Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

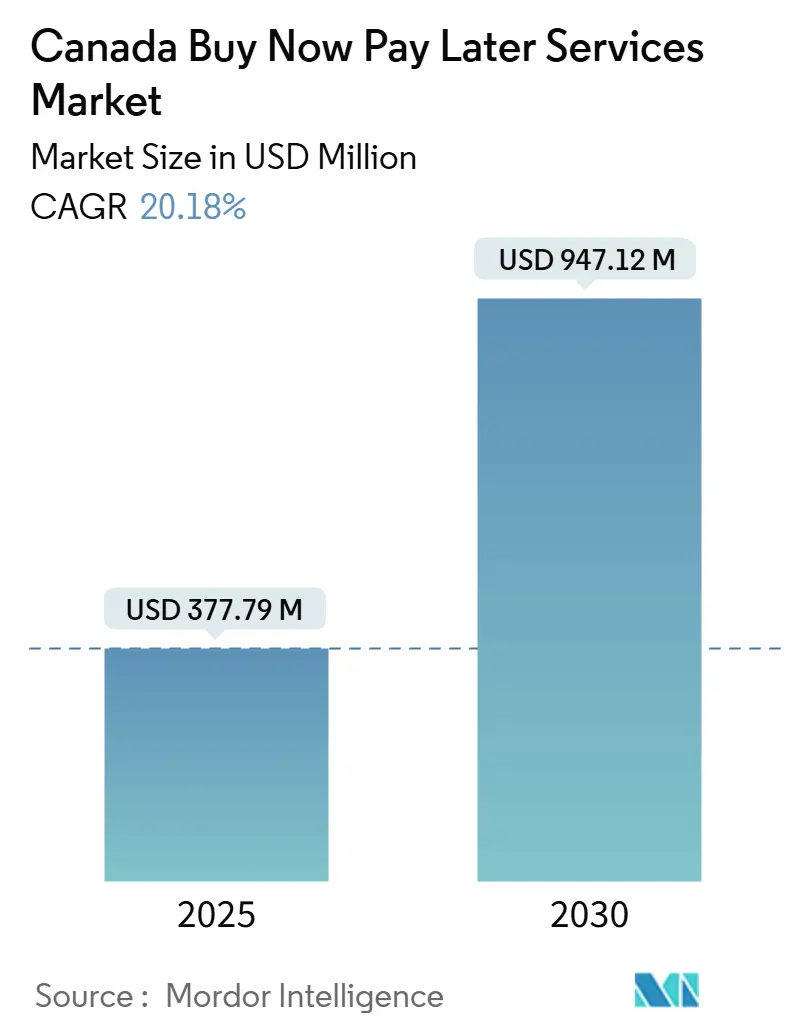

| Market Size (2025) | USD 377.79 Million |

| Market Size (2030) | USD 947.12 Million |

| Growth Rate (2025 - 2030) | 20.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Buy Now Pay Later Services Market Analysis by Mordor Intelligence

The Canada Buy Now Pay Later market size stood at USD 377.78 million in 2025 and is projected to climb to USD 947.12 million by 2030, advancing at a 20.18% CAGR, underscoring the brisk expansion of the Canada Buy Now Pay Later market. Rising e-commerce turnover, the 35% criminal-interest-rate cap that took effect on 1 January 2025, and the forthcoming Real-Time Rail (RTR) settlement network are steering consumers away from revolving credit and toward interest-free installments. BNPL penetration deepened as online shopping reached CAD 74 billion (USD 54.2 billion) in 2025 and 78% of Canadians bought goods digitally, with mobile devices generating 40% of those transactions. Banks are countering fintech momentum by rolling out zero-interest installment options for existing cardholders, while fintechs are broadening merchant networks and exploring healthcare, home improvement, and immigrant-lending niches. Regulatory tightening, elevated delinquency rates, and data-privacy constraints weigh on margins, yet real-time account-to-account rails, open-banking write access, and richer cash-flow data promise long-run efficiency gains for the Canada Buy Now Pay Later market.

Key Report Takeaways

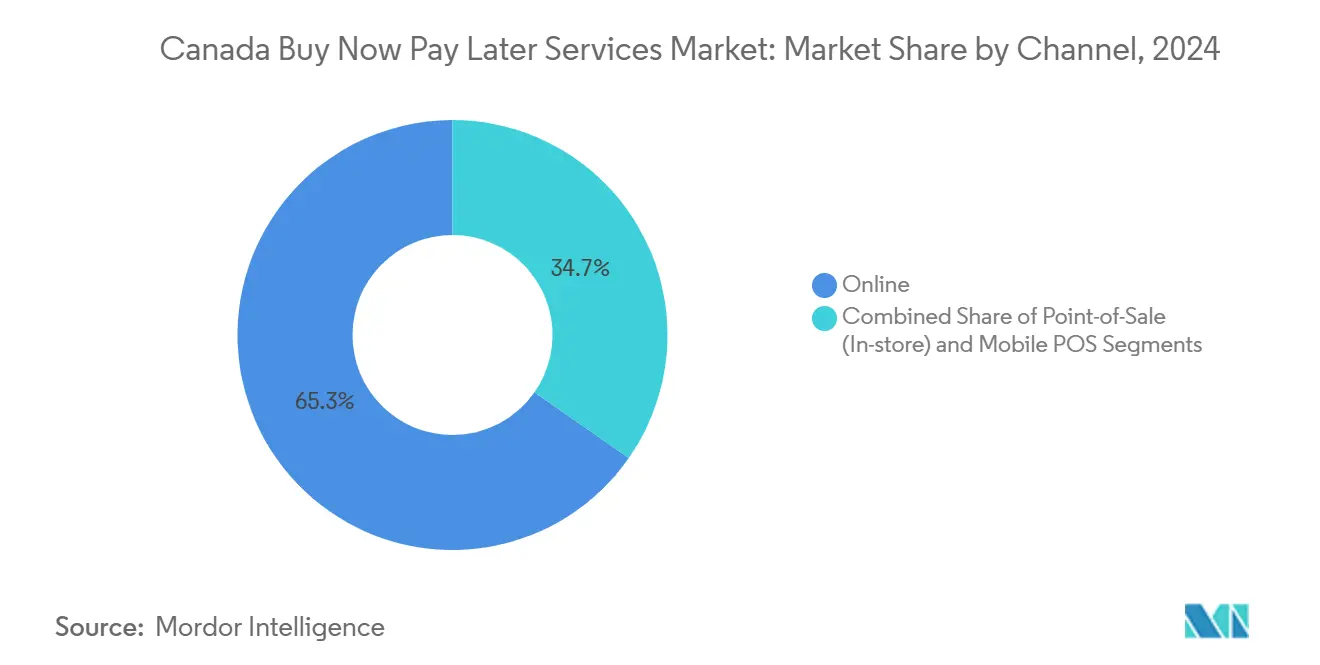

- By channel, online checkouts commanded 65.3% of the Canada Buy Now Pay Later market share in 2024, whereas mobile point-of-sale is forecast to post a 22.1% CAGR through 2030.

- By enterprise size, large companies held 72.8% share of the Canada Buy Now Pay Later market size in 2024, while small and medium enterprises (SMEs) are projected to expand at a 21.63% CAGR between 2025 and 2030.

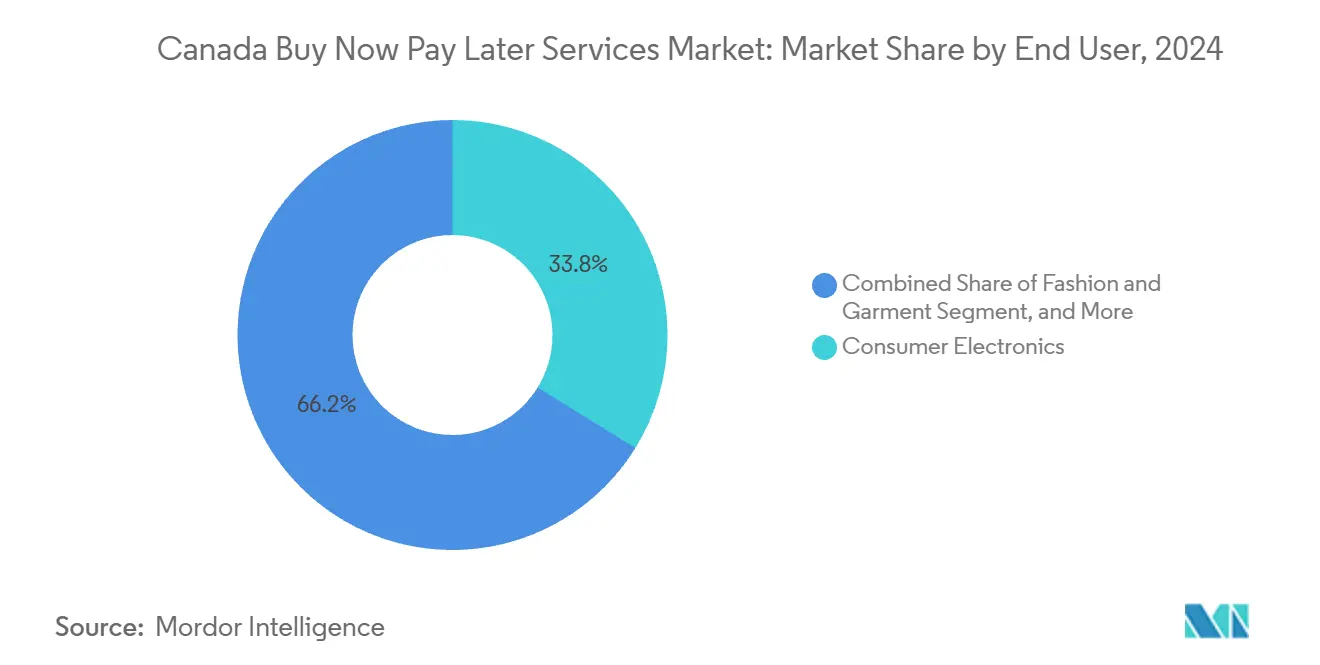

- By end user, consumer electronics led with 33.8% revenue share in 2024; healthcare is poised to grow at a 24.18% CAGR to 2030.

- By payment structure, Pay-in-4 plans captured 47.02% of the Canada Buy Now Pay Later market size in 2024, whereas Pay-in-12 options are expected to accelerate at a 22.51% CAGR over the forecast period.

Canada Buy Now Pay Later Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce transactions | +4.2% | Ontario, British Columbia, nationwide online shoppers | Medium term (2-4 years) |

| Consumer preference for interest-free installments | +3.8% | Millennials and Gen Z in Quebec, Alberta; national | Short term (≤ 2 years) |

| Increasing merchant adoption to boost conversion | +3.5% | Ontario, British Columbia, Quebec retail hubs | Medium term (2-4 years) |

| Integration with open banking and real-time rails | +2.9% | Nationwide, strongest post-RTR launch | Long term (≥ 4 years) |

| Demand from immigrant and thin-file consumers | +2.1% | Ontario, British Columbia newcomer centers | Medium term (2-4 years) |

| Healthcare financing tie-ups | +1.8% | Ontario, Alberta, British Columbia clinics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in E-commerce Transactions

Online retail sales climbed to CAD 74 billion (USD 54.2 billion) in 2025, and 78% of Canadians shopped on the web, creating a structural pull for BNPL at checkout. Digital share of total retail advanced from 5.8% in 2019 to 7.2% in 2024, while mobile devices accounted for 40% of digital purchases, favoring one-click BNPL approvals for fashion, electronics, and home goods. The Bank of Canada observed that cards still dominate by value, yet 29% of cardholders revolve balances, highlighting appetite for interest-free alternatives. Shopify’s two-million-merchant base embeds BNPL in cart flows, and Moneris, Canada’s top acquirer, routes installment offers at scale. An NBER working paper estimated that BNPL raises merchant sales about 20%, prompting retailers to absorb discount fees of 2–6%.[1] National Bureau of Economic Research, “BNPL Impact on Merchant Sales Study,” nber.org

Consumer Preference for Interest-Free Installments

The 35% APR ceiling, effective 2025 and climbing, household debt-service ratios redirect borrowers toward zero-fee BNPL plans that preserve cash flow. TransUnion recorded a 1.74% 90-day delinquency rate on non-mortgage credit in Q2 2024, up 22 bps year over year, while card balances grew 4.7%. FICO’s Q1 2025 dataset showed payment rates sliding to 47% and two-plus-miss rates on monoline cards reaching 6.3%. A PayPal poll found 60% of respondents willing to try BNPL if fees were absent, with strong interest in appliances and electronics. Millennials and Gen Z in Quebec and Alberta adopt faster after 2024 provincial disclosure rules clarified the total borrowing cost.

Increasing Merchant Adoption to Boost Conversion

Eighty-five percent of merchants surveyed by PYMNTS reported higher BNPL usage, and 40% already offer installment plans. Shopify and Affirm launched Shop Pay Installments nationally in summer 2025, giving two million storefronts instant access to plans ranging from 0% to 31.99% APR. Square added Afterpay to its terminals to extend BNPL in physical stores, and Lightspeed replicated the strategy in hospitality and specialty retail. PayPal’s November 2025 rollout of Pay in 4 across Home Depot, Sephora, and Ticketmaster underscored BNPL’s shift from a niche to baseline payment rail. Retailers without installment plans risk basket attrition to rivals that advertise flexible terms.

Integration with Open Banking and Real-Time Rails

Budget 2025 locked in phased open-banking rules, read access in 2025 and write access from mid-2027. RTR, scheduled for 2026, will clear instant account-to-account transfers, slashing card network fees for BNPL providers. Payments Canada invited fintechs to join RTR directly, bolstering reach. Interac’s November 2025 launch of KONEK, backed by the six largest banks, marked incumbents’ bid to safeguard payment flows ahead of open-banking write access. Nuvei’s May 2025 pact with Mastercard Move for rapid merchant payouts shows infrastructure convergence accelerating. Yet PIPEDA requires explicit consent for alternative data underwriting, tempering the scale speeds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory scrutiny by FCAC and provinces | -2.3% | British Columbia, Quebec, Ontario | Short term (≤ 2 years) |

| Elevated default risk in macro slowdowns | -1.9% | Alberta, nationwide | Medium term (2-4 years) |

| Bank-led in-house installment plans | -1.6% | All provinces via cardholders | Medium term (2-4 years) |

| Data-privacy limits on AI underwriting | -1.2% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Scrutiny by FCAC and Provinces

The Financial Consumer Agency of Canada mandated plain-language cost disclosures in 2024, while British Columbia’s Bill 19 and Quebec’s Bill 72 tightened advertising rules and added cooling-off periods, inflating compliance costs for smaller fintechs. The Retail Payments Activities Act extended Bank of Canada oversight to BNPL operators, layering operational risk, cybersecurity, and reporting standards.[2]Bank of Canada, “Real-Time Rail Infrastructure,” bankofcanada.ca Budget 2025 introduced stablecoin and AML requirements, as well as a new Financial Crimes Agency, adding complexity for platforms experimenting with crypto payments. The 35% APR ceiling hit subprime-focused lenders such as Mogo, which warned of an 8–10% revenue dip in 2025. Altogether, enforcement is tightest in British Columbia, Quebec, and Ontario, squeezing margins and deterring new entrants.

Elevated Default Risk in Macro Slowdowns

FICO data showed payment rates at 47% in Q1 2025 and monoline card two-plus-miss delinquencies at 6.3%, revealing fragile consumer liquidity. TransUnion found 90-day non-mortgage delinquency at 1.74% in Q2 2024, with card balances still rising. The Bank of Canada notes that 29% of cardholders carry revolving balances, exposing them to rate shocks. Afterpay’s parent, Block, reported 96% on-time installment repayment but acknowledged sensitivity to Alberta’s commodity cycles. Affirm’s 96% repeat-customer ratio indicates loyalty among prime borrowers, yet first-time or subprime users pose higher loss risk in downturns. Providers are raising merchant discount rates and trimming credit limits to offset expected losses, which can dampen transaction growth for the Canada Buy Now Pay Later market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Channel: Mobile POS Drives In-Store Convergence

Mobile point-of-sale (mPOS) transactions are forecast to grow at a 22.1% CAGR from 2025 to 2030, chipping away at the 65.3% share that online checkouts commanded in 2024 within the Canada Buy Now Pay Later market. Square, Lightspeed, and Shopify POS integrate installment plans at physical tills, allowing retailers to replicate e-commerce flexibility in-store. PayPal’s Pay in 4 launch, spanning Home Depot and Sephora, underscores in-store demand for frictionless financing.

In-store orders typically have higher average ticket values for furniture, appliances, and home improvements. Interac’s KONEK network, first deployed at Staples Canada, enables direct-from-bank payments that bypass card rails, hinting at future disintermediation of conventional BNPL providers. Younger shoppers in Vancouver and Toronto are increasingly using smartphone wallets at checkout, reinforcing omnichannel adoption and solidifying the Canada Buy Now Pay Later market footprint across sales channels.

By Enterprise Size: SMEs Narrow the Gap

Large enterprises controlled 72.8% of the Canada Buy Now Pay Later market share in 2024, yet SMEs are projected to expand 21.63% annually through 2030 as turnkey integrations lower entry barriers. Shop Pay Installments lets even micro-sellers activate financing without custom code, while Square’s Afterpay embed targets small retailers.

PYMNTS found that 85% of merchants offering BNPL report higher usage, a conversion bump that resonates with fashion and electronics boutiques operating on thin margins. Moneris’ standardized BNPL APIs further democratize access across merchant tiers. As SMEs scale, the Canada Buy Now Pay Later market size for this cohort is expected to rise steadily, diversifying revenue beyond enterprise clients.

By End User: Healthcare Financing Unlocks Elective Demand

Consumer electronics led in 2024, accounting for 33.8% of the Canada Buy Now Pay Later market size, driven by high-ticket devices and rapid refresh cycles at Best Buy and Apple stores. Conversely, healthcare is set to expand at a 24.18% CAGR, the fastest among end users, driven by financing for dental, cosmetic, and fertility procedures ranging from CAD 500 to CAD 15,000 (USD 366–10,980).

Humm Canada, LendCare, and Affirm doubled their healthcare merchant bases by partnering with clinics that pre-qualify patients to curb defaults. PayPal surveys show 31% of respondents are open to financing appliances and 26% electronics, but gaps in elective medical coverage suggest headroom for BNPL growth in clinics. As higher-ticket treatments migrate online, longer-tenor plans deepen penetration, expanding the Canada Buy Now Pay Later market.

By Payment Structure: Longer Tenors Gain Traction

Pay-in-4 plans held 47.02% of the Canada Buy Now Pay Later market share in 2024, favored for fashion, small electronics, and home goods. Pay-in-12 products are projected to grow at 22.51% CAGR through 2030 as consumers finance healthcare, furniture, and renovations.

Royal Bank of Canada’s PayPlan and CIBC’s Pace It offer 36-month terms for prime customers, while Shopify-Affirm supports multiple tenor options at up to 31.99% APR. The 35% APR ceiling nudges subprime lenders out of longer-tenor space, concentrating growth among prime and near-prime borrowers. This structural tilt toward higher-value baskets expands the total Canada Buy Now Pay Later market revenue, even as unit volumes moderate.

Geography Analysis

Ontario leads the Canada Buy Now Pay Later market due to dense e-commerce volumes and early merchant integrations in the Greater Toronto Area. Quebec follows, propelled by French-language platforms that comply with Bill 96 and Bill 72 consumer-protection mandates, boosting trust and take-up. British Columbia ranks third, with Vancouver’s tech-savvy consumers fueling 22.1% CAGR in mPOS adoption.

Alberta’s resource-linked economy produces higher income but also volatility; defaults rise during commodity downturns, tempering BNPL expansion yet sustaining longer-tenor demand among prime borrowers in Calgary and Edmonton. The rest of Canada, which includes Saskatchewan, Manitoba, the Atlantic provinces, and the territories, lags due to lower population density and fewer merchant integrations, although Shopify’s national footprint continues to expand, providing BNPL access.

RTR and KONEK infrastructure investments concentrate initially in Ontario, Quebec, and British Columbia, where transaction volumes justify the costs. Statistics Canada reports that 14.8% of newcomers are credit-invisible, compared to 7.5% of native-born Canadians, a gap that BNPL helps bridge. Nova Credit’s ties with RBC, Scotiabank, and Equifax let immigrants port overseas histories, spurring adoption especially in Ontario and British Columbia landing points.[3]Statistics Canada, “E-commerce and Digital Economy Statistics 2025,” statcan.gc.ca

Competitive Landscape

Competition is moderate, with global fintechs such as Affirm, Klarna, Sezzle, and PayPal challenging incumbent banks. RBC, CIBC, Scotiabank, and TD offer zero-interest installment plans that leverage existing cards and bypass merchant fees, directly cannibalizing fintech market share. Shopify’s Shop Pay Installments, powered by Affirm, positions the fintech to serve more than two million Canadian merchants. Klarna’s September 2025 IPO at a USD 15 billion valuation underscores investor faith in global BNPL reach.

White-space opportunities sit in healthcare financing, immigrant credit access, and high-ticket categories. Humm Canada and LendCare offer medical financing with APRs ranging from 9.9% to 29.9%, capturing unmet demand for elective procedures. Interac’s KONEK network represents banks’ proactive defense as open-banking write access nears, with Staples Canada as its first live merchant.

Emerging disruptors include Flexiti in the home improvement and healthcare segments, and Mogo, which is pivoting toward prime borrowers after facing revenue pressure from rate caps. Block’s Afterpay maintains 96% on-time payments, while Affirm logged 41.4 million transactions in Q1 FY 2026, up 52.2% year over year. Strategic variations in underwriting, tenor mix, and data partnerships will determine share trajectories within the Canada Buy Now Pay Later market.

Canada Buy Now Pay Later Services Industry Leaders

Afterpay Limited

Sezzle Inc.

ZIP Co Limited

Klarna Bank AB

Affirm Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: PayPal introduced Pay in 4, permitting customers to split CAD 30–1,500 transactions into four interest-free payments across Home Depot, Sephora, and Ticketmaster, intensifying rivalry in the Canada Buy Now Pay Later market.

- November 2025: Interac and Canada’s six largest banks launched KONEK, a real-time A2A network, with Staples Canada as the first merchant, aiming to pre-empt fintech disintermediation before 2027 open-banking write access.

- September 2025: Klarna completed a USD 15 billion NYSE IPO, shares rising 15% on day one, reaffirming investor confidence in cross-border BNPL expansion.

- May 2025: Nuvei partnered with Mastercard Move for near-instant merchant payouts, shrinking settlement windows from days to minutes.

Canada Buy Now Pay Later Services Market Report Scope

The Canada Buy Now Pay Later (BNPL) market refers to the financial services segment that enables consumers and businesses to purchase goods or services and pay for them over time through short-term, interest-free, or low-interest installment plans. This market includes online, in-store, and mobile point-of-sale financing options offered by fintech firms, banks, and retailers. It supports transactions across multiple end-use sectors, including electronics, fashion, healthcare, and BFSI. BNPL solutions help enhance purchasing power, improve checkout conversion rates, and offer flexible payment structures ranging from Pay-in-4 to longer installment plans.

The Canada Buy Now Pay Later Services Market Report is Segmented by Channel (Online, Point-of-Sale In-store, Mobile POS), Enterprise Size (Large Enterprises, Small and Medium Enterprises), End User (Consumer Electronics, Fashion and Garment, Banking Financial Services and Insurance, Healthcare, Other End Users), Payment Structure (Pay-in-4, Pay-in-6, Pay-in-12, Revolving Installment Plans), and Geography (Ontario, Quebec, British Columbia, Alberta, Rest of Canada). The Market Forecasts are Provided in Terms of Value (USD).

By Channel

| Online |

| Point-of-Sale (In-store) |

| Mobile POS |

By Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises |

By End User

| Consumer Electronics |

| Fashion and Garment |

| Banking, Financial Services and Insurance |

| Healthcare |

| Other End Users |

By Payment Structure

| Pay-in-4 |

| Pay-in-6 |

| Pay-in-12 |

| Revolving Installment Plans |

By Region

| Ontario |

| Quebec |

| British Columbia |

| Alberta |

| Rest of Canada |

| By Channel | Online |

| Point-of-Sale (In-store) | |

| Mobile POS | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End User | Consumer Electronics |

| Fashion and Garment | |

| Banking, Financial Services and Insurance | |

| Healthcare | |

| Other End Users | |

| By Payment Structure | Pay-in-4 |

| Pay-in-6 | |

| Pay-in-12 | |

| Revolving Installment Plans | |

| By Region | Ontario |

| Quebec | |

| British Columbia | |

| Alberta | |

| Rest of Canada |

Key Questions Answered in the Report

How fast is BNPL spending growing in Canada?

The Canada Buy Now Pay Later market is forecast to expand from USD 377.78 million in 2025 to USD 947.12 million by 2030, a 20.18% CAGR.

Which segment adds the most new volume?

Healthcare is the fastest mover, projected to rise at 24.18% CAGR as elective procedures adopt installment plans.

Do banks or fintechs dominate Canadian installments?

Banks control card-linked zero-interest plans for existing customers, but fintechs such as Affirm, Klarna, and PayPal lead merchant-integrated checkout financing.

What is driving merchant adoption?

Studies show BNPL raises conversion by roughly 20%, prompting 40% of Canadian retailers to integrate installments despite 26% discount fees.

How will real-time rails affect BNPL?

RTR and open-banking write access will allow direct bank debits, lowering network fees and enabling faster settlement for BNPL providers and merchants.

Are compliance costs rising?

Yes, FCAC guidelines, provincial rules, and the Retail Payments Activities Act impose new disclosure, cybersecurity, and reporting standards that raise operating costs.

Page last updated on: