Cannabis Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.29 Billion |

| Market Size (2031) | USD 4.65 Billion |

| Growth Rate (2026 - 2031) | 15.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cannabis Packaging Market Analysis by Mordor Intelligence

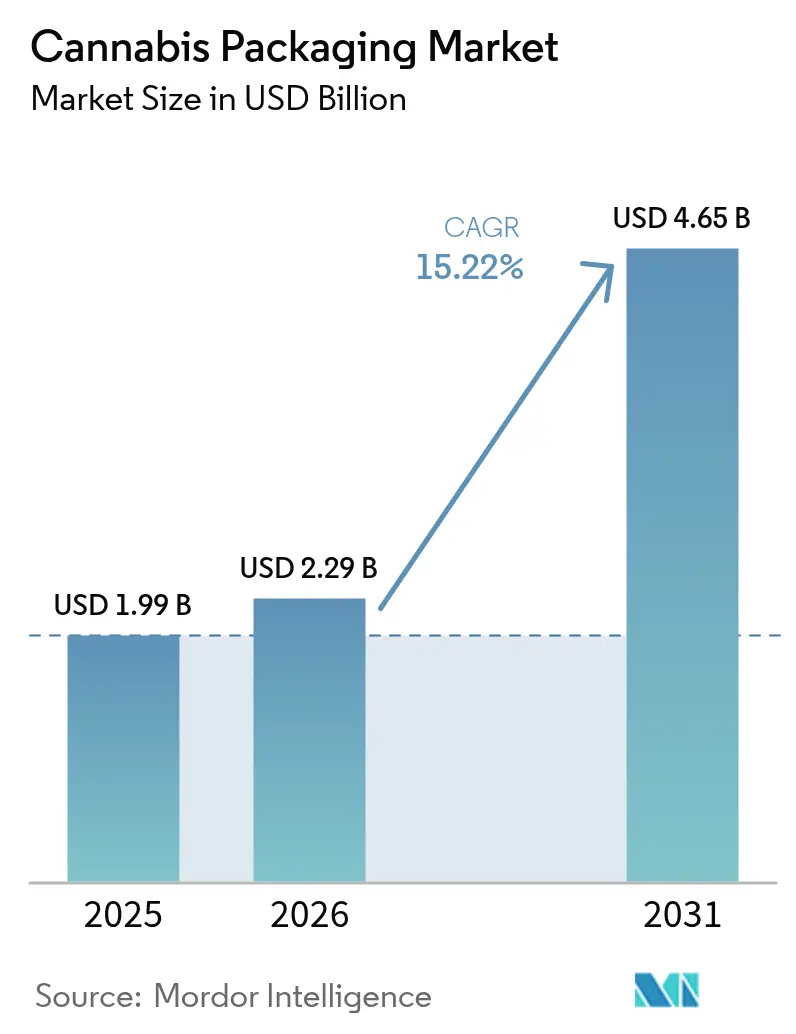

The cannabis packaging market size is expected to grow from USD 1.99 billion in 2025 to USD 2.29 billion in 2026 and is forecast to reach USD 4.65 billion by 2031 at 15.22% CAGR over 2026-2031. This upward trajectory is linked to the expanding legalization of cannabis, stricter global compliance mandates, and rising consumer demand for premium, sustainable packs. The rising demand for medical and recreational cannabis is driving revenue growth in the global cannabis packaging market during the forecast period. Cannabis legalization has significantly increased the demand for various products, necessitating proper packaging to enhance shelf life. This trend is expected to support market revenue growth. Additionally, the growing number of start-ups has introduced a wide range of cannabis-based products, such as oils and beverages, which is anticipated to substantially boost the demand for cannabis packaging. These start-ups are focusing on scaling cultivation, industrial production, and commercializing diverse cannabis products across multiple countries, thereby propelling market growth.

Key Report Takeaways

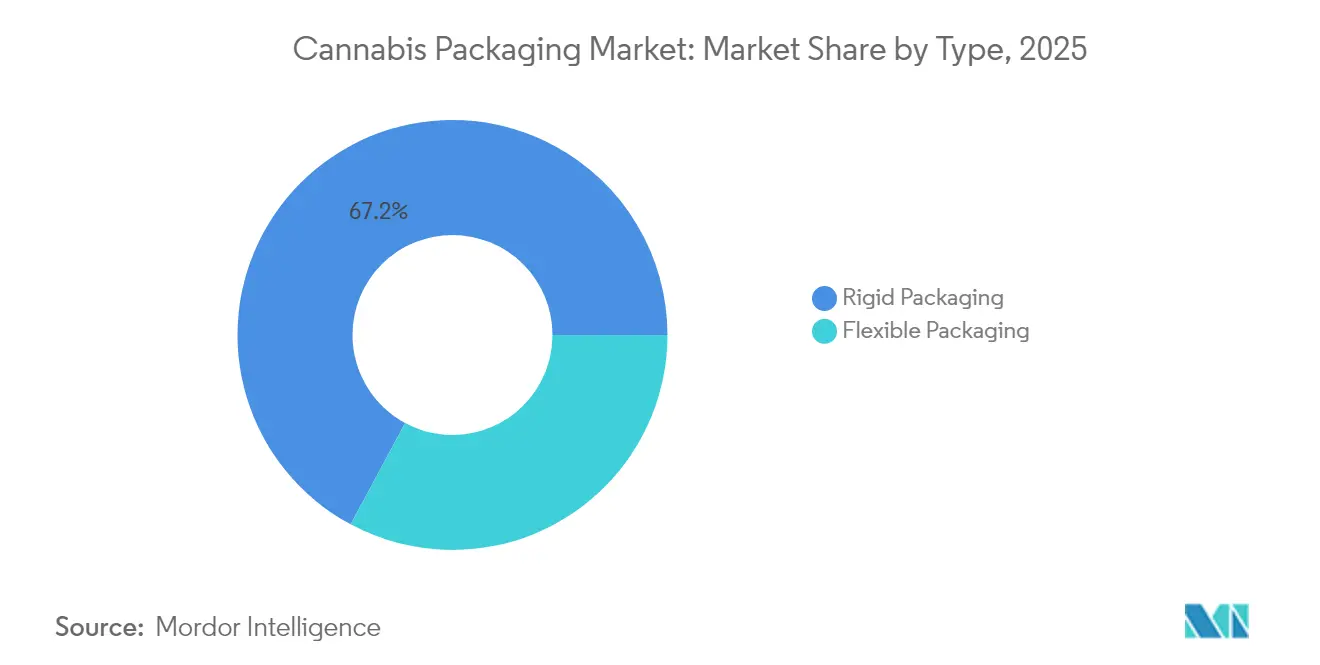

- By type, rigid packaging led with 67.15% of cannabis packaging market share in 2025; flexible packaging is projected to post the highest 17.05% CAGR through 2031.

- By packaging material, plastics commanded 54.20% share of the cannabis packaging market size in 2025, whereas biopolymers are set to advance at a 16.55% CAGR to 2031.

- By application, recreational cannabis accounted for 62.40% of the cannabis packaging market size in 2025; medical cannabis is expanding at a 17.35% CAGR to 2031.

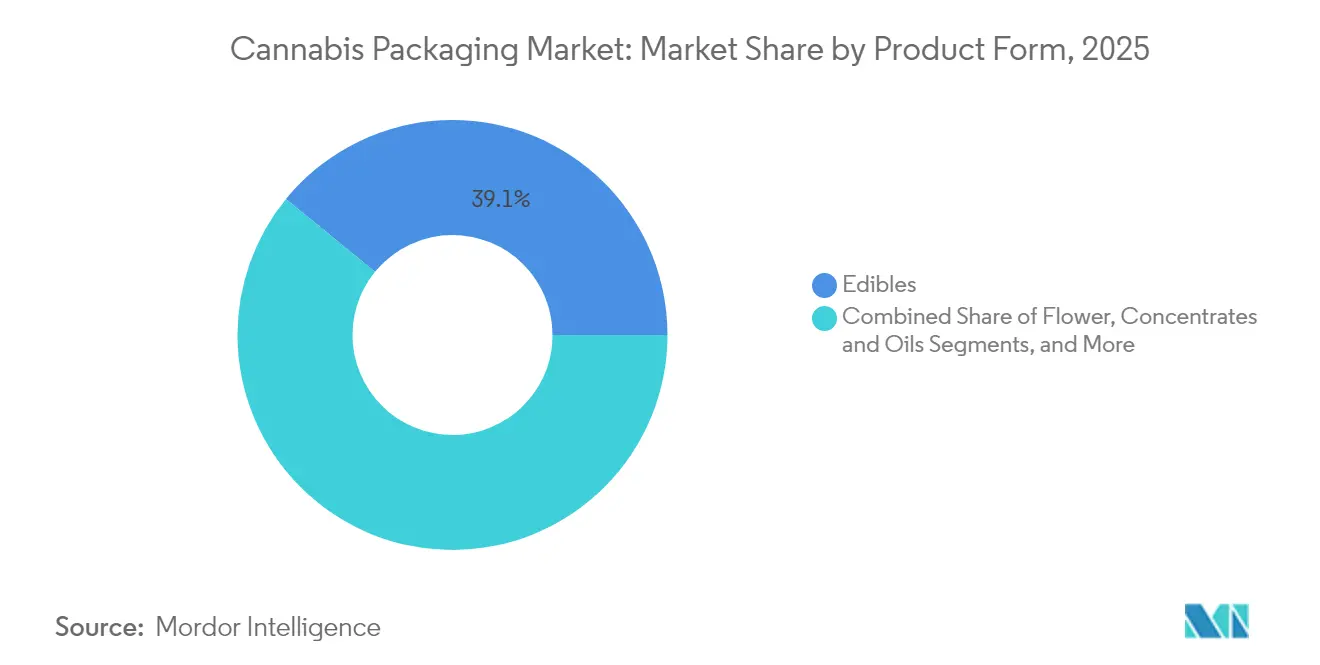

- By product form, edibles held 39.10% revenue share in 2025, while concentrates and oils are forecast to post an 17.60% CAGR through 2031.

- By end user, cultivators and producers represented 44.80% of demand in 2025; processors and manufacturers are set to grow at a 16.08% CAGR through 2031.

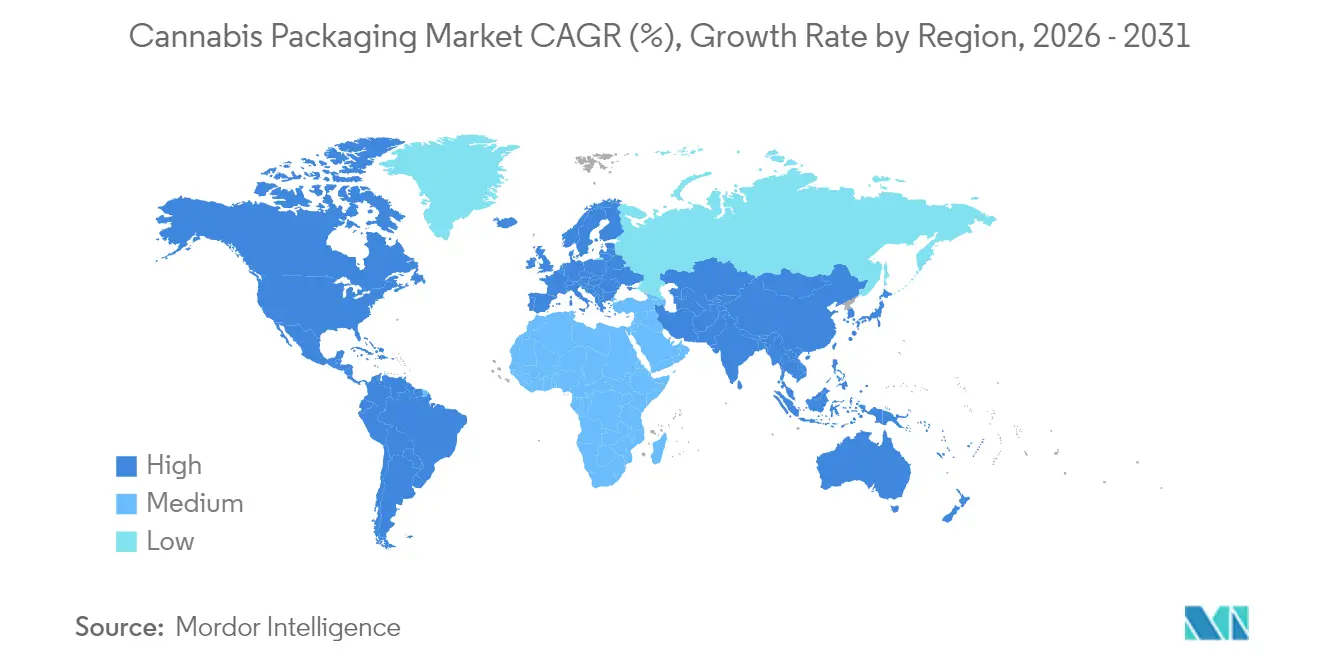

- By geography, North America led with 31.90% share in 2025, yet Asia-Pacific is on track for the fastest 16.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Cannabis Packaging Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legalization wave expanding beyond North America | +4.2% | Global, with early gains in Germany, Australia, Latin America | Medium term (2-4 years) |

| Rising demand for medical and adult-use cannabis products | +3.8% | North America and EU core, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Regulatory push for child-resistant/tamper-evident packs | +2.9% | Global | Short term (≤ 2 years) |

| Growth in CBD-infused novel formats | +2.1% | North America, Europe, Asia-Pacific emerging | Medium term (2-4 years) |

| E-commerce and home-delivery driving unit-level secure packs | +1.7% | Urban centers globally | Short term (≤ 2 years) |

| Smart track-and-trace (NFC/RFID) adoption for compliance | +1.2% | Regulated markets primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legalization wave expanding beyond North America

Germany’s 2024 adult-use approval shifted European packaging from wellness positioning to pharmaceutical-grade expectations, as the Medical Cannabis Act now enforces EU-GMP standards that exceed typical fast-moving consumer goods rules.[1]CMS Germany, “Medical Cannabis Act and Packaging Compliance,” cms.lawAustralia followed with a national reform effective September 2024 that mandates minimum recycled content and recyclability labeling, compelling converters to redesign material mixes. Argentina’s early medical framework continues to shape packaging norms across Brazil and Mexico where new bills reference patient-safe containers and traceability codes. These combined changes add medium-term tailwinds that lift the cannabis packaging market worldwide.

Rising demand for medical and adult-use cannabis products

Pre-rolls now contribute more than 12% of dispensary turnover in mature U.S. states, prompting brands to employ unique structural designs and color codes to signal potency tiers.[2]Sorting Robotics, “Automation Trends in Pre-Roll Packaging,” sortingrobotics.comGreen Thumb Industries refreshed its Dogwalkers line with paperboard cartons that meet child-resistant protocols yet convey a premium feel. Drops Candies reported a six-fold increase in order throughput after installing automated cartoners integrated with compliance printers, proof that end-to-end automation can unlock scale for edibles. Tilray’s Q2 2025 results showed USD 66 million cannabis sales and 36% beverage growth, highlighting cross-category synergies that demand versatile secondary packs.

Regulatory push for child-resistant/tamper-evident packs

New York’s 2024 rule requires 25% post-consumer resin in every cannabis container without sacrificing child resistance, prompting suppliers to blend recycled and virgin materials creatively. Oklahoma’s HB 3361, effective June 2025, mandates flower to be pre-packed in 0.5-3 oz formats with labels that avoid child-appealing graphics, sharpening oversight on visual elements. Canada now allows transparent windows and QR codes, yet still enforces locking features, illustrating a shift toward information transparency without safety compromise. Patent filings for multi-layer latching lids underscore ongoing engineering investment in user-friendly, fail-safe closures.

Growth in CBD-infused novel formats

Japan kept the strictest global THC limit in July 2024, compelling exporters to guarantee zero contamination via high-barrier film and color-shift security inks. The United States Pharmacopeia adopted tighter heavy-metal thresholds that influence liner and sealant selections, especially for beverages and gummies.[3]United States Pharmacopeia, “Cannabis Quality Standards,” usp.orgCann’s drinkable “Cann Canns” line now leverages multi-layer cans with oxygen scavengers to meet stability needs across geographies. Aurora Cannabis recorded 93% international revenue growth and relies on pharmaceutical blister packs that deliver dose accuracy to hospitals, confirming the rising clinical emphasis on CBD formats.

Restraints Impact Analysis of Cannabis Packaging Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented and shifting global regulations | -2.8% | Global, particularly emerging markets | Medium term (2-4 years) |

| Sustainability pressure on single-use plastics | -1.9% | EU, North America, developed markets | Long term (≥ 4 years) |

| SKU churn causing packaging inventory write-offs | -1.4% | Multi-state operators primarily | Short term (≤ 2 years) |

| Supply chain disruptions and material cost inflation | -1.2% | Global, with acute impact in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented and shifting global regulations

A multi-state operator recently managed 2,230 distinct SKUs because every U.S. jurisdiction establishes unique pack sizes, warning labels, and ink color codes. The Universal Cannabis Information Label initiative argues for standard icons and data fields to cut complexity once federal legalization arrives. In Europe, at least 11 legal pathways exist for harmonizing domestic reforms with UN treaties, lengthening approval cycles for new labels. The regulatory mosaic drags on speed-to-shelf, trimming growth momentum for the cannabis packaging market.

Sustainability pressure on single-use plastics

Canada’s legal sector generates millions of pounds of waste annually because opaque, child-resistant jars rarely enter curbside streams. Aqualitas repurposes ocean-bound resin, while 48North turned to compostable carton board, yet policymakers still require opaque surfaces that hinder recyclability. Grove Bags addressed the dilemma with ExIce, a fully water-soluble pouch that maintains terpene integrity and dissolves safely in marine environments. Emerging Extended Producer Responsibility rules will soon shift disposal costs to brand owners, squeezing margins unless greener substitutes achieve parity on performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Cannabis Packaging Market Segment Analysis

By Type:

Automation boosts flexible penetrationRigid formats dominated the cannabis packaging market in 2025 at 67.15% share, primarily through glass jars and double-wall plastic containers that enhance shelf presence for premium flower. The segment benefits from perceived durability and consumer familiarity, yet it faces scrutiny for bulkiness and higher freight intensity. Flexible packs grow at a 17.05% CAGR, underpinned by low material waste, lightweight logistics, and compatibility with high-speed form-fill-seal lines. Stand-up pouches and pillow bags gain traction in edibles, where tamper-evident tear notches and resealable zippers align with portion control mandates.

Automation advantages sustain this shift. Viking Masek’s rotary pouch system supports quick tool-less changeovers that cut downtime when SKU counts climb, a trend visible among multi-state operators. Modified Atmosphere Packaging now integrates nitrogen flushing that curbs terpenoid oxidation, extending shelf life without preservatives. As legalization spreads, contract packers opt for flexible webs to manage volume spikes quickly, enabling the cannabis packaging market to diversify pack formats across global channels.

By Packaging Material:

Biopolymers challenge plasticsPlastics accounted for 54.20% of the cannabis packaging market share in 2025 because of cost efficiency, barrier versatility, and established supply chains. Polypropylene snap lids and PET bottles remain dominant in beverages and tinctures. Biopolymers, however, register the fastest 16.55% CAGR thanks to hemp-based resins and corn-starch PLA recipes that comply with child-resistant torque thresholds. Sana Packaging introduced hemp plastic tubes composed entirely of plant matter, creating petroleum-free value propositions that appeal to eco-minded consumers.

Glass retains a premium niche among medical users who associate it with pharmaceutical purity, while metal tins advance in concentrates for light-protected storage. Paperboard innovation now includes crush-proof pre-roll boxes with hidden locking tabs, resolving earlier structural weaknesses. Research on chitosan-hemp composites demonstrated tensile strength gains of up to 65%, pointing to future bio-based structural carriers that could displace fossil-fuel polymers.

By Cannabis Application:

Medical segment acceleratesRecreational channels led the cannabis packaging market size in 2025 with 62.40% revenue share, bolstered by established adult-use states where branding offers a primary differentiator. Medical adoption rises faster at 17.35% CAGR, driven by hospital procurement and insurance reimbursements that prioritize EU-GMP certified packaging. Aurora Cannabis generated USD 61.3 million from medical lines, surpassing domestic adult-use revenue for the first time, signaling a pivot toward clinical supply.

New therapeutic approvals in epilepsy, chronic pain, and PTSD expand dosage forms from dried flower to orally disintegrating tablets, each requiring distinct moisture-control features. Pharmacies favor blister card presentations that enhance adherence tracking and lot-level recall capability. As more countries reimburse cannabinoid prescriptions, pharmaceutical wholesalers drive volume for tamper-evident tertiary cartons with serialized 2D barcodes, strengthening data integrity across cold chains.

By Product Form:

Concentrates lead innovationEdibles maintained the largest share at 39.10% in 2025 as consumers gravitate toward discrete intake and precise dosing. Brands invest in child-resistant tins with click-lock buttons that complement gummy portion sizes. Concentrates and oils record the fastest 17.60% CAGR, reflecting demand for vape cartridges and live resin dabs. Grove Bags tailored its ExIce pouch to protect frozen rosin, preventing freezer burn and terpene loss while remaining fully water-soluble for zero-waste disposal.

Flower remains a core form, yet automation upgrades now weigh containers automatically to offset jar-to-jar variance, streamlining compliance with net-weight rules. Topicals advance steadily through transdermal patches and nano-emulsion lotions that require multilayer foil-and-film sachets to shield cannabinoids from light and oxygen. This product diversification underpins continuous material and machinery innovation within the cannabis packaging market.

By End User:

Processors invest in automationCultivators and producers held 44.80% of demand, often purchasing bulk liners, harvest bins, and cure jars that safeguard trichome structure during farm-to-process transfer. Processors and manufacturers post the highest 16.08% CAGR as automation helps them scale multi-ingredient SKUs. Paxiom’s turnkey pouch cells integrate upstream weighers and downstream case packers, producing tamper-evident bags at 60-plus packs per minute.

Hefestus automated cone fillers to 1,200 joints per hour, reducing labor costs by 80% while preserving product consistency. Dispensaries focus on shelf impact and QR-code-enabled authentication to aid budtender education, aided by KYND Packaging’s custom foil pouches with high-resolution rotogravure prints. Integration with RFID tracking platforms like StashStock delivers real-time seed-to-sale visibility, limiting diversion and expediting audits.

Geography Analysis

North America Cannabis Packaging Market

North America generated 31.90% of global value in 2025, buoyed by the United States’ state-driven legalization that encourages brand experimentation and premium shelf strategies. Canada streamlined rules in March 2025 to permit transparent windows and scannable QR codes without weakening child-resistant metrics, thereby lowering unit costs for converters already versed in pharmaceutical norms. Mexico’s pharmacy-only sales model creates specialized pack compliance but limits near-term volume until adult-use provisions progress.

Europe Cannabis Packaging Market

Europe is in rapid flux after Germany’s Cannabis Light model won approval, forcing converters to meet EU-GMP credentials and serialized traceability on every carton. The United Kingdom estimates a potential EUR 9.5 billion (USD 11.19 billion) market pending regulatory clarity, and existing medical supply in Italy and the Netherlands sustains demand for blister strips and amber glass bottles. Eastern Europe assesses 11 different legal pathways to comply with UN treaties, gradually converging on standardized icons that could harmonize packaging rules across member states.

APAC Cannabis Packaging Market

Asia-Pacific shows the quickest 16.35% CAGR through 2031, led by Australia’s projected USD 540.6 million cannabis sales that rely heavily on imports packaged to local recycled-content guidelines. Japan’s USD 154 million CBD segment demands ultraclean, tamper-evident bottles that certify zero THC residue. South Korea experiments with medical frameworks that stipulate hermetic blister packs with braille characters, creating niche opportunities for specialized converters. Regional momentum suggests Asia-Pacific will extend its contribution to the cannabis packaging market over the long term.

Regulatory Landscape

Cannabis packaging regulation continues to be centered on child-resistant and tamper-evident requirements, anchored to established safety standards such as the Poison Prevention Packaging Act (16 CFR 1700.15/1700.20) and common child-resistant classifications (for example, ASTM D3475). In the United States, labeling and symbol requirements remain prescriptive, with universal cannabis symbols mandated in markets such as California and Virginia, and measurement and label-format rules referencing national metrology frameworks (for example, Washington state alignment with NIST Handbook 130-related uniform packaging and labeling practices, and Missouri guidance requiring SI units such as grams and milligrams on labels). These rules increase the design and certification bar for closures, labels, and testing documentation across both rigid and flexible formats.

Sustainability and traceability requirements are being added on top of safety. New Yorks cannabis packaging framework includes a minimum post-consumer recycled content requirement for plastic packaging (25% PCR), pushing packaging suppliers toward verified recycled resin supply and requalification of child-resistant systems. In Canada, Health Canada maintains plain packaging and labeling constraints to reduce youth appeal, while still allowing some information-forward elements as rules evolve. California is also tightening operational controls around certain formats, including proposed Department of Cannabis Control requirements for multipack cannabis goods that focus on physical separation and track-and-trace logging, which adds compliance complexity for co-packers and brands using bundled presentations.

Competitive Landscape

The cannabis packaging market remains moderately fragmented, with few companies topping double-digit volume shares. Greenlane Holdings posted 52% sequential revenue growth to USD 4 million in Q3 2024, achieving 75% gross margins through child-resistant accessories and just-in-time distribution. Berry Global recorded 2% organic volume growth in Q1 2025 and redirected capital to its consumer packaging unit, accelerating investments in recycled-content resin for regulated markets.

Strategic alliances are critical. Döhler Ventures invested in Vertosa to enhance beverage infusion, forcing co-packers to adopt linings compatible with nano-emulsions. StashStock’s RFID readers integrate with METRC systems and scan up to 40 tags per second, reducing reconciliation time and contamination risk. Sana Packaging exploits proprietary hemp and ocean-bound plastics to satisfy dual mandates of recyclability and child safety.

Traditional suppliers are entering the space. TricorBraun acquired Veritiv Containers to boost rigid capacity across North America, forecasting synergies for glass jars and PP vials. Patent activity focuses on tamper-evident lidding, cannabinoid-infused rolling substrates, and blockchain authentication, raising intellectual property barriers for new entrants.

Cannabis Packaging Industry Leaders

KushCo (Greenlane Holdings, Inc.)

The BoxMaker, Inc.

Diamond Packaging

N2 Packaging Systems LLC

BrandMyDispo

- *Disclaimer: Major Players sorted in no particular order

Cannabis Packaging Market Companies Covered in this Report

- Greenlane Holdings Inc. (KushCo)

- N2 Packaging Systems LLC

- Dymapak / Quark Distribution

- Diamond Packaging

- Green Rush Packaging

- Berlin Packaging

- Berry Global Inc.

- Grove Bags

- Contempo Specialty Packaging

- Elevate Packaging Inc.

- The BoxMaker Inc.

- Cannaline Packaging Solutions

- JL Clark

- Automating Cannabis Packaging Equipment

- BrandMyDispo

- THC Label Solutions

- PaperTube Co.

- Paxiom Group

- LeafyPack

- KindPack

Market Opportunities and Future Outlook

Near-term opportunity sits at the intersection of compliance and circularity, where brands need child-resistant packaging that can also meet tightening recyclability and producer-responsibility requirements. The European Unions Packaging and Packaging Waste Regulation (PPWR), which entered into force in February 2025, sets a recyclability direction through 2030 and challenges multi-layer flexible laminates commonly used to achieve odor and moisture barriers in cannabis. That shift creates opportunities for mono-material redesigns, particularly polyolefin structures, along with suppliers that can validate performance and compliance on simplified material stacks while maintaining required warning panels, symbols, and tamper evidence.

Operational programs also point to practical ways to scale circular packaging in regulated markets. In Oregon, P3 Distributing established an operational recycling facility in Portland to process polypropylene cannabis containers into feedstock for downstream manufacturing, and it highlighted that material standardization, such as polypropylene labels on polypropylene containers, reduces separation steps and improves direct granulation economics. Similar hub-and-spoke collection and processing models, combined with compliant label and adhesive selections, create space for converters, label suppliers, and distributors offering closed-loop services to multi-site operators managing high SKU churn and frequent rule updates. On the compliance technology side, continued rollout of track-and-trace and scannable information elements, including QR-code-enabled packs in regulated markets, supports demand for packaging that integrates authentication, lot-level traceability, and audit-ready labeling without undermining child resistance.

Recent Industry Developments in Cannabis Packaging Market

- June 2026: P3 Distributing implemented an onsite alcohol distillation system at its Portland, Oregon cannabis packaging recycling operations to recover isopropyl alcohol used in label-removal processes. The capability reduces solvent consumption and supports higher-throughput reprocessing of post-consumer polypropylene containers into usable feedstock. It strengthens the business case for circular packaging programs that rely on efficient cleaning and de-labeling steps.

- May 2025: SupplyOne completed the acquisition of The BoxMaker, expanding its digitally printed custom corrugated box and label capabilities in the US Northwest. The move increases access to short-run, high-variation packaging workflows that fit cannabis SKU churn and frequent compliance-driven artwork changes. It also broadens capacity for secondary packaging and ship-ready solutions serving regulated operators.

- May 2024: Greenlane Holdings reported full-year 2024 results reflecting continued emphasis on ancillary cannabis products and distribution-led strategies, including packaging-related accessories and compliant product presentation needs. The update underscored the importance of inventory and distribution execution in a market shaped by evolving state-by-state packaging rules. For packaging suppliers, it reinforces demand for dependable fulfillment and compliant assortment breadth for multi-jurisdiction customers.

Cannabis Packaging Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers packaging formats and materials used to store, protect, and label regulated cannabis products so they can be safely sold through legal channels. It includes packs designed for compliance needs like child resistance, tamper evidence, and required on-pack information.

Scope exclusions: We exclude unregulated, homegrown packaging use and any spend that is purely on non-packaging items such as in-store fixtures or generic promotional merchandise.

Segments Covered in This Report

- By Type

- Rigid Packaging

- Flexible Packaging

- By Packaging Material

- Plastics

- Glass

- Metal

- Paper and Paperboard

- Biopolymer and Other Materials

- By Cannabis Application

- Medical

- Recreational

- By Product Form

- Flower

- Edibles

- Concentrates and Oils

- Topicals and Others

- By End User

- Cultivators and Producers

- Processors / Manufacturers

- Dispensaries and Retail Chains

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- Spain

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- Australia

- South Korea

- India

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- UAE

- Israel

- Turkey

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the guardrails for what compliant cannabis packaging looks like by geography, and to map how demand forms across medical and adult use programs. We referenced public sources such as government cannabis regulatory portals, state or provincial rulebooks, customs and trade statistics for packaging materials, and environment agency guidance on packaging waste and recyclability.

To ground the numbers, we also reviewed company filings and investor presentations from packaging suppliers and converters, along with association publications and reputable press that track packaging trends like child-resistant closures and labeling rules. In parallel, we used paid subscriptions for company financials and intelligence, patent databases, and shipment-level import or export records where available, which helped cross-check product claims and trade flows. The sources listed here are illustrative, and many additional public documents and datasets were also used for data collection and clarification.

Primary Interviews and Surveys

Primary work focused on validating which pack types are actually used for flower, edibles, concentrates, and topicals, and how quickly formats are changing due to compliance and sustainability needs. We spoke with a mix of packaging suppliers, converters, cannabis brand owners, and channel participants. Coverage was balanced across APAC, EMEA, and the Americas so regional rule differences informed the assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 17% | APAC: 46% |

| Mid tier: 46% | Functional/Unit leaders: 25% | EMEA: 35% |

| Smaller Players: 18% | Managers: 58% | Americas: 19% |

Market-Sizing & Forecasting

Market sizing is built using a top-down and bottom-up approach. The starting point is the legal cannabis demand pool by region and application, which is then translated into packaging demand using typical pack configurations and replacement rates. Once the pack count is reconstructed, we apply pricing and mix so the model reflects differences between rigid and flexible formats, and between materials such as plastic, glass, metal, and paperboard.

Key inputs used in the model include the pace of legalization and store rollout, the share split between medical and recreational programs, average packs per unit sold for flower and edibles, adoption of child-resistant and tamper-evident features, and material substitution trends linked to sustainability rules. For cross-checking, we corroborate the totals with selective bottom-up approximations, such as sampled supplier revenue splits, channel checks on common pack formats, and indicative ASP by material and closure type. Where bottom-up coverage is incomplete in smaller countries, gaps are handled by using proxy pack mix from similar regulatory markets, then adjusting with interview feedback.

Forecasting uses scenario analysis supported by trend-based smoothing on key drivers. The timing of policy implementation and compliance upgrades can shift packaging demand faster than normal packaging cycles. The final forward view is reviewed against expected changes in regulations, product form mix, and material preferences shared by industry respondents.

Data Validation & Update Cycle

Validation is done by checking model outputs against independent signals, such as regulatory program counts, the direction of material demand, and supplier commentary on capacity and order patterns. If an outlier shows up, the assumption is traced back to the specific driver, and then reviewed again before the estimate is finalized.

A multi-step analyst review ensures calculations, unit conversions, and regional rollups stay consistent. When major events occur, such as a new legalization wave, a sharp regulatory packaging change, or a material price shock, the team triggers re-checks and may re-contact respondents to confirm what is changing. Reports are refreshed annually, with interim updates for material events, and a final pre-delivery pass is completed so clients receive the latest view.

Mordor Intelligence's Cannabis Packaging Market Size Measured Against Other Published Estimates

Published market sizes for cannabis packaging can look far apart because the market boundary is not always set the same way, and because time periods differ across studies. Differences also come from whether compliance features are treated as part of packaging value, and how local currency pricing is converted into USD.

By tracking pack-format mix, compliance feature adoption, and local currency timing, Mordor Intelligence keeps the cannabis packaging total tied to legal sales volumes and realistic pricing steps. This reduces inflation from loosely defined add-on services or aggressive unit assumptions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.29 B (2026) | |

| Global Consultancy A | USD 6.48 B (2025) | Uses a much larger starting base that appears to reflect broader packaging value capture across adjacent packaging activities and wider channel coverage, and it also applies a longer forecast window where mix and pricing upgrades can compound faster. |

| Industry Research Group B | USD 2.24 B (2023) | Anchors the market on an earlier year and applies a higher growth rate, which can shift the implied current-year value depending on how legalization timing and product-form mix are assumed to move year to year. |

The spread across the table mainly comes from scope boundaries, base-year choice, and how pack counts and pricing are linked to regulated demand. Our approach stays practical by tying the model to observable legalization signals, common packaging configurations by product form, and interview-validated price and mix assumptions that can be rechecked when conditions change.

Key Questions Answered in the Report

What is the current size of the cannabis packaging market?

The cannabis packaging market size reached USD 2.29 billion in 2026 and is forecast to hit USD 4.65 billion by 2031, translating to a 15.22% CAGR.

Which packaging format grows fastest in cannabis applications?

Flexible packaging is expanding at a 17.05% CAGR through 2031 because of automation compatibility and reduced material waste.

Why are biopolymers gaining traction in cannabis packaging?

Why are biopolymers gaining traction in cannabis packaging?

Which geographic region will show the highest growth?

Asia-Pacific is projected to log a 16.35% CAGR to 2031, driven by reforms in Australia, Japan, and emerging South-East Asian markets.

What regulatory trend most influences future cannabis packs?

Global moves toward mandatory recycled content while retaining child-resistant standards place dual pressure on material innovation and compliance engineering.

Page last updated on: