Brazil Home Loan Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 62.99 Billion |

| Market Size (2031) | USD 104.81 Billion |

| Growth Rate (2026 - 2031) | 10.72% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Home Loan Market Analysis by Mordor Intelligence

The Brazil home loan market size is USD 62.99 billion in 2026, and it is projected to reach USD 104.81 billion by 2031 at a 10.72% CAGR during the forecast period (2026-2031). Demand is reinforced by urbanization and middle-income expansion, with 87% of residents living in cities and household formation continuing to add new buyers. Policy support through Minha Casa, Minha Vida, and updated SBPE rules expands eligibility and keeps originations resilient across rate cycles. Open Finance and Pix adoption compress underwriting timelines by enabling cash-flow-based credit assessment and instant data sharing[1]IBGE, “2022 Census, 87% of the Brazilian population lives in urban areas,” IBGE News Agency, ibge.gov.br. Competitive strategies concentrate on digital onboarding, AI-driven decisioning, and bank–fintech partnerships that link origination speed with stable funding.

Key Report Takeaways

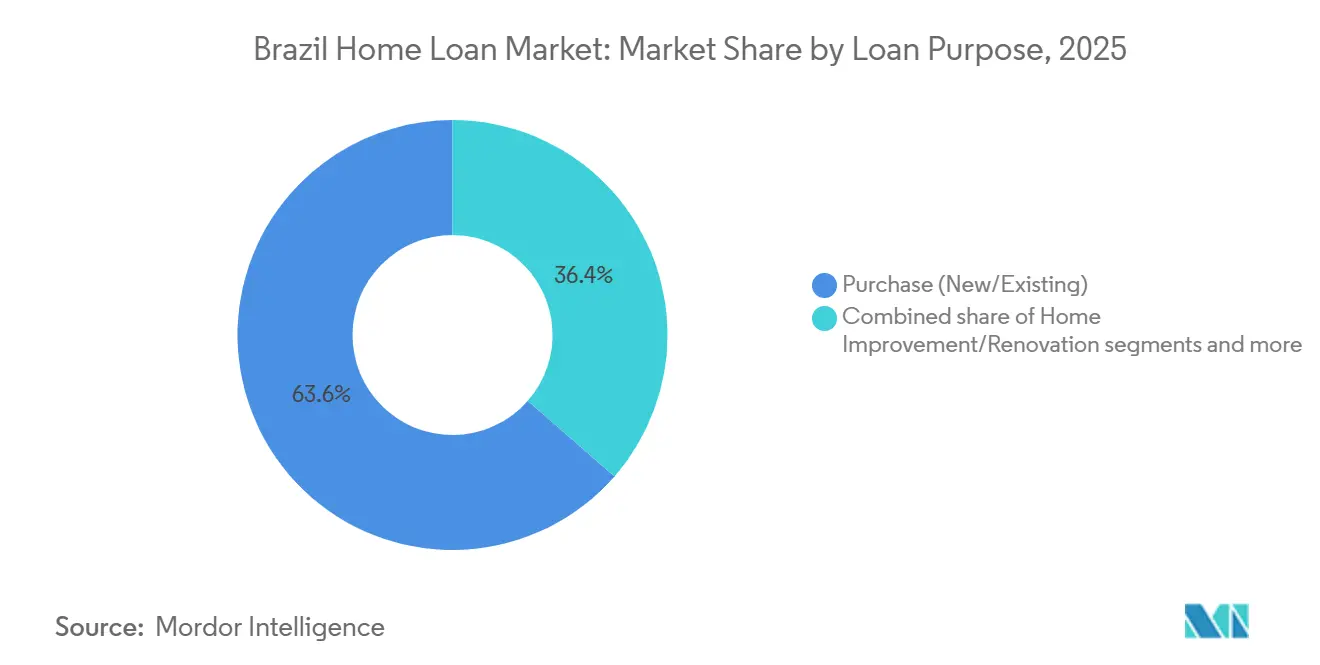

- By loan purpose, Purchase (New or Existing) led the Brazil home loan market with a 63.57% share in 2025, while Home Improvement and Renovation is projected to grow at a 10.04% CAGR through 2031.

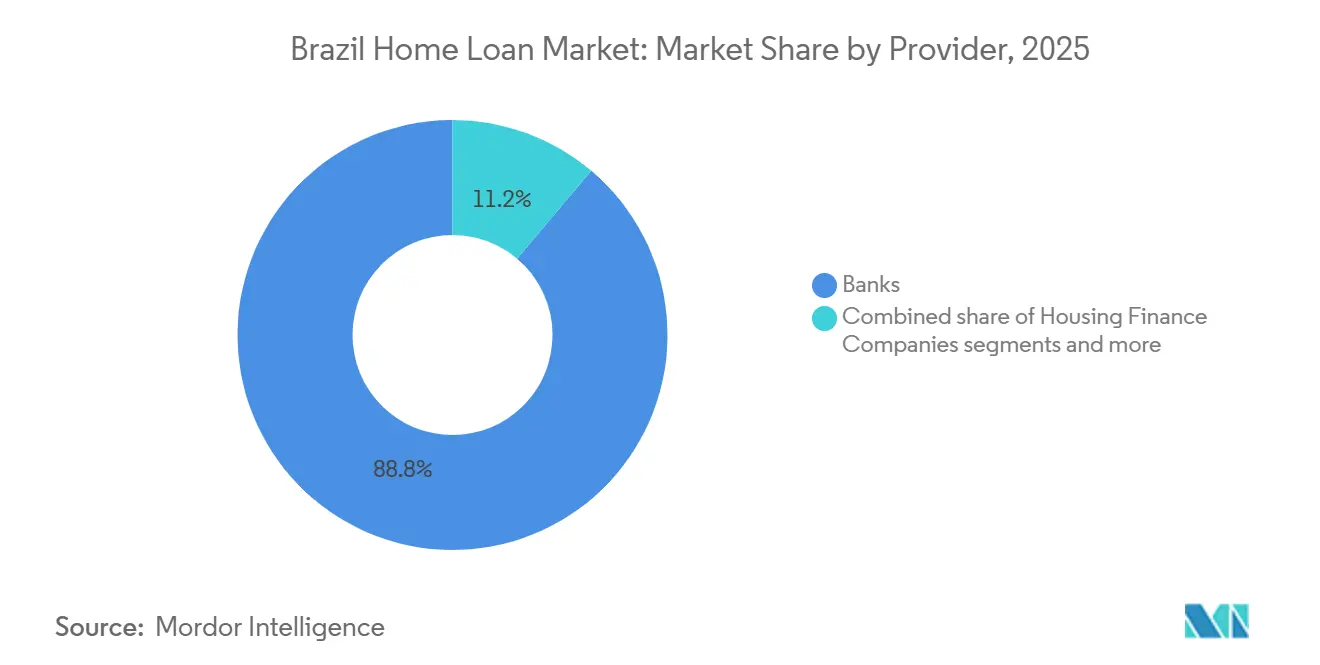

- By provider, Banks dominated the Brazil home loan market with an 88.83% share in 2025, while Others are forecast to expand at a 12.82% CAGR during 2026 - 2031.

- By interest rates, Floating Interest Rates accounted for 93.25% of the Brazil home loan market in 2025, while Fixed Interest Rates are expected to advance at a 14.57% CAGR through 2031.

- By loan tenure, terms greater than 20 Years held a 50.04% share of the Brazil home loan market in 2025, while 11 to 20 Years are set to grow at a 13.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of Brazil. The home loan market share in our global report expresses these relative weights.

Brazil Home Loan Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Housing Support Programs | +1.8% | National, with enhanced subsidies in the North and Northeast regions | Short term (≤ 2 years) |

| Urbanization and Middle-Class Expansion | +2.1% | National core, fastest growth in medium-sized cities | Medium term (2-4 years) |

| Macroeconomic Growth and Rising Disposable Income | +1.4% | National, concentrated in Southeast | Medium term (2-4 years) |

| Fintech-Led Credit Accessibility | +1.6% | National urban centers, strongest in São Paulo, Rio, and Brasília | Short term (≤ 2 years) |

| Interest Rate Environment and Mortgage Uptake | +2.3% | National | Long term (≥ 4 years) |

| Technological Advancements in Mortgage Lending | +1.5% | National urban, digital-first platforms in metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Housing Support Programs

Minha Casa, Minha Vida expansions increase affordability through income-calibrated subsidies and subsidized coupon bands, which stabilize purchase decisions for eligible families across income brackets. The program’s 2025 adjustments add a new income tier and update value ceilings, which bring middle-income borrowers into regulated pricing without removing priority from lower-income cohorts. Location criteria that prioritize transit proximity and service access reduce hidden costs for households and improve the livability of financed units. FGTS-backed flows and Caixa’s execution capacity shorten the time from project launch to origination, which supports steady disbursement during tight monetary conditions[2]CAIXA, “CAIXA News and Releases,” CAIXA, caixa.gov.br. As program visibility improves, developers align pipelines with the updated thresholds, reinforcing purchase-led volumes within the Brazil home loan market. These adjustments contribute a measurable positive effect on the long-run adoption of formal housing credit among first-time and returning buyers.

Urbanization and Middle-Class Expansion

Urbanization stands at 87% of the population and supports deeper mortgage penetration through higher formal employment shares and service sector concentration. Household formation rises through the mid-2020s and creates sustained demand for purchases and targeted renovations in both core and secondary cities. Income levels vary across regions, which yields larger average loan sizes in the Southeast and volume-led growth in regions with higher subsidy intensity. Labor market improvements in 2025 align with higher formal earnings and help more borrowers qualify under SBPE and FGTS criteria. Growing digital adoption makes mid-tenure and renovation products accessible to younger cohorts who favor predictable budgeting. These dynamics collectively expand the addressable base for the Brazil home loan market as migration shifts support sustained urban absorption.

Macroeconomic Growth and Rising Disposable Income

Macroeconomic growth in 2026 remains steady while fiscal consolidation aims to improve risk premia and reduce funding spreads across banking channels[3]OECD, “Economic Outlook, Brazil Chapter,” OECD, oecd.org. Real wages and formal employment gains in 2025 improved household cash flows, which support incremental credit capacity within underwriting criteria. Regional income dispersion channels higher-ticket financing to large metros while program support keeps momentum in other areas. Banks and non-banks use cash-flow analytics and collateral-backed structures to serve borrowers without traditional paycheck documentation. As policy anchors take hold, lenders scale originations through SBPE and FGTS frameworks with measured risk controls. These conditions reinforce a gradual and broad-based expansion path for the Brazil home loan market through the forecast period.

Fintech-Led Credit Accessibility

Open Finance and Pix deliver consented, real-time data that lenders use to score applicants on observed cash flows, which increases approval rates for self-employed and gig-economy workers. Instant payment transactions supply high-frequency signals on bill payment and income variability that complement traditional bureau files. Leading private institutions integrate these datasets into their superapps to produce pre-approved offers that reduce friction and accelerate decisions. Regulatory updates define roles for payment initiation and API standards, which enable fintechs to operate adjacent to banks in origination while relying on bank funding[4]Itaú Unibanco, “Institutional Presentation,” Itaú Unibanco, itau.com.br. Caixa’s Banking-as-a-Service model illustrates this division of labor as partners handle front-end experiences and Caixa provides balance sheet and compliance infrastructure. These capabilities widen access and shorten time to cash, which is supportive for the Brazil home loan market in dense urban corridors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated and Volatile Interest Rate Environment | -2.0% | National | Short term (≤ 2 years) |

| Macroeconomic Uncertainty and Consumer Confidence Risks | -0.9% | National, acute pressure in the Northeast states | Medium term (2-4 years) |

| Regulatory Constraints and Bureaucratic Bottlenecks | -0.7% | National, pronounced in smaller municipalities | Long term (≥ 4 years) |

| High Household Indebtedness Limiting Borrowing Capacity | -1.2% | National, the highest debt-service in urban Southeast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Elevated and Volatile Interest Rate Environment

The policy rate plateaued at a restrictive level in late 2025 and filtered into higher lending coupons for non-subsidized mortgages, which lifted monthly installments and reduced affordability. Banks transmitted rate changes to SBPE loans while FGTS-linked lines remained partially insulated by subsidized pricing rules. Higher coupons led developers to delay some greenfield projects, which shifted borrower focus toward ready inventory and renovation upgrades. As inflation indicators move closer to the target band, lenders anticipate scope for coupon moderation that would reactivate deferred demand. Borrowers respond to volatility by favoring predictable installment structures in the mid-tenure and fixed-rate segments where available. This restraint is most pronounced in the short term and gradually fades with policy normalization and improved price dynamics.

Macroeconomic Uncertainty and Consumer Confidence Risks

Economic uncertainty dampens housing intent when households prioritize liquidity buffers over long-duration obligations. Confidence-sensitive cohorts slow large-ticket decisions until they see sustained stabilization in employment, inflation, and borrowing costs. In regions with lower average incomes, the same uncertainty generates larger swings in intent and approval, which yield uneven origination patterns. Lenders adjust risk appetite and pricing to keep portfolios resilient without closing the credit window for qualified applicants. Policy signals that clarify program funding and capital rules improve visibility for developers and banks, which helps stabilize forward pipelines. The net effect moderates over the medium term as macro indicators align with targets and underwriting precision improves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Loan Purpose: Renovation Demand Propels Niche Growth

"Purchase, New or Existing" leads the Brazil home loan market with a 63.57% share in 2025, driven by household formations and improved affordability under updated program thresholds. Acquisition volumes rose as buyers secured inventory, leveraging clear policy guidance and financing. SBPE reforms increased the SFH property value ceiling to BRL 2.25 million (USD 401,786), expanding access for middle-income families to regulated rates and predictable amortization. Major metros and regional centers remain purchase-driven, supported by program and SBPE channels. Digital origination growth has prompted lenders to focus on pre-approvals and cash-flow-verified offers, sustaining purchase momentum into 2026.

Home Improvement and Renovation is the fastest-growing segment, with a 10.04% CAGR from 2026 to 2031. Shorter tenures, smaller ticket sizes, and simplified registration support growth. Public credit lines for renovations and efficiency upgrades meet urban borrowers’ needs for targeted improvements without long-term exposure. Policies allowing collateral reuse enable owners to extract equity for upgrades while retaining core financing. The "Others" category, including construction and refinancing, remains cyclical, influenced by funding costs and developer pipelines. Digital verification and quick decision-making drive the expansion of renovation-aligned products, catering to smaller projects requiring rapid execution.

By Provider: Fintech Platforms Disrupt Bank Hegemony

Banks hold an 88.83% market share in 2025, driven by deposit funding, SBPE mandates, and operational scale in SBPE and FGTS segments. The leading public bank executes nationwide subsidy-linked housing finance programs. Private leaders invest in AI-enabled origination and superapps with pre-approvals and debt-service calculators to streamline decisions. Other players are projected to grow at a 12.82% CAGR as fintech originators and specialized finance firms scale Open Finance data and securitization, enhancing participation through Banking-as-a-Service and structured partnerships in Brazil's home loan market.

Regulatory modernization clarifies Open Finance roles and expands licensed finance companies' scope in the credit ecosystem. Bradesco and peers report higher digital disbursement shares, highlighting the durability of end-to-end digital origination in retail credit. Banks maintain a funding cost advantage by pairing SBPE deposits with TR-linked liabilities for stable pricing. Non-banks scale by standardizing analytics and investor reporting for receivables issuance, improving execution for portfolios above economic thresholds. These developments ensure Brazil's home loan market remains competitive and inclusive while adhering to prudential standards.

By Interest Rates: Fixed Gains Traction Amid Volatility

Floating Interest Rates account for 93.25% of balances in 2025 and reflect TR-linked portfolios that moderate nominal installment variability for eligible borrowers. Savings deposit mechanics tie funding costs to TR, which supports asset-liability alignment and reduces duration risk in the bank channel. FGTS-backed loans frequently default to floating arrangements, which sustains the segment’s dominance across cycles and income tiers. Borrowers prioritize approval and monthly affordability under program rules, which reinforces floating-rate selection under current frameworks. Floating prevalence remains a structural feature of the Brazil home loan market, given funding design and program mandates.

Fixed Interest Rates are projected to grow at a 14.57% CAGR through 2031, supported by updated amortization guidance that stabilizes nominal installments and improves predictability. Regulators outlined how amortization components can offset inflation-related updates to protect monthly budgets while managing price dynamics. Middle-income buyers in the new SFH ceiling band show early interest in fixed structures to improve household budgeting under tighter conditions. Lenders diversify into fixed exposures to improve risk metrics and portfolio resilience within ISO-aligned frameworks. The Brazil home loan market gains product diversity as fixed offerings complement floating staples during and after policy normalization.

By Loan Tenure: Mid-Tenures Optimize Affordability

Terms greater than 20 Years held a 50.04% share in 2025, driven by subsidy-linked structures extending repayments up to 35 years to match income-constrained budgets. The SFH framework supports longer tenures, reducing monthly obligations compared to 20-year terms and improving loan-to-income ratios at approval. Households with stronger cash positions prefer shorter tenures to minimize total interest while preserving liquidity. Digital platforms use consented account data to tailor tenures based on verified cash flows, reinforcing tenure stratification by income band in Brazil's home loan market.

The 11 to 20 Years segment is the fastest-growing tenure, with a 13.67% CAGR from 2026 to 2031, as borrowers balance affordability and total interest costs under the updated SFH ceiling. Approval systems optimize tenure and monthly obligations to align with borrower cash flows and property prices. Shorter tenures dominate premium and investor segments, where liquidity and asset strategies favor faster amortization. The rising share of mid-tenures reflects improved applicant qualification under predictable installment structures and enhanced digital screening. This shift supports healthier borrower profiles and steadier servicing across economic cycles.

Geography Analysis

Regional distribution in 2025 aligns with population and income patterns, with the Southeast estimated at 43.1% of origination value, reflecting larger average ticket sizes and dense employment hubs. The Brazil home loan market share for the Southeast tracks its higher per capita income and infrastructure depth, which sustains purchase-led flows in metropolitan areas and peripheries. Urbanization and transit investments support absorption, with new corridors improving access to employment and services that underpin demand. The Brazil home loan market benefits from this concentration of value while policy changes expand the eligible base for regulated financing.

The Northeast is the fastest-growing region as program intensity, lifestyle migration, and services expansion bring more qualified households into formal mortgage channels. Differentiated subsidy rates and eligibility criteria reflect local income profiles and support originations in key capitals and growth corridors. Lenders focus on urban centers with stronger employment and stable collateral values to ensure portfolio performance. The Brazil home loan market expands through this regional rotation while maintaining exposure to core metropolitan volumes. Diversification by city size and sector mix improves resilience during monetary transitions.

The South contributes steady volumes with diversified economies and high urbanization that support consistent demand for mid-tenure and fixed options. The Central-West shows strong population growth and government-linked employment that raises eligibility for SBPE and FGTS-backed loans. The North remains smaller in value terms due to income and infrastructure gaps, yet industrial hubs with formal employment increase FGTS-linked participation. As Open Finance widens underwriting precision, regional access improves and supports broader inclusion within the Brazil home loan market.

Mordor Intelligence examines the home loan market across diverse other regional markets as well, offering granular country-level perspectives for United States, China, and India and more.

Competitive Landscape

Brazil's home loan market is highly concentrated, with a few major institutions dominating origination and servicing. Leading banks control most volumes and funding access. State-backed channels focus on subsidy-linked loans, while private banks use AI-driven origination within mobile platforms to reduce decision times. Open Finance consent flows and real-time debt-service calculators enable pre-approved offers and higher conversion rates. Public sector leaders expand housing disbursements via SBPE and FGTS, maintaining low non-performing ratios. Banco do Brasil strengthens regional lending through ESG-linked international partnerships, addressing housing and infrastructure needs.

Digital transactions are rising as Bradesco and peers increase online disbursements using automated KYC and app-based support. Bank-fintech collaborations grow through Banking-as-a-Service, where fintechs handle origination, and banks provide balance sheets and compliance. Open Finance and Pix streamline underwriting, reducing manual documentation and improving access for cash-flow-rich but thin-file borrowers. SBPE deposits anchor bank funding, while securitization supports non-bank scaling. Program reforms, set for 2026, raise ceilings and refine amortization rules, expanding the borrower base.

Strategic efforts focus on speed, predictability, and inclusion. Itaú integrates real-time pre-approvals into its superapp, tailoring offers via Open Finance. Bradesco accelerates digital origination with automated KYC workflows. Banco do Brasil deepens ESG-linked financing for resilient construction and infrastructure. Caixa's BaaS initiative extends white-label channels to fintechs, enhancing reach with incumbent-grade funding and compliance.

Brazil Home Loan Industry Leaders

Banco do Brasil S.A.

Caixa Econômica Federal (CEF)

Banco Bradesco S.A.

Itaú Unibanco Holding S.A.

Banco Santander Brasil S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Caixa has launched a Banking-as-a-Service initiative, inviting fintech partners to white-label origination journeys. Caixa will provide the SBPE funding base and ensure regulatory compliance. This strategy maintains its funding and execution advantages while expanding into digital-first channels, enabling faster cash access for qualified borrowers.

- July 2025: CDP, with SACE's guarantee, has provided a €250 million (USD 23.52 million) loan to Banco do Brasil. This funding supports ESG-linked lending, focusing on low-impact construction and resilient infrastructure in environmentally vulnerable regions. The transaction strengthens Banco do Brasil's ability to finance sustainable housing and related projects with improved funding competitiveness.

- April 2025: The federal government has launched 'Faixa 4' under the 'Minha Casa, Minha Vida' program to assist families earning above the previous income limits but unable to afford market-rate mortgages. This measure expands regulated credit access and fosters inclusion in metropolitan areas where property values are nearing the revised thresholds, ensuring more families benefit from affordable housing opportunities.

Brazil Home Loan Market Report Scope

The Brazil home loan market refers to the structured financial system that provides housing loans for property purchases, construction, refinancing, and home improvement across the country. It plays a central role in expanding homeownership, supporting residential development, and enabling long‑term wealth creation for households. The market is shaped by government housing support programs, rapid urbanization, middle‑class expansion, rising disposable incomes, and fintech‑enabled credit accessibility, while interest‑rate dynamics and technological advancements continue to influence mortgage uptake and lending practices nationwide.

The market is segmented by loan purpose, provider type, interest rate structure, and loan tenure. By loan purpose, it includes purchase of new or existing homes, home improvement and renovation loans, and other categories such as construction and refinancing, reflecting the diverse financing needs of Brazilian households. By provider, the market spans banks, housing finance companies, and other lending institutions, each contributing to credit availability through distinct underwriting models and capital structures. By interest rate type, the market is divided into fixed and floating rate mortgages, capturing borrower preferences under varying macroeconomic and monetary conditions. By loan tenure, the market includes loans of up to 10 years, 11–20 years, and more than 20 years, aligning with affordability considerations and long‑term repayment capacity. The report offers Market size and forecasts for the Brazil Home Loan Market in value (USD Billion) for all the above segments.

| Purchase (New/Existing) |

| Home Improvement/Renovation |

| Others (Construction, Refinance, etc.) |

| Banks |

| Housing Finance Companies |

| Others |

| Fixed Interest Rates |

| Floating Interest Rates |

| ≤ 10 Years |

| 11 – 20 Years |

| Greater than 20 years |

| By Loan Purpose | Purchase (New/Existing) |

| Home Improvement/Renovation | |

| Others (Construction, Refinance, etc.) | |

| By Provider | Banks |

| Housing Finance Companies | |

| Others | |

| By Interest Rates | Fixed Interest Rates |

| Floating Interest Rates | |

| By Loan Tenure | ≤ 10 Years |

| 11 – 20 Years | |

| Greater than 20 years |

Key Questions Answered in the Report

What is the size and growth outlook for the Brazil home loan market from 2026 to 2031?

The Brazil home loan market size is USD 62.99 billion in 2026, and it is projected to reach USD 104.81 billion by 2031 at a 10.72% CAGR.

Which loan purpose category leads, and which is growing fastest in Brazil?

Purchase, New or Existing, leads with a 63.57% share in 2025, and Home Improvement and Renovation is the fastest-growing at a 10.04% CAGR from 2026 to 2031.

How is the provider mix changing in Brazil’s housing finance?

Banks hold 88.83% of originations in 2025, while Others are projected to grow at a 12.82% CAGR as fintechs scale Open Finance-driven origination and securitization partnerships.

What rate structures do borrowers prefer in Brazil, and how is that shifting?

Floating Interest Rates hold a 93.25% share in 2025 due to TR-linked structures and program design, and fixed offerings are gaining traction at a 14.57% CAGR under updated amortization guidance.

Which regions lead value and which show the fastest expansion in Brazil?

The Southeast leads by value with an estimated 43.1% share in 2025, and the Northeast shows the fastest trajectory under enhanced subsidies and urban migration.

What policy changes are most relevant for product and tenure choices in Brazil?

The SFH ceiling increase to BRL 2.25 million and amortization refinements support mid-tenure and fixed-structure adoption while preserving affordability in subsidy-linked segments.

Page last updated on: