Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2017 - 2023 |

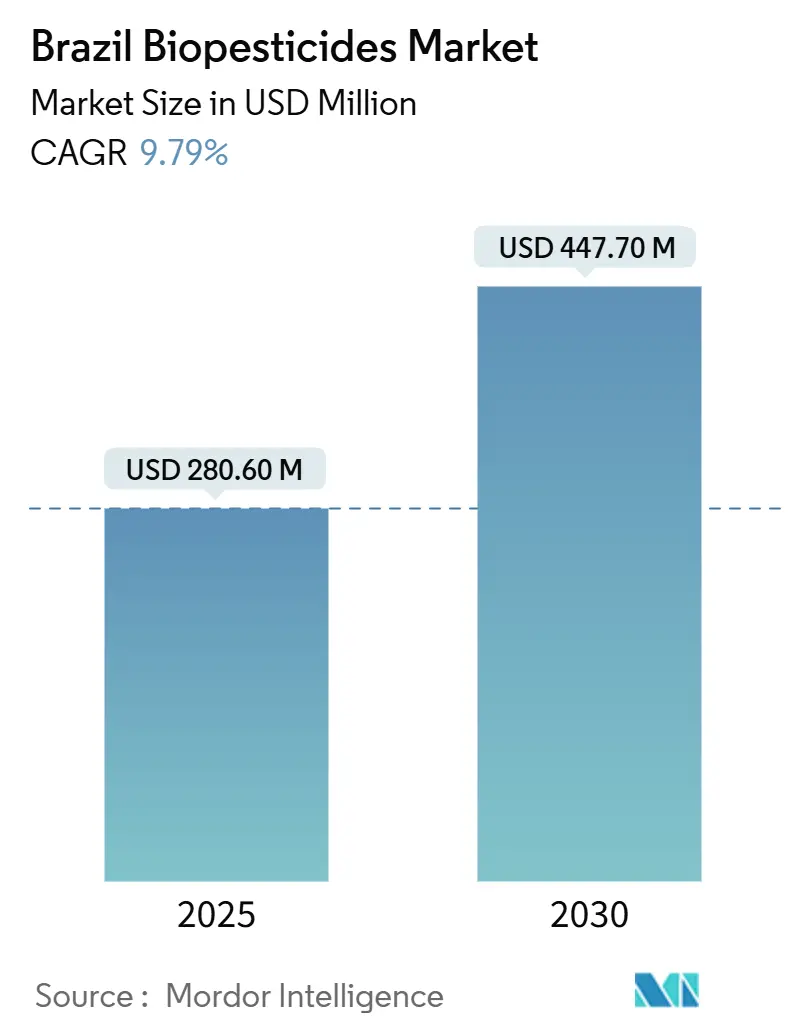

| Market Size (2025) | USD 280.60 Million |

| Market Size (2030) | USD 447.70 Million |

| Growth Rate (2025 - 2030) | 9.79% CAGR |

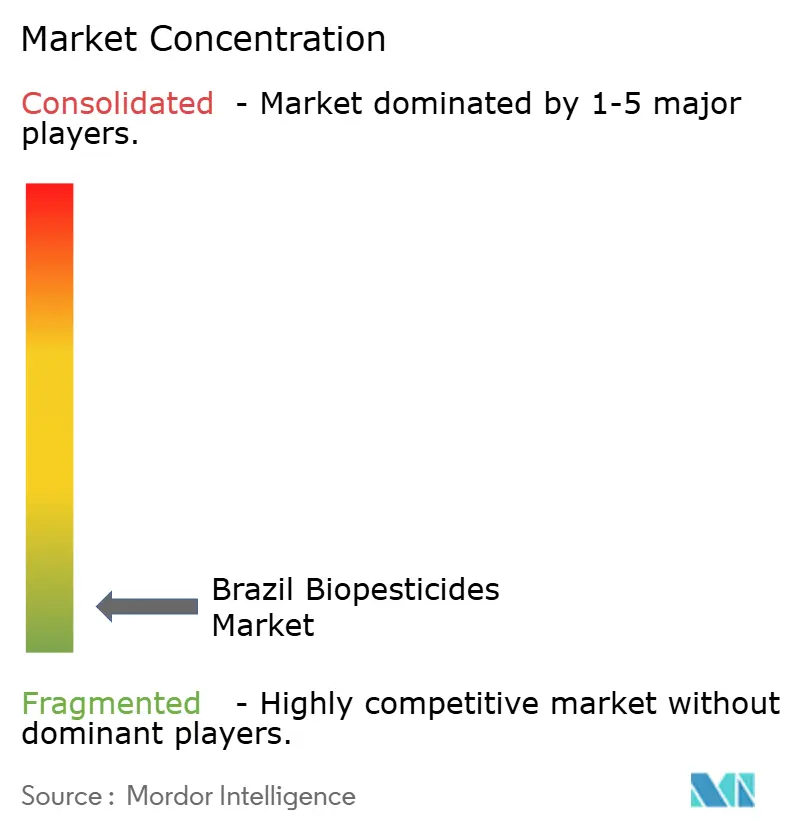

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Biopesticides Market Analysis by Mordor Intelligence

The Brazil biopesticides market size stood at USD 280.6 million in 2025 and is projected to reach USD 447.7 million by 2030, registering a 9.79% CAGR during the forecast period. Growing demand for residue-free commodities, progressive regulatory support from the National Bio-inputs Program, and mounting chemical-resistance pressures in soybean and corn are propelling the Brazil biopesticides market. Rapid registration timelines, tax incentives, and subsidized credit lines have lowered entry barriers, enticing both domestic innovators and global majors. Large growers in Mato Grosso and Goiás are scaling on-farm biofactories to secure cost-effective supply, while digital sales platforms broaden product access nationwide. Fragmented leadership, with the top five suppliers holding only 38.5%, signals ample room for consolidation and niche specialization. [1]Source: USDA Foreign Agricultural Service, “Brazilian Legislation for Biopesticides – On-farm Biopesticides Production,” apps.fas.usda.gov

Key Report Takeaways

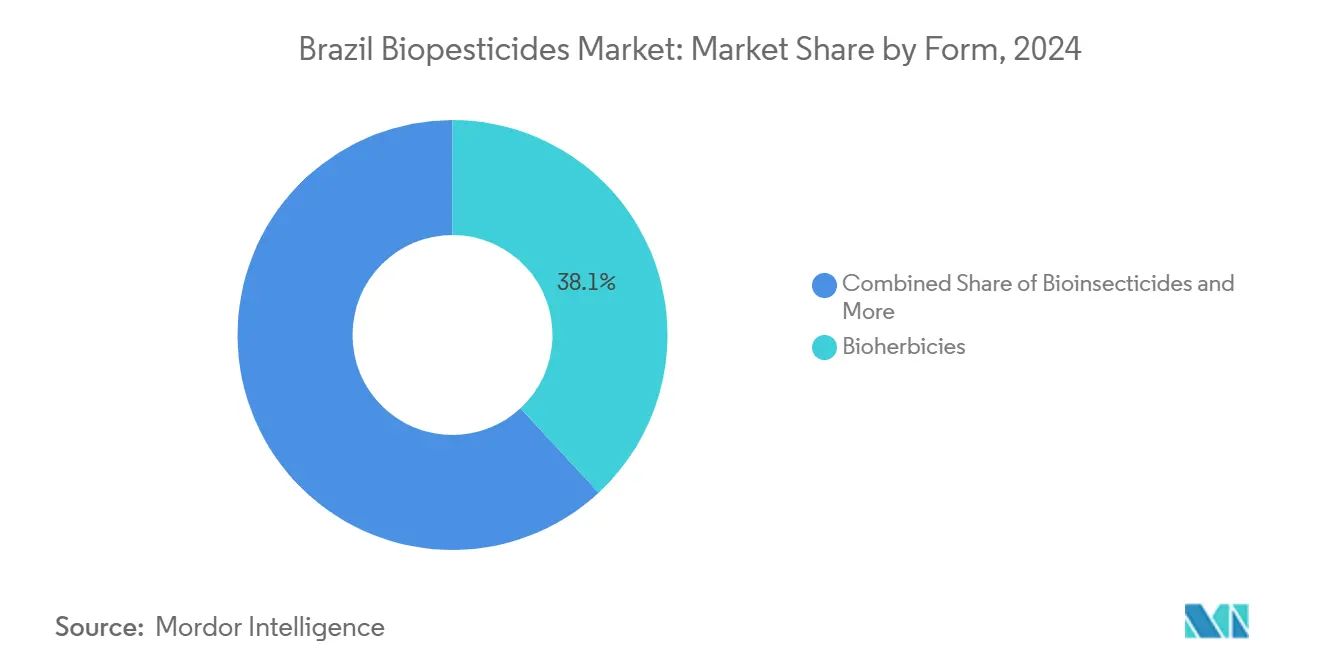

By Form, bioherbicides led with 38.1% revenue share in 2024, while bioinsecticides are forecast to expand at a 10.2% CAGR through 2030.

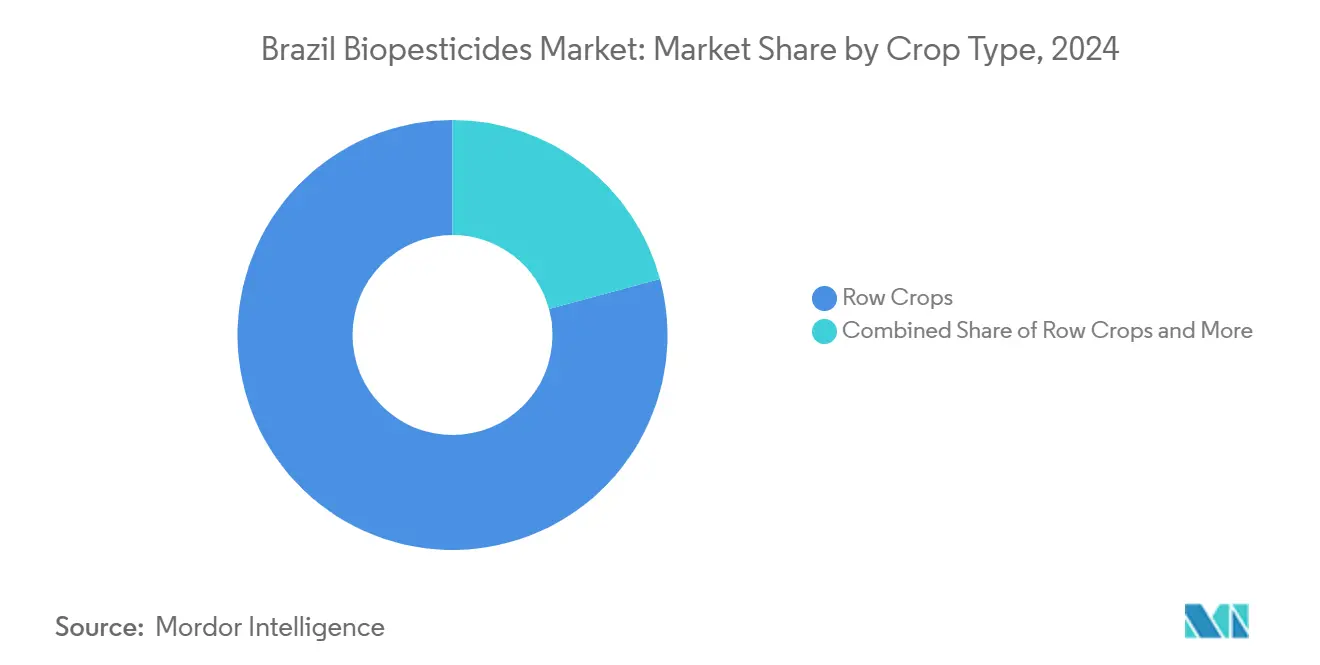

By Crop Type, row crops captured a 79.0% share of the Brazil biopesticides market size in 2024, and are expected to post the fastest 9.85% CAGR through 2030.

Brazil Biopesticides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Bio-inputs Program incentives | +2.8% | Nationwide, strongest in Midwest and South | Medium term (2-4 years) |

| Chemical-pesticide resistance crisis | +3.1% | Nationwide, acute in Cerrado and Southern regions | Short term (≤ 2 years) |

| Export-market residue standards | +2.2% | Nationwide, export-focused corridors | Medium term (2-4 years) |

| Lower registration costs than chemicals | +1.4% | Nationwide | Long term (≥ 4 years) |

| On-farm biofactory pilots | +0.8% | Mato Grosso, Goiás, expanding Midwest | Long term (≥ 4 years) |

| Digital agro-marketplace expansion | +0.6% | Nationwide, higher in developed farm regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National Bio-inputs Program incentives

Brazil’s National Bio-inputs Program established a dedicated pathway that trims registration cycles from eight years to under twenty-four months, backed by BRL 1.2 billion (USD 240 million) in subsidized credit through 2027. Reduced ICMS levies lower shelf prices 15% to 20%, helping biologicals match synthetic costs and accelerating adoption in the Brazil biopesticides market. Faster approvals encourage broader product pipelines, while predictable timelines attract venture funding. Smallholders gain affordable access to proven microbial technologies, reducing yield risk and boosting rural incomes. The program’s financial carrots and streamlined oversight jointly lift market penetration across diverse farm sizes. [2]Source: Ministry of Agriculture Livestock and Food Supply, “National Bio-inputs Program,” agricultura.gov.br

Chemical-pesticide resistance crisis

Glyphosate resistance now affects over 40% of surveyed soybean fields, and pyrethroid resistance handicaps 60% of corn hectares. Lost efficacy raises weed and pest management costs by 18% and prompts yield drops of up to 25% in hotspot regions. Biopesticides deliver novel modes of action, easing resistance pressure and restoring yield stability. Demand concentrates in the Cerrado, where intensive, two-cycle cropping accelerates resistance, making biologicals a cost-effective safeguard. Multinationals and Brazilian specialists release stacked microbial blends to broaden control spectra, keeping the Brazil biopesticides market on a double-digit growth path.

Export-market residue standards

European Union Farm to Fork mandates and China’s zero-tolerance rules compel Brazilian exporters to cut chemical residues or risk shipment rejections. Premium buyers pay 5% to 10% more for compliant corn and soybean cargoes. Growers in Mato Grosso, Rio Grande do Sul, and Paraná deploy biological crop protection to meet tougher tolerances and secure access to high-value contracts. The resulting margin uplift offsets product transition costs, propelling the Brazil biopesticides market deeper into mainstream agronomic programs.

Lower registration costs than chemicals

Biological dossiers require far fewer toxicology studies, trimming compliance outlays by roughly 60% relative to synthetic counterparts. Start-ups and university spin-offs leverage this cost edge to commercialize native microbial strains rapidly. Freed capital fuels additional field trials and formulation upgrades, widening product choice for farmers. Predictable MAPA review cycles de-risk R&D investments, luring foreign direct investment into the Brazil biopesticides industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-linked efficacy variability | -1.8% | Nationwide, sharpest in North and Northeast | Short term (≤ 2 years) |

| Cold-chain and storage gaps | -1.2% | Remote agricultural zones | Medium term (2-4 years) |

| Native-strain patent disputes | -0.7% | Nationwide | Long term (≥ 4 years) |

| Skilled-labor shortage for application | -0.9% | Expanding frontiers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Climate-linked efficacy variability

Tropical heat above 35 °C can cut microbial spore viability by 60% within a day, while intense ultraviolet light degrades botanical actives. Regional weather swings complicate application timing and inflate insurance premiums against performance failure. Suppliers invest in UV-protective encapsulation and thermotolerant strains, but added R&D costs lift final prices. Northern states face the sharpest shortfalls, slowing the overall progress of the Brazil biopesticides market until climate-resilient formulations scale.

Cold-chain and storage gaps

Refrigeration shortfalls shorten product shelf life from twenty-four months to as few as eight, hiking distributor wastage and end-user costs by nearly 30%. Farmers in remote frontiers delay purchases, awaiting cooler months or resorting to synthetics. Logistics companies begin piloting solar-powered reefer hubs along key highways, yet full coverage remains years away, restraining uptake in underserved districts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Bioherbicides maintain top billing as bioinsecticides accelerate

Bioherbicides held 38.1% of the Brazil biopesticides market in 2024 and generated robust demand in soybean and corn, where weed control absorbs the largest share of crop protection budgets. Bioinsecticides are projected to expand at a 10.2% CAGR through 2030, fueled by escalating caterpillar outbreaks and export-driven residue strictures. The former segment leverages well-validated Bacillus formulations that deliver consistent suppression of Palmer amaranth and morning glory. Adoption rises fastest in the Midwest, where growers target glyphosate-resistant escapes. Corteva and Simbiose Agro’s May 2025 collaboration focuses on Trichoderma-based bioinsecticide solutions, reflecting a strategic pivot toward pest-control niches with limited chemical options. The dual momentum of herbicidal stability and insecticidal innovation cements steady double-digit advances across the broader Brazil biopesticides market.

Complementary product innovation sustains competitiveness. Liquid suspension concentrates dominate by share owing to equipment compatibility, while seed-applied biofungicides gain momentum for an early disease shield. Policy levers that remove registration bottlenecks allow suppliers to extend portfolios across modes, ensuring integrated weed and pest programs. As large farms blend bioherbicides and bioinsecticides into a unified rotation plan, formulators pursue multi-strain cocktails that widen efficacy windows and curb resistance build-up.

Crop Type: Row crops sustain volume, cash crops chase value

Row crops accounted for 79.2% of the Brazil biopesticides market size in 2024, with fastest fastest-growing CAGR of 9.8% as soybean and corn plantations embrace biological solutions to offset chemical fatigue and meet export pledges. Farms exceeding 10,000 hectares build biofactories to secure cost certainty and timely supply. High-value horticulture remains a niche in absolute terms yet sets the benchmark for integrated pest management protocols.

The row crop segment’s scale underwrites R&D investments in strain discovery and precision application, spinning off innovations later repurposed for specialty acreage. Agronomists design rotation calendars that combine seed-applied Trichoderma with foliar Beauveria, smoothing demand spikes throughout the season. This segmentation cascade anchors predictable consumption patterns within the Brazil biopesticides market.

Geography Analysis

Brazil’s regional adoption landscape mirrors agronomic intensity, infrastructure maturity, and export orientation. The Midwest leads with a 45% slice of 2024 sales and posts an 11.2% CAGR outlook, fueled by soybean and corn mega-farms that absorb technology at scale. Mato Grosso alone processes more than 2.5 million hectares with biologicals, banking on residue-free certification to secure European and Chinese contracts. Government-backed credit eases capital expenditure on on-farm fermenters, allowing growers to cut procurement costs and guarantee supply during high-pressure windows.

The South’s 32% share results from long-established agribusiness clusters and dense extension networks. Progressive growers in Rio Grande do Sul pioneered rotational use of Trichoderma seed treatments and Beauveria foliar sprays, showing consistent yield resilience and cost parity with chemical programs. Although its CAGR moderates to 8.9% amid maturity, the region continues to incubate product and formulation innovation that later diffuses nationwide.[3]Source: Brazilian Association of Biological Control, “Market Development Report 2024,” controlebiologico.com.br

The Southeast, Northeast, and North together own a 23% share but highlight the Brazil biopesticides market’s next growth frontier. Sugarcane mills in São Paulo deploy Bacillus biofungicides to curb brown rust, while citrus sectors adopt semi-commercial orchard spraying protocols. Northeast cotton growers turn to bioinsecticides to tackle bollworm outbreaks as chemical efficacy wanes. Amazonian frontier clearings pivot toward biologicals early, aiming to avoid resistance mistakes seen elsewhere. Cold-chain expansion, digital advisory apps, and mobile reefer stations gradually dismantle logistical barriers, positioning these zones for 12% plus CAGR through 2030.

Competitive Landscape

Market concentration remains low, signaling space for both consolidation and specialization. Vittia Group leads by leveraging local fermentation capacity and a forty-seven-product biological lineup. FMC follows after acquiring Ballagro technology to enrich its microbial catalog. Coromandel International focuses on Bacillus-based biofertigation solutions tailored to high-pH soils.

Strategic alliances define competition. Corteva partnered with Simbiose Agro to co-develop Trichoderma insecticides that meet strict EU residue demands. BASF fast-tracked its Velifer Bacillus thuringiensis launch through MAPA’s expedited pathway, bolstering credibility among soy growers. UPL’s minority stake in Biotrop grants access to native strain libraries and a robust distributor network. Patent filings surged 340% from 2020 to 2024, underscoring the innovation race and raising the likelihood of cross-licensing negotiations.

Digital agriculture capabilities increasingly differentiate suppliers. Bayer’s Paulínia center integrates UAV delivery research, while Syngenta and the University of São Paulo refine IoT-enabled timing algorithms. Firms that pair strong microbial portfolios with precise application tech position themselves to capture premium contracts and stem newcomer erosion, sustaining competitive vigor in the Brazil biopesticides market.

Brazil Biopesticides Industry Leaders

Atlántica Agrícola

Coromandel International Ltd

FMC Corporation

Valent Biosciences LLC

Vittia Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Corteva Agriscience forged a strategic partnership with Simbiose Agro to co-develop and market Trichoderma-based bioinsecticides aimed at lepidopteran pests in corn and soybean systems. The agreement combines Corteva’s global discovery infrastructure with Simbiose’s localized strain optimization and regulatory expertise.

- January 2025: Amaggi Group commissioned its BRL 120 million (USD 24 million) biofactory in Mato Grosso, capable of producing Bacillus and Trichoderma inputs for 500,000 hectares each season. The facility integrates closed-loop quality monitoring and positions Amaggi to reduce input costs by 25% versus commercial purchases.

- March 2024: BASF SE launched Velifer, a Bacillus thuringiensis bioinsecticide tailored to withstand Brazil’s high UV index, after securing priority registration through MAPA’s biological pathway. Field trials recorded 92% worm suppression within seventy-two hours.

Brazil Biopesticides Market Report Scope

The Brazil Biopesticides Market Report is Segmented by Form (Biofungicides, Bioherbicides, and Bioinsecticides), and Crop Type (Cash Crops, Row Crops, and Horticultural Crops). The Market Forecasts are Provided in Terms of Value (USD) and Volume (metric Tons).

Form

| Biofungicides |

| Bioherbicides |

| Bioinsecticides |

| Other Biopesticides |

Crop Type

| Cash Crops |

| Horticultural Crops |

| Row Crops |

| Form | Biofungicides |

| Bioherbicides | |

| Bioinsecticides | |

| Other Biopesticides | |

| Crop Type | Cash Crops |

| Horticultural Crops | |

| Row Crops |

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of biopesticides applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - The Crop Protection function of agirucultural biological include products that prevent or control various biotic and abiotic stress.

- TYPE - Biopesticides prevent or control various pests, including insects, diseases, and weeds, from causing crop damage and yield loss.

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.