Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.9 Billion |

| Market Size (2031) | USD 1.17 Billion |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

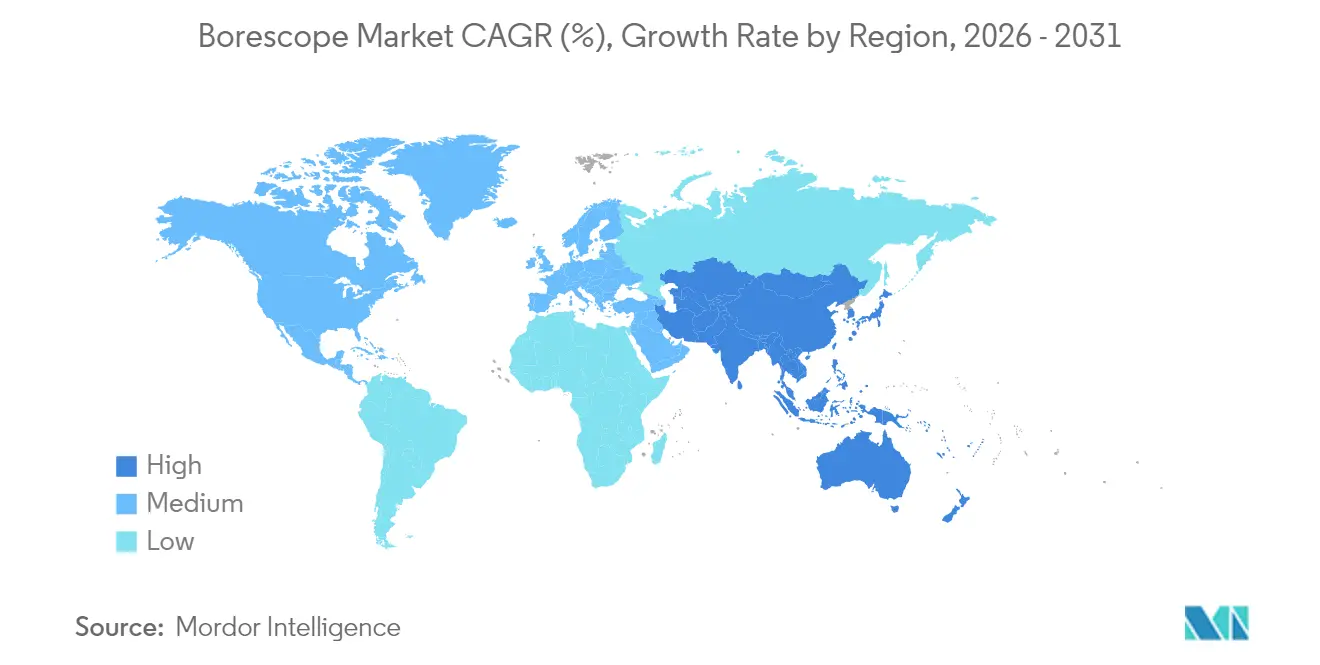

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

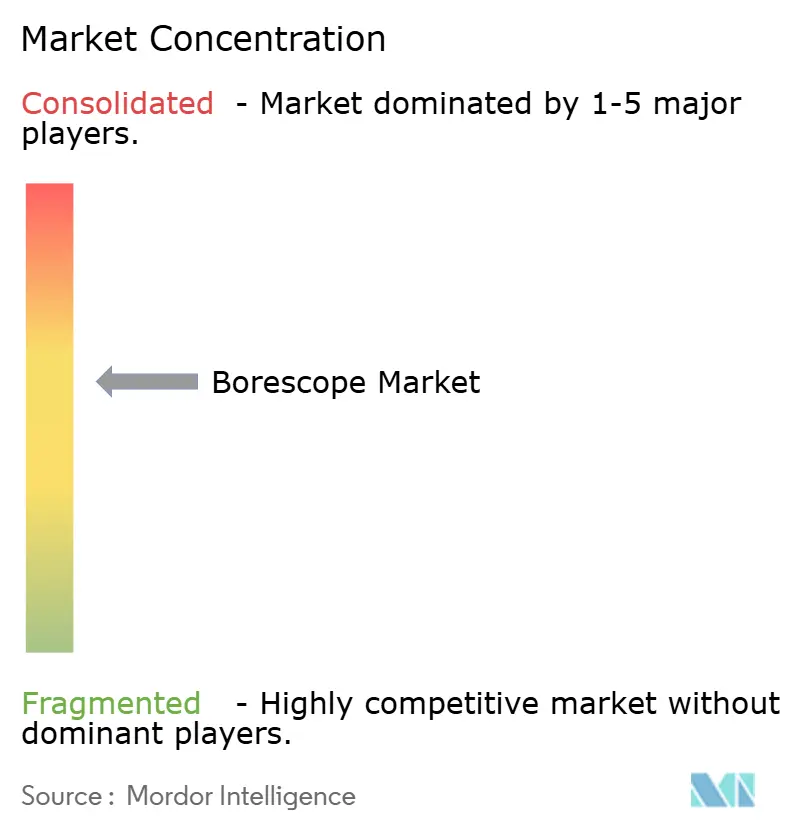

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Borescope Market Analysis by Mordor Intelligence

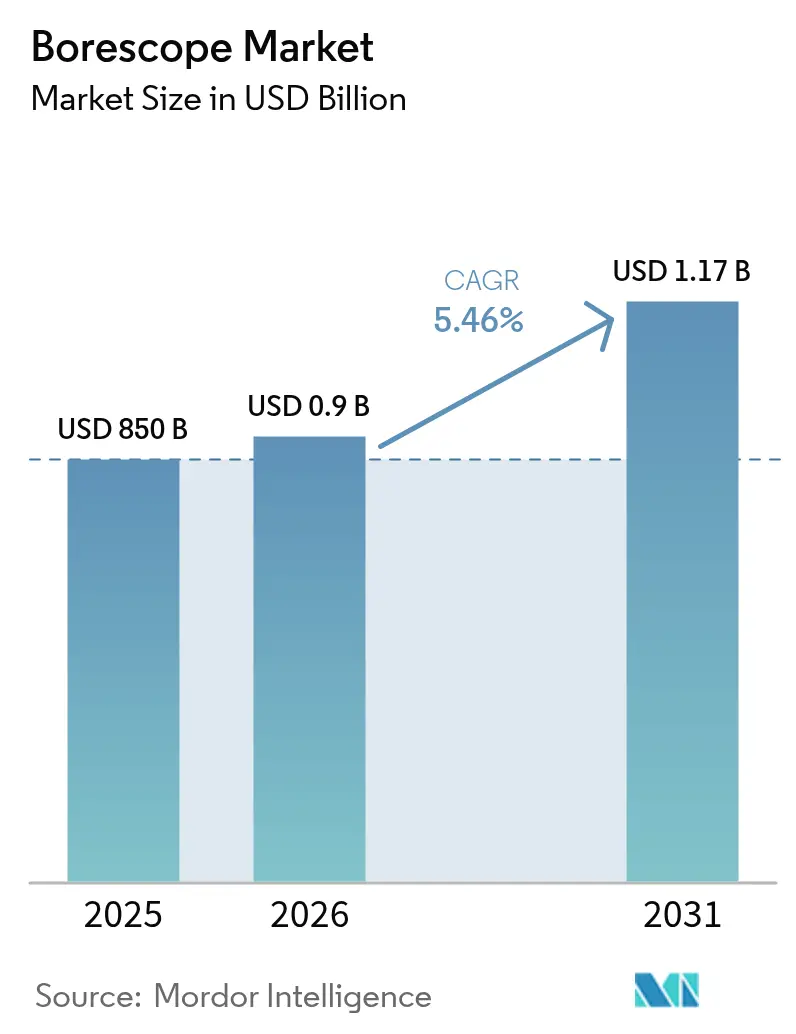

The borescope market size was valued at USD 850 million in 2025 and estimated to grow from USD 900 million in 2026 to reach USD 1.17 billion by 2031, at a CAGR of 5.46% during the forecast period (2026-2031). Sustained demand for non-destructive inspection across aviation, energy, oil and gas, and precision manufacturing forms the backbone of this expansion. Operators view high-definition internal visualization as a practical hedge against unplanned downtime, a concern that escalates as critical infrastructure ages and safety regulations tighten. Miniaturization of CMOS sensors, wider‐angle articulation, and seamless cloud connectivity now allow inspectors to reach previously inaccessible cavities without dismantling assets, compressing maintenance cycles and lowering lifetime operating cost. In parallel, artificial-intelligence routines are migrating from pilot projects to standard features that automatically flag blade pitting, corrosion, or weld porosity, diminishing operator subjectivity and shortening training curves. Regulatory bodies on both sides of the Atlantic continue to update inspection mandates, compelling asset owners to document findings with time-stamped imagery—an administrative requirement that invariably pushes buyers toward premium video borescopes. Competitive pressure favors suppliers capable of bundling hardware with data analytics, on-site training, and outcome-based service contracts that align with operators’ shift from reactive to predictive maintenance models.

Key Report Takeaways

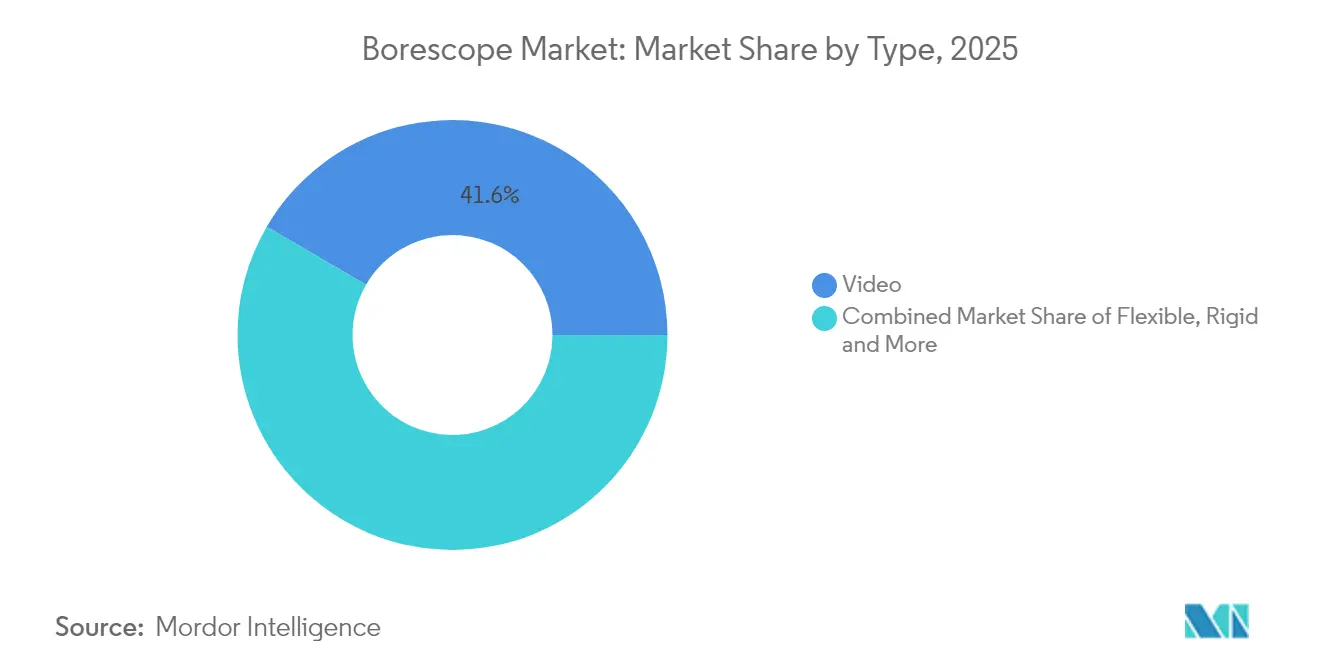

- By technology, video borescopes led with 41.60% of the borescope market share in 2025; the segment is forecast to grow at a 7.64% CAGR through 2031.

- By end-user industry, aviation accounted for 27.60% share of the borescope market size in 2025, while oil and gas is expected to expand at a 7.22% CAGR during 2026-2031.

- By diameter, the 6–10 mm category captured 34.50% of the borescope market share in 2025; the 0–3 mm range is projected to rise at a 6.19% CAGR over the same period.

- By viewing angle, 0°–90° systems held 39.70% revenue share in 2025, whereas 180°–360° devices are set to post the fastest 6.37% CAGR to 2031.

- By geography, North America dominated with 33.70% of the borescope market size in 2025; Asia-Pacific is poised for a 6.74% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Borescope Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for high operational productivity | +1.20% | Global; concentration in North America & Europe | Medium term (2-4 years) |

| Accelerating adoption of video borescopes in MRO programs | +1.00% | Global; led by North America & APAC | Short term (≤ 2 years) |

| Regulatory inspection mandates in aviation & energy sectors | +0.90% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Preventive-maintenance push in oil & gas & power generation | +0.80% | Global; emphasis on mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High Operational Productivity

Industrial managers increasingly link downtime costs to shareholder returns; as a result, visual inspection budgets are shifting from discretionary to mandated line items. Modern gas-turbine operators report that high-definition borescope passes can detect blade deterioration a full maintenance season before routine strip-downs, allowing repairs to be scheduled during low-demand windows. Micro-diameter probes have entered quality-control cells on automotive engine lines to spot casting voids before final assembly. AI-assisted recognition shortens each inspection loop, boosting throughput in factories that once considered visual checks a bottleneck. Across these settings, the borescope market benefits from a clear value narrative: small capital outlays avert multimillion-dollar outages.

Accelerating Adoption of Video Borescopes in MRO Programs

Maintenance, repair, and overhaul providers now favor video systems that capture 4K imagery, store audit trails, and enable live remote collaboration. Aviation MRO teams cite 30-40% cycle-time savings versus legacy fiber scopes, while higher resolution delivers more confident go-no-go decisions. Military specifications reinforce the shift; USSOCOM’s 2025 tender requires waterproof, low-latency, 4K forensic cameras, a specification that cascades to civilian suppliers. [1]United States Special Operations Command, “USSOCOM Tactical Forensics Event 2025,” SAM.gov, sam.gov The net result is an upgrade wave that anchors the borescope market in digital workflows.

Regulatory Inspection Mandates in Aviation and Energy Sectors

The U.S. Pipeline and Hazardous Materials Safety Administration broadened 49 CFR 192.493 in 2024, obliging pipeline operators to deploy in-line and visual tools where conventional pigs cannot travel. [2]Pipeline and Hazardous Materials Safety Administration, “Pipeline Safety: Periodic Updates of Regulatory References to Technical Standards and Miscellaneous Amendments,” Federal Register, federalregister.gov Aviation regulators similarly require deeper documentation of turbine health following high-profile in-flight failures. Olympus responded by shipping extended-depth-of-field scopes that achieved FDA clearance in 2025, underscoring the feedback loop between policy and product. This compliance environment compels operators to replace aging optics, supporting mid-term demand for premium solutions.

Preventive-Maintenance Push in Oil & Gas & Power Generation

Following several pipeline ruptures, supermajors are formalizing condition-based maintenance programs. Petrobras partnered with Baker Hughes to develop corrosion-resistant flexible pipes and an inspection regime that aligns with a 30-year design life. Power utilities apply similar logic: regular turbine borescoping can extend component life by up to 30%, freeing cash for plant upgrades. Integrating findings with digital twins lets asset managers model degradation curves and stagger outages, reinforcing the borescope market’s role in predictive strategies.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront acquisition and training costs | −0.7% | Global; particularly emerging markets | Short term (≤ 2 years) |

| Skilled-operator shortage in emerging markets | −0.5% | APAC & Latin America, expanding to Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Acquisition and Training Costs

Premium video scopes equipped with AI analytics often list between USD 50,000 and USD 100,000—well above the capital budgets of small repair shops. Certification programs can add another USD 10,000-15,000 per technician. [3]InterNACHI, “Borescopes for Home Inspectors,” nachi.org These economics slow adoption in developing economies, creating a two-tier structure in which large fleet operators access advanced optics while smaller vendors continue with lower-resolution tools.

Skilled-Operator Shortage in Emerging Markets

Rapid industrialization has outpaced the supply of certified technicians across APAC and Latin America. Training content remains English-centric, and travel costs to overseas academies are prohibitive for smaller firms. The resulting talent gap limits the velocity at which new borescope installations translate into usable inspection hours, restraining full-cycle market potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Video Dominance Drives Digital Transformation

Video systems held the largest 41.60% slice of the borescope market in 2025, a position underwritten by regulatory calls for image archiving and remote audit trails. The segment’s 7.64% forecast CAGR will push its revenue from an estimated USD 360 million in 2025 to roughly USD 560.15 million by 2031, reinforcing the borescope market size leadership of digital platforms. Flexible video models win where complex geometries demand articulation, while rigid optics remain the choice when absolute image clarity outweighs reach. Hybrid semi-rigid probes carve out niches in small-engine inspection, balancing maneuverability against cost.

Continued feature infusion shapes competitive moats. Olympus introduced the EZ1500 line with extended depth-of-field imaging, mitigating the focus drift that once plagued deep bores. Cloud APIs now funnel footage into AI object-detection services that tag pitting, fatigue, and scale without human oversight. These dynamics collectively ensure that the video category remains the borescope market’s digital vanguard and the primary gateway for downstream analytics revenues.

By Diameter: Miniaturization Enables New Applications

The 6–10 mm range—home to mainstream turbine and pipeline work—accounted for 34.50% of borescope market share in 2025. This sweet spot combines high lumen output with adequate articulation, keeping lifetime service costs in check. Meanwhile, 0–3 mm probes are registering a 6.19% CAGR as semiconductor fabs and medical-device plants pursue defect detection at micrometer scale. Gradient Lens has commercialized 0.5 mm models that thread through narrow coolant channels on micro-milling equipment. SCHÖLLY’s 0.35 mm fiberscope, comprising 3,000 individual fibers, underscores a roadmap toward sub-millimeter inspection.

Larger diameters above 10 mm remain indispensable for boiler tubes and petrochemical vessels, where lumen intensity and integrated measurement modules trump size. Across all classes, advances in CMOS sensitivity and LED lighting sustain image clarity even as external diameters shrink, ensuring the borescope market can service industries moving toward perpetual miniaturization.

By Angle: Wide-Angle Systems Enhance Inspection Coverage

Viewing angles between 0° and 90° delivered 39.70% of the 2025 turnover, reflecting their adaptability to most standard inspection routes. That said, 180°–360° articulation is climbing at a 6.37% CAGR because pressure-vessel codes and aviation manuals now stipulate near-total internal surface coverage. Baker Hughes’ Mentor Visual iQ+ brings joystick-controlled tip articulation coupled with 3D metrology, allowing inspectors to measure crack depth without repositioning the probe. As operators quantify the labor savings of single-pass surveys, demand gravitates toward full-rotation heads.

Angles in the 90°–180° band continue to serve compact engine blocks and small-bore piping, although the gap between mid-range and full-rotation pricing narrows each product cycle. Overall, broader articulation expands the borescope market’s addressable envelope by trimming access tooling, scaffolding, and inspection time.

By End-user Industry: Aviation Leads While Oil and Gas Accelerates

Aviation retained a commanding 27.60% share in 2025 and remains the most compliance-sensitive vertical. Aircraft engines are multi-million-dollar assets governed by airworthiness directives that explicitly reference borescope findings, embedding visual inspection deep within MRO budgets. The sector prefers high-resolution video units with cloud archives that can be revisited after teardown. Simultaneously, oil and gas is tracking a 7.22% CAGR as pipeline operators migrate from five-year hydrostatic tests to annual visual passes integrated with digital twins. Petrobras’ multiyear contracts with Baker Hughes illustrate how inspection deliverables bundle with broader integrity-management services.Power generation ranks close behind, leveraging turbine inspections to synchronize outages with capacity-planning windows. On the automotive front, video flex scopes enter battery-pack QA lines to examine cell-bond welds, while defense agencies procure ruggedized scopes for field forensics. This diverse application spread insulates the borescope market from single-sector volatility.

Geography Analysis

North America maintained 33.70% of borescope market revenue in 2025, anchored by the United States’ extensive pipeline grid and the Federal Aviation Administration’s stringent engine-inspection directives. PHMSA’s 2024 rulemaking added more than 20 technical standards, compelling pipeline operators to collect detailed visual evidence of compliance. Early uptake of AI-enabled analytics further embeds premium scopes in operator budgets, and a mature service ecosystem sustains high aftermarket revenues.Asia-Pacific is advancing at a 6.74% CAGR, converting factory expansions and infrastructure build-outs into sustained equipment demand. Chinese OEMs such as QBH Technology leverage scale economics to offer competitively priced scopes across more than 60 export destinations. Japan and South Korea, driven by shipbuilding and semiconductor investments, purchase high-end optics that stand up to clean-room protocols. India’s push for industrial safety audits in power and chemical plants opens green-field opportunities where service capacity is still nascent, positioning the region as the fastest-moving component of the global borescope market.

Europe shows consistent mid-single-digit growth as aging industrial assets, offshore wind farms, and nuclear facilities adopt predictive inspection regimes. Germany’s Industrie 4.0 rollout embeds scopes within automated quality gateways, while the United Kingdom’s mature North Sea assets rely on high-angle probes that operate in confined, high-pressure environments. EU environmental directives reinforce condition-monitoring investments, keeping replacement cycles steady and supporting stable contribution to overall borescope market size.

Competitive Landscape

The borescope market remains moderately fragmented but is consolidating as incumbents seek scale in digital analytics. Wabtec’s USD 1.78 billion purchase of Evident’s Inspection Technologies unit in 2025 doubled its addressable market and integrated optical hardware into its rail-centric Digital Intelligence platform. Baker Hughes extends a systems-of-systems strategy: turbine OEM expertise blends with inspection know-how, letting the firm command turnkey integrity programs from hardware through data-science dashboards. Olympus leverages medical imaging R&D to roll out industrial scopes with extended depth of field, a cross-vertical play that defends high-margin product tiers.

Emerging challengers differentiate through ultra-thin diameters, AI-native software stacks, or SaaS business models that convert capex into subscription opex. Patent filings target conformable transducers capable of self-position sensing—technology that improves tip-location accuracy inside convoluted vessels. Strategic partnerships are multiplying as optics firms ally with cloud providers to speed compute-heavy defect classification. Regional service integrators also enter co-branding deals to secure distribution in skill-scarce markets, underscoring the shift from standalone devices toward holistic outcome contracts that bundle training, analytics, and lifecycle support.

Borescope Industry Leaders

Olympus Corporation

AB SKF

Baker Hughes Company

FLIR Systems

Fluke Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Olympus Corporation received FDA 510(k) clearance for its EZ1500 endoscopes with Extended Depth of Field, signalling cross-pollination of medical imaging advances into industrial inspection.

- March 2025: Baker Hughes and Petrobras launched a joint program to engineer 30-year flexible pipes for high-CO₂ environments, bolstering integrity-driven demand for advanced inspection.

- January 2025: Wabtec Corporation closed its USD 1.78 billion acquisition of Evident’s Inspection Technologies division, expanding its Digital Intelligence footprint.

- January 2025: Baker Hughes introduced SureCONNECT FE, the first downhole fiber-optic wet-mate system for HP/HT wells, illustrating convergence between connectivity and inspection.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the global borescope market as all newly manufactured optical or video inspection devices, rigid, semi-rigid, flexible, or videoscopes, sold for non-medical remote visual inspection across aviation, automotive, energy, process industries, construction, and security.

Units intended strictly for human or veterinary endoscopy are excluded.

Segmentation Overview

- By Type

- Video

- Flexible

- Rigid

- Semi-rigid

- Endoscopes

- By Diameter

- 0–3 mm

- 3-6 mm

- 6-10 mm

- Above 10 mm

- By Angle

- 0°–90°

- 90°–180°

- 180°–360°

- By End-user Industry

- Automotive

- Aviation

- Power Generation

- Oil and Gas

- Manufacturing

- Chemicals

- Food and Beverages

- Pharmaceuticals

- Mining and Construction

- Defense and Security

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- ASEAN

- Rest of APAC

- Middle East and Africa

- Middle East

- GCC

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured questionnaires with borescope OEM engineers, MRO managers, power-plant inspectors, and regional distributors across North America, Europe, and Asia helped validate volume run-rates, average selling prices, and adoption triggers, while surveys of safety auditors clarified replacement cycles and diameter preferences.

Desk Research

We built the foundation with open data from agencies and trade bodies such as the Federal Aviation Administration, International Energy Agency, European Automobile Manufacturers Association, and International Organization for Standardization, complemented by customs statistics and peer-reviewed NDT journals. Company 10-Ks, product catalogs, safety-authority directives, and reputable press releases added recent shipment, pricing, and regulatory context. For financial cross-checks, our analysts accessed D&B Hoovers and Dow Jones Factiva. (These sources illustrate the breadth; many others were referenced.)

Market-Sizing & Forecasting

A top-down model started with industrial maintenance spending and installed base metrics, then applied penetration rates for visual inspection tools by sector. Selective bottom-up checks, supplier revenue roll-ups and sample ASP×units, served as guardrails. Key variables include aircraft fleet age, global vehicle production, gas-turbine additions, average inspection frequency, and video-scope ASP erosion. Multi-variate regression linked these drivers to historic sales, and a damped exponential smoothing routine projected 2025-2030 demand, with scenario tweaks from primary-research consensus. Gap areas in bottom-up data were bridged with normalized margin bands from public earnings.

Data Validation & Update Cycle

Outputs pass three-layer review: automated anomaly flags, senior-analyst peer checks, and a final lead-analyst sign-off. Models refresh annually, with mid-cycle updates triggered by material events such as major air-worthiness directives or step-change technology launches.

Why Mordor's Borescope Baseline Commands Reliability

Published figures vary because firms choose different device scopes, base years, and price-mix assumptions.

We anchor on industrial-only units, 2025 USD, and a balanced base-case scenario.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.85 B (2025) | Mordor Intelligence | - |

| USD 0.84 B (2024) | Global Consultancy A | counts select refurbished units and uses 2018 ASPs |

| USD 0.68 B (2024) | Trade Journal B | omits sub-6 mm scopes and applies constant currency from 2022 |

| USD 0.89 B (2024) | Industry Analytics C | relies on vendor capacity surveys without end-user confirmation |

These comparisons show how differing scope cuts and aging price decks swing totals by up to USD 210 million.

By grounding estimates in refreshed variables and dual-track validation, Mordor Intelligence supplies a stable, transparent baseline managers can confidently build upon.

Key Questions Answered in the Report

What is the current size of the borescope market?

The borescope market size stands at USD 900 million in 2026 and is on track to reach USD 1.17 billion by 2031.

Which technology segment leads the borescope market?

Video borescopes hold the leading 41.60% share thanks to high-resolution imaging and mandatory documentation requirements.

Which end-user vertical is expanding fastest?

The oil and gas sector is forecast to grow at a 7.22% CAGR between 2026 and 2031 as operators migrate toward predictive maintenance.

Why is Asia-Pacific the fastest-growing regional market?

Rapid industrialization, expanding manufacturing capacity, and stronger safety regulations push Asia-Pacific borescope market demand at a 6.74% CAGR.

What factors restrain wider adoption of advanced borescopes?

High acquisition costs and scarcity of certified operators in emerging markets slow uptake of premium video systems.

How are artificial-intelligence features shaping competitive strategy?

Vendors embed AI for automated defect detection, enabling service-based revenue models while reducing training time, a key differentiator in the evolving borescope market.

Page last updated on: