Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

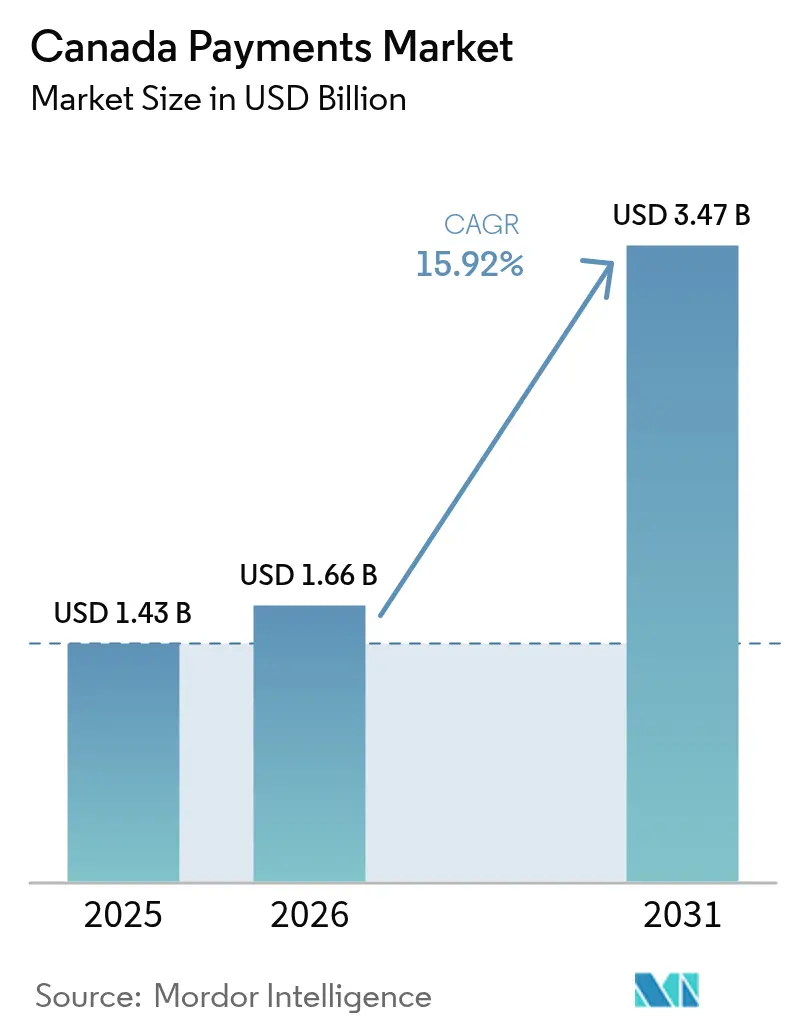

| Base Year Market Size (2025) | USD 1.43 Billion |

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 3.47 Billion |

| Growth Rate (2026 - 2031) | 15.92% CAGR |

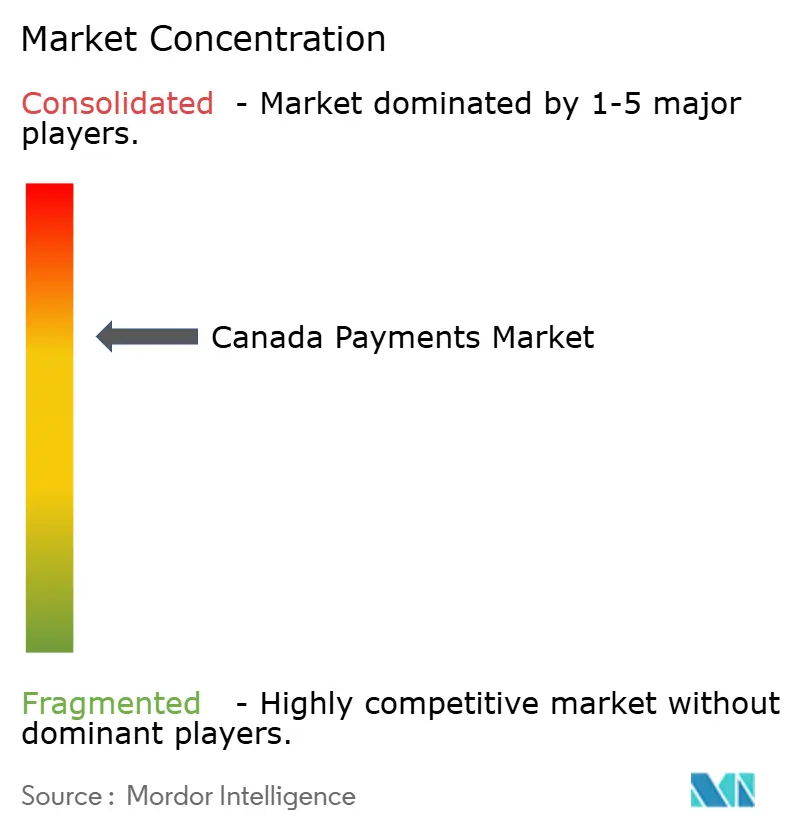

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Payments Market Analysis by Mordor Intelligence

The Canada payments market size is expected to grow from USD 1.43 billion in 2025 to USD 1.66 billion in 2026 and is forecast to reach USD 3.47 billion by 2031 at 15.92% CAGR over 2026-2031. Rapid regulatory modernization under the Retail Payment Activities Act (RPAA), accelerating contactless adoption, and the surge of e-commerce all reinforce a nationwide shift toward digital rails. The mandatory November 2024 registration of every payment service provider with the Bank of Canada boosts systemic trust and sets consistent risk-management baselines, which in turn fuels merchant and consumer confidence. Meanwhile, the federal agreement that trims interchange on small-ticket credit transactions to 0.95% improves merchant economics and redirects spending toward innovation. Growing dual-network contactless card issuance, together with Apple’s Tap-to-Pay rollout, signals a decisive pivot away from mag-stripe and chip-and-PIN architectures and redefines the competitive canvas for issuers, networks, and fintechs. Untapped upside remains in cross-border U.S.–Canada corridors, where harmonized rule sets and real-time settlement rails promise to unlock meaningful fee savings and faster liquidity cycles for exporters.

Key Report Takeaways

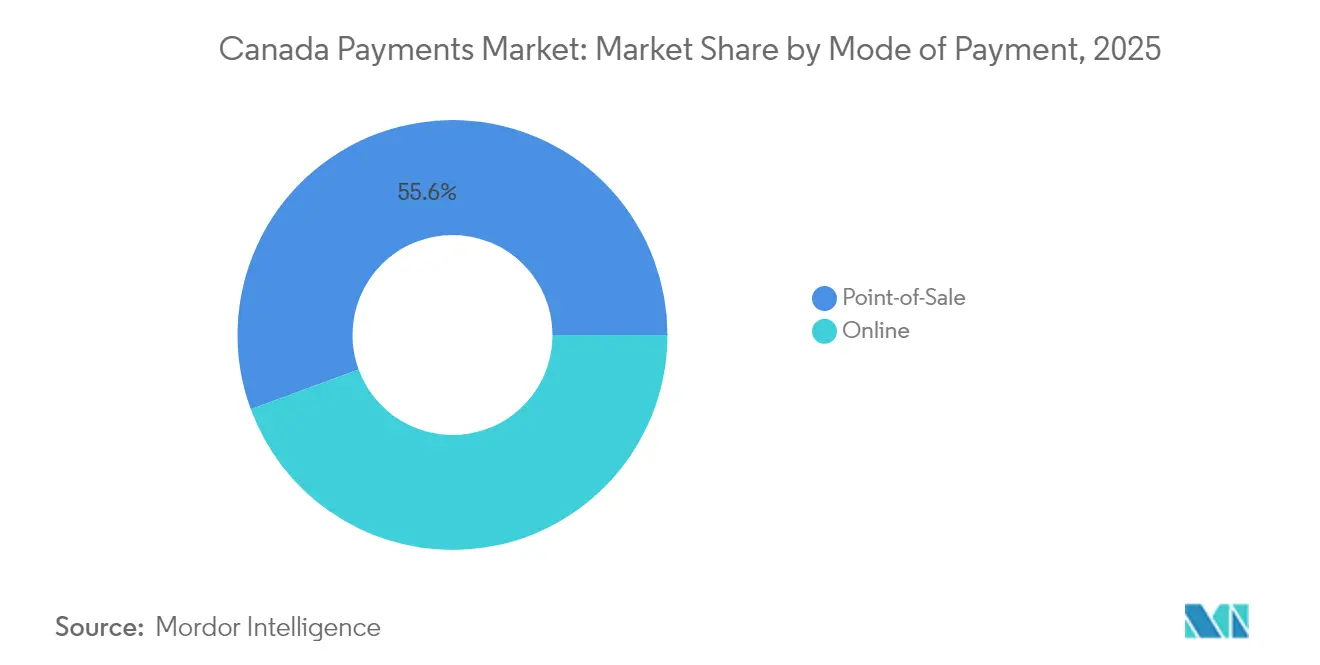

- By mode of payment, card transactions led with 44.60% revenue share in 2025, while digital wallets are projected to advance at an 17.82% CAGR to 2031. Overall Point-of-Sale led with 55.62% revenue share.

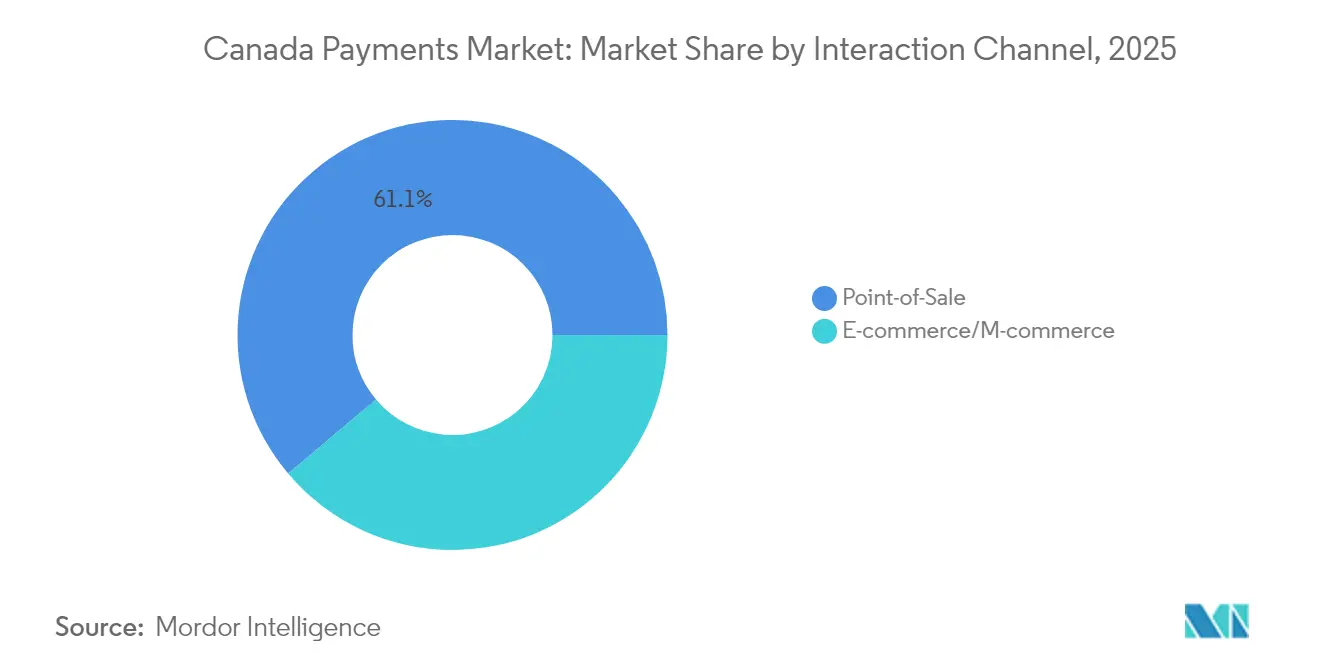

- By interaction channel, point-of-sale captured 61.15% of the Canada payments market share in 2025, whereas e-commerce and mobile channels are set to expand at an 17.84% CAGR through 2031.

- By transaction type, business-to-business flows accounted for 31.65% of the Canada payments market size in 2025; person-to-person transfers will accelerate at a 16.74% CAGR over the same horizon.

- By end-user industry, retail held 54.62% revenue share in 2025, with healthcare anticipated to grow at a 19.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid migration from Interac debit to dual-network contactless cards | +3.2% | National, with higher adoption in urban centers | Medium term (2-4 years) |

| BNPL regulation-light regime fuelling non-bank originations | +2.8% | National, excluding Quebec due to consumer protection laws | Short term (≤ 2 years) |

| Merchant surcharging rule-change boosting alternative rails adoption | +2.1% | National excluding Quebec, concentrated in retail sectors | Short term (≤ 2 years) |

| Provincial-level digital-ID roll-outs simplifying KYC | +1.9% | British Columbia, Ontario leading, gradual provincial expansion | Long term (≥ 4 years) |

| Expansion of U.S.–Canada cross-border e-commerce corridors | +1.7% | Border provinces, major urban centers with cross-border trade | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Migration from Interac Debit to Dual-Network Contactless Cards

Canadian issuers are pivoting toward dual-network debit credentials that combine Interac with Visa or Mastercard rails, giving consumers the flexibility to toggle between domestic low-cost clearing and globally accepted networks at checkout.[1]Reserve Bank of Australia, “Dual-Network Debit Card Reforms,” rba.gov.au Early adopters such as major banks report noticeable payment-routing savings as software decides the lowest-cost path in real time. Merchant enablement remains the key gating factor; however, the anticipated 2026 Real-Time Rail (RTR) launch should reduce settlement risk and improve liquidity for retailers that accept dual-network tokens. Real-estate services provider FCT already embeds Interac Verified IDs in property closings, underscoring how contactless credentials now extend well beyond general retail.[2]Financial Post, “FCT and Interac to Provide Verified ID in Real Estate,” financialpost.com

BNPL Regulation-Light Regime Boosting Non-Bank Originations

Unlike Australia or the European Union, Canada has opted for a principles-based BNPL framework under existing consumer-credit statutes rather than imposing new licensing obligations. Fintechs thus iterate products rapidly, capturing younger cohorts who prefer zero-interest instalments at checkout. Large banks counter by embedding split-payments into existing credit cards, defending cross-sell economics. The segment is forecast to jump from USD 6.69 billion in 2024 to USD 11.32 billion by 2030, equating to a double-digit compound clip that outpaces revolving credit growth. Policymakers signal ongoing monitoring to guard against consumer over-extension, but a heavy compliance overlay remains unlikely in the near term.

Merchant Surcharging Rule Change Accelerating Alternative Rails**

Effective October 2022, retailers may pass up to 2.4% of interchange directly to shoppers, a policy shift already embraced or under active consideration by roughly one-fifth of small businesses. Price-sensitive consumers increasingly sidestep surcharge lines by paying with debit, Interac e-Transfer, or account-to-account wallets, accelerating the 19.3% CAGR logged by alternative rails. Quebec’s legal carve-out complicates national rollout plans, yet anecdotal data show competitive pressure forcing multi-province chains to dual-price across most storefronts. Networks respond by promoting lower-fee small-ticket programs to sustain credit usage.

Provincial Digital-ID Rollouts Simplifying KYC

British Columbia’s Services Card and Ontario’s Verified.Me pilots are paving the way for a federated digital-ID backbone that slashes onboarding times across banking, insurance, and retail platforms.[3]GBBC, “Digital Identity in British Columbia,” gbbcouncil.org Interac’s credentialing service is now live in pilot real-estate closings, eliminating paper-based identity checks. Once scaled, the framework promises cost reductions for banks that spend millions on manual KYC reviews, while simultaneously elevating fraud-detection effectiveness. Long-term network effects should cascade into faster loan decisioning and real-time account opening, reinforcing digital payments penetration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interchange caps constraining issuer revenue pools | -2.4% | National, with concentrated impact on small business segments | Medium term (2-4 years) |

| Persistently high cash preference in rural Prairies & Atlantic Canada | -1.8% | Rural Prairies, Atlantic Canada, remote communities | Long term (≥ 4 years) |

| Data-localisation clause in Québec Bill-64 raising compliance costs | -1.3% | Quebec-specific, with spillover effects on national providers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Interchange Caps Constraining Issuer Revenue Pools

From October 2024, consumer credit interchange on qualifying small-business transactions cannot exceed 0.95%, a 27% drop that removes roughly USD 1 billion of income from issuers over five years. Card programmes recalibrate by trimming rewards accrual rates or charging subscription-like bundle fees. Over time, issuers are expected to channel investment into proprietary BNPL, value-added data APIs, and embedded finance plays to rebuild yield.

Persistently High Cash Preference in Rural Prairies & Atlantic Canada

Bank of Canada’s 2023 merchant survey confirms that 96% of SMEs still accept notes and coins, with 92% not planning to go cash-free. Patchy high-speed internet and an aging demographic underpin slower digital uptake. Ottawa’s Universal Broadband Fund continues to subsidize fiber deployment, yet logistical challenges in sparsely populated areas mean full coverage could be several years away. Providers therefore maintain hybrid acceptance stacks, supporting both cash and QR-based mobile payments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment – Point of Sale: Cards Lead Digital Transformation

Cards retained a 44.60% grip on in-store spend in 2025, giving them the single largest slice of the Canada payments market size at the physical checkout. Overall Point-of-Sale led with 55.62% revenue share. Dual-network contactless credentials now push tap-rate penetration above 81%, nudging consumers away from chip insert. Digital wallets, while still niche in bricks-and-mortar, are clocking an 17.82% CAGR, buoyed by Apple’s Tap-to-Pay entry that eliminates countertop hardware for micro-merchants. Cash still appears in 1 of every 5 rural purchases, confirming that omnichannel hardware strategies remain essential until high-speed coverage becomes universal. Forward-looking retailers invest in software defined terminals able to route transactions dynamically, seeking interchange optimization and loyalty integration.

Regulators stress risk controls under RPAA, mandating that every wallet operator document treasury, cyber, and operational safeguards. Fintechs leverage that clarity to court mid-market exporters, rearranging their payout flows into real-time bank pushes that bypass traditional acquirers. Fraud-rate headwinds on card-not-present (CNP) transactions accelerate migration toward tokenized wallet solutions, particularly in high-average-ticket segments like travel and luxury goods. Embedded BNPL inside wallets widens revenue pools without re-directing customers to third-party pages, strengthening platform stickiness.

By Transaction Type – B2B Dominance Meets P2P Innovation

Commercial payments represented 31.65% of aggregate transaction value in 2025, underscoring the primacy of B2B flows in the Canada payments market. Corporates demand richer remittance data and integrated reconciliation; consequently, API-based EFT aggregators and ERP plug-ins gain acceptance. On the consumer side, person-to-person transfers grow at 16.74% CAGR, fueled by the ubiquity of Interac e-Transfer, which settles within minutes and now layers request-to-pay functionality. Real-time disbursement use cases—insurance payouts and gig-wage releases—bridge the gap between B2B functionality and P2P UX expectations.

Risk oversight remains paramount: the Bank of Canada designated Lynx as a systemically important backbone, requiring enhanced contingency procedures. For small corporates, fintech portals that marry invoicing, FX hedging, and payment initiation sharply cut manual processes. Parallel momentum in remittances intensifies as corridors to South Asia and Latin America adopt retail wallets, thereby sidestepping high-fee wire services. Such developments broaden ecosystem stickiness and strengthen data-monetization prospects for networks.

By Interaction Channel – POS Stability Contrasts Online Acceleration

In-person commerce still drives 61.15% of national tender volume, confirming the resilience of traditional checkout experiences even as smartphone penetration exceeds 91%. The Canada payments market share for e-commerce channels is climbing, supported by an 17.84% CAGR through 2031. Holiday 2024 data indicated a 22% year-over-year spike in Black Friday payment counts, validating the need for elastic omnichannel capacity. Tourism spending reached CAD 23.3 billion (USD 17.2 billion) in Q4 2023, with a heavy skew toward mobile wallet usage by foreign visitors.

Mobile QR acceptance grows fastest in food-service and personal-care, where queue-busting and gratuity prompts lift average tickets. For car dealerships and other high-ticket merchants, hybrid checkout flows let customers scan a showroom QR, finance via BNPL, and e-sign on their phones, compressing sales cycles. Payment-facilitator models proliferate, giving micro-sellers sub-24-hour onboarding and consolidated chargeback management. In sum, channel convergence mandates orchestration layers capable of routing across POS, web, and in-app sessions under a single credential.

By End-User Industry – Retail Leadership Meets Healthcare Innovation

Retail dominated with 54.62% of 2025 inflows, reinforcing its role as first mover on contactless and loyalty-linked payments. High-frequency foot traffic and thin margins make cost-to-tender optimization a board-level KPI. Healthcare, projected to surge at 19.36% CAGR, accelerates digital invoice and co-pay adoption as clinics embrace upfront price transparency. Hospital procurement units layer dynamic discounting on EFT rails to capture early-pay rebates, reducing working-capital drag. OECD analyses of medical supply chain disruptions underscore the need for resilient settlement mechanisms that can reroute funds when suppliers shift geography.

Media and entertainment funnel recurring micro-charges through subscription wallets, yielding predictable ARPU. Hospitality operators retrofit PMS interfaces to handle multi-currency tips and instant refunds, essential features now that travel contributes 1.58% of GDP and sustains 682,500 jobs nationwide. Public-sector billers integrate digital ID to let citizens pay taxes or renew licenses without re-entering card data, decreasing friction and administrative overhead.

Geography Analysis

Ontario and British Columbia anchor the Canada payments market due to dense populations, vibrant technology ecosystems, and progressive regulatory pilots. These provinces enjoy near-universal broadband availability, enabling pervasive wallet and BNPL adoption across urban retail and service sectors. Quebec, however, imposes Bill 64 data-localization duties that create dual compliance tracks for national PSPs, raising entry barriers and elevating operating expenses. The legislation is prompting vendors to build province-specific data pods or contract licensed local processors, constraining smaller entrants.

The Prairie provinces combine high B2B agricultural trade flows with lower digital consumer uptake, producing a bifurcated opportunity landscape. Energy and commodities firms push high-value wires through Lynx, whereas rural general stores still favor cash, citing patchy LTE coverage. Atlantic Canada mirrors this profile but skews more toward tourism, amplifying the benefit of interchange relief for merchants posting annual Visa volumes under CAD 300,000 (USD 221,000). Seasonal swings in visitor inflows necessitate flexible acquiring fees and multi-currency settlement to support cruise-port terminals and hospitality operators. Cross-border corridors along Ontario-Michigan and British Columbia-Washington trade lanes exhibit above-average transaction velocity. Exporters exploit payment platforms that bundle logistics tracking and auto-FX, capturing cost saves up to 120 basis points versus legacy bank wires. The upcoming RTR is expected to integrate with U.S. instant rails, streamlining reconciliations and obviating daylight overdrafts. Market players that secure early participation rights are poised to capture disproportionate flows once the rail becomes production-ready in 2026.

Competitive Landscape

Market concentration is moderate. Interac, Visa, Mastercard, and Shopify collectively processed just over 70% of 2024 digital transaction volume, yet a long-tail of fintechs injects competitive vigor across niche verticals. The interchange cap compels networks and issuers to pivot toward value-added services—risk scoring, loyalty engines, and small-business analytics—leveraging their data reservoirs to retain relevance. Visa’s 2025 roadmap outlines expansion into account-to-account flows and near-real-time treasury solutions, reflecting a strategic hedge against card cannibalization.

Shopify’s merchant-of-record model blurs the line between e-commerce platform and payment processor, letting it internalize economics that acquirers traditionally captured. Its USD 8.9 billion revenue in 2024 evidences the scale at play and incentivizes peers such as Lightspeed to deepen payment attach rates. Interac focuses on security; its tokenization and verified-ID rails anchor not only peer-to-peer but upcoming request-to-pay and payroll disbursements, positioning the network as indispensable middleware for real-time retail.

Fintech upstarts—Neo Financial, KOHO, and Wealthsimple—target specific pain points: fee-free prepaid cards, high-interest cash accounts, and commission-free brokerage respectively. Their low overhead allows aggressive pricing that appeals to Gen Z and immigrant segments. Meanwhile, global processors like Stripe and Adyen bolster Canadian engineering hubs to connect local merchants to international buyers. The looming RTR will reset competitive boundaries; players fastest to certify and commercialize connections stand to acquire share in time-critical B2B payouts.

Canada Payments Industry Leaders

Matercard Inc.

Visa Inc.

Interac Corp.

PayPal Holdings Inc.

Apple Inc. (Apple Pay)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Payments Canada opened a consultation on widening system access, laying groundwork for fintechs registered under RPAA to settle directly in central-bank funds.

- February 2025: Visa told investors it will chase the USD 23 trillion untapped consumer spend pool by scaling account-to-account transfers and issuing network-agnostic APIs.

- January 2025: Moneris reported record Black Friday throughput, prompting a 24-month POS terminal refresh strategy centered on software-defined architecture.

- November 2024: The Financial Consumer Agency of Canada enforced a revised Code of Conduct, extending disclosure duties to every network operator, heightening transparency across the acceptance chain.

Canada Payments Market Report Scope

The Canada Payments Market is segmented by Mode of Payment (Point of Sale (Card Payments, Digital Wallet, Cash), Online Sale (Card Payments, Digital Wallet)), and by End-user Industries (Retail, Entertainment, Healthcare, Hospitality). E-commerce payments include online purchases of goods and services such as purchases made on e-commerce websites and online booking of travel and accommodation. The scope of the market excludes online purchases of motor vehicles, real estate, utility bill payments (such as water, heating, and electricity), mortgage payments, loans, credit card bills, or purchases of shares and bonds. As for Point-of-Sale, all transactions that occur at the physical point of sale are included in the scope of the market. It includes traditional in-store transactions and all face-to-face transactions regardless of the location of the transaction. Cash is also considered for both cases (cash-on-delivery for e-commerce sales).

The study tracks key market metrics, underlying growth influencers, and significant industry vendors, providing support for Canada's market estimates and growth rates throughout the anticipated period. The study looks at COVID-19's overall influence on the Canadian payment ecosystem.

By Mode of Payment

| Point-of-Sale | Card (Debit, Credit, Pre-paid) |

| Digital Wallets (Apple Pay, Google Pay, Interac Flash) | |

| Cash | |

| Other POS (Gift-cards, QR, Wearables) | |

| Online | Card (Card-Not-Present) |

| Digital Wallet and Account-to-Account (Interac e-Transfer, PayPal) | |

| Other Online (COD, BNPL, Bank Transfer) |

By Interaction Channel

| Point-of-Sale |

| E-commerce/M-commerce |

By Transaction Type

| Person-to-Person (P2P) |

| Consumer-to-Business (C2B) |

| Business-to-Business (B2B) |

| Remittances and Cross-border |

By End-user Industry

| Retail |

| Entertainment and Digital Content |

| Healthcare |

| Hospitality and Travel |

| Government and Utilities |

| Other End-user Industries |

| By Mode of Payment | Point-of-Sale | Card (Debit, Credit, Pre-paid) |

| Digital Wallets (Apple Pay, Google Pay, Interac Flash) | ||

| Cash | ||

| Other POS (Gift-cards, QR, Wearables) | ||

| Online | Card (Card-Not-Present) | |

| Digital Wallet and Account-to-Account (Interac e-Transfer, PayPal) | ||

| Other Online (COD, BNPL, Bank Transfer) | ||

| By Interaction Channel | Point-of-Sale | |

| E-commerce/M-commerce | ||

| By Transaction Type | Person-to-Person (P2P) | |

| Consumer-to-Business (C2B) | ||

| Business-to-Business (B2B) | ||

| Remittances and Cross-border | ||

| By End-user Industry | Retail | |

| Entertainment and Digital Content | ||

| Healthcare | ||

| Hospitality and Travel | ||

| Government and Utilities | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What is the current value of the Canada payments market?

The market stands at USD 1.66 billion in 2026 and is projected to climb to USD 3.47 billion by 2031.

How fast is digital wallet adoption growing at Canadian checkouts?

Digital wallets at the point of sale are rising at an 17.82% CAGR, the quickest rate among in-store payment methods.

Which transaction type is expanding the most?

Person-to-person transfers are forecast to grow at 16.74% annually as consumers embrace instant, low-fee money movement.

How will the interchange fee cap affect issuers?

Lower interchange trims issuer revenue pools by up to USD 1 billion over five years, pushing banks toward fee-based and data-driven services.

What strategic benefit will the forthcoming Real-Time Rail provide?

RTR will enable near-instant settlement across retail and commercial use cases, enhancing liquidity and cutting counterparty risk, especially for cross-border traders.

Why is healthcare seen as a high-growth vertical?

Hospitals and clinics are digitizing billing and procurement processes, driving a 19.36% CAGR outlook for payment volumes in the healthcare space.

Page last updated on: