Cerebral Oximetry Monitoring Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

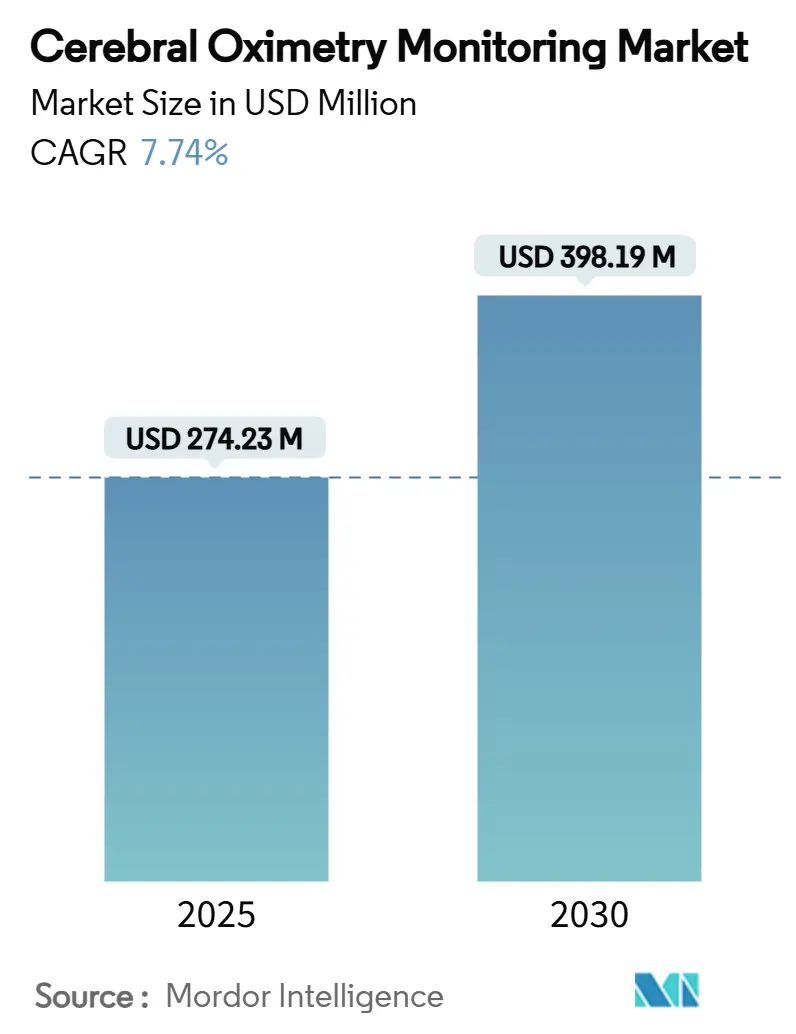

| Market Size (2025) | USD 274.23 Million |

| Market Size (2030) | USD 398.19 Million |

| Growth Rate (2025 - 2030) | 7.74% CAGR |

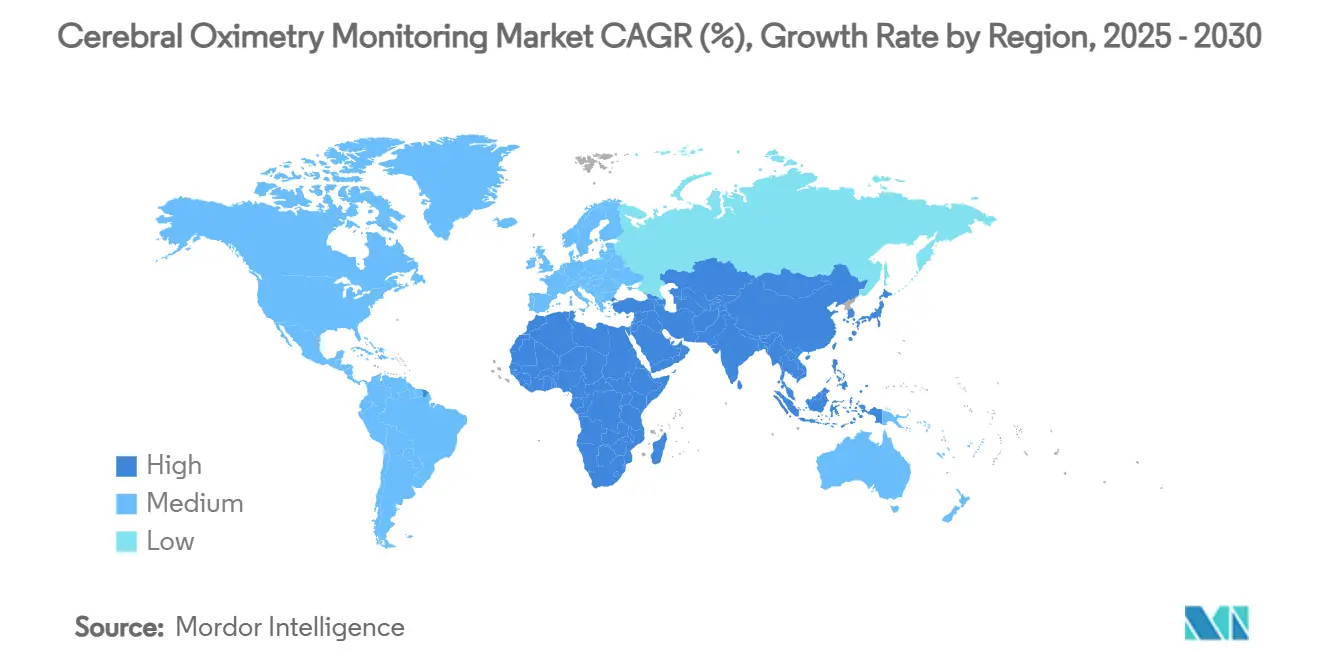

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cerebral Oximetry Monitoring Market Analysis by Mordor Intelligence

The cerebral oximetry monitoring market size reached USD 274.23 million in 2025 and is projected to expand at a 7.74% CAGR to touch USD 398.19 million in 2030. Enhanced patient-safety protocols, rising volumes of high-risk surgeries, and growing regulatory support for brain-protective monitoring underline the momentum. Hospitals are standardizing cerebral oxygen saturation thresholds across cardiothoracic, neuro, and neonatal theatres, pushing multi-parameter platforms that bundle cerebral oximetry with hemodynamic and EEG analytics. Manufacturers are layering artificial-intelligence algorithms onto near-infrared spectroscopy (NIRS) consoles to filter motion noise, flag impending desaturation events, and interface with electronic medical records. Disposable sensors dominate recurring revenues because infection-control norms favor single-use consumables, yet frequency-domain NIRS is accelerating as clinicians seek absolute tissue oxygenation values for complex cases. Regional growth pivots toward Asia-Pacific, where infrastructure upgrades and an aging population combine with government stimulus for advanced medical devices.

Key Report Takeaways

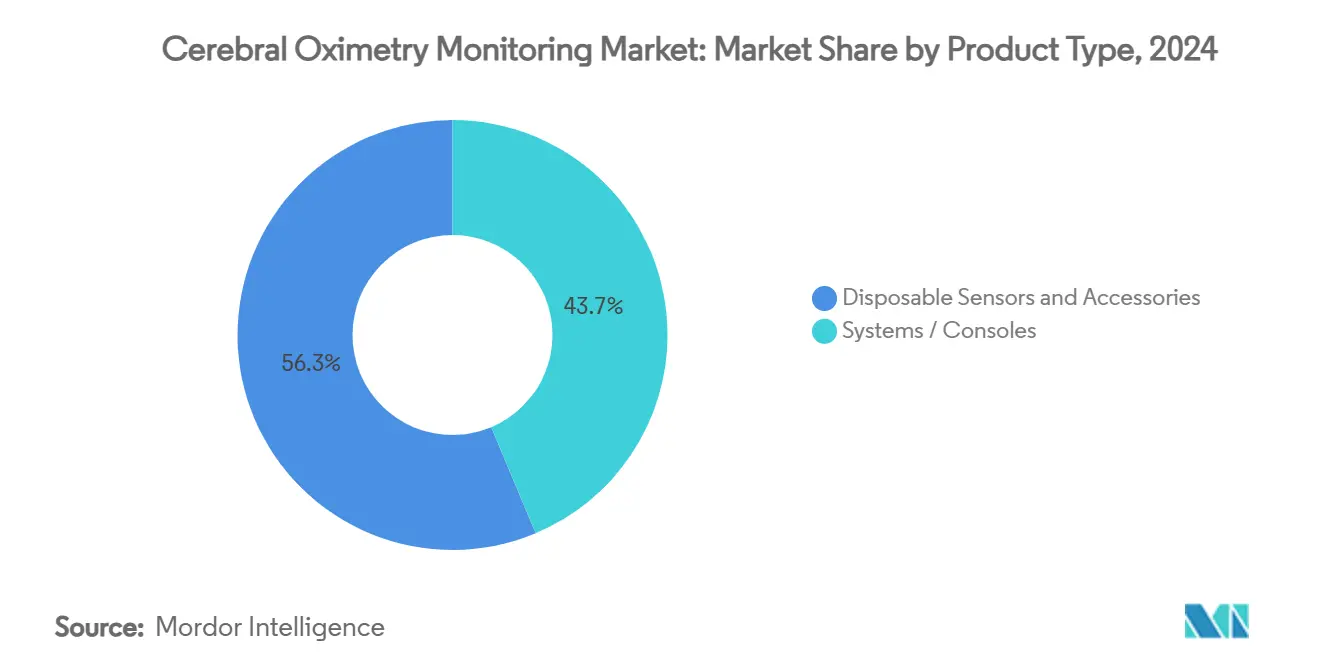

- By product type, disposable sensors captured 56.33% of the cerebral oximetry monitoring market share in 2024 and are projected to grow at an 11.26% CAGR through 2030.

- By technology, continuous-wave NIRS led with 62.58% of the cerebral oximetry monitoring market size in 2024, while frequency-domain NIRS is forecast to expand at a 10.69% CAGR to 2030.

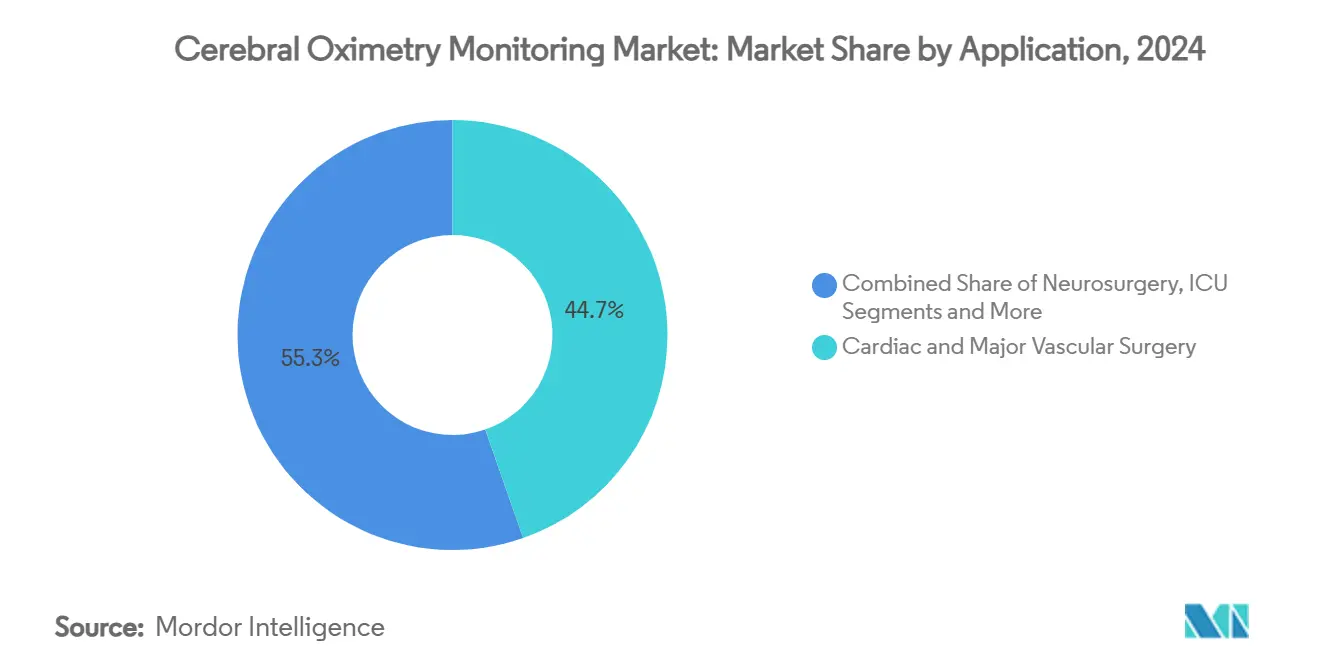

- By application, cardiac and major vascular surgery accounted for 44.67% of the cerebral oximetry monitoring market share in 2024; neonatology and pediatrics is advancing at an 11.88% CAGR through 2030.

- By end user, hospitals held 71.42% of the cerebral oximetry monitoring market size in 2024, whereas ambulatory surgical centers are climbing at a 9.35% CAGR to 2030.

- By geography, North America retained 41.68% of the cerebral oximetry monitoring market size in 2024, while Asia-Pacific is expected to register a 10.04% CAGR through 2030.

Global Cerebral Oximetry Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption in cardiac & vascular surgeries | +1.1% | North America & Europe, global diffusion | Medium term (2-4 years) |

| Increase in high-risk geriatric surgeries worldwide | +1.2% | Developed markets | Long term (≥ 4 years) |

| Neonatal intensive-care protocols mandating RSO₂ monitoring | +1.3% | Early uptake in Asia-Pacific, global spread | Short term (≤ 2 years) |

| AI-driven sensor fusion improving signal-to-noise ratios | +1.4% | North America & Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Emerging pay-for-performance models rewarding desaturation reduction | +1.5% | North America, pilots in Europe | Long term (≥ 4 years) |

| Regulatory clearances expanding indications | +1.1% | Global, led by FDA and CE Mark | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption in Cardiac & Vascular Surgeries

Cerebral oximetry is now embedded in cardiothoracic operating-room checklists because evidence links saturation below 60% during bypass to postoperative cognitive decline and kidney injury.[1]Bahi Hyasat et al., “Real-Time Blood Gas Management: Evaluating Quantum Perfusion System's Accuracy Against a Standard Blood Gas Analysis in CPB,” Journal of Cardiothoracic Surgery, cardiothoracicsurgery.biomedcentral.comCenters integrate brain oximetry with cardiac-output modules, allowing clinicians to titrate perfusion flow and arterial pressure proactively. AI algorithms correlate oxygen saturation trends with pump flow changes, offering predictive alerts many minutes before critical desaturation. Uptake is most visible in aortic arch reconstruction, ventricular-assist implantation, and complex congenital cases, where neurologic preservation translates into shorter ICU stays and lower readmission penalties. Cost-saving metrics under bundled-payment contracts reinforce adoption as hospitals prioritize value-based outcomes.

Increase in High-Risk Geriatric Surgeries Worldwide

Aging demographics boost volumes of hip fracture repairs, valve replacements, and oncologic resections performed on patients older than 70 years. These individuals are prone to cerebral hypoperfusion, delirium, and long-term cognitive loss. Meta-analysis places the global prevalence of postoperative hypoxemia at 16.76%, with geriatric cohorts experiencing the highest incidence.[2]Amare Belete Getahun, “Global Prevalence of Postoperative Hypoxemia Among Adult and Pediatric Surgical Patients: A Systematic Review and Meta-Analysis,” BMC Anesthesiology, bmcanesthesiology.biomedcentral.comHealth systems are therefore codifying cerebral oximetry in geriatric anesthesia bundles, aiming to curb extended-care costs linked to cognitive morbidity. Guidelines in the United States, Germany, and Japan recommend multimodal monitoring that incorporates brain oximetry alongside EEG depth assessment for elderly patients undergoing lengthy procedures.

Neonatal Intensive-Care Protocols Mandating RSO₂ Monitoring

Continuous regional cerebral oxygen saturation (RSO₂) readings have proven superior to intermittently checked SpO₂ in predicting intraventricular hemorrhage and hypoxic-ischemic encephalopathy. A 2025 systematic review documented significant RSO₂ gains after red-blood-cell transfusion in preterm infants.[3]Shao Cong Zheng and Shan He, “Near-Infrared Spectroscopy to Evaluate Neonatal Improvement After Transfusion: A Systematic Review and Meta-Analysis,” BMC Pediatrics, bmcpediatrics.biomedcentral.com The U.S. FDA’s clearance of pediatric-specific O3 sensors for patients 5–40 kg expanded device labeling, encouraging hospitals to align neonatal brain-protection bundles with real-time cerebral monitoring. Integrated platforms that stream RSO₂, heart rate, and ventilator parameters to a single dashboard support faster intervention, facilitating reduced incidence of cerebral palsy and developmental delays.

AI-Driven Sensor Fusion Improving Signal-To-Noise Ratios

Research labs have validated multi-wavelength, wireless NIRS headgear that uses machine-learning classifiers to suppress motion artifacts and ambient-light interference. Commercial vendors are porting similar algorithms into operating-room consoles, delivering stable readings even during electrocautery usage or patient repositioning. Predictive analytics trained on large desaturation event datasets now generate risk scores that notify anesthesia teams before cerebral hypoxia manifests clinically, enabling pre-emptive perfusion adjustments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High average selling price of disposable sensors | -0.8% | Emerging economies, cost-sensitive facilities | Short term (≤ 2 years) |

| Limited reimbursement in developing economies | -0.9% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Accuracy concerns in patients with dark skin or thick scalp | -0.7% | Global, diversity-rich regions | Medium term (2-4 years) |

| Limited plug-and-play interoperability with EMR platforms | -0.6% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Average Selling Price of Disposable Sensors

Single-use cerebral oximetry patches carry premium pricing because they embed multiple emitters and detectors plus shielding layers. While major hospitals absorb these costs, budget-constrained facilities delay adoption until vendors launch validated reusable options. Manufacturers are now prototyping disinfectable optical cuvettes that preserve signal fidelity while trimming per-procedure expense, but regulatory clearance cycles may limit near-term availability.

Limited Reimbursement in Developing Economies

Systematic review shows fragmented reimbursement grids impede diffusion of high-value monitoring tools in low-and-middle-income countries. Absent procedure codes for cerebral oximetry, hospitals rely on discretionary budgets or patient self-pay, dampening penetration despite clinical interest. Stakeholders lobby for inclusion of brain-monitoring bundles in national insurance formularies to unlock latent demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disposable Sensors Sustain Recurring Revenue Momentum

Disposable sensors contributed 56.33% of the cerebral oximetry monitoring market size in 2024, and their double-digit 11.26% CAGR to 2030 underscores the appeal of infection-free, ready-to-use consumables. Hospitals appreciate predictable ordering cycles and regulatory alignment with single-use infection-control guidelines. Manufacturers defend margins by bundling sensors with software subscriptions that unlock AI trend analysis dashboards. Systems and consoles growth remains tethered to new operating-room builds and replacement cycles; facilities refresh hardware to leverage wireless connectivity, depth-resolved algorithms, and integrated hemodynamic modules.

The recurring-revenue consumables model stabilizes corporate cash flow, incentivizing R&D investments in thinner adhesive substrates that contour to neonatal heads or obese adults without compromising optical coupling. As vendors roll out cloud-based analytics suites, each sensor activation streams de-identified data that can train predictive models, reinforcing technological lock-in.

By Technology: Continuous-Wave Dominance Meets Frequency-Domain Ascendancy

Continuous-wave NIRS maintained 62.58% of the cerebral oximetry monitoring market share in 2024 because its hardware is simpler, less costly, and thoroughly validated in routine surgical monitoring. Multi-channel CW devices satisfy most clinicians who require trend tracking rather than absolute saturation figures. However, frequency-domain NIRS, growing at 10.69% CAGR, now appeals to cardiovascular and neurocritical-care teams demanding quantifiable hemoglobin-oxygen values across deeper cortical layers. Hybrid consoles that toggle between CW and FD modes are emerging, allowing facilities to scale capabilities without purchasing separate platforms.

Time-domain NIRS remains a niche modality in academic centers analyzing cerebral autoregulation with picosecond photon-migration profiling. Although technical complexity restrains uptake, breakthroughs in compact laser diodes and on-chip time-correlated single-photon counting may broaden feasibility over the forecast horizon.

By Application: Cardiac Leadership Faces Neonatal Surge

Cardiac and major vascular surgery secured 44.67% of the cerebral oximetry monitoring market share in 2024 as perfusionists synchronized pump flow with cerebral saturation alarms. Evidence-driven guidelines from anesthesiology societies codify brain oximetry during complex bypass, cementing adoption. Yet neonatology and pediatrics, the fastest-growing application, is charting an 11.88% CAGR. Pediatric-specific sensors that address head-size variability and FDA clearances spur routine RSO₂ surveillance in premature infants. As neonatal survival rates climb, care teams intensify focus on long-term neurodevelopment, positioning cerebral oximetry as a cornerstone of brain-protection bundles.

Neurosurgery leverages direct cortical exposure to calibrate NIRS against micro-Doppler flow, while general intensive-care units increasingly incorporate brain oximetry for sepsis, ECMO, and traumatic brain injury patients. Emerging use cases, such as transcatheter aortic-valve replacements performed under conscious sedation, further diversify demand.

By End User: Hospitals Dominate, ASCs Accelerate

Hospitals generated 71.42% of the cerebral oximetry monitoring market size in 2024 because they host the bulk of high-acuity procedures requiring multimodal monitoring. Institutional purchasing committees deploy enterprise contracts that bundle consoles, disposable sensors, and post-processing software across surgical, ICU, and neonatal departments. Vendor-managed inventory models minimize stockouts, ensuring continuous availability.

Ambulatory surgical centers, posting a 9.35% CAGR, capitalize on minimally invasive techniques migrating to outpatient settings. As case complexity increases, anesthesiologists insist on brain-safety metrics comparable to hospital standards. Portable battery-powered NIRS units suit ASC workflow, offering fast setup and wireless data transfer to cloud EMRs. Specialty clinics, including interventional pain and sports-medicine facilities, represent early-stage users exploring cerebral oximetry for concussion management and high-altitude training evaluation.

Geography Analysis

North America commanded 41.68% of the cerebral oximetry monitoring market size in 2024, anchored by robust reimbursement, widespread clinical evidence, and multi-center registries that quantify neurologic outcome gains from brain oximetry. Strategic alliances, such as Sutter Health’s partnership with GE HealthCare to deploy AI-powered imaging and monitoring, reinforce technology diffusion.

Europe exhibits steady uptake as CE-marked devices benefit from the Medical Device Regulation’s post-market surveillance rules, encouraging data-driven adoption across Germany, France, and the Nordics. National health services are piloting pay-for-performance contracts that link bonus payouts to reduced postoperative delirium rates.

Asia-Pacific is the fastest-growing territory with a 10.04% CAGR through 2030. Japan’s revised QMS ordinance has lengthened submission requirements but simultaneously clarified clinical-evaluation pathways, prompting global manufacturers to expand local R&D footprints. China and India allocate infrastructure stimulus toward tertiary-care expansion, creating fresh console installations and accelerating disposable sensor volumes.

The Middle East & Africa and South America display nascent yet rising demand. Private centers in the Gulf Cooperation Council procure advanced monitoring to meet expatriate expectations, whereas Brazil’s ANVISA priority listing for critical-care devices may shorten future clearance cycles. However, reimbursement lags and supply-chain constraints moderate near-term penetration.

Competitive Landscape

The cerebral oximetry monitoring market is moderately consolidated. Becton, Dickinson and Company (BD) closed a USD 4.2 billion purchase of Edwards Lifesciences’ Critical Care portfolio, integrating tissue oximetry probes into BD’s connected-care ecosystem. The deal enhances cross-selling between infusion pumps, hemodynamic sensors, and cerebral monitoring.

Medtronic and Philips forged a collaboration to embed BIS™ brain-function and regional oximetry analytics into Philips patient-monitoring workstations, broadening channel access across 100-plus countries. GE HealthCare, leveraging partnerships with AWS and NVIDIA, is developing generative-AI overlays that harmonize imaging with physiologic data, positioning its Edison platform as a unified cockpit for surgery and ICU teams.

Emerging entrants prioritize wearable, wireless headbands aimed at sports medicine and military triage. Academic-spinoff startups experiment with printable optodes and edge-AI chips, attempting to disrupt incumbent pricing structures. Competitive intensity thus hinges on proprietary algorithms, interoperability credentials, and the breadth of subscription-based analytics services.

Cerebral Oximetry Monitoring Industry Leaders

Medtronic plc

Edwards Lifesciences Corp.

Nonin Medical Inc.

Masimo Corporation

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: GE HealthCare partnered with AWS to advance generative-AI tools for diagnostic workflows, with cerebral oximetry data envisioned as a future input stream.

- May 2024: GE HealthCare and Medis Medical Imaging agreed to integrate QFR technology into the Allia platform, augmenting cath-lab visualization capabilities.

Global Cerebral Oximetry Monitoring Market Report Scope

| Systems / Consoles |

| Disposable Sensors & Accessories |

| Continuous-Wave NIRS |

| Frequency-Domain NIRS |

| Time-Domain NIRS |

| Cardiac & Major Vascular Surgery |

| Neurosurgery |

| Intensive & Critical Care (ICU) |

| Neonatology & Pediatrics |

| Other Surgical Procedures |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Systems / Consoles | |

| Disposable Sensors & Accessories | ||

| By Technology | Continuous-Wave NIRS | |

| Frequency-Domain NIRS | ||

| Time-Domain NIRS | ||

| By Application | Cardiac & Major Vascular Surgery | |

| Neurosurgery | ||

| Intensive & Critical Care (ICU) | ||

| Neonatology & Pediatrics | ||

| Other Surgical Procedures | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current value of the cerebral oximetry monitoring market?

The market stands at USD 274.23 million in 2025 and is forecast to reach USD 398.19 million by 2030.

2. Which product segment leads revenue generation?

Disposable sensors hold 56.33% of global revenue due to infection-control preferences and recurring-revenue models.

3. Why is Asia-Pacific the fastest-growing region?

Infrastructure investment, an aging population, and regulatory reforms push a 10.04% CAGR to 2030.

4. How do AI tools improve cerebral oximetry performance?

Machine-learning algorithms filter motion artifacts and generate predictive alerts, enhancing measurement reliability.

5. What clinical area shows the highest growth?

Neonatology and pediatrics post an 11.88% CAGR as NICUs adopt mandatory regional saturation monitoring for brain protection.

Page last updated on: