Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

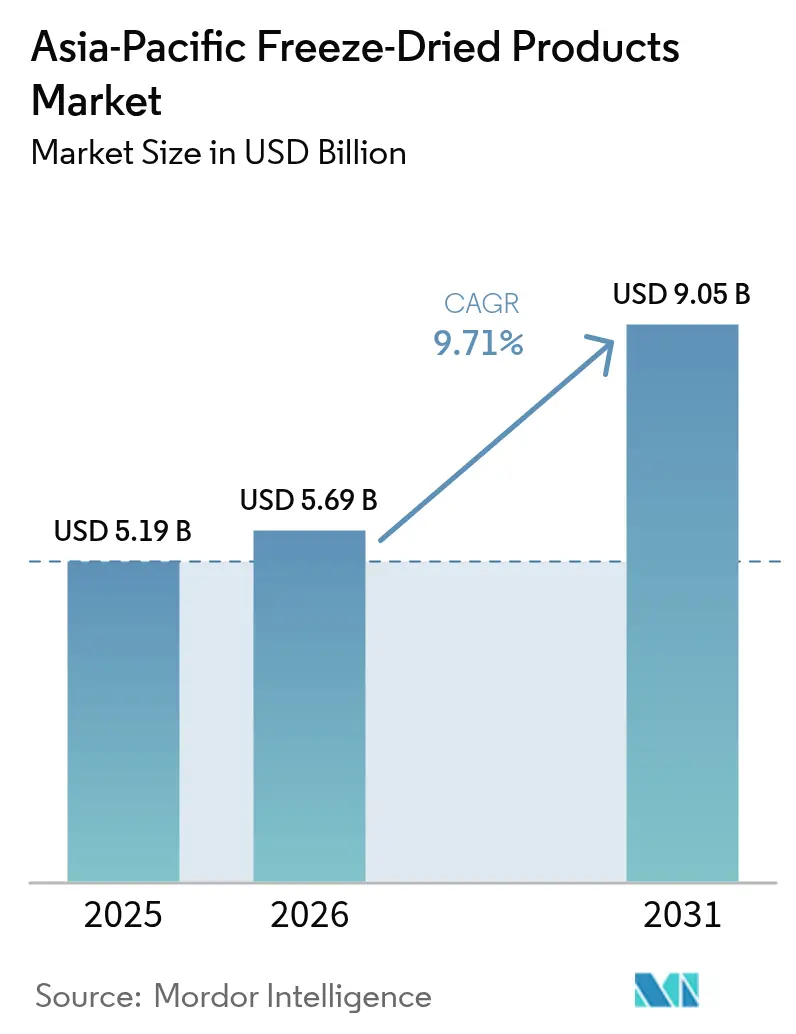

| Base Year Market Size (2025) | USD 5.19 Billion |

| Market Size (2026) | USD 5.69 Billion |

| Market Size (2031) | USD 9.05 Billion |

| Growth Rate (2026 - 2031) | 9.71% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Freeze-Dried Products Market Analysis by Mordor Intelligence

Asia-Pacific freeze-dried products market size in 2026 is estimated at USD 5.69 billion, growing from 2025 value of USD 5.19 billion with 2031 projections showing USD 9.05 billion, growing at 9.71% CAGR over 2026-2031. Rising demand for nutritious, shelf-stable foods, coupled with urbanization-driven lifestyle changes and consistent investments in advanced preservation technologies, fuels strong growth across both developed and emerging economies. Snack manufacturers are increasingly turning to freeze-drying, a method that safeguards vitamins and flavor without the need for refrigeration. Retailers, on the other hand, appreciate the lighter shipping weight that freeze-drying offers, leading to reduced logistics costs. In a bid to bolster the agricultural sector, local governments are championing value-addition programs. This initiative not only aids processors in securing raw materials but also ensures they do so at predictable prices. The surge in digital commerce amplifies product visibility, while trends in premiumization ignite innovation, particularly in areas like protein-fortified dairy, plant-based meal kits, and single-serve convenience lines. Regional players are keenly attuned to diverse cultural preferences, customizing flavors, package sizes, and labeling to resonate with each national market.

Key Report Takeaways

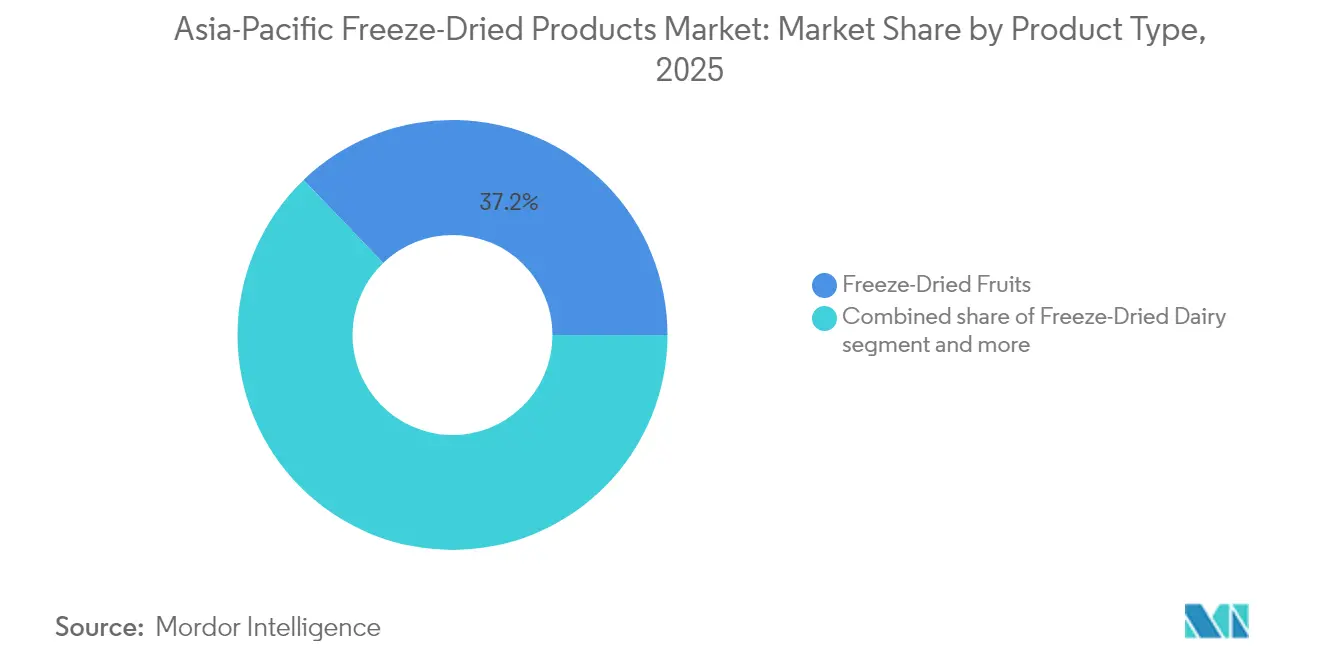

- By product type, freeze-dried fruits held 37.18% of the 2025 Asia-Pacific freeze-dried products market share, and freeze-dried dairy is projected to register a 11.98% CAGR during 2026-2031.

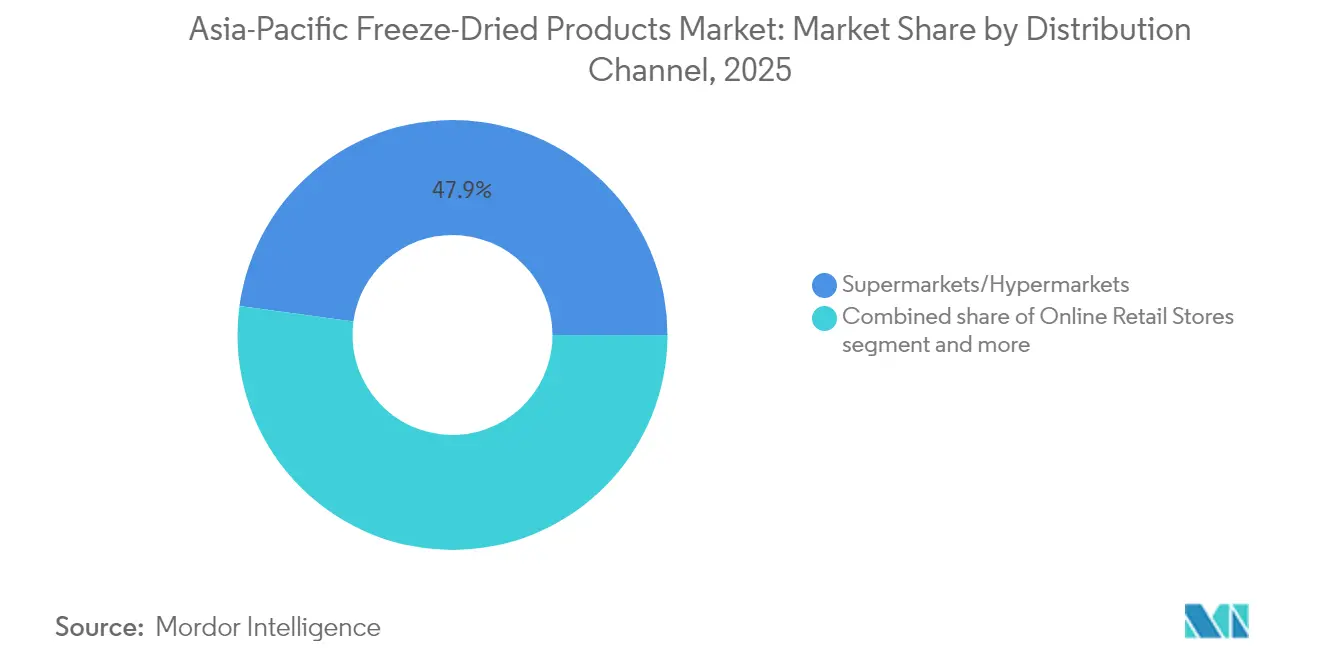

- By distribution channel, supermarkets/hypermarkets controlled 47.85% of the 2025 share, while online retail is expected to grow at a 13.05% CAGR through 2031.

- By nature, conventional lines represented 73.62% of the 2025 market, and organic alternatives are forecast to expand at an 11.06% CAGR over the same period.

- By geography, China accounted for 43.78% of the 2025 value, whereas India is set to post a 14.84% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Asia-Pacific Freeze-Dried Products Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for long-shelf-life healthy snacks | +2.1% | Global, with early gains in China, Japan, Southeast Asia | Medium term (2-4 years) |

| Expansion of e-grocery platforms | +1.8% | Asia-pacific core, spill-over to emerging markets | Short term (≤ 2 years) |

| Rising consumer demand for convenient ready-to-eat meals | +2.3% | Global, particularly strong in urban centers | Short term (≤ 2 years) |

| Preference for clean-label, natural ingredients over additives | +1.6% | North America and Europe influence spreading to Asia-Pacific | Medium term (2-4 years) |

| Plant-based meal-kit brands incorporating freeze-dried produce | +1.2% | Premium markets: Japan, Australia, urban China | Long term (≥ 4 years) |

| Government-backed programs to valorise climate-impacted crops | +0.9% | National, with early gains in Thailand, Philippines, Indonesia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for long-shelf-life healthy snacks

Health-conscious consumers are increasingly opting for high-protein, fiber-rich snacks that are portable and don't require refrigeration. These snacks cater to the growing demand for convenient yet nutritious options, aligning with shifting dietary preferences. Freeze-drying, which preserves color, texture, and micronutrients more effectively than thermal dehydration, is becoming the preferred method for producing fruit, yogurt, and vegetable chips. This technique not only enhances the shelf life of products but also maintains their nutritional value, making them appealing to health-focused buyers. Japanese processors are witnessing triple-digit growth by promoting single-serve vegetable portions, catering to busy households that prioritize premium convenience and are willing to pay a premium for quality. In response to tightening additive limits from food safety agencies, brands are emphasizing their clean-label credentials and showcasing natural ingredient lists, which resonate strongly with consumers seeking transparency and healthier choices.

Expansion of e-grocery platforms

Mobile-first shoppers are turning to digital marketplaces for their pantry staples. Freeze-dried products, thanks to their low shipping weight, long shelf life, and tamper-evident packaging, navigate parcel networks with ease. In tier-one Chinese cities, same-day fulfillment fosters consumer trust. Meanwhile, click-and-collect services in Indonesia and Vietnam address local infrastructure challenges. The Indo-Pacific's mobile-centric shopping, bolstered by platforms like Tmall, Lazada, and Shopee, mitigates purchase risks with standardized policies and offers competitive listings for packaged goods [1]Source: Export Development Canada,"E-commerce grocery platforms deliver growth across the Indo-Pacific", edc.ca. Supermarket chains are adapting by aligning their online assortments with in-store inventory, maintaining uniform pricing and promotions. Brands that prioritize product imagery, recipe videos, and localized keywords see a boost in search rankings and conversions.

Rising consumer demand for convenient ready-to-eat meals

In the Philippines, retail sales of ready meals surged by 12% in 2020, reaching USD 81 million, as consumers adapted to post-pandemic lifestyles [2]Source: USDA FAS,"Philippines: Shelf-Stable and Frozen Ready Meals Market Brief", fas.usda.gov. Amidst COVID-19 disruptions, the demand for ready-to-eat solutions remained robust, driven by remote work and fragmented meal occasions. This trend has led to heightened interest in rehydratable soups, porridges, and rice bowls. In response, Japanese innovators introduced freeze-dried chazuke kits, which can be reconstituted with cold water. These kits have garnered attention from both office workers and those preparing for emergencies. As of 2024, Philippine ready-meal sales continued their upward trajectory, climbing another 12%. Processors, however, anticipate a more tempered mid-single-digit growth moving forward, suggesting that these new eating habits may be here to stay. Meanwhile, research and development teams are honing freeze-dry cycles, aiming to maintain the integrity of complex sauces and protein inclusions. Their goal is to achieve a sensory experience on par with chilled counterparts. Additionally, government standards on shelf-life labeling are leaning towards this technology, as it allows for predictable “best before” dating without the need for preservatives.

Preference for clean-label, natural ingredients over additives

As health consciousness rises across diverse demographics, a notable shift in consumer demand toward clean-label, natural ingredients is significantly propelling the market. In the region, consumers are closely scrutinizing ingredient lists, actively favoring minimally processed foods devoid of synthetic additives or intricate chemical components. This preference aligns seamlessly with the core attributes of freeze-dried products. Urban middle-class populations and younger consumers, who prioritize transparency and nutritional integrity in their premium food selections, particularly underscore this trend. In response, manufacturers are innovating and reformulating their products, eliminating artificial preservatives and opting for simple, recognizable ingredients. This shift directly amplifies the appeal of freeze-dried offerings. The market growth is further bolstered by the clean-label's association with sustainability, food safety, and plant-based trends. This has prompted companies to carve out distinctions in both mainstream and niche categories. Consequently, the clean-label movement not only fortifies consumer trust but also propels long-term growth for freeze-dried food manufacturers throughout the Asia-Pacific region.

Restraints Impact Analysis of Asia-Pacific Freeze-Dried Products Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure of freeze-drying equipment | -1.8% | Global, particularly affecting SME market entry | Medium term (2-4 years) |

| Growing popularity of "fresh-equivalent" HPP and aseptic technologies | -1.4% | North America and Europe, spreading to premium Asia-Pacific segments | Long term (≥ 4 years) |

| Volatile upstream energy prices impacting process costs | -2.1% | Global, with acute impact in energy-import dependent markets | Short term (≤ 2 years) |

| Tightening Chinese export rules on agri-by-products | -0.9% | China-centric, affecting regional supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capital expenditure of freeze-drying equipment

Commercial freeze-dryers, priced between USD 1–3 million, pose a significant hurdle for small and mid-sized processors. Their large footprints necessitate purpose-built facilities, complete with reinforced floors and a clean-room design, leading to increased construction costs. On average, producing a kilogram of the finished product consumes 2.65 kWh of electricity, contributing to elevated operating expenses. While equipment manufacturers have introduced energy-efficient condensers and modular shelf systems that can nearly halve energy consumption, the payback periods for these investments still surpass three years. To navigate these challenges, contract manufacturing steps in, providing tolling services with minimal volume requirements, although scheduling queues can sometimes push back product launches.

Growing popularity of "fresh-equivalent" HPP and aseptic technologies

High-pressure processing (HPP) and aseptic filling are extending the chilled shelf life of products while maintaining their sensory quality. This advancement poses a challenge to freeze-drying, especially in the premium juice and ready-to-eat meat markets. HPP offers several advantages, including lower capital costs per pound processed and vitamin retention rates that are comparable to those of raw produce, making it an attractive option for manufacturers aiming to deliver high-quality products. However, the need for continuous refrigeration complicates logistics, particularly outside urban cold chains, where maintaining a consistent cold supply chain can be resource-intensive and costly. Furthermore, some regulators in ASEAN countries have not yet recognized HPP as being on par with pasteurization, which restricts interstate trade and limits market expansion opportunities for producers relying on this technology. In response to these challenges, hybrid brands are mitigating risks by pairing HPP beverages with freeze-dried toppings, marketing them as mix-ins to appeal to consumers seeking convenience and premium product offerings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Asia-Pacific Freeze-Dried Products Market Segment Analysis

By Product Type:

Fruits Retain Leadership, Dairy Gains MomentumIn 2025, freeze-dried fruits dominated the Asia-Pacific freeze-dried products market, securing a 37.18% share. Their authentic flavor and versatility in snacks, breakfast cereals, and bakery fillings drove this popularity. With abundant local fruit harvests and a boom in domestic tourism, the demand for snacks and gifting surged. Freeze-dried fruits emerged as the go-to portable souvenir. Manufacturers, in collaboration with flavor houses, are crafting unique retail offerings by infusing tropical notes and botanicals. Innovations in snacks and custom cereal blends bolster the fruit segment's appeal. Sensory panels fine-tune sweetness and crunch to cater to diverse regional preferences. Thanks to advances in vacuum drying, throughput has surged by up to 20%, enabling large-scale supply while preserving nutrient integrity. Premium pet food brands harness freeze-drying to maintain amino acids and cut out preservatives, allowing them to command premium prices at specialty retailers.

While freeze-dried dairy holds a smaller market share, it's the fastest-growing segment, projected to leap at a 11.98% CAGR. This growth is fueled by consumers' heightened focus on protein quality and immune benefits. Processors are introducing yogurt bites, cheese crisps, and portable milk powder, targeting urban consumers and school lunchboxes in Asia-Pacific. Dairy-fruit fusion cubes for smoothies highlight innovative collaborations, introducing novel textures and flavors. The micro-encapsulation of heat-sensitive probiotics is steering product development, bolstering functional claims that resonate with health-conscious buyers. The market's growth is underpinned by a rising appetite for shelf-stable dairy and the ability to bridge cold-chain logistics gaps in rural areas with limited refrigeration. Several manufacturers are experimenting with proprietary vacuum profiles and advanced freeze-drying techniques, aiming to optimize cycle time and enhance product integrity, thus propelling both market growth and technological advancements in the segment.

By Nature:

Conventional Dominates, Organic AcceleratesIn 2025, conventional freeze-dried products captured a dominant 73.62% share of the Asia-Pacific market. This surge was driven by cost-effective conventional farming methods and the widespread availability of these products in supermarkets, catering to a trend of bulk buying and value-oriented consumption. Middle-income families and institutional buyers are drawn to these products, thanks to established logistics and retail collaborations that strike a balance between price and quality. These scale advantages not only enhance throughput but also enable processors to cater to both spontaneous and planned purchases, all while keeping distribution costs in check. With a vast supermarket presence and strategic pushes, conventional products enjoy robust repeat sales, riding the wave of increasing demand for convenience foods. Retailers, banking on the familiarity of conventional stock-keeping units (SKUs), ensure swift shelf turnover, maintaining market equilibrium even as premium segments see growth.

While organic freeze-dried products currently hold a smaller market share, they're witnessing the fastest growth at an impressive 11.06% CAGR. This surge is largely attributed to rising urban affluence and heightened consumer awareness regarding pesticide residues. Brands boasting certifications from USDA, JAS, or EU schemes can command a notable 20–40% price premium. However, this premium is being tempered by increasing disposable incomes and the advantageous trends in e-commerce, which empower niche producers to sidestep traditional listing fees. Furthermore, brands are leveraging blockchain-based traceability platforms to authenticate farm origins a feature that resonates deeply with millennials and parents prioritizing chemical safety. Retailers are experimenting with “store-in-store” organic sections, integrating QR codes that narrate farm stories and highlight carbon footprints, thereby bolstering trust and emphasizing premium attributes.

By Distribution Channel:

Brick-and-Mortar Holds Scale, Online Races AheadIn 2025, supermarkets and hypermarkets commanded a dominant 47.85% share of the retail turnover in the Asia-Pacific freeze-dried products market. They achieved this by leveraging expansive assortments, in-store sampling, and loyalty programs, effectively driving both impulse purchases and routine replenishments. Merchandisers strategically position freeze-dried snacks alongside breakfast cereals and trail mixes, capitalizing on cross-merchandising opportunities. Meanwhile, premium duty-free assortments at airports cater to the burgeoning trend of healthy gifting. Convenience stores, recognizing the urban pace, expand single-serve offerings for late-night shoppers and transit commuters, effectively capturing impulse sales.

Online sales are on a rapid ascent, projected to grow at a CAGR of 13.05%. This surge is bolstered by the widespread adoption of mobile payment solutions and dependable parcel logistics in the Asia-Pacific's interconnected markets. Subscription models via virtual storefronts successfully entice monthly repeat buyers. At the same time, cross-border e-commerce empowers niche brands from Australia and Japan, granting them direct access to Southeast Asian consumers without the hurdles of shelf placement. Retailers are also embracing omnichannel strategies, implementing click-and-collect counters, AI-driven inventory planning, and dynamic pricing engines that adjust promotions in real-time to maximize margins and minimize waste. South Korea, as an early adopter, is piloting voice-commerce reordering through smart speakers, broadening access for tech-savvy demographics.

Geography Analysis

China Freeze-Dried Products Market

In 2025, China secured its leading position with 43.78% of sales, driven by large-scale manufacturing, a sophisticated domestic e-commerce landscape, and robust government backing for agri-processing enhancements. While the lifting of quarantine restrictions on frozen fruit imports broadens the spectrum of raw material choices, exporters still grapple with shifting labeling regulations and tariff schedules. Local suppliers are bolstering regional advantages by offering competitively priced custom freeze-dryers. As middle-class households elevate their spending, there's a noticeable surge in demand for premium organic imports .

India and Japan Freeze-Dried Products Market

India is experiencing rapid growth, with a projected CAGR of 14.84% until 2031. Key drivers include urbanization, increased investments in cold-chain infrastructure, and nutrition-focused advertising, which are boosting the demand for ready-to-eat fruit and dairy snacks. Export incentives are encouraging the development of integrated processing parks that enhance supply chain efficiency by incorporating pre-cooling, freeze-drying, and packaging processes. However, the complex state regulations on food additives and labeling require careful compliance. Japan continues to lead in technological advancements, with companies driving innovation in meal and beverage solutions.

APAC Freeze-Dried Products Market

Australia, Thailand, Vietnam, and Indonesia are establishing distinct positions in the market. Australia focuses on premium products, highlighting freeze-dried berries and honey-infused yogurt crisps. Thailand is utilizing funds from its bio-circular economy initiative for pilot projects that convert surplus pineapples and jackfruits into export-ready, shelf-stable products. In Vietnam, contract manufacturing hubs are offering tolling services to regional brands, benefiting from the country's competitive labor costs and strategic port locations.

Competitive Landscape

In a landscape marked by moderate industry concentration, both multinationals and agile local specialists find their footing. Leveraging category management expertise, robust research and development pipelines, and multi-country manufacturing assets, giants like Ajinomoto, Asahi Group, and Nestlé work diligently to maintain their market share. After introducing freeze-dried soups enriched with amino acids, Ajinomoto celebrated a fiscal 2024 uptick in regional food sales, reaching JPY 399.2 billion. Meanwhile, major players are channeling investments into energy-efficient condensers and advanced smart factory systems, a move that's not only slashing unit costs but also amplifying profit margins.

Regional specialists carve out their niche, emphasizing organic certifications, unique ethnic flavor profiles, or a commitment to plant-based offerings. Thrive Freeze Dry broadened its horizons by acquiring Germany's Paradiesfrucht, a strategic move that bolstered its European berry sourcing and strengthened customer ties. In Vietnam, Asuzac Foods is making waves, scaling operations with adaptable batch capacities tailored for niche Japanese retailers who prioritize low minimum order quantities.

Strategic maneuvers abound: from vertical integration into fruit orchards ensuring a steady supply, to partnerships with packaging pioneers crafting oxygen-barrier pouches. Brands are also venturing into direct-to-consumer webshops, harnessing the power of first-party data. Not stopping there, they're dabbling in augmented-reality labeling, letting consumers visualize the farm-to-fork journey right on their smartphones. Patent filings are buzzing around innovations like vacuum cycle optimization and natural flavor encapsulation. The Asia-Pacific freeze-dried products industry stands as a testament to the rewards of agility, be it in innovation, navigating regulations, or diversifying channels.

Asia-Pacific Freeze-Dried Products Industry Leaders

-

Asahi Group Holdings, Ltd.

-

Harmony House Foods, Inc.

-

Ajinomoto Co. Inc

-

Fujian Lixing Foods Co. Ltd.

-

Nestle S.A.

- *Disclaimer: Major Players sorted in no particular order

Asia-Pacific Freeze-Dried Products Market Companies Covered in this Report

- Ajinomoto Co Inc.

- Asahi Group Holdings Ltd.

- Expedition Foods Ltd.

- Campers Pantry Pty Ltd.

- Harmony House Foods Inc.

- Nestle S.A.

- The Forager Food Co.

- Priffco Foods

- Fujian Lixing Foods Co Ltd.

- Nagatanien Holdings Co Ltd.

- Zhejiang Natural Foods Co Ltd.

- Chongqing Jinglong Freeze-Dry Co.

- Guangzhou Lvyuan Foods Co Ltd.

- Qingdao Liuting Food Co Ltd.

- Gansu Dunhuang Seed Freeze-Dry

- Lyofood Sp. z o.o. (APAC subsidiary)

- Kirin FreezeTech Co.

- Dalian Tianshan Freeze-Dry Foods

- Backpacker's Pantry (Asia operations)

- Thrive Life LLC (Asia distributors)

Read Analysis of Asia-Pacific Freeze-Dried Products Companies

Recent Industry Developments in Asia-Pacific Freeze-Dried Products Market

- September 2024: 3 Seasons Holdings, based in Thailand, unveiled a new line of freeze-dried fruits and vegetables. These offerings, which include powders for B2B clients and snacks for retail, mark the company's recent expansion into Middle Eastern markets. Manufacturing takes place at their Chonburi facility, sourcing all raw materials locally, save for a select few imported fruits. The product lineup emphasizes clean-label standards and boasts certifications like halal, kosher, and USDA Organic. Notably, they've introduced okra powder, touting its gut health benefits, and have harnessed advanced freeze-drying techniques to ensure maximum nutrient retention.

- May 2024: Paradise Fruits made waves in Southeast Asia with their launch of freeze-dried berries and tropical fruits. Their offerings, which include yogurt melts, fruit crisps, and on-the-go snacks, are marketed as premium, convenient nutritional choices with an extended shelf life. Targeting a younger, urban demographic, the expansion capitalizes on the rising health consciousness and the trend of online shopping, making products available both in retail outlets and online.

- February 2024: Amano Foods, rolled out a range of assorted freeze-dried vegetable soup packs. With a focus on advanced quick rehydration, these packs cater to the busy Japanese consumer demographic, emphasizing healthy, instant meals with minimal preservatives. The new soup offerings spotlight ingredients like carrots, peas, mushrooms, and other regional specialties.

- January 2024: New Zealand's Ovavo, a budding startup, debuted its freeze-dried avocado powder. This innovative product not only emphasizes preservation but also nutrition, appealing to the health-conscious consumer base. Designed for versatility, the powder serves as a shelf-stable ingredient for baking, smoothies, and dietary supplements. With an eye on expansion, Ovavo is targeting Asian markets, highlighting the health benefits of avocados, including their rich healthy fats and vitamins.

Asia-Pacific Freeze-Dried Products Market Report Scope

Freeze drying the food is a low-temperature dehydration method that entails freezing the product, reducing the pressure, and then sublimating the ice. Asia-Pacific freeze-dried food market is segmented by product type, distribution channel, and geography. Based on the product type, the market is segmented into freeze-dried fruits, freeze-dried vegetables, freeze-dried meat and seafood, freeze-dried beverages, freeze-dried dairy products, prepared meals, and pet food. The fruit segment is further segmented into strawberry, raspberry, pineapple, apple, mango, and other fruits. The vegetable segment is further segmented into peas, corn, carrot, potato, mushroom, and other vegetables. Based on the distribution channel, the market studied is segmented into supermarkets/hypermarkets, convenience stores, online stores, and other distribution channels. Based on geography, the market is segmented into China, India, Australia, Japan, and the Rest of Asia-Pacific. For each segment, the market sizing and forecasts have been done based on value (in USD million).

Segmentation Overview

By Product Type

| Freeze-Dried Fruits | Strawberry |

| Raspberry | |

| Pineapple | |

| Apple | |

| Mango | |

| Other Fruits | |

| Freeze-Dried Vegetables | Pea |

| Corn | |

| Carrot | |

| Potato | |

| Mushroom | |

| Other Vegetables | |

| Freeze-Dried Meat and Seafood | |

| Freeze-Dried Dairy Products | |

| Freeze-Dried Beverages | |

| Prepared Meals | |

| Pet Food |

By Nature

| Conventional |

| Organic |

Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channel |

By Geography

| China |

| Japan |

| India |

| Australia |

| New Zealand |

| Indonesia |

| Thailand |

| Vietnam |

| Malaysia |

| Philippines |

| Rest of Asia-Pacific |

| By Product Type | Freeze-Dried Fruits | Strawberry |

| Raspberry | ||

| Pineapple | ||

| Apple | ||

| Mango | ||

| Other Fruits | ||

| Freeze-Dried Vegetables | Pea | |

| Corn | ||

| Carrot | ||

| Potato | ||

| Mushroom | ||

| Other Vegetables | ||

| Freeze-Dried Meat and Seafood | ||

| Freeze-Dried Dairy Products | ||

| Freeze-Dried Beverages | ||

| Prepared Meals | ||

| Pet Food | ||

| By Nature | Conventional | |

| Organic | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | China | |

| Japan | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Malaysia | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the projected value of the Asia-Pacific freeze-dried products market in 2031?

It is expected to reach USD 9.05 billion.

Which country will grow the fastest in freeze-dried products sales through 2031?

India is forecast to post a 14.84% CAGR.

Which product type currently holds the largest share?

Freeze-dried fruits lead with 37.18% of 2025 sales.

Which channel is expanding quickest?

Online retail is projected to grow at a 13.05% CAGR.

Page last updated on: