Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.25 Billion |

| Market Size (2026) | USD 2.38 Billion |

| Market Size (2031) | USD 3.12 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

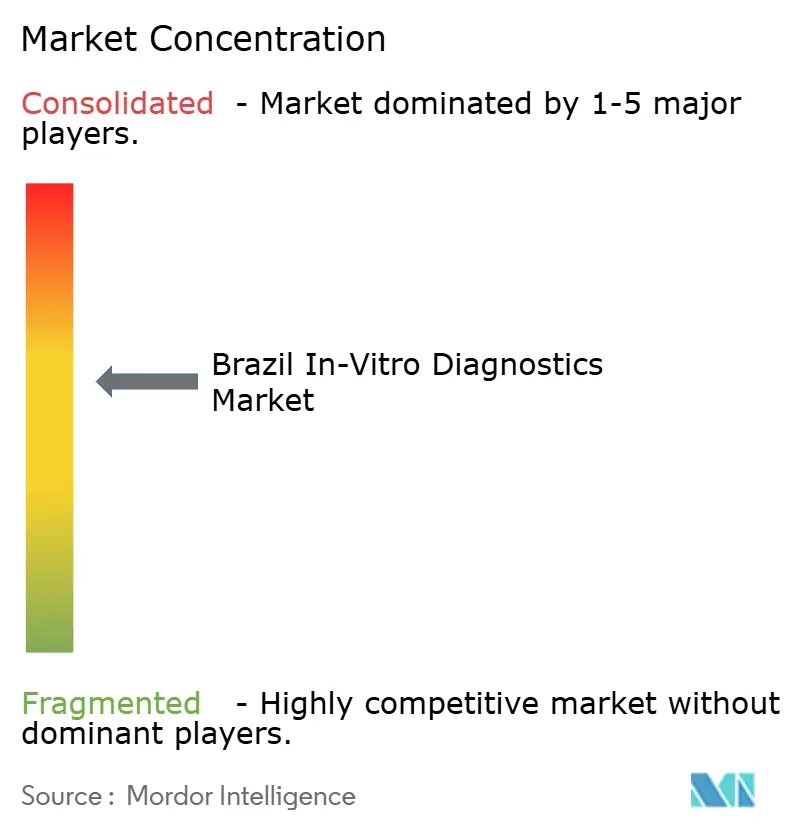

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil In-Vitro Diagnostics Market Analysis by Mordor Intelligence

The Brazil IVD market size was valued at USD 2.25 billion in 2025 and estimated to grow from USD 2.38 billion in 2026 to reach USD 3.12 billion by 2031, at a CAGR of 5.62% during the forecast period (2026-2031). Rising demand stems from an aging population of more than 32 million people over 60 years, expanded public-sector funding through the Sistema Único de Saúde, and ANVISA’s 2024-2025 regulatory agenda that prioritizes faster pathways for innovative diagnostics. Investments in point-of-care (POC) infrastructure, telehealth integration, tier-2-city insurance penetration, and local reagent manufacturing further reinforce growth prospects. Competitive momentum intensifies as laboratories consolidate, device makers on-shore production to offset currency risk, and software vendors embed artificial intelligence into test workflows. Collectively, these forces position the Brazil IVD market for sustained mid-single-digit expansion through the decade.

Key Report Takeaways

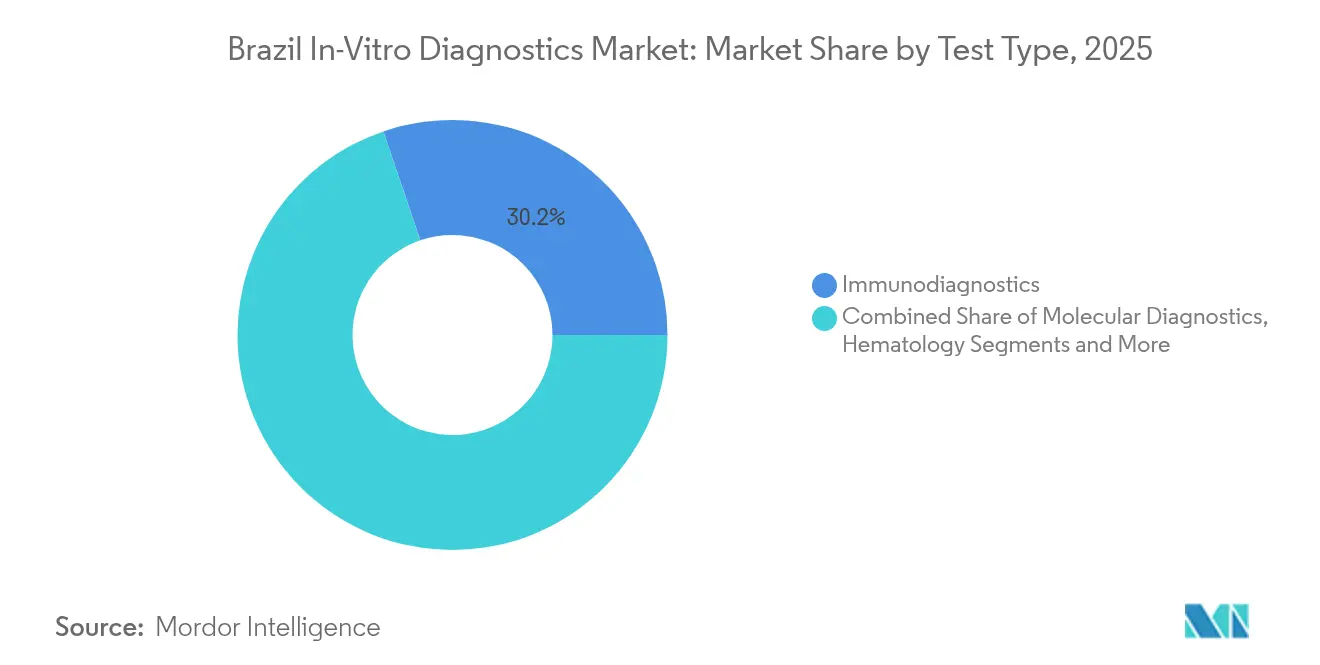

- By test type, immunodiagnostics held 30.21% of Brazil IVD market share in 2025 while molecular diagnostics is advancing at a 12.02% CAGR to 2031.

- By product, reagents and kits accounted for 55.05% of the Brazil IVD market size in 2025; software and services register the highest projected growth at 11.15% CAGR through 2031.

- By usability, disposable devices led with 64.10% revenue share in 2025, whereas reusable devices are expanding at a 8.95% CAGR over the forecast window.

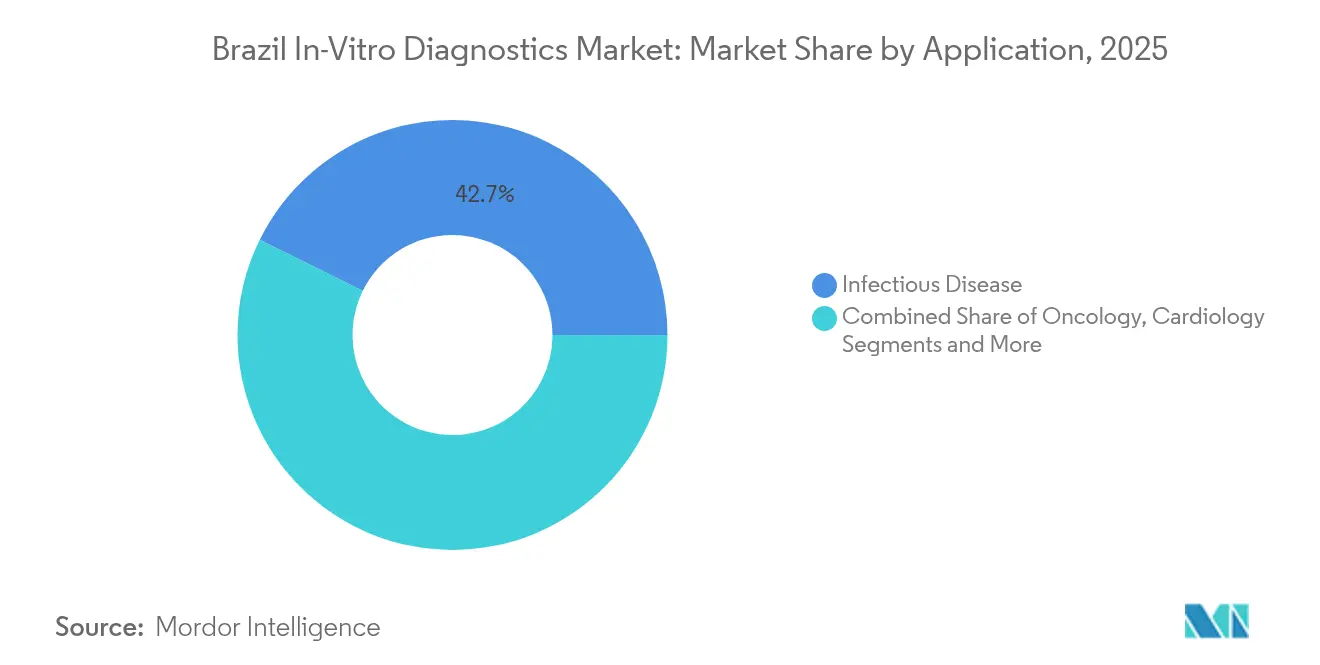

- By application, infectious-disease testing commanded 42.70% share of the Brazil IVD market size in 2025, and oncology testing shows the fastest trajectory at 11.88% CAGR to 2031.

- By end user, diagnostic laboratories represented 53.70% share in 2025, while home-care and self-testing are growing at 13.10% CAGR amid telemedicine adoption.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of chronic & lifestyle diseases | +1.8% | National; higher in Southeast & South | Long term (≥ 4 years) |

| Growing adoption of point-of-care diagnostics | +1.2% | Rural areas & tier-2 cities | Medium term (2-4 years) |

| Expansion of private health-insurance in tier-2 cities | +0.9% | Minas Gerais & interior São Paulo | Medium term (2-4 years) |

| Telehealth-linked sample-collection kiosks | +0.7% | Amazon, Northeast, Center-West | Long term (≥ 4 years) |

| Local manufacturing of low-cost reagents | +0.6% | São Paulo & Rio de Janeiro hubs | Short term (≤ 2 years) |

| Aging population & SUS reimbursement reforms | +1.1% | National; strongest in South & Southeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Prevalence Of Chronic & Lifestyle Diseases

Brazil’s epidemiological transition toward obesity, diabetes, and cardiovascular disorders drives sustained use of immunodiagnostics and clinical-chemistry assays. Point-of-care HbA1c testing in primary care delivers cost-effective monitoring and shortens result times from weeks to minutes. SUS reimbursement reforms embedded in the Previne Brasil model reward early detection, enlarging the test volume eligible for public funding. The Brasil Saudável program’s plan to eliminate 14 neglected diseases requires expanded laboratory capacity for serological and molecular screening. Cardiovascular disease affecting more than 14 million residents fuels demand for high-sensitivity troponin and natriuretic-peptide platforms. Together, these factors add 1.8 percentage points to the Brazil IVD market CAGR.

Growing Adoption Of Point-Of-Care (POC) Diagnostics

Infrastructure constraints across Brazil’s 5,570 municipalities make rapid testing essential for timely care. Field studies in Vitória da Conquista show POC-A1c devices achieving 90% accuracy versus central labs while lowering patient travel costs. In the Amazon, POC syphilis tests record 95% sensitivity and 100% specificity, replacing multi-day laboratory logistics. ANVISA’s streamlined rules under RDC 751 and its 2024-2025 software-cybersecurity agenda accelerate market entry for connected POC devices. Rural programs leverage POC kits to compensate for technician shortages, as only 29% of states meet minimum lab standards. The aggregate impact lifts the CAGR by 1.2 percentage points.

Rapid Expansion Of Private Health-Insurance Coverage In Tier-2 Brazilian Cities

New insurance enrollment of 957,197 beneficiaries in 2023 raised total covered lives to 51 million, expanding demand for reimbursed diagnostics outside major metros. Hapvida’s USD 74 million hospital build-out in Rio de Janeiro illustrates operators’ pivot toward interior growth corridors. Regulatory floor requirements oblige insurers to cover broad diagnostic panels, ensuring test utilization in emerging middle-income cities. Job creation of 1.9 million formal positions in 2023 enhances affordability, although penetration among the poorest quintile remains under 6%. Insurance-driven utilization contributes 0.9 percentage points to overall CAGR.

Telehealth-Linked Sample-Collection Kiosks In Rural Areas

Brazil’s UBS+Digital project logged 6,300 telehealth sessions in 2023 with 85% case-resolution rates, demonstrating scalable remote diagnostics[1]Celina de Almeida Lamas et al., “Telehealth Initiative to Enhance Primary Care Access in Brazil,” Journal of Medical Internet Research, JMIR.ORG. Tele-ICU services in northern states delivered 3,971 virtual rounds for 5,471 patients, linking specialists to remote hospitals. ANVISA’s telemedicine framework authorizes certified professionals to supervise remote specimen collection while maintaining chain-of-custody. Private 5G pilots such as OpenCare5G at Hospital das Clínicas enable real-time imaging uploads and rapid pathology consultations. Collectively, kiosks and mobile units add 0.7 percentage points to forecast growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent ANVISA approval timelines | -0.8% | National | Short term (≤ 2 years) |

| High import tariffs on IVD instruments | -1.1% | National; larger hit on small labs | Medium term (2-4 years) |

| Fragmented public-sector procurement & delayed payments | -0.7% | SUS-dependent regions | Long term (≥ 4 years) |

| Shortage of skilled molecular-lab technicians outside Southeast | -0.9% | North, Northeast, Center-West | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent ANVISA Approval Timelines

Class III and IV devices can face 12-18-month registration windows, challenging rapid product launches. ANVISA’s 2024 legislation allowing reliance on FDA and Health Canada clearances should reduce duplication, yet compliance with Portuguese labeling and cybersecurity files still extends preparation cycles[2]Emergo by UL, “Brazil ANVISA Legislation Allows Leveraging Regulatory Authorizations,” EMERGOBYUL.COM. While a pilot for innovative devices drew 100 applicants, capacity limits persist, especially for molecular technologies needing bioinformatics validation. The resulting drag subtracts 0.8 percentage points from the Brazil IVD market CAGR.

High Import Tariffs On IVD Instruments

Shipments valued above USD 50 incur 60% duty plus ICMS state tax calculated on freight-inclusive customs value. INMETRO and ANATEL certifications add time and cost for wireless analyzers. Although the Mercosur waiver for capital goods runs through 2028, domestic lobbies can trigger reviews, sustaining uncertainty. Combined fiscal pressures shave 1.1 percentage points off growth, especially for smaller independent laboratories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Diagnostics Drives Innovation

Immunodiagnostics retained 30.21% Brazil IVD market share in 2025 thanks to high-volume infectious-disease and cardiac biomarker panels. Molecular diagnostics, boosted by COVID-19 infrastructure and precision oncology, is expected to post a 12.02% CAGR through 2031, the fastest within the Brazil IVD market. Oncology sequencing and antimicrobial-resistance panels anchor demand, yet per-run costs average USD 3,500, challenging wider diffusion. Government approval of homologous recombination deficiency testing for ovarian-cancer therapy selection underscores policy support for genomics. Platform vendors partner with public hospitals to broaden access, while ANVISA’s reliance agreements speed assay clearance. Continued reagent cost declines and cloud-based bioinformatics are set to expand molecular adoption beyond tertiary centers by the decade’s end.

By Product: Software Integration Accelerates

Reagents and kits produced 55.05% of the Brazil IVD market size in 2025, reflecting consumable-driven revenue streams across laboratory and POC settings. However, software and services are advancing at 11.15% CAGR as laboratories overhaul information systems to meet telehealth data-exchange mandates and cybersecurity rules. AI-enabled quality-control modules reduce error flags by up to 30% in pilot SUS facilities. DASA’s Nav Pro portal allows clinicians to visualize longitudinal test results, lifting portal login rates five-fold in 2025. Meanwhile, instrument upgrades hinge on flexible reagent rentals to manage capital constraints. Vendors bundling middleware analytics with reagents secure stickier contracts and unlock incremental margin pools.

By Usability: Sustainability Drives Reusable Growth

Disposable formats commanded 64.10% share in 2025 after pandemic-triggered infection-control protocols boosted rapid-test purchases. As pandemic volumes normalize, reusable analyzers are projected to rise 8.95% CAGR through 2031, underpinned by waste-reduction policies and lifecycle-cost calculations. ANVISA’s 2024 risk-based reprocessing rules permit sterilization of selected single-use devices, lowering consumable spend for high-volume laboratories. Public hospitals evaluating green-procurement criteria now weight disposal cost at 10% of tender scoring. Vendors offering take-back programs and recyclable cartridges gain traction, balancing safety with environmental stewardship.

By Application: Oncology Testing Transformation

Infectious-disease assays held 42.70% share of Brazil IVD market size in 2025, fueled by HIV, dengue, and COVID-19 surveillance. Oncology panels are the fastest riser, predicted to advance 11.88% CAGR as precision therapies demand companion diagnostics. National Cancer Institute forecasts a 74.5% jump in new cases by 2050, necessitating biomarker stratification at earlier stages. Public insurance now reimburses PD-L1 and HRD testing, accelerating uptake beyond private networks. Meanwhile, diabetes and cardiology panels benefit from integrated POC meters in primary care. Autoimmune and nephrology tests expand gradually as clinical pathways embed algorithm-based reflex testing.

By End User: Home Testing Revolution

Diagnostic laboratories generated 53.70% of 2025 revenue, but home-care and self-testing channels are expanding 13.10% CAGR on the back of regulatory clearance for OTC assays and teleconsult follow-up workflows. Conexa’s platform handled 1.25 million virtual encounters in 2024, with 40% including lab orders fulfilled via at-home collection kits. Retail pharmacies pilot kiosk-based COVID-19, pregnancy, and cholesterol testing, cutting wait times to under 15 minutes. Hospital networks integrate bedside POC blood gas analyzers to streamline emergency care. Academic institutes continue to drive assay validation studies, feeding innovation pipelines for commercial launch.

Geography Analysis

Southeast Brazil accounts for 82% of diagnostic procedures despite housing only 42% of the population, underpinned by dense private-insurance coverage and concentrated laboratory groups such as DASA and Fleury. São Paulo alone processes one-third of national test volumes through 200-plus collection centers and high-throughput core labs. Rio de Janeiro’s pipeline of new hospitals, including Hapvida’s 250-bed unit, will deepen regional dominance and widen network referral opportunities.

Northeast and North regions register lower physician ratios but show strong upside due to telehealth and mobile-kiosk deployments. Tele-ICU programs in Pará and Maranhão achieved 70% case-resolution without patient transfers, validating remote-interpretation models for hematology and imaging. Amazon river municipalities rely on rapid tests for malaria and leptospirosis, where logistics preclude central-lab processing. Center-West agribusiness wealth boosts private-clinic expansion in Goiânia and Cuiabá, attracting vendors of molecular panels for zoonotic-disease surveillance. The South maintains robust infrastructure and the country’s highest per-capita private-insurance enrollment, sustaining steady demand for chronic-disease monitoring. Collectively, geographic diversification into tier-2 cities where private coverage added nearly 1 million lives in 2023 underpins future growth.

Competitive Landscape

Global majors Danaher, Roche, and Siemens Healthineers compete with domestic champions DASA and Fleury in a moderately consolidated field. DASA’s merger with Amil’s hospital assets created a USD 1.84 billion revenue platform spanning 4,400 beds, enabling bundled diagnostic-plus-care contracts with insurers. Fleury’s reported talks with Rede D’Or signal further vertical integration to capture inpatient-testing flows.

Technology capabilities differentiate players: Roche’s acquisition of LumiraDx’s microfluidics enhances its POC menu, while Abbott leverages continuous glucose-monitor data to cross-sell lab services[3]Abbott, “Second-Quarter 2025 Results,” ABBOTT.MEDIAROOM.COM. Domestic startups emphasize software; Conexa’s AI triage reduces unnecessary lab orders by 15%, improving payer acceptance.

White-space potential lies in low-penetration regions and oncology genomics. International entrants partner with local distributors to navigate ANVISA requirements, whereas Brazilian reagent manufacturers gain share under currency depreciation.

Brazil In-Vitro Diagnostics Industry Leaders

bioMérieux

Becton, Dickinson and Company

Bio-Rad Laboratories Inc.

Roche Diagnostics

Danaher Corp. (Beckman Coulter & Cepheid)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Hapvida unveiled a USD 74 million expansion plan in Rio de Janeiro comprising a 250-bed hospital and urgent-care centers.

- June 2025: ANVISA launched the Siud unique-device-identification system to enhance traceability of all medical devices nationwide.

Brazil In-Vitro Diagnostics Market Report Scope

As per the scope of the report, in vitro diagnostics involve medical devices and consumables that are utilized to perform in vitro tests on various biological samples. They are used for the diagnosis of various medical conditions, such as chronic diseases. In the report, a detailed analysis of the in vitro diagnostics market is presented, with specific attention toward diabetes and thalassemia. Brazil in vitro diagnostics market is segmented by test type (clinical chemistry, molecular diagnostics, immunodiagnostics, hematology, and other test types), product (instrument, reagent, and other products), usability (disposable IVD devices and reusable IVD devices), application (infectious disease, diabetes, cancer/oncology, cardiology, autoimmune disease, nephrology, and other applications), and end user (diagnostic laboratories, hospitals and clinics, and other end users). The report offers the value (in USD million) for the above segments.

By Test Type

| Clinical Chemistry |

| Molecular Diagnostics |

| Immunodiagnostics |

| Hematology |

| Microbiology & Virology |

| Coagulation |

| Point-of-Care Testing |

| Others |

By Product

| Instruments |

| Reagents & Kits |

| Software & Services |

By Usability

| Disposable IVD Devices |

| Reusable IVD Devices |

By Application

| Infectious Disease |

| Diabetes |

| Oncology |

| Cardiology |

| Autoimmune Disease |

| Nephrology |

| Rare Genetic Disorders |

| Others |

By End User

| Diagnostic Laboratories |

| Hospitals & Clinics |

| Home-care & Self-testing |

| Academic & Research Institutes |

| Others |

| By Test Type | Clinical Chemistry |

| Molecular Diagnostics | |

| Immunodiagnostics | |

| Hematology | |

| Microbiology & Virology | |

| Coagulation | |

| Point-of-Care Testing | |

| Others | |

| By Product | Instruments |

| Reagents & Kits | |

| Software & Services | |

| By Usability | Disposable IVD Devices |

| Reusable IVD Devices | |

| By Application | Infectious Disease |

| Diabetes | |

| Oncology | |

| Cardiology | |

| Autoimmune Disease | |

| Nephrology | |

| Rare Genetic Disorders | |

| Others | |

| By End User | Diagnostic Laboratories |

| Hospitals & Clinics | |

| Home-care & Self-testing | |

| Academic & Research Institutes | |

| Others |

Key Questions Answered in the Report

What is the projected value of the Brazil IVD market in 2031?

The market is forecast to reach USD 3.12 billion by 2031 at a 5.62% CAGR.

Which test type is growing fastest within Brazil's diagnostics space?

Molecular diagnostics is projected to grow 12.02% annually, driven by precision oncology and infectious-disease surveillance.

How dominant are reagents and kits in overall revenue?

Reagents and kits represented 55.05% of 2025 revenue, making them the largest product category.

Why are tier-2 cities important for diagnostic providers?

Private health-insurance enrollment in interior cities rose by 957,197 lives in 2023, creating fresh demand for reimbursed testing services.

What regulatory change may shorten device approvals?

ANVISA's 2024 rule permitting reliance on FDA and Health Canada clearances can reduce Class III and IV approval times.

How fast is the home-care and self-testing segment expanding?

Home-based testing is growing 13.10% annually, fueled by telemedicine and OTC assay approvals.

Page last updated on: