Cable Lugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.39 Billion |

| Market Size (2031) | USD 4.54 Billion |

| Growth Rate (2026 - 2031) | 6.01% CAGR |

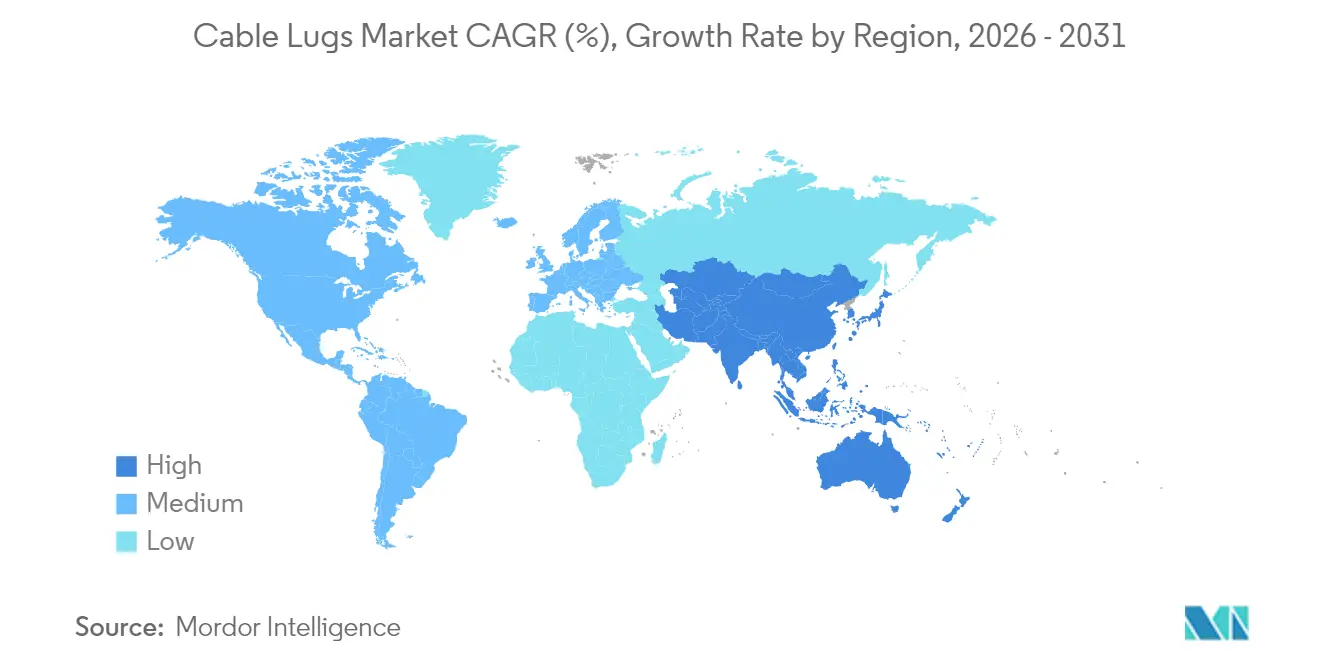

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cable Lugs Market Analysis by Mordor Intelligence

The cable lugs market size was valued at USD 3.20 billion in 2025 and estimated to grow from USD 3.39 billion in 2026 to reach USD 4.54 billion by 2031, at a CAGR of 6.01% during the forecast period (2026-2031). Current demand reflects grid modernization programs that integrate renewables, the rising electrification of commercial vehicles, and hyperscale data center buildouts that favor low-impedance grounding. The cable lugs market gains further traction from safety-code revisions in North America and the European Union that mandate touch-safe terminations, while volatile copper and aluminum prices challenge margin protection for manufacturers. Competitive intensity centers on compliance with IEC 61238 and UL 486A-486B, rapid die customization, and the ability to supply pre-insulated variants for battery storage projects. The cable lugs industry also faces counterfeiting risks in price-sensitive regions and substitution threats from laser-welded terminals in automotive battery packs.

Key Report Takeaways

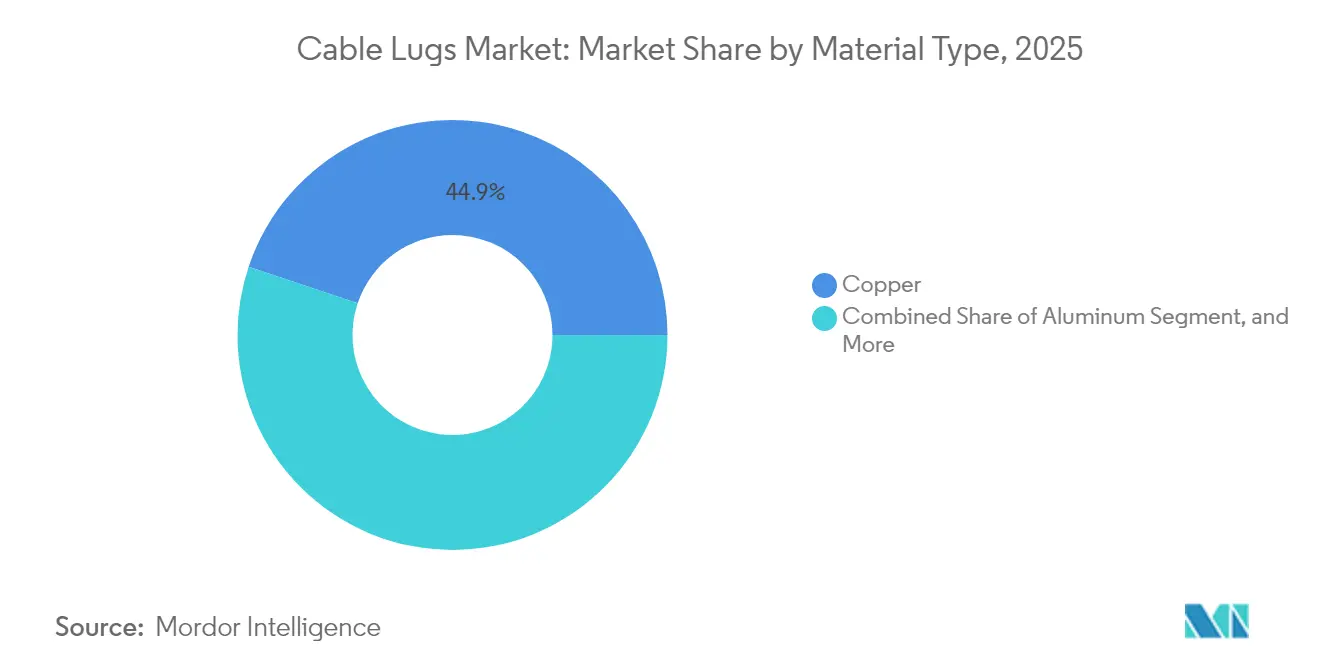

- By material type, copper lugs led the cable lugs market, accounting for a 44.85% revenue share in 2025. Meanwhile, plastic variants are forecast to expand at a 7.84% CAGR through 2031.

- By lug type, ring lugs captured 33.25% of the 2025 revenue of the cable lugs market, whereas butt splice lugs are projected to grow at a 8.79% CAGR to 2031.

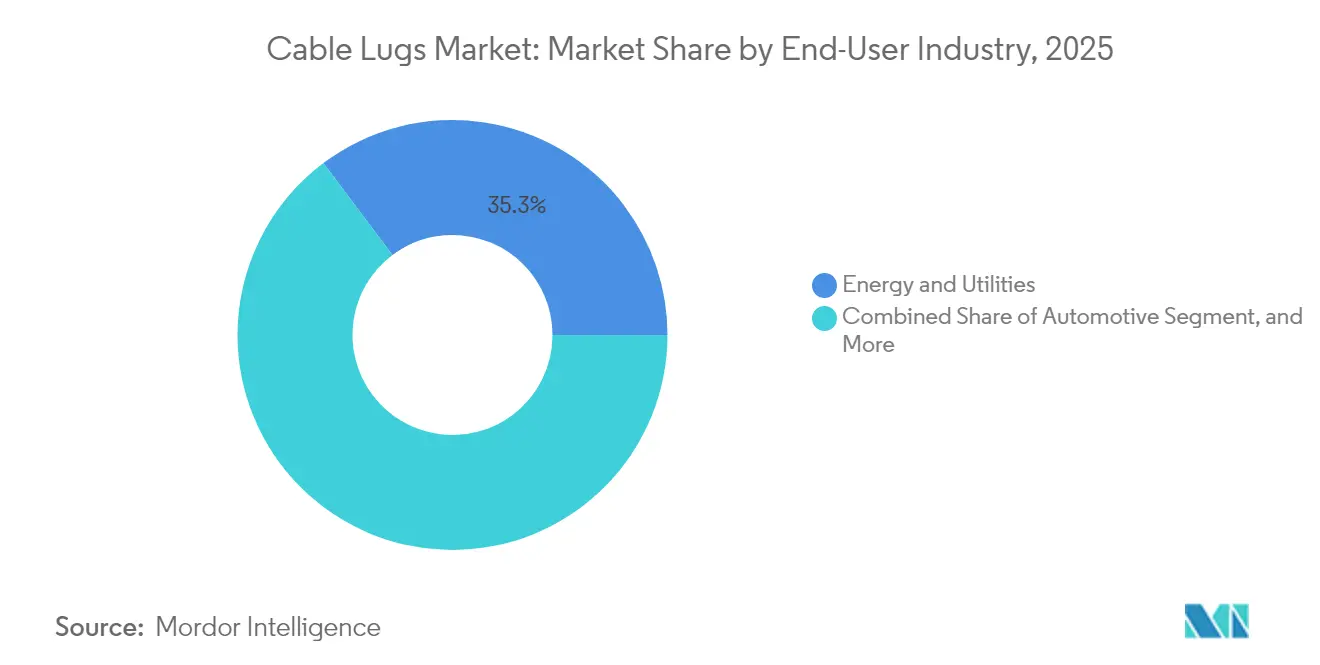

- By end-user industry, energy and utilities held a 35.25% share of the cable lugs market in 2025, while the automotive sector is projected to advance at an 8.45% CAGR through 2031.

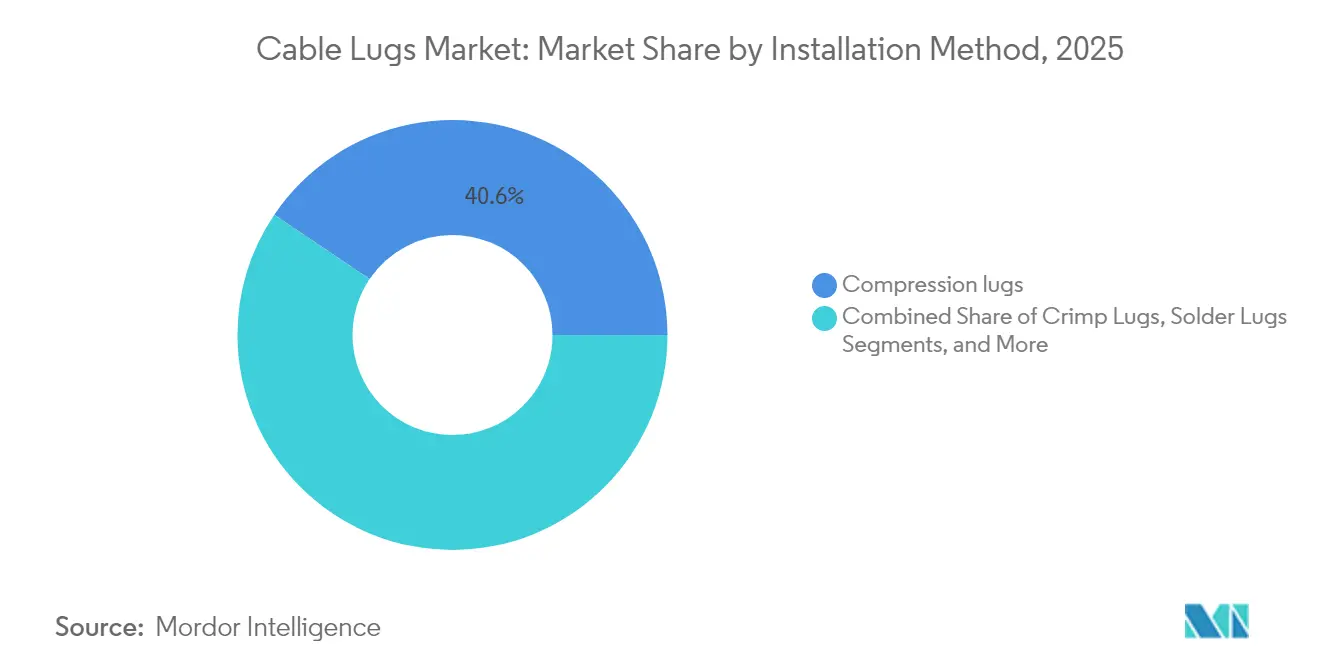

- By installation method, compression lugs commanded a 40.55% share of the cable lugs market in 2025, whereas mechanical lugs are set to post an 7.92% CAGR toward 2031.

- By insulation type, fully insulated lugs accounted for 49.60% of the 2025 revenue of the cable lugs market and are projected to grow at an 7.68% CAGR through 2031.

- By geography, the Asia-Pacific region dominated the cable lugs market with a 39.85% revenue share in 2025, while the Middle East and Africa region is expected to register an 8.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cable Lugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated grid modernization and renewable energy interconnections | +1.8% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Electrification of commercial vehicle powertrains | +1.5% | North America, Europe, China | Medium term (2-4 years) |

| Surge in data-center construction requiring low-impedance grounding | +1.2% | North America, Europe, Asia-Pacific | Short term (≤2 years) |

| Rapid adoption of prefabricated wiring harnesses in modular buildings | +0.8% | North America, Northern Europe, Global | Medium term (2-4 years) |

| Stringent safety codes mandating insulated compression lugs | +0.6% | Europe, North America, spillover Asia-Pacific | Long term (≥4 years) |

| Government incentives for industrial energy-efficiency retrofits | +0.5% | Europe, North America, select Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerated Grid Modernization And Renewable Energy Interconnections

Utilities in the United States, the European Union, and the Asia-Pacific are reconductoring legacy lines and adding high-voltage direct-current corridors that require cable lugs qualified for voltages above 500 kilovolts.[1]United States Department of Energy, “National Transmission Planning Study,” ENERGY.GOV The Grid Resilience and Innovation Partnerships program allocated USD 10.5 billion in 2024 to modernize substations, which boosts demand for compression lugs that withstand thermal expansion 40% higher than traditional ACSR conductors. Offshore wind interconnections in the North Sea and Taiwan Strait utilize tinned-copper lugs with silicone insulation, which maintain dielectric strength above 10 kV/mm in saltwater environments. The Electric Power Research Institute recommends mechanical lugs for live-line work to reduce outage windows from eight hours to 90 minutes per splice. Consequently, the cable lugs market benefits from steady procurement cycles tied to grid-hardening mandates and renewable energy targets.

Electrification Of Commercial Vehicle Powertrains

Battery-electric trucks and buses are transitioning to 800-volt architectures, which require cable lugs rated above 500 amperes and insulation materials capable of continuous operation at 150 °C.[2]United States Department of Transportation, “National Electric Vehicle Infrastructure Formula Program,” DOT.GOV ISO 6469-3 and IEEE 2030.1 standards require touch-safe terminations with secondary locking features, steering OEMs toward fully insulated ring lugs. European regulations introduced in 2024 require vehicles exceeding 12 tons to utilize UL-listed cable lugs with traceability markings, which raises entry barriers for low-cost suppliers. The compression approach used in battery packs reduces assembly time by 25% but relies on hydraulic crimpers that are calibrated within a 5% tonnage tolerance. As fleet electrification scales, the cable lugs market gains a lucrative growth avenue in heavy-duty mobility applications.

Surge In Data-Center Construction Requiring Low-Impedance Grounding

Hyperscale facilities plan more than 10 GW of additional capacity in 2025 across North America, Europe, and the Asia-Pacific. Each campus installs 200–300 cable lugs for grounding grids that must maintain an impedance below 1 ohm to protect power-dense AI servers. IEC 61936-1 now mandates compression lugs with inspection windows, enabling infrared scans to detect loose terminations before arc-flash events. Modular data centers utilize factory-crimped lugs within pre-fabricated PDUs, reducing commissioning schedules from 12 weeks to six. Although copper prices averaged USD 9,200 t-¹ in 2024, operators prefer tinned-copper lugs that keep contact resistance under 50 µΩ for 20 years, sustaining premium demand in this segment of the cable lugs market.

Rapid Adoption Of Prefabricated Wiring Harnesses In Modular Buildings

Healthcare, education, and multifamily projects are embracing modular construction, which utilizes factory-installed cable lugs to reduce on-site labor by 60% and shorten project schedules by 30%. Partnerships such as ABB and Wieland supply butt splice lugs that enable tool-free connections between wall modules and main panels. Spring-cage lugs developed by Weidmüller accommodate conductor tolerance variations of ±10%, lowering rework. The United Kingdom’s Building Safety Act 2024 enforces third-party inspection of terminations for high-rise housing, driving adoption of serialized lugs with blockchain traceability. This modular trend fuels diversified growth opportunities for the cable lugs market across North America and Northern Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in copper and aluminum prices | -0.9% | Global | Short term (≤2 years) |

| Direct laser-welded terminals cannibalizing lug demand | -0.7% | Automotive, North America, Europe, China | Medium term (2-4 years) |

| Proliferation of quality counterfeits | -0.4% | Asia-Pacific, Middle East, Africa | Short term (≤2 years) |

| Skilled-labor shortage for correct crimping and installation | -0.6% | North America, Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatility In Copper And Aluminum Prices

Copper spot prices oscillated between USD 8,400 and USD 10,200 t-¹ during 2024, while aluminum traded from USD 2,300 to USD 2,700 t-¹.[3]London Metal Exchange, “Copper and Aluminum Price Data 2024,” LME.COM Cable lug manufacturers operate on gross margins of 18–22%, leaving limited room to absorb raw material spikes without incurring price surcharges. Contractors typically lock materials 90 days before mobilization, but double-digit copper hikes during that window can erode project margins by up to 4 percentage points. Some buyers, therefore, switch to aluminum lugs despite 60% larger barrel diameters. Persistent volatility clouds the short-term outlook for the cable lugs market, although hybrid copper-clad aluminum lugs offer partial relief.

Direct Laser-Welded Terminals Cannibalizing Lug Demand

Automotive battery-pack producers now laser-weld cell tabs directly to busbars, reducing assembly time from 45 seconds to 12 seconds per joint. Tesla’s 4680 platform endures 10,000 thermal cycles without retorque, outperforming bolted lugs that need maintenance every 2,000 cycles. While laser-weld stations cost USD 150,000–300,000 each, savings on dies and torque tools offset investments for high-volume plants. Field installations remain unsuitable for welding due to inert-gas and cleanliness requirements, so the cable lugs market retains utility and infrastructure demand, yet automotive substitution will nibble at growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Copper Dominance Faces Lightweight Challengers

Copper still accounts for 44.85% of 2025 revenue, as its 58 MS m-¹ conductivity supports high-ampere circuits in substations and data centers. Plastic lugs are projected to expand at an 7.84% CAGR to 2031, as automakers reduce the weight of powertrains by 3–5 kg. Aluminum lugs gain market share in utility-scale solar, where a 35% cost advantage offsets their larger diameter. Stainless-steel lugs remain a niche product but command a 200% price premium for use in chemical and marine applications. The cable lugs market size for copper products is poised to rise steadily, but it will lose a few points of market share to plastic and aluminum alternatives. Composite lugs pairing glass-fiber-reinforced nylon with brass inserts cut weight by 40% while satisfying IEC 61238-1 pull-out thresholds, positioning them as mid-range options. Copper-clad aluminum hybrids deliver 90% of copper conductivity at half the weight, yet National Electrical Code rules confine them to circuits below 400 A. Suppliers therefore juggle portfolios that balance conductivity, corrosion resistance, and cost under shifting regulatory rules.

The cable lugs market benefits when copper grades, such as ETP and OFHC, command price premiums that lift average selling prices; however, the upside is offset whenever volatile commodity swings squeeze project budgets. Manufacturers hedge their operations with virtual warehousing programs that lock in metal at the time of purchase order placement, thereby smoothing revenue flows. Plastic lugs also open up a new aftermarket for heat-shrink sleeves rated above 150 °C, providing distributors with complementary revenue. Altogether, material diversification ensures resilient market growth even if copper prices trend upward for prolonged periods.

By Lug Type: Ring Lugs Lead While Butt Splices Surge

Ring lugs account for 33.25% of 2025 revenue, as their 360-degree contact profile meets stringent ground-fault and short-circuit requirements in substations. Butt splice lugs are recording a 8.79% CAGR as solar and wind developers favor modular harnesses that cut site labor by 35%. Fork lugs address control panels that require frequent disconnections, whereas pin lugs populate screw-clamp terminal blocks commonly found in European machinery. Offset-tongue and flag styles are suitable for confined battery enclosures and telecom cabinets. The cable lugs market share for ring lugs will erode modestly yet remain dominant, as utilities and industrial plants value the decades of proven performance. Developers now deploy butt splice lugs on reconductoring projects to speed work before peak-load seasons, a practice supported by EPRI field trials.

Growth in butt splice demand compels manufacturers to launch new die sets that maintain compression ratios of 75–85% per UL 486A-486B. Quick-change die heads cut tool downtime by 20%, enhancing contractor productivity. Fork lugs face shared pressure from spring-cage connectors, which offer tool-less installation in low-current circuits. Still, retrofit work on aging control panels will support fork and pin variants through 2031. Balanced product development across lug types thus remains vital to capture opportunities throughout the cable lugs market.

By End-User Industry: Energy Utilities Anchor Demand As Automotive Accelerates

Energy and utilities accounted for 35.25% of cable lug volume in 2025, driven by substation upgrades and the construction of ultra-high-voltage transmission lines. Automotive demand is scaling at an 8.45% CAGR as battery-electric vehicles require 40–60 lugs per powertrain. Construction remains a perennial segment due to building-code mandates for grounding electrode terminations. Manufacturing and processing industries specify lugs for motor control centers and variable-frequency drives, while telecom and rail complete the mix. The cable lugs market size for automotive applications is expected to grow the fastest because 800-volt systems double the electrical stress on terminations, prompting OEMs to adopt higher-value, fully insulated lugs.

European Union rules enacted in 2024 oblige battery packs to incorporate color-coded lugs with secondary locks to prevent dislodgement during crashes. Utilities broaden specifications to include lugs qualified for 50 kA short-circuit withstand for one second. Data-center operators adopt tinned-copper lugs despite a 15% cost premium to limit oxidation, motivating suppliers to expand plating capacity. Consequently, each vertical maintains distinct value drivers that balance overall revenue streams in the cable lugs market.

By Installation Method: Compression Dominates As Mechanical Variants Gain Ground

Compression lugs represented 40.55% of 2025 installations because they achieve gas-tight joints that sustain contact resistance below 50 µΩ under cyclic loading. Mechanical lugs have been on an 7.92% CAGR trajectory since they require only torque wrenches, rather than hydraulic crimpers, priced at USD 3,000–8,000. Crimp lugs remain popular for temporary power distribution, whereas solder lugs persist in aerospace and defense instrumentation. The cable lugs market size derived from compression products will continue to rise, yet mechanical styles will secure incremental share in remote substations and offshore platforms.

Mechanical lugs employ set-screw or shear-bolt designs that withstand pull-out forces of 10 kN without the need for specialized tools. NEMA torque tables published in 2024 guide installers on 15–135 N m settings across conductor sizes, improving consistency. Offshore wind developers prefer mechanical lugs because cramped nacelles hinder the use of hydraulic tools. Meanwhile, compression lugs undergo regular renewals in industrial plants, where decades of field data validate their reliability. This twin-track demand underpins steady expansion in the cable lugs market.

By Insulation Type: Fully Insulated Lugs Lead On Safety Mandates

Fully insulated lugs captured 49.60% of 2025 revenue and are advancing at an 7.68% CAGR as NFPA 70E and European codes impose touch-safe standards. Non-insulated variants are suitable for high-temperature zones above 200 °C, such as arc furnaces, while partially insulated designs facilitate visual inspection inside control panels. The cable lugs market share of insulated products will widen because EV charging stations and commercial buildings increasingly specify sleeves with dielectric strengths above 10 kV.

UL 486E requires insulation to resist 100 N axial pull without separation, forcing manufacturers to refine adhesive chemistries. Color-coded sleeves reduce wiring errors by 30% in data centers, according to field audits. Suppliers also explore modular systems with removable sleeves that fit multiple barrel sizes, trimming distributor inventories by 30%. Enhanced safety mandates, therefore, reinforce a robust growth pipeline for insulated offerings across the cable lugs market.

Geography Analysis

Asia-Pacific accounted for 39.85% of 2025 revenue thanks to China’s 120 GW solar and 75 GW wind additions that each need 300–500 lugs per megawatt for inverter and grounding circuits. India installed 18 GW of renewables in 2024 and targets 500 GW non-fossil capacity by 2030, keeping compression lugs rated 33 and 66 kV in continuous demand. Japan and South Korea advance offshore wind pipelines beyond 5 GW each, requiring salt-spray-resistant tinned-copper lugs. Southeast Asia adds coal and gas plants to meet 7% annual load growth, thus buying mechanical lugs for generator step-up transformers. Australia plans 3 GW of battery storage by 2030, employing 200–300 lugs per megawatt-hour. Collectively, Asia-Pacific projects cement the region’s lead in the cable lugs market.

The Middle East and Africa are projected to grow at an 8.05% CAGR, driven by Saudi Arabia’s 58.7 GW renewables roadmap and the United Arab Emirates’ 5 GW Al Dhafra solar park, which boosts demand. Egypt’s 1.8 GW Benban complex used more than 500,000 compression lugs for medium-voltage grids, while South Africa’s REIPPP awarded 2.6 GW of projects that need 132 kV terminations spanning 200 km lines. Nigeria upgrades substations to accommodate 4 GW of new capacity, opting for mechanical lugs for live-line maintenance. Turkey’s 150,000 EVs built in 2024 rely on fully insulated lugs for export compliance. These developments propel regional share in the cable lugs market.

North America and Europe collectively account for approximately 5.00% of the market. The U.S. Grid Resilience and Innovation Partnerships program funds 58 projects that will order roughly 2 million lugs for reconductoring and substation upgrades. Germany’s offshore wind fleet reached 8.5 GW in 2024, with each turbine carrying 80–120 lugs of nacelle wiring. The UK Building Safety Act 2024 requires contractors to use factory-tested lugs with traceable serial numbers. South America experiences a moderate uptake, as Brazil added 4.5 GW of wind in 2024, whereas Argentina’s Vaca Muerta gas program requires mechanical lugs for remote substations. Geographic diversity thus cushions the cable lugs market against localized slowdowns.

Competitive Landscape

The cable lugs market is moderately fragmented, with the top 10 suppliers accounting for roughly 55% of the 2024 revenue. ABB, Schneider Electric, and TE Connectivity leverage vertically integrated portfolios that bundle lugs with switchgear, easing procurement for contractors. Klauke, Burndy, and Panduit differentiate through proprietary compression ratios and inspection-window designs that facilitate infrared surveys. Molex, HellermannTyton, and NKT target niche applications such as telecom cabinets and marine duty, rounding out a balanced vendor mix.

Competition pivots on three axes. First, conformity to IEC 61238 and UL 486A-486B is mandatory for utility and industrial bids. Second, tooling agility matters; Klauke ships custom dies within 72 h, while TE Connectivity launched torque-indicating mechanical lugs that remove calibrated tool dependence. Third, emerging battery-storage and offshore wind projects demand corrosion-resistant alloys and factory-tested terminations. Counterfeiting risk remains acute in Southeast Asia, where UL warned that 12% of samples failed short-circuit tests. Authentic suppliers combat fakes with laser-etched serials and blockchain registries.

White-space opportunities arise in direct-current circuits above 1,500 V where galvanic corrosion degrades copper-aluminum bimetallic lugs. TE Connectivity filed a 2024 patent for carbon-nanotube barrels that cut contact resistance by 15% and withstand 20,000 thermal cycles. Legrand invests in copper-clad aluminum research to halve weight, while Eaton partners with Nexans on prefabricated harnesses that trim field work by 50%. As sustainability drives the need for wider conductor sizes and higher voltages, vendors that align rapid R&D with standards compliance are best positioned in the cable lugs market.

Cable Lugs Industry Leaders

The 3M Company

Weidmüller Interface GmbH and Co. KG

Legrand SA

Schneider Electric SE

Hubbell Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Schneider Electric committed EUR 85 million (USD 92 million) to expand its Grenoble, France, plant, adding lines for 800-V fully insulated lugs aimed at European EV makers.

- September 2025: ABB acquired 60% of Klauke GmbH, merging hydraulic crimp tools and specialty lugs into its Electrification unit to gain share in European grid upgrades.

- August 2025: TE Connectivity released mechanical lugs with color-changing torque screws that verify tightness without a wrench, certified to IEC 61238-1.

- July 2025: Hubbell opened a USD 45 million automated plant in Monterrey, Mexico, producing 15 million lugs annually for EV and data-center customers.

- June 2025: Eaton partnered with Nexans to deliver prefabricated wiring harnesses for AI-centric data centers, halving field installation time.

- May 2025: Legrand invested EUR 30 million (USD 33 million) in an R&D center exploring copper-clad aluminum lugs for circuits above 400 A.

- April 2025: Amphenol bought a minority stake in a Chinese plastic-lug producer to secure glass-fiber-reinforced nylon components for lightweight EV applications.

- March 2025: Panduit achieved UL 486E certification for 150 °C fully insulated lugs targeting EV chargers and motor control centers.

Global Cable Lugs Market Report Scope

The Cable Lugs Market Report is segmented by Material Type, which includes Copper, Aluminum, Plastic, and Other Material Types (Stainless Steel and Others); by Lug Type, categorized into Ring Lugs, Fork Lugs, Pin Lugs, Butt Splice Lugs, and Others; by End-User Industry, covering Construction, Automotive, Energy and Utilities, Manufacturing and Processing, and Other End-user Verticals; by Installation Method, which includes Crimp Lugs, Solder Lugs, Compression Lugs, and Mechanical Lugs; and by Insulation Type, including Non-Insulated, Partially Insulated, and Fully Insulated. Geographically, the report covers North America (United States, Canada, Mexico), South America (Brazil, Argentina, Rest of South America), Europe (Germany, United Kingdom, France, Italy, Spain, Russia, Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia, Rest of Asia-Pacific), and Middle East and Africa (Middle East: Saudi Arabia, United Arab Emirates, Turkey, Rest of Middle East; Africa: South Africa, Nigeria, Egypt, Rest of Africa). The market forecasts are provided in terms of value (USD).

| Copper |

| Aluminum |

| Plastic |

| Other Material Types (Stainless Steel and Others) |

| Ring Lugs |

| Fork Lugs |

| Pin Lugs |

| Butt Splice Lugs |

| Others |

| Construction |

| Automotive |

| Energy and Utilities |

| Manufacturing and Processing |

| Other End-user Verticals |

| Crimp Lugs |

| Solder Lugs |

| Compression Lugs |

| Mechanical Lugs |

| Non-Insulated |

| Partially Insulated |

| Fully Insulated |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Material Type | Copper | ||

| Aluminum | |||

| Plastic | |||

| Other Material Types (Stainless Steel and Others) | |||

| By Lug Type | Ring Lugs | ||

| Fork Lugs | |||

| Pin Lugs | |||

| Butt Splice Lugs | |||

| Others | |||

| By End-user Industry | Construction | ||

| Automotive | |||

| Energy and Utilities | |||

| Manufacturing and Processing | |||

| Other End-user Verticals | |||

| By Installation Method | Crimp Lugs | ||

| Solder Lugs | |||

| Compression Lugs | |||

| Mechanical Lugs | |||

| By Insulation Type | Non-Insulated | ||

| Partially Insulated | |||

| Fully Insulated | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the cable lugs market in 2026 and how fast is it growing?

The cable lugs market size is USD 3.39 billion in 2026 and is forecast to rise at a 6.01% CAGR to reach USD 4.54 billion by 2031.

Which lug material holds the biggest share today?

Copper lugs command 44.85% of 2025 revenue because of their high conductivity and proven reliability.

What segment is expanding fastest within the cable lugs business?

Butt splice lugs show the highest growth, advancing at a 8.79% CAGR as solar and wind projects adopt modular harnesses.

Which region leads global demand for cable lugs?

Asia Pacific accounts for about 39.85% of 2025 revenue, propelled by large-scale renewable installations in China and India.

How are safety regulations influencing product demand?

Updated NFPA 70E and European codes mandate fully insulated, touch-safe terminations, propelling demand for insulated compression lugs.

What competitive factors matter most when selecting a lug supplier?

Compliance with IEC 61238 and UL 486A-486B, rapid tooling customization, and traceability features top the procurement checklist for contractors and OEMs.

Page last updated on: