Bovine Mastitis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.76 Billion |

| Market Size (2031) | USD 2.24 Billion |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bovine Mastitis Market Analysis by Mordor Intelligence

Bovine mastitis market size in 2026 is estimated at USD 1.76 billion, growing from 2025 value of USD 1.68 billion with 2031 projections showing USD 2.24 billion, growing at 4.88% CAGR over 2026-2031. Growth is tied to dairy processors tightening milk-quality rules, regulators curbing prophylactic antibiotic use, and farm operators investing in rapid diagnostics and precision herd-health platforms. Heightened economic losses from mastitis, estimated at up to USD 32 billion a year, are pushing producers toward prevention-centric protocols that blend selective dry-cow therapy with on-farm culture kits. Vaccine pipelines, phage formulations, and short-withdrawal intramammary drugs are expanding as antimicrobial-resistance (AMR) pressure reshapes treatment choices. Strategic alliances that fuse therapeutics with data-driven decision tools—such as Zoetis’ partnership with Danone on genetic resistance—signal the next phase of integrated solutions in the bovine mastitis market.

Key Report Takeaways

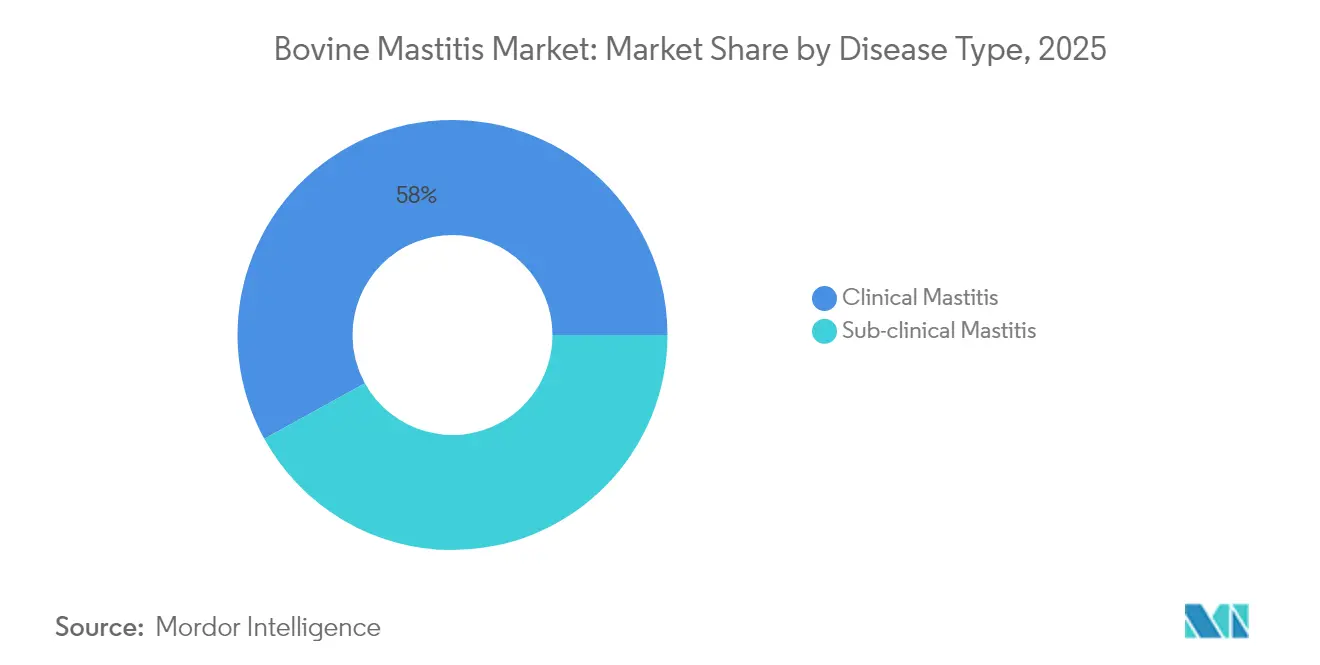

- By disease type, clinical mastitis commanded 58.02% of the bovine mastitis market size in 2025; the subclinical segment exhibits the highest projected CAGR at 5.33% through 2031.

- By product type, antibiotics held 76.62% of the bovine mastitis market share in 2025; vaccines are the fastest-growing product category at a 5.62% CAGR to 2031.

- By route of administration, the systemic segment accounted for 86.10% of the bovine mastitis market size in 2025 and is poised to expand at a 5.05% CAGR through 2031.

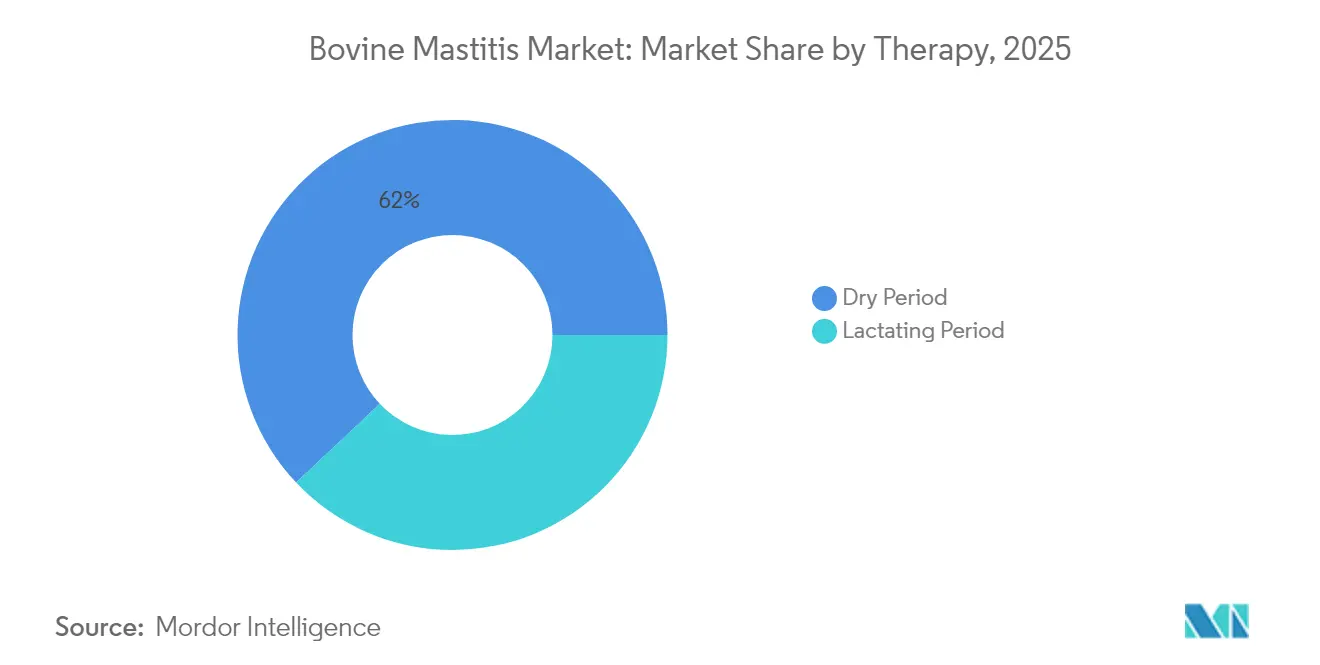

- By therapy, dry-period treatment captured 62.04% revenue share in 2025 and leads growth with a 5.36% CAGR to 2031.

- By end-user, dairy farms & cooperatives held 79.55% of the bovine mastitis market share in 2025 and is also the fastest-growing segment at 5.11% CAGR to 2031.

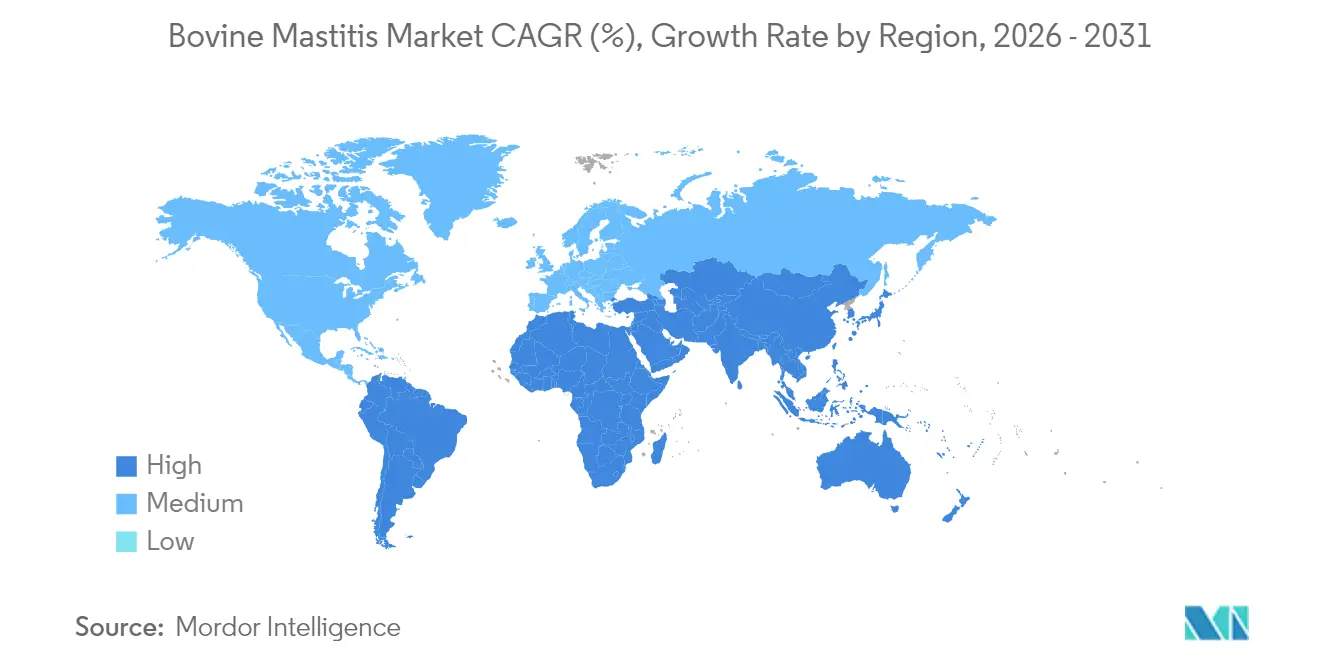

- By geography, North America led with 33.12% share of the bovine mastitis market in 2025 while Asia-Pacific is the fastest-growing region at a 5.86% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bovine Mastitis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence and cost burden | +1.2% | Global | Medium term (2-4 years) |

| Veterinary spending and herd-automation growth | +0.9% | APAC and Latin America | Long term (≥ 4 years) |

| Advances in on-farm diagnostics | +0.8% | North America & EU | Short term (≤ 2 years) |

| Short-withdrawal intramammary drugs | +0.6% | EU & North America | Medium term (2-4 years) |

| ESG-linked responsible-antibiotic sourcing | +0.5% | EU first, then Global | Medium term (2-4 years) |

| Venture funding in phage and peptide therapy | +0.4% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence and Cost Burden

Mastitis affects one in four U.S. dairy cows each year, with every clinical case costing from USD 128 to USD 444 in lost milk, treatment, and culling expenses[1]Thermo Fisher Scientific, “Bovine Diagnostics: How Much Does Mastitis Cost Dairy Producers Annually,” thedairysite.com. Subclinical infections silently depress yield by 10% to 20% per cow, prompting European herds to adopt routine somatic-cell screening to avoid milk-quality penalties. The mounting financial toll steers producer budgets toward predictive analytics, vaccination programs, and selective therapy, which all underpin sustained demand in the bovine mastitis market.

Growth in Veterinary Spending and Herd-Management Automation

Large farms are allocating bigger capital outlays to automated milking systems, inline sensors, and professional veterinary services. DeLaval and John Deere’s Milk Sustainability Center illustrates how cloud-based dashboards now merge feed, fertility, and udder-health data to boost profitability. Asia-Pacific herds are scaling rapidly, replicating Western automation models and lifting regional sales of diagnostics, vaccines, and decision-support software that keep the bovine mastitis market expanding at the fastest clip worldwide.

Technological Advances in On-Farm Diagnostics and Sensors

AI-enabled image analysis and IoT milk-conductivity probes detect Gram-positive pathogens in hours rather than days. Zoetis’ Vetscan Mastigram+ identifies Gram-positive mastitis within 8 hours, cutting blanket antibiotic use. Trial data show machine-learning models reach over 95% accuracy for subclinical detection[2]Moonsun Shin, “AI-Based Smart Monitoring Framework for Livestock Farms,” Applied Sciences, mdpi.com , though farms still face false-positive alerts that vendors are tackling through refined algorithms.

Adoption of Short-Withdrawal Intramammary Antibiotics

Regulators now favor products that preserve milk sales. The FDA approval of Flunine and Merck’s BANAMINE TRANSDERMAL set the tone for 48-hour milk-withdrawal therapies. EU rules mandating selective dry-cow therapy spur R&D into formulations that balance potency with minimal residue, reinforcing demand in the bovine mastitis market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating antimicrobial resistance | -0.7% | EU & North America | Short term (≤ 2 years) |

| Low farmer adherence to protocols | -0.5% | APAC, Latin America, MEA | Medium term (2-4 years) |

| Stricter milk-residue audits | -0.4% | EU & North America | Medium term (2-4 years) |

| Variable accuracy of pen-side kits | -0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Antimicrobial Resistance (AMR)

EU Regulation 2019/6 has banned prophylactic use and tightened metaphylactic approvals[3]Ivo Schmerold, “European regulations on the use of antibiotics in veterinary medicine,” European Journal of Pharmaceutical Sciences, sciencedirect.com, forcing practitioners to blend systemic and intramammary drugs with NSAIDs to manage resistant strains. MRSA outbreaks in cattle shrink cure rates and elevate costs, dampening short-term growth until vaccines and phage solutions mature.

Low Farmer Adherence in Emerging Markets

Studies in Brazil and Rwanda show gaps between veterinary guidance and on-farm practice, owing to cost constraints and limited extension services. Pilot One-Health projects[4]Sara N Garcia, “A one health framework to advance food safety and security: An on-farm case study in the Rwandan dairy sector,” PubMed, pubmed.ncbi.nlm.nih.gov lift compliance to 90% when training is provided, yet scaling such programs remains a hurdle that restrains the bovine mastitis industry in developing regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Clinical Cases Drive Treatment Urgency

Clinical mastitis held 58.02% of the bovine mastitis market size in 2025 and is expanding at 5.18% CAGR on the back of visible symptoms that demand immediate treatment to avoid milk loss and animal welfare penalties. Rapid therapy translates to higher spending per case, sustaining revenue streams for antibiotics and NSAIDs. The economic sting of each clinical outbreak keeps producers alert to early warning sensors that flag udder swelling or milk discoloration.

Subclinical infections trail in market value yet contribute 10%-20% latent yield loss, prompting investment in somatic-cell count trackers and AI pattern recognition. Smartphones now deliver 2-minute cell-count reads, nudging farms toward proactive cures that could soon narrow the revenue gap with clinical cases. As technology shrinks diagnostic costs, the subclinical sub-segment may accelerate faster than headline projections, adding depth to the bovine mastitis market.

By Product: Antibiotic Dominance Faces Innovation Pressure

Antibiotics accounted for 76.62% of the bovine mastitis market share in 2025 and are on track to grow at a good pace through 2031. Their dominance stems from fast, reliable cures in acute clinical cases, which protect both cow welfare and farm income. Regulators are tightening oversight; however, the European Union now restricts prophylactic use and scrutinizes critical drug classes, prompting more selective prescribing.

Vaccines are the quickest-rising category, advancing at a 5.62% CAGR, as prevention proves cheaper than treatment and supports industry efforts to curb antibiotic reliance. Zoetis’ Protivity for Mycoplasma bovis and other multi-pathogen projects show the pivot toward immunological control.

By Route of Administration: Systemic Delivery Maintains Dominance

Systemic therapies made up 86.10% of the bovine mastitis market size in 2025 and are set to climb at 5.05% CAGR because they address both localized and systemic infections while simplifying dosing. Injectable ceftiofur or oral formulations save labor in large herds where time per cow is at a premium.

Intramammary products, though smaller in value, allow high local drug concentrations and reduced residues. The FDA’s 21 CFR Part 526 pathway guides new extended-release tubes that maintain therapy across the dry period without repeated infusions. As more selective dry-cow programs roll out, intramammary lines may edge up their contribution to overall bovine mastitis market growth.

By Therapy: Dry-Period Treatment Leads Prevention Focus

Dry-period therapy captured 62.04% of the bovine mastitis market share in 2025 and posts the fastest CAGR at 5.36%. Treating cows between lactations sidesteps withdrawal losses and lets antibiotics linger for complete pathogen clearance. EU mandates now require culture-based selection, spurring diagnostics that decide which quarters need dosing and which can transition to internal teat sealants alone.

Lactation-period therapy grapples with milk-discard costs and AMR rules but benefits from recent approvals that cut withholding intervals to 48 hours. Anti-inflammatory combinations shorten clinical signs and help producers keep mastitis-affected cows in production. Both dynamics preserve demand across the bovine mastitis market as farms balance productivity with compliance.

By End-User: Dairy Farms Drive Direct Implementation

Dairy farms and cooperatives accounted for 79.55% of the bovine mastitis market size in 2025 and advance at 5.11% CAGR because they shoulder the direct economic burden of mastitis. Consolidating herds wield procurement power, purchasing diagnostics and therapeutics in bulk and integrating them into digital farm-management suites.

Veterinary hospitals remain central for complex or chronic cases that need culture, sensitivity testing, or surgery. Zoetis’ Louisville reference lab extension offers faster microbial identification, underscoring the link between lab capacity and frontline mastitis control. Academic institutions and government labs continue to drive basic research that filters into commercial solutions, reinforcing an innovation pipeline vital for the bovine mastitis industry.

Geography Analysis

North America generated 33.12% of bovine mastitis market revenue in 2025 and will climb at 4.65% CAGR through 2031. Investment exceeding USD 8 billion in new U.S. processing capacity boosts milk-quality demands, motivating farms to adopt selective therapy and inline diagnostics. The FDA’s evolving antibacterial guidance shapes label claims and withdrawal times, rewarding firms that navigate compliance swiftly.

Europe follows a 4.92% CAGR backed by some of the world’s strictest antimicrobial policies. Regulation 2019/6 pushes selective dry-cow therapy and caps prophylactic use, intensifying demand for sensor-driven treatment decisions and alternative biologics. Nordic producers showcase low somatic-cell averages, proving preventive systems can maintain output while shrinking antibiotic loads.

Asia-Pacific is the fastest propeller with a 5.86% CAGR thanks to surging dairy consumption in China, India, and Southeast Asia. Larger herd sizes, international joint ventures, and Western farming models necessitate structured mastitis control. Investments in milk-analysis labs and vet services unlock pent-up demand for culture kits, vaccines, and AI platforms, enlarging regional share of the bovine mastitis market. Latin America and the Middle East & Africa trail at slightly lower yet robust CAGRs of 5.72% and 5.31% respectively as integrated farm projects scale up in Brazil and the Gulf states.

Competitive Landscape

The bovine mastitis market shows moderate fragmentation. Zoetis, Elanco, and Boehringer Ingelheim lead with diversified antibiotic and vaccine lines plus global distribution. Zoetis sold its medicated-feed unit to Phibro for USD 350 million to fund diagnostics and genetics, signaling a pivot toward data-centric offerings. Elanco pairs therapy pipelines with Medgene’s mRNA technology to diversify against AMR headwinds.

Emerging biotech firms court venture capital to advance phage and peptide candidates that directly attack resistant pathogens. Strategic tie-ups, such as Zoetis-Danone’s genomic-selection program, illustrate the drive toward value-chain integration where therapeutic efficacy merges with milk-quality bonuses.

White-space opportunities exist in developing markets where limited veterinary infrastructure and cost-sensitive customers require simplified, affordable solutions that can be implemented by farmers with minimal professional oversight. This creates potential for disruptive business models that challenge traditional distribution approaches.

Bovine Mastitis Industry Leaders

Boehringer Ingelheim GmbH

Elanco Animal Health

Phibro Animal Health Corporation

Virbac SA

Zoetis Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Zoetis opened a Louisville, KY diagnostics reference laboratory, co-located with UPS Healthcare, to accelerate mastitis culture turnaround times.

- February 2025: Elanco and Medgene partnered to commercialize an H5N1 dairy-cattle vaccine awaiting USDA conditional license approval.

- January 2025: John Deere and DeLaval introduced the Milk Sustainability Center, a free digital platform that merges agronomic and animal metrics for select U.S., Dutch, and German farms.

- September 2024: Anpario acquired Bio-Vet Inc. to expand natural feed additive options for U.S. dairy operations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study considers the global bovine mastitis market as the total annual revenue generated by therapeutic and preventive products, principally antibiotics, teat sealants, vaccines, and supportive NSAIDs used to treat or avert inflammation of the bovine udder across dairy and beef cattle. Products tracked are valued at manufacturer-level prices and cover both dry-cow and lactation regimens across all herd management models.

Scope exclusion: routine milking parlor hygiene chemicals and standalone diagnostic test kits are not counted within this value chain.

Segmentation Overview

- By Disease Type

- Clinical Mastitis

- Sub-clinical Mastitis

- By Product

- Antibiotics

- Vaccines

- NSAIDs & Pain-killers

- Others

- By Route of Administration

- Intramammary

- Systemic

- By Therapy

- Lactating Period

- Dry Period

- By End-User

- Hospitals & Veterinary Clinics

- Dairy Farms & Cooperatives

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured questionnaires with dairy veterinarians, herd consultants, pharmaceutical sales managers, and cooperative purchasing heads across North America, Europe, Asia-Pacific, and Latin America supplied real-world incidence rates, average treatment cycles, and emerging practice shifts (selective dry-cow therapy). Feedback also validated assumed average selling prices and probable vaccine uptake.

Desk Research

Mordor analysts first built a fact base from public tier-one sources such as the United States Department of Agriculture, Eurostat livestock statistics, FAO milk production data, the World Organisation for Animal Health disease reports, and International Dairy Federation cost-of-disease models. Industry insight was deepened with company 10-Ks, farmer cooperative annual reviews, peer-reviewed journals in the Journal of Dairy Science, and trade association white papers. Paid data services including D&B Hoovers for company revenues and Dow Jones Factiva for shipment news helped anchor supplier benchmarks. This list illustrates the breadth of desk work; many further sources were referenced for cross-checks, clarifications, and historical trends.

Market-Sizing & Forecasting

A top-down build starts with regional milking-cow populations, average clinical plus sub-clinical incidence, and treatment penetration to derive annual treated-case volumes, which are then combined with blended ASPs to estimate value. Supplier roll-ups and sampled farm spend provided a selective bottom-up counter-view; differences above a certain threshold triggered re-work. Key variables modeled include: 1) lactating-cow numbers, 2) weighted mastitis incidence by housing system, 3) proportion of cows placed on dry-cow therapy, 4) antibiotic-to-vaccine substitution trend, and 5) regulatory caps on blanket antibiotic use. A multivariate regression with milk price, incidence, and regulatory intensity as predictors generated the growth path, while scenario analysis captured rapid adoption of non-antibiotic solutions. Where bottom-up evidence was thin, regional proxies such as antibiotic sales volume were ratioed back to cow populations to close gaps.

Data Validation & Update Cycle

Outputs undergo three-layer checks: automated variance scans flag outliers versus historic ratios; senior analysts review driver coherence; a domain expert revisits any abnormal swings. Reports refresh yearly, with interim updates triggered by material events such as a major product ban. Before delivery, an analyst re-pulls high-frequency indicators so clients receive the freshest view.

Why Our Bovine Mastitis Baseline Earns Decision-Maker Trust

Published numbers differ widely because firms vary the product basket, base year, currency handling, and refresh rhythm.

Key gap drivers include whether diagnostics are bundled, if sub-clinical cases are monetized, the ASP uplift method, and the speed at which forthcoming antibiotic restrictions are baked into forecasts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.68 Billion (2025) | Mordor Intelligence | - |

| USD 1.67 Billion (2024) | Global Consultancy A | excludes vaccine revenues; converts volumes at fixed 2020 FX |

| USD 2.00 Billion (2024) | Industry Association B | counts diagnostic kits and udder sanitizers in scope |

| USD 1.23 Billion (2019) | Regional Consultancy C | older base year and linear forecast, limited Asia sampling |

The comparison shows that scope breadth, currency treatment, and refresh cadence materially shift totals. By aligning variables to real herd behavior, applying dual-track validation, and updating annually, Mordor Intelligence delivers a balanced, transparent baseline that stakeholders can reproduce and confidently use for planning.

Key Questions Answered in the Report

How are dairy sustainability goals influencing mastitis treatment choices?

Processors are rewarding farms that document responsible antibiotic use, so producers increasingly adopt rapid diagnostics and selective dry-cow therapy to qualify for premiums tied to ESG metrics.

Why are vaccines gaining momentum in mastitis control programs?

Vaccines lower antibiotic dependence and align with antimicrobial-stewardship rules, making them attractive to regulators, retailers, and large herds seeking long-term disease resilience.

What role do AI-enabled sensors play in early mastitis detection?

Inline conductivity probes and machine-learning image tools flag subtle udder changes within hours, allowing targeted treatment before clinical signs appear and reducing discarded milk.

How is antimicrobial resistance shaping product pipelines?

Rising resistance to conventional drugs is accelerating investment in phage therapies, antimicrobial peptides, and short-withdrawal intramammary formulas that minimize residue risks.

Why are strategic partnerships between animal-health firms and dairy processors becoming more common?

Collaborations combine genetic testing, diagnostics, and treatment protocols, helping processors secure consistent milk quality while giving suppliers real-time herd data to refine products.

What factors limit mastitis-management adoption in emerging dairy markets?

Limited veterinary infrastructure and cost constraints reduce farmer adherence to treatment guidelines, prompting demand for low-cost culture kits and mobile training programs that bridge knowledge gaps.

Page last updated on: