Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 196.89 Million |

| Market Size (2026) | USD 213.51 Million |

| Market Size (2031) | USD 345.05 Million |

| Growth Rate (2026 - 2031) | 10.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Aesthetic Devices Market Analysis by Mordor Intelligence

The Brazil Aesthetic Devices Market size is projected to expand from USD 196.89 million in 2025 and USD 213.51 million in 2026 to USD 345.05 million by 2031, registering a CAGR of 10.08% between 2026 to 2031.

Rapid uptake of minimally and non-invasive procedures, a broadening practitioner base that now includes dentists and general practitioners, and faster ANVISA approvals are accelerating sales of injectables and energy-based platforms. Device demand is also buoyed by a sharp rise in obesity, social-media-driven beauty norms, and private-equity-funded franchise models that lower entry barriers for new clinics. At the same time, elevated SELIC rates, a weaker Brazilian real, and sporadic enforcement against grey-market imports create cost headwinds that favor companies with strong balance sheets and compliant portfolios. Competitive intensity is increasing as South Korean and U.S. manufacturers acquire local distributors or sign exclusive partnerships, signaling that the Brazil aesthetic devices market is becoming a regional launch pad rather than a stand-alone destination.

Key Report Takeaways

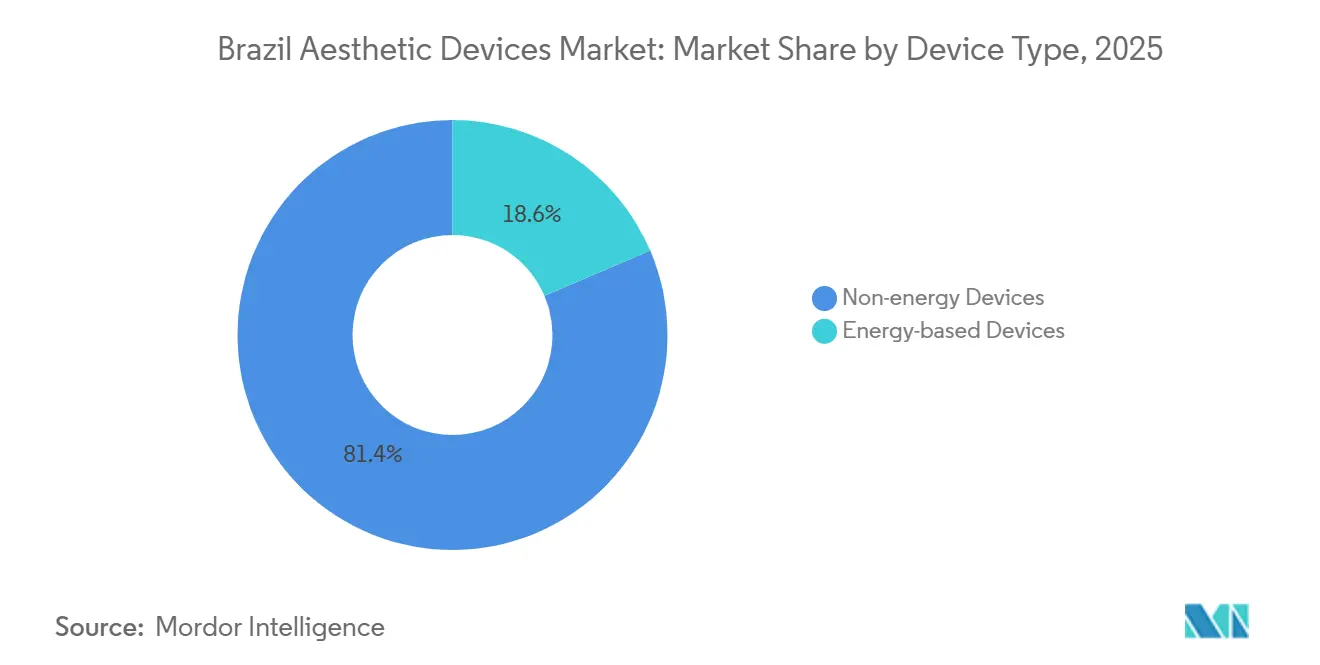

- By device type, non-energy devices dominated with 81.42% share of the Brazil aesthetic devices market in 2025, while energy-based platforms are projected to grow fastest at a 13.43% CAGR through 2031.

- By application, skin resurfacing and tightening led with 27.45% revenue share in 2025, whereas body contouring and cellulite reduction are forecast to expand at a 14.67% CAGR through 2031.

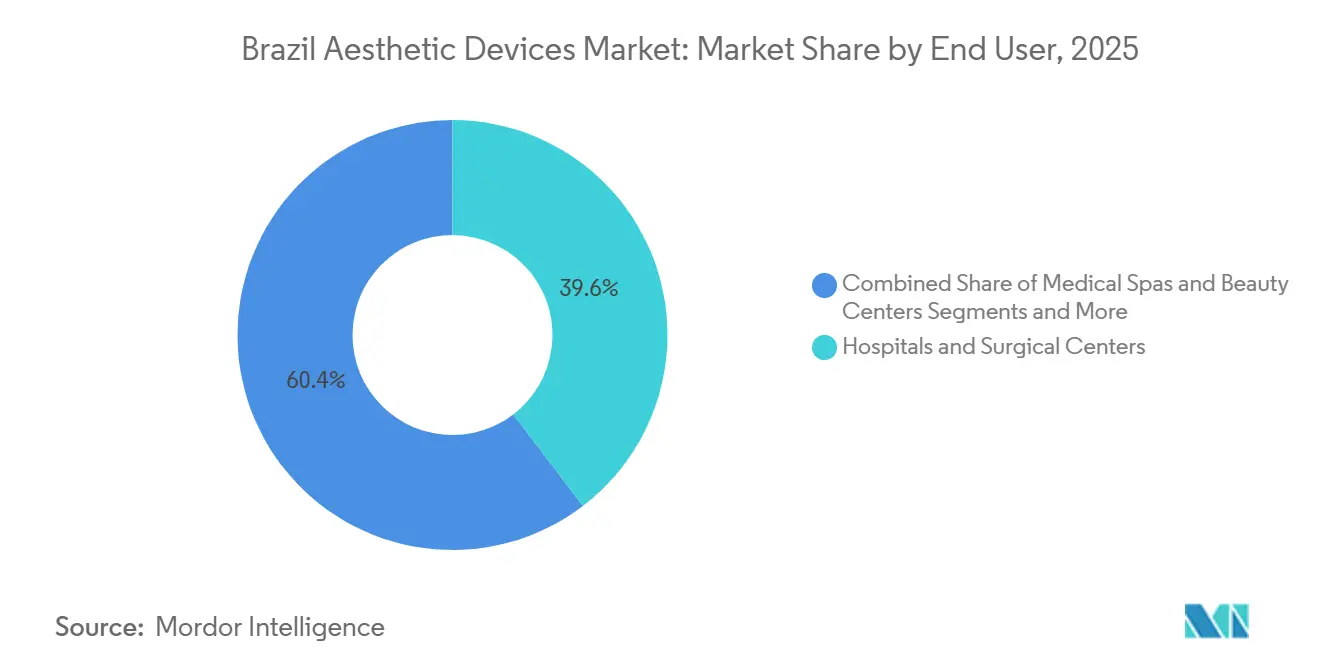

- By end user, hospitals and surgical centers captured 39.63% share in 2025, but medical spas and beauty centers are advancing at a 13.42% CAGR over the forecast period.

- By gender, female patients accounted for 76.24% of total procedures in 2025, yet male treatments are increasing at a 12.77% CAGR through 2031.

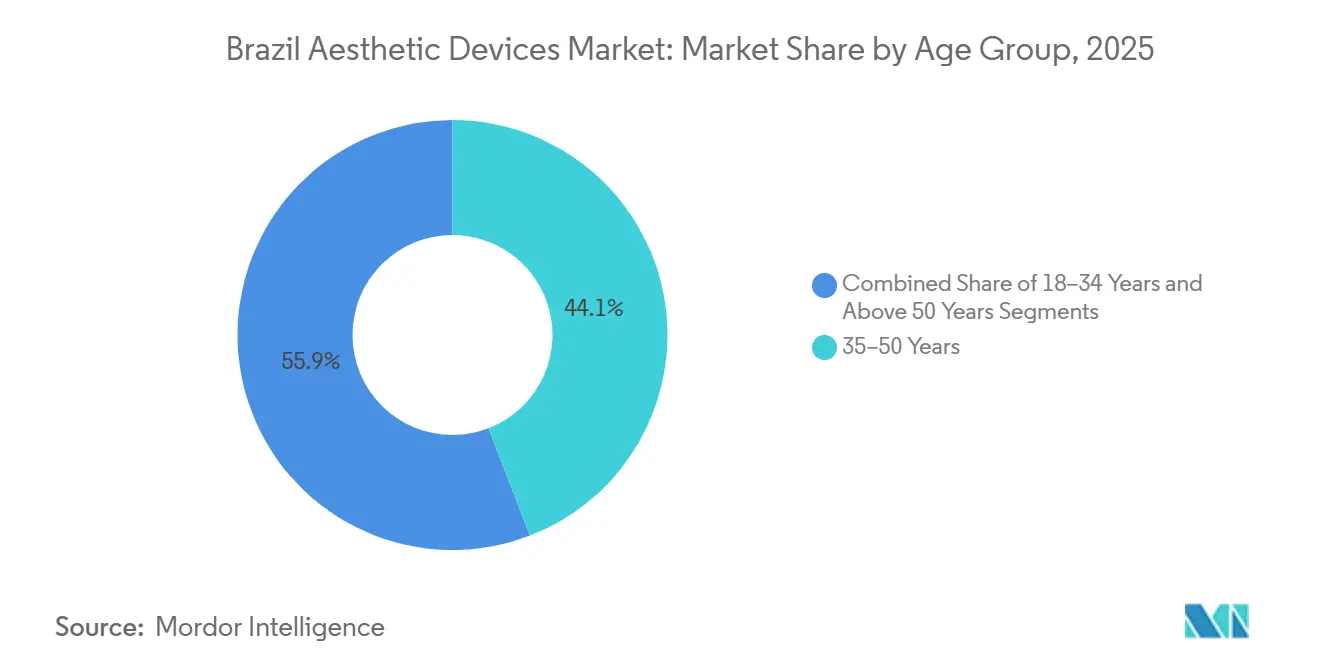

- By age group, individuals aged 35–50 years held 44.13% share in 2025, while the 18–34 cohort is on track to grow at a 13.82% CAGR during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Uptake of Minimally & Non-Invasive Procedures | +2.5% | São Paulo, Rio de Janeiro, Brasília | Medium term (2-4 years) |

| Growing Social-Media-Driven Beauty Consciousness | +1.8% | Urban centers with high Instagram/TikTok penetration | Short term (≤ 2 years) |

| Ageing & Obesity Trends Driving Body Contouring | +2.2% | Southeast and South regions | Long term (≥ 4 years) |

| Device Miniaturization Spurring Home-Use Segment | +1.0% | Affluent urban households | Medium term (2-4 years) |

| ANVISA Fast-Track Approvals (RDC 751/2022) | +1.5% | Nationwide | Short term (≤ 2 years) |

| Venture-Capital Inflow to Local OEMs | +0.8% | São Paulo, Rio de Janeiro | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Uptake of Minimally & Non-Invasive Procedures

Brazil performed 3.1 million aesthetic procedures in 2024—2.35 million surgical and 769,000 non-surgical—making it one of the top five countries worldwide.[1] ISAPS Staff, “2024 Global Survey Results,” International Society of Aesthetic Plastic Surgery, isaps.org Non-surgical demand is expanding faster because treatments such as botulinum toxin and hyaluronic-acid fillers require no anesthesia, create little downtime, and can be administered in dentist offices that already own laser or radiofrequency systems. Dentists executed 43% of clinic-based procedures in 2024 and 87% of total applications, effectively bypassing dermatology bottlenecks and shortening the device-adoption cycle.[2]Bruno Freitas, “Dentists’ Participation in Aesthetic Procedures in Brazil,” Revista Brasileira de Odontologia, scielo.br Franchise operators amplify this reach; JL Health alone supplies 18 equipment brands and expects revenue to reach BRL 700 million in 2024. By widening the practitioner base, these dynamics add 2.5 percentage points to the overall CAGR of the Brazil aesthetic devices market.

Growing Social-Media-Driven Beauty Consciousness

A Croma survey published in 2024 found that 72% of Brazilian men care about their looks and 68% openly discuss it, while Instagram and TikTok have become discovery engines for “before-after” content. Academic work confirms a causal link between social-media exposure and willingness to undergo procedures.[3] Fernanda Silva, “Social Media Exposure and Intent to Undergo Aesthetic Procedures,” International Journal of Environmental Research and Public Health, mdpi.com Clinics package multi-modality treatments such as the “Sleeping Beauty” combo of botulinum toxin plus JetPeel for viral storytelling, pulling younger patients into routine maintenance programs. This cultural shift is especially potent among 18-34-year-olds, who are growing at a 13.82% CAGR, and it lifts the market trajectory by roughly 1.8 percentage points.

Ageing & Obesity Trends Driving Body Contouring Demand

Obesity prevalence climbed from 14.5% in 2008 to 32.9% in 2021 and could hit 45.5% by 2030. Meanwhile, the share of Brazilians over 65 is on track to reach 17% by 2042. These twin demographics fuel demand for cryolipolysis, radiofrequency, and high-intensity-focused ultrasound (HIFU) treatments that offer fat reduction with minimal downtime. Brazilian studies have already validated 1470 nm endolaser techniques for localized adiposity, and micro-focused ultrasound trials report measurable collagen remodeling without surgery. Together they add an estimated 2.2 percentage points to the CAGR of the Brazil aesthetic devices market.

Device Miniaturization Spurring Home-Use Segment

Shrinking laser diodes and RF generators allow brands to pack clinical technology into handheld gadgets priced at USD 200-500. Portable IPL hair-removal devices and RF skin-tightening wands now populate Brazilian e-commerce platforms, targeting affluent urban households as an at-home bridge between clinic visits. JL Health is testing consumer sub-brands to capture recurring revenue from cartridge refills and RF gel packs. Although the category is small today, it adds roughly 1 percentage point to the market CAGR and offers manufacturers a hedge against clinic-channel saturation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cap-Ex for Advanced Platforms | -1.5% | Smaller cities and solo practices | Medium term (2-4 years) |

| Practitioner-Training Gaps & Safety Incidents | -1.2% | Nationwide, higher in non-metro areas | Short term (≤ 2 years) |

| Economic Volatility Hitting Discretionary Spend | -2.0% | Lower-income households nationwide | Short term (≤ 2 years) |

| Grey-Market Device Imports | -0.8% | Border states and online channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cap-Ex for Advanced Platforms

Fractional CO₂ lasers, hybrid HIFU/RF consoles, and picosecond tattoo-removal systems cost between BRL 200,000 and BRL 1.3 million, a steep hurdle for independent clinics. With real interest rates hovering near 10% after the SELIC peaked at 14.75% in 2025, equipment leases erode profitability and delay technology upgrades. A 22% depreciation of the real in 2024 also inflated import prices. The resulting cap-ex drag trims about 1.5 percentage points off CAGR.

Practitioner-Training Gaps & Safety Incidents

Narrative reviews in Anais Brasileiros de Dermatologia link poor anatomical knowledge to vascular occlusion, blindness, and strokes after filler injections. Dentists handle 87% of aesthetic injectables yet often lack structured facial-danger-zone training. Proposed legislation mandating adverse-event reporting remains stalled, keeping true complication rates opaque. High-profile mishaps spark negative media cycles that shave 1.2 percentage points from short-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Non-Energy Dominates, Energy Platforms Accelerate

Non-energy products represented 81.42% of the Brazil aesthetic devices market in 2025, led by 121 ANVISA-approved hyaluronic-acid fillers that generate repeat sales without large capital outlays. Allergan’s HArmonyCa hybrid and Merz’s Radiesse add collagen-stimulating options that increase procedure frequency among millennials seeking “pre-juvenation.” Implants remain a smaller category but benefit from Silimed’s 12,000 m² factory that supplies domestic clinics and exports to Mercosur neighbors.

Energy-based systems—lasers, RF, IPL, and HIFU—captured 18.58% in 2025 and will grow at a 13.43% CAGR, pushing the segment’s Brazil aesthetic devices market size above USD 90 million by 2031. Clinical studies show that 1470 nm diode endolaser reduces subcutaneous fat while tightening skin, and BTL’s Emsculpt Neo has logged 55,000 Brazilian treatments that combine RF lipolysis and electromagnetic muscle stimulation. Classys’ acquisition of JL Health provides a direct path to market for the Shurink Universe HIFU system, intensifying competition against Ultherapy and Ultraformer.

By Application: Body Contouring Momentum Builds

Skin resurfacing and tightening accounted for 27.45% of 2025 revenue, thanks to fractional CO₂ lasers and micro-focused ultrasound that treat photodamage and laxity with minimal downtime. Hair-removal demand remains robust across diode and IPL platforms, anchored by cultural norms favoring smooth skin and falling per-session pricing.

Body-contouring revenues are poised to rise faster than any other indication, expanding at a 14.67% CAGR as obesity heads toward a 45.5% adult prevalence by 2030. Cryolipolysis, RF, and HIFU technologies appeal to both post-bariatric patients and younger consumers chasing “summer-ready” physiques. The segment could surpass 25% of the overall Brazil aesthetic devices market share by 2031 if forecast adoption rates hold.

By End User: Medical Spa Franchises Scale Quickly

Hospitals and surgical centers retained 39.63% of the Brazil aesthetic devices market size in 2025 due to their capacity to combine surgical and non-surgical offerings under one roof. Yet franchise-backed medical spas are growing 13.42% annually by leveraging group purchasing, standardized protocols, and aggressive social-media marketing.

XP’s strategic stake in JL Health links equipment sales with Vision One’s hospital network, enabling bundled procurement that squeezes out smaller distributors. Solo dermatology practices struggle to match franchise pricing, especially while SELIC hovers above 13%, raising the cost of financing for new lasers and HIFU platforms.

By Gender: Male Uptake Narrows the Gap

Women still represented 76.24% of procedure volume in 2025, sustained by high filler usage and female-specific indications such as intimate rejuvenation.

Male demand is expanding at 12.77% CAGR, with liposuction volumes up 46% over five years and rising interest in botulinum toxin, RF skin tightening, and Fotona laser facial harmonization. Clinics now market “Bro-Tox” and body-sculpt packages expressly to male influencers and athletes, eroding the once-wide gender gap.

By Age Group: Digital Natives Spur Preventive Care

Patients aged 35-50 held 44.13% share in 2025, anchored by corrective treatments such as deep-plane fillers and fractional resurfacing.

The 18-34 cohort is accelerating at a 13.82% CAGR, normalizing quarterly micro-botox and biostimulator boosters as routine skin maintenance. Academic evidence ties Instagram exposure to elevated procedural interest, turning first-time patients into long-term subscribers who drive repeat device utilization.

Geography Analysis

Brazil’s Southeast corridor—São Paulo, Rio de Janeiro, and Minas Gerais—generates more than 60% of national revenue and attracts the earliest launches of new lasers, fillers, and hybrid injectables. São Paulo alone logged 42 healthcare-sector M&A deals worth BRL 7.69 billion in 2021, confirming its status as the commercial backbone for the Brazil aesthetic devices market. Enforcement under ANVISA’s “Safe Aesthetics Operation” is most vigorous here, giving compliant clinics a marketing edge.

The South—Paraná, Santa Catarina, and Rio Grande do Sul—shows high male procedure penetration and rapid uptake of franchise medical-spa formats. Santa Catarina clinics report steady demand for facial harmonization among men in their early thirties, reflecting regional cultural openness to aesthetic intervention.

Growth frontiers include the Northeast and Central-West, where improving household incomes intersect with rising obesity and aging metrics. Nonetheless, sparse dermatologist density and limited capital access slow technology adoption relative to the coast. The North remains the most underserved; logistical obstacles and fewer accredited practitioners curtail supply, though local manufacturers such as Silimed leverage lower operating costs to ship implants region-wide.

Regulatory Landscape

Aesthetic correction and beautification equipment is regulated in Brazil as medical devices under ANVISA rules, with active devices explicitly captured under RDC 751/2022. Products follow a risk-based pathway (Classes I to IV): lower-risk devices typically proceed via notification, while higher-risk devices require prior marketing authorization, which influences launch sequencing for energy-based platforms and implantable or other higher-risk categories.

Compliance also extends beyond product approvals to operational controls. Importation runs through the Portal Unico de Comercio Exterior (PUCOMEX) and is subject to sanitary intervention by ANVISA, with technical oversight anchored in the agency's ports, airports, and border function (GGPAF). Importers and distributors must hold an ANVISA Autorizacao de Funcionamento (AFE), and labeling and instructions in Portuguese are required, which raises the value of local regulatory representation and traceable, compliant supply chains as enforcement targets unauthorized and grey-market products.

Value Chain Analysis

The Brazil aesthetic devices value chain links multinational and domestic OEMs with local manufacturers (notably in implants and select energy-based systems), then relies on importers, distributors, and clinic end users such as hospitals and surgical centers, dermatology and aesthetic clinics, and rapidly scaling medical spa and beauty-center chains. More broadly, Brazil is still import-dependent for medical devices, and industry association reporting indicates imports of about USD 8 billion in 2024 versus roughly USD 800 million in exports, which heightens exposure to FX movements and logistics costs and increases the strategic value of established import and distribution infrastructure.

Regulatory readiness and after-sales service are key points of leverage in the chain. Companies need to meet ANVISA requirements under RDC 751/2022 (and related GMP expectations for higher-risk products) and ensure importer and distributor licensing (AFE) alongside compliant import processing via the Single Window. Industry bodies such as ABIMO and ABIMED shape coordination through compliance guidance and trade engagement, while export and capability-building programs like Brazilian Health Devices (ABIMO with ApexBrasil) support domestic manufacturers. Training, installation, maintenance, and consumables refills (cartridges, tips, gels, and injectables replenishment) drive recurring revenue and strengthen the role of distributor-led educator networks in accelerating device utilization.

Competitive Landscape

The Brazil aesthetic devices market hosts a mix of multinationals includes AbbVie/Allergan, Galderma, Merz, BTL, Candela, Cutera, and Lumenis and local champions such as JL Health, HTM Eletrônica, Ibramed, and Silimed. Bain-Capital-backed Classys now owns 77.5% of JL Health, turning the distributor into a forward operating base for the Shurink Universe HIFU system. XP’s BRL 225 million minority stake injects capital to push JL Health into gynecology, ophthalmology, and orthopedics while bundling device sales with Vision One hospital purchases .

Technology pipelines focus on hybrid and combination platforms: Allergan’s HArmonyCa mixes HA with CaHa microspheres; BTL’s Emsculpt Neo pairs RF lipolysis with magnetic muscle stimulation. Korean innovators Hugel and Classys differentiate through competitive pricing and robust educator networks, evidenced by Hugel’s partnership with Derma Dream to launch Letybo toxin across elite clinics in Rio and São Paulo.

ANVISA’s rigorous but transparent regulatory process, especially under RDC 751/2022, advantages firms with deep clinical dossiers. Grey-market crackdowns further tilt share toward companies that can document sterility, traceability, and post-market surveillance, setting up consolidation waves that favor players with diversified product portfolios and strong compliance teams.

Brazil Aesthetic Devices Industry Leaders

Cutera Inc.

Galderma

AbbVie (Allergan Aesthetics)

Candela Corporation

Lumenis Be Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear opportunity is the shift from third-party distribution toward direct, compliance-controlled commercial operations and vertical integration. Completed transactions show this direction: MedSystems acquired local laser manufacturer Vydence Medical in March 2025, followed by Classys completing the acquisition of a 77.5% stake in JL Health (MedSystems holding company) in March 2026, reinforcing Brazil as a hub for regional execution across nearby South American markets. These structures improve control over traceability, professional training, and service quality in a market where enforcement pressure on unauthorized devices is ongoing.

Regulatory modernization and tighter clinic oversight also create room for compliant portfolios and service-based models. RDC 751/2022 provides a more explicit framework for classifying and approving active aesthetic devices as medical devices, while ANVISA actions such as the Safe Aesthetics Operation raise the cost of non-compliance and favor suppliers with documented labeling, import controls, and post-market discipline. On the demand side, Brazil's large procedure base and the widening practitioner pool, including dentists and franchise-backed medical spas, supports placements for energy-based platforms and injectables. At the same time, home-use device miniaturization opens a parallel consumer channel, and brands that can manage Portuguese labeling, claims discipline, and authorized distribution gain an advantage over grey-market listings.

Recent Industry Developments

- June 2026: Galderma launched the "Acorde pronta com Restylane" campaign in Brazil to promote its Restylane hyaluronic-acid injectable portfolio. The effort reinforces brand pull-through at clinics and medical spas and supports repeatable, consumable-driven procedure volumes that complement capital equipment utilization.

- March 2026: Classys completed the acquisition of a 77.5% stake in JL Health, the holding company of MedSystems in Brazil. The transaction strengthens direct commercial execution, training reach, and after-sales control in Brazil, while also positioning the country as an operating base for broader South American expansion.

- June 2024: Galderma announced a USD 6.5 million investment linked to its Hortolandia, Brazil, manufacturing footprint, including acquisition of the plant and an adjacent 48,000 sq m plot to expand capacity. The investment improves local supply resilience for injectable aesthetics and reduces dependency on imported supply as demand and compliance requirements increase.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We define the Brazil aesthetic devices market as the value of equipment and device products used to perform aesthetic and cosmetic treatments in Brazil across clinical and consumer settings, counted at manufacturer selling prices for the country.

Scope exclusions: We exclude procedure fees, clinic service revenue, and general skincare products that are not regulated as aesthetic devices.

Segmentation Overview

- By Device Type

- Energy-based Devices

- Laser-based

- Radiofrequency

- IPL & Light-based

- Ultrasound / HIFU

- Non-energy Devices

- Dermal Fillers & Injectables

- Implants

- Microdermabrasion & Dermarollers

- Energy-based Devices

- By Application

- Skin Resurfacing & Tightening

- Hair Removal

- Body Contouring & Cellulite Reduction

- Facial Aesthetic Procedures

- Pigmented & Vascular Lesion Treatment

- Others

- By End User

- Dermatology and Asthetic Clinics

- Hospitals & Surgical Centers

- Medical Spas & Beauty Centers

- Home-use

- By Gender

- Female

- Male

- By Age Group

- 18-34 Years

- 35-50 Years

- Above 50 Years

Data Sources, Market Sizing, and Validation

Desk Research

To set the base structure of the market, we start with public data that helps us map procedure activity, healthcare supply, and imports that typically track with device demand. Sources used include ANVISA device registration and regulatory lists, Brazil trade and customs statistics such as Comex Stat, and WHO and World Bank macro and health spending series, along with peer-reviewed dermatology and plastic surgery literature that tracks procedure prevalence and modality shifts.

Once the market logic is built, we cross-check it using company filings and investor materials for portfolios exposed to Brazil, press releases on product launches and approvals, and association websites that comment on clinic adoption. In a few cases, we also used paid subscriptions for company financials and intelligence, and for shipment-level import and export checks to reduce blind spots around cross-border device flows. The sources listed here are illustrative only, and we also used additional public references during validation and clarification.

Primary Interviews and Surveys

For primary work, we spoke with a mix of device distributors, clinic owners, dermatology and aesthetic practitioners, and managers who run procurement and utilization planning. Because Brazil demand varies by city tier and the private care mix, we checked assumptions across major demand pockets and re-tested pricing and utilization trends when responses did not align.

These conversations were used to confirm which device modalities are actively purchased, how often systems are replaced, and how pricing is being negotiated across clinics and channels.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 21% | |

| Mid tier: 43% | Functional/Unit leaders: 29% | |

| Smaller Players: 21% | Managers: 50% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where procedure intensity and clinic capacity signals translate into device demand pools, then gets filtered through modality mix and typical replacement cycles. For Brazil, the model places weight on the installed base of systems in clinics, annual procedure throughput per site, and the share of treatments using energy-based platforms versus non-energy options.

The totals are then corroborated using selective bottom-up approximations, such as sampled ASP times expected unit shipments for key device groups, plus channel checks with distributors on yearly placements. Where primary inputs show gaps, for example home-use volumes that are not tracked consistently, we use conservative penetration assumptions and validate them with retail availability signals and interview feedback.

For forecasting, we run scenario analysis anchored to a short list of drivers practitioners repeatedly referenced, including consumer spend sensitivity, financing availability for clinics, new product approvals and launches, and the pace of technology upgrades in laser, RF, and ultrasound systems. We also keep the outlook tied to observable indicators such as import trends for capital devices and the expected shift toward minimally invasive treatments.

Data Validation & Update Cycle

We validate outputs by comparing model results against independent signals, such as trade flows for device categories, growth comments from public company materials, and practitioner reported utilization changes. When an outlier appears, we re-check the underlying inputs, including the assumptions that drive the change, such as ASP movement or replacement timing, before sign-off.

A multi-step internal review is followed so the calculation logic, scope, and country mapping stay consistent across the time series. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major regulatory changes, notable pricing shifts, or sudden demand swings. Before delivery, a fresh final pass is completed so clients receive the most current view available.

Mordor Intelligence's Brazil Aesthetic Devices Market Size Compared With Other Published Estimates

It is normal to see different market values for Brazil aesthetic devices because publishers do not always count the same product lines, pricing points, or sales channels, and they may also anchor their numbers to different years. Differences also show up when some estimates lean on broad forecasts without checking whether they match what clinics are actually buying and using.

One common gap driver is scope, since some published figures fold in procedure and treatment revenue or widen the definition into general beauty equipment, inflating the total. Some estimates also assume faster ASP increases across capital systems, and they may not re-check those assumptions against distributor pricing and import unit trends. In contrast, service revenue is kept out and only device product value is counted in the model applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 196.89 M (2025) | |

| Industry Publisher A | USD 203.24 M (2025) | This estimate appears to use a slightly wider application list and end-user mapping (including more consumer and regional splits), which can lift totals if home-use and adjacent equipment are counted more broadly. |

| Consultancy B | USD 1.40 B (2024) | This figure likely blends devices with procedure-related revenue and includes non-device aesthetic treatments, and it is anchored to a different base year, which makes the market look much larger than a device-only product valuation. |

Across the three figures, the biggest spread is explained by what is being counted and the year used, not by a simple math difference. Keeping the inputs tied to clinic utilization, replacement timing, and observed price points makes the result easier to trace and repeat, and it also helps users compare growth over time on a like-for-like basis.

Key Questions Answered in the Report

How large is the Brazil aesthetic devices market in 2026?

It was valued at USD 213.51 million in 2026 and is projected to reach USD 345.05 million by 2031 at a 10.08% CAGR.

Which segment is growing fastest in Brazilian body-contouring treatments?

Body-contouring and cellulite-reduction devices are forecast to expand at 14.67% CAGR through 2031, outpacing all other applications.

Why are dentists important buyers of aesthetic devices in Brazil?

Dentists perform 43% of clinic-based procedures and 87% of total injectables, widening the practitioner base and accelerating equipment adoption.

How is macroeconomic volatility affecting device sales?

High SELIC rates, a weaker real, and slower GDP growth are raising financing costs and suppressing discretionary spending, cutting 2.0 percentage points from near-term CAGR.

What regulatory change is most influential for new device launches?

ANVISA’s RDC 751/2022 fast-track pathway shortens approval times by referencing FDA and CE dossiers, adding 1.5 percentage points to market CAGR in the short term.

Which companies recently made strategic moves in Brazil?

Classys bought 77.5% of JL Health to launch Shurink Universe HIFU, while Hugel partnered with Derma Dream to roll out Letybo botulinum toxin.

Page last updated on: