Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

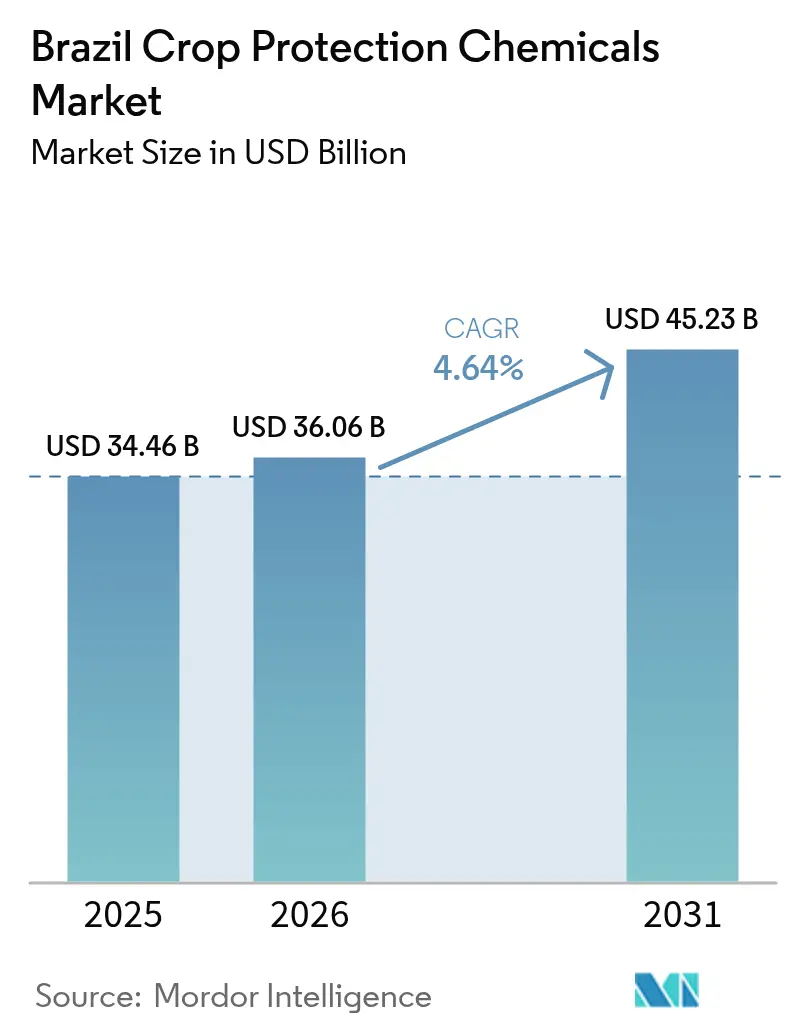

| Base Year Market Size (2025) | USD 34.46 Billion |

| Market Size (2026) | USD 36.06 Billion |

| Market Size (2031) | USD 45.23 Billion |

| Growth Rate (2026 - 2031) | 4.64% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Crop Protection Chemicals Market Analysis by Mordor Intelligence

Brazil crop protection chemicals market size in 2026 is estimated at USD 36.06 billion, growing from 2025 value of USD 34.46 billion with 2031 projections showing USD 45.23 billion, growing at 4.64% CAGR over 2026-2031. The strong export-oriented expansion of soybeans and corn, combined with rising pest resistance and drone-enabled precision farming, sustains steady demand for synthetic formulations. Fast-track generic approvals, enacted under Law 14.785/2023, compress the time-to-market and intensify price competition, while currency swings raise the cost of imported active ingredients and encourage the development of local formulation capacity. Growth in soil treatment and seed-applied products reflects tighter environmental rules and farmer adoption of integrated pest management. Fragmented competitive dynamics favor both global innovators and nimble domestic firms that tailor solutions to Brazil’s diverse agro-climatic zones.

Key Report Takeaways

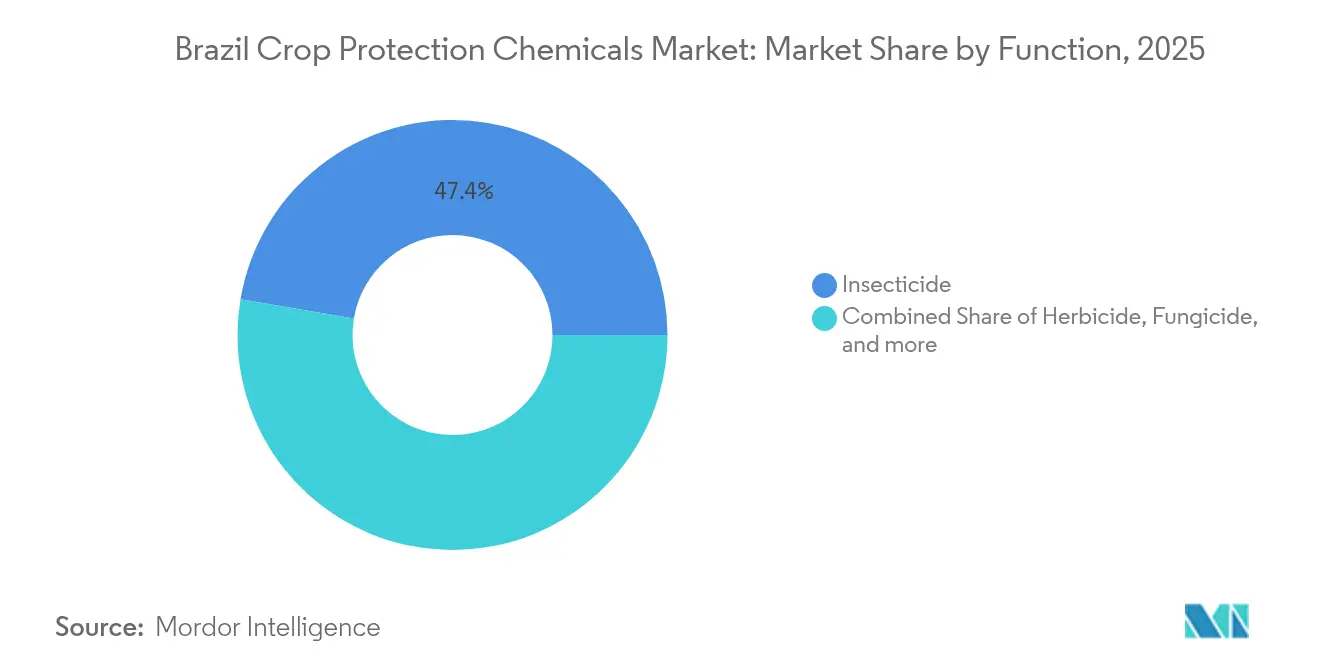

- By function, insecticides led with 47.35% of Brazil crop protection chemicals market share in 2025, molluscicides are forecast to expand at an 8.45% CAGR through 2031.

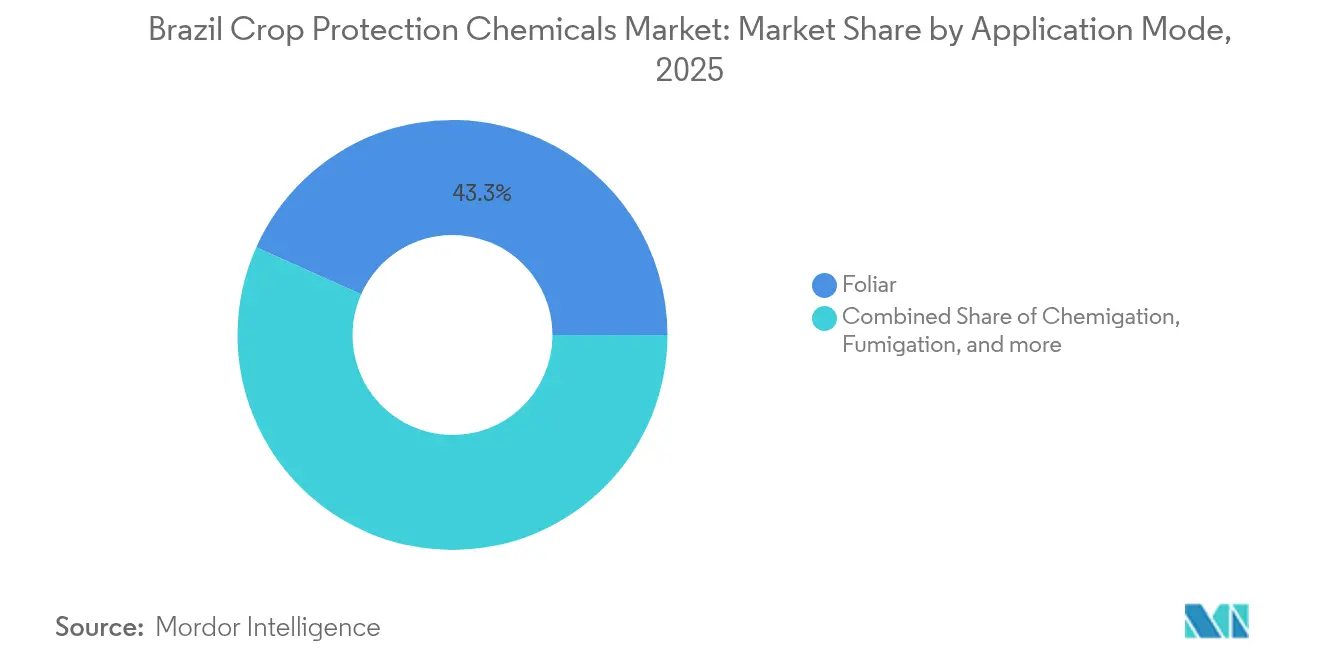

- By application mode, foliar treatments held 43.30% of the Brazil crop protection chemicals market size in 2025, while soil treatment is projected to rise at a 5.12% CAGR to 2031.

- By crop type, pulses and oilseeds commanded 49.10% of the Brazil crop protection chemicals market size in 2025 and are advancing at a 4.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Crop Protection Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of soybean and corn acreage | +1.2% | Brazil, spillover to Paraguay and Bolivia | Medium term (2-4 years) |

| Herbicide-resistant weeds driving combination products | +0.9% | Brazil national | Short term (≤ 2 years) |

| Fast-track registration of generics lowering prices | +0.6% | Brazil national, limited regional spillover | Short term (≤ 2 years) |

| Export-oriented phytosanitary compliance | +0.5% | Brazil export regions, international standards alignment | Long term (≥ 4 years) |

| Drone-based ultra-low-volume spraying adoption | +0.4% | Brazil core agricultural regions | Medium term (2-4 years) |

| Intensification of safrinha crop cycles | +0.8% | Brazil Cerrado and Center-West regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Soybean and Corn Acreage

Soybean plantings in the Cerrado reached around 45.2 million hectares in 2024, a 3.1% rise year-on-year. Newly converted land demands higher application rates as growers battle virgin-soil pests, necessitating diverse chemical portfolios across two crop cycles per year. Safrinha corn follows soybeans on the same fields and doubles spray rounds, lifting per-hectare spending on herbicides, fungicides, and seed treatments. Compliance with MAPA (Department of Agriculture, Livestock, and Food Supply) rotation guidelines obliges farmers to alternate modes of action, thereby further widening the demand for branded and generic actives. Export-linked certifications enhance the use of premium, low-residue products and biological complements, solidifying Brazil's crop protection chemicals market as a core input partner for Cerrado agribusiness.

Herbicide-resistant Weeds Driving Higher-dose Combination Products

Resistance now affects around 15.8 million hectares, with glyphosate-tolerant palmer amaranth and sourgrass most problematic. Farmers increasingly adopt pre-mixes that blend auxin mimics, ACCase inhibitors, and photosystem blockers, lifting chemical costs by 25-40% per hectare. ANVISA cleared 47 new mixtures in 2024, geared toward resistance management, enabling suppliers to command premium margins while safeguarding yields. Continuous cropping and no-till practices accelerate resistance spread, reinforcing demand for novel chemistry and stewardship programs that embed digital recommendation tools. These dynamics propel combination product volumes and sustain price resilience in the Brazil crop protection chemicals market.

Fast-track Registration of Generics Lowering Prices

Law 14.785/2023 cut generic approval timelines from eight to three years, resulting in 156 registrations in 2024 [1]Brazilian Health Regulatory Agency, “Pesticide Registration Reports 2024-2025,” gov.br . Cheaper copies, typically 20-30% below originator list prices, broaden access for midsize distributors and cooperatives. Chinese and Indian technical suppliers joint-venture with local formulators to leverage shortened pathways, boosting regional manufacturing and dampening import reliance. Although margins compress for innovators, larger market volume offsets the impact, and competitive pricing accelerates adoption of modern molecules among smallholders. The mechanism also intensifies differentiation pressure, prompting branded suppliers to bundle agronomic support and digital tools.

Drone-based Ultra-Low-Volume Spraying Adoption

Registered ag-drones reached 35,000 units in 2025 following the publication of Ordinance No. 298 by the Ministry of Agriculture and Livestock (MAPA) which regulated their use. Their 0.5-1.0 liter-per-hectare rates require formulations three to five times more concentrated, stimulating R&D in solvent-free dispersions and micro-encapsulated actives. Drones allow timely fungicide targeting in soybean flowering windows, cutting disease spread and reducing labor. Small farmers gain affordable access to precision, widening high-value chemical addressability. MAPA guidelines now prescribe drone protocols, further standardizing product design and cementing aerial delivery as a mainstream growth vector for the Brazil crop protection chemicals market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ANVISA toxicity reassessments and active bans | -0.7% | Brazil national, regulatory spillover effects | Short term (≤ 2 years) |

| Volatility in exchange rates inflating input costs | -0.5% | Brazil national, import-dependent regions | Short term (≤ 2 years) |

| Shift toward biological crop protection alternatives | -0.4% | Brazil core agricultural regions, premium markets | Long term (≥ 4 years) |

| Community lawsuits over spray drift in frontier areas | -0.3% | Brazil frontier regions, environmentally sensitive zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ANVISA Toxicity Reassessments and Active Bans

Twenty-seven actives, including paraquat and certain 2,4-D salts, lost approval in 2024 [2]Brazilian Health Regulatory Agency, “Toxicological Assessment Reports 2024-2025,” gov.br . Sudden withdrawals unsettle supply chains and oblige farmers to reconfigure programs, often at higher cost per hectare. Manufacturers bear write-offs on inventories and must channel R&D funds into safer replacements while forecasting future regulatory shifts. Although new combinations partly offset lost volume, uncertainty delays investment decisions and can slow rollout of innovative chemistry, tempering the Brazil crop protection chemicals market growth in the near term.

Community Lawsuits Over Spray Drift Near Frontier Areas

Eighty-nine active cases targeted drift damages in 2024 [3]Brazilian Federal Court System, “Environmental Cases 2024,” stf.jus.br . Courts impose buffer zones and time-of-day restrictions, compelling farmers to adopt low-volatility formulations and anti-drift nozzles. Settlement and compliance costs drive interest in precision systems, but also deter chemical use near sensitive biomes. Public scrutiny shapes stricter local ordinances that may outpace federal regulation, adding complexity and potential penalties that weigh on demand in frontier regions, thus dampening the Brazil crop protection chemicals market trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Demand concentration in insecticides with rapid molluscicide rise

Insecticides generated 47.35% of 2025 revenue as continuous cropping sustains fall armyworm and stink bug outbreaks. This dominance anchors volume stability for the Brazil crop protection chemicals market. Fungicides reflect persistent soybean rust and corn leaf blight threats. Herbicides captured significant share, constrained by growing resistance yet indispensable to no-till systems that cut soil erosion. Molluscicides expand at 8.45% CAGR owing to slug proliferation under conservation tillage. Regulatory pressure favors safer actives, prompting suppliers to reformulate legacy molecules.

Second-generation insecticide chemistries, including diamides and spinosyns, gain share as resistance erodes pyrethroid efficacy. Companies bundle insecticides with proprietary adjuvants to enhance leaf coverage and rainfastness, differentiating offerings in an otherwise price-intensive landscape. Fungicide innovation focuses on triazole-SDHI mixtures that extend residual control, key for elongated wet seasons. Herbicide portfolios shift toward pre-emergence and residual products integrated with cover crop systems. Molluscicide newcomers emphasize low-dose metaldehyde replacements to satisfy stricter environmental norms. These trends collectively reinforce product diversity and sustain the breadth of the Brazil crop protection chemicals market.

By Application Mode: Foliar leads, soil treatments accelerate

Foliar sprays accounted for 43.30% of 2025 value, underpinned by the need for timely curative action against foliar diseases and insects. Seed treatments, propelled by high-concentration systemic actives that protect vulnerable germinating plants. Chemigation also occupied a major share, leveraging center-pivot irrigation in Mato Grosso and Goiás. Soil treatments represented a smaller share but deliver the fastest 5.12% CAGR as variable-rate technology enables targeted in-furrow dosing. Fumigation remained a niche for specialty crops.

Precision tools such as prescription maps and optical sensors drive modal shifts. Farmers combine seed treatments with in-row soil drenches to manage early nematode pressure, reducing the number of foliar rescue sprays. Drone capacity expands foliar frequency during critical phenological stages, while ultra-low-volume products limit water use and labor. As regulators push drift mitigation, electrostatic and enclosed sprayers gain ground, altering formulation design and application service models. These evolutions diversify revenue streams and strengthen resilience of the Brazil crop protection chemicals market.

By Crop Type: Soybean-centric structure shapes demand

Pulses and oilseeds, mainly soybean, dominate with 49.10% share and fastest-growing with a 4.86% CAGR. Yield-critical diseases such as Asian rust justify multilayer fungicide programs, maximizing the Brazil crop protection chemicals market size at farm level. Grains and cereals hold 31.45%, centered on safrinha corn’s compressed window that necessitates robust residual herbicides and systemic insecticides. Commercial crops such as cotton, sugarcane, coffee account for 12.25%, each requiring tailored portfolios for bollworms, borers and leaf rust. Fruits and vegetables, despite small acreage, reach 5.05% value on high per-hectare spend for residue-compliant fungicides and biologicals. Turf and ornamental niches fill 2.15%, mainly urban.

Soybean expansion into MATOPIBA and Pará adds fresh hectare gains, whereas corn intensification boosts double-crop rotations. Cotton acreage stability redirects chemical focus to resistance stewardship. Sugarcane renewal cycles drive soil insecticide and herbicide pulses. Specialty fresh produce plantations near consumer hubs adopt reduced-risk actives to satisfy supermarket protocols, nurturing premium subsegments and reinforcing diversification of the Brazil crop protection chemicals market.

Geography Analysis

Brazil contributes roughly 85.00% of South American crop protection demand. The Center-West regions such as Mato Grosso, Mato Grosso do Sul and Goiás absorbs 64.60% of national consumption, mirroring its dominance in soybean and corn monoculture. Large farms averaging 2,500 hectares employ high-throughput planes and drones, favoring bulk procurement and integrated advisory contracts with input distributors.

The South supplies 25.55% of demand through diversified holdings that blend grains with horticulture, supporting a broader product mix for fruits and vegetables. MATOPIBA frontier zones log 7.65% annual consumption growth, as land conversion sparks new pest complexes requiring establishment-phase controls IBGE. Regional climatic contrasts mold product timing, humid Paraná necessitates multiple fungicide passes, while semi-arid Bahia prioritizes soil moisture-saving pre-emergence herbicides.

Exchange-rate sensitivity is acute in import-dependent Northeast cotton clusters, spurring cooperative bulk purchase schemes to smooth price shocks. Frontier deforestation litigation intensifies operator scrutiny in Pará and Rondônia, inviting precision drift solutions. Collectively, these nuances shape tailored go-to-market strategies and anchor geographic resilience of the Brazil crop protection chemicals market.

Competitive Landscape

The top five companies hold a low aggregate share, assigning the Brazil crop protection chemicals market a fragmentation profile. Multinational leaders leverage global discovery pipelines to introduce differentiated actives such as Bayer’s triazole-SDHI fungicides, while domestic players like Nortox and Ourofino scale generics and locally adapted mixtures. Combination packs aimed at resistance rotate multiple modes of action, helping suppliers defend margins amidst generic proliferation. Biological alliances, exemplified by BASF-Embrapa, extend portfolios into microbials and RNA-based products.

Precision delivery services become a core differentiator with Syngenta’s digital scouting tools integrate with drone application protocols, whereas FMC bundles subscription agronomic platforms with Benevia MIP launches. Currency hedging and local production investments, such as Sumitomo’s Rondonópolis plant, buffer volatility and ensure supply continuity.

Niche growth pockets in molluscicides and soil treatments lure specialty entrants, intensifying competition yet widening farmer choice. These dynamics reinforce innovation, service depth and price transparency across the Brazil crop protection chemicals market. Overall, the Brazil crop protection industry is characterized by a balance of innovation and competition, ensuring diverse solutions for farmers. The market's fragmentation and evolving dynamics present opportunities for both global and local players.

Brazil Crop Protection Chemicals Industry Leaders

Syngenta Group

Bayer AG

Corteva Agriscience

FMC Corporation

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Albaugh LLC Brazil launched Sultan, a new insecticide formulated with the active ingredient Etiprole. The product targets soybean stink bugs and is also registered for use on crops such as cotton, rice, coffee and sugarcane, providing growers with a more potent and streamlined solution.

- May 2024: FMC Corporation announced on that it has secured Brazilian registration for two herbicides Azugro and Ezanya which are powered by its novel active ingredient Isoflex (bixlozone). These products target cotton, tobacco and wheat crops, offering a new mode of action (classified by Herbicide Resistance Action Committee as Group 13) to address increasing herbicide resistance among grass and broadleaf weeds.

- February 2023: ADAMA opened a new multi-purpose facility in Brazil. With this factory, the company will be able to deliver all the Prothioconazole-based products in its pipeline to the global market and achieve its objective of introducing a number of innovative items to the Brazilian market in the upcoming years.

Brazil Crop Protection Chemicals Market Report Scope

Fungicide, Herbicide, Insecticide, Molluscicide, Nematicide are covered as segments by Function. Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.Function

| Fungicide |

| Herbicide |

| Insecticide |

| Molluscicide |

| Nematicide |

Application Mode

| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

Crop Type

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

| Function | Fungicide |

| Herbicide | |

| Insecticide | |

| Molluscicide | |

| Nematicide | |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental |

Market Definition

- Function - Crop Protection Chemicals are apllied to control or prevent pests, including insects, fungi, weeds, nematodes, and mollusks, from damaging the crop and to protect the crop yield.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms