Waterjet Cutting Machine Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

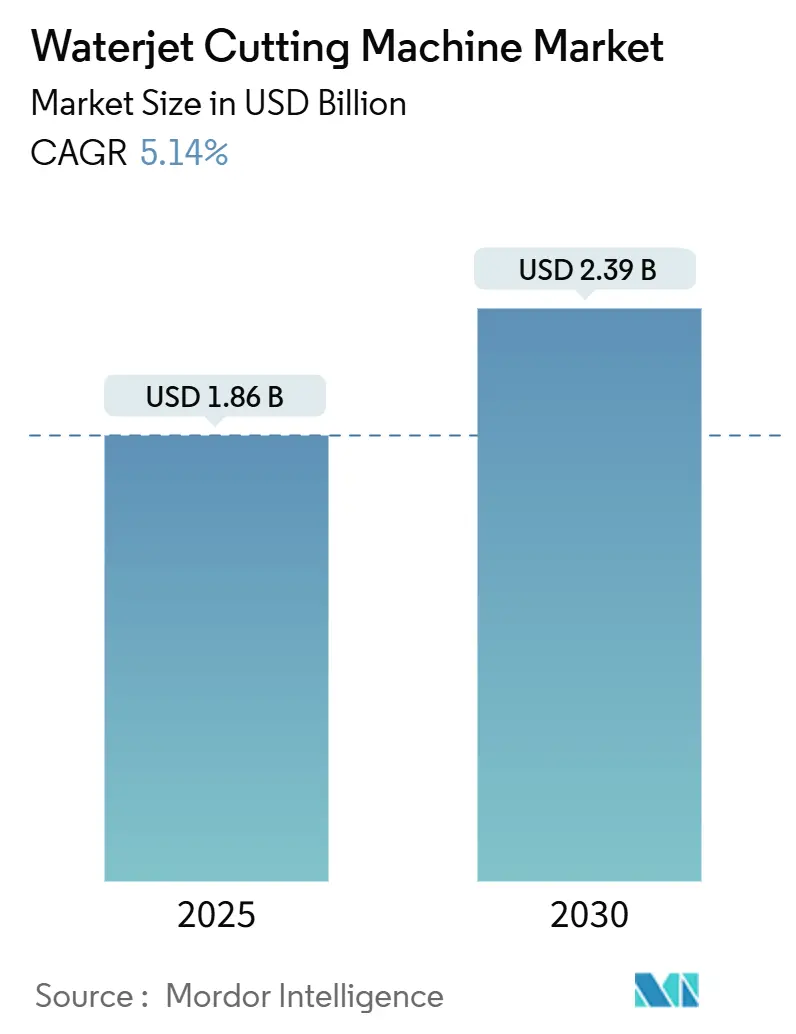

| Market Size (2025) | USD 1.86 Billion |

| Market Size (2030) | USD 2.39 Billion |

| Growth Rate (2025 - 2030) | 5.14% CAGR |

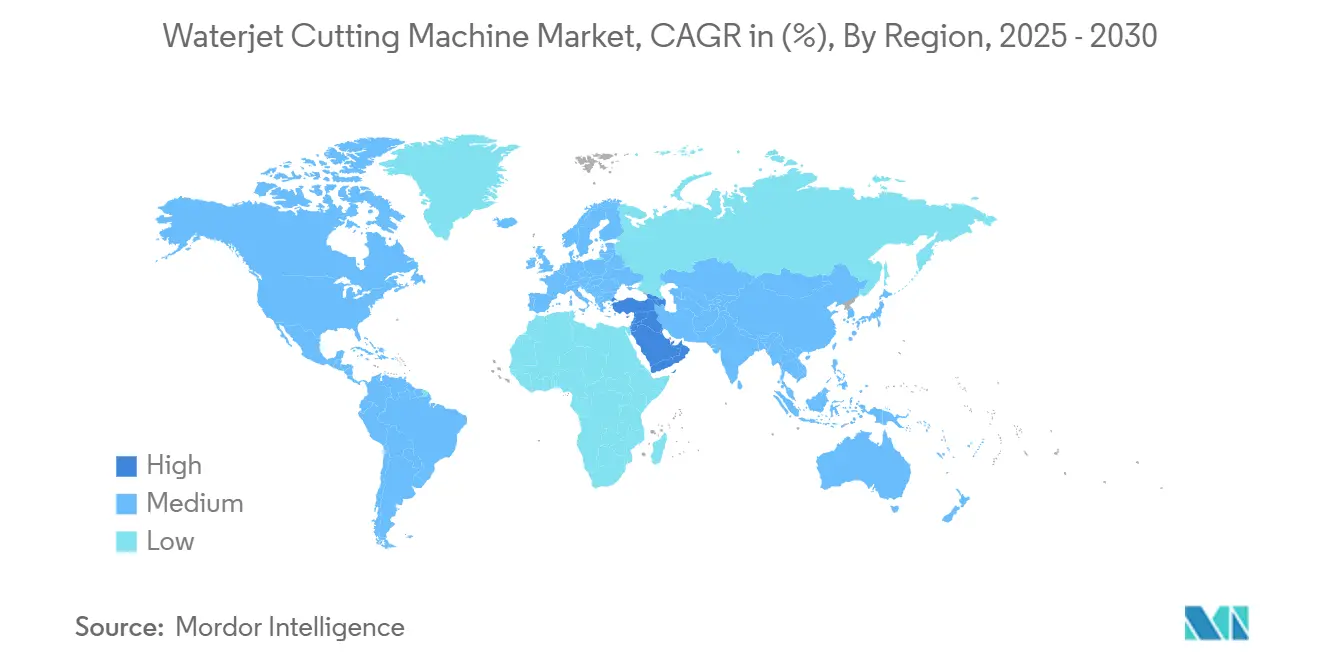

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

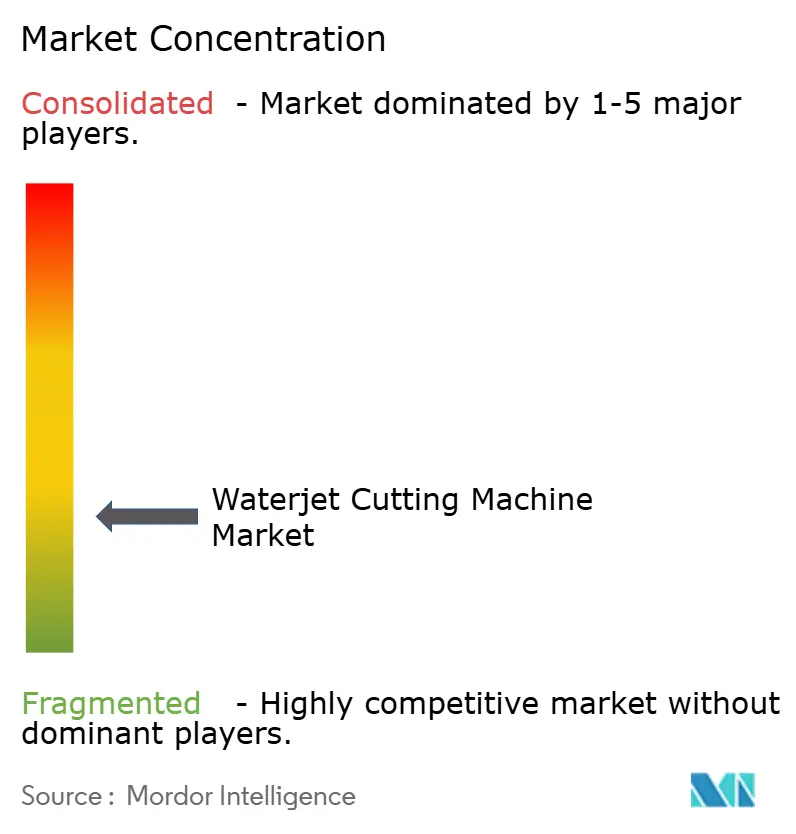

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Waterjet Cutting Machine Market Analysis by Mordor Intelligence

The Waterjet Cutting Machine Market size is estimated at USD 1.86 billion in 2025, and is expected to reach USD 2.39 billion by 2030, at a CAGR of 5.14% during the forecast period (2025-2030). Consistent demand for non-thermal, high-precision cutting in aerospace, automotive, and medical manufacturing sustains expansion even as the technology matures. Ultra-high-pressure systems above 6,000 bar set the performance frontier, enabling rapid processing of carbon-fiber composites and hard-to-machine EV alloys. Asia-Pacific retains volume leadership, while Middle East industrial diversification drives the fastest regional upswing. Competitive differentiation pivots on pump efficiency, automation software, and service reach instead of headline price.

Key Report Takeaways

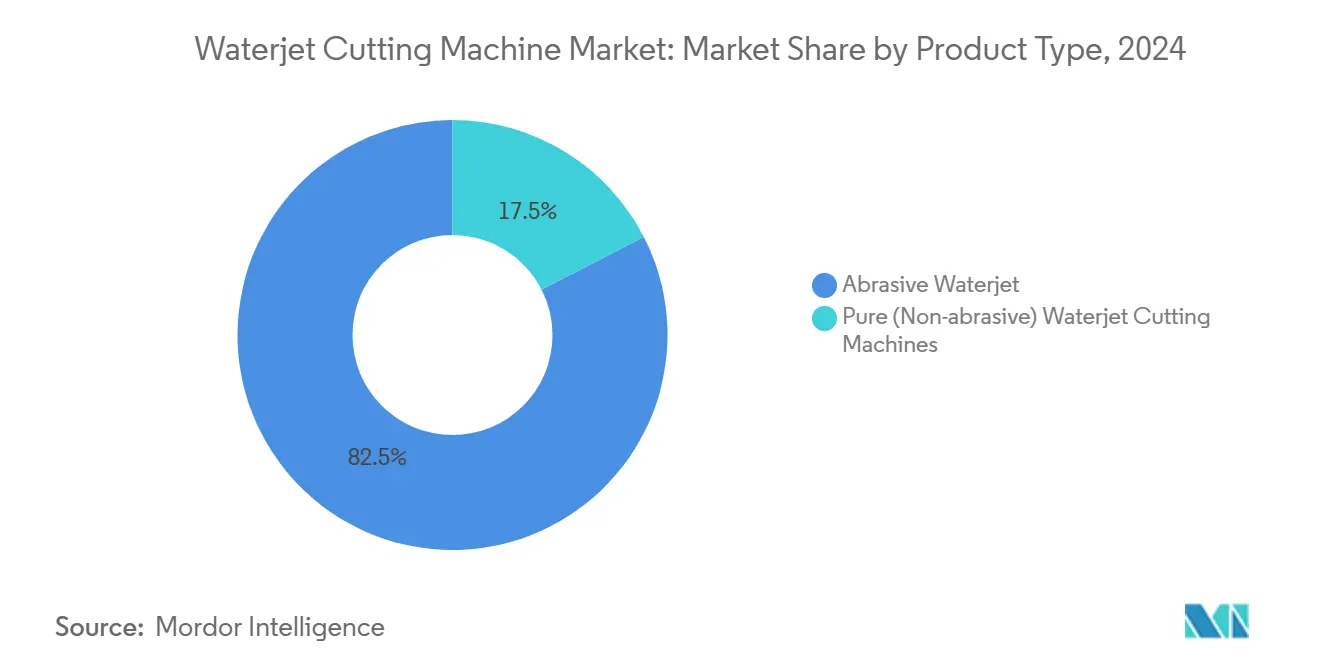

- By product type, abrasive systems commanded 82.54% of the waterjet cutting machine market share in 2024; pure waterjet solutions are projected to climb at a 7.5% CAGR to 2030.

- By axis configuration, 3-axis tables led with 50.44% revenue share in 2024, while 5-axis formats exhibit the highest growth at 7.8% CAGR.

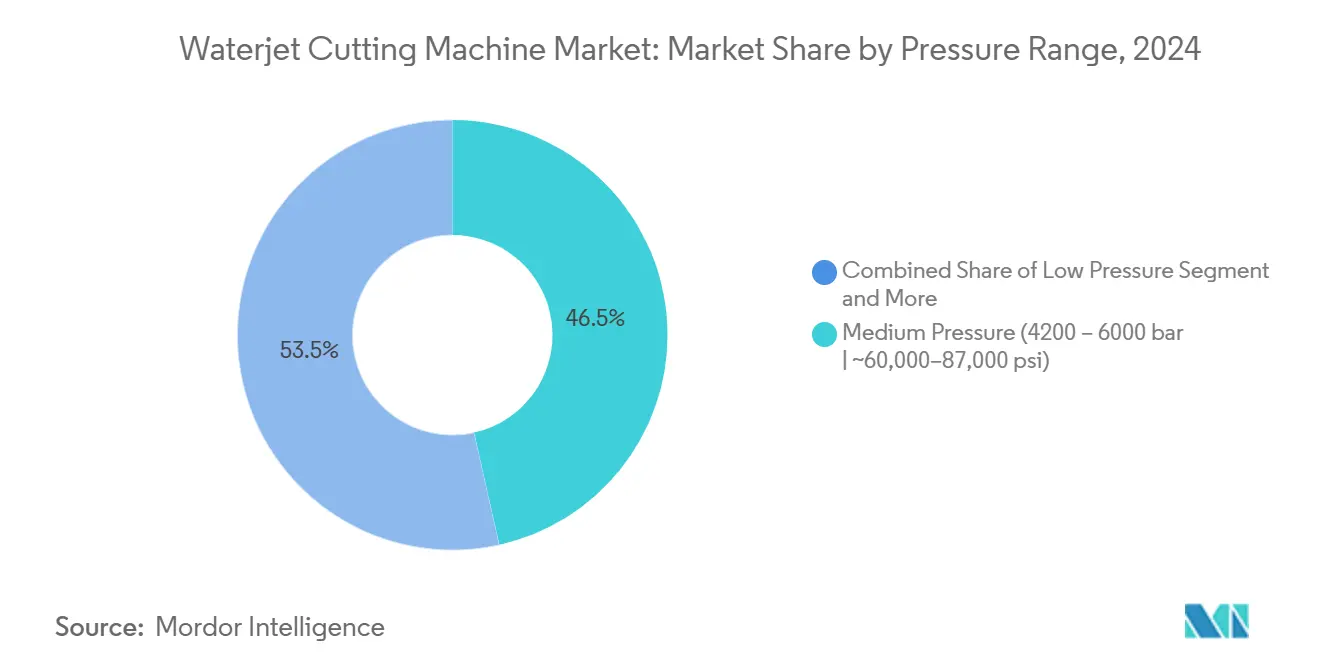

- By pressure range, medium-pressure units (4,200-6,000 bar) held 46.5% share of the waterjet cutting machine market size in 2024, whereas ultra-high-pressure models exceeded all segments with an 8.8% CAGR through 2030.

- By pump type, hydraulic intensifier systems retained a 61.5% share of the waterjet cutting machine market in 2024; direct-drive pumps post an 8.3% CAGR on efficiency gains.

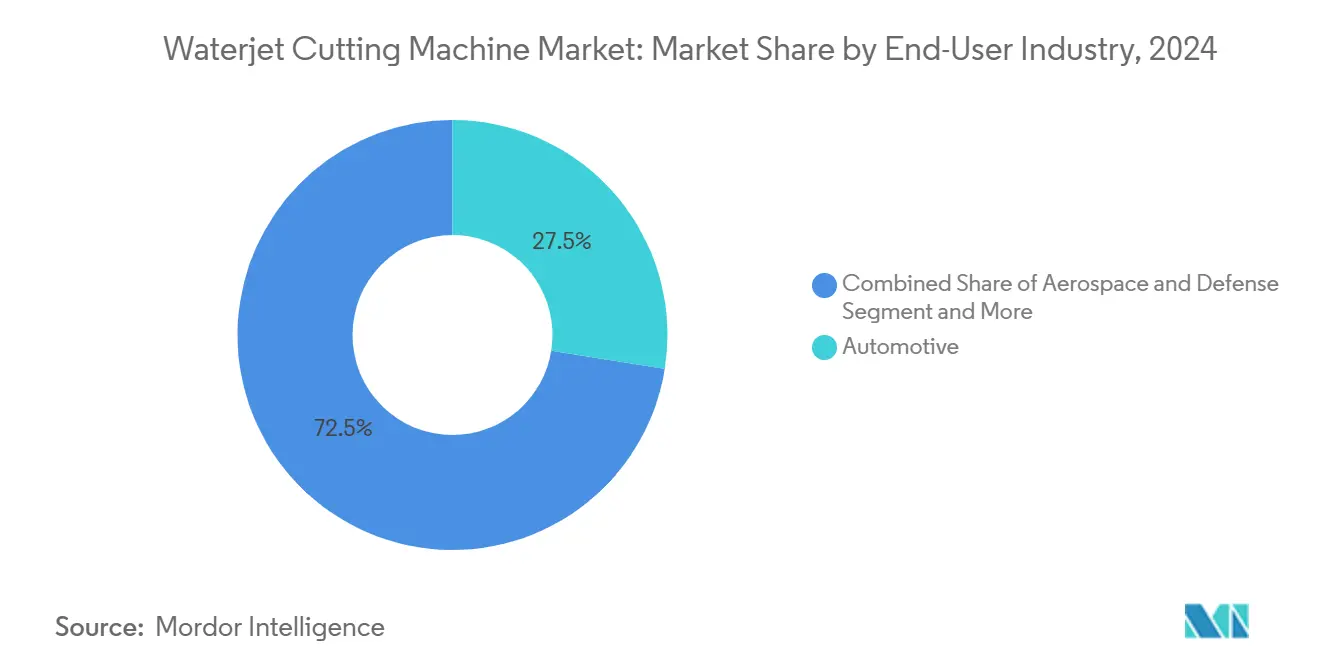

- By end-user industry, automotive applications contributed 27.5% of 2024 revenue in the waterjet cutting machine market; medical devices show the strongest trajectory, expanding at 8.6% CAGR to 2030.

- By geography, Asia-Pacific generated 37.8% of 2024 revenues; the Middle East is set to rise at a 7.3% CAGR through 2030.

Global Waterjet Cutting Machine Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid penetration of 5-axis & robotic waterjet systems in precision fabrication | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rising adoption for hard-to-machine alloys in EV & e-mobility parts | +0.9% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Growing use of ultra-high-pressure (greater than 6k bar) jets in aerospace composites | +0.8% | North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| Reshoring-led capex cycle in North American metal shops | +0.7% | North America, secondary impact in Mexico | Medium term (2-4 years) |

| Modular intensifier pumps reducing operating cost per cut | +0.6% | Global | Long term (≥ 4 years) |

| ESG-driven shift away from plasma & laser in food and pharma packaging | +0.5% | Global, with early adoption in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Penetration of 5-Axis & Robotic Waterjet Systems in Precision Fabrication

Advanced motion control transforms conventional 2D cutting into true 3D manufacturing, allowing a single setup to replace multiple downstream operations. Dynamic Waterjet heads equipped with active tolerance compensation now deliver 2-4 × faster cycle times while preserving edge quality. Articulated robots running at 90,000 PSI integrate beveling and piercing in automotive cell production, easing labor-skill constraints and enabling lights-out shifts. Demonstrations of ±2 µm tolerances in micro-waterjet platforms extend the application envelope to surgical implants, reflecting the tool-room precision now achievable on shop floors.

Rising Adoption for Hard-to-Machine Alloys in EV & E-Mobility Parts

Battery housings, structural beams, and motor cores fabricated from titanium, high-strength steels, and composite stacks benefit from the waterjet’s cold-cut attribute that avoids heat-affected zones. Cut thickness capability up to 24 inches removes secondary milling, lowering takt times for EV chassis components. Pump pressures of 90,000 PSI provide the energy density needed for thick-stack piercing, while integrated nesting software maximizes material utilization amid elevated alloy costs.

Reshoring-Led Capex Cycle in North American Metal Shops

Tighter supply chains and incentives for local production spark renewed machine-tool investment across U.S. and Mexican fab shops. Domestic waterjet builders emphasize vertically integrated plants that shorten delivery and service lead times. Investments exceeding USD 10 million in new southeastern U.S. production lines hint at a broader industrial infrastructure renewal that favors flexible, non-thermal cutting systems capable of multi-material workloads[1]U.S. Bureau of Labor Statistics Analysts, “Manufacturing Reshoring Indicators: 2024 Update,” U.S. Department of Labor, bls.gov.

Modular Intensifier Pumps Reducing Operating Cost Per Cut

Next-gen pumps feature cartridge-style seals, electronic pressure regulation, and condition-based monitoring that together lengthen maintenance intervals and curb unplanned downtime. Direct-drive variants achieve energy efficiencies above 83% and eliminate hydraulic oil, while ultra-high-pressure intensifiers bring dual-pressure modes that fine-tune jet performance for thin and thick sections alike.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising abrasive procurement/logistics costs due to supply chain volatility | -0.9% | Global, with acute impact in regions dependent on imports | Medium term (2-4 years) |

| Intensifier seal-life limitations in greater than 6k bar systems | -0.8% | Global, particularly affecting high-pressure applications | Short term (≤ 2 years) |

| Availability of low-cost CO₂ laser tables in Asia | -0.7% | APAC core, competitive pressure globally | Short term (≤ 2 years) |

| Facility-level noise & slurry disposal compliance costs (EU) | -0.6% | Europe, with regulatory spillover to other regions | Medium term (2-4 years) |

| Scarcity of garnet abrasives in Nordic quarries post-2023 bans | -0.4% | Europe & North America, affecting premium abrasive supply | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifier Seal-Life Limitations in Greater Than 6 k Bar Systems

Seal fatigue accelerates with rising jet pressures, triggering maintenance cycles after only 250,000 strokes and complicating high-volume composite machining. Predictive diagnostics mitigate unscheduled stops yet do not fully resolve the materials-science hurdle that restrains full-shift utilization of 90,000 PSI pumps.

Facility-Level Noise & Slurry Disposal Compliance Costs (EU)

European directives mandate strict decibel ceilings and classify spent garnet as regulated waste if metallic contaminants exceed thresholds. SMEs face capital outlays for sound-dampening enclosures and closed-loop filtration, raising the total cost of ownership in an otherwise price-sensitive equipment segment[2]European Commission Directorate-General Environment, “Best Available Techniques (BAT) Reference Document for Waste Treatment,” European Commission, ec.europa.eu.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Abrasive Systems Drive Volume Growth

Abrasive platforms captured 82.54% of 2024 revenue, reinforcing their status as the workhorse of the waterjet cutting machine market. Their capability to slice 24-inch-thick Inconel plates at ±0.001-inch tolerances underpins adoption in aerospace skins and heavy equipment frames. Conversely, pure-water variants gain ground in sanitary packaging lines, advancing at a 7.5% CAGR as USDA-compliant designs avoid cross-contamination and reduce wash-down time.

Growth trajectories diverge because abrasive jets excel on rigid substrates, whereas nozzle-only systems target delicate food, pharma film, and foam tasks. Regulatory emphasis on hygiene, plus lower consumables cost, positions pure waterjet as an entry path for processors seeking gentle, residue-free cutting. The cross-segment dynamic ensures that the waterjet cutting machine market continues broadening its addressable base without cannibalizing its industrial stronghold.

By Axis Configuration: Multi-Axis Systems Enable Complex Geometries

Three-axis tables still represent half of global shipments, reflecting entrenched demand for flat-plate profiling in job shops. Yet 5-axis machines post a 7.8% CAGR as beveling, taper compensation, and 3D sculpting shrink fixture counts and boost first-part accuracy. Automated tilt heads linked to CAD-CAM suites now contour CFRP wing spars in one pass, replacing costly, multi-station milling.

Robotic cells sit in the premium tier, pairing articulated arms with ultra-high-pressure pumps to deliver endless reach for dashboard trimming, battery pack venting, and pie-shaped rotor slots. Micro-waterjet systems, meanwhile, push into sub-50-µm kerf widths, bridging the gap between EDM and mechanical micro-milling. Collectively, motion complexity upgrades are redefining the capability ceiling of the waterjet cutting machine market.

By Pressure Range: Ultra-High Pressure Drives Performance Gains

Medium-pressure equipment (4,200-6,000 bar) remains mainstream with 46.5% of 2024 billings, supplying balanced speed, cost, and maintenance profiles for shops processing mild steel, stainless, and stone. Ultra-high-pressure offerings, however, climb at 8.8% CAGR as aerospace primes and Formula E constructors chase faster feed rates and cleaner edges in carbon ceramics and titanium.

R&D advances in cyclic-fatigue resistant components and servo-controlled ramps allow 90,000 PSI jets to operate for longer bursts, narrowing the maintenance penalty historically linked with extreme pressures. As price gaps shrink and throughput gains materialize, more fabricators justify the premium, moving the performance benchmark of the waterjet cutting machine market steadily upward[3]Yasushi Takagi, “Effect of Working Pressure on CFRP Cut Quality With 500 MPa Waterjet,” ASME Journal of Manufacturing Science and Engineering, asme.org.

By Pump Type: Direct-Drive Systems Challenge Traditional Designs

Hydraulic intensifiers keep a 61.5% hold on revenues thanks to unrivaled pressure ceilings above 60,000 PSI that suit aerospace and defense contracts. Direct-drive pumps, expanding 8.3% annually, attract energy-sensitive users with 20-30% lower electricity draw and minimal hydraulic fluid overhead.

Recent launches feature swash-plate designs with real-time speed modulation that stabilize jet coherence at low nozzle diameters. Efficient water usage aligns with corporate sustainability initiatives, making direct-drive units a favored upgrade path for sheet-metal shops inside net-zero roadmaps. The co-existence of both architectures ensures a wide choice, reinforcing the adaptability of the waterjet cutting machine market.

By End-User Industry: Medical Devices Lead Growth Acceleration

Automotive producers anchored 27.5% of 2024 turnover through high-mix EV body structures and battery housings that need cold cutting. Medical-device firms, though smaller in revenue, accelerate fastest at 8.6% CAGR, leveraging micron-level accuracy for orthopedic screws, cardiovascular stents, and dental implants where burr-free edges are mandatory.

Aerospace continues to drive pump and nozzle innovation for composite fuselages, while electronics assemblers adopt pure-water variants to dice brittle glass substrates without inducing micro-cracks. The widening spectrum of addressable sectors underlines how the waterjet cutting machine market leverages its non-thermal nature to penetrate niches unreachable by lasers or plasma.

By Material Cut: Advanced Materials Drive Segment Expansion

Metal sheets and billets still account for 58.9% of feedstock run through global machines, cementing the technology’s importance in metal fabrication value chains. Yet plastics, composites, and foams register the quickest rise at 8.2% CAGR, propelled by e-mobility battery insulation liners and lightweight interior panels.

Architectural stone and ceramic tiling hold steady in the construction domain, while tempered glass for infotainment displays fuels niche growth in consumer electronics. Versatility across dissimilar substrates differentiates the waterjet cutting machine market from thermal peers that struggle with reflective or layered materials.

Geography Analysis

Asia-Pacific generated 37.8% of worldwide 2024 revenue in the waterjet cutting machine market, underpinned by dense manufacturing ecosystems in China, India, Japan, and the ASEAN bloc. Government initiatives championing localized high-value production, together with surging EV output, anchor long-term demand. Domestic OEMs offer cost-competitive models, but Western brands retain share in ultra-high-precision installations, illustrating a two-tier import-local mix.

The Middle East is poised to outpace all regions at a 7.3% CAGR to 2030. Sovereign programs such as Saudi Vision 2030 funnel capital into aerospace, shipbuilding, and renewable infrastructure, each requiring advanced cutting methods. Localization agreements between global pump specialists and Gulf manufacturers signal an emergent regional supply chain for the waterjet cutting machine market[4]Saudi Press Agency Staff, “MAKEEN Signs MoU With Kongsberg Maritime to Localize Waterjet Industry,” Saudi Press Agency, spa.gov.sa.

North America sustains a high installed-base value through reshoring tailwinds and defense procurement. Aerospace composite wingskins, naval propulsion housings, and custom vehicle mods keep demand stable, while Mexico’s maquiladora corridors add greenfield opportunities. Europe remains technology-intensive yet price-pressured, with strict environmental directives steering buyers toward energy-efficient, closed-loop systems that satisfy EU waste and noise norms.

Competitive Landscape

The sector features a cluster of long-standing specialists, Flow International, OMAX, and Hypertherm Associates, supplemented by regional integrators and abrasive suppliers. Technology roadmaps emphasize predictive analytics, cloud-connected controllers, and low-maintenance pumps rather than headline horsepower alone. Hypertherm’s minority stake in BLM Group pairs tube-cutting expertise with in-house plasma and waterjet know-how, broadening channel coverage across Europe and North America.

IP filings spotlight nozzle geometries that recycle abrasive particles, plus software that dynamically alters jet lag for curved contours. Mid-sized entrants carve out footholds through application kits for pharma pouches or micro-nozzle stents, niches that giants consider sub-scale. Price sensitivity persists, yet buyers increasingly evaluate total lifecycle cost, favoring vendors with in-region service crews and parts depots—an advantage leveraged by manufacturers operating vertically integrated U.S. campuses.

Overall, rivalry intensity remains moderate. Switching costs tied to operator training and spare-parts ecosystems deter rapid vendor turnover, fostering recurring revenue via maintenance contracts. As consolidation creeps in, the market rewards firms that fuse pump R&D with intuitive software, ensuring the waterjet cutting machine market evolves toward smarter, more reliable platforms.

Waterjet Cutting Machine Industry Leaders

OMAX Corporation

Flow International Corporation

Hypertherm Inc.

Bystronic Group

WardJet LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Hypertherm Associates acquired a minority stake in BLM Group, aligning plasma, waterjet, and tube-processing portfolios for broader geographic reach.

- November 2024: BLM GROUP entered a comprehensive distribution pact with Hypertherm, retaining operational autonomy while accessing wider channels.

- October 2024: MAKEEN and Kongsberg Maritime signed an MoU to localize waterjet assembly and training programs in Saudi Arabia, advancing Vision 2030 manufacturing goals.

- October 2024: Flow International appeared on Netflix’s “Car Masters: Rust to Riches” Season 6, showcasing a Mach 500 system in custom auto builds.

Global Waterjet Cutting Machine Market Report Scope

| Abrasive Waterjet Cutting Machines |

| Pure (Non-abrasive) Waterjet Cutting Machines |

| 3-axis Tables |

| 5-axis Tables |

| Others (Robotic (Articulated-arm) Waterjet Cells, Micro-precision Waterjet Systems) |

| Low Pressure (Less than 4200 bar | Less than ~60,000 psi) |

| Medium Pressure (4200 – 6000 bar | ~60,000–87,000 psi) |

| Ultra-High Pressure (Greater than 6000 bar | Greater than ~87,000 psi) |

| Direct-drive Pumps |

| Hydraulic Intensifier Pumps |

| Automotive |

| Aerospace & Defense |

| Electronics & Semiconductors |

| Metal Fabrication |

| Construction & Mining |

| Medical Devices |

| Others (Textile & Leather, Food & Beverage Processing) |

| Metals |

| Stone, Ceramic & Tiles |

| Glass |

| Others (Plastics & Composites, Rubber, Foam, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Abrasive Waterjet Cutting Machines | |

| Pure (Non-abrasive) Waterjet Cutting Machines | ||

| By Axis / Configuration | 3-axis Tables | |

| 5-axis Tables | ||

| Others (Robotic (Articulated-arm) Waterjet Cells, Micro-precision Waterjet Systems) | ||

| By Pressure Range | Low Pressure (Less than 4200 bar | Less than ~60,000 psi) |

| Medium Pressure (4200 – 6000 bar | ~60,000–87,000 psi) | |

| Ultra-High Pressure (Greater than 6000 bar | Greater than ~87,000 psi) | |

| By Pump Type | Direct-drive Pumps | |

| Hydraulic Intensifier Pumps | ||

| By End-user Industry | Automotive | |

| Aerospace & Defense | ||

| Electronics & Semiconductors | ||

| Metal Fabrication | ||

| Construction & Mining | ||

| Medical Devices | ||

| Others (Textile & Leather, Food & Beverage Processing) | ||

| By Material Cut | Metals | |

| Stone, Ceramic & Tiles | ||

| Glass | ||

| Others (Plastics & Composites, Rubber, Foam, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the waterjet cutting machine market?

The market is valued at USD 1.86 billion in 2025 and is forecast to grow to USD 2.39 billion by 2030 at a 5.14% CAGR.

Which region holds the largest share of the waterjet cutting machine market?

Asia-Pacific leads with 37.8% of 2024 revenue, supported by extensive manufacturing activity.

Why are medical devices a high-growth end-user sector?

Medical manufacturers require ±2 µm tolerances and burr-free edges for implants, needs that waterjet cutting meets without heat-affected zones.

How are pump innovations lowering ownership costs?

Modular seal cartridges, electronic pressure regulation, and predictive maintenance extend service intervals and reduce unplanned downtime.

Page last updated on: