Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

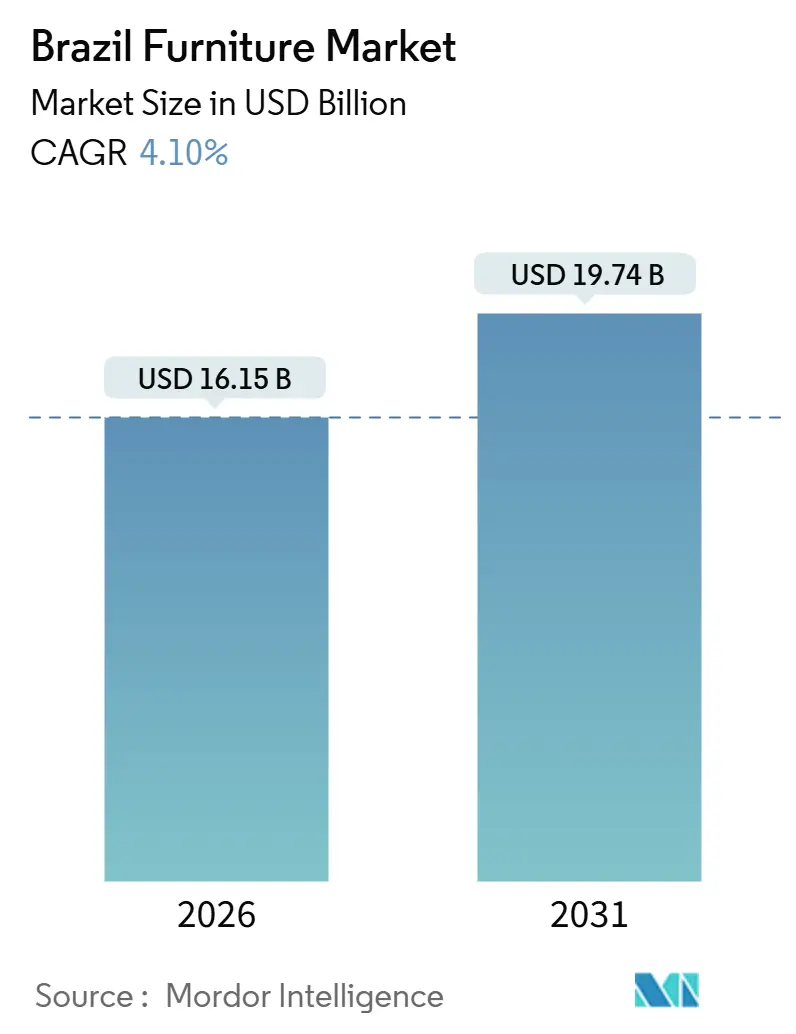

| Market Size (2026) | USD 16.15 Billion |

| Market Size (2031) | USD 19.74 Billion |

| Growth Rate (2026 - 2031) | 4.10% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Brazil Furniture Market Analysis by Mordor Intelligence

The Brazil furniture market size reached USD 16.15 billion in 2026 and is projected to reach USD 19.74 billion by 2031, expanding at a 4.10% CAGR. The Brazil furniture market is experiencing steady growth, driven by a combination of strategic shifts and evolving consumer demand. Companies are increasingly focusing on value-chain efficiency and optimizing their product mix, reflecting a shift from competing on volume to competing on price realization, margin protection, and selective promotional strategies. The sector is also adapting to changes in pricing, certification, and fulfillment models following a period of market volatility, which is helping businesses strengthen operational resilience. Export opportunities are expanding, particularly toward Europe and within Mercosur countries, as Brazilian manufacturers prepare to take advantage of anticipated tariff-free access under the Europe-Mercosur trade framework. This is placing greater emphasis on traceability, quality standards, and alignment with international market requirements, boosting the competitiveness of Brazilian furniture abroad. On the domestic front, demand is supported by government housing programs that create consistent orders for entry-level cabinetry, modular kitchens, and bedroom furnishings targeted at lower to middle-income consumers. As financing conditions improve, there is potential for households to resume deferred purchases of higher-value furniture items, further supporting market expansion.

Key Report Takeaways

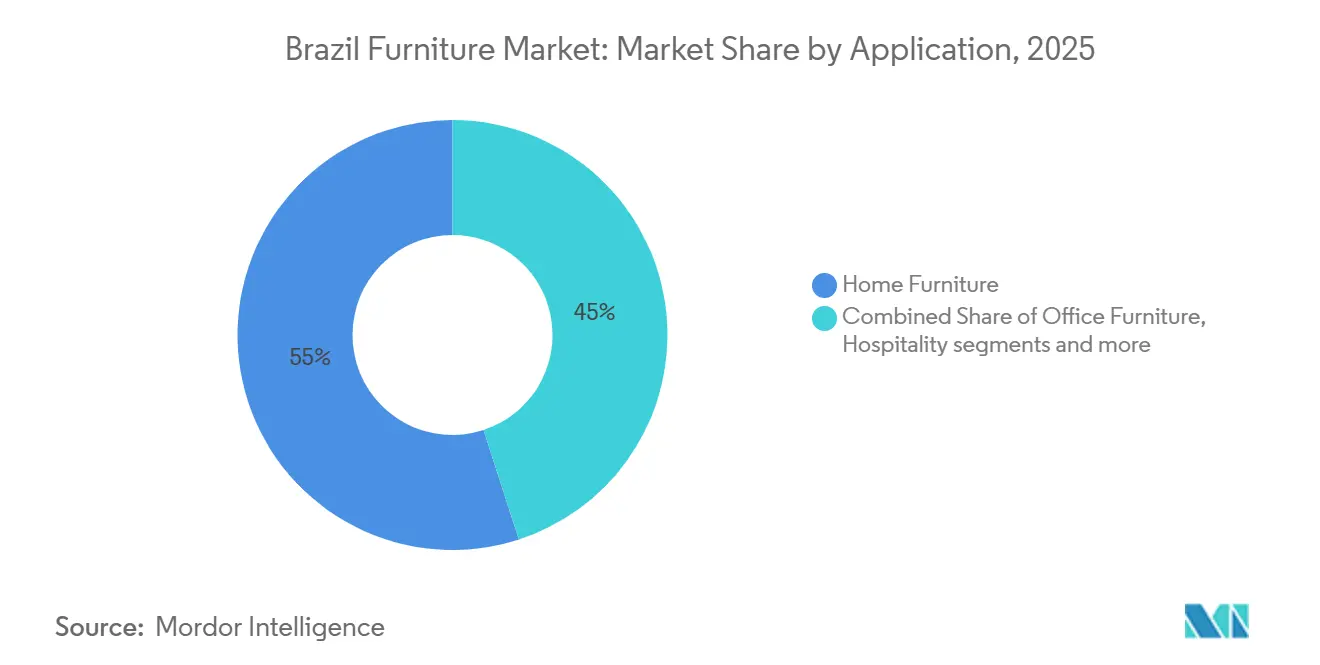

- By application, home furniture led with 55.0% of the Brazil furniture market share in 2025. Healthcare furniture is projected to expand at a 5.66% CAGR through 2031.

- By material, wood retained 62.0% of the Brazil furniture market share in 2025. Plastic and polymer are projected to grow at a 4.94% CAGR through 2031.

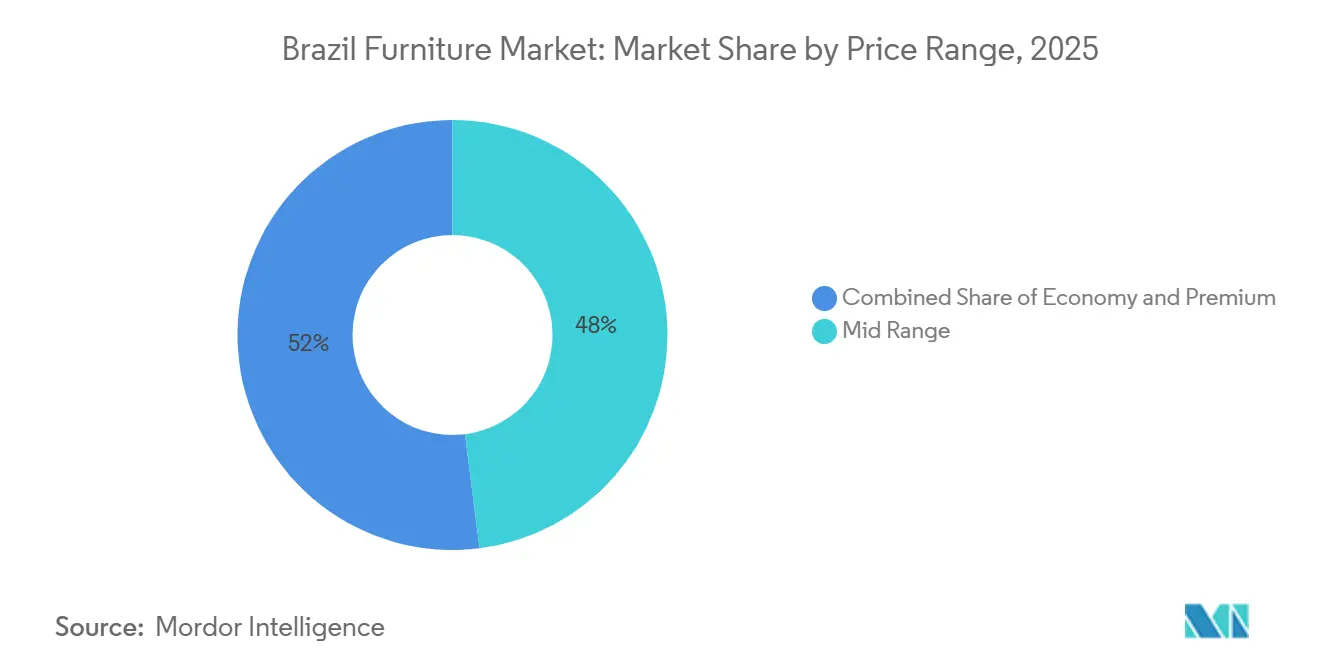

- By price range, mid-range held 48.0% of the Brazil furniture market share in 2025. The premium tier is projected to advance at a 4.61% CAGR through 2031.

- By distribution channel, B2C or retail accounted for 75.0% of the Brazil furniture market share in 2025. Online channels within B2C are projected to grow at a 7.36% CAGR through 2031.

- By geography, Southeast Brazil captured 47.0% of the Brazil furniture market share in 2025. The North is projected to be the fastest-growing region at a 4.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce penetration beyond Tier-1 cities | +0.9% | National, with early gains in São Paulo, Paraná, and Northeast capitals | Medium term (2-4 years) |

| Growing middle-class credit access | +0.7% | Concentrated in Southeast/South; spillover to the Midwest | Short term (≤ 2 years) |

| Government-backed housing stimulus (Minha Casa Minha Vida) | +0.5% | National, highest impact in Southeast/Northeast Faixa 1-3 zones | Medium term (2-4 years) |

| ESG-driven certified-wood demand (FSC, PEFC) | +0.3% | Export-oriented and domestic premium clusters in large metros | Long term (≥ 4 years) |

| Furniture-subscription and leasing platforms | +0.2% | Primarily Southeast metros; pilot expansion in the South | Long term (≥ 4 years) |

| Digital-twin enabled mass-customization | +0.1% | High-income urban centers; limited SME adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce Penetration Beyond Tier-1 Cities Unlocks Latent Rural Demand

Online expansion in the Brazil furniture market is widening beyond major metros as marketplaces and sellers build assortments for interior municipalities and reduce delivery friction for bulky goods. Platforms are standardizing catalogs, tightening delivery windows in high-density corridors, and aligning inventory with regional preferences to improve conversion and repeat rates. As channel strategies mature, physical showrooms provide touchpoints for high-consideration categories while digital funnels capture traffic and close sales. Retail calendar effects remain material, with national statistics showing peaks and troughs around promotional moments that pull demand across months. Industry updates confirm that production volumes did not keep pace with nominal revenue in late 2025, which signals continued optimization of pricing, logistics, and assortment as e-commerce deepens into underserved locations in the Brazil furniture market.

Growing Middle-Class Credit Access Fuels Installment-Driven Consumption

The Brazil furniture market is increasingly shaped by household access to consumer credit. Brazil’s official data show that household credit has risen steadily and reached record levels by late 2025, totaling over USD 688 billion at the end of 2024. This expansion enables middle-income consumers to use multi-month installment plans for higher ticket items such as kitchens, wardrobes, and bundled furniture packages.[1]Source: Central Bank of Brazil, “Household Credit", TheGlobalEconomy.com Elevated borrowing costs and household delinquency constrained purchases in late 2025, prompting consumers to prioritize essential replacements over full-room sets. As financing conditions ease in 2026, affordability for installment purchases is expected to improve, supporting a gradual rebound in average ticket sizes. Production and sales data highlight the cyclical nature of demand, with early-year gains giving way to slower activity aligned with tighter credit. Retailers are balancing accessible price points with margin discipline to capture demand as deferred purchases are released.

Government-Backed Housing Stimulus Drives Entry-Tier Furniture Demand

The Minha Casa Minha Vida housing program has been a key driver of baseline demand for entry-level cabinetry, modular kitchens, and bedroom furniture by supporting household formation among lower-income and emerging middle-class families. By the end of 2024, the program had contracted over 1.26 million housing units, exceeded its original targets, and highlighted strong participation from its intended beneficiaries. The program prioritizes ready-to-occupy housing, which encourages the purchase of essential furniture items rather than luxury or custom pieces, shaping the product mix toward modular, space-efficient solutions.[2]Source: Central Government of Brazil, Minha Casa Minha Vida 2024 contracts, Agência Gov. Flexible financing and subsidies embedded in the program increase affordability for lower-income buyers, enabling them to gradually furnish their new homes using installment-based purchases, which aligns with the broader trend of credit-driven consumption in Brazil. Beneficiaries typically sequence furniture purchases over time, first acquiring essential items at move-in and later upgrading or replacing pieces as household budgets allow, supporting repeat sales and aftermarket demand.

ESG-Driven Certified-Wood Demand Repositions Brazil in Premium Export Tiers

Rising regulatory and buyer expectations in Europe are increasing the value of certified and traceable timber, reshaping both export strategies and premium domestic furniture lines. Brazil has recently updated and strengthened national forestry standards to support sustainable forest management and certified timber production, which underpins traceability and environmental credibility in global supply chains. The Forest Stewardship Council’s new national standard for natural forests, developed through public consultation and field testing, came into effect in October 2025, promoting responsible forest practices, biodiversity conservation, and stronger rights protections for local communities. [3]Source: Forest Stewardship Council, New FSC Forest Stewardship Standard for Natural Forests in Brazil Updated standards strengthen low-impact logging practices and community protections, raising the bar for verified supply chains and sustainable sourcing. Anticipated trade frameworks, such as the EU-Mercosur agreement, further emphasize sustainability by prioritizing deforestation-free materials and reliable audit trails, which can reduce barriers for compliant Brazilian exporters. Industry programs have equipped manufacturers with ESG diagnostics, carbon accounting aligned with global protocols, and certification checklists to accelerate compliance, enabling faster market access and improving competitiveness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High logistics costs in the North and the Center-West | -0.6% | North and Center-West states; limited infrastructure corridors | Short term (≤ 2 years) |

| Exchange-rate volatility on imported inputs | -0.5% | National exposure for machinery and hardware imports; export competitiveness | Short term (≤ 2 years) |

| Skilled labor shortage in customized joinery | -0.3% | Hubs in Paraná, Santa Catarina, Rio Grande do Sul | Medium term (2-4 years) |

| Tighter formaldehyde-emission regulations | -0.2% | National production; compliance costs for MDF and particleboard | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Logistics Costs in North and Central-West Erode Retailer Margins

Delivery costs for bulky furniture remain structurally high in regions with sparse warehousing and long transportation routes, particularly in the North and the Center-West. Retailers targeting price-sensitive households face margin pressure when freight expenses consume a significant portion of transaction value, limiting the adoption of higher-ticket items. Late 2025 production data and industry reporting highlight how rising distribution costs and logistical constraints impacted inventory planning and throughput. In response, the Brazil furniture market is implementing micro-fulfillment centers, route optimization, and tighter product assortments to protect service levels and reduce return costs. Sellers are also experimenting with hybrid operating models that combine marketplace exposure with localized pickup or scheduled delivery to maintain customer experience while controlling expenses. These strategies are increasingly critical as redirected export capacity intensifies competition in domestic channels and emphasizes the need for precise, efficient supply chain management.

Exchange-Rate Volatility on Imported Inputs Compresses Manufacturer Profitability

Manufacturers dependent on imported machinery, hardware, and chemical inputs face planning and cost challenges when currency fluctuations alter landed costs and complicate pricing. While higher export receipts in 2024 partially offset these pressures, they were insufficient to fully support investment in automation and capacity upgrades. Companies that diversify sourcing within Mercosur can mitigate long lead times, hedge some currency risk, and align with emerging Europe-Mercosur trade opportunities. Larger multinational players leverage steady execution in contract channels to buffer consumer-facing segments from foreign exchange volatility. Improved visibility on policy rates and FX bands is expected to enhance planning certainty, allowing manufacturers to unlock deferred capital expenditures for productivity and certification initiatives. These investments in efficiency and compliance expand the addressable market for Brazilian furniture, particularly in export-oriented and higher-value segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Planned Furniture Pivots from Premium to Functional Necessity

Home furniture accounted for 55.0% in 2025, anchoring the Brazil furniture market share at the application level with planned and modular solutions moving beyond upper-income niches. Momentum in fitted cabinetry and compact storage reflects a growing focus on functional, space-optimized designs that enhance everyday utility. Healthcare furniture is emerging as a rapidly expanding application, driven by demand for durable, certified materials in hospitals and clinics. Contract segments, including office and hospitality, show mixed growth, with corporate projects progressing gradually while small businesses adopt modular workstations for hybrid work setups.

The market is aligning product assortments with these trends by prioritizing configurable systems that meet safety and durability standards while ensuring reliable delivery. Aftermarket dynamics complement new-home purchases, as subsidized housing beneficiaries gradually complete rooms and upgrade key pieces as finances allow. Retailers are optimizing product ladders for standardized layouts in affordable housing and emphasizing installation simplicity to control service costs. Overall, improving consumer credit conditions are expected to support steadier demand for planned kitchens, storage-heavy furniture, and installment-friendly categories, strengthening both domestic consumption and structured delivery models.

By Material: Wood Retains Dominance as Low-Emission MDF Gains Premium Traction

Wood remained the largest material category with a 62.0% share in 2025, supported by robust panel capacity and deep forestry resources that underpin the Brazil furniture market. Engineered panels such as MDF and particleboard continue to serve as the backbone for configurable and flat-pack formats that improve logistics efficiency for nationwide distribution. Industry programs emphasize sustainability and certification readiness, which guide resin selection, finishing, and sourcing aligned to global buyer requirements. Plastic and polymer are projected to be the fastest-growing materials at a 4.94% CAGR through 2031, especially in categories that value durability, cleanability, and weight advantages. Export-facing producers are also reinforcing certified wood chains to comply with European sustainability rules while protecting access to premium channels in the Brazil furniture market.

Evolving expectations for verified sourcing and environmental performance continue to favor FSC and other recognized certification labels, which simplify compliance audits and retailer onboarding. Industry initiatives provide manufacturers with diagnostics, carbon accounting tools, and structured checklists to accelerate the certification process recognized by international buyers. As these capabilities extend from larger exporters to mid-sized suppliers, the Brazil furniture market is positioned to broaden its reach in regulated export destinations and increase the share of eco-labeled assortments in the domestic market. Advances in panel chemistry and finishing systems support this transition while maintaining cost competitiveness. Together, material innovation and rigorous chain-of-custody practices are becoming central to long-term strategic positioning in both export markets and premium local segments.

By Price Range: Mid-Range Compression Drives Polarization Toward Budget and Premium

Mid-range accounted for 48.0% in 2025, and it remains the largest price band even as households adjusted purchases under tighter credit in late 2025 in the Brazil furniture market. The premium tier is projected to grow at a 4.61% CAGR through 2031 as higher-income cohorts continue to prioritize quality, durability, and certified materials. Promotional cycles in the national retail calendar shift demand across months more than they expand the total wallet, which points to the importance of timing and disciplined inventory planning. Industry reporting shows unit softness in late 2025 despite nominal revenue growth, which indicates ticket values were supported by pricing actions and targeted discounts rather than broad volume gains. As financing costs decline in 2026, retailers expect an improved backdrop for mid-range recovery in planned kitchens, bedroom sets, and living room anchors in the Brazil furniture market.

Premium assortments rely on eco-labeled woods, enhanced ergonomics, and modularity that fit compact urban spaces with minimal waste, thereby sustaining differentiation and resale value. Certification roadmaps from industry programs help brands substantiate claims that resonate with higher-income buyers in large metros. Budget ranges remain sensitive to freight and last-mile costs, which require lean packaging and standardized SKUs to control delivery expenses without reducing perceived value. Retailers are trimming long-tail assortments and improving vendor-managed inventory to stabilize stock turns across price bands. As conditions improve, the Brazil furniture market should display steadier distribution of spend across budget, mid-range, and premium tiers while maintaining a stronger link between financing, fulfillment, and value perception.

By Distribution Channel: Marketplace Aggregation Reshapes B2C Competitive Dynamics

B2C or retail channels accounted for 75.0% in 2025, and online subchannels within B2C are projected to grow at a 7.36% CAGR through 2031 as convenience and assortment deepen in the Brazil furniture market. Sellers continue to integrate online discovery with showroom validation for high-consideration purchases while streamlining pickup and scheduled delivery to manage bulky items at scale. National retail patterns show how promotions can reallocate demand between months, which supports calendar-driven strategies for major categories. Project channels in office, hospitality, and healthcare maintain longer cycles and different margin structures, and multinational filings indicate stable service to Latin America clients that include Brazil. These attributes make B2C the principal arena for share battles while projects supply a predictable base of orders in contract-grade segments.

Compliance capabilities remain a differentiator in safety-critical categories, since reliable testing and certification reduce the risk of delays and returns for multi-seller marketplaces. Association programs that codify ESG and quality requirements are helping smaller firms document processes that satisfy buyer due diligence. Retailers are also improving packaging, routing, and delivery coordination to reduce damage in transit and to preserve NPS at scale. As these operating disciplines spread, the Brazil furniture market will maintain a hybrid model with online-led growth, targeted showroom support, and a steady project pipeline that absorbs specialized capacity. Inventory visibility and fulfillment speed will be critical to margin integrity in this environment.

Geography Analysis

Southeast Brazil accounted for 47.0% of furniture consumption in 2025, reinforcing its position as the country’s main market and production base. Large urban centers, mature distribution networks, and strong retail density continue to drive demand across categories. Production clusters in the South complement this demand by supplying the national market through well-established wood-furniture hubs. These clusters benefit from skilled labor and dense supplier ecosystems built over decades. Together, scale, logistics, and access to certified inputs support premium and export-oriented furniture lines.

In late 2025, furniture unit sales declined even as nominal revenues increased, reflecting inflation effects, cautious discounting, and uneven regional demand. Manufacturers responded by adjusting production schedules, demonstrating flexibility amid tighter credit and softer consumption. As financing conditions normalize in 2026, demand in the Southeast is expected to stabilize. More predictable order cycles should emerge across residential and contract categories. This environment favors disciplined inventory management and value-driven pricing strategies.

The South remains a strategic export platform as manufacturers diversify shipments toward Europe and neighboring regional markets. In the Northeast, housing programs such as Minha Casa Minha Vida sustain demand for essential, standardized furniture focused on durability and ease of installation. Retailers in the region emphasize compact, value-oriented products to manage logistics and affordability. The North is projected to be the fastest-growing region at a 4.82% CAGR through 2031, supported by logistics improvements and digital marketplace expansion. Meanwhile, Center-West demand is shaped by institutional and public-sector purchases, reinforcing a more balanced and export-ready Brazilian furniture market.

Competitive Landscape

The Brazil furniture market remains highly fragmented, with numerous manufacturers and retailers competing across diverse price points and channels. Recent industry trends show that while unit volumes moderated, revenue gains suggest companies relied on disciplined pricing and targeted promotions to protect margins. National retail data reflect month-to-month variability, particularly around promotion-driven periods that influence purchase timing in categories requiring longer consideration. Export-oriented firms are preparing for Europe-Mercosur access by investing in certification, traceability, and chain-of-custody processes aligned with European standards. Industry initiatives are helping close capability gaps, equipping more companies to compete effectively in premium export channels.

Two strategic moves highlight how scale and compliance shape competitive advantage in the Brazil furniture market. Structured buyer programs connecting vetted manufacturers with international purchasers have strengthened export relationships and improved order visibility. Multinational companies with diversified product portfolios maintain steady activity in Latin America, especially in contract segments that demand certified materials and robust service networks. These developments underscore the importance of integrating compliance, logistics, and financing to deliver a cohesive value proposition. Companies that can combine these capabilities across price tiers are best positioned to capture market share.

Association and government agendas continue to reinforce quality, safety, and sustainability standards, which favor producers with reliable testing infrastructure and documented processes. Firms are leveraging the Europe-Mercosur roadmap to prioritize investments that facilitate entry into regulated markets while maintaining balanced domestic B2C operations sensitive to promotions and delivery experience. Omnichannel execution and export readiness are becoming central to strategic differentiation, ensuring consistent service levels and market responsiveness. The operating pattern for the coming years emphasizes capital discipline, regulatory compliance, and supply chain precision. Together, these measures support a steadier growth trajectory for the Brazil furniture market.

Brazil Furniture Industry Leaders

-

IKEA

-

Ashley Furniture Industries, Inc.

-

MillerKnoll Inc.

-

Natuzzi S.p.A.

-

La-Z-Boy Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Bertolini launched its Linha Serena at Movelpar Home Show 2025, a contemporary furniture collection focused on natural wood tones, clean lines, and functional details. The line targets modern residential interiors, combining light aesthetics, practicality, and refined finishing to meet current consumer lifestyle trends.

- February 2025: At Movelpar 2025, Itatiaia introduced a new steel kitchen furniture line with updated colors, modular layouts, and enhanced durability. The launch focuses on practicality, affordability, and contemporary design, reinforcing the brand’s strength in functional kitchen solutions for urban Brazilian households.

- February 2025: Santos Andirá unveiled new wardrobe collections inspired by Brazilian regions, combining modern internal layouts, optimized storage, and clean exterior designs. The launch highlights regional identity, improved usability, and adaptability to different bedroom sizes, targeting both retail and mass-market segments.

Brazil Furniture Market Report Scope

By Application

| Home Furniture | Chairs |

| Tables (side tables, coffee tables, dressing tables, etc.) | |

| Beds | |

| Wardrobes | |

| Sofas | |

| Dining Tables / Dining Sets | |

| Kitchen Cabinets | |

| Other Home Furniture (bathroom, outdoor, etc.) | |

| Office Furniture | Office Chairs |

| Tables | |

| Storage Cabinets | |

| Desks | |

| Sofas & Other Soft Seating | |

| Other Office Furniture | |

| Hospitality Furniture | |

| Educational Furniture | |

| Healthcare Furniture | |

| Other Applications (public places, retail malls, government offices, etc.) |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

By Price Range

| Economy |

| Mid-Range |

| Premium |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Local Workshops (unorganized market) | |

| Other Distribution Channels | |

| B2B / Project |

By Region

| Southeast |

| South |

| Northeast |

| North |

| Central-West |

| By Application | Home Furniture | Chairs |

| Tables (side tables, coffee tables, dressing tables, etc.) | ||

| Beds | ||

| Wardrobes | ||

| Sofas | ||

| Dining Tables / Dining Sets | ||

| Kitchen Cabinets | ||

| Other Home Furniture (bathroom, outdoor, etc.) | ||

| Office Furniture | Office Chairs | |

| Tables | ||

| Storage Cabinets | ||

| Desks | ||

| Sofas & Other Soft Seating | ||

| Other Office Furniture | ||

| Hospitality Furniture | ||

| Educational Furniture | ||

| Healthcare Furniture | ||

| Other Applications (public places, retail malls, government offices, etc.) | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By Price Range | Economy | |

| Mid-Range | ||

| Premium | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Local Workshops (unorganized market) | ||

| Other Distribution Channels | ||

| B2B / Project | ||

| By Region | Southeast | |

| South | ||

| Northeast | ||

| North | ||

| Central-West | ||

Key Questions Answered in the Report

What is the current size and projected growth of the Brazil furniture market?

The Brazil furniture market size reached USD 16.15 billion in 2026 and is projected to reach USD 19.74 billion by 2031 at a 4.10% CAGR.

Which application segment leads and which grows fastest in the Brazil furniture market?

Home furniture led with a 55.0% share in 2025, while healthcare furniture is projected to grow at a 5.66% CAGR through 2031.

Which materials dominate the Brazil furniture market and where is growth strongest?

Wood retained a 62.0% share in 2025, and plastic and polymer are projected to be the fastest-growing materials at a 4.94% CAGR through 2031.

What channels are expanding fastest in the Brazil furniture market?

B2C accounted for 75.0% in 2025, and online subchannels within B2C are projected to grow at a 7.36% CAGR to 2031.

Which regions lead, and where is growth strongest across Brazil?

Southeast Brazil held 47.0% of consumption in 2025, and the North is forecast to grow fastest at a 4.82% CAGR through 2031.

Page last updated on: