Bleaching Clay Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

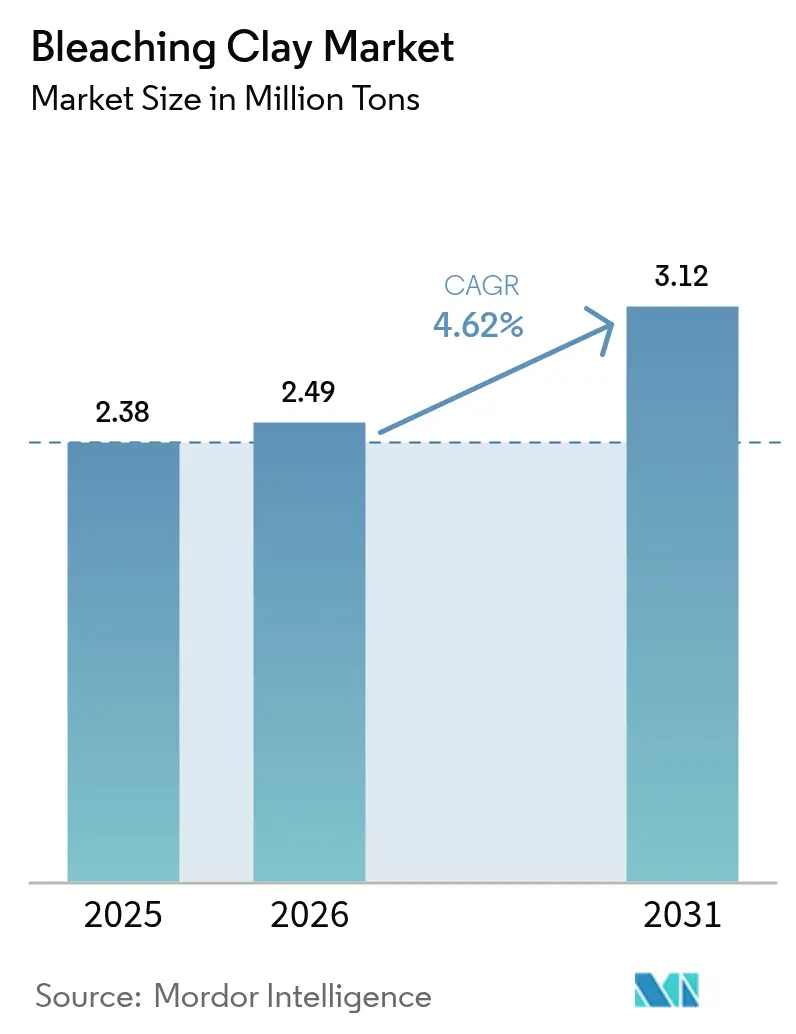

| Market Volume (2026) | 2.49 Million tons |

| Market Volume (2031) | 3.12 Million tons |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bleaching Clay Market Analysis by Mordor Intelligence

The Bleaching Clay market size is expected to grow from 2.38 Million tons in 2025 to 2.49 Million tons in 2026 and is forecast to reach 3.12 Million tons by 2031 at 4.62% CAGR over 2026-2031. This growth reflects steady expansion in refined vegetable oil production, rising adoption in biodiesel purification, and new uses in premium cosmetics. Fuller's Earth, notable for its low oil-loss rate, remains the dominant product type, while activated clays record the quickest uptake because refiners need higher adsorption capacity for specialty oils. Asia-Pacific leads the bleaching clay market with 47.29% volume share in 2024 as Chinese and Indian refineries scale capacity, yet North America and Europe steer high-margin niches such as pharmaceutical-grade oils and ultra-low-sulfur lubricants. Despite price pressure from bentonite cost swings, players offset margin risks through technical differentiation, recycling of spent bleaching earth, and selective price rises. Environmental regulation—especially EU rules classifying spent bleaching earth as hazardous waste—tightens operational requirements but fuels innovation in closed-loop processing where up to 85% biodiesel yield has been demonstrated from recovered oil.

Key Report Takeaways

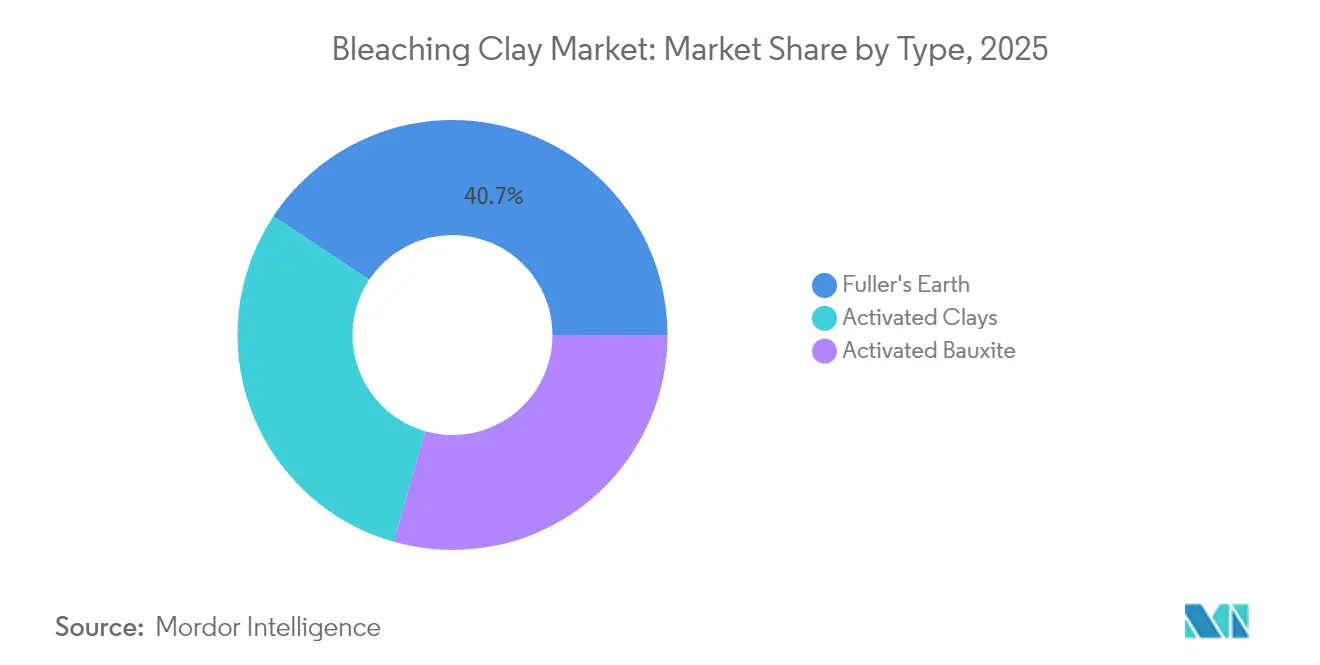

- By type, Fuller's Earth commanded 40.68% of bleaching clay market share in 2025, while activated clays posted the highest projected growth at 5.21% CAGR through 2031.

- By application, vegetable oil and animal fats accounted for 85.30% share of the bleaching clay market size in 2025 and is advancing at a 5.43% CAGR between 2026 and 2031.

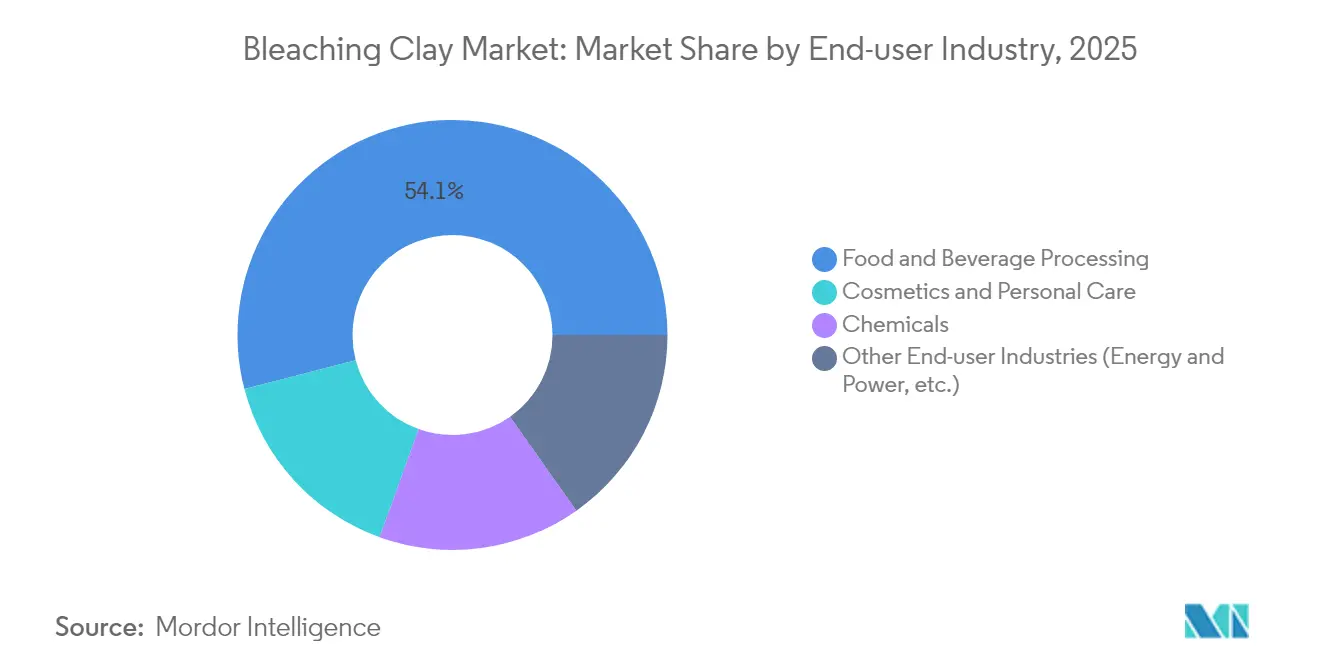

- By end-user, food and beverage processing held 54.05% share of the bleaching clay market size in 2025, while cosmetics and personal care is the fastest growing at 5.02% CAGR to 2031.

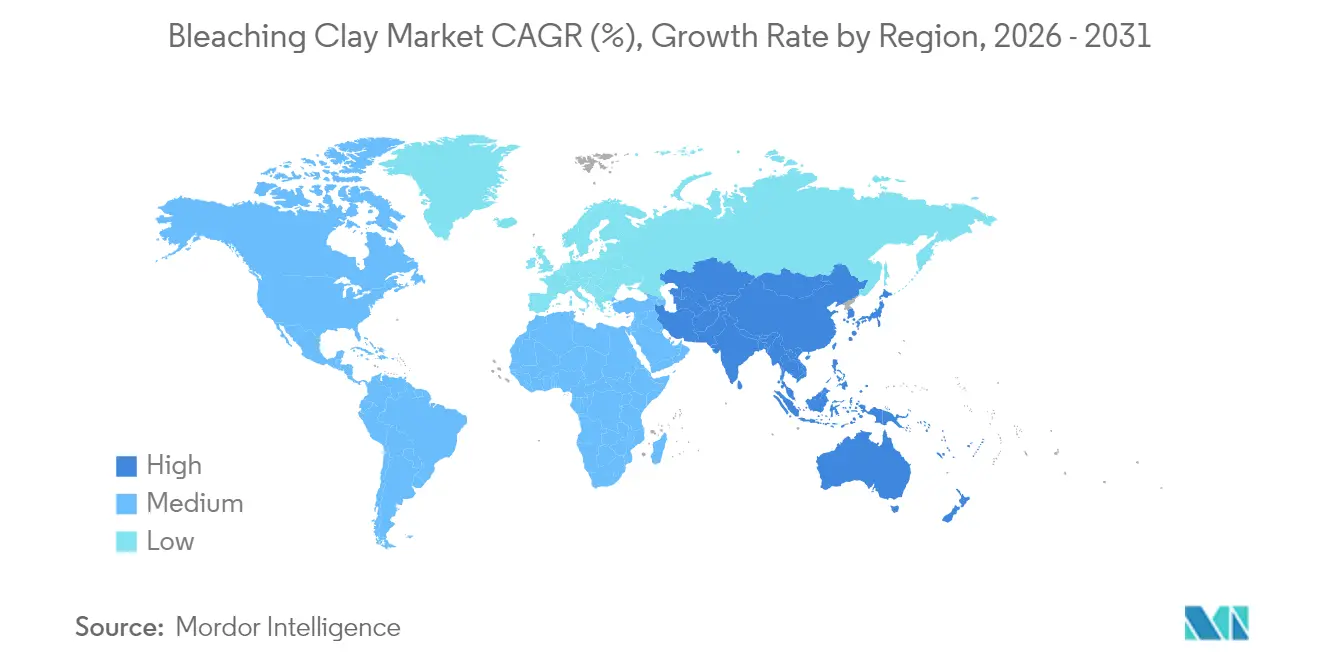

- By geography, Asia-Pacific contributed 47.10% volume share in 2025 and is growing at 4.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bleaching Clay Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Consumption of Refined Vegetable Oils | +1.2% | Global, with APAC leading growth | Medium term (2-4 years) |

| Rising Demand from Cosmetics and Personal Care Formulations | +0.9% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Growth Of Biodiesel and Renewable Diesel Refining | +0.8% | Global, with EU and North America leading | Medium term (2-4 years) |

| Increasing Need for Ultra-Low-Sulfur Mineral Oils and Lubricants | +0.7% | Global, driven by automotive regulations | Short term (≤ 2 years) |

| Pharmaceutical-Grade Cannabinoid Oil Purification Adoption | +0.6% | North America, expanding to EU | Long term (≥ 4 years) |

| Local Beneficiation of Bentonite Deposits In Africa | +0.5% | Africa, with spillover to global supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Consumption of Refined Vegetable Oils

Global oilseed output is set to touch 680 million tons in the 2024/25 season, lifting demand for specialized bleaching formulations that remove chlorophyll, carotenoids, and trace metals from solvent-extracted oils. Asia-Pacific refiners, supported by favorable logistics and expanding crushing capacity, represent the largest incremental volume. The segment also benefits from dietary shifts toward soybean and sunflower oil, both of which require higher clay dosage rates than cold-pressed alternatives. Producers that can tailor pore structure for specific oil chemistries capture procurement preference, especially as OPEC projects 19.2 million barrels per day of new refining capacity in developing regions by 2050[1]Organisation of the Petroleum Exporting Countries, “World Oil Outlook 2045,” opec.org. This structural uplift secures long-run volume visibility for the bleaching clay market.

Rising Demand from Cosmetics and Personal Care Formulations

Cosmetic brands increasingly replace synthetic absorbents with naturally derived clays to meet clean-label expectations and regulatory pressure over microplastics. High surface area and cation exchange capacity allow bleaching clays to act both as oil absorbers and as stabilizers for ultraviolet filters, encouraging wider use in sun-care and matte-finish products. Clariant’s acquisition of Lucas Meyer Cosmetics strengthens value-added supply for this high-margin end-use, evidenced by the firm’s Care Chemicals profitability increase in 2024. Premium formulations demand low-heavy-metal content clays, which supports price differentiation and compensates for the smaller tonnage relative to edible oils.

Growth of Biodiesel and Renewable Diesel Refining

Mandatory blending targets in the EU, United States, and parts of Asia raise feedstock purification needs. Specialty grades such as TONSIL™ remove phosphorus and metals that shorten catalyst life during transesterification, directly impacting plant economics. Research confirms that spent bleaching earth can itself convert to biodiesel with up to 85% yield through in-situ esterification, creating a secondary revenue stream and reducing disposal liabilities. This dual benefit reinforces the bleaching clay market as a circular-economy enabler.

Increasing Need for Ultra-Low-Sulfur Mineral Oils and Lubricants

Tighter automotive and industrial emission norms compel lubricant formulators to cut sulfur and trace metal content to parts-per-million levels. Activated bentonite grades provide efficient adsorption without impairing viscosity index modifiers, making them essential for multigrade hydraulic fluids and synthetic base stocks. The technical barrier to replicate such performance protects incumbents and supports premium pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict Environmental Regulations on Mining and Acid Activation Waste | -0.4% | Global, with EU leading regulatory stringency | Short term (≤ 2 years) |

| Competition from Synthetic Adsorbents (Silica Gels) | -0.3% | North America and EU, expanding globally | Medium term (2-4 years) |

| Volatile Bentonite Prices Due to Supply Concentration | -0.2% | Global, with regional supply chain impacts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strict Environmental Regulations on Mining and Acid Activation Waste

EPA discharge revisions and EU hazardous waste designation for spent bleaching earth add USD 50–100 per ton to processing costs, prompting facilities to invest in zero-liquid-discharge systems[2]United States Environmental Protection Agency, “Effluent Guidelines for Mineral Mining and Processing,” epa.gov[. Smaller operators struggle to finance such upgrades, leading to capacity rationalization and potential consolidation. Conversely, the push for sustainability accelerates R&D into solvent extraction and pyrolysis routes that recover up to 35% oil from certain clay types, cutting waste volumes and generating secondary products.

Competition from Synthetic Adsorbents (Silica Gels)

Engineered silica offers narrow pore-size distribution and consistent batch quality attractive to pharmaceutical and specialty chemical processors. As clay processors shoulder higher compliance costs, the price gap narrows, increasing substitution risk in high-purity applications. To defend share, leading suppliers develop hybrid systems that anchor silica nanoparticles inside clay matrices, delivering performance parity while retaining a natural product narrative that resonates with brand owners focused on sustainability..

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fuller's Earth Dominates Through Superior Oil Retention

Fuller's Earth captured 40.68% of bleaching clay market share in 2025 by delivering 15-20% lower oil loss than attapulgite or sepiolite alternatives, a saving that can reach USD 3 million annually for a refinery processing 1 million tons of soybean oil. The segment benefits from abundant global deposits and simple activation requirements, supporting cost leadership. Activated clays, however, are forecast to outpace Fuller's Earth at 5.21% CAGR as producers refine acid activation to raise surface area beyond 250 m²/g, unlocking higher adsorption capacity essential for pharmaceutical and cosmetic oils. Over the forecast period, refiners will balance unit cost with performance, keeping both segments relevant to the bleaching clay market.

Activated bauxite serves a focused subset of petroleum applications where processing temperatures exceed 200 °C. Although supply is limited, its stable lattice earns preference in transformer oil and aviation lubricant purification. Continued R&D shows that optimal bleaching capacity lies in a 50–60 Å average pore radius, encouraging investments in controlled activation technology that narrows performance variance. These advances underpin enduring, if modest, contribution from niche grades to the bleaching clay market size.

By Application: Vegetable Oil Processing Drives Market Leadership

Vegetable oil and animal fats retained an 85.30% share of the bleaching clay market size in 2025 while registering a 5.43% CAGR outlook, underscoring the critical role in global nutrition and biofuel supply chains. Solvent-extracted soybean, palm, and sunflower oils need higher clay dosage than expeller-pressed alternatives, and expanding biodiesel mandates will lift demand further. Industrial oil users, notably metalworking fluids, rely on clays for stabilizing additive packages and extending fluid life, adding incremental volume though at lower tonnage.

Mineral oils and waxes require formulations tuned for hydrocarbon matrices. Blending of renewable diesel with fossil feedstock has created hybrid streams demanding versatile adsorbents that cope with divergent polarity. Spent bleaching earth from vegetable oils is increasingly valorized as feedstock for in-situ biodiesel production at 85% conversion efficiency, aligning purification with circular-economy objectives and adding downstream value for processors.

By End-user Industry: Food Processing Leads While Cosmetics Accelerates

Food and beverage processing held 54.05% share in 2025 because edible oil safety regulations enforce strict limits on chlorophyll, peroxide value, and trace metals. Compliance requires certified food-grade clays free of aflatoxins and heavy metals, supporting premium positioning for top suppliers. Cosmetics and personal care, though smaller in tonnage, is gaining at 5.02% CAGR as brands adopt natural multifunctional ingredients. Clay’s dual role as adsorbent and active skin-care component allows formulators to reduce ingredient lists, dovetailing with minimalist product trends.

The chemicals segment spans catalyst supports, pigment carriers, and specialized adsorbents for petrochemical streams. Rising demand for low-aromatic transformer oils and biobased hydraulic fluids creates cross-selling potential. Other industries, including energy storage and wastewater treatment, experiment with modified clays for ion removal and thermal insulation, hinting at diversified growth avenues for the bleaching clay market.

Geography Analysis

Asia-Pacific’s 47.10% volume share in 2025 stems from vast refining footprints in China, India, Indonesia, and Malaysia, each benefitting from proximity to oilseed production and large consumer markets. The region’s 4.95% CAGR forecast links to OPEC-projected incremental refining capacity of up to 4.9 million barrels per day by 2028. Indonesia alone uses roughly 200,000 tons of bentonite annually in cooking-oil refining, illustrating the scale advantage that supports dedicated clay activation facilities. Local universities collaborate with industry on spent earth recycling methods achieving 85% biodiesel yield, reinforcing supply security and environmental compliance.

North America combines technological leadership with regulatory discipline. Refiners use low-metal clays to protect hydrotreating catalysts in renewable diesel, and lubricant blenders demand grades delivering parts-per-billion sulfur removal. Oil-Dri’s price adjustment of 5–8% in late 2024 shows the region’s ability to pass on cost inflation amid persistent demand. Europe’s stringent waste regulation raises compliance costs yet accelerates investment in closed-loop processing. Recycling techniques that recover 35% oil from sepiolite illustrate the region’s innovation pace. High-precision German and Swiss cosmetic manufacturers source ultra-pure clays under pharmacopeia specifications, adding premium tonnage.

South America benefits from Brazil’s dominance in soybean cultivation, offering synergies between crushing capacity and local clay demand. Middle-East and Africa present emerging potentials, especially where governments push for downstream mineral processing. South Africa’s mining contribution of 8.3% GDP and Nigeria’s sector modernization foster local beneficiation that can reduce import reliance. These developments diversify the bleaching clay market supply chain and add resilience against regional disruptions.

Competitive Landscape

The bleaching clay market remains moderately fragmented. Clariant, Oil-Dri, and Minerals Technologies together hold about 28% global volume, leveraging mine-to-market integration, technical service networks, and proprietary activation processes. Clariant reported a 16.4% EBITDA margin in Q4 2024 thanks to strong Care Chemicals demand, illustrating resilience in specialty niches. Oil-Dri’s November 2024 price increase reflected feedstock inflation but also confidence in product differentiation. Minerals Technologies posted record Q1 2024 earnings driven by Consumer and Specialties, confirming that premium positioning yields margin uplift.

Regional specialists, such as Taiko Clay in Malaysia and Refoil Earth in India, defend share through localized logistics and quick product customization. African entrants aim to undercut landed cost for APAC customers by processing bentonite near the mine mouth. Competitive tactics include hybrid product development, where natural clay carriers host engineered silica, and investment in spent earth recycling plants that convert waste to sellable biodiesel.

Threats arise from synthetic adsorbent innovators offering tighter performance tolerances attractive to pharmaceutical users. In response, incumbents highlight the lower carbon footprint of natural clays and publish lifecycle assessment data to satisfy customer ESG audits. Long-term supply agreements with vegetable-oil majors provide volume stability, allowing continuous R&D funding despite commodity price swings.

Bleaching Clay Industry Leaders

Clariant AG

Taiko Clay Marketing

Oil-Dri Corporation of America

Ashapura Group

U.S. Silica

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Clariant introduced Geko™ clay, a specialized molding material for the foundry industry, at Metal China 2024. The bleaching clay addresses sustainability requirements and customer demands in the foundry market.

- November 2022: Shell acquired EcoOils, a Malaysian bleaching clay recycling company. The acquisition encompassed 100% ownership of EcoOils' Malaysian subsidiaries and 90% of its Indonesian subsidiary. EcoOils extracts oil from spent bleaching clay which is used to remove impurities during vegetable oil refining.

Global Bleaching Clay Market Report Scope

Bleaching clays are absorbent clay that is used to remove coloring matters from liquids such as oils. The bleaching clays market is segmented by type, application, end-user industry, and geography. By type, the market is segmented into Activated Bauxite, Activated Clays, and Fuller's Earth. By application, the market is segmented into Industrial Oil, Mineral Oil and Waxes, and Vegetable Oil and Animal Fats. By end-user industry, the market is segmented into Food and Beverage, Cosmetics and Personal Care, Chemicals, and Other End-user Industries. The report also offers market size and forecasts for 15 countries across major regions. For all the above segments, market sizing and forecasts have been done on the basis of revenue (USD million).

| Activated Clays |

| Fuller's Earth |

| Activated Bauxite |

| Mineral Oil and Waxes |

| Industrial Oil |

| Vegetable Oil and Animal Fats |

| Food and Beverage Processing |

| Cosmetics and Personal Care |

| Chemicals |

| Other End-user Industries (Energy and Power, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Activated Clays | |

| Fuller's Earth | ||

| Activated Bauxite | ||

| By Application | Mineral Oil and Waxes | |

| Industrial Oil | ||

| Vegetable Oil and Animal Fats | ||

| By End-user Industry | Food and Beverage Processing | |

| Cosmetics and Personal Care | ||

| Chemicals | ||

| Other End-user Industries (Energy and Power, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current bleaching clay market size and how fast is it growing?

The bleaching clay market size reached 2.49 million tons in 2026 and is projected to rise at a 4.62% CAGR to 3.12 million tons by 2031.

Which region leads the bleaching clay market?

Asia-Pacific holds the leading 47.10% market share thanks to extensive vegetable-oil refining capacity and expanding biodiesel programs.

Why does Fuller's Earth dominate among product types?

Fuller’s Earth offers 15–20% lower oil retention loss than alternative clays, resulting in significant cost savings for edible-oil refineries.

How are environmental regulations shaping the bleaching clay industry?

EU hazardous-waste rules and tighter EPA discharge standards raise compliance costs but stimulate innovations such as spent-earth biodiesel recovery that improve sustainability.

Which end-use sector is growing fastest?

Cosmetics and personal care is expanding at 5.02% CAGR as brands favor natural multifunctional clays for oil control and UV-filter stabilization.

Page last updated on: