Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.19 Billion |

| Market Size (2026) | USD 1.25 Billion |

| Market Size (2030) | USD 1.62 Billion |

| Growth Rate (2026 - 2031) | 5.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Ophthalmic Devices Market Analysis by Mordor Intelligence

The Brazil Ophthalmic Devices Market size is expected to increase from USD 1.19 billion in 2025 to USD 1.25 billion in 2026 and reach USD 1.62 billion by 2030, growing at a CAGR of 5.35% over 2026-2030.

An aging population, rising diabetes prevalence, and fast-track regulatory pathways are expanding procedure volumes and shortening device-launch lags, while currency volatility continues to inflate import costs. Vision-care products dominate revenue today, yet diagnostic platforms for diabetic retinopathy screening and swept-source OCT are expanding faster as public tele-ophthalmology pilots scale and private clinics modernize their imaging fleets. Competitive intensity is moderate; five multinational suppliers account for about 58% of sales, whereas dozens of domestic distributors still win public tenders in secondary cities. Private equity capital is accelerating the migration of cataract and refractive surgeries from hospitals to ambulatory surgery centers, improving equipment utilization and boosting premium-IOL uptake.

Key Report Takeaways

- By device type, vision care devices captured 59.77% of Brazil ophthalmic devices market share in 2025, while diagnostic and monitoring devices are projected to post the highest 8.52% CAGR through 2031.

- By disease indication, cataract devices accounted for 37.16% of 2025 revenue; diabetic retinopathy platforms are forecast to expand fastest at a 7.78% CAGR, driven by mandatory screening mandates.

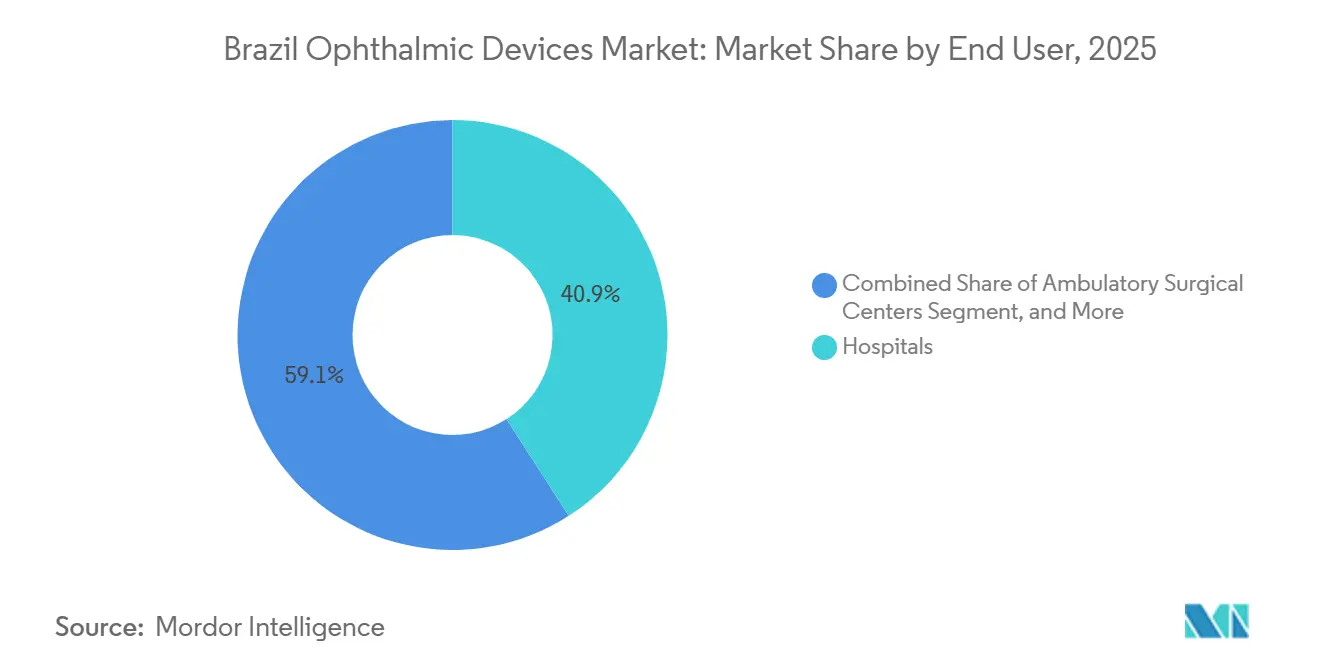

- By end user, hospitals accounted for 40.89% of end-user spending in 2025, yet ambulatory surgery centers are set to grow at a 10.49% CAGR as private insurers reimburse outpatient cataract and refractive procedures.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Ophthalmic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diabetic-retinopathy prevalence and demand for OCT | +0.9% | Nationwide; strongest in southeast | Medium term (2-4 years) |

| Femtosecond-laser adoption in private cataract suites | +0.7% | São Paulo, Rio de Janeiro, Brasília | Long term (≥ 4 years) |

| “Saúde Visual” mobile-screening expansion | +0.5% | North and Northeast | Short term (≤ 2 years) |

| Rising private-insurance coverage for premium IOLs | +0.6% | Southeast economic corridor | Medium term (2-4 years) |

| Expansion of tele-ophthalmology networks in remote & Amazon regions | +0.4% | Amazon basin and remote interior states | Short term (≤ 2 years) |

| Rising screen time in youth fueling myopia & demand for vision correction | +0.3% | Urban centers nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population Fuelling Cataract and AMD Procedure Volumes

More than 31 million Brazilians were aged 60 or older in 2021, and this cohort is projected to top 40 million by 2030.[1]Instituto Brasileiro de Geografia e Estatística, “Population Projections 2021-2030,” ibge.gov.br Cataract surgeries climbed to 1.18 million in 2024 after a Ministry of Health backlog-reduction fund injected R$1.2 billion, yet volumes remain below the 3,000-per-million rate the WHO recommends. Premium IOLs already account for 35% of private implants, and femtosecond laser–assisted cataract surgery accounts for 25% of São Paulo ASC cases, signaling strong upside for premium platforms. Anti-VEGF injections for AMD exceeded 1.8 million in 2025, though public facilities still rely on off-label bevacizumab due to cost differentials of up to 90%. ANVISA’s 2024 post-market-surveillance rule now covers toric and EDOF lenses, raising compliance costs but improving safety tracking.

Rising Diabetes Prevalence Driving Retinal Diagnostics and Laser Therapy

Diabetes affects 10.2% of Brazilian adults, equating to 16.6 million people, and 36.3% carry some level of diabetic retinopathy.[2]International Diabetes Federation, “IDF Diabetes Atlas 10th Ed.,” diabetesatlas.org Only 21% of diabetics were screened in 2019, leaving nearly 4.5 million undiagnosed cases that now enter AI-enabled triage streams. Phelcom’s smartphone fundus camera, cleared by ANVISA in 2023, processes images in 60 seconds and reaches 94% sensitivity, slashing referral backlogs in 120 municipalities. Private diagnostic chains installed 18% more swept-source OCT units in 2024, detecting macular edema 6 months earlier than time-domain systems and spurring demand for anti-VEGF treatment. Regulatory updates for software-as-medical-device tools require AI vendors to demonstrate AUC scores above 0.92 on Brazilian datasets, yet fast-track filings still finalize in under 180 days.

Technological Advances Accelerating Adoption

Device-registration lags have dropped from a year to roughly six months as ANVISA prioritizes digital and AI submissions.[3]Agência Nacional de Vigilância Sanitária, “Medical Device Registration Performance Report 2023,” gov.br/anvisa Alcon’s 2025 acquisition of LENSAR introduced the ALLY femtosecond platform with real-time wavefront guidance, immediately challenging Carl Zeiss’s VisuMax 800 in premium cataract suites. Small-incision lenticule extraction now represents 18% of Brazil’s refractive surgeries, up from 9% in 2023, and offers faster visual recovery than LASIK. Swept-source OCT and ultra-widefield cameras extend diagnostic accuracy into the choroid and the retinal periphery, enabling earlier intervention for AMD and DR. Local assembly in the Manaus Free-Trade Zone trims landed costs up to 20% for select lasers and OCT units, cushioning BRL depreciation.

SUS-Backed Tele-Ophthalmology Pilots Boosting Portable Device Uptake

The Ministry of Health funded 2,500 TeleOftalmo sites with R$47 million in 2024, targeting municipalities where ophthalmologist density sits below 1 per 50,000 residents. Portable cameras weighing less than 2 kg allow health workers to screen 40 patients per day and sync images to cloud databases that retinal specialists review within 48 hours. Screening coverage in pilot states jumped from 12% in 2018 to 35% in 2024, cutting late-stage referrals by 28%. Mobile surgical buses performed 12,400 cataract procedures in rural Bahia and Ceará last year, demonstrating demand elasticity when access barriers are removed. ANVISA now mandates AES-256 encryption for imaging and domestic data storage, raising infrastructure spending but protecting patient privacy.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of fellowship-trained ophthalmic surgeons | –0.8% | North and Northeast public hospitals | Long term (≥ 4 years) |

| High import tariffs and BRL volatility | –0.7% | Nationwide | Short term (≤ 2 years) |

| Supply-chain delays for high-end diagnostic capital equipment | –0.5% | Ports of Santos, Rio, and inland routes | Medium term (2-4 years) |

| Low SUS reimbursement rates for new surgical technologies | –0.6% | Nationwide public facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

BRL Currency Volatility Inflating Import Prices

The real lost 14% against the dollar between 2023 and 2024, lifting landed prices for OCT scanners, lasers, and microscopes 12-18%. SUS cataract reimbursements have stayed flat at R$580 since 2019, squeezing hospital margins and delaying equipment replacements by up to nine months. Private ASCs increasingly opt for five-year leasing in local currency, while wholesalers without hedging saw gross-margin erosion of 300 basis points in 2024. Manaus tax exemptions offset only a small slice of exposure, as just 15% of ophthalmic SKUs are locally assembled. Retail chains passed price hikes selectively, pushing premium progressive lenses up 8-10% while keeping entry-level SKUs flat to protect volume.

Ophthalmologist Shortage Outside Southeast Limits Device Utilization

Only 8.96 ophthalmologists serve every 100,000 Brazilians, but 60% practice in São Paulo, Rio de Janeiro, and Minas Gerais. Amazonas reports just 3.6 specialists per 100,000, leaving OCT scanners idle 60% of clinic hours. Residency slots expanded 12% between 2020 and 2024, yet 70% of graduates remain in the wealthier Southeast. Tele-ophthalmology solves screening gaps but cannot replace slit-lamp or surgical expertise, so advanced devices still cluster in urban hubs. The national council now proposes linking future SUS equipment tenders to minimum ophthalmologist-density thresholds, a policy that could slow procurement in underserved states.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Diagnostic Platforms Outpace Vision Care Growth

Diagnostic and monitoring devices accounted for a modest base in 2025 but are projected to outpace every other category at an 8.52% CAGR, propelled by nationwide diabetic retinopathy mandates and AI-ready OCT systems. Vision-care goods nevertheless retained 59.77% of 2025 revenue, reflecting the country’s 71,226 optical outlets and a consumer tilt toward monthly silicone-hydrogel lenses. Contact-lens leaders Johnson & Johnson Vision and CooperVision exploit pharmacy networks to cover urban and peri-urban zones, while EssilorLuxottica leverages two domestic factories to buffer exchange-rate shocks on frames and Rx lenses.

Swept-source OCT scanners from Heidelberg Engineering and Nidek captured 60% of new premium installs last year, offering non-dye angiography that trims imaging sessions from 45 minutes to 12. Portable fundus cameras priced below USD 5,000 now feature in SUS bids across 120 municipalities, supporting 340,000 retinal images annually. Surgical devices are set to post a solid 7.9% CAGR as femtosecond laser–assisted cataract surgery penetration climbs beyond 10% nationally by 2031. The Brazil ophthalmic devices market share held by surgical consoles is likely to rise by two points by the end of the decade as private insurers reimburse outpatient cataract bundles that include premium IOLs.

By Disease Indication: Retinopathy Narrows Cataract’s Lead

Cataract systems accounted for 37.16% of revenue in 2025, driven by 1.18 million SUS procedures and 664,000 private surgeries. Still, diabetic retinopathy solutions will log the quickest 7.78% CAGR through 2031 as screening coverage broadens under federal mandates. Glaucoma devices hold a mid-teens slice, buoyed by 12% MIGS penetration in private ASCs, whereas AMD therapeutics lean heavily on bevacizumab in public hospitals but showcase growing uptake of port-delivery implants in affluent metros.

Cataract dominance stems from demographic pressure; Brazil adds 650,000 seniors annually, and premium IOL penetration in private centers already surpasses 35%. Conversely, one in three diabetics has retinal disease, yet fewer than a quarter receive annual imaging. AI-triage platforms flagging referable cases at 94% sensitivity shorten waitlists but also expose capacity gaps in laser therapy and anti-VEGF supply. As reimbursement codes for OCT angiography and portable ultrasound devices mature, retinopathy could overtake glaucoma spending by 2029.

By End-User: ASCs Capture Surgical Volume Shift

Hospitals handled 40.89% of the 2025 spend due to SUS cataract subsidies, but Brazil's ophthalmic devices market growth among ambulatory surgery centers is forecast at 10.49% CAGR, the fastest of any channel. Consolidators such as TecLASER For Eyes and Pátria-backed Oftalmax aggregate high-volume cataract and refractive caseloads, lifting equipment utilization above 90%. Specialty ophthalmic clinics held roughly one-third of the market share, leveraging retina and refractive niches to justify ultra-widefield cameras and SMILE lasers.

ASC economics are compelling: outpatient cataract bundles cost 30-40% less than hospital tariffs and allow same-day discharge, a feature prized by private insurers seeking cost containment. Public hospitals, by contrast, defer device upgrades amid frozen reimbursements and BRL headwinds, granting ASCs a technology lead in premium IOLs and femtosecond lasers. Optical retail chains remain important for vision-care turnover, and their 8% outlet expansion in 2024 underscores latent consumer demand even in a tight economy.

Geography Analysis

The Southeast mirrors its concentration of 60% of all ophthalmologists and 70% of private ASCs. São Paulo alone hosts more femtosecond lasers than the entire North and Northeast combined, a reality that speeds adoption curves for premium IOLs and SMILE surgery. High private-insurance penetration, 44% of residents, also bolsters early uptake of AI diagnostics.

The Center-West is driven by Brasília’s affluent insurance base and Goiás clinics acquiring swept-source OCT units in 2024. The North mobile surgical buses and battery-powered imaging devices bridge Amazonian river networks to reach remote populations. Strict data-localization rules compel cloud-service investments in regional hubs such as Manaus and Belém, raising overhead but safeguarding privacy.

Competitive Landscape

The Brazilian ophthalmic devices market has a moderate concentration score. Alcon’s USD 356 million purchase of LENSAR added the ALLY adaptive femtosecond platform, expected to command 40% of FLACS procedures by 2027. Carl Zeiss Meditec leverages its VisuMax 800 and AI IOL Calculator to lock in refractive and cataract surgeons, while Bausch + Lomb promotes the Stellaris Elite phaco system in SUS tenders. Johnson & Johnson Vision launched the TECNIS Odyssey in 2025, raising the premium-IOL stakes, and EssilorLuxottica integrates frames through 1,450 franchises and two factories that blunt currency swings.

Domestic disrupter Phelcom undercuts tabletop fundus units by 80%, placing 150 Eyer cameras in public clinics and courting export markets across Latin America. Glaukos and Alcon jostle for MIGS leadership, yet adoption outside private ASCs is thin until SUS updates its reimbursement list. Private equity fuels consolidation: Pátria Investimentos bought a 40% stake in Oftalmax in 2024 and targets 25% EBITDA by maximizing theatre throughput. Overall, the competitive field balances scale advantages with nimble regional distributors that supply 3,800 municipalities lacking major-brand service coverage.

Brazil Ophthalmic Devices Industry Leaders

Alcon Inc.

Johnson & Johnson Vision Care, Inc.

Carl Zeiss Meditec AG

Bausch + Lomb Corp.a SA

EssilorLuxottica SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BVI Medical received 510(k) clearance from the U.S. FDA for the Leos Laser Endoscopy Ophthalmic System, paving the way for Brazilian registration and a future glaucoma-surgery portfolio.

- February 2025: The Brazilian Ministry of Health standardized telehealth procedures, including tele-ophthalmology, within the SUS system to improve care quality and expand access in remote areas

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Brazil's ophthalmic devices market as the total annual revenue generated within the country from new diagnostic and monitoring systems, surgical equipment, and vision-care products that are formally approved by ANVISA for human eye-health use. This spans optical coherence tomography scanners, fundus cameras, phaco consoles, femtosecond lasers, intra-ocular lenses, spectacles, and contact lenses that reach hospitals, specialty clinics, ambulatory surgery centers, and retail channels.

Scope exclusion: refurbished units and unregulated cosmetic lenses are not counted within the baseline.

Segmentation Overview

- By Device Type

- Diagnostic & Monitoring Devices

- OCT Scanners

- Fundus & Retinal Cameras

- Autorefractors & Keratometers

- Corneal Topography Systems

- Ultrasound Imaging Systems

- Perimeters & Tonometers

- Other Diagnostic & Monitoring Devices

- Surgical Devices

- Cataract Surgical Devices

- Vitreoretinal Surgical Devices

- Refreactive Surgical Devices

- Glaucoma Surgical Devices

- Other Surgical Devices

- Vision Care Devices

- Spectacles Frames & Lenses

- Contact Lenses

- Diagnostic & Monitoring Devices

- By Disease Indication

- Cataract

- Glaucoma

- Diabetic Retinopathy

- Other Disease Indications

- By End-user

- Hospitals

- Specialty Ophthalmic Clinics

- Ambulatory Surgery Centers (ASCs)

- Other End-users

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed cataract surgeons, biomedical engineers at private hospitals, procurement heads at three regional purchasing groups, and executives of domestic distributors across São Paulo, Recife, and Porto Alegre. These conversations validated utilization rates, average selling prices, and replacement cycles, and they refined our assumptions on public versus private demand pools.

Desk Research

We opened the model with public datasets from Brazil's Ministry of Health (DATASUS discharge records, SUS procedure tariffs) and IBGE population projections, which tell us how many potential patients exist and how many surgeries are financed each year. Trade associations such as the Brazilian Council of Ophthalmology, customs statistics on HS codes 9001 and 9018, ANVISA device registration filings, and peer-reviewed papers in Arquivos Brasileiros de Oftalmologia offered unit flow, import value, and prevalence clues.

To price devices, we referenced financial disclosures and investor decks of listed manufacturers, plus press releases that reveal launch pricing and tender awards, while paid databases like D&B Hoovers and Dow Jones Factiva helped verify company revenues and shipment directionality. The sources above illustrate the mix used; many additional publications and datasets were reviewed to cross-check gaps and anomalies.

Market-Sizing & Forecasting

The top-down build starts with cataract, refractive, glaucoma, and retina procedure volumes, which are then multiplied by device penetration and replacement factors gleaned from field interviews. Results are corroborated through selective bottom-up roll-ups of supplier revenues and channel checks to fine-tune totals. Key variables include aging population growth, diabetic retinopathy prevalence, OCT scanner installed base, private insurance enrollment, and BRL-USD exchange shifts. A multivariate regression with three lags models how these drivers move device demand, and an ARIMA overlay projects near-term seasonality. Where supplier data are partial, gaps are bridged by weighted averages of ASPs reported by adjacent vendors and validated by import statistics.

Data Validation & Update Cycle

Outputs pass a two-step analyst peer review, followed by variance scans against external shipment data and hospital procurement notices. Any deviation above three percentage points triggers re-contact of industry experts before sign-off.

Reports refresh every twelve months, with interim updates issued when ANVISA policy or macro shocks materially alter the outlook.

Why Mordor's Brazil Ophthalmic Devices Baseline Commands Reliability

Published estimates often diverge because firms choose different device mixes, price bases, and update rhythms.

Understanding those levers helps readers reconcile the spread.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.19 B (2025) | Mordor Intelligence | - |

| USD 486 M (2024) | Regional Consultancy A | Excludes vision-care products and applies ex-factory prices only |

| USD 764 M (2024) | Global Consultancy B | Omits femtosecond lasers, converts at Q1-2024 BRL spot, refreshes biennially |

The comparison shows that once scope and pricing bases are aligned, Mordor's disciplined mix of transparent variables, annual refresh, and multi-source validation offers decision-makers the most dependable benchmark for Brazil's eye-care equipment opportunity.

Key Questions Answered in the Report

What is the projected value of the Brazil ophthalmic devices market in 2031?

The Brazil ophthalmic devices market size is projected to reach USD 1.62 billion by 2031.

W hich device category will grow fastest through 2031?

Diagnostic and monitoring devices are expected to post the highest CAGR of 8.52% in diabetic retinopathy screening.

Why are ambulatory surgery centers gaining share?

Private insurers reimburse outpatient cataract and refractive procedures at lower cost, and ASCs deliver shorter wait times plus access to premium IOLs.

How is tele-ophthalmology influencing regional demand?

TeleOftalmo hubs and portable fundus cameras raised screening coverage to 35% in pilot states, spurring purchases of low-cost diagnostic kits in underserved areas.

What major regulatory change speeds device launches?

ANVISA’s 2025 fast-track pathway cut approval timelines to 180 days, allowing AI diagnostics and premium IOLs to reach surgeons six months after global release.

Page last updated on: