Brazil Car Loan Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

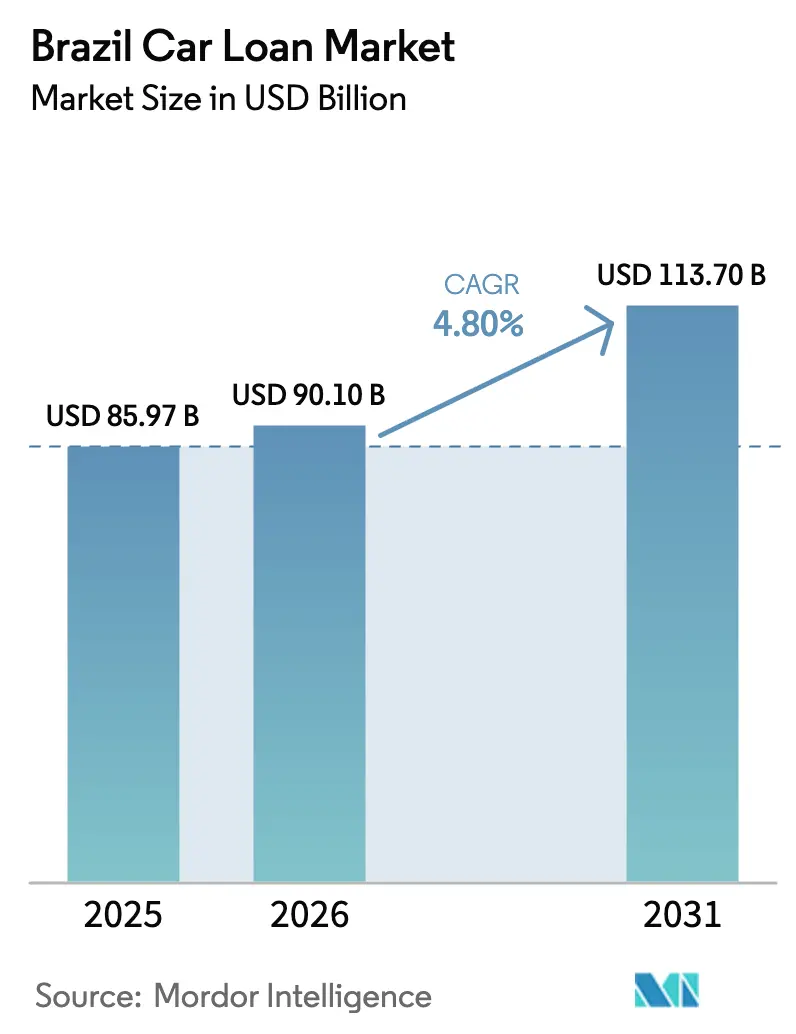

| Base Year Market Size (2025) | USD 85.97 Billion |

| Market Size (2026) | USD 90.10 Billion |

| Market Size (2031) | USD 113.70 Billion |

| Growth Rate (2026 - 2031) | 4.80% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Car Loan Market Analysis by Mordor Intelligence

The Brazil Car Loan Market size is projected to be USD 85.97 billion in 2025, USD 90.10 billion in 2026, and reach USD 113.70 billion by 2031, growing at a CAGR of 4.80% from 2026 to 2031.

High funding costs define current conditions as the Central Bank held the Selic policy rate at 15.00% in December 2025, which sustained auto credit rates near multi-year highs and kept affordability under pressure. Even within this restrictive setting, vehicle financing expanded by 2.3% month over month in November 2025, as lenders leveraged digital origination, embedded insurance, and well-targeted credit programs to support demand[1]Banco Central do Brasil, “Selic interest rate,” Banco Central do Brasil, bcb.gov.br. Risk controls remain central as lenders respond to the Central Bank’s financial stability guidance, while evolving insurance rules improve claims-handling timelines and clarify expectations at the point of sale, helping sustain attachment rates on financed vehicles. The Brazil car loan market continues to be shaped by OEM captive finance coordination, leading banks’ omnichannel footprints, and fintechs that scale via Open Finance data sharing and faster underwriting cycles.

Key Report Takeaways

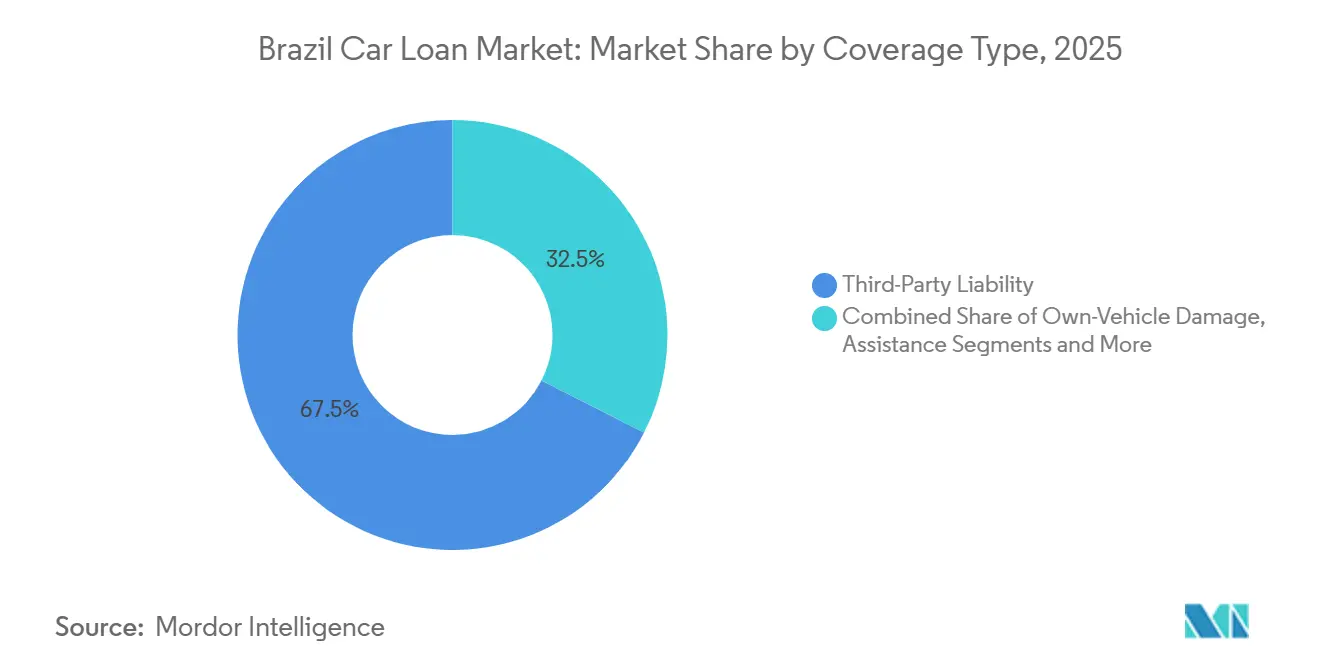

- By coverage type, third-party liability led the Brazil car loan market with 67.50% revenue share in 2025, while comprehensive own vehicle damage coverage is forecast to expand at a 5.82% CAGR through 2031.

- By vehicle type, passenger cars accounted for 58.80% of the Brazil car loan market share in 2025, while commercial vehicles are projected to grow at a 5.43% CAGR to 2031.

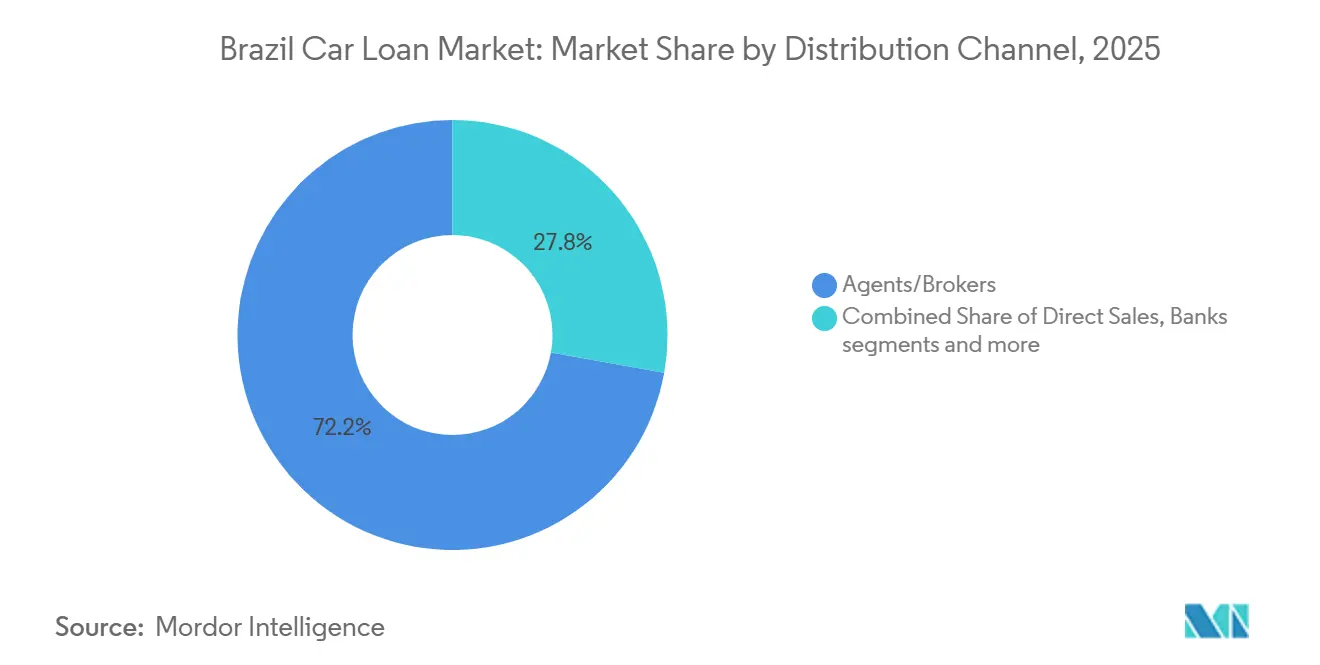

- By distribution channel, agents and brokers held 72.20% of the Brazil car loan market share in 2025 and posted the fastest growth outlook at a 7.54% CAGR to 2031.

- By powertrain, ICE vehicles represented 59.70% of the Brazil car loan market share in 2025, while hybrids are the fastest growing at a 7.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of Brazil. The car loan market share in our global report expresses these relative weights.

Brazil Car Loan Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in vehicle ownership and financed purchases supporting bundled insurance demand | +1.2% | National, with higher penetration in São Paulo, Rio de Janeiro, Minas Gerais | Medium term (2-4 years) |

| Digital auto‑lending platforms improving loan and insurance penetration | +0.9% | National, led by Southeast and South regions, expanding to Northeast | Short term (≤ 2 years) |

| Competitive lending landscape offering flexible, insurance‑linked auto finance options | +0.7% | National | Medium term (2-4 years) |

| Urban expansion driving sustained demand for personal mobility and vehicle financing | +0.8% | National, strongest in metropolitan regions and state capitals | Long term (≥ 4 years) |

| Mandatory third‑party liability norms reinforcing insurance attachment rates | +0.5% | National | Long term (≥ 4 years) |

| Strengthening consumer confidence and credit access encouraging vehicle ownership | +1.0% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in vehicle ownership and financed purchases supporting bundled insurance demand

Brazil’s registered vehicle base continued to expand in 2024, creating a larger pool of credit-eligible assets and reinforcing insurance attachment at the point of sale in the Brazil car loan market. Lenders and insurers increasingly use bundled offers to connect financing with third-party liability and comprehensive add-ons, which stabilize recovery values and improve borrower protection through the term. Auto-linked bank verticals deliver cross-sell synergies that raise policy uptake and service penetration, which supports fee income and improves lifetime value per financed customer[2]Porto Seguro, “Conference Call Transcript 1Q25 Results,” Porto Seguro, portoseguro.com.br. Underwriting and claims modernization in 2025 reduces processing frictions and increases transparency, which encourages attachment of broader coverage and lowers disputes for financed vehicles in the Brazil car loan market. The structure of the Brazil car loan market benefits from these dynamics because higher insured penetration also protects collateral value and reduces charge-offs for lenders, particularly in prime retail portfolios.

Digital auto lending platforms are improving loan and insurance penetration

Digital origination continued to gain share of applications in 2025 as lenders integrated mobile flows, marketplace listings, and real-time data sources that compress time to yes in the Brazil car loan market. Banco PAN scaled its vehicle portfolio with omnichannel origination and standardized credit journeys, while marketplace integrations with thousands of dealers widened funnel reach and improved conversion. Creditas grew auto equity and auto finance volumes in 2025 by applying AI native underwriting and Open Finance data to lower acquisition costs and enhance credit selection across segments. Digital distribution of motor insurance advanced in parallel, helped by large consumer platforms that plug insurance into everyday financial journeys, which lifts policy attachment among financed borrowers in the Brazilian car loan market[3]Nu International, “Insurance, policy launches and milestones,” Nu International, international.nubank.com.br. These advances shorten approval cycles, lower operating cost per loan, and support safer growth even while headline rates are high, adding resilience to the Brazil car loan market.

Competitive lending landscape offering flexible, insurance linked auto finance options

Competition intensified as banks, captives, and fintechs diversified offers, including insurance linked financing at the point of sale in the Brazil car loan market. Santander’s consumer finance franchise reinforced leadership in new vehicle financing across Latin America in 2025 and used embedded journeys in dealer networks to raise policy attachment and optimize acquisition costs. Volkswagen Financial Services grew originations and introduced a fintech platform for dealers that centralizes cash management and receivables, which strengthens captive ecosystems around financing and insurance[4]Volkswagen Financial Services Overseas, “Annual Report IFRS 2024,” Volkswagen Financial Services Overseas, vwfs-overseas.com. Usage-based and telematics-enabled motor policies add pricing precision for safer drivers and create better alignment between credit risk and insurance premiums for financed customers. Flexible combinations of tenor, coverage, and bundled services improve affordability and expand the addressable base in the Brazil car loan market even when benchmark rates are elevated.

Urban expansion driving sustained demand for personal mobility and vehicle financing

Sustained urban growth keeps personal mobility central to household and microbusiness economics, which supports recurring demand for vehicle financing in the Brazil car loan market. The rise of app-based transport and delivery services continues to broaden the pool of borrowers for two-wheelers, passenger cars, and light commercial vehicles used for work and commuting. Municipal fleet transition programs, including zero-emission bus initiatives in major capitals, redirect financing demand toward new vehicle categories and complementary infrastructure in the Brazil car loan market. Public-private credit enhancement structures launched in 2025 support early deployments and crowd in private lenders, which broadens customer choice and improves long-term ecosystem readiness. As local EV and hybrid assembly scales, consumer choice widens, and residual values stabilize, adding more financing options across powertrains in the Brazil car loan market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic volatility and elevated interest rates constraining auto financing demand | -1.8% | National | Short term (≤ 2 years) |

| Inflationary pressures reducing affordability of insured vehicle loans | -0.9% | National, most acute in lower‑income regions | Medium term (2-4 years) |

| Rising credit risk and defaults leading to tighter lending and underwriting criteria | -0.7% | National, concentrated in Northeast and North regions | Medium term (2-4 years) |

| Regulatory complexity increasing compliance burdens for insurers and lenders | -0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Macroeconomic volatility and elevated interest rates constraining auto financing demand

The Selic rate remained at 15.00% at the end of 2025, which kept monthly installments high and weighed on affordability for many prospective borrowers in the Brazil car loan market. Central Bank data show system household credit expanded in November, but the cost of non-earmarked auto credit remained elevated, limiting the pace of demand normalization. The Monetary Policy Report signaled persistent risks around inflation expectations, which constrained near term room for policy easing and reinforced cautious underwriting in the Brazil car loan market. Lenders with strong dealer channels used promotional pricing and bundled coverage to protect volumes, but originations still reflected strict debt service limits and down payment discipline. Portfolio managers emphasized margin protection and risk-adjusted returns, which kept the Brazil car loan market on a measured growth track into 2026.

Inflationary pressures reducing affordability of insured vehicle loans

Headline price dynamics moderated compared with prior peaks, yet kept operating costs for vehicle ownership elevated, especially when financed with comprehensive insurance required by lenders in the Brazil car loan market. Manufacturers and distributors faced input cost pass-through that influenced sticker prices, while borrowers also absorbed higher nominal premiums for broader coverage selections. Banks retained tighter credit score thresholds to preserve portfolio quality, which pushed some shoppers toward longer terms or delayed purchases in the Brazil car loan market. Consumers prioritized essential coverage and priced options more actively through digital channels, which sharpened competition among insurers and brokers. These combined forces incrementally reduced affordability for lower-income borrowers even as lenders refined bundled offers to keep monthly payments manageable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage Type: Liability mandates anchor, comprehensive damage accelerates at 5.82% CAGR

Third-party liability captured 67.50% in 2025, establishing the baseline layer of protection for financed vehicles in the Brazil car loan market share. Lenders typically enforce proof of valid liability coverage during the life of the contract, which improves recoveries and supports loss mitigation for the Brazil car loan market. The regulator’s focus on timely claims decisioning enhances customer experience and reduces disputes, which supports stable attachment rates at origination in the Brazil car loan market. Large integrated groups use bank insurance linkages to cross-sell roadside assistance and warranty extensions that complement liability coverage for financed customers. These practices anchor the Brazil car loan industry to a transparent coverage floor while keeping pricing responsive to driver risk and vehicle profile.

Comprehensive and own damage policies expand faster than liability, growing at a 5.82% CAGR through 2031 as lenders require full coverage to protect collateral in the Brazil car loan market. Captive and bank-led embedded journeys increasingly integrate premiums into financing flows, which simplifies purchase and lowers customer acquisition costs for insurers. Digital claims and telematics enhance pricing accuracy for safe drivers, a feature that supports adoption among younger and urban borrowers using financing. As coverage becomes more modular, borrowers can match add-ons to use patterns, which supports persistency and lowers loss severity for lenders and insurers in the Brazil car loan market. Greater product choice and faster fulfilment across channels sustain the upward trajectory for comprehensive attachment on financed vehicles.

By Vehicle Type: Passenger cars 58.80%, commercial vehicles accelerate at 5.43% CAGR

Passenger cars accounted for 58.80% of financed units in 2025, maintaining the anchor role for retail portfolios in the Brazil car loan market. Dealers and marketplaces expanded omnichannel flows that accelerate approvals and support used car financing, which broadened access for consumers seeking predictable monthly payments. Large banks leveraged branch reach and digital banking to sustain origination scale for mainstream models and to embed insurance offers at the point of sale. Captives prioritized brand loyalty and residual value stability, which benefited new car penetration and ancillary services in the Brazil car loan market. As underwriting incorporates more verified income and transaction data, approval quality improves and delinquency risk moderates across passenger car borrowers.

Commercial vehicles are projected to grow at a 5.43% CAGR through 2031, reflecting rising last-mile logistics, municipal fleet upgrades, and small business vehicle needs in the Brazil car loan market. New credit enhancement programs for zero-emission buses help crowd in private capital and create bankable templates that can scale to more cities. OEMs broadened the range of urban delivery vans and light trucks available for financing, and captives used dealer ecosystems to bundle service contracts with loans. Business borrowers rely on a predictable total cost of ownership, which makes insurance attachment and maintenance packages valuable alongside financing in the Brazil car loan industry. As the local assembly of electrified commercial models advances, financing options are expected to broaden further.

By Distribution Channel: Agents/brokers 72.20%, digital embedded models scale rapidly

Agents and brokers held 72.20% in 2025 and show the strongest expansion trajectory to 2031, reflecting their deep dealer integration and ability to configure coverage at the point of sale in the Brazil car loan market. Consolidation of broker networks and adoption of digital quoting tools shortened issuance times and enhanced price transparency, which supports higher conversion in financed segments. Banks continued to cross-sell motor policies to loan customers and used account-level data to pre-fill applications, which reduces friction for financed buyers. Fintech insurers and digital banks scaled cost-efficient embedded journeys for auto coverage, improving reach into first-time insurance customers connected to loan applications. This mix of traditional and embedded channels increases consumer choice and supports broader attachment in the Brazil car loan market.

While agents and brokers remain the dominant conduit, embedded and marketplace models scale quickly from a small base by leveraging traffic from banking apps and auto listings in the Brazil car loan market. Dealer-linked embedded insurance can be integrated into loan flows, which streamlines pricing and reduces abandonment during the customer journey. As Open Finance adoption deepens, cross-institution data sharing supports more accurate quotes and underwriting in real time, which is additive to both conversion and risk management in the Brazil car loan market. The distribution landscape is therefore diversifying toward hybrid models that combine broker expertise, bank reach, and embedded digital journeys. Over time, this should raise competitive intensity and value for borrowers in the Brazil car loan market.

By Powertrain: ICE 59.70%, hybrids fastest at 7.65% CAGR on flex fuel synergy

ICE vehicles, including flex fuel models, accounted for 59.70% of financed volume in 2025 and continue to anchor portfolio composition in the Brazil car loan market. The flex fuel platform remains a structural advantage given wide fueling availability and competitive operating costs when ethanol pricing is favorable. Lenders use standard terms and well-tested residual models for ICE, which support scalable underwriting and predictable recoveries in the Brazil car loan market. ICE borrowers often qualify for bundled roadside assistance and extended warranty packages that improve the total cost of ownership predictability under financing. As electrification options broaden, lenders are positioned to offer side-by-side comparisons that keep ICE competitive in price-sensitive segments of the Brazil car loan market.

Hybrids are the fastest growing powertrain at a 7.65% CAGR through 2031 in the Brazil car loan market, supported by flex hybrid models tailored to local fuels and usage patterns. Policy levers under the MOVER program, including targeted IPI treatment and R&D support, encourage OEM investments that expand model availability and reduce prices. As domestic assembly ramps up, lenders gain more confidence in residuals and battery warranty support, which increases financing acceptance for hybrid and plug-in variants. Captives and banks are adapting tenor and coverage bundles to align with electrified maintenance profiles, including packages for battery, drivetrain, and roadside services. These developments strengthen the financing case for hybrids as a bridge technology in the Brazil car loan market.

Geography Analysis

The Southeast region holds more than 60% of national vehicle financing volume, which secures the region’s leadership in the Brazil car loan market and provides lenders with the densest concentration of dealer networks and digital banking users. High network density enables faster approvals, tighter fraud controls, and broader insurance attachment for financed vehicles in this region. Universal banks utilize omnichannel models that combine branches and mobile journeys, supported by captive programs that integrate finance and coverage at the dealership. As embedded insurance expands, borrowers in the Southeast are more likely to encounter dynamic quotes and one-click attachment in loan flows, which lifts conversion for financed purchases in the Brazil car loan market. The region’s mix of new and used vehicles aligns well with the strengths of banks, captives, and digital lenders.

The South features a higher propensity for early adoption of electrified models and a dense dealer ecosystem, which fosters a diverse mix of retail and SME borrowers in the Brazil car loan market. Local tax treatment and state-level incentives for low-emission vehicles complement federal policies that steer investment toward cleaner technologies. Captive finance units leverage strong dealer relationships to pilot embedded insurance and post-sale support services that encourage financing uptake. Digital insurers and consumer platforms have also built meaningful policy bases in the region, improving selection and speed for borrowers who prefer mobile experiences. These features sustain healthy competition and choice for consumers and microbusinesses in the Brazil car loan market.

The Northeast is the fastest growing region with a 6.2% CAGR, supported by the rise of digital origination, embedded models, and lenders’ focus on under served segments in the Brazil car loan market size conversation at the regional level. Fintechs use alternative data and Open Finance records to expand access among borrowers with limited traditional credit history, which reduces rejection rates and improves fairness. Banks and captives are also extending coverage via broker partnerships and dealer integrations to raise attachment in financed sales. As payment and underwriting data become more portable, underwriting models better reflect actual cash flows, which improves access and portfolio performance in the Brazil car loan market. These trends point to convergence in product availability across regions over the forecast period.

Mordor Intelligence examines the car loan market across diverse other regional markets as well, including Europe and Asia, while also offering granular country-level perspectives for United Kingdom, Japan, China, India, India, France, and Russia and more.

Competitive Landscape

The Brazil car loan market exhibits moderate concentration, with universal banks and captives retaining structural distribution advantages while digital entrants expand share through underwriting innovation and embedded flows. Lenders with large dealer networks continue to capture scale benefits in origination, servicing, and cross-selling of motor insurance and assistance bundles that are integral to financed purchases. Banks use omnichannel reach and data depth to streamline approvals and maintain strict risk controls aligned to Central Bank guidance. Captives focus on brand penetration, residual value stability, and dealer-centric journeys that preserve customer loyalty within each OEM’s ecosystem. Fintechs target cost-to-serve reductions and faster time to yes, using Open Finance data to enrich credit models and improve conversion. Insurance attachment remains a common differentiator, with digital and broker channels enabling choice at the point of sale in the Brazil car loan market.

Bank-led consumer finance franchises preserved their leadership in 2025 on the strength of dealer partnerships, branch presence, and mobile penetration. Santander’s Digital Consumer Bank reinforced its position in new vehicle financing across Latin America and maintained momentum in Brazil through deeper dealer integration and disciplined risk provisions to reflect macro updates. Banco PAN expanded originations with its marketplace-enabled funnel and standardized credit journeys that compress approval times and improve dealer experience. Banco BV continued to differentiate in vehicles through data integrations and sustainability positioning for financed fleets. These institutions complement financing with embedded motor insurance routed through brokers and banking channels, helping maintain high attachment rates in the Brazil car loan market.

Specialist lenders and fintechs posted faster growth by lowering acquisition costs and using AI native underwriting on top of Open Finance data to improve risk selection. Creditas increased origination in 2025 and accessed securitization markets for funding diversification, while keeping customer acquisition costs low by using automation and data pipelines. Captive lenders used dealer ecosystems and white label fintech platforms to embed payments, receivables, and insurance in streamlined workflows for retailers and customers. Insurance groups strengthened bank partnerships and expanded telematics-enabled pricing that rewards safe drivers, which aligns premiums with credit risk for financed vehicles in the Brazil car loan market. Across the ecosystem, the competitive focus centers on embedded insurance, alternative data underwriting, and electrified fleet financing templates that can scale.

Brazil Car Loan Industry Leaders

Porto Seguro Companhia de Seguros Gerais

Tokio Marine Seguradora S.A.

MAPFRE Seguros Gerais S.A.

Allianz Seguros S.A.

HDI Seguros S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Banco Central do Brasil released November 2025 monetary statistics showing vehicle financing expanded 2.3% month over month, with household credit up 11.1% year over year.

- November 2025: Brazil launched a credit enhancement structure for zero-emission buses, designed to mobilize private capital alongside public and philanthropic commitments.

- July 2025: Creditas announced a new FIDC program to support auto equity and auto finance operations, enhancing funding diversification for origination growth.

- June 2024: Banco Volkswagen S.A. detailed funding diversification in its 2024 IFRS report, supporting over 1.5 million contracts and enhancing captive lending capacity for dealers and consumers.

Brazil Car Loan Market Report Scope

A car loan, also known as an auto or vehicle loan, is financing provided by a financial institution or lender to help individuals purchase a car. A complete background analysis of the brazil car loan market includes an assessment of the industry associations, the overall economy, and emerging market trends by segment. Significant changes in the market dynamics and market overview are also covered in the report.

The Brazilian car loan market is segmented by product type and provider type. By product type, the market is sub-segmented into used cars (consumer use & business use) and new cars (consumer use & business use). By provider types, the market is sub-segmented into banks, non-banking financial services, original equipment manufacturers, and others (fintech companies). The report offers the value (USD) for the above segments.

| Third-Party Liability | |

| Own-Vehicle Damage | Collision |

| Comprehensive (Theft, Glass, Fire, etc.) | |

| Assistance & Add-ons (Roadside, Legal) |

| Passenger Cars |

| Commercial Vehicles |

| Direct |

| Agents/Brokers |

| Banks |

| Embedded Channels (OEM, Affinity, etc.) |

| Digital Platforms and Other Emerging Channels |

| ICE Vehicles |

| Electric Vehicles |

| Hybrid Vehicles |

| Others (Hydrogen FCEV, LPG/CNG, etc.) |

| By Coverage Type | Third-Party Liability | |

| Own-Vehicle Damage | Collision | |

| Comprehensive (Theft, Glass, Fire, etc.) | ||

| Assistance & Add-ons (Roadside, Legal) | ||

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Distribution Channel | Direct | |

| Agents/Brokers | ||

| Banks | ||

| Embedded Channels (OEM, Affinity, etc.) | ||

| Digital Platforms and Other Emerging Channels | ||

| By Powertrain | ICE Vehicles | |

| Electric Vehicles | ||

| Hybrid Vehicles | ||

| Others (Hydrogen FCEV, LPG/CNG, etc.) | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Brazil car loan market?

The Brazil car loan market stands at USD 90.1 billion in 2026 and is projected to reach USD 113.7 billion by 2031, reflecting a 4.80% CAGR.

How do current interest rates impact car loan affordability in Brazil?

The Selic policy rate stood at 15.00% in December 2025, which keeps borrowing costs elevated for consumers. Vehicle financing still grew 2.3% month over month in November 2025 as digital origination and bundled offers supported demand.

Which customer and product segments are leading in the Brazil car loan market?

Passenger cars held 58.80% of financed volume in 2025, agents and brokers handled 72.20% of distribution, and ICE vehicles made up 59.70%, while hybrids and comprehensive coverage are the fastest growing at 7.65% and 5.82% CAGRs.

Which regions show the strongest activity and fastest growth for Brazil car loans?

The Southeast accounts for more than 60% of vehicle financing volume, while the Northeast is the fastest growing region at a 6.2% CAGR.

What role do digital lenders and embedded insurance play in Brazil auto financing?

Banks and fintechs use digital origination and embedded insurance to speed approvals and lower acquisition costs, including Banco PAN's omnichannel scale and Creditas' AI native underwriting with Open Finance data. Consumer platforms expand policy attachment for financed buyers, as Nubank reached 2 million insurance policies by mid 2024.

How is electrification influencing the Brazil car loan market?

Hybrids are the fastest-growing powertrain at a 7.65% CAGR, supported by targeted incentives and localization that improve financing acceptance. Public-private initiatives for zero-emission buses mobilize private lenders and create scalable templates for fleet financing.

Page last updated on: