Brain-computer Interface Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 1.4 Billion |

| Market Size (2031) | USD 2.26 Billion |

| Growth Rate (2026 - 2031) | 10.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brain-computer Interface Market Analysis by Mordor Intelligence

Brain-computer Interface market size in 2026 is estimated at USD 1.4 billion, growing from 2025 value of USD 1.27 billion with 2031 projections showing USD 2.26 billion, growing at 10.1% CAGR over 2026-2031.

Capital inflows, maturing hardware platforms, and the pairing of neural decoding with advanced artificial intelligence are the primary forces behind this expansion. Venture funding continues to shorten commercialization timelines, hospitals accelerate early adoption of implantable solutions, and consumer-facing headsets extend the reach of the Brain-Computer Interface market into gaming, well-being, and human–machine symbiosis. Hybrid signal architectures and software-defined features further support product differentiation, while government-funded clinical trials push forward standards for safety and ethics [1]Source: National Institutes of Health, “Brain-computer interface helps paralyzed man speak,” nih.gov . On the demand side, rising prevalence of neuro-degenerative disorders and heightened expectations for assistive communication tools keep clinical users at the core of revenue generation.

Key Report Takeaways

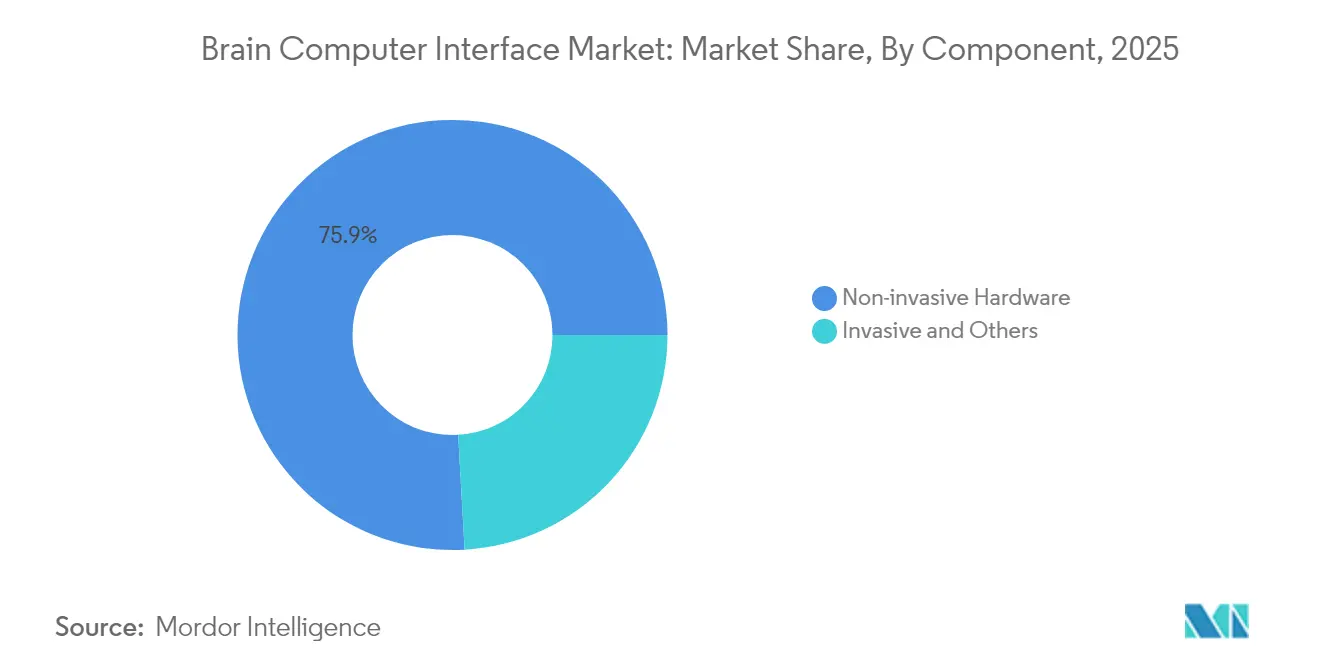

- By component, non-invasive hardware held 75.90% of the Brain-Computer Interface market share in 2025; software and algorithms post the fastest 11.88% CAGR through 2031.

- By interface type, motor/output BCIs led with 50.30% revenue share in 2025; hybrid systems advance at a 13.34% CAGR to 2031.

- By application, neuro-prosthetics captured 49.10% of the Brain-Computer Interface market size in 2025, while communication and control applications rise at 12.78% CAGR.

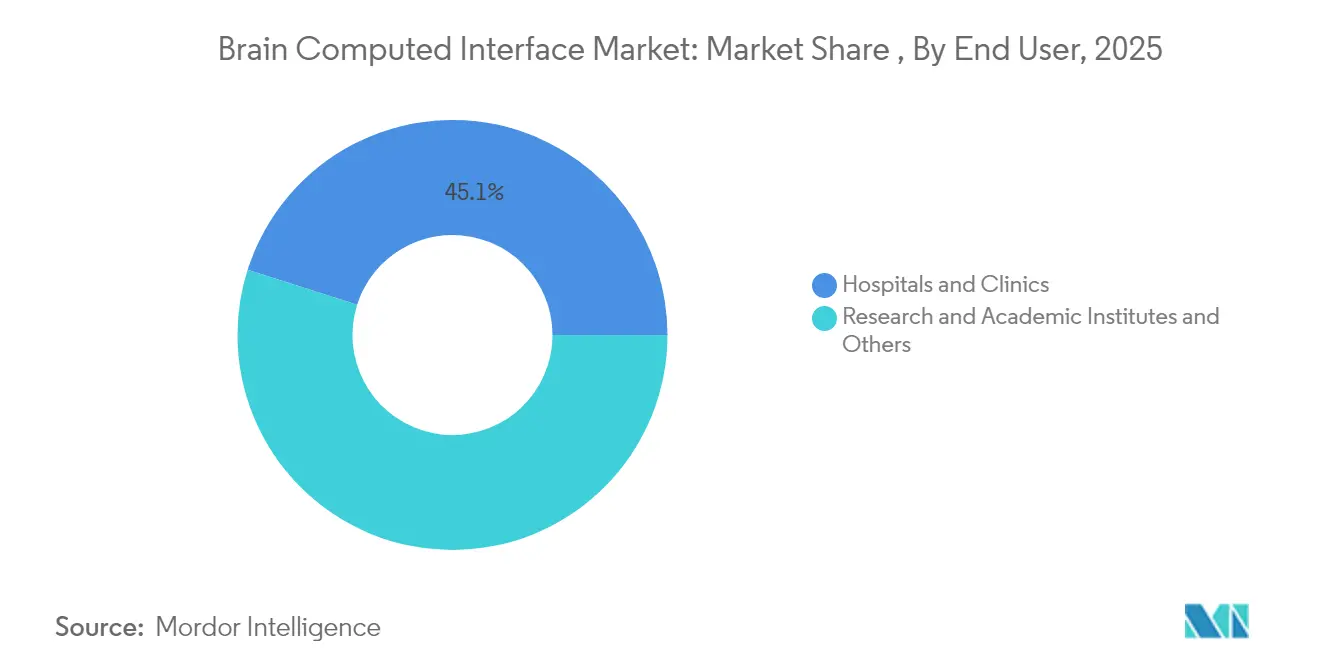

- By end-user, hospitals and clinics commanded 45.10% share of the Brain-Computer Interface market in 2025; research and academic institutes record the highest projected 12.29% CAGR.

- By geography, North America contributed 48.10% to 2025 revenues; Asia-Pacific is set to register a 12.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Brain-computer Interface Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Surging demand for assistive communication technologies for ALS and severe paralysis patients | ~+2.3 | Global, with emphasis on North America and Europe | Medium term (~ 3-4 yrs) |

| Rapid adoption of EEG-based wearable headsets by eSports and gaming companies | ~+1.5 | North America, Europe, East Asia | Short term (≤ 2 yrs) |

| High VC funding in neuro-tech hubs (Silicon Valley, Lausanne, Vienna) accelerating product commercialization timelines | ~+2.1 | North America (Silicon Valley), Europe (Lausanne, Vienna) | Short term (≤ 2 yrs) |

| Rising R&D Activities by Government to Improve the Brain-computer Interface Technology | ~+1.8 | Global, with emphasis on US, UK, China | Medium term (~ 3-4 yrs) |

| Rising prevalence of neuro-degenerative disorders in ageing populations of Japan and EU spurring clinical trials | ~+1.4 | Japan, EU, North America | Long term (≥ 5 yrs |

| Source: Mordor Intelligence | |||

Surging demand for assistive communication technologies

National Institutes of Health–backed research restored intelligible speech for a paralyzed patient with 99% word-level accuracy [2]. Synchron subsequently paired its Stentrode implant with a generative-AI model, enabling hands-free texting for additional users. Hospitals report shorter caregiver cycles and higher patient-autonomy scores, expanding the clinical addressable pool beyond ALS to traumatic spinal-cord injury and brain-stem stroke (user data). Private insurers in the United States have begun reviewing early reimbursement cases for speech-decoding implants, indicating growing payer recognition of durable quality-of-life gains. European teaching hospitals now integrate language-model–enhanced BCIs in multidisciplinary neuro-rehabilitation programs, reinforcing mid-term adoption across the region.

Rapid adoption of EEG-based wearable headsets

Gaming studios, e-sports organizers, and consumer-wellness brands integrate dry-electrode headsets into interactive titles, fitness programs, and meditation platforms. Streamers demonstrate full-gameplay control with neural inputs, while competitive leagues trial concentration and emotional-state data for coaching. These deployments sharpen algorithms for low-latency signal extraction, accelerate miniaturization, and educate non-medical audiences on everyday benefits of brain–computer interaction. As shipments grow, economies of scale begin to lower unit costs, allowing vendors to bundle subscription-based analytics that deepen revenue per user.

High VC funding in neuro-tech hubs

Single-round investments surpassing USD 100 million enable rapid scale-up of clean-room electrode fabrication, animal studies, and early human trials. Capital clustering in Silicon Valley, Lausanne, and Vienna fuels a dense knowledge network that transfers best practices across start-ups, universities, and contract manufacturers. Portfolio diversification by cryptocurrency platforms and cloud-service providers signals cross-industry confidence in neural interface monetization. Investors demand accelerated regulatory filings, prompting firms to raise internal quality-assurance capabilities and shorten iteration cycles between prototype and pivotal trial.

Rising R&D activities by government

The United Kingdom’s National Health Service allocated GBP 69 million to precision-neurotechnology trials, including a GBP 6.5 million study evaluating ultrasound-based mood-enhancement BCIs. China’s Ministry of Industry and Information Technology listed brain-machine interfaces as a strategic priority and formed a national standard-setting committee. The U.S. Government Accountability Office meanwhile recommended policy frameworks to clarify data ownership and reimbursement pathway.

Restraints Impact Analysis of Brain-computer Interface Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Surgical risks and regulatory hurdles limiting adoption of implantable BCI systems | -1.9 | Global | Medium term (~ 3-4 yrs) |

| Data-privacy concerns over neural data collection | -1.2 | North America, Europe | Short term (≤ 2 yrs) |

| Signal accuracy challenges due to hair & scalp impedance in mass-market EEG devices | -1.0 | Global, with emphasis on consumer markets | Short term (≤ 2 yrs) |

| Scarcity of reimbursement codes for BCI-based rehabilitation therapies in public healthcare systems | -0.7 | Global, with emphasis on emerging markets | Medium term (~ 3-4 yrs) |

| Source: Mordor Intelligence | |||

Surgical risks and regulatory hurdles

Implantable systems deliver superior signal fidelity yet involve cranial or vascular procedures that few centers can perform. Reports of electrode migration, infection, and device retrieval create caution among clinicians and insurers. Regulatory agencies require lengthy safety monitoring, stretching time-to-market and inflating trial budgets. These obstacles confine early adoption to well-funded academic hospitals and wealthy self-pay patients, slowing broad penetration. Vendors respond by refining stent-like delivery tools and developing reversible implants but must still navigate multi-year approval pathways.

Data-privacy concerns over neural data collection

Legislators classify neuro-data as sensitive, forcing firms to maintain explicit consent, local storage options, and granular user controls. The absence of federal standards in the United States and differing regional rules in Europe add integration complexity for cloud services. Consumer groups warn that thought-pattern analytics could reveal intent, political views, or mental-health status, deterring mass-market uptake of wellness and gaming headsets. Companies are now embedding on-device encryption, edge-processing, and data-anonymization features to bolster trust, though compliance overhead increases development costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Brain-computer Interface Market Segment Analysis

By Component:

Non-invasive hardware retains leadership while software acceleratesNon-invasive headsets and electrode arrays generated 75.90% of 2025 revenue, underscoring their role as the entry point for many developers in the Brain-Computer Interface market. Product launches with dry electrodes and low-energy Bluetooth have reduced setup times and improved comfort, enabling everyday usage scenarios such as virtual-reality gaming and remote neurofeedback. Hospitals appreciate the avoidance of surgical risk, and consumer brands leverage lower regulatory hurdles to speed shelf placement. Price declines and improved signal-to-noise ratios continue to support double-digit growth despite intensifying competition.

Software and algorithm layers are expanding at a 1Mass General Brigham, “Implantable Brain-Computer Interface Collaborative Community,” massgeneralbrigham.org 1Mass General Brigham, “Implantable Brain-Computer Interface Collaborative Community,” massgeneralbrigham.org.88% CAGR, a pace that outstrips hardware because every incremental headset installation yields recurring licensing opportunities. Transformer-based decoders, transfer learning, and self-calibrating frameworks raise information-transfer rates by triple-digit percentages. These advances create an emergent SaaS sub-segment forecast to climb from USD 0.38 billion to USD 0.97 billion by 203 1Mass General Brigham, “Implantable Brain-Computer Interface Collaborative Community,” massgeneralbrigham.org. Service providers follow close behind, offering cloud dashboards, electrode-maintenance contracts, and compliance audits to clinical buyers who lack in-house specialists. Together, these activities sustain a balanced revenue mix that shields vendors from pure hardware margin compression.

By Interface Type:

Motor/output dominates while hybrid systems surgeMotor/output platforms accounted for 50.30% of spending in 2025, reflecting clinical priorities around restoring cursor control, wheelchair navigation, and prosthetic manipulation for paralysis patients. Successful demonstrations of non-invasive deep-learning decoders capable of sub-second response rates have widened appeal beyond the intensive-care unit. Consumer developers adapt these breakthroughs to gesture-less input for augmented-reality headsets and smart-home devices, reinforcing the segment’s maturity.

Hybrid architectures, combining EEG, electromyography, functional near-infrared spectroscopy, or focused ultrasound, are on course for 1Mass General Brigham, “Implantable Brain-Computer Interface Collaborative Community,” massgeneralbrigham.org3.34% CAGR. They lift reliability by fusing multiple neural and peripheral signals, thereby compensating for artifacts that hamper single-modality systems. Experimental stroke-rehabilitation rigs illustrate the benefit: after two weeks of hybrid brain-muscle training, 83% of patients regained measurable hand function. As component costs fall, hybrid circuitry will migrate from the laboratory into modular consumer accessories.

By Application:

Neuro-prosthetics steers revenue while communication acceleratesNeuro-prosthetics and motor-restoration solutions controlled 49. 1Mass General Brigham, “Implantable Brain-Computer Interface Collaborative Community,” massgeneralbrigham.org0% of 2025 sales, cementing their place at the heart of the Brain-Computer Interface market. Direct cortical stimulation now delivers tactile feedback on shape, pressure, and texture, enabling more intuitive use of robotic limbs. Regulatory bodies prioritize these life-changing therapies, granting breakthrough-device designations that streamline pivotal trials. Military-medicine grants and insurance pilots further reinforce a resilient reimbursement outlook for neuro-prosthetic indications.

Communication and control systems are the fastest-growing at a 1Mass General Brigham, “Implantable Brain-Computer Interface Collaborative Community,” massgeneralbrigham.org2.78% CAGR as language-model integration trims keystrokes by more than half and multiplies transfer rates. Universal BCIs that bypass personalized calibration shrink training time, promising scalable deployment across rehabilitation centers and home-care settings. Early success stories of thought-based texting foster public awareness, while social-media coverage accelerates uptake among tech-savvy patients. Secondary applications in cognitive-state monitoring and digital wellness broaden market horizons.

By End-User:

Hospitals dominate while research institutes accelerateHospitals and clinics governed 45. 1Mass General Brigham, “Implantable Brain-Computer Interface Collaborative Community,” massgeneralbrigham.org0% of 2025 turnover owing to their role in complex implant surgeries, long-term rehabilitation, and multidisciplinary care teams. Top academic centers run parallel programs in speech restoration, sensory feedback, and neuromodulation, allowing device manufacturers to access diverse patient cohorts under a single contractual framework. Collaborative bodies such as the Implantable Brain-Computer Interface Community align protocol standards, reducing administrative drag for trial sponsors.

Research and academic institutes will expand at 1Mass General Brigham, “Implantable Brain-Computer Interface Collaborative Community,” massgeneralbrigham.org2.29% CAGR through 203 1Mass General Brigham, “Implantable Brain-Computer Interface Collaborative Community,” massgeneralbrigham.org as engineering, psychology, and computer-science faculties form cross-disciplinary labs, often with venture-capital participation. Grants targeting hybrid reality, adaptive learning, and precision mental-health interventions stimulate prototype production well ahead of commercial scale. These campuses double as talent pipelines for start-ups and large device companies, ensuring a steady flow of innovation into future product generations.

Geography Analysis

North America Brain-computer Interface Market

North America generated 48. 1Mass General Brigham, “Implantable Brain-Computer Interface Collaborative Community,” massgeneralbrigham.org0% of 2025 revenue and remains the anchor of the Brain-Computer Interface market. National Institutes of Health funding, deep venture pools, and specialized surgical teams underpin a continuous trial pipeline that spans speech decoding, bidirectional sensation, and neuromodulation for depression. The region benefits from early adopter health systems that integrate reimbursement studies into clinical workflows, accelerating payer acceptance. Privacy legislation is evolving rapidly, creating both compliance overhead and competitive advantage for firms that invest early in secure data architectures.

APAC Brain-computer Interface Market

Asia-Pacific delivers the fastest 1Mass General Brigham, “Implantable Brain-Computer Interface Collaborative Community,” massgeneralbrigham.org2.38% CAGR, propelled by Chinese government designation of brain-machine interfaces as a strategic industry. State grants encourage industrial-academic consortia, while new standards bodies tackle signal-acquisition protocols and ethical guidelines. Chinese start-ups have already demonstrated 7 1Mass General Brigham, “Implantable Brain-Computer Interface Collaborative Community,” massgeneralbrigham.org% accuracy in decoding Mandarin speech, underscoring regional momentum. Japan’s aging demographics add a structural demand driver for neuro-degenerative disease management, and South-Korean electronics majors contribute sensor miniaturization expertise.

EMEA and South America Brain-computer Interface Market

Europe holds a significant share, with public-health systems funding mood-enhancement trials and stroke-recovery programs. The National Health Service’s GBP 6.5 million ultrasound-based BCI trial reinforces policy-level commitment to non-pharma approaches for mental-health conditions. The forthcoming EU AI Act classifies many AI-enabled medical devices as high-risk, compelling vendors to adopt rigorous cyber-security and performance-validation procedures that can become competitive differentiators in other regions. Smaller but growing markets in the Middle East, Africa, and South America invest in tele-rehabilitation and remote neuromonitoring, leveraging mobile connectivity and cross-border training partnerships.

Regulatory Landscape

Regulation for brain-computer interfaces continues to split between clinical-grade implantable systems and lower-risk non-invasive devices, with the United States anchored by US Food and Drug Administration pathways for neurological devices and early-stage BCI feasibility studies under IDEs. Because this report sits in a device-drug combination context, Primary Mode of Action (PMOA) determination remains a gating step for products that pair neural interfaces with medicinal or biologic components, directing review via the FDA Office of Combination Products to CDRH, CDER, or CBER and shaping whether the submission follows device-led pathways (PMA/510(k)) or drug/biologic-led routes.

Internationally, EU market access for drug-device combinations relies heavily on Notified Bodies assessing conformity to MDR General Safety and Performance Requirements for the device constituent, raising documentation burden for usability, risk management, and biocompatibility. Standardization is tightening for interoperability and data handling: ISO/IEC 8663:2025 (published September 2025) formalizes BCI vocabulary, and ISO/IEC TS 27571:2026 (published April 2026) specifies data formats for non-invasive brain information collection (including EEG and fNIRS). In parallel, ISO/IEC JTC 1/SC 43 continues to develop reference architectures and testing protocols, including for non-medical post-market surveillance, which affects how consumer headset vendors structure data pipelines and compliance controls across regions.

Competitive Landscape

Competitive Landscape

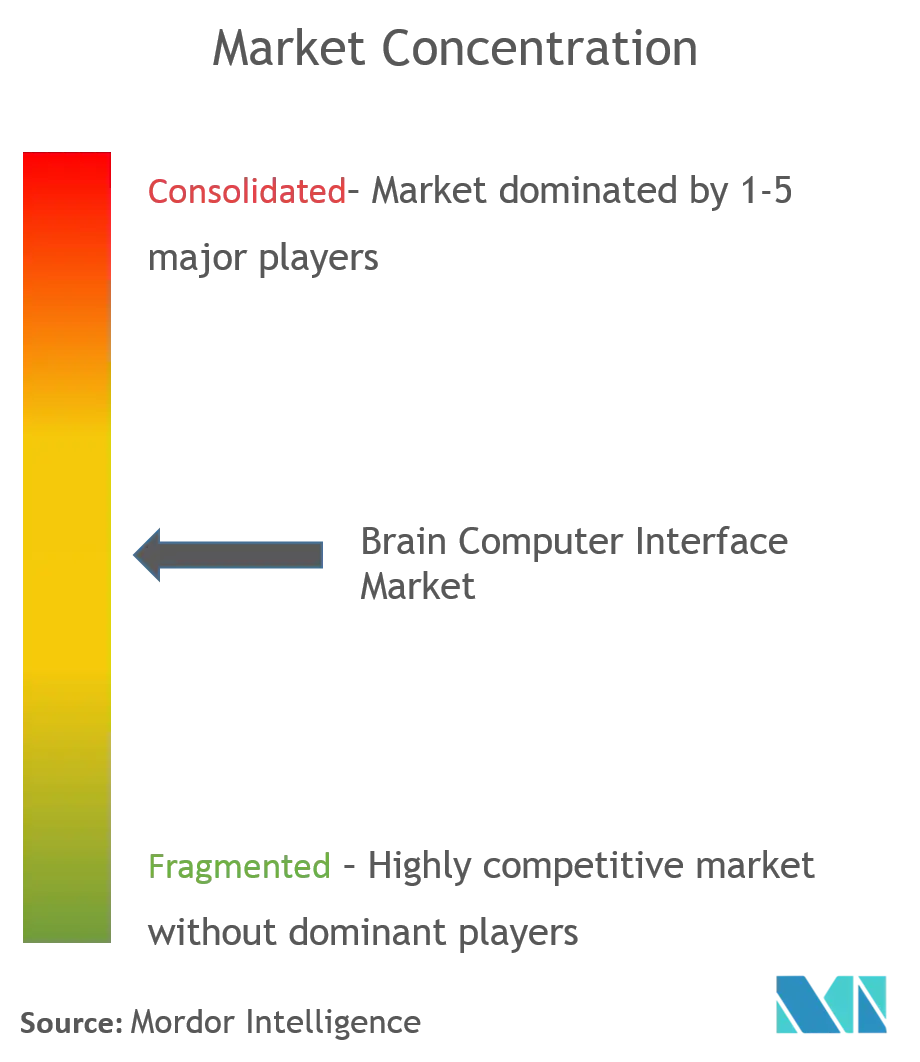

The Brain-Computer Interface market is moderately fragmented, with dynamic interplay among incumbent med-tech manufacturers, venture-backed specialists, and technology conglomerates. Leading invasive-device companies secure multi-year hospital contracts by showcasing clinical-trial outcomes that document restored speech, typing, and limb movement. Non-invasive consumer-focused vendors chase scale through mass production of affordable EEG headsets bundled with cloud analytics. Technology giants explore in-house silicon and software stacks that promise deeper ecosystem integration.

Strategic alliances redefine market boundaries. Cryptocurrency investors acquiring controlling stakes in implantable BCI firms inject liquidity and expand payment-system interoperability for future neuro-app stores. Cloud-service providers partner with headset makers to co-develop low-latency neural-processing interfaces that feed edge-computing platforms. Meanwhile, emergent disruptors scale wafer-thin cortical grids with electrode counts exceeding 1,000, opening paths to high-resolution sensory feedback.

White-space opportunities center on hybrid architectures that couple central-nervous, peripheral-nervous, and muscle signals into unified control schemas. Demand also rises for verticalized solutions targeting speech disorders, chronic pain, and mental-health applications. Vendors differentiate by embedding advanced encryption, local-inference engines, and clinician-friendly dashboards that simplify longitudinal monitoring. As value shifts toward software brilliance and service reliability, pricing power migrates away from pure hardware and toward full-stack neuro-platforms.

Brain-computer Interface Industry Leaders

Natus Medical Incorporated

Compumedics Ltd

EMOTIV

g.tec medical engineering GmbH

NeuroSky

- *Disclaimer: Major Players sorted in no particular order

Brain-computer Interface Market Companies Covered in this Report

- g.tec medical engineering

- Blackrock Neurotech

- Emotiv, Inc.

- NeuroSky, Inc.

- Kernel

- Paradromics, Inc.

- MindMaze SA

- Cognixion

- CTRL-Labs (Meta Platforms)

- NextMind (Snap Inc.)

- OpenBCI

- Synchron

- Neurable

- BrainCo, Inc.

- Interaxon Inc. (Muse)

- Bitbrain Technologies

- Cyberkinetics

- Nihon Kohden

- Compumedics

- Alea Neurotherapeutics

Market Opportunities and Future Outlook

A core commercialization whitespace is the transition from laboratory-supervised BCI use to routine home use with reduced specialist intervention, which directly expands the addressable service and software layer in hospitals, clinics, and home-care settings. Peer-reviewed BrainGate2 evidence in 2026 highlights this shift in practical utility: published results reported thousands of hours of independent at-home use over a multi-month period and demonstrated a touch-typing neuroprosthesis reaching 22 words per minute, both of which raise demand for workflow software, automated setup, and remote monitoring toolchains rather than one-off hardware sales.

Regulatory and standards activity creates additional room for vendors to differentiate via updateable decoding software and data interoperability. FDA programs such as Breakthrough Devices are being used by developers pursuing speech restoration (for example, Neuralink received a Breakthrough Device designation in May 2025), while the absence of full FDA PMA for motor-control BCI systems (as of July 2026) keeps near-term spending concentrated in clinical trials, quality systems, and evidence generation. With ISO/IEC TS 27571:2026 standardizing non-invasive BCI data formats, opportunities expand for cross-device analytics, third-party algorithm marketplaces, and multi-center trial harmonization, particularly for software and algorithm providers that can support secure, regulator-friendly update processes (including Predetermined Change Control Plan approaches for AI-driven decoders).

Recent Industry Developments in Brain-computer Interface Market

- March 2026: Natus Medical Incorporated announced the global launch of autoSCORE, an AI analysis tool for clinical EEG interpretation, supported by FDA 510(k) clearance and a CE mark. The release strengthens standardized EEG analytics and report automation, capabilities that support BCI-adjacent signal processing workflows and can lower interpretation bottlenecks in clinical neurotechnology programs.

- May 2025: Neuralink received FDA Breakthrough Device designation for a speech restoration device. The designation increases the intensity and structure of FDA interactions for a high-impact BCI indication and reinforces the industry focus on assistive communication outcomes as an early clinical pathway.

- July 2024: Synchron demonstrated control of Apple Vision Pro using its implanted BCI for users with limited mobility. The interoperability milestone connected an implantable neural interface to a major consumer computing platform, sharpening the value proposition for ecosystem partnerships and expanding BCI use cases beyond purely clinical endpoints.

Brain-computer Interface Market Report Scope and Research Methodology

Market Definition and Coverage

This market is defined as revenue generated from brain-computer interface systems that capture brain signals, translate them into digital commands, and enable control of a device or software, covering hardware, supporting software, and related services across major end users.

Scope exclusions: Neurostimulation implants that do not decode brain signals and stand-alone AR or VR headsets without neural sensors are excluded.

Segments Covered in This Report

- By Component (Value)

- Hardware

- Invasive

- Non-invasive

- Others

- Software & Algorithms

- Services

- Hardware

- By Interface Type (Value)

- Motor / Output BCI

- Communication BCI

- Passive / Monitoring BCI

- Hybrid BCI

- By Application (Value)

- Neuro-prosthetics & Motor Restoration

- Communication & Control

- Others

- By End-User (Value)

- Hospitals & Clinics

- Research & Academic Institutes

- Others

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia- Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with aligning what is counted as a BCI sale, and then collecting anchor indicators that explain demand and adoption. We mainly refer to public sources such as FDA device databases and clearances, the National Institutes of Health (NIH) funding and publication records, the World Health Organization (WHO) neurological condition statistics, OECD health data, and IEEE or peer-reviewed neuroscience and biomedical engineering journals.

Next, market context is built using company annual reports, investor presentations, clinical trial registries, university lab releases, and reputable press coverage of pilot deployments. Paid subscriptions are used in a limited way for company financials and intelligence, news and financials, patent databases, and shipment-level import and export checks where trade coding allows meaningful signal. The sources listed here are illustrative, and many other public references were used to cross-check, validate, and clarify data points.

Primary Interviews and Surveys

Primary work is used to validate how BCI revenues form in practice, including average selling price ranges, typical device and software bundling, and the time lag between trials and commercial rollouts. We speak with a mix of device developers, component and software specialists, clinical users, research groups, and channel partners across APAC, EMEA, and the Americas so assumptions can be challenged and then tightened.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | APAC: 45% |

| Mid tier: 47% | Functional/Unit leaders: 40% | EMEA: 32% |

| Smaller Players: 20% | Managers: 47% | Americas: 23% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where the addressable demand pool is reconstructed using observable adoption signals, and then filtered by what qualifies as a BCI purchase. For example, procedure and trial activity, the installed base of EEG and implanted sensing systems used for BCI, hospital and research lab procurement patterns, and the pace of regulatory clearances are used to shape year-by-year volumes, which are then converted into value using typical ASP ranges.

The totals are then corroborated with selective bottom-up approximations, such as rolling up a sample set of supplier revenues, checking channel pricing, and testing volume times ASP for key use cases to make sure the outcome stays realistic. Where company disclosures are limited, gaps are handled using peer-group benchmarks and adoption ratios validated in expert calls. Forecasts are produced using scenario analysis supported by a short set of drivers, including device pricing progression, clinical pipeline conversion into commercial deployments, funding intensity for neurotech research, and regional readiness of clinical infrastructure, and then we sanity-check the trend against expert expectations.

Data Validation & Update Cycle

Outputs are validated through a set of checks that compare the model to independent signals, and then investigate any unusual jumps before final sign-off. We run variance checks across regions, compare implied volumes against known deployment capacity, and review whether pricing assumptions match what is seen in channel conversations and public procurement references.

A multi-step analyst review is completed, and respondents are re-contacted when mismatches appear around adoption timing, pricing, or what is being counted as BCI revenue. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery review pass is done so clients receive the latest updated view.

Mordor Intelligence's Brain Computer Interface Market Size Measured Against Other Published Estimates

Published market sizes for brain-computer interfaces can look far apart because different studies count different product families, choose different base years, and apply different assumptions for pricing and deployment speed. In practice, even small differences in what is treated as a BCI sale can shift the total value quickly.

Neurostimulation implants that do not decode brain signals sit outside Mordor Intelligence's scope, and that single exclusion can pull the market size down versus studies that blend stimulation, sensing, and broader neurotech together. Other common gap drivers include whether consumer wellness headsets are counted as BCI, how multi-year service revenue is recognized, how ASP decline is modeled as volumes rise, and whether currency conversion is applied at annual average rates or held constant.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.40 B (2026) | |

| Trade Publisher A | USD 2.10 B (2023) | Uses an earlier base year and a broader segmentation frame that can pick up adjacent neurotechnology revenues, and then projects forward with a faster commercialization ramp, which inflates the comparable total. |

| Global Research Desk B | USD 2.62 B (2025) | Typically applies a wider product and application lens and a higher growth track, and the scope description is less explicit about excluding non-decoding neuro devices, so the counted revenue pool can be larger. |

The table shows that the spread is largely explained by what is included as BCI revenue and the year chosen for the starting point. By keeping the inputs tied to adoption signals, pricing ranges, and validation calls that can be repeated, our estimate stays traceable to clear steps and practical assumptions.

Key Questions Answered in the Report

Q1. What is the current value of the Brain-Computer Interface market?

A1. The Brain-Computer Interface market size reached USD 1.4 billion in 2026 and is projected to reach USD 2.26 billion by 2031 at a 10.10% CAGR.

Q2. Which component category leads the Brain-Computer Interface market? -computer Interface Market size?

A2. Non-invasive hardware dominates with 75.90% share in 2025, supported by user-friendly headsets and lower regulatory hurdles.

Q3. Which application is growing fastest?

A3. Communication and control applications post the highest 12.78% CAGR to 2031, driven by AI-enhanced speech-decoding BCIs.

Q4. Why is Asia-Pacific the fastest-growing region?

A4. Focused government funding, standard-setting initiatives, and breakthroughs such as Mandarin speech decoding propel Asia-Pacific toward a 12.38% CAGR.

Q5. What are major restraints facing the market?

A5. Surgical risk for implantable systems and evolving neural-data privacy regulations subtract 1.9 percentage points and 1.2 percentage points from forecast CAGR respectively, necessitating design and compliance innovation.

Q6. How concentrated is competition among key players?

A6. With the top five companies holding around 35% of revenue, competition is moderately fragmented, fostering continuous product differentiation and partnership activity.

Page last updated on: