Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

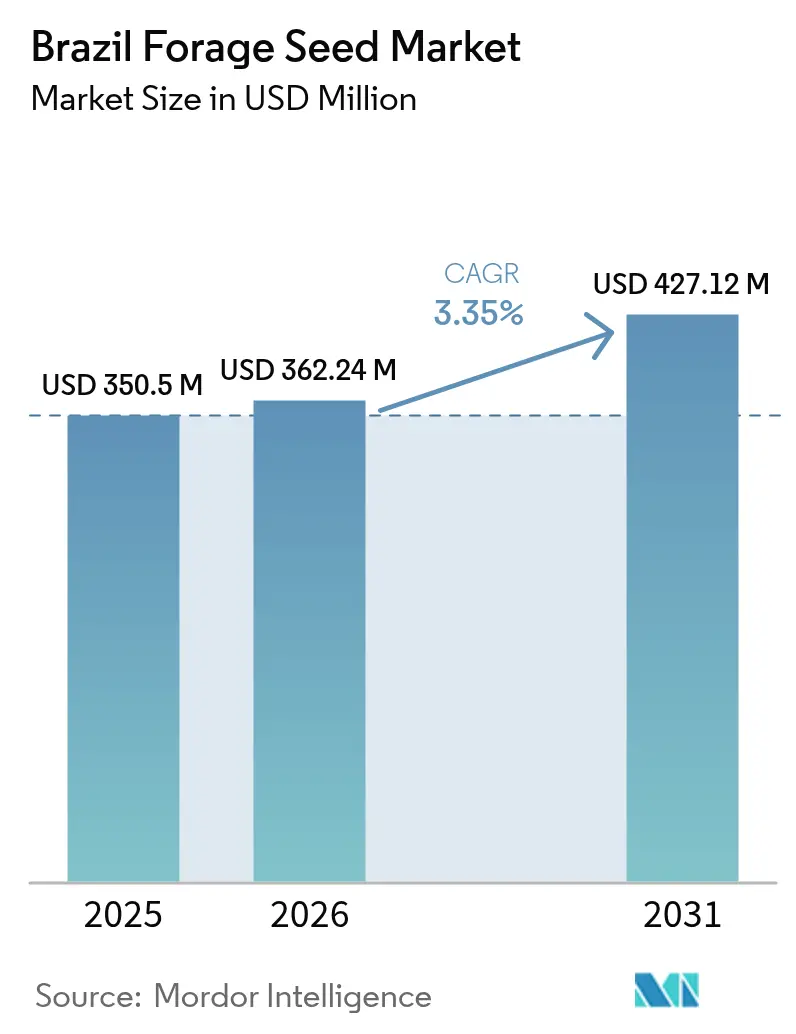

| Base Year Market Size (2025) | USD 350.50 Million |

| Market Size (2026) | USD 362.24 Million |

| Market Size (2031) | USD 427.12 Million |

| Growth Rate (2026 - 2031) | 3.35% CAGR |

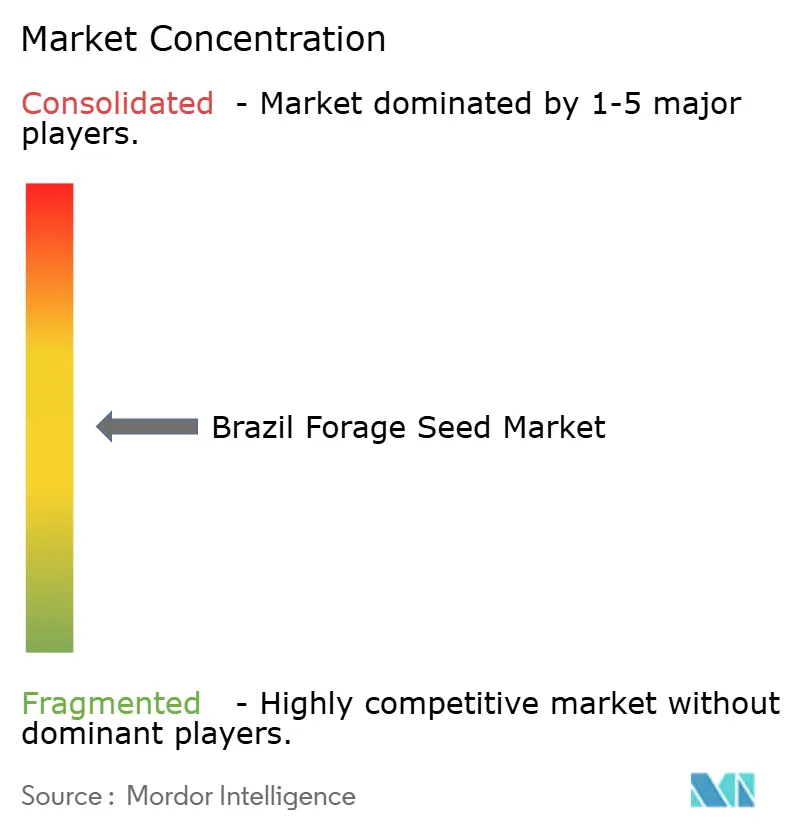

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Forage Seed Market Analysis by Mordor Intelligence

Brazil forage seed market size in 2026 is estimated at USD 362.24 million, growing from 2025 value of USD 350.50 million with 2031 projections showing USD 427.12 million, growing at 3.35% CAGR over 2026-2031. Livestock intensification, the shift toward hybrid genetics, and the 2024 Bio-inputs Law together reshape technology priorities as producers pursue higher stocking rates, stress-tolerant cultivars, and certified seed that complies with emerging sustainability metrics.[1]Source: Ministério da Agricultura e Pecuária, “Bio-inputs Law 15,070/2024,” gov.br Over 170 million head of cattle graze more than 100 million hectares of managed pasture, anchoring steady year-round demand for the Brazil forage seed market across the Center-West, Southeast, South, and expanding frontier zones.[2]Source: Empresa Brasileira de Pesquisa Agropecuária (EMBRAPA), “Livestock Intensification Potential in Brazil,” embrapa.br Hybrid cultivars dominate the genetic mix, while forage corn and sorghum programs receive increasing budget share in corporate research pipelines that emphasize yield stability under erratic weather. Although counterfeit seed and logistics congestion remain headwinds, precision-agriculture platforms, digital seed-credit apps, and state-backed pasture-recovery loans collectively shorten the payback period on premium genetics, reinforcing adoption momentum across the Brazil forage seed market landscape.

Key Report Takeaways

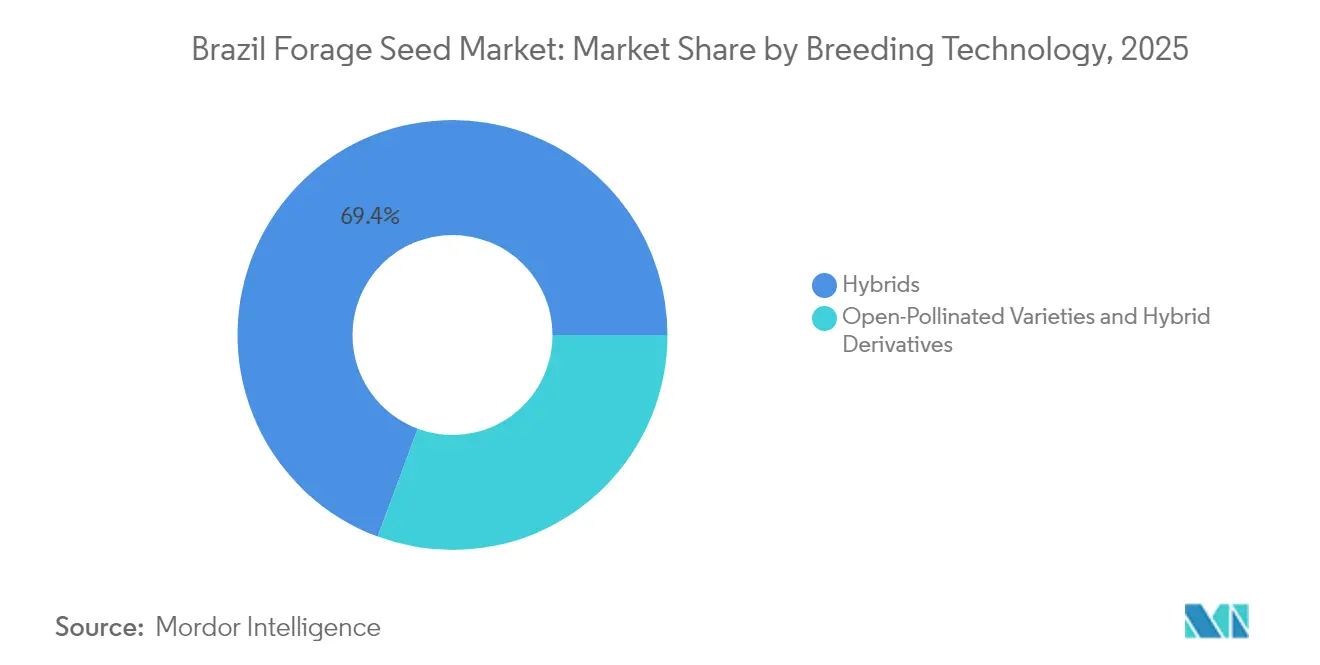

- By breeding technology, hybrid varieties accounted for 69.35% of the Brazil forage seed market share in 2025, while Transgenic Hybrids are anticipated to grow at a 9.84% CAGR.

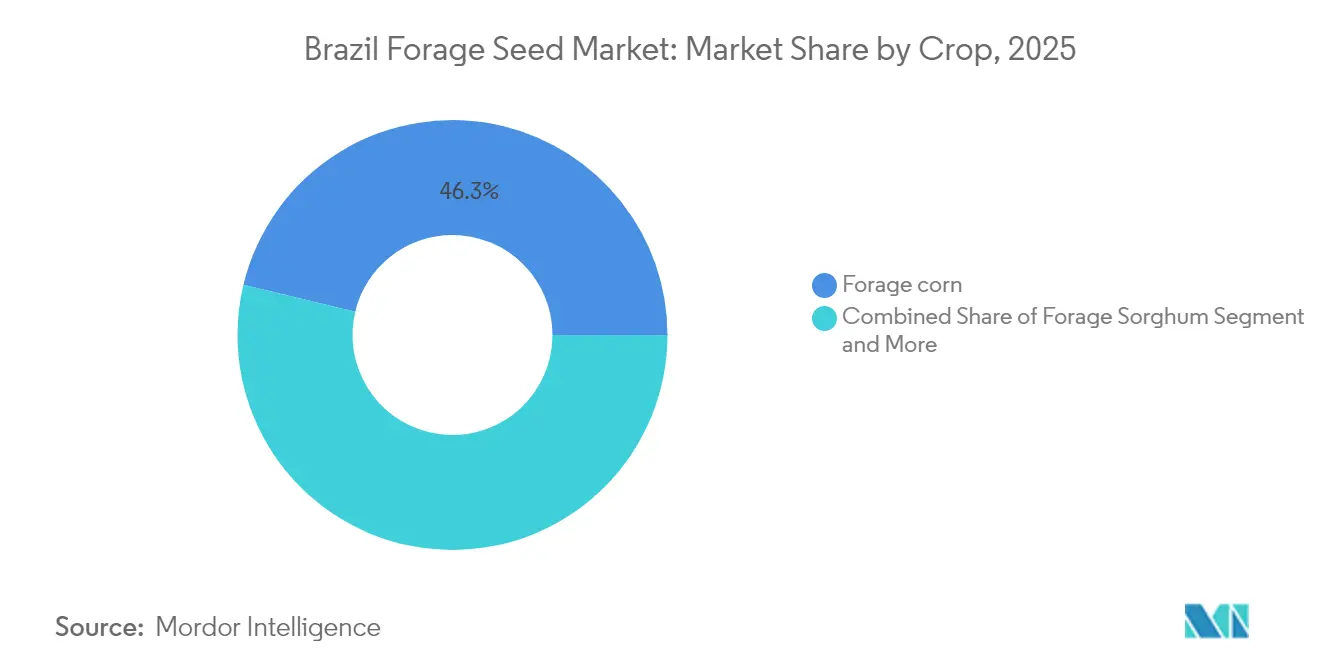

- By crop, forage corn held a 46.25% share of the Brazil forage seed market size in 2025, while forage sorghum recorded the fastest crop-specific CAGR at 8.95% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Forage Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Livestock expansion and intensification | +0.8% | Center-West, Southeast, and South | Medium term (2-4 years) |

| Adoption of improved tropical grass cultivars | +0.6% | National, with focus on Cerrado and Amazon transition | Long term (≥ 4 years) |

| Government ILPF and ABC-Carbon programs | +0.5% | Center-West, Northeast, and Amazon transition | Long term (≥ 4 years) |

| Growing corn-silage demand from dairy and feedlots | +0.4% | South, Southeast, selected Center-West micro-regions | Medium term (2-4 years) |

| Digital seed-credit and e-commerce platforms | +0.3% | National, early adoption in South and Southeast | Short term (≤ 2 years) |

| Seed-coating innovations for tropical climates | +0.2% | National, emphasis on semi-arid Northeast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Livestock expansion and intensification

Rising stocking-rate targets from the present 0.97 animal units per hectare toward 3.60 units create a structural pull for high-germination, nutrient-dense seed lots. Commercial ranches redesign grazing rotations around grass-legume mixtures that stabilize protein intake and lower urea costs, stimulating premium-segment growth. Export-oriented packers increasingly require traceability documentation that starts at seed purchase, adding compliance value to branded products. Intensification also prompts demand for coated seed that shortens pasture establishment times and delivers uniform stands under variable rainfall.

Adoption of improved tropical grass cultivars

Successive cultivar releases such as BRS Capiaçu elephant grass (33% higher dry-matter yield) and BRS 661 forage sorghum (70 metric tons per hectare potential) underscore a pipeline of genetics tailored to regional moisture and pest profiles. Early-adopting corporate ranches in Mato Grosso and Pará pay premium prices to capture the feed-conversion advantage, while smallholders lag due to credit constraints. Public–private multiplication agreements shorten the seed-to-market cycle, yet early-cycle shortages surface during launch seasons, keeping price realizations firm.

Government ILPF and ABC-Carbon programs

The ABC+ plan allocated BRL 7.05 billion (USD 1.4 billion) in concessional rural credit for sustainable practices in 2024, with a significant tranche earmarked for pasture restoration and diversified forage stands. Participating farms install tree-shaded paddocks that require shade-tolerant grasses and deep-rooted legumes, nudging breeders toward niche selections with documented carbon-sequestration attributes. Mandatory technical-assistance packages embedded in the loans improve correct seeding rates and establishment, reducing wastage and bolstering repeat purchases.

Growing corn-silage demand from dairy and feedlots

The number of confinement feedlots rose 11% in 2024, and dairy processors added 4.5 million liters per day of new capacity, both trends translating into surging silage demand.[3]Source: Centro de Estudos Avançados em Economia Aplicada, “Climate Impacts on Seed Production,” cepea.org.br Seed developers respond with ultra-early and medium-maturity hybrids that allow staggered harvesting, meeting year-round bunker-fill schedules. Precision harvesters require uniform plant height and moisture, favoring purpose-bred silage types over conventional grain cultivars.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of low-quality “pirate” seed | -0.4% | National, highest in Northeast and North | Short term (≤ 2 years) |

| Climate-driven droughts and floods | -0.3% | Northeast (drought), South (floods), Amazon transition | Medium term (2-4 years) |

| Port/logistics bottlenecks in peak season | -0.2% | National, critical in North and Northeast corridors | Short term (≤ 2 years) |

| Rising seed-borne fungal contamination | -0.2% | Humid tropical zones nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prevalence of low-quality “pirate” seed

Informal roadside vendors flood local markets with unlabeled seed that often contains less than 60% pure live seed, undermining confidence in certified offerings and compressing price premiums. Enforcement sweeps confiscated 1,800 metric tons of illegal stock in 2024, yet remote areas remain difficult to monitor. Legitimate suppliers counter by embossing lot numbers on coated seed and offering field-germination warranties to safeguard brand reputation.

Climate-driven droughts and floods

Brazil's increasing climate variability disrupts both seed production and end-user planting schedules, creating supply-demand imbalances that constrain market growth. The 2024 drought in Rio Grande do Sul reduced seed multiplication areas while flooding damaged storage facilities and distribution infrastructure. Extreme weather events force producers to delay or abandon planting, reducing annual seed consumption and creating inventory management challenges for distributors. Climate impacts particularly affect rain-fed seed production areas where irrigation infrastructure remains limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Command a Premium Position

Hybrid lines captured 69.35% of revenue in the Brazil forage seed market share during 2025, underscoring widespread acceptance of predictable yield, uniform maturity, and multi-trait disease shields. In large Center-West ranches, hybrids consistently out-yield open-pollinated varieties by 18% in dry-matter and deliver 2 points higher crude protein, metrics the finance teams track within feed-cost dashboards. Non-transgenic hybrids still dominate volume, serving buyers who seek performance gains without genetically modified organism regulatory overhead. Transgenic hybrids are advancing at a 9.84% CAGR, buoyed by herbicide-tolerance traits that cut manual weeding and align with conservation tillage mandates.

Open-pollinated varieties persist among smallholders and organic dairies where lower seed costs and certification rules discourage biotech use. Hybrid derivatives seed blends that capture partial heterosis offer a mid-priced bridge for growers upgrading from traditional lines. The Brazil forage seed market size for hybrid derivatives remains modest yet shows consistent renewal demand in marginal rainfall belts. As CTNBio (National Technical Commission on Biosafety) streamlines dossier review, breeders allocate greater capital to gene-edited traits such as brown midrib lignin reductions that can lift in-rumen digestibility by up to 5 percentage points.

By Crop: Forage Corn Retains the Energy Crown

Forage corn accounted for 46.25% of the forage seed market size in 2025, due to its exceptional starch density and well-developed silage logistics. Elite silage hybrids now hit 22 metric tons of dry-matter per hectare under drip irrigation in São Paulo clusters and maintain digestibility above 68% neutral-detergent fiber, a performance that underpins milk-yield gains in total mixed ration operations. Dual-purpose corn hybrids give feedlot managers flexibility to pivot between grain and silage harvest, buffering commodity-price swings.

Forage sorghum, expanding at a 8.95% CAGR, appeals to regions with 500 millimeters or less annual rainfall. BRS 661 underscores the genetic acceleration, blending drought resilience with 70 metric tons of biomass ceilings. Dairy outreach programs in semi-arid Bahia showcase sorghum-corn rotation models that distribute risk and flatten seasonal feed costs. Alfalfa retains loyal acreage in temperate southern micro-climates due to its 20% crude-protein benchmark, while millet, ryegrass, and oat mixes fill window crops that bridge rainy-season transition gaps. The diverse crop palette ensures the Brazil forage seed market meets discrete nutritional and climatic specs across latitude and altitude gradients.

Geography Analysis

The Center-West dominates the Brazil forage seed market, fueled by expansive ranches in Mato Grosso, Mato Grosso do Sul, and Goiás that each re-seed thousands of hectares annually to sustain higher stocking densities. Corporate growers possess capital for hybrid germplasm bundles, precision sowing machinery, and telemetry-guided variable-rate fertilization, raising per-hectare seed budgets well above the national average. Distribution hubs in Rondonópolis and Sorriso link directly to certified seed farms, shortening lead times and curbing viability losses.

The Southeast ranks second, spearheaded by Minas Gerais dairy basins and feedlots around São Paulo that favor silage-focused corn and sorghum hybrids with contractually specified starch and fiber parameters. Fintech-enabled input loans proliferate, enabling medium operations to lock in hybrid seed early and secure volume rebates. Southeastern growers also pilot drone-based stand-counts, feeding real-time data to seed suppliers that fine-tune plant-population recommendations by cultivar. The South presents a distinct crop mix where temperate pasture and winter cereals maintain rotation diversity. Rio Grande do Sul remains a key hybrid-seed multiplication zone, but the 2024 drought exposed water-stress vulnerability, prompting a pivot to supplementary irrigation and insurance hedges. Santa Catarina poultry integrators now stipulate forage cover on free-range plots, widening the scope for low-height ryegrass seed. The Northeast and North together represent high-growth frontiers. Semi-arid zones in Piauí and Maranhão adopt drought-tolerant forage sorghum hybrids funded by ABC credits, while Pará’s humid frontier trials shade-tolerant grass-legume mixes under emerging agroforestry corridors. Logistics remain challenging, so e-commerce and mobile wallet payments play a critical role in expanding certified-seed reach. Overall, regional heterogeneity mandates a broad cultivar portfolio, reinforcing the Brazil forage seed market resilience across climatic extremes.

Competitive Landscape

The competitive landscape is concentrated, with the top five breeders controlling more than 50% of revenue, and is characterized by research pipelines, proprietary traits, and digital delivery models. Multinationals leverage global germplasm libraries and molecular labs to stack traits quickly, while domestic players capitalize on local agronomy know-how and rural-extension networks. Vertical integration from breeding plots to retail channels compresses time-to-market, especially for transgenic launches that navigate CTNBio clearance.

Strategic mergers and acquisitions reshape asset footprints. KWS divested its South American corn franchise to GDM, freeing capital for vegetable and sugar beet programs, yet retaining forage-hybrid research and development via a new Uberlândia hub. Barenbrug purchased Corteva's Brachiaria portfolio to deepen tropical-grass dominance, while regional operator Boa Safra merged with SememBras, consolidating storage and coating capacity. Trait stacks now incorporate CRISPR-induced brown-midrib lignin cuts, insecticidal proteins, and drought-responsive gene promoters, although commercial rollouts hinge on consumer perception and European Union import rules.

Digital platforms become differentiators. Market leaders embed satellite biomass indices and smartphone scouting logs directly into seed invoices, allowing ranch managers to benchmark cultivar performance against neighbor averages. Biological seed treatments emerge as the next battleground following the Bio-inputs Law, with Syngenta and local start-ups racing to patent microbial consortia that boost phosphorus solubilization. These innovations elevate switching costs, bolstering customer stickiness in the Brazil forage seed market.

Brazil Forage Seed Industry Leaders

Barenbrug do Brasil Ltda (Royal Barenbrug Group)

Corteva Inc.

DLF Seeds and Science (DLF A/S)

UPL Ltd.

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Corteva formed a partnership with BASF and M.S. Technologies to launch Brazil's first nematode-resistant soybean variety, which protects against root lesion and soybean cyst nematodes.

- March 2025: Embrapa showcased new forage seed varieties BRS Capiaçu, BRS Kurumi, and BRS Integra at Dinapec, reinforcing public investment in tropical forage breeding.

- March 2024: KWS completed the sale of its South American corn business to GDM, reallocating resources toward specialty seed segments, including forage seeds.

Brazil Forage Seed Market Report Scope

Forages are plants or parts of plants eaten by herbivorous animals. The report covers the seed market of forage crops and the analysis of different types of forages. The information regarding market overview, especially in terms of maturity provided in the study, is essential towards developing apt growth strategies suitable for Brazil considered in the study. Profiles of major players active in countries studied will provide decisive information towards developing a competitive strategy.

By Breeding Technology

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide-Tolerant Hybrids | |

| Other Traits | ||

| Open-Pollinated Varieties and Hybrid Derivatives | ||

By Crop

| Alfalfa |

| Forage Corn |

| Forage Sorghum |

| Other Forage Crops (Millet, Oats) |

| By Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide-Tolerant Hybrids | ||

| Other Traits | |||

| Open-Pollinated Varieties and Hybrid Derivatives | |||

| By Crop | Alfalfa | ||

| Forage Corn | |||

| Forage Sorghum | |||

| Other Forage Crops (Millet, Oats) | |||

Key Questions Answered in the Report

How large is the Brazil forage seed market in 2026?

The Brazil forage seed market size stands at USD 362.24 million in 2026, with a forecast value of USD 427.12 million by 2031.

How fast is the Brazil forage seed market growing?

The market is advancing at a 3.35% CAGR from 2026 to 2031.

Which breeding technology dominates sales?

Hybrid genetics lead with 69.35% of 2025 revenue.

Why is forage sorghum gaining popularity?

Its drought tolerance and 70 metric ton yield potential drive a 8.95% CAGR through 2031.

Page last updated on: