing digital platforms and services to provide comprehensive crop protection products to farmers. The focus on sustainable agriculture and integrated pest management has driven companies to develop bio-based alternatives and precision application technologies.

Consolidated Market Led By Global Players

The Canadian crop protection market is highly consolidated, dominated by large multinational corporations with established global presence and extensive research capabilities. These major players leverage their international experience, technological expertise, and robust distribution networks to maintain their market positions. The market structure favors companies with diverse product portfolios spanning multiple crop protection segments, allowing them to offer comprehensive solutions to farmers. Local players primarily operate as distributors or specialized product manufacturers, often forming strategic partnerships with global leaders to enhance their market reach.

The market has witnessed significant merger and acquisition activities, particularly among global agrochemical companies seeking to consolidate their positions and achieve economies of scale. These consolidations have resulted in increased market concentration, with the top companies controlling a substantial portion of the market share. The trend towards consolidation is driven by factors such as the need for enhanced research and development capabilities, access to new technologies, and the desire to expand geographic presence. Companies are also pursuing vertical integration strategies to strengthen their position across the value chain.

Innovation and Sustainability Drive Future Success

For incumbent companies to maintain and increase their market share, focusing on sustainable product development and digital integration will be crucial. Success factors include investing in research and development to create more effective and environmentally friendly formulations, developing resistance management solutions, and expanding bio-based product portfolios. Companies must also strengthen their distribution networks, provide comprehensive technical support to farmers, and leverage digital technologies for precision agriculture. Building strong relationships with key stakeholders, including farmers, agricultural institutions, and regulatory bodies, will be essential for long-term success.

Contenders looking to gain ground in the market need to focus on specialized market segments and develop innovative solutions for specific crop protection challenges. This includes identifying underserved market niches, developing cost-effective alternatives to existing products, and establishing strategic partnerships with established players. The increasing focus on sustainable agriculture and stricter regulatory requirements presents opportunities for companies offering environmentally friendly solutions. Success will also depend on building efficient distribution networks, providing excellent customer service, and developing strong technical expertise in specific crop segments. Companies must also consider potential regulatory changes regarding pesticide use and environmental protection, adapting their strategies accordingly.

Canada Crop Protection Chemicals Industry Leaders

BASF SE

Bayer AG

Corteva Agriscience

FMC Corporation

Nufarm Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2023: ADAMA introduced new products, Davai A Plus and Clearfield Broad-Spectrum Herbicide Solutions, for imidazolinone-tolerant legumes like lentils, peas, and soybeans.

- January 2023: For the Canadian horticulture market, Gowan Canada Inc. introduced Magister SC Miticide. The product provides rapid action against certain species of mites in both Eriophyidae and Tetranychidae families and pear psylla.

- January 2023: Bayer formed a new partnership with Oerth Bio to enhance crop protection technology and create more eco-friendly crop protection solutions.

Canada Crop Protection Chemicals Market Report Scope

Fungicide, Herbicide, Insecticide, Molluscicide, Nematicide are covered as segments by Function. Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.Function

| Fungicide |

| Herbicide |

| Insecticide |

| Molluscicide |

| Nematicide |

Application Mode

| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

Crop Type

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

| Function | Fungicide |

| Herbicide | |

| Insecticide | |

| Molluscicide | |

| Nematicide | |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental |

Market Definition

- Function - Crop Protection Chemicals are apllied to control or prevent pests, including insects, fungi, weeds, nematodes, and mollusks, from damaging the crop and to protect the crop yield.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms