Bonded Abrasives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

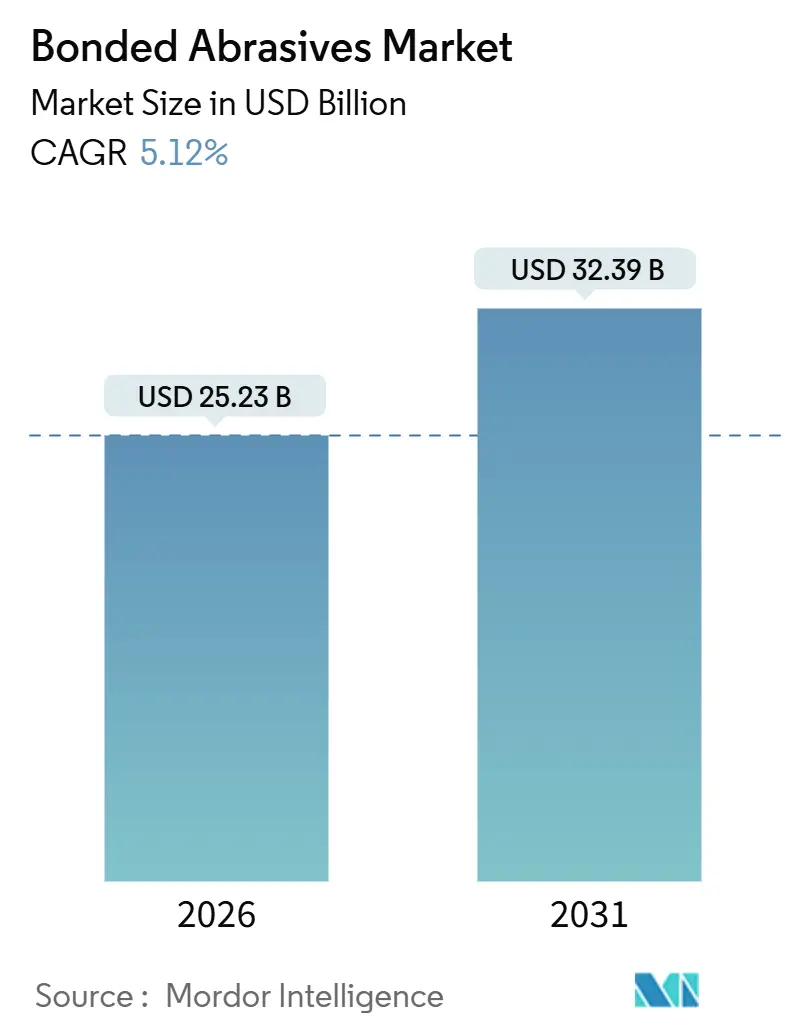

| Market Size (2026) | USD 25.23 Billion |

| Market Size (2031) | USD 32.39 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

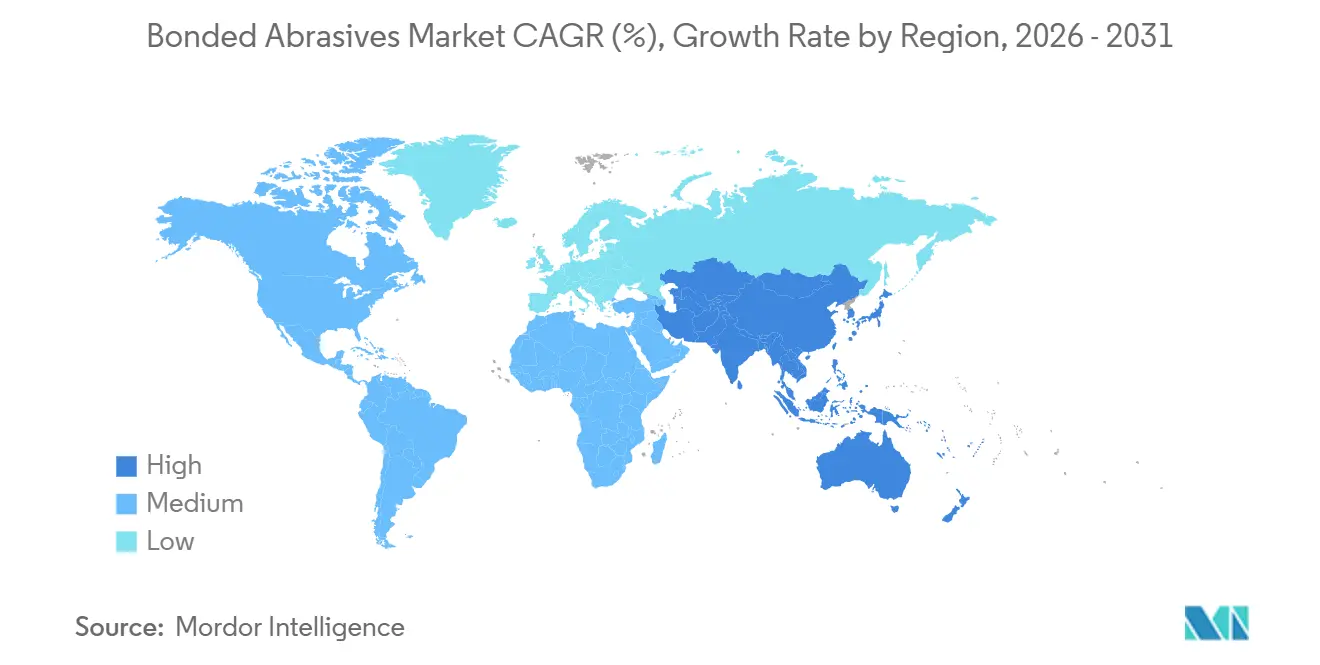

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

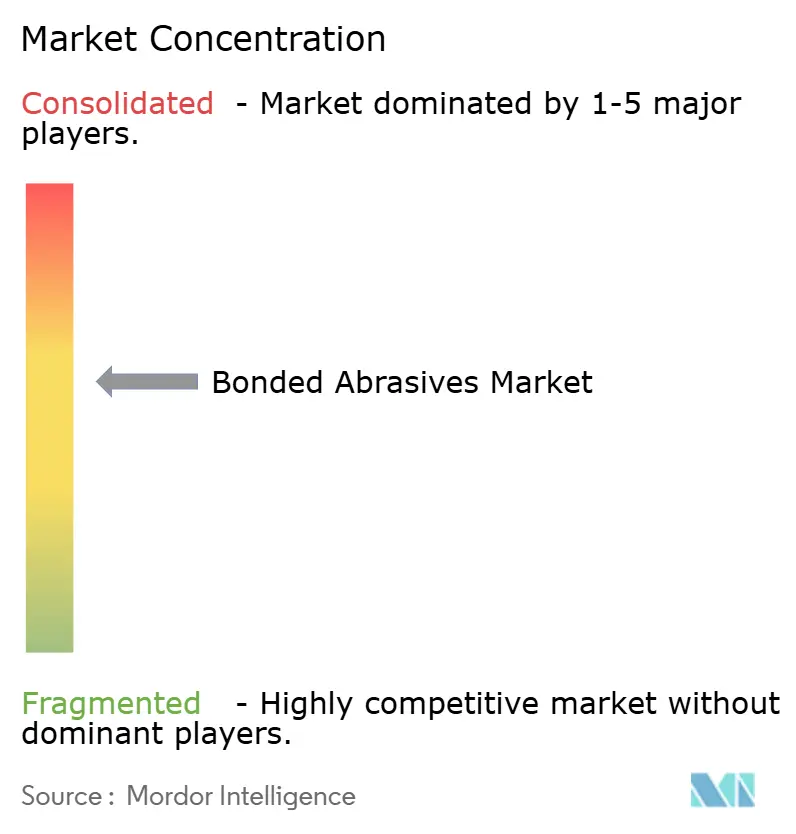

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bonded Abrasives Market Analysis by Mordor Intelligence

The Bonded Abrasives Market size is estimated at USD 25.23 billion in 2026, and is expected to reach USD 32.39 billion by 2031, at a CAGR of 5.12% during the forecast period (2026-2031). Continued electrification in vehicle powertrains, aerospace reshoring across North America and Europe, and infrastructure-driven metal-working expansions in Asia-Pacific collectively sustain demand for precision grinding wheels. Vitrified bond products dominate heavy-duty cylindrical and surface grinding lines, while resin bonds penetrate high-speed setups that exceed 25 m/s peripheral speed. Tighter geometric tolerances in electric motors and battery housings widen the application base for cubic boron nitride (CBN) and ceramic grains, and AI-enabled tool-room automation improves productivity by shortening dressing cycles. Regional players are scaling capacity in thin cutting wheels and high-purity silicon carbide, intensifying competition with incumbents that still control 40-45% of global revenue.

Key Report Takeaways

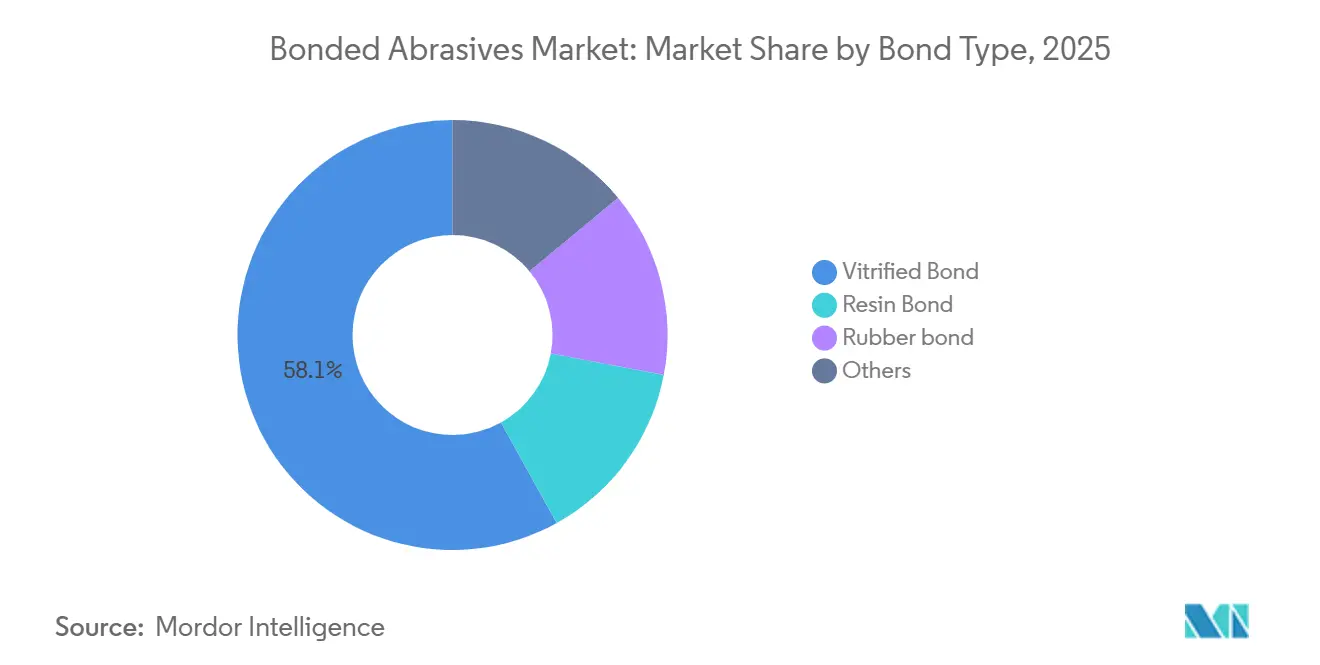

- By bond type, vitrified bond led with 58.06% bonded abrasives market share in 2025 and is projected to register a 5.49% CAGR through 2031.

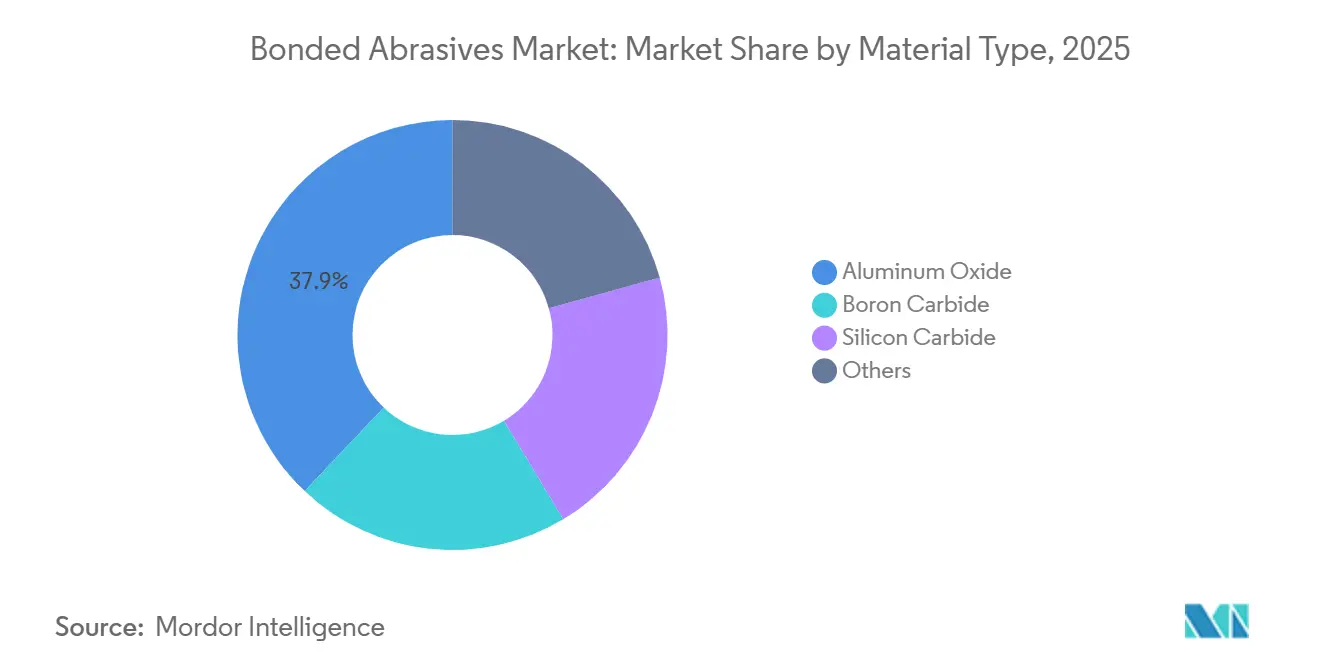

- By material type, aluminum oxide accounted for 37.93% of the bonded abrasives market size in 2025 and is advancing at a 5.46% CAGR through 2031.

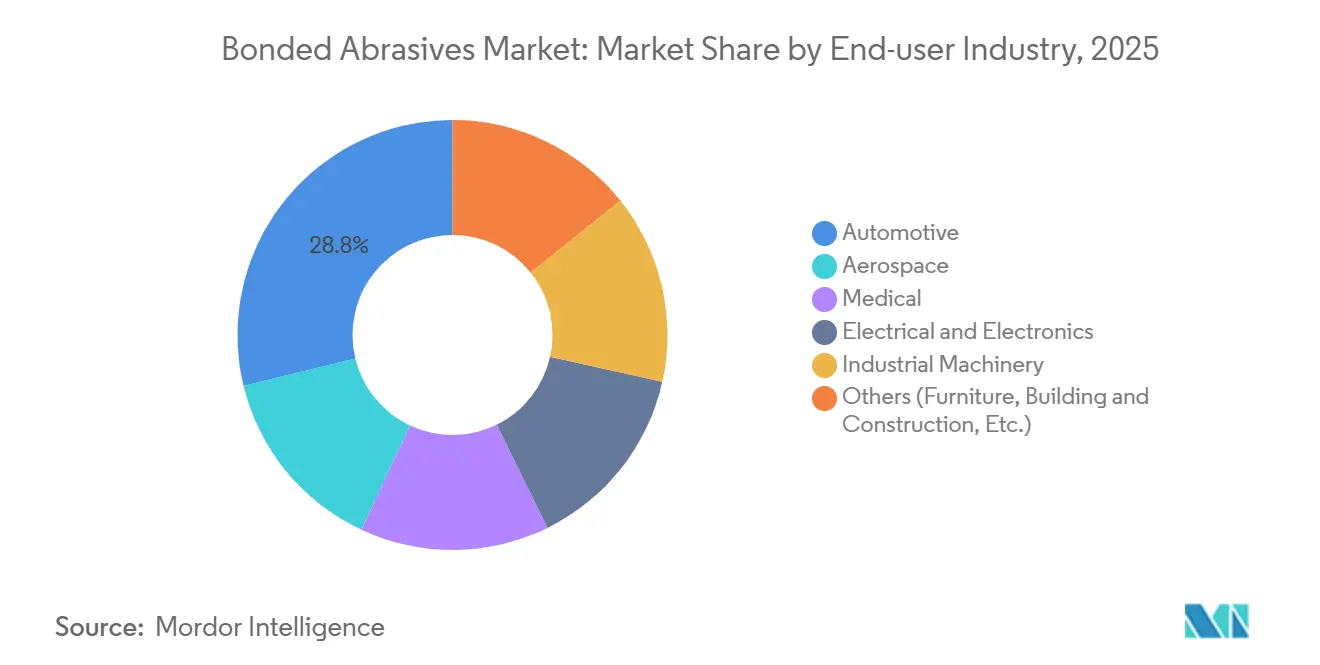

- By end-user industry, automotive held 28.79% revenue in 2025 and is projected to expand at a 5.56% CAGR during 2026-2031.

- By geography, Asia-Pacific captured 56.48% revenue in 2025; the region is forecast to post a 5.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bonded Abrasives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-Led Metal-Working Boom in Asia | +1.5% | Asia-Pacific core, spillover to Middle East and Africa | Long term (≥ 4 years) |

| Resinoid Wheels Enabling Greater Than 25 m/s High-Speed Grinding Lines | +1.0% | Global, concentrated in North America and Europe aerospace hubs | Medium term (2-4 years) |

| Shift To Precision Ceramics and CBN Grains in EV Power-Trains | +1.3% | Global, led by China, Europe, North America EV manufacturing clusters | Medium term (2-4 years) |

| AI-Driven Tool-Room Automation (Self-Sharpening Set-Ups) | +0.8% | North America and Europe advanced manufacturing, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Re-Shoring of US/EU Aerospace Machining Capacity | +0.9% | North America and Europe, focused on Midwest, South, Mountain West regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infrastructure-Led Metal-Working Boom in Asia

Regional steel output is rising as India produced 144.3 million t in fiscal 2024, up 13.4% year on year, while new capacity in Vietnam and Indonesia adds flat-rolled output for construction projects[1]Ministry of Steel, “Annual Report 2023-24,” steel.gov.in . More steel means more billet grinding, structural-beam finishing, and rebar cutting, which directly lifts bonded abrasives market demand. Chinese mill utilization is softening, yet Wood Mackenzie expects India, Thailand, and the Philippines to absorb volume through 2031, shifting wheel consumption southward. Japan and South Korea remain buyers of CBN and diamond wheels for semiconductor wafer and micro-finishing work, underscoring a stable premium niche. Governments channel infrastructure budgets into metro rail, port dredging, and bridge expansion, locking in multi-year orders for aluminum-oxide wheels. The result is predictable long-cycle revenue visibility for both global and local producers.

Resinoid Wheels Supporting greater than 25 m/s Grinding Lines

Automotive crankshaft and aerospace turbine machining increasingly runs at peripheral speeds that vitrified wheels cannot safely withstand, so resin bonds with elastic phenolic matrices are preferred. Peer-reviewed trials show resin-bond diamond wheels sustain 125 m/s in production, slashing cycle time by 30% and reducing heat-affected zones on nickel superalloys. Aerospace OEMs therefore cut finishing passes while maintaining Ra ≤ 0.4 µm surface finishes. Electric-vehicle motor shafts require roundness within 5 µm, a tolerance easier to hit with shock-resistant resin wheels. Automotive tier-1 suppliers deploy these wheels to hit takt times below 60 s per shaft, protecting throughput. With peripheral speeds still climbing, demand elasticity favors suppliers able to certify wheels under ISO 21940 burst-test criteria.

Precision Ceramics and CBN for EV Powertrains

CBN generates lower grinding forces and up to 15% finer surface finishes on induction-hardened steel shafts than aluminum oxide, eliminating secondary polish steps. Electric motors that spin beyond 15,000 rpm need such finishes to avoid vibration, and EV makers now specify CBN wheels in purchasing tenders. Ceramic grains that micro-fracture under load create a self-sharpening action on aluminum housings, preventing built-up edge. Battery pack machining for thin-wall aluminum castings benefits from this self-sharpening, extending wheel life by nearly 20% versus conventional abrasives. The bonded abrasives market therefore pivots toward higher-margin super-abrasive formats, boosting average selling price even if volume growth moderates.

AI-Driven Tool-Room Automation

Fraunhofer IEM’s RoboGrinder uses vibration and acoustic sensors to adjust feed and speed in real time, trimming cycle time by 40% and cutting dressing frequency 15% in pilot runs. Chalmers University’s Grinding 4.0 digital twin predicts wheel wear with 98.1% accuracy, guiding optimal dressing-infeed depth and length. Shops achieve lights-out production during night shifts, trimming labor expense and improving spindle utilization. Suppliers able to embed RFID chips that communicate wheel ID and wear history position themselves for service-based revenue streams. Early adopters report scrap reductions of 7 pp, reinforcing a data-driven pull for high-precision wheels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-Intensive Firing Furnaces Facing Carbon Taxes | -0.6% | Europe and North America, emerging in China | Medium term (2-4 years) |

| Ti-Oxide And Phenolic-Resin Price Volatility greater than 18% YoY | -0.4% | Global, acute in North America and Europe due to import reliance | Short term (≤ 2 years) |

| Stricter PM2.5 Limits in India and China Grinding Shops | -0.5% | Asia-Pacific, concentrated in India and China manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy-Intensive Firing Furnaces and Carbon Taxes

Vitrified wheels fire above 1,200 °C, consuming 3-5 MWh per tonne and emitting significant CO2. The European Commission requires 55% emissions cuts by 2030, obliging ceramic plants to retrofit electric or hydrogen kilns that each cost more than EUR 10 million[2]European Commission, “Industrial Carbon Management Strategy COM 2024/62,” ec.europa.eu . U.S. industrial policy offers tax credits for electrified furnaces, yet smaller producers still face USD 8-12 million up-front capital. Chinese dual-control caps have already forced Henan and Shandong operations to curtail peak-season output, lengthening wheel lead times to eight weeks. Higher energy surcharges narrow operating margins and could delay capacity additions, moderating bonded abrasives market expansion where vitrified products dominate.

Ti-Oxide and Phenolic-Resin Price Volatility greater than 18% YoY

Titanium dioxide and phenolic resin spot prices swung more than 18% year on year in 2024-2025, squeezing resin-bond wheel makers that lack hedging cover. U.S. fused alumina output hovers near 22,000 t, leaving import dependence above 95%, with China supplying 91% of crude tonnage. Freight spikes and tariffs amplify cost uncertainty. BASF is boosting MDI capacity in Louisiana by 58% to stabilize resin feedstock, but the new train will not commission until 2026. Producers increasingly trial bio-based resins, yet scale remains limited, so pricing risk remains a near-term headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bond Type: Vitrified Bond Hold Precision Edge

Vitrified bond secured 58.06% bonded abrasives market share in 2025 and is projected to register a 5.49% CAGR to 2031. Its rigid, porous structure resists burn and preserves geometry on crankshafts, camshafts, and turbine blades even under heavy normal forces. Vitrified variants also enable in-process conditioning that keeps surface integrity consistent during long production runs. Research partnerships such as Chalmers Grinding 4.0 lower tool cost per part by predicting dressing intervals, improving wheel utilization by 15 pp.

Resin bonds, cured below 200 °C, are capturing high-speed applications where elastic matrices absorb shock and limit catastrophic bursts. Automotive EV lines value that resilience for motor shaft grinding at peripheral speeds above 80 m/s. Rubber bonds, while niche at single-digit share, remain essential for thin cutting disks and centerless grinding where vibration damping improves finish. Metal and shellac bonds fill ultra-precision optics roles, rounding out a diverse bonded abrasives market.

By Material Type: Aluminum Oxide Anchors Ferrous Grinding

Aluminum oxide captured 37.93% of bonded abrasives market size in 2025 and is forecast at a 5.46% CAGR through 2031, driven by cost-effective grinding of carbon and alloy steel. Import concentration exposes users to tariff shocks, yet volume remains sticky because no other conventional grain balances cost and toughness as effectively. Silicon carbide targets non-ferrous metals, ceramics, and composites where friable edges slice cleanly. CUMI’s high-purity plant now under construction addresses semiconductor wafer lapping where 99.5% purity matters.

CBN and engineered ceramic grains penetrate EV, aerospace, and medical implants where lower grinding forces and self-sharpening improve part integrity. B4C satisfies sapphire wafer and armor applications but stays limited due to brittleness and price. Regulatory pressure on dust and VOC emissions pushes producers to incorporate cool-cutting engineered pores that lower grinding temperature and improve environmental compliance.

By End-User Industry: Automotive Leads, Medical Precision Rises

Automotive absorbed 28.79% bonded abrasives market revenue in 2025, the largest slice, and is expanding at 5.56% CAGR on the back of tighter EV tolerances and higher rotating speeds. EV assembly requires CBN wheels to hit sub-5 µm concentricity on drive shafts, while aluminum housings shift toward ceramic grains for smear-free cuts. Aerospace follows, consuming resin-bond CBN wheels for superalloy turbine blades as global shop visits rise with fleet age.

Medical device makers increasingly demand ultra-smooth titanium and cobalt-chrome implant surfaces, opening upscale niches for cotton-fiber and resin unitized wheels that run cool. Electronics manufacturers specify diamond and CBN disks to finish silicon carbide wafers to Ra less than 0.1 µm. Industrial machinery, construction fabrication, and general engineering round out demand, prioritizing wheel life and cost per cut over extreme precision.

Geography Analysis

Asia-Pacific commanded 56.48% bonded abrasives market revenue in 2025 and is forecast for a 5.71% CAGR to 2031, the quickest global pace. India is the swing consumer as crude steel output rose 13.4% to 144.3 million t in 2024, and capital spending on thin-wheel and silicon-carbide lines underscores local appetite. Tyrolit’s new Pune plant strengthens regional access to CBN and diamond wheels, shrinking freight time from Europe to two weeks. Southeast Asia funnels public funds into bridges and rail corridors, pulling demand for cost-effective aluminum-oxide wheels on structural steel. Japan and South Korea hold premium niches in semiconductor wafer grinding, reliant on CBN and diamond grains.

In North America, aerospace reshoring stimulates CBN demand, yet carbon taxes and high electricity tariffs raise vitrified production costs. DOE tax credits encourage kiln electrification, but only large plants achieve the scale to invest. Tariff exposure remains acute because 91% of fused alumina imports originate in China, motivating alternative supply chains from Australia and Guyana.

Europe mirrors North American challenges. The EU Industrial Carbon Management strategy compels 55% CO2 reductions by 2030, so Saint-Gobain pilots hydrogen kilns in France while midsized Italian manufacturers weigh LNG-to-electric transitions. Germany, Italy, and France together sustain automotive and aerospace grinding volumes, but cost pressures shift some downstream machining to Eastern Europe.

South America and Middle East and Africa together represent low bonded abrasives market revenue. Brazil’s vehicle assembly plants still grind crankshafts with vitrified aluminum-oxide wheels, while Saudi Arabian infrastructure projects buy cutting disks for pipeline fabrication. South African mining operations use resin-bond wheels for drill-bit sharpening where wheel life outweighs finish requirements.

Competitive Landscape

Global bonded abrasives competition is moderately concentrated. 3M, Saint-Gobain, Bosch, Tyrolit, and CUMI together captured about 42% of 2025 sales. 3M released 169 new abrasive products in 2024, including Cubitron 3 belts for robotic cells that enable higher removal rates at lower pressure. Saint-Gobain invests in hydrogen-ready tunnel kilns to trim Scope 1 emissions by 30% in French plants, meeting EU targets. Bosch runs a 20-site carbide recycling loop, delivering 50% carbon reduction and cost savings for end users who offset raw-material volatility.

CUMI acquired Germany-based Rhodius for EUR 55 million in 2022, gaining the world’s thinnest cutting wheel technology and expanding European distribution. The company follows with INR 350 crore in fiscal 2025 capex for a 50 million-wheel plant and a 6 t/month high-purity SiC furnace. Tyrolit’s Pune facility, operational by 2026, targets double-digit Asia share within five years through localized CBN and diamond production.

Emerging challengers, especially in India and China, scale thin-wheel lines and exploit lower energy costs, pressuring incumbents on price. Technology differentiation shifts toward sensor-embedded wheels and cloud analytics that predict wear. Suppliers offering AI-enabled process control win contracts in aerospace blade refurbishment lines seeking to minimize scrap. Raw-material backward integration, particularly in fused alumina and SiC, becomes a hedge against geopolitical trade risk.

Bonded Abrasives Industry Leaders

3M

Saint-Gobain

Tyrolit AG

CUMI

Robert Bosch Power Tools GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Mirka Ltd completed the acquisition of all bonded conventional abrasive wheels assets from Hermes Schleifmittel GmbH, a producer of abrasives. The addition of Hermes' bonded wheels expands Mirka's portfolio, which now includes diamond, CBN, and conventional wheels.

- June 2025: Tyrolit AG commenced construction of its first Indian manufacturing facility in Pune. The plant will produce CBN and diamond grinding wheels, which are key components of the bonded abrasives market.

Global Bonded Abrasives Market Report Scope

Bonded abrasives are a mixture of abrasive grains, fillers, and bonding materials. They are used to remove surface materials such as metal, ceramics, glass, plastics, and paints. These abrasives are used in both grinding wheels and abrasives stones or sticks.

The bonded abrasives market is segmented by bond type, material type, end-user industry, and geography. By bond type, the market is segmented into vitrified bond, resin bond, rubber bond, and others. By material type, the market is segmented into aluminum oxide, boron carbide, silicon carbide, and others. By end-user industry, the market is segmented into automotive, aerospace, medical, electrical and electronics, industrial machinery, and others (including furniture, building and construction). The report also covers the market size and forecasts for 16 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of value (USD).

| Vitrified Bond |

| Resin Bond |

| Rubber bond |

| Others |

| Aluminum Oxide |

| Boron Carbide |

| Silicon Carbide |

| Others |

| Automotive |

| Aerospace |

| Medical |

| Electrical and Electronics |

| Industrial Machinery |

| Others (Furniture, Building and Construction, Etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Bond Type | Vitrified Bond | |

| Resin Bond | ||

| Rubber bond | ||

| Others | ||

| By Material Type | Aluminum Oxide | |

| Boron Carbide | ||

| Silicon Carbide | ||

| Others | ||

| By End-user Industry | Automotive | |

| Aerospace | ||

| Medical | ||

| Electrical and Electronics | ||

| Industrial Machinery | ||

| Others (Furniture, Building and Construction, Etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current bonded abrasives market size?

The bonded abrasives market size totaled USD 25.23 billion in 2026 and is projected at USD 32.39 billion by 2031.

Which segment leads by bond type?

Vitrified bond dominates with 58.06% bonded abrasives market share in 2025.

Which region is growing fastest?

Asia-Pacific shows the quickest growth, forecast at a 5.71% CAGR during 2026-2031.

How are carbon taxes affecting producers?

European and North American plants must retrofit kilns, raising capital needs by USD 8-12 million per facility and pressuring margins.

Page last updated on: