Yacht Charter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.8 Billion |

| Market Size (2031) | USD 12.69 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

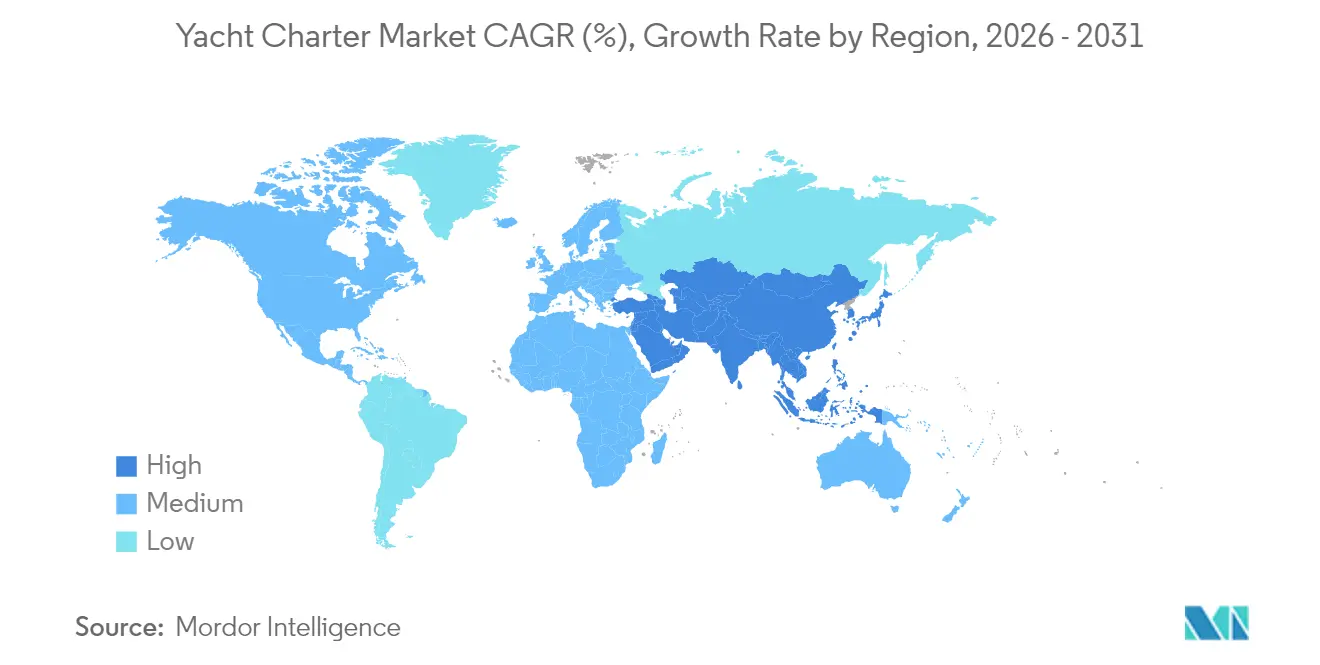

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Yacht Charter Market Analysis by Mordor Intelligence

The yacht charter market size is expected to grow from USD 9.30 billion in 2025 to USD 9.80 billion in 2026 and is forecast to reach USD 12.69 billion by 2031 at 5.32% CAGR over 2026-2031. Rising wealth in Asia and the Middle East, relaxed Mediterranean rules, and digital booking tools widen access and support growth. Motor yachts remain the revenue backbone, but greener sailing options and catamarans are winning newcomers. Short-duration and cabin charters open premium experiences to wider budgets, while corporate events push the ultra-large segment forward. Competition now pivots fleet sustainability, online reach, and the ability to tailor trips for diverse cultural and business needs.

Key Report Takeaways

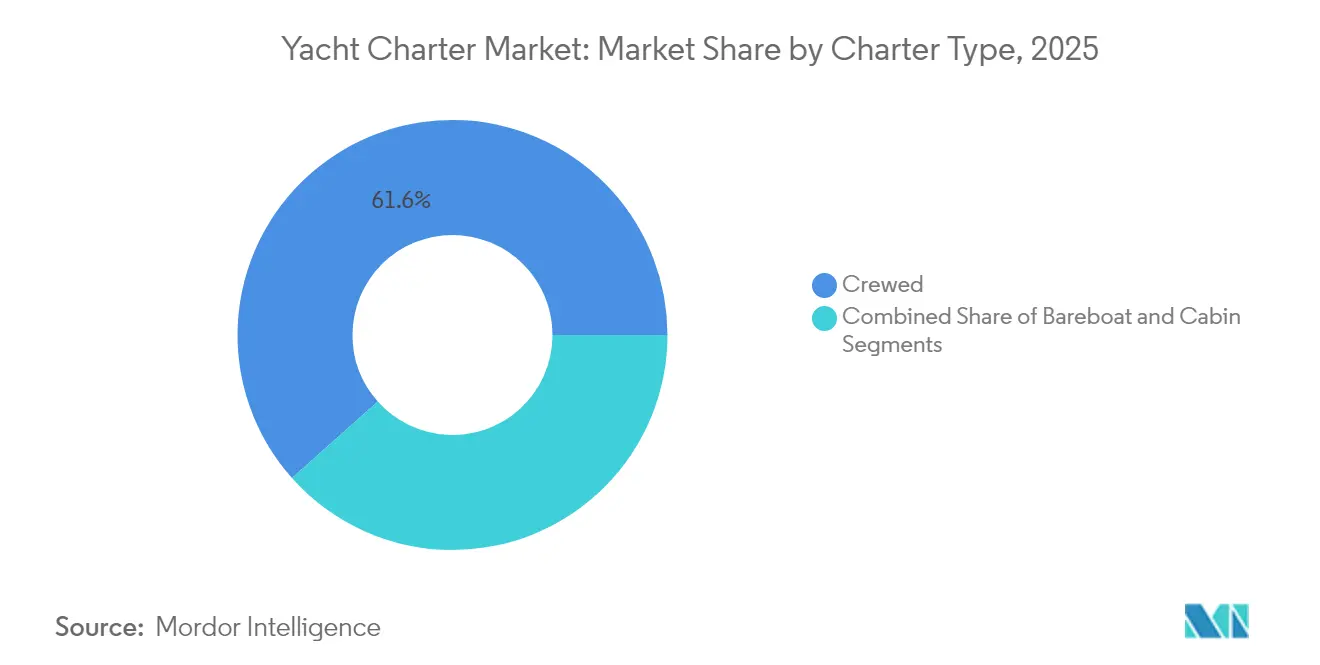

- By charter type, crewed charters led with 61.58% revenue share in 2025; cabin charters are projected to expand at a 9.31% CAGR to 2031.

- By yacht type, motor yachts held 57.52% of the yacht charter market share in 2025, while sailing yachts recorded the highest projected CAGR at 8.20% through 2031.

- By yacht size, the 24 to 40 m class accounted for 39.78% share of the yacht charter market size in 2025; yachts above 60 m are advancing at a 9.62% CAGR through 2031.

- By booking channel, broker-assisted bookings retained a 69.74% share in 2025, whereas online marketplaces are climbing at a 11.80% CAGR.

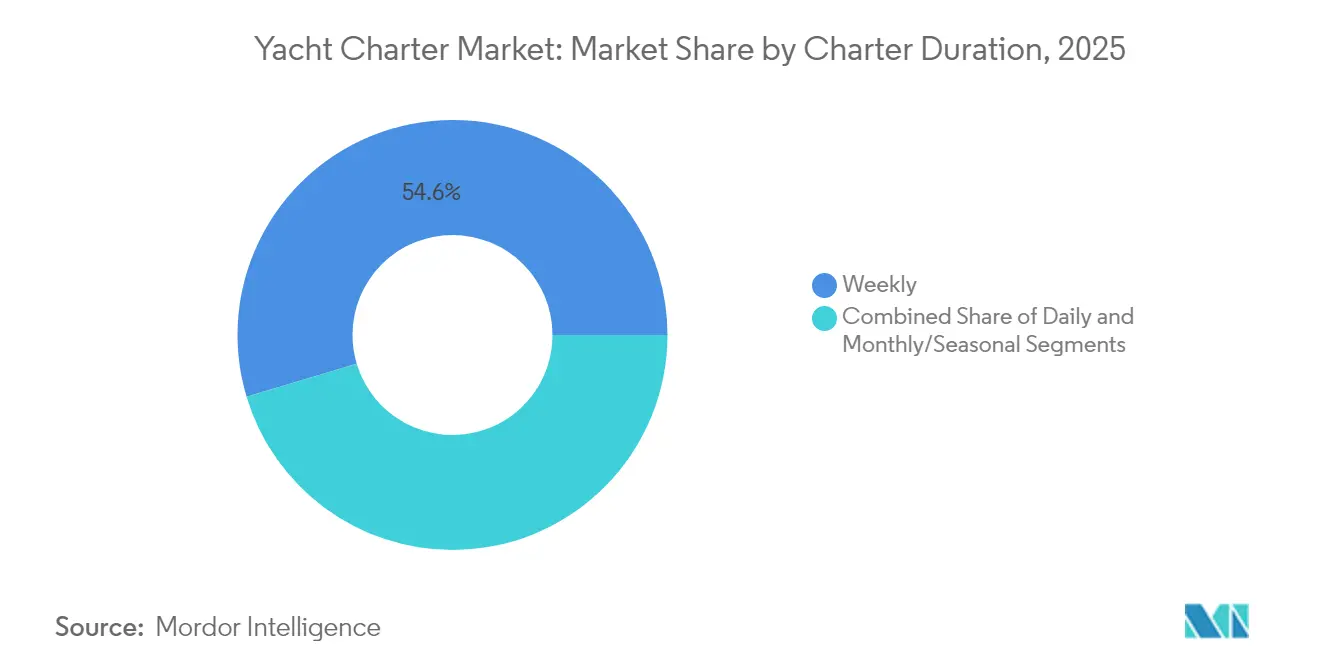

- By charter duration, weekly charters captured a 54.63% share in 2025; daily charters are set to rise at an 10.82% CAGR to 2031.

- By end-user, private and leisure trips formed 77.88% of 2025 revenue, yet corporate and MICE demand is forecast to grow at a 8.74% CAGR.

- By geography, Europe commanded 45.05% of global revenue in 2025, while Asia is on track for the fastest 8.35% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Yacht Charter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in UHNWIs in Asia and Middle East Catalyzing First-time Charters | +1.6% | Asia, Middle East, with spillover to Mediterranean | Medium term (2-4 years) |

| Expansion of Online Platforms Boosting Utilization in Europe | +1.2% | Europe, North America | Short term (≤ 2 years) |

| Experiential Tourism Demand Driving Catamaran Charters in the Caribbean | +0.9% | Caribbean, Mediterranean | Medium term (2-4 years) |

| Relaxed Mediterranean Charter Regulations Unlocking Capacity | +0.7% | Mediterranean, particularly Greece and Croatia | Short term (≤ 2 years) |

| Corporate Incentive Travel Adoption in North America | +0.5% | North America, with spillover to Caribbean | Medium term (2-4 years) |

| Eco-friendly Hybrid-Propulsion Yachts Attracting Scandinavian and Oceania Clientele | +0.4% | Scandinavia, Oceania, Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in UHNWIs in Asia and Middle East catalyzing First-time Charters

The expanding UHNWI population in Asia and the Middle East is fundamentally reshaping the yacht charter market, with approximately 44% of family offices looking to increase allocations to luxury assets, including yacht investments, in 2025. This wealth surge creates a new class of first-time charterers who view yachting as a status symbol and an exclusive retreat from increasingly dense urban centers. The trend is particularly pronounced in China, where the number of individuals with investable assets exceeding USD 30 million grew by 15% in 2024, creating ripple effects across the global charter market. Knight Frank's Wealth Report 2025 reveals that these new entrants are not merely passive consumers but actively influence yacht design and amenities, demanding culturally specific experiences that charter companies must adapt to. The impact extends beyond Asia's waters, with Mediterranean charter operators reporting a 22% increase in Asian clientele in 2024, driving innovation in service offerings and cultural accommodations aboard luxury vessels.[1]Liam Bailey, “The Wealth Report 2025,” Knight Frank, knightfrank.com.

Expansion of Online Platforms Boosting Utilization in Europe

Digital marketplace platforms are revolutionizing the European yacht charter landscape by dramatically reducing idle vessel time and expanding the customer base beyond traditional wealthy demographics. Click&Boat, Europe's leading yacht charter platform, has achieved a 28.13% traffic share, primarily from France and Italy, while emerging platforms like Boataround are gaining significant traction in Central Europe. These platforms have transformed the booking process, with users spending an average of 11 minutes per session exploring listings, resulting in a 30% increase in overall fleet utilization rates compared to traditional broker-only models. The democratization effect is particularly evident in Croatia, where PlainSailing.com reports that digital bookings have contributed to a 7% increase in UK-originated charters in 2024, with Lefkas in Greece emerging as a particularly popular destination due to its affordability and favorable sailing conditions. This digital transformation is not merely changing how yachts are booked but is fundamentally altering who books them, with millennials now representing 35% of all online yacht charter customers in Europe.

Experiential Tourism Demand Driving Catamaran Charters in the Caribbean

The Caribbean market is experiencing unprecedented growth as travelers increasingly prioritize immersive experiences over traditional luxury accommodations. This shift is evidenced by the rise of eco-sailing with hybrid or electric propulsion systems and customized itineraries that blend cultural immersion with natural exploration. The San Blas Islands have emerged as a premier destination, known for their untouched beauty and cultural richness, while the Exuma Cays are gaining popularity for their unique wildlife interactions and secluded settings. Catamaran Adventures reports that 80% of charter companies have noted increased demand for catamarans, which offer superior stability and space compared to monohull vessels.

Relaxed Mediterranean Charter Regulations Unlocking Capacity

Regulatory liberalization across Mediterranean countries has significantly expanded the yacht charter market capacity, most notably in Greece, where introducing the 'e-Charter Permission' system now enables non-EU-flagged yachts over 35 meters LOA to charter for up to 28 days annually. This regulatory shift replaces previous restrictions that required foreign-flagged yachts to be owned by companies with Greek branches, effectively opening the market to a broader range of international vessels. The impact is particularly significant for the superyacht segment, with the Greek government implementing a Special Charter Fee based on a yacht's duration in Greek waters rather than imposing blanket restrictions. Similar regulatory easing in Croatia has contributed to its emergence as a charter hotspot for 2025, with Nautilus Yachting highlighting the Dalmatian Coast as a prime booking area. These regulatory changes create a more unified Mediterranean charter environment, reduce operational complexities for fleet operators, and enable more efficient deployment of vessels across multiple jurisdictions, ultimately increasing overall market capacity and operational flexibility.[2]“Greece Opens Superyacht Charters,” Boat International, boatinternational.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Peak-season Crew Shortages Inflating Mediterranean Charter Costs | -0.8% | Mediterranean, particularly Greece, Croatia, and Italy | Short term (≤ 2 years) |

| IMO Tier III Compliance Refits Pressuring Margins | -0.6% | Global, with higher impact in Europe and North America | Medium term (2-4 years) |

| Limited Marina Berths on Caribbean Islands Constraining Fleet Growth | -0.4% | Caribbean, particularly British Virgin Islands and Bahamas | Long term (≥ 4 years) |

| High Discretionary-Spend Sensitivity in European Market | -0.3% | Europe, particularly Southern European countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Peak-season Crew Shortages Inflating Mediterranean Charter Costs

The Mediterranean yacht charter market is grappling with a critical crew shortage during peak seasons, driving operational costs up by 15-20% in 2024 and forcing operators to make difficult trade-offs between service quality and profitability. This shortage is particularly acute for specialized roles such as engineers and chefs, with some owners opting for minimum crewing standards to reduce costs despite the potential impact on service quality. Charter operators report that crew salaries have increased by up to 25% for the 2025 season as companies compete for qualified personnel, with these costs inevitably passed on to clients through higher charter rates. The shortage has strategic implications for fleet deployment, with some operators redirecting vessels to regions with more stable labor markets or investing in crew retention programs that include year-round employment guarantees and professional development opportunities to secure talent in an increasingly competitive labor market.[3]“Mediterranean Crew Salary Trends 2025,” Burgess, burgessyachts.com.

IMO Tier III Compliance Refits Pressuring Margins

The International Maritime Organization's Tier III nitrogen oxide (NOx) emission standards are creating significant financial pressure on yacht charter operators, with compliance refits costing between USD 200,000 and USD 500,000 per vessel, depending on size and existing systems. These regulations, which apply to vessels constructed after January 1, 2016, and operating in Emission Control Areas (ECAs), require a 75% reduction in NOx emissions compared to Tier II standards. Charter operators face a strategic dilemma: absorb these compliance costs, accept reduced margins, or pass them on to customers and risk losing price-sensitive segments. The impact is particularly severe for mid-sized operators with fleets of 5-15 vessels, who lack both the economies of scale of larger companies and the niche appeal of boutique operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Charter Type: Cabin Charters Democratize Luxury Access

Crewed Charters had a 61.58% of the yacht charter market share in 2025, due to a fully staffed service that appeals to newcomers and time-pressed travelers. Vessels in this class often assign one crew member per guest pair, reinforcing value through personalized care. While modest in revenue, Cabin charters are scaling quickly at a 9.31% CAGR, broadening the yacht charter market to middle-income groups who pay per cabin rather than per vessel. In Southeast Asia, cabin offers now represent one in five bookings, underscoring their role in market expansion.

Digital booking hubs report that 70% of 2025 cabin and crewed reservations came via online channels, indicating transparency and convenience outweigh the historical reliance on personal brokers. Bareboat charters, roughly 40-60% cheaper than crewed trips, remain the choice for licensed sailors and contribute steady off-season income in tradewind regions. Enhanced navigation software and remote support deepen bareboat safety, enlarging the qualified client pool. Operators combining flexible staffing, add-on chef packages, and easy online checkout stand to capture the next wave of demand in the yacht charter industry.

By Yacht Type: Sustainability Drives Sailing Resurgence

Motor yachts accounted for 57.52% of the 2025 revenue pool, favored for expansive saloons and faster repositioning between hotspots. Yet rising eco-awareness is steering an 8.20% CAGR for sailing yachts, especially on Mediterranean island loops where wind availability suits carbon-light cruising. Meanwhile, the yacht charter market size for catamarans has surged, as two-hull designs match the stability of generous deck plans prized by families.

Hybrid propulsion, once a niche, saw more than 300 yachts added to global fleets in 2024, meeting both regulatory obligations and tenant preference for quiet anchorage stays. Operators blending sail and hybrid tech market fuel-savings of 20-30%, resonating with budget-sensitive renters as fuel prices fluctuate. Choice is now less about pure speed and more about aligning trip ethos with traveler values. Motor-yacht builders answer by integrating solar arrays and battery banks, signaling that sustainability has moved from optional to baseline expectation within the yacht charter market.

By Yacht Size: Ultra-Large Segment Defies Economic Headwinds

Vessels between 24 m and 40 m commanded 39.78% of 2025 revenue, the sweet spot for 8-12 guests who want luxury without super-port fees. These yachts often combine gym space, beach clubs, and shallow drafts, suiting Mediterranean harbors and Caribbean anchorages. Despite higher running costs, yachts above 60 m are growing at a 9.62% CAGR as elite clients seek status events and unmatched privacy. The yacht charter market size for this bracket benefits from corporate retreats, brand launches, and influencer activations that justify premium rates.

Sub-24 m craft make up 65% of all contracts, vital for first-time renters testing the waters. Stabilizer upgrades and gyro systems lessen motion, lowering seasickness concerns and widening appeal. The 40 to 60 m range bridges volume and exclusivity; demand is steady among multi-family groups that prefer self-contained cinemas and spas, yet remain under prevailing berth limits in European marinas. Balanced fleet portfolios across size classes help operators hedge economic swings and capture cross-selling upsell paths in the yacht charter industry.

By Booking Channel: Digital Platforms Challenge Broker Dominance

Offline brokers still own 69.74% of 2025 bookings because they orchestrate bespoke routes and VIP concierge services. Their deep yacht knowledge and port relationships reassure high-spend clients. However, the online segment is scaling fastest at 11.80% CAGR, bringing transparent price filters, reviews, and instant contracts that appeal to tech-native audiences. Click&Boat leads Europe with 28.13% traffic share, while GetMyBoat tops in the United States at 14.01%.

Platforms use virtual walkthroughs and AI-matching to narrow selections efficiently, encouraging explorers to book shoulder-season slots and smaller vessels. Brokers strike back by integrating chatbots and photo-realistic 3D tours, creating a blended service path. The yacht charter market now rewards firms that can move seamlessly between channels, giving planners speedy information yet backing it with human expertise. Expect alliances where brokers white-label tech engines and platforms invest in destination specialists.

By Charter Duration: Daily Charters Expand Market Accessibility

Weekly charters dominate the yacht charter market with a 54.63% share in 2025, offering the optimal balance between operational efficiency for operators and immersive experiences for clients. This duration allows charterers to explore multiple destinations while providing operators with predictable scheduling and reduced turnover costs compared to shorter charters. However, daily charters are experiencing the strongest growth at 10.82% CAGR (2026-2031), driven by changing consumer preferences for shorter, more frequent leisure experiences rather than extended vacations. This shift is particularly evident in coastal urban markets where affluent professionals seek luxury experiences that fit within weekend timeframes.

While smaller in transaction volume, the monthly/seasonal charter segment represents a significant portion of market value due to the premium pricing these extended charters command. This segment is particularly strong in winter Caribbean and summer Mediterranean seasons, where wealthy clients seek extended escapes from unfavorable weather in their home regions.

By End-user: Corporate Segment Drives Innovation

The private and leisure segment dominates the yacht charter market with a 77.88% share in 2025, reflecting the industry's historical focus on vacation and lifestyle experiences. This segment's strength is particularly evident in traditional charter destinations like the Mediterranean and Caribbean, where personal leisure remains the primary motivation for chartering. Though smaller, the corporate and MICE (Meetings, Incentives, Conferences, and Exhibitions) segment is experiencing the fastest growth at 8.74% CAGR (2026-2031), driven by companies seeking distinctive venues for high-value client engagement and team-building activities.

The corporate segment's growth is reshaping yacht design and amenities, with newer vessels increasingly incorporating features specifically tailored to business functions, such as enhanced connectivity, multimedia capabilities, and configurable spaces that can transition between formal meetings and relaxed networking. This trend is particularly pronounced in Asia, where corporate usage for entertainment is driving a shift toward larger yachts ranging from 60ft to 130ft.

Geography Analysis

Europe retained a 45.05% share of global revenue in 2025, underpinned by dense marina networks and standardized charter rules. Greece’s new e-Charter Permission drew a wave of non-EU superyachts, while Croatia’s Dalmatian Coast captured price-sensitive bookings. Crew wage inflation of up to 25% and limited peak-season berths raise costs; online portals make secondary ports visible, smoothing demand over the entire year.

Asia is the fastest-rising market, predicted to expand at an 8.35% CAGR from 2026 to 2031. China’s pool of individuals with more than USD 30 million in liquid assets jumped 15% in 2024, and marinas in Hainan, Phuket, and Bali are scaling to meet larger hull drafts. Digital discovery replaces broker gatekeeping, helping first-time charterers arrange corporate sail-aways and family reunions. Regional governments offer tax breaks on new marinas, spurring private investment.

The Caribbean holds winter appeal as yachts migrate from Europe for dual-season revenue. Catamaran charters climbed 15% year-on-year in 2024 thanks to spacious designs suited to island hopping. Growth is capped by berth shortages in the British Virgin Islands and Bahamas, while tightened U.S. environmental rules, such as California’s Commercial Harbor Craft Regulation, raise compliance stakes for operators repositioning to Pacific ports. North America benefits from a strong domestic base and rising corporate incentives afloat, opening chances for themed charters that merge meetings with leisure.

Mordor Intelligence provides coverage of the yacht charter market across other key regional markets. Detailed country-level analysis extends to Saudi Arabia incorporating local coverage and market participation, as required.

Competitive Landscape

Market concentration is moderate. Dream Yacht Charter and The Moorings anchor the traditional fleet model, while Zizoo and GetMyBoat lead digital disruption. Sunsail and The Moorings secured an exclusive deal with Dufour to add 75 yachts over two seasons, reinforcing premium status. Reciprocal U.S. tariffs on EU yachts, announced in April 2025, may redirect procurement to domestic builders, tilting competitive balance.

Technology investment now decides speed to market. ViewYacht’s 2025 channel-manager rollout synchronizes inventory across platforms, cutting broker admin time. Virtual tours, AI price predictors, and personalized itineraries based on past feedback drive retention. Environmental credentials add a parallel contest; The Moorings’ OCEAN Promise with Blue Marine Foundation signals the shift from optional charity to core brand value.

White-space opportunities lie in Indonesia and the Philippines, where marinas are coming online and crews are plentiful. Health-and-wellness packages, from onboard nutritionists to mindfulness coaches, remain underexploited differentiators. Firms that can blend sustainable fleets, digital reach, and specialized experiences are best placed to enlarge their footprint in the yacht charter market.

Yacht Charter Industry Leaders

OceanBLUE Yachts Ltd.

Burgess

Simpson Marine

Northrop and Johnson

Dream Yacht Worldwide

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ViewYacht launched an enhanced Yacht Charter Channel Manager that synchronizes data across platforms, improving efficiency and reducing administrative burdens for charter brokers. This technological advancement enables brokers to focus more on client service and sales, potentially transforming business operations in the competitive yacht charter market.

- January 2024: The Greek government launched the 'e-Charter Permission' system, enabling non-EU-flagged yachts over 35 meters LOA to charter in Greece for up to 28 days annually. This regulatory change replaces previous restrictions requiring foreign-flagged yachts to be owned by companies with Greek branches, effectively expanding market capacity and creating new opportunities for international vessels.

- January 2024: The Moorings' 403PC won the European Powerboat of the Year award, enhancing the company's reputation for quality and innovation in the charter fleet market. This recognition strengthens The Moorings' position in the power catamaran segment, which is gaining popularity for its combination of space, stability, and ease of operation.

Global Yacht Charter Market Report Scope

Yacht charters are typically used for leisure, business, and vacation activities. A yacht charter offers a convenient and easy way to enjoy a long holiday with friends and family without owning a yacht. Yacht charter firms provide the yacht and deliver the best itinerary as per the requirements of the clients, with crew and captain and online or on-call support till total charter duration.

The yacht charter market is segmented by charter type, yacht type, and geography. By charter type, the market is segmented into the bareboat, cabin, and crewed. By yacht type, the market is segmented into sailing yacht, motorboat yacht, and other yacht types.

By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World.

| Bareboat |

| Cabin |

| Crewed |

| Sailing Yacht |

| Motor Yacht |

| Catamaran and Others |

| Less than 24 meters |

| 24 to 40 meters |

| 40 to 60 meters |

| More than 60 meters |

| Broker-Assisted Offline |

| Online Marketplace |

| Daily |

| Weekly |

| Monthly/Seasonal |

| Private and Leisure |

| Corporate and MICE |

| Government and Institutional |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Greece | |

| Croatia | |

| Rest of Europe | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Thailand | |

| Rest of Asia Pacific |

| By Charter Type | Bareboat | |

| Cabin | ||

| Crewed | ||

| By Yacht Type | Sailing Yacht | |

| Motor Yacht | ||

| Catamaran and Others | ||

| By Yacht Size | Less than 24 meters | |

| 24 to 40 meters | ||

| 40 to 60 meters | ||

| More than 60 meters | ||

| By Booking Channel | Broker-Assisted Offline | |

| Online Marketplace | ||

| By Charter Duration | Daily | |

| Weekly | ||

| Monthly/Seasonal | ||

| By End-user | Private and Leisure | |

| Corporate and MICE | ||

| Government and Institutional | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Greece | ||

| Croatia | ||

| Rest of Europe | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Thailand | ||

| Rest of Asia Pacific | ||

Key Questions Answered in the Report

What is the current Yacht Charter Market size?

The yacht charter market size is USD 9.80 billion in 2026.

How are online platforms impacting yacht charter bookings?

Online marketplaces are growing at a 11.80% CAGR, bringing transparent pricing and broader access while still coexisting with broker expertise.

Why are daily charters becoming popular?

Busy professionals favor short luxury escapes; daily charters, advancing at an 10.82% CAGR, cater to this time-sensitive demand.

Which yacht size segment holds the largest share

The 24 to 40 m category captures 39.78% of 2025 revenue, balancing luxury features with manageable operating costs.

Page last updated on: