Blood Glucose Test Strips Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.74 Billion |

| Market Size (2031) | USD 17.01 Billion |

| Growth Rate (2026 - 2031) | 5.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

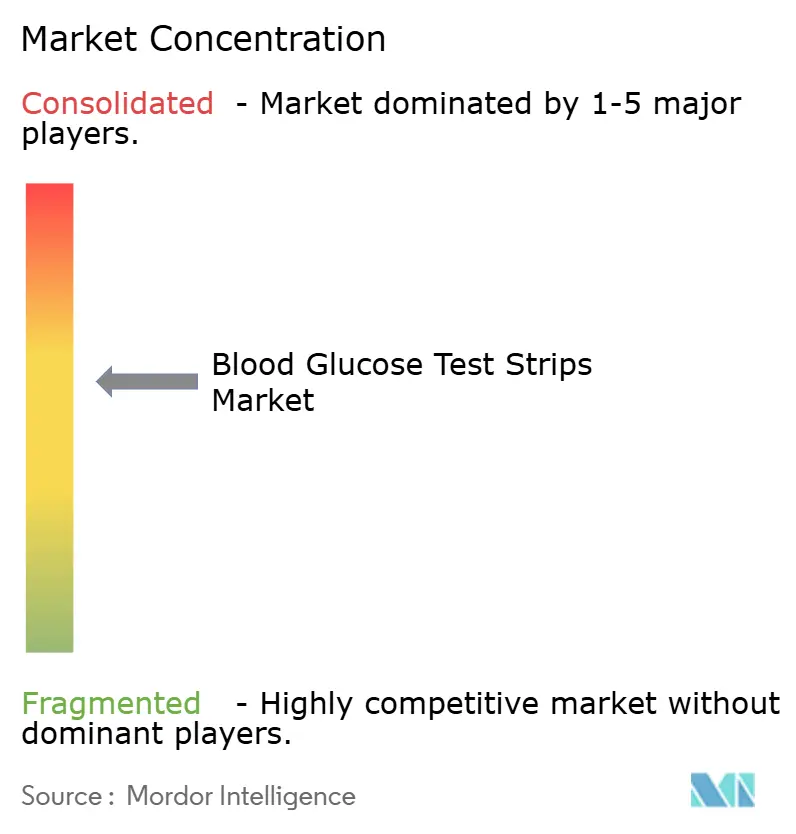

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Glucose Test Strips Market Analysis by Mordor Intelligence

The Blood Glucose Test Strips Market size was valued at USD 12.12 billion in 2025 and is estimated to grow from USD 12.74 billion in 2026 to reach USD 17.01 billion by 2031, at a CAGR of 5.96% during the forecast period (2026-2031).

The upward trajectory is supported by rising global diabetes prevalence, broader self-monitoring guidelines, and steady demand for strips among the vast population of Type 2 non-insulin-dependent individuals, even as continuous glucose monitoring (CGM) gains traction. Competitive bidding in the United States, India’s Production Linked Incentive subsidies, and China’s fast-tracked approvals are lowering manufacturing costs, which keeps retail prices within reach of price-sensitive patients. At the same time, Bluetooth-enabled meters that push real-time readings into telehealth platforms are transforming strips from stand-alone consumables into connected data endpoints. This shift unlocks Remote Patient Monitoring reimbursements. Counterbalancing these positives, CGM devices priced as low as USD 55 per two-week sensor are beginning to cannibalize strip volumes among Type 1 users and affluent Type 2 cohorts, moderating overall growth momentum.

Key Report Takeaways

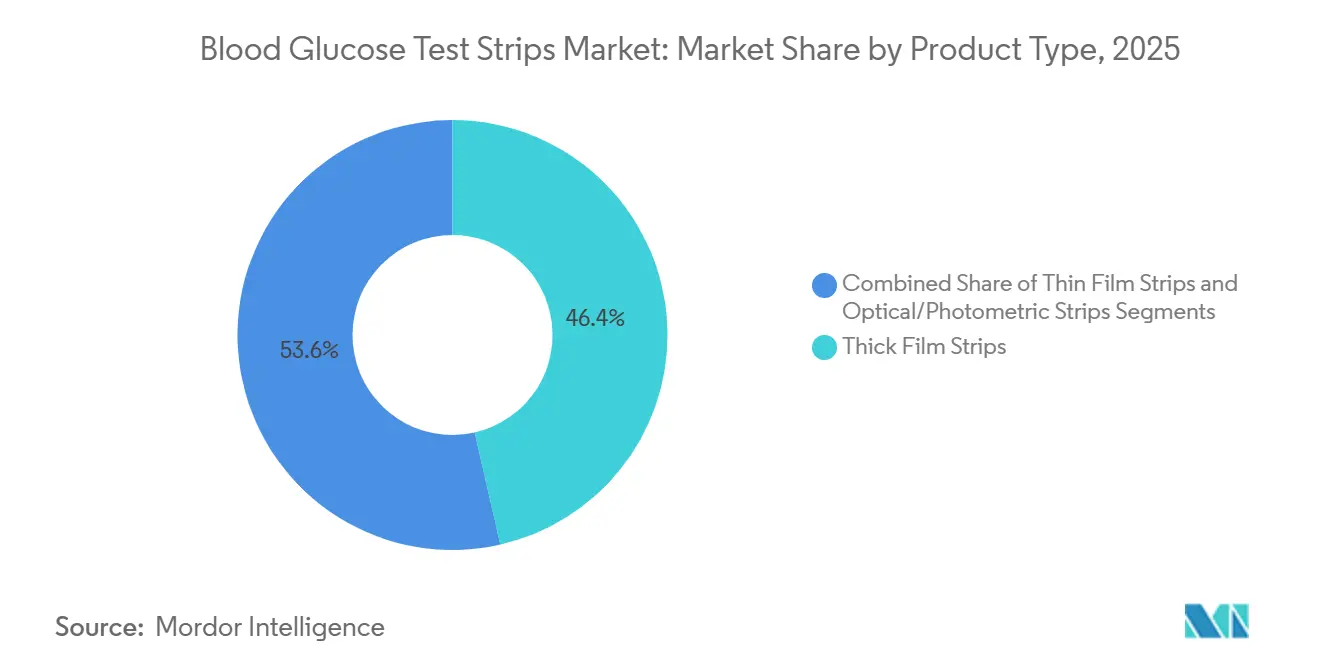

- By product type, thick film strips led with a 46.43% revenue share in 2025; optical/photometric formats are forecasted to deliver the fastest growth, at a 7.54% CAGR, through 2031.

- By diabetes type, Type 2 patients generated 67.54% of the blood glucose test strips market share in 2025, while gestational and other diabetes categories are expanding at 7.65% CAGR to 2031.

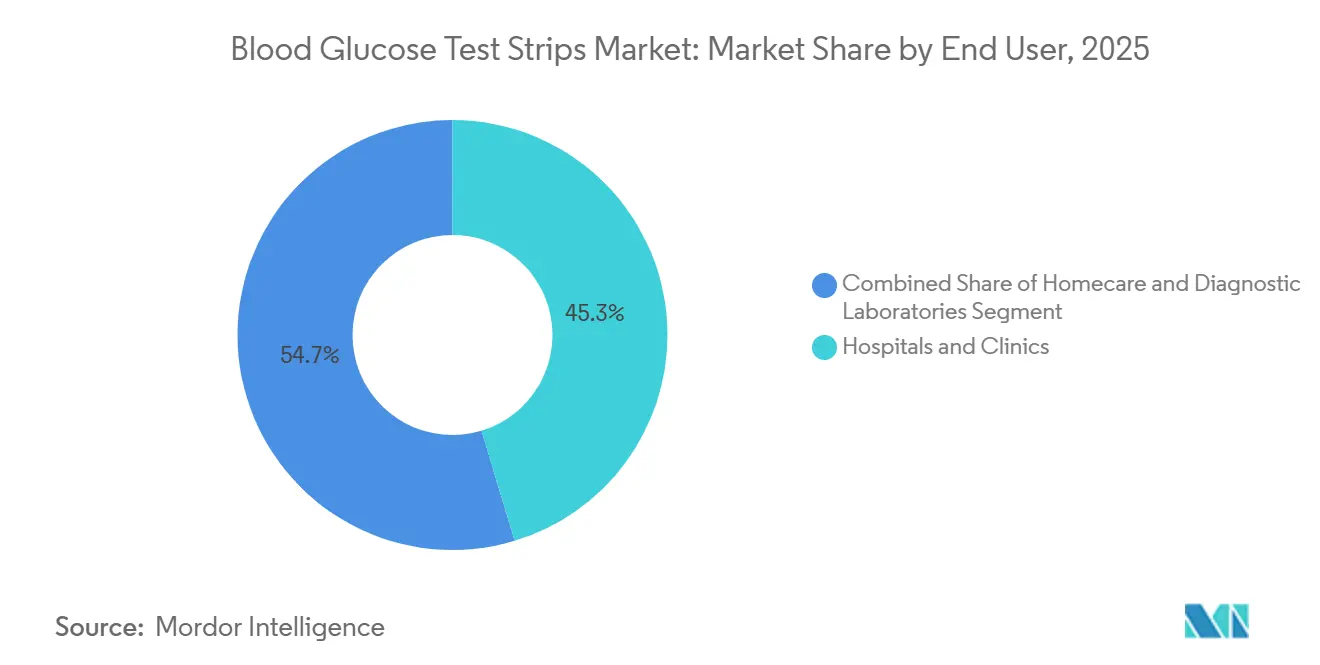

- By end user, hospitals and clinics held 45.32% of the blood glucose test strips market size in 2025, yet home care is rising at an 8.77% CAGR through 2031.

- By distribution channel, hospital pharmacies captured 55.76% of 2025 sales; online pharmacies represent the fastest 8.54% CAGR opportunity to 2031.

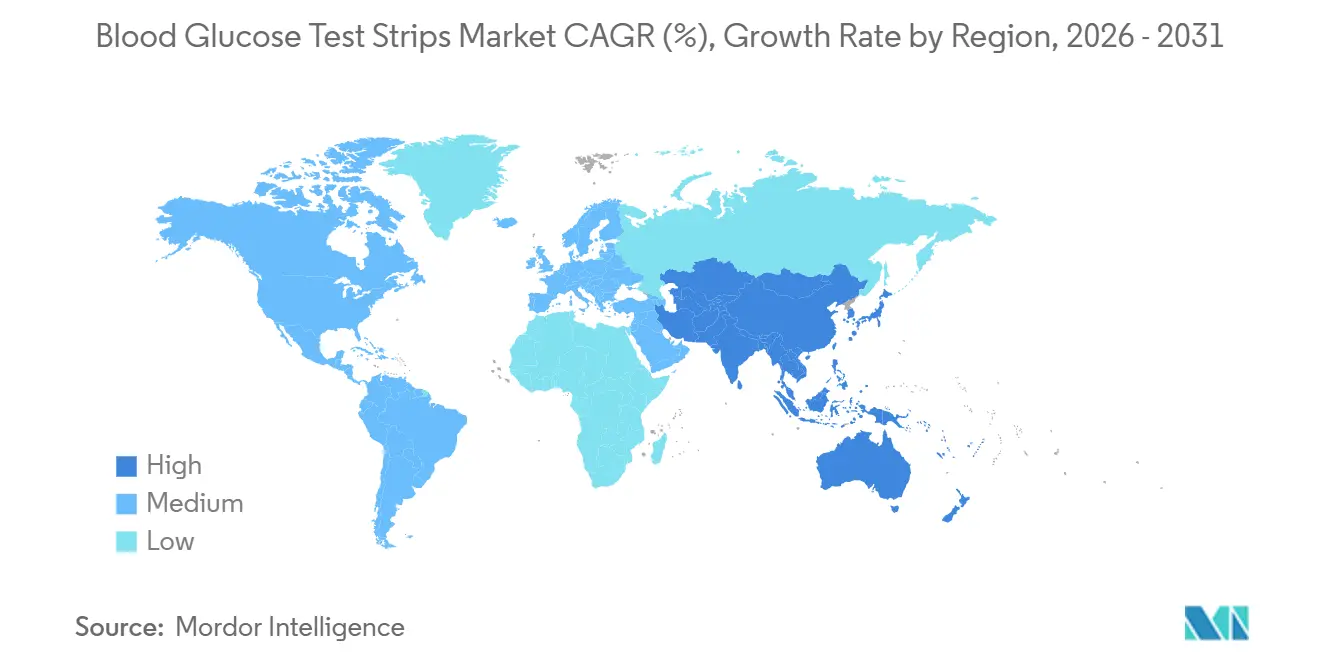

- By geography, North America accounted for 43.56% revenue in 2025; Asia-Pacific is set to register the highest 6.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Blood Glucose Test Strips Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global Diabetes Prevalence | +2.1% | Global, especially APAC & North America | Long term (≥ 4 years) |

| Emphasis On Self-Monitoring And Preventive Care | +1.4% | North America, Europe, urban APAC | Medium term (2-4 years) |

| Technological Enhancements In Enzymatic Strip Chemistry | +0.9% | Global, early adoption in North America & Europe | Medium term (2-4 years) |

| Integration Of Bluetooth-Enabled Smart Meters With Telehealth Platforms | +1.2% | North America, Western Europe, urban China | Short term (≤ 2 years) |

| Expanding Insurance Reimbursement For SMBG Consumables | +1.0% | United States, Canada, Western Europe | Short term (≤ 2 years) |

| Localization Of Strip Manufacturing Driven By Supply-Chain Incentives | +0.8% | India, China, Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Diabetes Prevalence

Global diabetes cases reached 588.7 million adults in 2024, and 251.7 million remain undiagnosed, underscoring a vast latent user base for test strips. China recorded 140.9 million patients in 2021 and is adding roughly 10 million seniors annually, a demographic that tests glucose frequently as comorbidities mount. India distributed 1.2 million glucometers through public primary care centers in 2024, each requiring 100–200 strips per year, resulting in 120–240 million incremental units[1]Ministry of Health and Family Welfare (India), “National Programme for Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases and Stroke,” mohfw.gov.in. The International Diabetes Federation foresees 852.5 million diabetics by 2050, with the sharpest acceleration in sub-Saharan Africa and Southeast Asia, regions where CGM remains cost-prohibitive. These rising numbers create structural demand that anchors the blood glucose test strips market even as technology evolves.

Emphasis on Self-Monitoring and Preventive Care

The American Diabetes Association’s 2026 Standards of Care newly recommend self-monitoring for non-insulin Type 2 patients experiencing glycemic variability, broadening the addressable patient pool by an estimated 30% (diabetes.org). Medicare’s 2024 pilot authorizes 100 strips every quarter for high-risk non-insulin users, potentially covering 2 million additional beneficiaries. Across Europe, primary-care physicians now conduct quarterly HbA1c testing, supplemented by at-home strip checks, which has increased per-patient strip use from 50 to 150 annually in the United Kingdom. Large U.S. employers, such as Johnson & Johnson, distribute free meters and 200 strips annually to employees with elevated fasting glucose, turning preventive screenings into recurring purchases. Collectively, these policies cultivate daily testing habits that sustain the blood glucose test strips market.

Technological Enhancements in Enzymatic Strip Chemistry

Manufacturers have reduced sample volumes from 1 µL to 0.3 µL, thereby reducing finger-stick pain and enhancing compliance[2]U.S. Food and Drug Administration, “Self-Monitoring Blood Glucose Test Systems for Over-the-Counter Use,” fda.gov. Roche secured a 2024 patent for a multilayer enzyme matrix that maintains accuracy within ±10% across a hematocrit range of 20%-70%, resolving longstanding interference issues. Abbott’s 2025 tropical-stability formulation stays accurate for 18 months at 40 °C, extending shelf life in hot climates. Ascensia and MIT explored graphene-coated electrodes that cut measurement time from 5 seconds to 2 seconds, an upgrade that could help strips compete on convenience, where CGM remains too expensive. These innovations enhance the user experience and keep the blood glucose test strips market relevant in the face of emerging sensor-based alternatives.

Integration of Bluetooth-Enabled Smart Meters with Telehealth Platforms

The Centers for Medicare & Medicaid Services began paying providers USD 50-65 monthly in 2024 for reviewing patient-transmitted glucose data, triggering a surge in meter upgrades. Roche’s Accu-Chek Connect facilitated over 1.2 million telehealth encounters in Germany in 2025 by streaming data into the mySugr app. LifeScan’s OneTouch Reveal integrates with Epic electronic health records, an alignment that lifted OneTouch strip sales 18% among Medicare Advantage plans in 2025. The FDA guidance clarified that a wireless module does not require a separate 510(k) if its accuracy remains intact, reducing the time-to-market from 18 months to 6 months and facilitating rapid rollouts. These connected-care workflows reinforce the relevance of strips by embedding them within reimbursable digital models of chronic disease management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption Of Continuous Glucose Monitoring Systems | -1.8% | North America, Western Europe, urban China | Medium term (2-4 years) |

| Price Sensitivity In Low-Income Regions | -0.7% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Enzymatic Raw Material Supply Bottlenecks | -0.4% | Global, acute in Europe & Japan | Short term (≤ 2 years) |

| Regulatory Push Toward Eco-Friendly Strip Disposal Standards | -0.3% | European Union, Canada, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Continuous Glucose Monitoring Systems

Abbott’s FreeStyle Libre Rio, cleared in July 2024 at USD 55 per 14-day sensor, brings CGM within price parity for heavy strip users who test 4 times or more daily. Dexcom’s G7 extends wear time to 15 days and costs USD 1,460 annually, now reimbursed by many Medicare Advantage plans without prior authorization. The ADA’s 2026 Standards recommend CGM for all intensive insulin regimens, accelerating the migration among the 1.6 million U.S. Type 1 patients who historically consumed up to 10 strips a day. Senseonics’ 365-day implantable sensor eliminates finger-stick calibration, offering a zero-strip alternative for affluent users willing to pay USD 3,500 upfront. As CGM pricing falls and coverage widens, strip volumes in high-income segments will continue to shrink, curbing overall growth in the blood glucose test strips market.

Price Sensitivity in Low-Income Regions

Strips cost USD 0.50–1.20 in sub-Saharan Africa, consuming 5-10% of daily wages and limiting testing to once a week rather than the recommended three to four times daily[3]World Health Organization, “Essential Medicines and Health Products,” who.int. India’s bulk tenders lowered public-sector prices to USD 0.15, yet private pharmacies still charge USD 0.40-0.60, prompting 70% of diabetics to ration strips. Brazil offers free strips to insulin users, but 42% of Type 2 patients test less than once weekly due to out-of-pocket costs averaging USD 0.60. While Chinese generics sell for below USD 0.10, a 2024 study found that 18% failed to meet accuracy thresholds, eroding trust and limiting their penetration. Sustained price pressure in low-income markets restricts testing frequency and tempers the global expansion of the blood glucose test strips market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electrochemical Dominance Faces Optical Disruption

Thick film formats accounted for 46.43% of the blood glucose test strips market in 2025, due to production costs of less than USD 0.08 and an accuracy of ±10%. Optical strips, however, are on track for a 7.54% CAGR through 2031 as colorimetric methods appeal to clinics without reliable electricity, particularly in sub-Saharan Africa and rural Asia. The blood glucose test strips market size for optical products is projected to widen as the World Health Organization’s 2024 Essential Diagnostics List prioritizes battery-free devices.

Electrochemical technology is evolving as well. Roche’s porous-carbon electrode wicks blood in under two seconds, marrying the costs of thick films with the speed of thin films. Abbott’s dual-enzyme system removes maltose interference for dialysis patients, and the FDA’s stricter ±10% guidance from 2024 will phase out sub-standard generics, channeling demand toward compliant brands. This competitive interplay keeps the blood glucose test strips market dynamic even as optical entries rise.

By Diabetes Type: Type 2 Volume Anchors Market Despite CGM Inroads

Type 2 diabetics generated 67.54% of strip consumption in 2025, illustrating that CGM remains economically unjustified for patients on oral drugs or lifestyle therapy. Gestational and other types of diabetes are growing at a 7.65% CAGR, driven by universal pregnancy screening that introduces three-strip checks per test episode, resulting in millions of additional annual uses in the United States and India.

The blood glucose test strips market share for Type 1 users is shrinking as CGM penetration hit 68% in 2025. Yet, the overall blood glucose test strips market size continues to rise because Type 2 comprises the vast majority of the global diabetic population. Public-health programs targeting undiagnosed adults further enlarge demand, counterbalancing CGM-led attrition in intensive-insulin cohorts.

By End User: Homecare Surge Reshapes Distribution Economics

Hospitals and clinics retained 45.32% of 2025 revenue as point-of-care testing guides acute insulin dosing. Homecare use, however, is advancing at 8.77% CAGR as chronic-care models emphasize daily self-testing, a shift that saves health systems an estimated USD 2,400 per patient yearly.

Home-based purchasing patterns commoditize strips, forcing producers to compete on price through online channels and subscription bundles. Automated strip-fed analyzers in diagnostic labs boost throughput but require sizeable capital, limiting adoption to high-volume centers. These mixed dynamics illustrate why the blood glucose test strips market remains split between institutional bulk buyers and increasingly cost-conscious consumers.

By Distribution Channel: Online Pharmacies Disrupt Traditional Retail

Hospital pharmacies captured 55.76% of the 2025 distribution due to formulary controls; however, their share is flattening as outpatient care migrates to ambulatory settings. Online pharmacies are growing at an 8.54% CAGR, driven by telehealth expansion and transparent price comparisons that resonate with self-pay users.

Direct-to-consumer shipping eliminates wholesaler and retail mark-ups, enabling 30-40% price cuts while preserving manufacturer margins. FDA rules issued in 2024 require online prescription verification, legitimizing large platforms and sidelining gray-market sellers. As Amazon Pharmacy and LifeScan subscription programs scale, they will further reshape the competitive landscape of the blood glucose test strips market.

Geography Analysis

North America accounted for 43.56% of the 2025 global revenue, primarily driven by Medicare Part B coverage, which guarantees demand for approximately 2.96 billion strips annually among insulin users. Competitive bidding trimmed reimbursement by 28% between 2021 and 2024, yet expanded eligibility to high-HbA1c non-insulin patients, preserving volume despite lower unit prices. Canada’s public formularies cap quantities - Ontario allows 3,000 strips yearly for Type 1 but only 400 for Type 2 - curbing upside despite high disease prevalence. U.S. FDA accuracy rules, effective in 2024, are expected to consolidate the market around Abbott, Roche, and Ascensia, pushing low-cost generics out of pharmacies.

Asia-Pacific is projected to post the fastest 6.64% CAGR through 2031 on the back of China’s 140.9 million and India’s 101 million patient bases. India’s Production Linked Incentive program subsidizes 5-7% of incremental sales, coaxing Sinocare and Bionime to build two billion-strip plants, which will lower public-sector per-unit costs and increase usage in rural clinics. China’s regulator cut approval times to nine months in 2024, enabling domestic firms to launch 12 new strip lines that undercut imports by up to 40%. Japan’s 12% reimbursement reduction in 2024 pressured margins, driving ARKRAY and Terumo to shift manufacturing to lower-cost Southeast Asian hubs.

Europe, the Middle East, and Africa, along with South America, collectively account for the remainder of global demand; however, fragmented reimbursement and price sensitivity restrain growth. German public insurers are forcing pharmacists to dispense the cheapest strip brand, thereby compressing Roche and Abbott’s combined market share from 68% to 54% by 2025. The United Kingdom now limits non-insulin users to two strips per day, but quarterly HbA1c tests, paired with at-home checks, help maintain baseline consumption. Brazil covers strips for insulin users but 42% of Type 2 patients test less than weekly due to USD 0.60 per-unit prices. Sub-Saharan African patients often forgo recommended testing frequencies as strips can cost up to 10% of daily wages, highlighting affordability as the primary ceiling on the blood glucose test strips market in low-income regions.

Competitive Landscape

The blood glucose test strips market is moderately concentrated, with Abbott, Roche, and Ascensia holding 52% of the global revenue in 2025. Abbott’s dual-portfolio approach keeps FreeStyle strips available for cost-conscious users, while FreeStyle Libre dominates CGM sales; however, internal cannibalization is inevitable as sensors replace finger sticks. Roche’s Accu-Chek Connect strategy embeds strip readings into reimbursable Remote Patient Monitoring workflows, defending share by aligning with telehealth economics. Patent filings reveal a chemistry arms race - Roche lodged 14 strip patents in 2024 centered on enzyme stability, while Abbott filed nine focused on sample-volume reduction and tropical shelf life.

White-space opportunities remain. Gestational diabetes adds 3.8 million U.S. screenings annually, yet no vendor offers a pregnancy-specific strip designed for hormonal interference patterns. The 251.7 million undiagnosed diabetics worldwide represent a greenfield market that requires pharmacy-based screening platforms, an area that smaller players, such as SD Biosensor and Sinocare, target aggressively through ultra-low-cost manufacturing.

Sinocare’s vertical integration across 18 plants yields a 30-40% cost advantage and helped it secure a 12% share in the Asia-Pacific market in 2025. The FDA’s ±10% accuracy mandate will phase out non-compliant generics, favoring companies with clinical-grade quality systems and deep R&D pipelines. However, local subsidies in India and China mean that domestic firms may still compete regionally on price.

Blood Glucose Test Strips Industry Leaders

Abbott Laboratories

F. Hoffmann-La Roche Ltd

LifeScan IP Holdings LLC

ARKRAY Inc.

Ascensia Diabetes Care Holdings AG.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Effective January 1, 2026, Independence Blue Cross Medicare Advantage plans will no longer cover OneTouch diabetic test strips at the preferred cost-sharing level. Accu-Chek and Contour will be the only preferred brands.

- October 2024: Trividia Health announced that its TRUE METRIX system and strips have achieved preferred status across all Managed Medicaid plans in Florida. This designation enhances access and affordability for patients using these diabetes management products. The move aims to improve diabetes care across the state.

- August 2024: Abbott Laboratories was awarded a USD 54 million victory in a legal case involving the diversion of glucose test strips. The case centered on allegations of misappropriation and distribution issues related to Abbott's medical products.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the blood glucose test-strips market as the sale of single-use electrochemical or optical strips that pair with handheld glucose meters for self-monitoring and professional point-of-care testing of capillary blood among people living with diabetes. Revenues include factory shipments as well as documented retail and institutional replenishment in more than forty nations that jointly account for over 95% of global diabetic prevalence.

Scope exclusion: disposable sensors for continuous glucose monitoring, lancets, and meter hardware fall outside this study's boundary.

Segmentation Overview

- By Product Type

- Thick Film Strips

- Thin Film Strips

- Optical / Photometric Strips

- By Diabetes Type

- Type 1 Diabetes

- Type 2 Diabetes

- Gestational and Others

- By End User

- Hospitals and Clinics

- Homecare / Personal Use

- Diagnostic Laboratories

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest Of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest Of Asia-Pacific

- Middle East And Africa

- GCC

- South Africa

- Rest Of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest Of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured discussions with endocrinologists, diabetes educators, procurement managers at retail chains, and operations directors of strip manufacturing plants across North America, Europe, and Asia Pacific. Insights on daily strip utilization, tender discounts, and the recent tilt toward pharmacy-managed subscription models helped validate secondary indicators and fine-tune forecast drivers.

Desk Research

Our analysts screened tier-1, open public datasets, such as International Diabetes Federation prevalence tables, WHO Global Health Observatory, US Centers for Medicare & Medicaid Services reimbursement files, Japanese PMDA device approvals, and Eurostat trade codes, to anchor patient pools, testing frequency norms, and cross-border shipment flows. Trade-association releases from Advanced Medical Technology Association, peer-reviewed articles in Diabetes Care, and customs records enriched benchmark volumes and price corridors. Proprietary look-ups on D&B Hoovers and Dow Jones Factiva supplied audited financials and channel commentary for leading strip producers. This list is illustrative; many additional sources were tapped for triangulation and clarity.

Market-Sizing & Forecasting

A top-down model begins with the diagnosed and treated diabetic population by country, multiplies average daily self-monitoring frequency, and layers reimbursement eligibility to derive annual strip demand, which is then cross-checked through selective bottom-up roll-ups of producer shipments and sampled ASP × volume audits. Key variables include new diabetes incidence, strip-per-patient ratios, inflation-adjusted retail ASPs, CGM substitution rates, tender penetration, and regional currency shifts. Multivariate regression combined with scenario analysis projects 2025-2030 values; outlier gaps are bridged with expert consensus where primary data run thin.

Data Validation & Update Cycle

Outputs undergo variance scans against external market indicators before a senior analyst signs off. Reports refresh yearly, with mid-cycle updates if material regulatory, pricing, or supply shocks emerge, ensuring clients receive the latest vetted outlook.

Why Mordor's Blood Glucose Test Strips Baseline Earns Trust

Published estimates often diverge because firms adopt unique product scopes, currency bases, and model refresh cadences.

Key gap drivers include the inclusion of CGM consumables within "strip" totals, exclusion of retail mark-ups, differing ASP erosion assumptions, and varied inflation conversions that others apply.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.02 B (2025) | Mordor Intelligence | - |

| USD 12.34 B (2025) | Regional Consultancy A | Counts pilot optical sensor strips and minor OTC ketone strips in scope |

| USD 20.53 B (2025) | Global Consultancy B | Pools meter hardware and home-use lancets alongside strips, inflating value |

| USD 8.61 B (2024) | Trade Journal C | Omits online and pharmacy retail sales, relies on constant 2021 USD without currency re-base |

The comparison shows that Mordor's disciplined boundary setting, annually refreshed inputs, and dual-path validation deliver a balanced baseline that decision-makers can replicate and defend with confidence.

Key Questions Answered in the Report

How large is the blood glucose test strips market in 2026?

The blood glucose test strips market size is USD 12.74 billion in 2026.

What is the expected CAGR for blood glucose test strips from 2026 to 2031?

The market is forecast to grow at a 5.96% CAGR to 2031.

Which product type leads global sales of blood glucose test strips?

Thick film electrochemical strips held 46.43% global revenue in 2025.

Which region is growing fastest for blood glucose test strips?

Asia-Pacific is projected to expand at a 6.64% CAGR through 2031.

How will CGM adoption affect blood glucose test strip demand?

CGM is reducing strip use among Type 1 and affluent Type 2 patients, but large untreated and non-insulin populations keep overall strip demand rising.

What share of the market do Abbott, Roche, and Ascensia hold?

The three companies collectively controlled 52% of global revenue in 2025.

Page last updated on: