Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

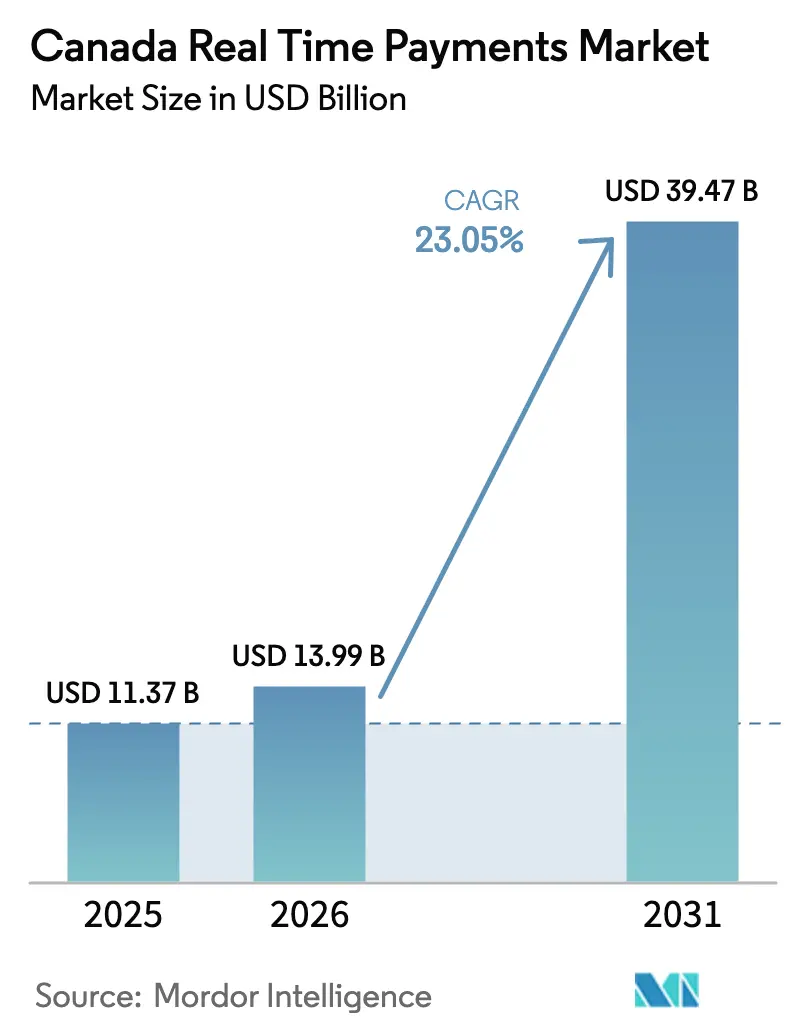

| Base Year Market Size (2025) | USD 11.37 Billion |

| Market Size (2026) | USD 13.99 Billion |

| Market Size (2031) | USD 39.47 Billion |

| Growth Rate (2026 - 2031) | 23.05% CAGR |

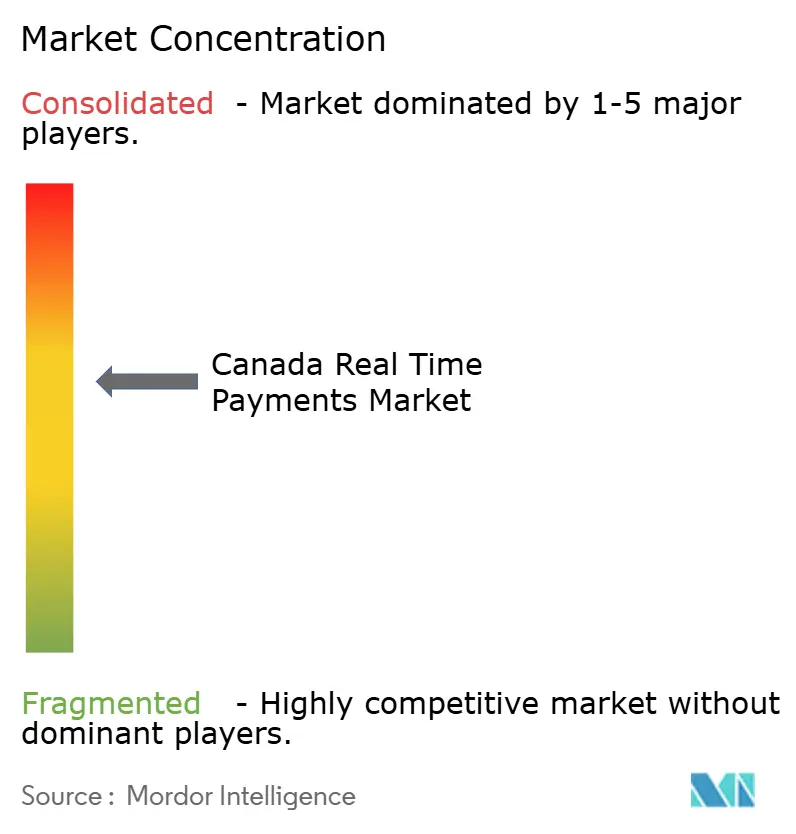

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Real Time Payments Market Analysis by Mordor Intelligence

The Canada real time payments market size is expected to grow from USD 11.37 billion in 2025 to USD 13.99 billion in 2026 and is forecast to reach USD 39.47 billion by 2031 at 23.05% CAGR over 2026-2031. Accelerated rollout of Payments Canada’s Real-Time Rail (RTR) platform, deepening ISO 20022 adoption, and widespread consumer preference for instant settlement are setting the pace. Interac e-Transfer continues to anchor day-to-day usage while cloud-first deployment models lower entry barriers for new providers. Collaboration between Tier-1 banks and fintechs in the Toronto–Waterloo corridor is widening use-case diversity, especially as application-programming-interface (API) standards mature. Meanwhile, provincial digital-identity programs and cross-border corridors that connect with the United States are expanding commercial reach for the Canada real time payments market.

Key Report Takeaways

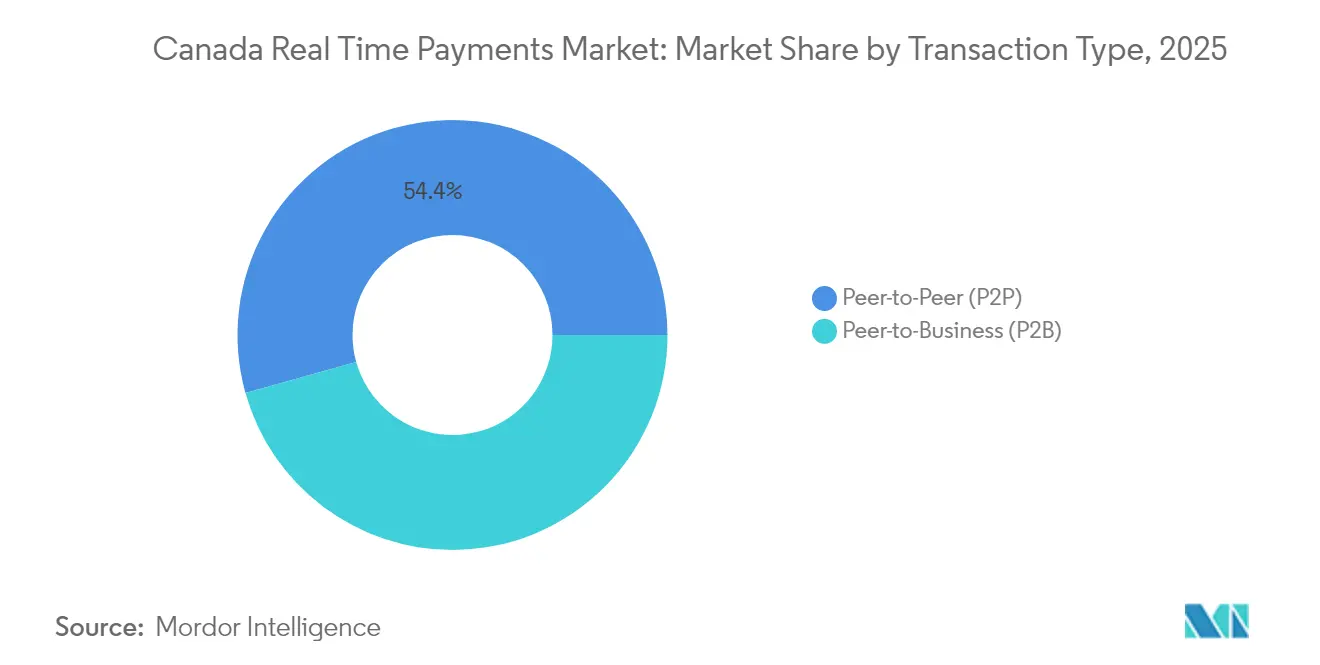

- By transaction type, Peer-to-Business led growth with a projected 26.07% CAGR to 2031, whereas Peer-to-Peer held 54.35% of the Canada real-time payments market share in 2025.

- By component, platforms retained a 64.30% revenue share in 2025, yet services are forecast to expand at a 27.12% CAGR through 2031.

- By deployment mode, cloud captured 71.20% of the Canada real-time payments market size in 2025 and will progress at 24.22% CAGR through 2031.

- By enterprise size, large enterprises controlled 59.40% share of the Canada real-time payments market size in 2025; SMEs are on track for a 24.98% CAGR.

- By end-user industry, Banking & Financial Services commanded 37.45% revenue share in 2025, while retail & e-commerce is poised to accelerate at a 28.47% CAGR

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Real Time Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Interac e-Transfer for Small-Value Payments Across Urban & Rural Canada | + 8.2% | National, with higher penetration in urban centers | Short term (≤ 2 years) |

| Launch of Payments Canada Real-Time Rail (RTR) Accelerating Financial-Institution Migration | + 5.1% | National | Medium term (2-4 years) |

| Strong FinTech Collaboration Culture in Toronto–Waterloo Corridor Enabling RTP APIs | + 4.3% | Ontario, with spillover effects nationally | Medium term (2-4 years) |

| Quebec Government Digital-Identity & Pay-Modernization Programs Spurring Usage in Francophone Provinces | + 3.7% | Quebec, with potential expansion to other provinces | Medium term (2-4 years) |

| Corporate Demand for Real-Time Treasury & Cash-Flow Visibility Among Canadian SMEs | + 2.1% | National, with concentration in major business centers | Long term (≥ 4 years) |

| Cross-Border RTP Corridors with the U.S. via FedNow Pilots Boosting Volumes | + 2.0% | Border regions and major trade hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Interac e-Transfer for Small-Value Payments Across Urban & Rural Canada

Interac e-Transfer reached record volumes in 2024, doubling year-over-year as Canadians shifted away from cash and cheques.[1]Tracey Black, “Payments Canada Opens Consultation on RTR Legal Framework,” Payments Canada, payments.ca The average user executed four transactions per month, signalling deep behavioural change across demographics. Importantly, the service has improved financial inclusion in remote communities, where branch networks remain sparse. Upcoming features such as request-to-pay and scheduled transfers will strengthen platform stickiness, laying a behavioural groundwork that speeds systemic adoption of the Canada real time payments market. A consumer survey found 40% of users plan to increase e-Transfer usage in 2025, underscoring the channel’s growth headroom.

Launch of Payments Canada Real-Time Rail (RTR) Accelerating Financial-Institution Migration

Payments Canada formalised the RTR roadmap in April 2024, committing to industry testing in 2026.[2]Timothy Lane, “RTR Program Milestone Announcement,” Payments Canada, payments.ca This certainty triggered capital allocation toward ISO 20022-ready cores, modern fraud analytics, and 24/7 liquidity solutions. Enhanced data fields remittance information, invoice numbers, structured references allow financial institutions to embed value-added services directly into payment flows. RTR’s open-access design is expected to broaden direct participation beyond traditional banks, reshaping competitive lines within the Canada real time payments market.

Strong Fintech Collaboration Culture in Toronto–Waterloo Corridor Enabling RTP APIs

The Toronto Waterloo corridor hosts specialised accelerators, university spin-outs, and venture programmes that co-create payment APIs with incumbent banks. TD Bank’s recent agreement with SideDrawer exemplifies how shared development models shorten integration cycles and expand feature depth.[3]Kristina Logue, “Real-Time Rail Quarterly Program Update,” Payments Canada, payments.ca Standardised APIs emerging from the corridor are already simplifying merchant onboarding and accelerating time-to-market for new real-time propositions. As cloud-native architecture dominates, these collaborations will underpin scale economics across the Canada real time payments market.

Quebec Government Digital-Identity & Pay-Modernization Programs Spurring Usage in Francophone Provinces

Quebec’s Ministry of Finance endorsed a province-wide digital-ID platform in 2024, aligning secure authentication with real-time disbursement use cases. Pilot programmes link government benefits and tax refunds to instant rails, reinforcing consumer trust among francophone users who value bilingual digital experiences. The provincial framework balances innovation with stringent data-privacy mandates, offering a blueprint that could inform nationwide standards and further harmonise the Canada real time payments market.

Restraints Impact Analysis*

| Restraint (concise description) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| RTR launch delays and certification uncertainty | –0.8% | National | Short term (≤ 2 years) |

| Credit-union legacy cores slowing ISO 20022 readiness | –1.2% | National; impact more pronounced in rural regions | Medium term (2–4 years) |

| Shoppers’ continued preference for Interac Debit at POS over account-to-account RTP | –1.1% | National; stronger effect in retail settings | Medium term (2–4 years) |

| Rising authorised push-payment (APP) fraud elevating risk-management costs | –1.4% | National; higher incidence in large metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Delay in RTR Go-Live & Certification Creating Industry-Implementation Uncertainty

Deferrals from the original 2023 launch date forced multiple re-scopings of IT roadmaps, straining budgets especially for mid-size lenders already juggling open-banking and cyber-defence mandates. Undefined accreditation criteria for scheme participants further complicate vendor selection and resource planning. Payments Canada’s shift to quarterly transparency has eased some concerns, yet small institutions still carry dual-track costs to support legacy rails while preparing for RTR readiness, tempering short-term momentum in the Canada real time payments market.

Legacy Core Banking Systems in Credit Unions Limiting ISO 20022 Readiness

Many rural credit unions operate on platforms lacking 24/7 processing and structured-data support. Transition paths often require expensive middleware or wholesale core replacement. Cooperative ownership models pose capital-raising constraints, creating a readiness gap that risks bifurcated service levels between urban and remote users. As a result, integration delays could slow inclusive uptake across the Canada real-time payments market until viable shared-service models or government incentives emerge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transaction Type: P2B Reshaping Business Payment Flows

The Peer-to-Business segment is forecast to expand at 26.07% CAGR to 2031, signalling a pivot from consumer-only use cases toward bill pay, subscription services, and gig-economy payouts. Merchants report meaningful reductions in card-processing fees and chargebacks when real-time rails are offered at checkout. RBC’s Interac e-Transfer for Business exemplifies enriched data fields that reconcile invoices instantly, improving working-capital cycles for both merchants and suppliers. In parallel, Peer-to-Peer remains foundational, sustaining 54.35% of the Canada real time payments market size in 2025 as consumers consolidate multiple micro-payments on a familiar platform. Convergence between P2P and P2B will intensify once RTR standardises formats, encouraging banks to roll out unified wallets that switch context between business and personal modes seamlessly.

Financial institutions are piloting overlay services such as request-to-pay, partial payments, and confirmation-of-payee that embed merchant branding directly into payment flows. These features support subscription models, point-of-sale financing, and on-demand services. As ISO 20022 functionality enables richer narrative data, accountants anticipate lower reconciliation costs. Together, these advances strengthen the competitive position of the Canada real time payments market against card networks for small-ticket transactions.

By Component: Services Sector Outpacing Platform Growth

Services revenue is projected to climb at 27.12% CAGR, fuelled by demand for advisory, integration, and managed-security offerings. Migration to ISO 20022 and continuous-operations mandates require specialised talent in payment orchestration, message mapping, and fraud analytics. Institutions such as TD Bank formed dedicated technology units in 2024 to orchestrate these complex transitions. Although platform software captured 64.30% revenue share in 2025, service partners are widening margins through value-added compliance and user-experience design. Consequently, the Canada real time payments market is witnessing ecosystem formation where platforms and services co-evolve.

Cloud-native platforms incorporate machine-learning modules that screen velocity anomalies in milliseconds, supporting transaction monitoring at scale. Up-time commitments of 99.999% and containerised deployment make these systems attractive for both incumbents and fintech entrants. Expanded data payload inherent to ISO 20022 facilitates downstream analytics for credit scoring and ESG reporting. With banks outsourcing non-core activities, specialist integrators sit at the centre of an increasingly service-centric Canada real time payments market.

By Deployment Mode: Cloud Dominance Reshapes Implementation Strategies

Cloud solutions commanded 71.20% market share in 2025 and are on pace for 24.22% CAGR through 2031, confirming the operational logic of elastic capacity for unpredictable peak loads. Financial institutions leverage regionally dispersed availability zones to guarantee business continuity and meet data-residency obligations. Kubernetes-based microservices allow discreet scaling of fraud engines or analytics modules without touching settlement cores, cutting change-management cycles from months to days. These efficiency gains position the cloud as default for new entrants into the Canada real time payments market.

On-premise deployments survive where latency, data-sovereignty, or bespoke integration demands preclude full cloud migration. Hybrid models local clearing plus cloud-based overlays are stabilising as an interim architecture for institutions with long depreciation schedules on datacentre assets. Security stacks now incorporate zero-trust frameworks, secure-access-service-edge gateways, and hardware-backed encryption keys, alleviating earlier reservations and cementing cloud’s prominence in the Canada real time payments market.

By Enterprise Size: SMEs Driving Innovation Through Rapid Adoption

SMEs will experience a 24.98% CAGR to 2031, bridging the adoption gap historically seen in innovation cycles. Lower interchange outlays and instant liquidity resonate strongly with cash-sensitive sectors such as hospitality, construction, and professional services. Fee reductions negotiated for small businesses in 2024 further tipped the calculus in favour of real-time options. In comparison, large enterprises, holding 59.40% of the Canada real time payments market size in 2025, utilise RTP for treasury optimisation, straight-through processing, and payroll disbursements that reduce administrative overhead.

Enterprise-resource-planning vendors embed RTP widgets that auto-tag remittance data, providing CFOs with near-live working-capital dashboards. Corporates also experiment with just-in-time supplier financing, reducing reliance on credit lines. Strategic interest from corporates boosts volume predictability, strengthening the network effects that underpin the Canada real time payments market.

By End-User Industry: Retail & E-Commerce Redefining Payment Experiences

Retail & e-commerce transactions are forecast to expand at 28.47% CAGR as merchants integrate QR codes and payment links into omnichannel journeys. Real-time confirmation mitigates cart abandonment and supports on-demand fulfilment models where shipment triggers depend on immediate funds availability. Banking & Financial Services secured 37.45% of 2025 revenue, leveraging the Canada real time payments market for instant loan disbursements, wealth-management transfers, and insurance payouts.

Healthcare providers explore RTP-enabled claims settlement that reduces administrative backlog, while government agencies migrate benefit disbursements to real-time rails to enhance citizen outcomes. Utilities and telecoms value instant bill-pay reconciliation, cutting days-sales-outstanding and improving customer retention. Collectively, these verticals illustrate the expanding canvas for the Canada real time payments industry.

Geography Analysis

Canada’s urban corridors, Toronto, Montreal, and Vancouver, represent the highest transaction density, buoyed by dense retail networks and a digitally literate population. The Toronto Waterloo cluster houses a critical mass of payment-tech talent, accelerating API standardisation for the Canada real time payments market. Quebec’s bilingual digital-ID programme promotes secure payment authentication, elevating transaction growth across francophone communities. Border provinces leverage pilot corridors linking RTR with FedNow, facilitating just-in-time inventory financing for manufacturing exporters. Such cross-border volumes fortify the Canada real time payments market as integrated North American supply chains demand faster cash cycles.

Regional credit unions deliver essential access in rural areas, yet legacy core limitations risk creating a service divide. The federal broadband initiative, aiming to connect 98% of households by 2026, should reduce digital-exclusion risk and unlock latent market potential. Remittance-heavy communities in Greater Toronto and Vancouver are early adopters of instant global transfers, reflecting lower average send costs. As RTR interlinks with international networks, provinces with diverse immigrant populations will experience additive volume gains, reinforcing network effects in the Canada real time payments market.

Provincial regulatory nuance shapes implementation. Alberta’s open-banking sandbox accelerates fintech licensing, while British Columbia’s consumer-protection statutes impose strict disclosure rules on fees. Payment service providers now adopt configurable compliance modules that adjust parameters by province. The national RTR framework harmonises core settlement yet preserves provincial overlays, creating a coherent but flexible backbone that sustains inclusive growth of the Canada real time payments market.

Regulatory Landscape

Regulation is converging around two pillars: Bank of Canada oversight of payment service providers under the Retail Payment Activities Act (RPAA) and Payments Canada governance for the Real-Time Rail (RTR). Retail payments supervision requirements for PSP operational risk management and end-user funds safeguarding came into force on September 8, 2025, raising baseline compliance expectations for both fintechs and incumbent PSP lines of business.

On the system side, Payments Canada advanced RTR rulemaking in 2026, with Canadian Payments Association By-law No. 10 (RTR) published in the Canada Gazette, Part II in June 2026. The by-law and RTR Rules are slated to come into force on August 24, 2026. Program communications also position RTR for a phased launch in Q4 2026, anchoring regulatory certainty around 24/7/365 operations, ISO 20022-aligned messaging, participation requirements, and liability expectations that shape product design, fraud controls, and participant onboarding.

Value Chain Analysis

The value chain starts with scheme governance and supervision, led by Payments Canada for RTR rules and operating requirements and by the Bank of Canada for RPAA-driven PSP oversight (risk management, incident handling, and safeguarding). Participation then flows through direct and indirect access models. Direct participants connect to the RTR exchange and settlement capabilities, while aggregators, processors, and technology vendors provide connectivity, message translation (ISO 20022), fraud screening, and operational tooling to smaller financial institutions and non-bank PSPs.

Downstream, financial institutions and PSPs deliver real-time payment services to end users through digital channels such as bank apps, wallets, and merchant checkouts. Providers also add overlay functions including request-to-pay, confirmation features, reconciliation data, and treasury visibility. In 2026, Payments Canada began Industry Solution Assurance testing, where participants connect and run their own workflows, and confirmed a sequenced onboarding approach. The first phase starts with Direct-to-Exchange participants at the Q4 2026 launch, followed by migration of existing Interac e-Transfer volumes, which makes testing, certification readiness, and 24/7 liquidity and fraud operations key bottlenecks and service-revenue drivers.

Competitive Landscape

The ecosystem centres on Interac, five domestic systemically important banks, and global card networks repositioning through tokenisation and open-loop real-time capabilities. Interac alone processed over 1 billion e-Transfer transactions in 2024, equal to more than one-third of all Canadian payment activity. Tier-1 banks invest heavily in proprietary fraud-analytics engines, forging data-sharing pacts to raise collective defence levels. Meanwhile, fintech entrants such as Nuvei, Lightspeed Commerce, and Versapay target niche workflows marketplaces, hospitality, accounts-receivable automation that incumbents do not fully address. These specialists rely on cloud-native design and event-driven microservices, lowering unit economics and enabling rapid feature iteration.

Strategic alliances dominate competitive manoeuvring. TD Bank’s SideDrawer tie-up, CIBC’s accelerator participation, and Scotiabank’s venture-fund investments illustrate a build-partner-buy continuum. Global schemes such as Mastercard and Visa augment local reach via tokenisation services that boost authorisation rates, aligning card rails with account-to-account user expectations. Regulatory clarity from the Retail Payment Activities Act is lowering entry barriers, yet operational-risk rules demand mature governance favouring players with solid compliance infrastructure. Technology differentiation pivots on AI-based anomaly detection, instant credit-decisioning, and premium data insights that embed frictionless fraud prevention in the Canada real time payments market.

White-space opportunities persist in value-added overlays: invoice financing, point-of-sale credit, and cross-border SME propositions. Providers that master connector APIs, ISO 20022 semantics, and consent-based data sharing are best placed to monetise incremental flows. As RTR nears launch, incumbent financial institutions accelerate defensive investment to retain primacy over customer relationships, even while partnering with fintechs to close capability gaps. The result is an innovation-led, yet stability-oriented, competitive equilibrium that propels sustainable expansion of the Canada real time payments market.

Canada Real Time Payments Industry Leaders

Google LLC (Google Pay)

Apple Inc. (Apple Pay)

Samsung Electronics Limited (Samsung Pay)

Mastercard Inc.

VISA Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

RTR program milestones in 2026 open near-term whitespace for implementation and compliance services, particularly for institutions that need ISO 20022 message mapping, 24/7 operational controls, and fraud management aligned to RPAA supervision. Payments Canada completed user acceptance testing in January 2026 and started non-functional testing in February 2026 (performance, resilience, and security). Industry Solution Assurance testing began in Q3 2026, expanding demand for connectivity, testing harnesses, monitoring, and incident-response tooling across banks, credit unions, and processors.

Opportunities also expand as Payments Canada membership broadens to non-bank PSPs. In 2026, new additions include Wise, KOHO, Float, Paramount Commerce, Brim Financial, and Meridian Credit Union, increasing the set of RTR-connected providers and distribution partners for merchants and platforms. The phased onboarding and planned migration path for Interac e-Transfer volumes create openings for overlay services that monetize richer payment data, such as invoice references and automated reconciliation. They also support cross-border workflow design aligned to emerging Canada-U.S. real-time corridors, while the Bank of Canada supervisory framework reinforces demand for managed risk, safeguarding, and audit-ready controls as differentiators.

Recent Industry Developments

- June 2026: Payments Canada announced that the RTR By-law (Canadian Payments Association By-law No. 10) and RTR Rules had received the necessary approvals, with the framework scheduled to come into force on August 24, 2026. This milestone reduces uncertainty around participation requirements, liabilities, and operating rules, which directly affects how banks, PSPs, and vendors finalize certification, fraud controls, and product terms ahead of launch.

- May 2026: Payments Canada confirmed a phased approach to RTR participant onboarding, starting at launch in Q4 2026 and extending broader access through 2027. The sequencing elevates readiness programs, connectivity providers, and managed service partners that can help participants meet testing, operational resilience, and 24/7 support requirements while controlling implementation risk.

- January 2026: Payments Canada completed user acceptance testing for RTR and began non-functional testing focusing on performance, resilience, and security. These activities validate connectivity and data integrity for participants ahead of the Q4 2026 launch.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the Canada real-time payments market is defined as revenues linked to enabling and processing payments that are authorized and confirmed in near real time for users in Canada, covering both consumer and business use cases.

Scope exclusions: We exclude traditional batch or delayed settlement rails, cash and check payments, and general card acquiring revenues that are not specifically tied to real-time account-to-account payment enablement.

Segmentation Overview

- By Transaction Type

- Peer-to-Peer (P2P)

- Peer-to-Business (P2B)

- By Component

- Platform / Solution

- Services

- By Deployment Mode

- Cloud

- On-Premise

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By End-User Industry

- Retail and E-Commerce

- BFSI

- Utilities and Telecom

- Healthcare

- Government and Public Sector

- Other End-user Industries

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual backbone for the model, so the market math starts from observable payment activity and the structure of Canadian payment rails. We relied on public references such as Payments Canada publications, Bank of Canada papers, Statistics Canada releases, and guidance from financial regulators. For market definitions, we also used selected ISO 20022 and payments standards documentation.

To ground pricing and the supply-side view, we reviewed sources such as company annual reports, investor presentations, audited financial statements, and reputable financial press coverage of payments modernization milestones. Where useful, we referenced paid subscriptions for company financials and news screening, and patent databases to track product direction and the pace of real-time payment related innovation. These sources are illustrative and not exhaustive, and many other references were used to collect data points, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on confirming what actually scales in Canada, including fee mechanics, adoption barriers, and which use cases are moving from pilot to steady volumes. We spoke with a balanced mix of ecosystem participants, including banks and credit unions, payment processors and technology providers, merchants and billers, and corporate treasury or finance teams, to validate the demand pool and practical price ranges.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 16% | |

| Mid tier: 44% | Functional/Unit leaders: 26% | |

| Smaller Players: 19% | Managers: 58% |

Market-Sizing & Forecasting

The core model uses a top-down and bottom-up combination. In the top-down build, we start from Canada payment activity signals and then reconstruct the real-time payment revenue pool using adoption by use case and realistic unit economics. In practice, we translate transaction volumes (and where needed, value) into addressable flows for real-time rails, and then apply blended revenue yields that reflect service mix.

Key inputs used to shape the totals include the pace of real-time capable participation across financial institutions, the split of flows by P2P, P2B, and B2B usage, typical transaction size patterns that influence pricing tiers, the share of API enabled initiation in enterprise flows, and expected fee compression as volume scales. Bottom-up checks are used to keep totals within a reasonable range, using selective roll-ups of supplier revenue disclosures, sampled pricing from bank and enterprise offerings, and channel checks on merchant acceptance readiness. When bottom-up visibility was incomplete, gaps were handled using conservative adoption bands by end-user type and then stress-tested in interviews.

For forecasting, we used scenario analysis supported by a simple multivariate regression layer, so growth is not driven by time alone. Variables such as expected rollout timing, enterprise onboarding speed, pricing progression, and substitution from slower rails were adjusted into base, faster, and slower cases, and then aligned to what primary respondents viewed as achievable over the forecast window.

Data Validation & Update Cycle

Validation is done through repeated cross-checks so the final numbers are not dependent on a single assumption. We compare outputs against independent signals such as publicly reported payment volumes, participation milestones, and observable shifts in digital payment usage, and then investigate any sharp jumps before sign-off.

A second analyst review is completed for calculation logic, unit consistency, and year-on-year reasonableness, followed by targeted re-contacts when a key input falls outside the agreed interview range. Reports are refreshed annually, and interim updates are made when material events occur, including major rail launch changes, regulation updates, or step-changes in pricing. Before delivery, a fresh review pass is completed so clients receive the latest updated view rather than an older snapshot.

Mordor Intelligence's Canada Real Time Payments Market Size Versus Other Published Estimates

It is common to see different market sizes published for Canada real-time payments because the topic sits between payments infrastructure and broader digital payments, and authors draw the line differently. Numbers also change when a study mixes transaction value with revenue, uses different currency timing, or projects adoption with a more aggressive rollout assumption.

Some external estimates widen scope by folding in general digital payment processing and card related revenues that are not tied to real-time account-to-account enablement. For Mordor Intelligence, the market total is limited to real-time payment enablement revenues in Canada, and it counts related software and services only when they directly support real-time transaction initiation, clearing, and confirmation.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.99 B (2026) | |

| Industry Association A | USD 10.80 B (2026) | This figure tends to stay closer to direct rail activity and may treat several enablement services as operating costs rather than market revenue, which compresses the total in early adoption years. |

| Global Consultancy B | USD 16.90 B (2026) | The estimate commonly expands the pool to include adjacent digital payments revenues and uses higher assumed monetization per transaction, which increases the market size even if transaction adoption is similar. |

Across the three figures, the spread is mainly explained by what gets counted as real-time payments revenue, plus differences in how yields are applied as volumes scale. By keeping the model tied to transaction adoption, service mix, and practical pricing ranges that can be rechecked, the final number stays transparent and repeatable year to year.

Key Questions Answered in the Report

What is the current value of the Canada real time payments market?

The market stands at USD 13.99 billion in 2026 and is projected to reach USD 39.47 billion by 2031.

How fast is the Canada real time payments market growing?

A compound annual growth rate of 23.05% is expected between 2026 and 2031, driven by RTR rollout, ISO 20022 adoption, and cloud deployment.

Which transaction type is expanding the quickest?

Peer-to-Business payments are forecast to grow at 26.07% CAGR, reflecting broader use cases in bill pay and e-commerce.

Why are SMEs adopting real-time payments rapidly?

SMEs benefit from lower processing fees and immediate cash-flow visibility, prompting a 24.98% CAGR for this enterprise segment.

How will the Real-Time Rail affect cross-border commerce?

RTR’s planned connectivity with FedNow will enable near-instant settlement for Canada–U.S. transactions, lowering costs and boosting trade liquidity.

What regulatory changes should payment service providers monitor?

The Retail Payment Activities Act requires PSP registration with the Bank of Canada and mandates operational-risk frameworks, shaping industry compliance standards.

Page last updated on: