Boat And Ship MRO Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 38.38 Billion |

| Market Size (2031) | USD 55.69 Billion |

| Growth Rate (2026 - 2031) | 7.73% CAGR |

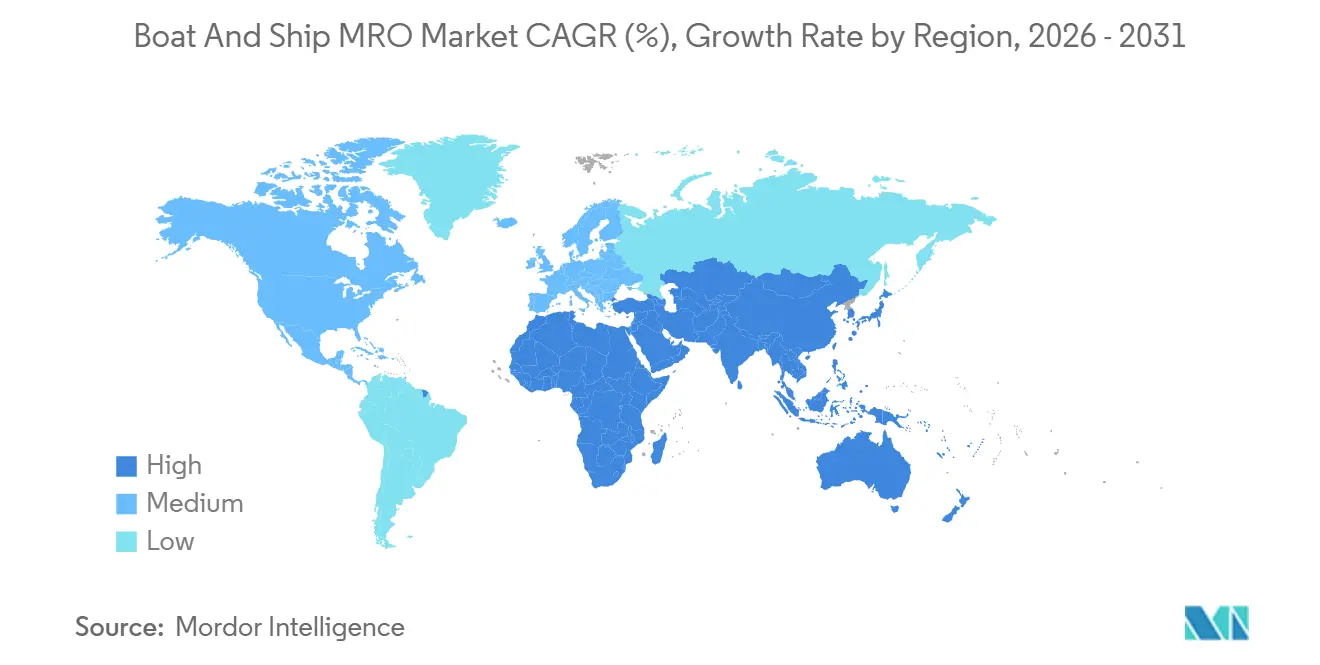

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

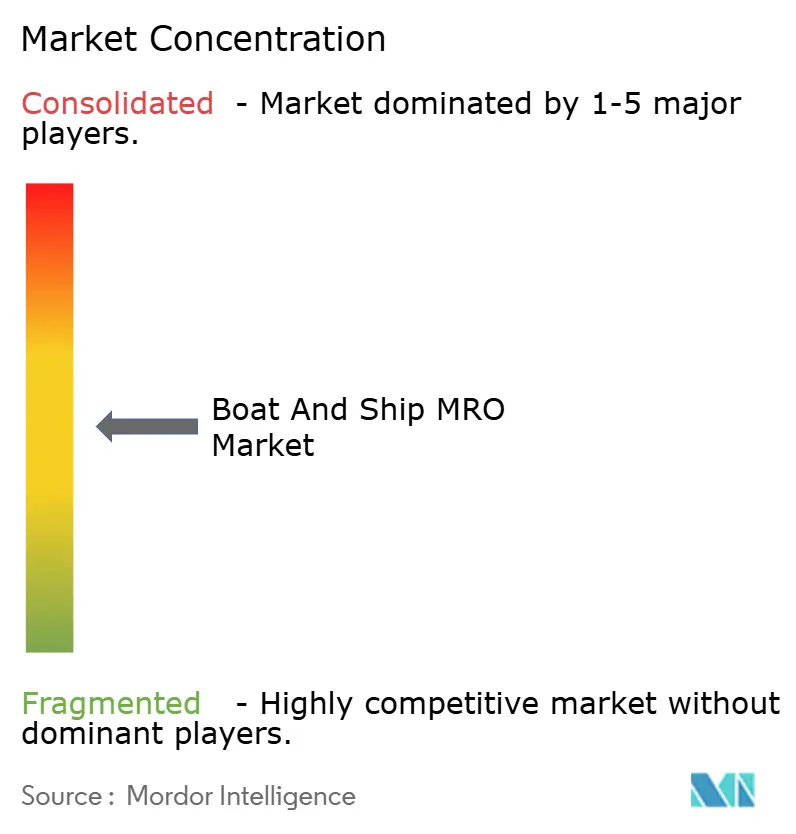

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Boat And Ship MRO Market Analysis by Mordor Intelligence

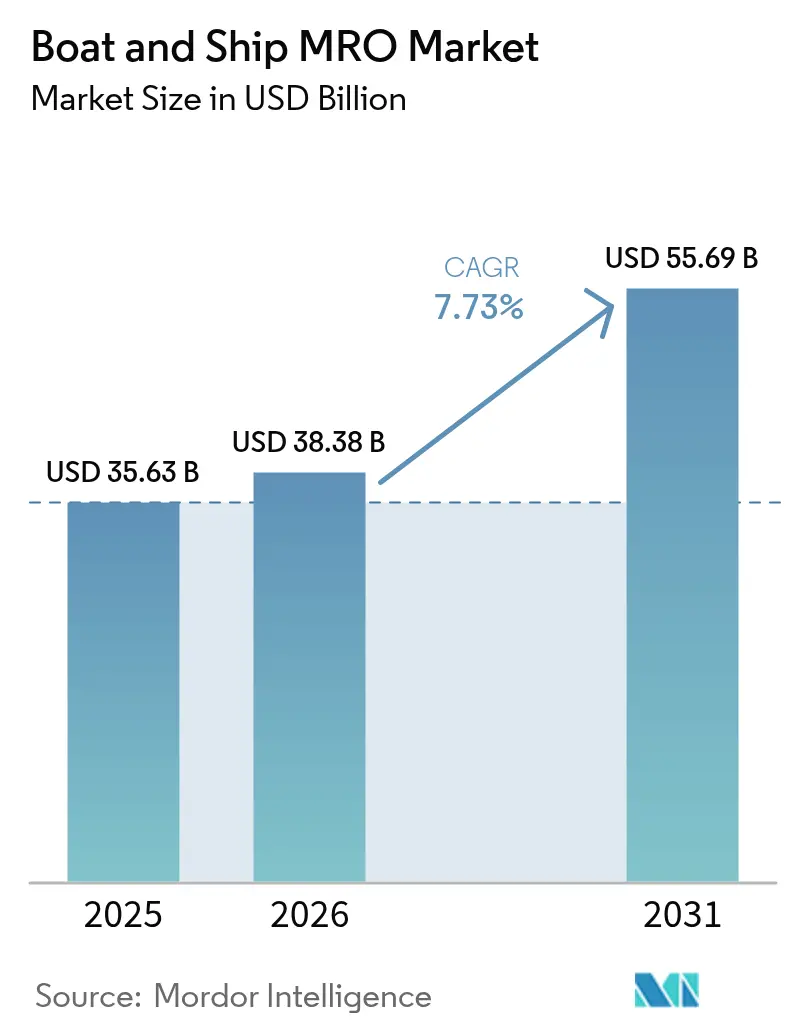

The Boat and Ship MRO Market size is projected to be USD 35.63 billion in 2025, USD 38.38 billion in 2026, and reach USD 55.69 billion by 2031, growing at a CAGR of 7.73% from 2026 to 2031. As of 2024, fleet owners are grappling with rising costs and stringent compliance requirements. The average age of vessels has reached a significant milestone, coinciding with the International Maritime Organization (IMO) tightening performance thresholds through its Energy Efficiency Existing Ship Index (EEXI) and Carbon Intensity Indicator (CII) regimes, set to take effect in the near future. While condition-based monitoring is prolonging docking intervals, the scope of overhauls during each visit is broadening. This shift has led to a notable increase in average yard invoices. Predictive maintenance platforms, spearheaded by OEMs such as Wärtsilä and ABB, now oversee a substantial number of vessels, resulting in a significant reduction in unplanned downtime. Meanwhile, green-retrofit subsidies in Europe and North America are driving the adoption of technologies like scrubbers, ballast-water systems, and dual-fuel engines. This trend is compelling mid-tier yards to either specialize or relinquish work to larger, vertically integrated OEM networks.

Key Report Takeaways

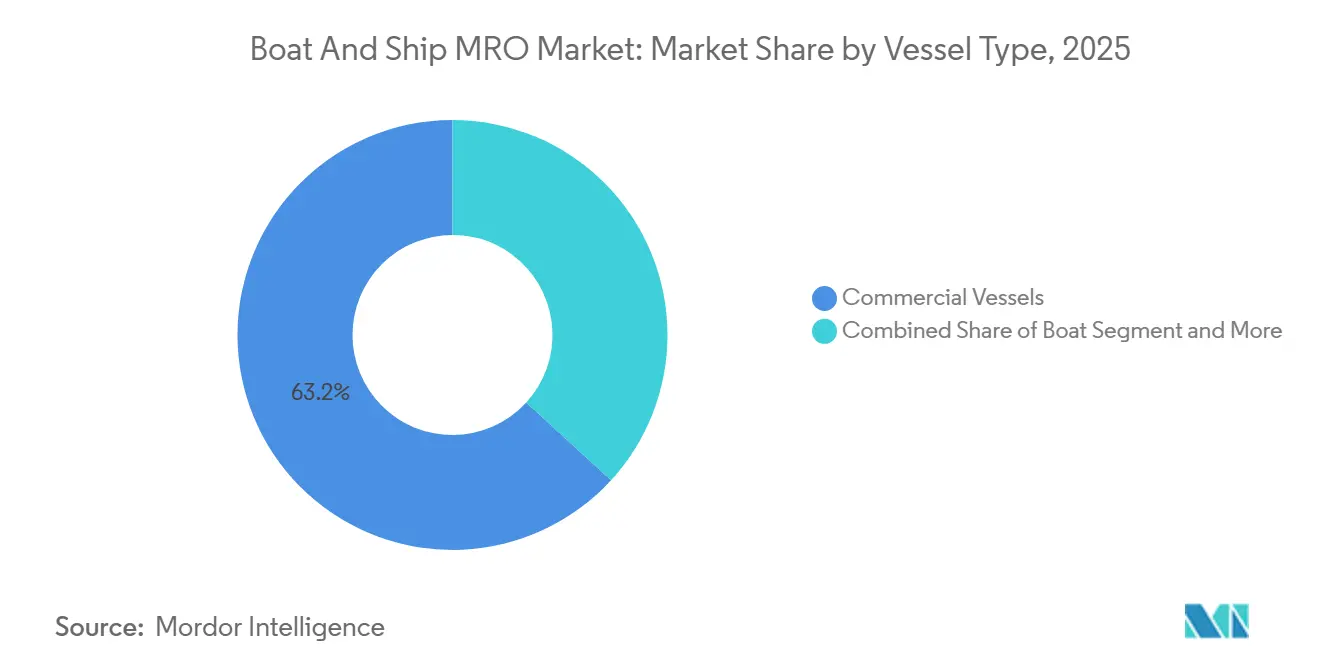

- By vessel type, commercial craft led with 63.17% of boat and ship MRO market share in 2025 and is projected to post the highest CAGR of 7.75% till 2031.

- By vessel application, commercial platforms accounted for 58.73% of the boat and ship MRO market size in 2025, yet defense programs are advancing at a 7.87% CAGR through 2031.

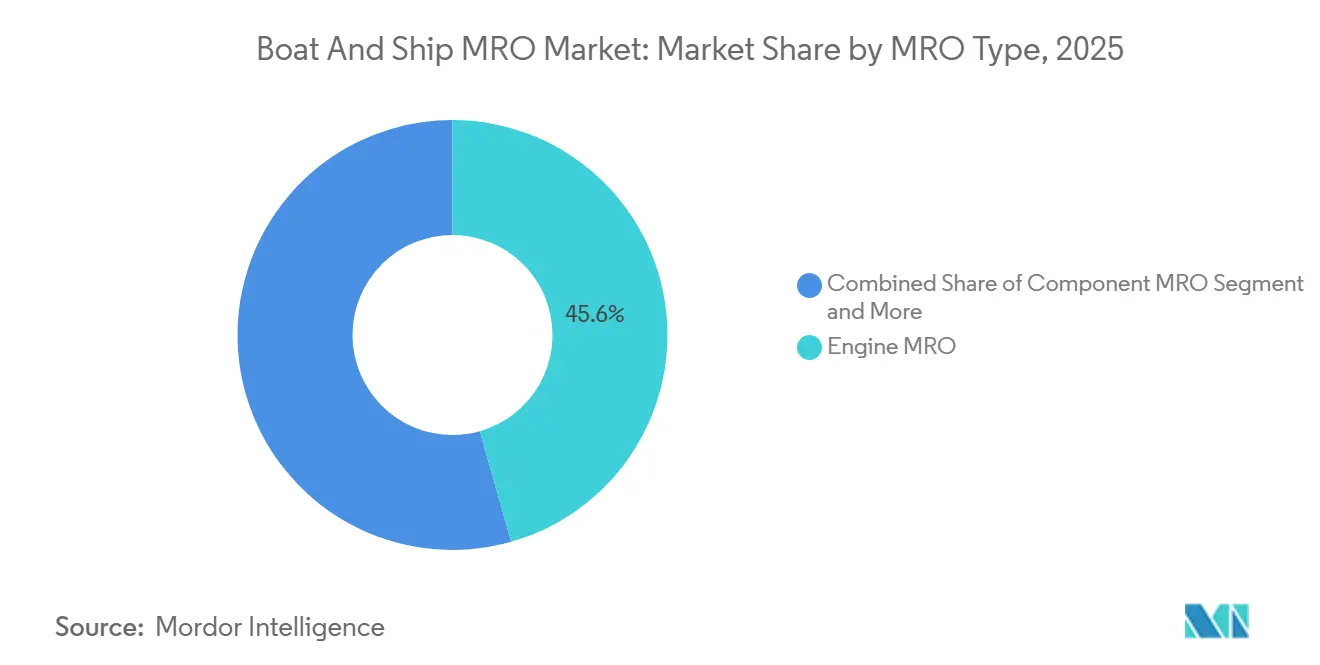

- By MRO type, engine work accounted for 45.56% of 2025 spending, whereas modifications and retrofits are forecast to expand at a 7.78% CAGR through 2031.

- By service-provider type, independent yards captured a 52.37% share in 2025, but OEM-affiliated networks are set to grow fastest at 7.85% through 2031.

- By geography, Asia Pacific accounted for 36.73% of revenue in 2025 and is projected to maintain a 7.83% growth trajectory, supported by Chinese yard consolidation and India’s Sagarmala coastal shipping push.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Boat And Ship MRO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter IMO Environmental Mandates | +1.8% | Global, with EU and North America leading enforcement | Medium term (2-4 years) |

| Aging Global Vessel Fleet | +1.5% | Global, concentrated in Europe and Asia Pacific | Long term (≥ 4 years) |

| Growth in Commercial Marine Trade | +1.2% | Asia Pacific core, spillover to Middle East and Africa | Medium term (2-4 years) |

| Naval Fleet Modernization Budget | +1.0% | North America, Europe, Asia Pacific (India, Japan, South Korea) | Long term (≥ 4 years) |

| Predictive-Maintenance Adoption by Mid-Sized Yards | +0.9% | Europe and North America early adopters, Asia Pacific scaling | Short term (≤ 2 years) |

| Green-Retrofit Subsidies for Coastal Tourism Craft | +0.6% | Europe (Mediterranean, Baltic), North America (Great Lakes, coastal states) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter IMO Environmental Mandates

In 2026, the EEXI and CII rules came into full effect, imposing penalties on vessels rated in lower performance bands. This has driven ship owners to adopt energy-efficiency retrofits, including measures such as low-friction hull coatings, propeller re-pitching, and engine derating. Starting in 2027, FuelEU Maritime will impose monetary penalties for voyages heading to the EU. This makes it economically viable for ships, especially those with significant remaining service life, to consider converting to scrubbers or LNG. In 2024, Maersk undertook retrofitting on a substantial portion of its container ships, achieving a notable reduction in fleet fuel consumption and postponing newbuild orders [1]“Sustainability Report 2025,” Maersk, maersk.com . Ballast-water installation backlogs now stretch into mid-2026 at Singapore and South Korean yards, reinforcing the competitive edge of facilities holding class approvals and OEM alliances.

Aging Global Vessel Fleet

The median age of merchant fleets has significantly increased, as owners delayed new builds during the pandemic. For older ships, steel renewals now account for a substantial portion of dry-dock budgets. Meanwhile, engine invoices are primarily driven by crankshaft grinding and turbocharger refurbishments. This trend is evident in the U.S. Jones Act fleet, where the average tanker age continues to rise. With replacement costs becoming prohibitively high, operators are increasingly committed to ongoing mid-life overhauls. Furthermore, independent yards, lacking access to OEM technical data, face difficulties executing complex diesel upgrades, leading to a shift of such work to branded service centers.

Growth in Commercial Marine Trade

In recent years, seaborne volumes have grown significantly, driven by container flows from Asia to North America and U.S. LNG exports to Europe. Ultra-large container vessels (ULCVs) and huge crude carriers (VLCCs) now require graving docks with wider beams, sidelining mid-tier facilities. Over the same period, MSC conducted numerous dry-dockings across multiple nations, opting for yards that offered swift turnarounds and scrubber capabilities. New regional hubs are emerging in the UAE and India, driven by corridors such as the India-Middle East-Europe Economic Corridor.

Naval Fleet Modernization Budget

In FY 2026, the U.S. Navy allocated a substantial budget for ship construction, with a significant portion directed toward Columbia-class SSBNs. These vessels will require specialized maintenance, repair, and overhaul (MRO) services at key facilities, including Electric Boat and Newport News. Meanwhile, Japan, India, and South Korea are actively expanding their destroyer and submarine fleets. They are incorporating long-term support clauses into their contracts, ensuring sustained yard utilization for decades. Furthermore, these defense contracts, characterized by cost-plus terms, require security clearances, thereby strengthening the positions of industry incumbents such as Huntington Ingalls, BAE Systems, and Fincantieri.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Intensity and Dock-Capacity Scarcity | -0.8% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Marine-Fuel Price Volatility Limiting Budgets | -0.6% | Global, most severe in emerging markets | Short term (≤ 2 years) |

| Skilled Labor Gap in Composite-Hull Repair | -0.4% | Europe and North America, niche impact in Asia Pacific | Long term (≥ 4 years) |

| Cyber-Security Compliance Cost for Connected Vessels | -0.3% | Global, with stricter enforcement in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity & Dock-Capacity Scarcity

Constructing a new dock for large ships can require significant investment and take several years, a timeline that deters expansion in regulated areas. U.S. East Coast shipyards operate at high capacity, with naval projects dominating the most sought-after slots; for instance, a major facility in Norfolk dedicated a substantial portion of its capacity to Navy surface combatants. Environmental clearances can lengthen these timelines, as highlighted by the California Coastal Commission's recent blockage of a dock extension in San Diego.

Marine-Fuel Price Volatility Limiting Budgets

In 2024-25, very-low-sulfur fuel oil prices fluctuated significantly. A notable price increase could eliminate profits for a small-sized bulker, leading owners to delay maintenance activities such as painting and steel work. In European hubs, LNG bunker prices also showed considerable volatility, leading to some dual-fuel retrofits being postponed. Independent yards, dependent on spot contracts, faced cancellations as operators prioritized cash conservation. In contrast, OEM networks benefited from the stability provided by multi-year service agreements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vessel Type: Commercial Dominance Masks Yacht Complexity

Commercial vessels held 63.17% of the boat and ship MRO market share in 2025 and are projected to post a 7.75% CAGR till 2031. With an extensive global fleet, the Panama Canal's recent draft restrictions prompted container ships to renew hull coatings, ensuring they retained their transit slots. While yachts represent a smaller tonnage class, they command premium returns on a dollar-per-meter basis. European yards in key countries secured a majority of high-value refits recently. However, labor shortages in composite repairs significantly extended queue times. Demand for recreational boats remains fragmented, channeled through marinas and mobile technicians. In contrast, research ships and dredgers depend on specialized yards adept at DP system calibration. Consequently, the boat and ship MRO market showcases varied service models, limiting economies of scale across its sub-segments.

The commercial fleet's retrofit cycle, with scrubber installations alone projected to contribute significantly to the market over the coming years, serves as a cornerstone for the boat and ship MRO market. While yacht refits are influenced by the discretionary spending of high-net-worth individuals—contracting in recent years but witnessing a rebound in the near future—boat work remains subject to seasonal fluctuations. These seasonal demands create staffing challenges each spring in North America. Such disparities compel yards to carve out specializations; those attempting to straddle both yachts and commercial hulls frequently find themselves grappling with margin underperformance, a consequence of mismatches in tooling and talent.

By Vessel Application: Defense Outpaces Commercial Growth

Commercial traffic accounted for 58.73% of the boat and ship MRO market in 2025, yet naval projects are set to record the fastest 7.87% CAGR through 2031 as modernization budgets rise. The U.S. Navy is making a significant investment to expand Groton facilities to support Columbia-class lifecycle operations. Meanwhile, Japan has approved a notable increase in its maritime defense budget for the upcoming fiscal year. While commercial revenues surpass those of the defense sector, the former face narrowing margins due to competitive tenders, prompting shipyards to focus on extended naval contracts.

Defense Maintenance, Repair, and Overhaul (MRO) operations are constrained by rigorous cybersecurity mandates and compliance with the Defense Federal Acquisition Regulation Supplement (DFARS). These requirements impose substantial infrastructure costs on shipyards, thereby raising entry barriers. Commercial entities are increasingly adopting naval availability contracts, agreeing to fixed annual fees in exchange for uptime assurances, a model that primarily benefits Original Equipment Manufacturer (OEM) networks. In the private-vessel MRO segment, the market remains highly fragmented, with a yard's reputation outweighing pricing considerations in the selection process.

By MRO Type: Retrofits Accelerate Amid Regulatory Pressure

Engine work accounted for 45.56% of 2025 spending, but retrofits will post the quickest 7.78% CAGR to 2031, driven by scrubber, ballast-water, and dual-fuel conversions. Wärtsilä reported a significant increase in 2025 retrofit bookings for its dual-fuel engines, highlighting a strategic shift. Meanwhile, Component MRO is leveraging predictive analytics, resulting in a notable reduction in emergency repairs for fleets using ABB’s monitoring suite.

Dry-dock and hull operations remain capital-intensive, as graving-dock amortization demands a substantial volume of work. With class-approved sensors, condition-based surveys now enable vessels to achieve extended docking windows. This not only alleviates scheduling pressures but also expands the scope of work during each visit. As a result, retrofits generate consistent, high-value demand, solidify relationships among yards, classification approvals, and OEM partnerships, and create a distinct separation from standard commodity repair shops.

By Service Provider Type: OEM Networks Gain Share

Independent providers retained a 52.37% share in 2025, but OEM-affiliated MROs are projected to compound at 7.85% through 2031. In a relatively short period, Wärtsilä's global service organization and Rolls-Royce's PerformancePlus contracts, which meld remote diagnostics with performance guarantees, have captured a significant share of the agreements for commercial vessels in Europe.

Independent yards, especially in Turkey and Romania, are offering considerably lower prices than their Western European counterparts for hull steel and paint jobs, areas where proprietary data carry less weight. While in-house operator facilities can manage daily repairs, they fall short in scale for extensive overhauls. As a result, the boat and ship MRO market is splitting into two distinct segments: high-tech OEM ecosystems and cost-effective independents, leaving a diminishing middle ground.

Geography Analysis

Asia Pacific dominated the boat and ship MRO market, accounting for 36.73% of revenue in 2025 and forecast to grow at a 7.83% CAGR through 2031. Chinese consolidation led by CSSC, Hanwha Ocean's recent deal with Philly Shipyard, marking South Korea's return to the Jones Act, and India's Sagarmala expansions are pivotal drivers. Seatrium, based in Singapore, secured a significant contract for offshore wind vessel refits in the near term, capitalizing on the combined strengths of Keppel and Sembcorp [2]“Annual Report 2025,” Seatrium Ltd., seatrium.com . While Japan's submarine life-extension program bolsters demand at Mitsubishi and Kawasaki yards, geopolitical tensions dampen Western owners' interest in Chinese facilities.

North America grapples with a dock shortage, as naval orders consume a substantial portion of available capacity. The Jones Act, while protective, inflates domestic MRO costs significantly compared to global norms. Recently, Canada’s Seaspan clinched a significant contract for icebreaker MRO, and U.S. yards like NASSCO are balancing Navy and commercial bookings well into the future, nudging operators to consider Mexican docks.

Europe harmonizes high-value naval and yacht endeavors with competitive commercial propositions from Turkey and Romania. Fincantieri's contract for the Italian Navy's LHD includes decades of lifecycle commitments, and Navantia's export of S-80 Plus submarines ensures Spanish facilities remain busy for an extended period [3]“FY 2026 Shipbuilding Budget Highlights,” U.S. Navy, navy.mil . While EU Innovation Fund subsidies for green retrofits favor local yards, budget-conscious owners are still opting to send tankers to Turkish graving docks, enjoying significant cost savings.

Competitive Landscape

The leading participants hold a significant share of the global dry-dock capacity, indicating a moderately concentrated market. In the U.S. and the U.K., Huntington Ingalls and BAE Systems dominate the naval MRO sector, leveraging their expertise in nuclear propulsion and holding crucial security clearances. Meanwhile, Fincantieri, Naval Group, and thyssenkrupp Marine Systems lead defense initiatives in continental Europe. In the commercial arena, Damen, Seatrium, and Cosco compete for hull contracts, focusing on turnaround speed and pricing.

OEM service networks like Wärtsilä, Rolls-Royce, and Caterpillar are strengthening their market presence. By integrating predictive analytics with their parts monopolies, they are effectively locking clients into proprietary ecosystems. While high-margin niches such as composite-hull repairs, autonomous-vessel maintenance, and electrification retrofits offer lucrative opportunities, they require advanced skills and significant capital investment.

Supported by state backing, Korean players Hanwha Ocean and HD Hyundai are offering competitive bids that challenge established players on Jones Act and allied-navy contracts, putting pressure on profit margins. In a move favoring digitally advanced yards, classification societies are revising regulations to allow condition-based survey intervals, reducing the demand for traditional dock cycles.

Boat And Ship MRO Industry Leaders

BAE Systems plc

Huntington Ingalls Industries Inc.

Damen Shipyards Group

Hyundai Heavy Industries Co.

Seatrium Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Seatrium Offshore Technology and Cochin Shipyard Limited inked an MoU, setting their sights on collaborative MRO (Maintenance, Repair, and Overhaul) projects throughout Asia. This partnership aims to leverage the strengths of both companies to address the growing demand for MRO services in the region, enhancing operational efficiency and expanding their market presence.

- August 2025: Hyundai Heavy Industries secured the scheduled overhaul of the USNS Alan Shepard in Ulsan. This project highlights Hyundai Heavy Industries' expertise in ship maintenance and repair, further strengthening its position in the global shipbuilding and repair market.

- August 2025: Vigor Marine Group and Samsung Heavy Industries have partnered to significantly expand MRO options in the Indo-Pacific for the U.S. Navy and the Military Sealift Command (MSC).

Global Boat And Ship MRO Market Report Scope

The scope of the report includes Vessel Type (Boat, Yacht, and More), Vessel Application (Private and More), MRO Type (Engine MRO and More), Service Provider Type (Independent Yards and More), and Geography.

| Boat |

| Yacht |

| Commercial Vessels |

| Other Types |

| Private |

| Commercial |

| Defense |

| Engine MRO |

| Component MRO |

| Dry-dock / Hull |

| Modifications and Retrofits |

| Other Types |

| Independent Yards |

| OEM-Affiliated MROs |

| In-house Operator Facilities |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vessel Type | Boat | |

| Yacht | ||

| Commercial Vessels | ||

| Other Types | ||

| By Vessel Application | Private | |

| Commercial | ||

| Defense | ||

| By MRO Type | Engine MRO | |

| Component MRO | ||

| Dry-dock / Hull | ||

| Modifications and Retrofits | ||

| Other Types | ||

| By Service Provider Type | Independent Yards | |

| OEM-Affiliated MROs | ||

| In-house Operator Facilities | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What value will the boat and ship MRO market reach by 2031?

It is forecast to expand at a 7.73% CAGR by 2031 reaching market value USD 55.69 billion.

Which segment drives the highest share of boat and ship MRO spending currently?

Engine maintenance accounts for 45.56% of 2025 expenditure, reflecting the cost intensity of diesel overhauls.

Why are OEM-affiliated networks growing faster than independent yards?

Predictive-maintenance platforms and captive parts supply let OEMs bundle fixed-price, uptime-guaranteed contracts, attracting operators seeking budget certainty.

How will stricter IMO rules influence retrofit demand?

The EEXI, CII, and upcoming FuelEU Maritime regulations impose performance penalties and fines, prompting owners to install scrubbers, ballast-water systems, and dual-fuel engines during scheduled dockings.

Which region offers the strongest growth outlook for MRO providers?

Asia Pacific combines 36.73% current revenue share with a projected 7.83% CAGR, supported by Chinese yard consolidation and Indian coastal-shipping initiatives.

What is the principal capacity constraint in North American ship repair?

Naval programs occupy up to 70% of dry-dock slots, forcing commercial ships to schedule 12-18 months ahead or seek Mexican or Caribbean yards.

Page last updated on: