Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

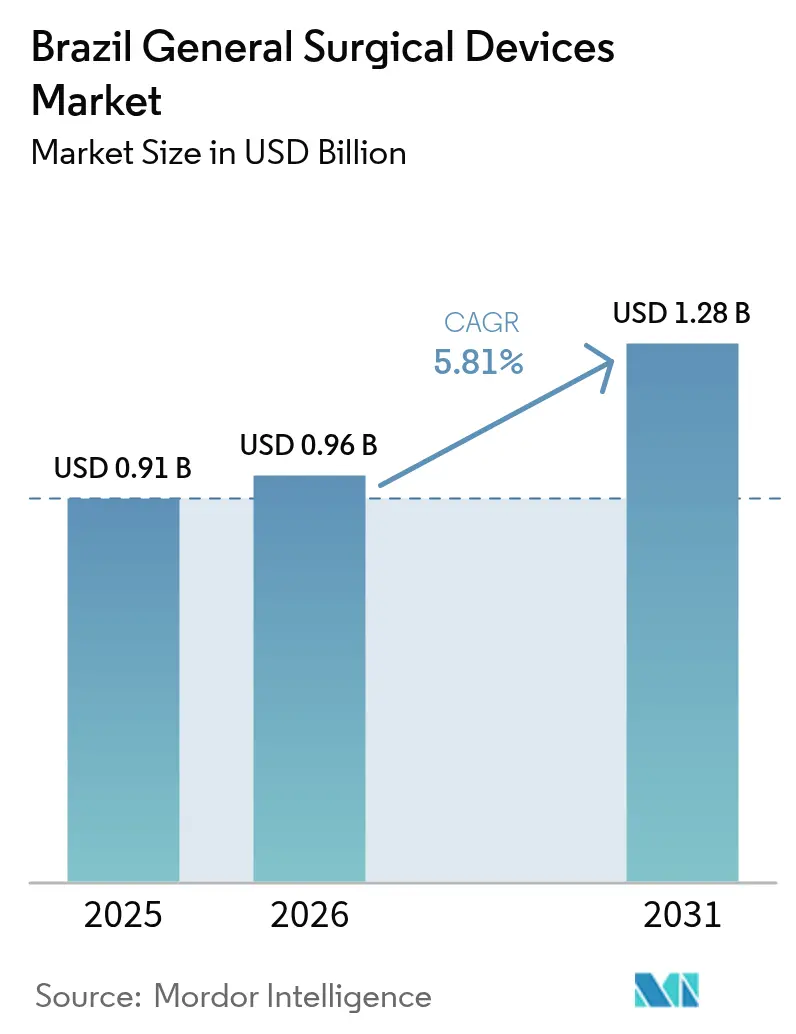

| Base Year Market Size (2025) | USD 0.91 Billion |

| Market Size (2026) | USD 0.96 Billion |

| Market Size (2031) | USD 1.28 Billion |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

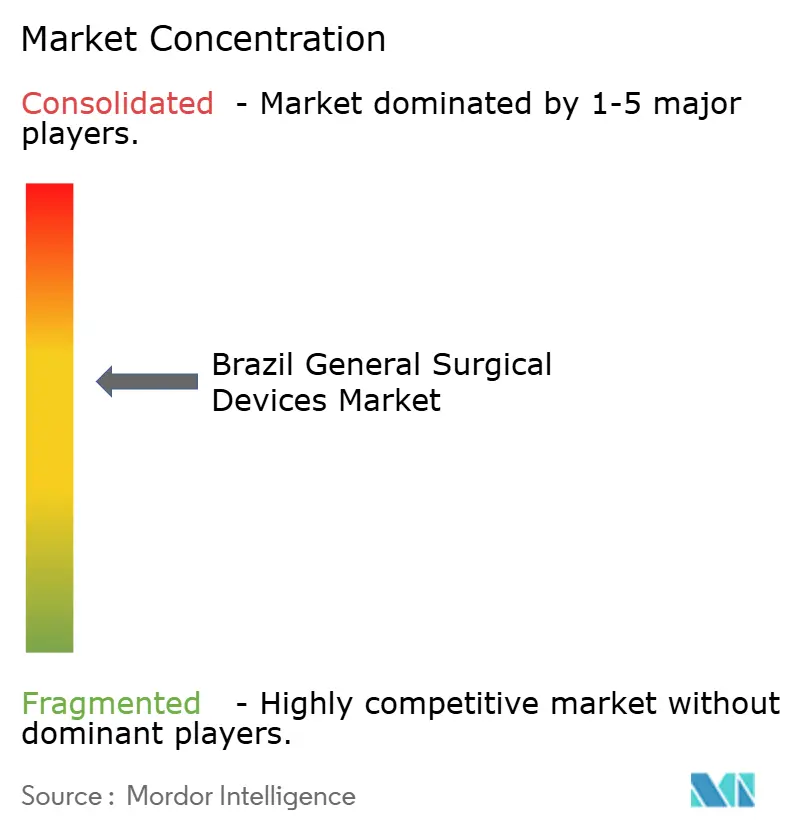

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil General Surgical Devices Market Analysis by Mordor Intelligence

Brazil General Surgical Devices Market size in 2026 is estimated at USD 0.96 billion, growing from 2025 value of USD 0.91 billion with 2031 projections showing USD 1.28 billion, growing at 5.81% CAGR over 2026-2031. Strong procedure volumes, rapid device approvals and a sizable private-insurance base cement Brazil’s position as Latin America’s surgical hub. Upgrading from conventional to minimally invasive and robotic platforms is reshaping procurement priorities, while industrial incentives support local production that cuts import reliance. Regional tele-health projects, notably UBS+Digital, shorten learning curves and widen specialist reach, creating demand for smart, connected instruments. Currency volatility still raises import costs, yet semiconductor and robotics tax credits under Nova Indústria Brasil buffer supply-chain risk. Private insurers covering 52.2 million lives in 2025 accelerate adoption of premium surgical technologies and outpatient centers.

Key Report Takeaways

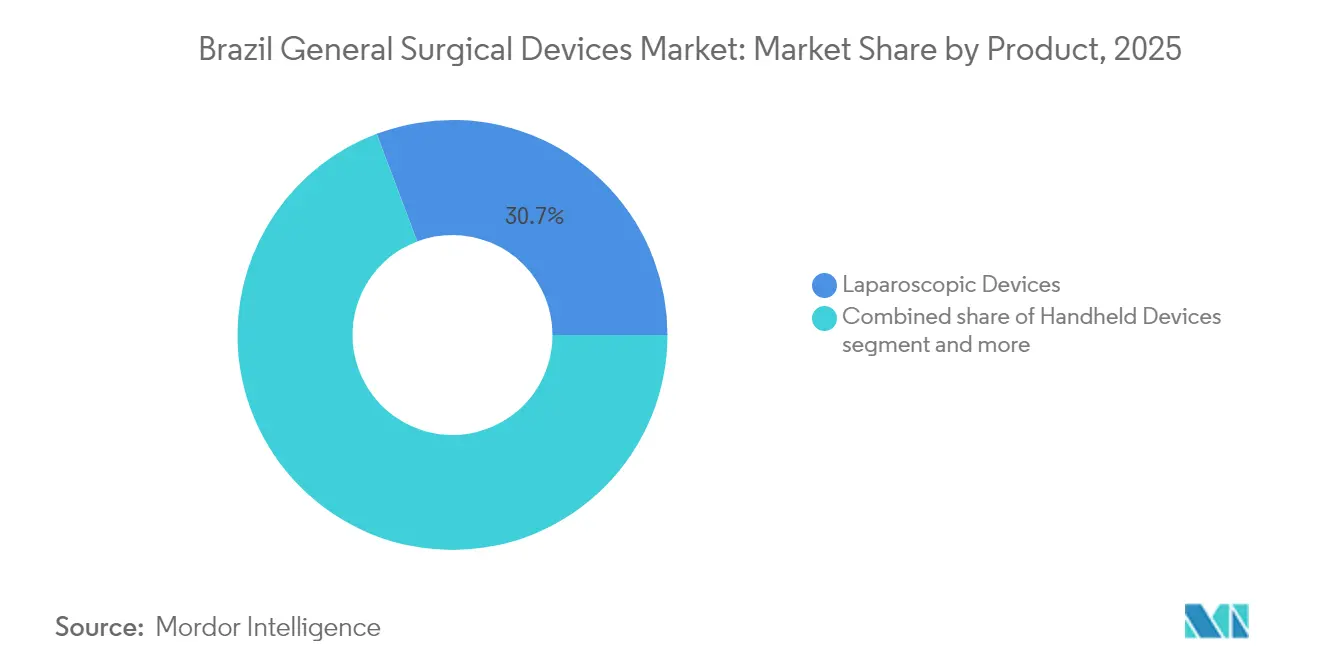

- By product, laparoscopic devices held 30.74% of Brazil general surgical devices market share in 2025; robotic and computer-assisted systems are forecast to rise at 6.70% CAGR through 2031.

- By procedure approach, minimally invasive surgery accounted for a 67.52% share of Brazil general surgical devices market size in 2025 and is poised to advance at 7.03% CAGR to 2031.

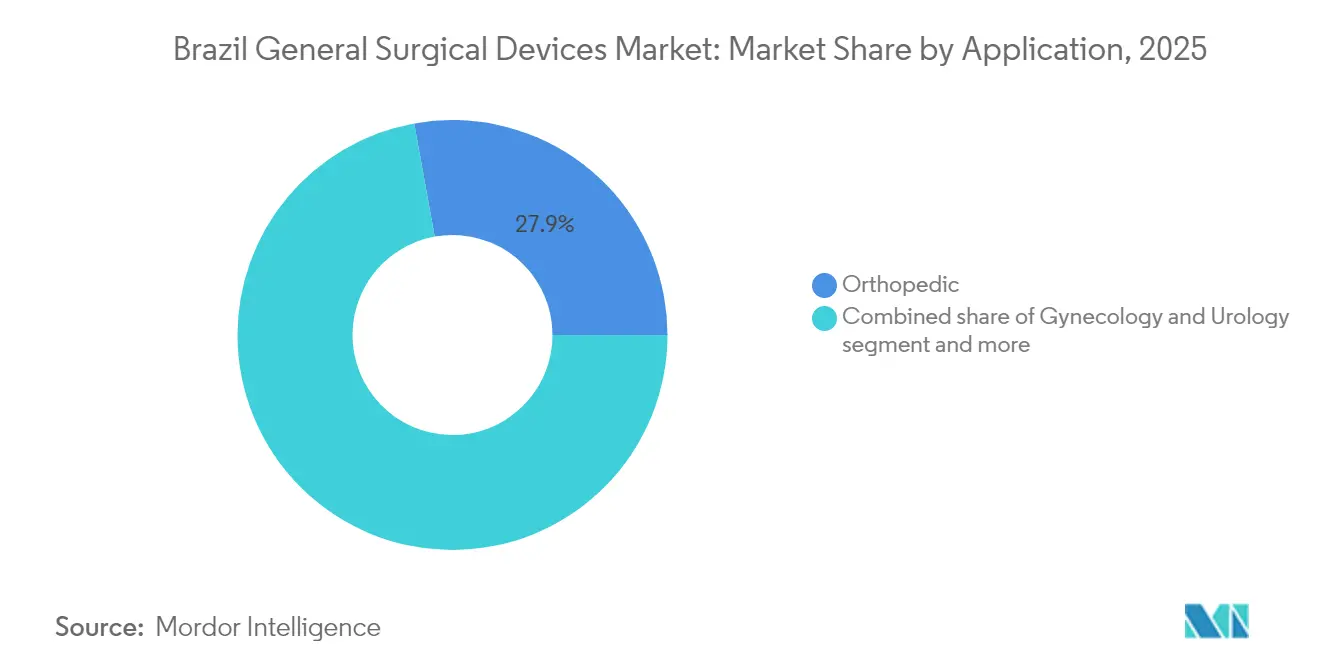

- By application, orthopedic procedures led with 27.85% revenue share in 2025, while gynecology and urology are projected to expand at 6.93% CAGR.

- By end-user, hospitals dominated with 72.44% share in 2025; ambulatory surgical centres record the highest projected CAGR at 6.84% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil General Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for surgical procedures owing to chronic diseases | +1.2% | National, concentrated in Southeast and South regions | Medium term (2-4 years) |

| Growing popularity of minimally-invasive surgery & tech. advances | +0.8% | National, with early adoption in Tier-1 cities | Short term (≤ 2 years) |

| Expansion of private health-insurance coverage | +0.6% | National, strongest in São Paulo, Minas Gerais, Rio de Janeiro | Medium term (2-4 years) |

| Government incentives for local medical-device manufacturing | +0.5% | National, focused on industrial hubs in Southeast | Long term (≥ 4 years) |

| Digitally-enabled remote surgical training & tele-mentoring | +0.4% | National, prioritizing North and Northeast regions | Medium term (2-4 years) |

| Accelerated ANVISA fast-track approvals for innovative devices | +0.3% | National regulatory impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for surgical procedures owing to chronic diseases

Cardiovascular disease remains Brazil’s top mortality driver, with public spending of BRL 1 billion (USD 200 million) on cardiac procedures in 2023.[1]Source: Estatística Cardiovascular – Brasil 2023, “Arq. Bras. Cardiol.,” scielo.br National surgical volume reached 4,433 interventions per 100,000 population, and aging demographics ensure continued growth in complex orthopedic, oncologic and vascular operations. Device makers gain as tertiary hospitals replace legacy instruments with advanced stapling, energy and imaging systems that shorten operating times. Regional procedure disparities open white-space for value-oriented tools in underserved states. As chronic disease prevalence climbs, Brazil general surgical devices market gains a predictable demand baseline that anchors five-year revenue visibility.

Growing popularity of minimally-invasive surgery and technology advances

Surgeons increasingly favor laparoscopy and robotics thanks to shorter stays and fewer complications, fueling consumables usage and capital purchases. The SkyWalker robotic arm’s first South American case at Vera Cruz Hospital shows institutional appetite for next-gen platforms. Early European experience with Hugo systems points to console times under 40 minutes and zero intra-operative events, reinforcing clinical benefit narratives. Enhanced imaging, such as microscope-integrated OCT, improves precision in vitreoretinal surgery. Rapid learning via tele-mentoring and AI-driven latency control lowers geographic barriers, extending adoption into mid-tier hospitals. Collectively, technology progress intensifies refresh cycles within Brazil general surgical devices market.

Expansion of private health-insurance coverage

Beneficiary rolls increased to 52.2 million in 2025, up 1.2 million from 2023, creating a paying cohort for premium implants and navigation systems. Regulatory rules enacted in 2024 mandate continuity in hospital networks, encouraging operators to invest in robotic theatres to remain accredited. Rising elective procedure volumes elevate instrument demand and spur ambulatory centres, a segment requiring portable energy platforms and compact towers. Device OEMs secure predictable cash-pay pipelines that hedge against slower public procurement, lifting overall Brazil general surgical devices market growth.

Government incentives for local medical-device manufacturing

The BRL 300 billion Nova Indústria Brasil credit line targets an increase in domestic device output from 42% to 70% by 2033,[2]Source: Government of Brazil, “Brazil launches new industrial policy with development goals and measures up to 2033,” gov.br granting tax breaks and preferential tender scoring to local firms. Semiconductor subsidies of BRL 7 billion annually ensure sensor availability for robotic arms and high-definition scopes, while BRL 186.6 billion earmarked for industrial digitalization expands cleanroom robotics. Manufacturers such as Lifemed and BMR Medical are scaling ISO-certified lines that shorten lead times and sidestep currency swings. Localization strengthens supply resilience and positions Brazil general surgical devices market as a regional export base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced devices | -0.7% | National, most pronounced in public healthcare sector | Medium term (2-4 years) |

| Currency depreciation raising import costs | -0.5% | National, affecting import-dependent devices | Short term (≤ 2 years) |

| Limited surgeon training outside Tier-1 cities | -0.4% | Regional, concentrated in North and Northeast | Long term (≥ 4 years) |

| Reimbursement hurdles for innovative procedures | -0.3% | National, primarily affecting SUS procedures | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost of advanced devices

Robotic theatres demand capital outlays of USD 0.5–2.5 million plus yearly service contracts above USD 200,000, straining SUS budgets and slowing diffusion to secondary hospitals.[3]Source: International Journal of Abdominal Wall and Hernia Surgery, “Do the costs of robotic surgery present an insurmountable obstacle?,” journals.lww.com Small facilities prioritize essential laparoscopic sets over premium articulation instruments, narrowing vendor opportunities. Two-tier access persists as private insurers reimburse robotics while public tariffs lag device depreciation schedules. Consequently, price sensitivity curbs the otherwise robust momentum of Brazil general surgical devices market.

Currency depreciation raising import costs

Real weakness lifts landed prices for imported scopes and staplers, with SELIC rates near 14.75% sustaining a strong-dollar environment. Import dependence remains a significant portion for medical devices, exposing hospitals to quarterly price resets and procurement delays. Hedging adds cost layers, impinging on operating margins and dampening near-term growth in Brazil general surgical devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product – teady laparoscopic leadership with brisk robotic gains

Laparoscopic devices generated 30.74% of Brazil general surgical devices market share in 2025, underpinned by high-volume cholecystectomy and bariatric procedures. Robust replacement cycles for towers, scopes and trocars keep revenue consistent. In contrast, robotic and computer-assisted systems show the fastest 6.70% CAGR. Early adopters cite 95% patient-satisfaction scores in knee arthroplasty, supporting wider hospital investment. Electrosurgical generators and advanced bipolar instruments gain traction as surgeons seek blood-sparing modalities. Wound-closure and access devices record parallel demand, reflecting procedure mix growth. Localized sourcing under Nova Indústria Brasil should shorten lead times for consumables, encouraging hospitals to standardize across single-vendor portfolios and stabilize market volumes.

In handheld instruments, forceps and retractors remain indispensable for both open and minimally invasive operations, ensuring baseline revenue even as high-tech segments rise. OEMs refresh portfolios with ergonomic redesigns and smart tagging for asset tracking. Other devices, such as 3D visualization platforms, progress from pilot to multi-site deployment, offering incremental upsell opportunities. Product diversification equips suppliers to capture budget-constrained public tenders while addressing premium needs in private institutions, reinforcing their foothold within Brazil general surgical devices market.

By Procedure Approach – Minimally invasive techniques dominate trajectories

Minimally invasive surgery controlled 67.52% of Brazil general surgical devices market size in 2025, and is expected to grow at 7.03% CAGR from 2026 to 2031. Surgeons leverage shorter stays to free hospital beds amid capacity pressures, validating capital expenditure on towers and articulating instruments. Remote training programs speed diffusion to secondary cities, pulling trocar and energy device demand. Robotic systems expand the spectrum of minimally invasive cases from urology to colorectal, stacking further growth on a large base.

Open surgery remains vital for trauma and complex oncologic resections yet sees bookings migrate to laparoscopy where feasible. Consumable volume stabilizes in thoracotomy and vascular applications but trends downward in routine abdominal work. Emerging single-incision and NOTES techniques hint at future shifts, yet incremental adoption ensures open platforms continue to contribute meaningful revenue, maintaining diversity in Brazil general surgical devices market.

By Application – Orthopedic scale meets gyne-urology momentum

Orthopedic procedures secured 27.85% of 2025 revenue, anchored by aging demographics and higher arthroplasty adoption. Robotic guidance improves alignment accuracy, boosting implant longevity and patient outcomes. The segment’s broad case mix supports steady instrument consumption, buffering cyclical swings elsewhere in Brazil general surgical devices market. Cardio-thoracic surgery, fueled by BRL 1 billion public spending on cardiovascular care, generates stable demand for sternotomy and heart-valve instruments.

Gynecology and urology, however, outpace at 6.93% CAGR on rising endometriosis, prostate and renal cancer interventions. Robotic platforms enable nerve-sparing prostatectomy and myomectomy with minimal blood loss, encouraging private hospitals to market ‘scarless’ packages. Neurosurgery and spine devices grow moderately, aided by expansion of high-complexity centres in underserved regions. This application blend diversifies vendor revenue streams and sustains expansion in Brazil general surgical devices market.

By End-User – Hospitals still rule as ambulatory centres surge

Hospitals retained a 72.44% share in 2025, reflecting the concentration of advanced imaging suites, ICU beds, and multi-disciplinary teams. Teaching centres pioneer the adoption of microscope-integrated OCT and dual-console robotics, creating reference sites that drive provincial uptake. Yet, ambulatory surgical centres will grow 6.84% CAGR to 2031 as payers push day-case pathways.

Vendors designing compact generators and mobile towers capture this fast-moving opportunity, increasing Brazil general surgical devices market penetration. Specialty clinics, though smaller in volume, influence technique preferences and serve as launchpads for niche devices such as single-use scopes.

Geography Analysis

Regional economic contrasts shape device adoption. The Southeast and South capture the bulk of spend due to higher income and dense hospital networks. São Paulo anchors corporate headquarters and hosts the largest cluster of private robotic suites, while Minas Gerais and Rio de Janeiro record rising insured populations that sustain premium procedure volumes. Paradoxically, the Southeast shows the lowest procedures per 100,000 citizens, implying underutilized capacity that suppliers can convert with training and workflow optimization.

The North and Northeast trail in equipment density but attract policy focus. Tele-ICU success stories boost confidence in technology-enabled care, paving entry for portable laparoscopic towers and modular ICU ventilators. Infrastructure grants under Nova Indústria Brasil include tax holidays for factories in Manaus Free Trade Zone, potentially lowering landed costs in remote states and expanding Brazil general surgical devices market footprint.

Center-West, propelled by agribusiness wealth and Brasília’s federal contracts, observes hospital expansions that incorporate smart OR designs. Variations in cardiovascular surgery access underscore latent demand for basic instrumentation and perfusion disposables. Consistent regulatory standards across Brazil simplify nationwide product rollout, yet logistics planning must account for continental distances and infrastructure gaps.

Regulatory Landscape

Brazilian regulation of general surgical devices is overseen by ANVISA, with core requirements for classification, labeling, and registration anchored in RDC No. 751/2022. A major 2026 shift is the move toward device digital data standards, led by IN 426/2026 for UDI submissions into the SIUD database, which standardizes master data and tightens labeling controls across risk classes.

Trade and import processes are converging on a single-window model. Since April 27, 2026, the Declaracao Unica de Importacao (DUIMP) requires ANVISA authorization to be included in a unified flow, while 2026 tariff actions by GECEX and 2025-2026 policy changes have tightened import costs and strengthened incentives for domestic production, with more emphasis on local value-add for tender competitiveness.

Competitive Landscape

International majors Johnson & Johnson, Medtronic, and Stryker dominate premium segments through multi-channel distribution and surgeon-training grants. Yet ANVISA fast-track policies lower entry barriers, enabling MicroPort, Olympus, and Purple Surgical to launch new platforms within months of global clearance. Local firms Lifemed, BMR Medical, and Locamed leverage Nova Indústria Brasil subsidies to scale production of trocars, staplers, and energy pens, winning price-sensitive SUS tenders. Strategic joint ventures pair foreign IP with domestic assembly, qualifying products for tariff exemptions and public quotas, thereby redirecting share within Brazil general surgical devices market.

M&A momentum rises as global players seek in-country manufacturing to secure tender preference. Meanwhile, startups funded by BRL 200 million BNDES-Butantan-Finep pool target AI-guided endoscopic systems and single-use robotic wrists.

Competitive intensity is further amplified by service models bundling disposables, analytics and uptime guarantees in subscription contracts that shift capex into opex. This evolving mix sustains innovation velocity and price competition across Brazil general surgical devices market.

Brazil General Surgical Devices Industry Leaders

B. Braun SE

Boston Scientific Corporation

Johnson & Johnson (Ethicon, DePuy Synthes)

Medtronic plc

Stryker Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Digital compliance and traceability are becoming a commercial lever as Brazil rolls out UDI via SIUD. With IN 426/2026 effective March 1, 2026, suppliers that implement scalable item-master governance (GTIN/UDI-DI mapping, labeling workflows, and distributor readiness) can reduce friction in renewals, audits, and multi-site hospital standardization, particularly for high-throughput categories such as laparoscopic consumables and wound-closure devices. The same data standards also support public procurement modernization, where transparent tender documentation influences participation and contracting within SUS workflows.

A second opportunity area is local manufacturing and supply-chain localization tied to Nova Indústria Brasil targets and financing. The policy targets domestic health technology production of 50% by 2026 and 70% by 2033, supported by the BNDES SUS Suppliers program, which offers credit for national manufacturers at a minimum threshold of R$10 million to fund capacity expansions in trocars, staplers, and energy devices. On the demand side, June 2026 actions by ANVISA to collect industry input (Edital de Chamamento 4/2026) for revising tecnovigilancia rules could lead to more differentiated post-market capabilities among large hospital networks and distributor partners when selecting suppliers.

Recent Industry Developments

- July 2026: The ICEfx cryoablation system from Hospital Israelita Albert Einstein was introduced as a Latin America-first adoption for minimally invasive tumor treatment. The installation strengthens Brazil's role as a reference market for advanced minimally invasive platforms and accelerates clinical pull-through for related surgical access and energy-enabled toolsets.

- May 2025: The AESCULAP Aicon rigid sterile barrier system line from B. Braun was launched in Brazil to support surgical instrument sterilization workflows. The move strengthens central sterile services modernization and helps hospitals manage rising procedure volumes.

- September 2024: ANVISA announced a phased expansion of tecnovigilancia requirements introducing digital reporting enhancements for high-volume surgical devices. The update is aimed at improving post-market surveillance across major hospital networks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of devices used to perform general surgery in Brazil, across open and minimally invasive procedures, as purchased by hospitals, ambulatory surgical centers, and specialty clinics.

Scope exclusions: patient monitoring, anesthesia equipment, imaging systems, and non-device consumables like drapes and general procedure packs are excluded.

Segmentation Overview

- By Product

- Handheld Devices

- Laparoscopic Devices

- Electrosurgical Devices

- Wound-Closure Devices

- Trocars and Access Systems

- Robotic and Computer-Assisted Systems

- Other Devices

- By Procedure Approach

- Open Surgery

- Minimally Invasive Surgery

- By Application

- Gynecology and Urology

- Cardiology and Cardiothoracic

- Orthopedic

- Neurology and Spine

- Other Applications

- By End-user

- Hospitals

- Ambulatory Surgical Centres

- Specialty Clinics

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with mapping the Brazil surgical care environment and device demand signals, then narrowing into general surgery device categories used in operating rooms. We relied on public sources such as Brazil Ministry of Health publications, ANVISA notices and regulatory updates, DATASUS procedure statistics, OECD health indicators, and trade and tariff references where useful for import exposure.

To turn those inputs into sizing-ready assumptions, we also reviewed company filings and investor presentations that discuss Brazil or Latin America performance, along with association websites and reputable press coverage of hospital investments and procurement cycles. In a few places, paid subscriptions we have for company financials, news and financials, patent databases, and shipment-level import and export data were used to sanity-check pricing direction and demand momentum. These examples are not exhaustive, and many other public and internal references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm which device categories are consistently purchased for general surgery in Brazil, and how pricing, tendering, and replacement cycles are behaving across public and private care settings. We spoke with manufacturers, distributors, procurement teams, and clinical stakeholders so the secondary signals could be corrected where they were too broad or outdated, then cross-checked those points across major regions in the country.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | |

| Mid tier: 55% | Functional/Unit leaders: 40% | |

| Smaller Players: 14% | Managers: 47% |

Market-Sizing & Forecasting

Sizing was built using a top-down path first, where procedure volumes and care delivery capacity were used to reconstruct the addressable demand pool for core general surgery tools, then translated into value using typical device mix and price bands seen in Brazil. Results were corroborated with selective bottom-up approximations, including sampled SKU pricing multiplied by expected volumes for key categories and channel checks on distributor throughput. Where a line item appeared overstated, we adjusted totals accordingly.

Key inputs in the model included surgical procedure trends by setting, shifts between open and minimally invasive approaches, hospital and ASC capacity expansion, adoption of energy-based tools and wound-closure formats, and inflation and currency timing that can change realized USD values. For forecasting, we used scenario analysis supported by expert views on procedure growth, procurement budgets, and adoption pace for higher value systems, then applied smoothing to avoid one-off spikes. Where the bottom-up check had gaps, we filled missing pieces using proxy mix shares from similar care settings and normalized them back to the top-down total.

Data Validation & Update Cycle

Multiple checks were used so the final numbers stay aligned with real-world signals. Outputs were compared against independent indicators such as procedure growth, import intensity for device-heavy categories, and typical price movement seen in tenders and hospital purchasing, and large variances were reviewed before sign-off.

If interview feedback or a new public data release suggests a meaningful shift, we re-contact sources and re-run the key assumptions that drive the model. Reports are refreshed annually, and interim updates are made when material events occur. Before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Brazil General Surgical Devices Market Size Compared Against Other Published Estimates

Published market sizes for Brazil general surgical devices do not always line up because the included product basket and the year used as the starting point can vary, even when the titles look similar. Differences also come from how quickly prices are assumed to move and whether growth is linked to procedure activity or to broad healthcare spend.

Disposable surgical supplies like gloves, drapes, and general procedure packs sit outside Mordor Intelligence's scope, which is one reason some published totals look higher when they bundle those high-volume consumables into the same number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.91 B (2025) | |

| Global Consultancy A | USD 1.31 B (2024) | Uses a broader definition that includes disposable surgical supplies and procedural kits, and it also starts from a 2024 base year which shifts the size upward when converted to the study timeline. |

| Industry Publisher B | USD 0.72 B (2024) | Appears to use a narrower counted basket and a lower realized pricing set for 2024, with limited clarity on how device mix is adjusted between open and minimally invasive procedures. |

The spread in the table is mainly explained by what is counted as a general surgery device versus an operating room consumable, and by base-year timing in USD. By keeping scope tied to core surgical instruments and systems and validating mix and pricing through repeated checks, the final value stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the current size of Brazil general surgical devices market?

The market stands at USD 0.96 billion in 2026 and is projected to grow to USD 1.28 billion by 2031 at a 5.81% CAGR.

Which product segment grows fastest in Brazil general surgical devices market?

Robotic and computer-assisted systems lead with a 6.70% CAGR through 2031.

How significant is minimally invasive surgery in Brazil?

Minimally invasive procedures account for 67.52% of Brazil general surgical devices market size in 2025, advancing at 7.03% CAGR.

What regional markets offer the highest upside?

North and Northeast regions present untapped potential as tele-health and manufacturing incentives improve surgical capacity.

How do government policies influence device procurement?

Nova Indústria Brasil offers BRL 300 billion in credit and tender preference for locally made devices, encouraging hospitals to source domestic products.

Why are ambulatory surgical centres important for future growth?

They post the highest 6.84% CAGR as payers and patients favor cost-effective outpatient procedures, driving demand for portable and minimally invasive device sets.

Page last updated on: