Activated Bleaching Earth Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

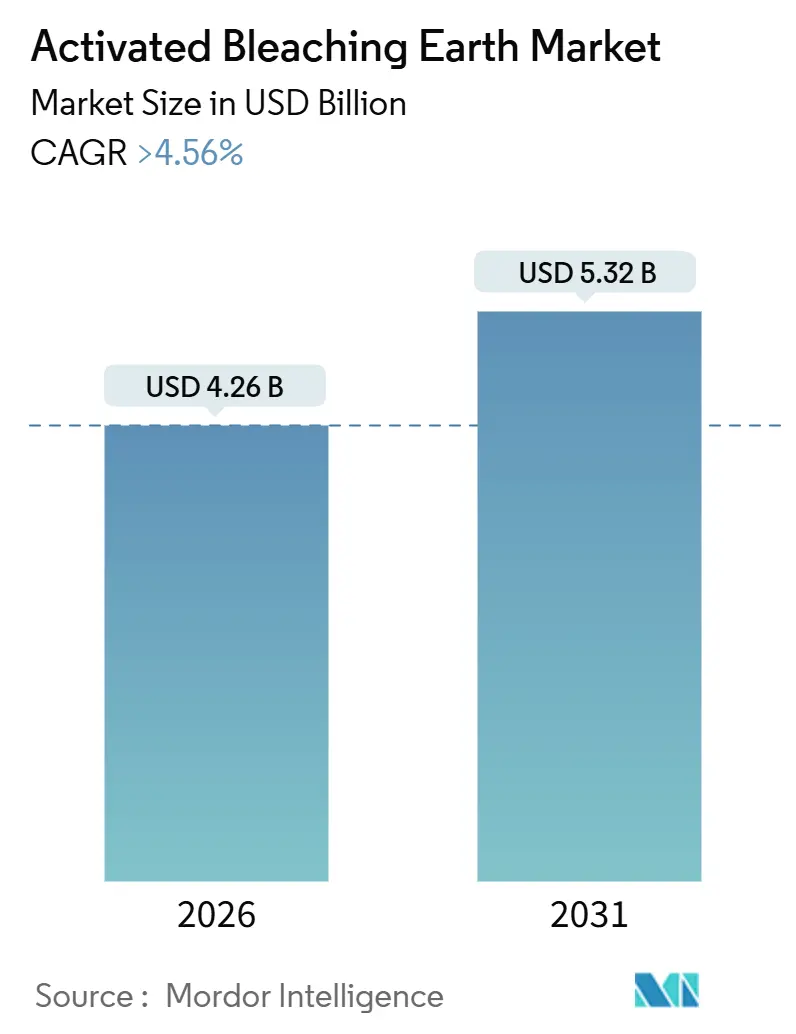

| Market Size (2026) | USD 4.26 Billion |

| Market Size (2031) | USD 5.32 Billion |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

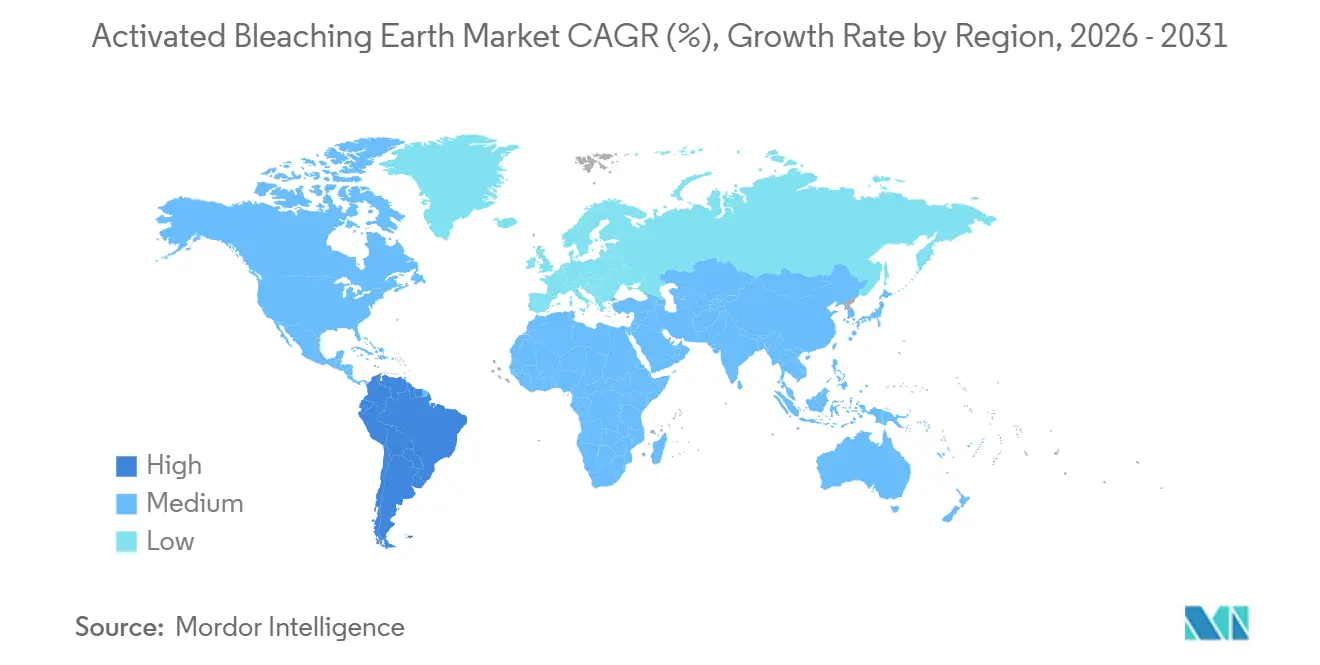

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Activated Bleaching Earth Market Analysis by Mordor Intelligence

The Activated Bleaching Earth Market size is estimated at USD 4.26 billion in 2026, and is expected to reach USD 5.32 billion by 2031, at a CAGR of greater than 4.56% during the forecast period (2026-2031). This steady expansion reflects the maturation of major edible-oil refining hubs and the incremental pull from biodiesel and mineral-oil polishing applications. Cost sensitivity in palm-oil corridors, tightening 3-MCPD rules in Europe, and dosage-reduction technologies are tempering per-tonne clay volumes even as refining throughput rises[1]USDA Foreign Agricultural Service, “Oilseeds and Products Annual, Indonesia,” usda.gov . In parallel, South America’s B15 mandates, growing synthetic-lubricant output in East Asia, and value-added oxalic-acid activation routes are opening new performance-driven niches. Suppliers with captive bentonite mines and low-dosage formulations are better positioned against feedstock volatility and alternative adsorbents. Overall, the Activated Bleaching Earth market is moving from pure volume play to a value-plus-compliance model built on vertical integration, technical service, and circular-economy alignment.

Key Report Takeaways

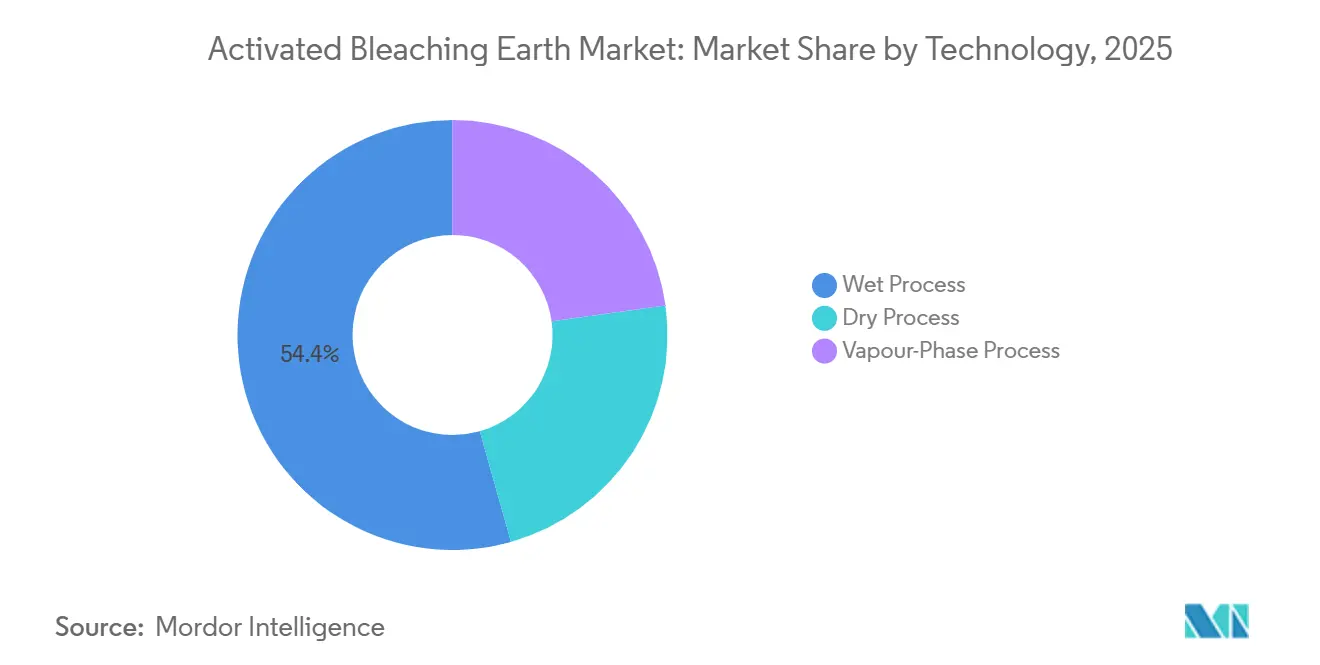

- By technology, Wet Process led with 54.38% revenue share in 2025 while Vapour-Phase Process is forecast to expand at a 5.12% CAGR through 2031.

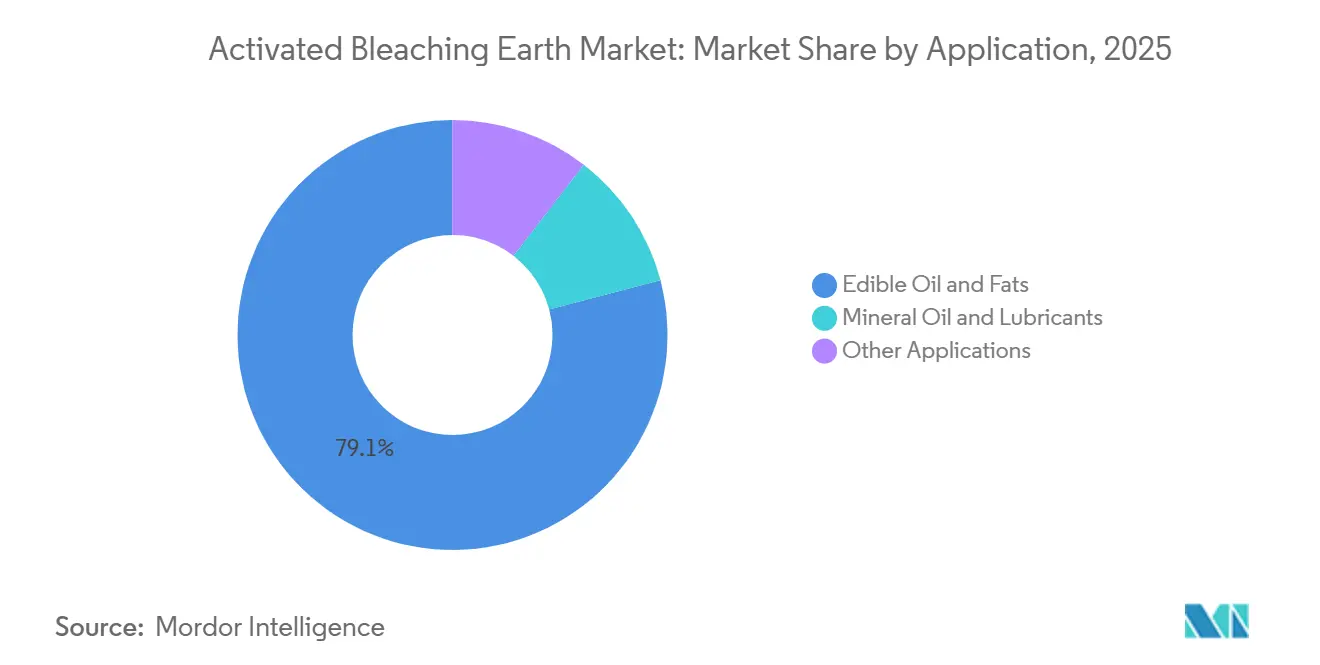

- By application, edible oil and fats accounted for 79.10% of the Activated Bleaching Earth market size in 2025 and mineral oil and lubricants are advancing at a 5.33% CAGR through 2031.

- By geography, Asia-Pacific commanded 60.12% revenue share of the Activated Bleaching Earth market in 2025 whereas South America is set to post the highest regional CAGR of 4.96% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Activated Bleaching Earth Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumption of Refined Edible Oils and Fats | +1.8% | Global, APAC core (China, India, ASEAN) | Long term (≥ 4 years) |

| Expansion of Biodiesel and Renewable Diesel Production | +1.2% | South America (Brazil, Argentina), ASEAN (Indonesia), Europe | Medium term (2-4 years) |

| Growth in Mineral Oil and Lubricant Quality Demands | +0.7% | North America, Europe, Asia-Pacific (Japan, South Korea) | Medium term (2-4 years) |

| Industrialisation Surge Across Asia-Pacific | +0.6% | APAC (India, Vietnam, Thailand, Bangladesh) | Long term (≥ 4 years) |

| Adoption of Ultrasound-Assisted Low-Dosage Bleaching | +0.3% | Global, early adopters in Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Consumption of Refined Edible Oils and Fats

Global vegetable-oil throughput keeps rising, pushed by population growth and processed-food diets. Indonesia processed 47.5 million t of crude palm oil in 2024, underlining continuous clay demand in degumming and bleaching. Refiners are cutting clay dosage from 1.5-3.0% to 0.5-1.5% by adding enzymatic degumming and silica-hydrogel pre-treatments, saving up to 40% on clay while meeting color targets. This efficiency tempers volume growth but rewards suppliers offering high-activity grades that sustain lower dosages. Palm-oil’s higher carotenoid load keeps clay needs above soybean benchmarks, and World Bank data showing 6% palm-oil price gains in 2025 incentivizes plants to maximize physical refining runs.

Expansion of Biodiesel and Renewable Diesel Production

Biofuel policies keep clay demand buoyant. Indonesia’s B35 program consumed 11.96 million t of palm oil in 2024 and is preparing for B40, each step requiring double bleaching stages. Brazil’s B15 and Argentina’s export-oriented biodiesel add further pull. Hydrotreated renewable-diesel units, such as Pertamina’s 477 kl-day plant, insist on ultra-low phosphorus feedstock, often pushing bleaching earth dosage toward the 1-3% ceiling. These projects shift procurement toward high-surface-area, low-metal clays that protect hydrotreating catalysts and create premium-grade demand.

Growth in Mineral-Oil and Lubricant Quality Demands

API Group II/III base-oil producers require precise adsorption of aromatics and sulfur post-hydrotreating. Activated clays engineered for narrow pore distribution are gaining share, delivering stable viscosity indexes without stripping base-oil fractions. This segment offers margin insulation because dosage is only 0.1-0.5%, yet quality failure risks additive poisoning. Lubricant demand correlates with industrial output and fleet renewal, giving suppliers a counter-cyclical hedge when edible-oil volumes soften. Clariant’s 2025 filings cited biofuel regulation changes that dented U.S. volumes, highlighting the value of diversified end-markets[2]Clariant AG, “Q3 2025 Financial Statement,” clariant.com .

Industrialization Surge Across Asia-Pacific

Mid-tier refineries in India, Vietnam, and Bangladesh are expanding to meet urban food-oil needs. India imported 16 million t of edible oil in 2025, 99.7% of palm group volumes in crude form, hinting at forthcoming domestic refining investment. Smaller plants lacking capital for membrane filtration rely heavily on activated clays as the main purification step, supporting volume resilience. Rising oleochemical capacity for fatty acids and alcohols further diversifies clay usage beyond cooking-oil streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of Alternative Adsorbents and Processes | -0.5% | Global, concentrated in Europe and North America | Medium term (2-4 years) |

| Volatile Bentonite Raw-Material Pricing and Supply | -0.4% | Global, acute in North America and China | Short term (≤ 2 years) |

| Tightening Mining/Disposal Regulation Compliance Costs | -0.3% | Europe, China, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Alternative Adsorbents and Processes

Silica hydrogels, synthetic zeolites, and activated carbon attract premium niches such as pharmaceutical-oil and cosmetic refining. Silica-hydrogel pretreatment can trim clay dosage by 40%, while activated-carbon’s 500-1,500 m²-g surface area outperforms clay in pesticide removal. Regenerable adsorbents also cut disposal costs, pressuring clay pricing. Yet for bulk edible-oil bleaching, acid-activated bentonite still delivers the lowest cost-per-tonne outcome under GRAS and EU food additive clearances, sustaining its dominance.

Volatile Bentonite Raw-Material Pricing and Supply

The U.S. bentonite Producer Price Index climbed to 166 in 2025 from the 2007 base of 100, reflecting energy and compliance costs. Imports leapt to 94,000 t in 2023, signaling tightened domestic supply. China’s mining quotas and stricter environmental approvals further squeeze high-grade feedstock availability. Vertically integrated suppliers, such as Clariant with 60 mines worldwide, cushion margin swings, whereas standalone processors face spot-price exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Wet Process Dominance Amid Vapour-Phase Gains

Wet Process technology retained 54.38% revenue in 2025, anchored in palm- and soybean-oil corridors where cost per tonne drives selection. Its unwashed, acid-activated clay yields sufficient performance for bulk refining and supports rapid supply cycles to captive refineries across ASEAN and India. Dry Process remains niche in regions with low-cost thermal energy, while Vapour-Phase is forecast to grow at 5.12% CAGR as premium applications seek surface areas exceeding 320 m²-g and minimal residual acid. The Activated Bleaching Earth market size for Vapour-Phase grades is projected to rise alongside renewable-diesel feedstock qualification. Oxalic-acid routes offer a greener path, producing biodegradable effluents and aligning with circular-economy policies, yet process optimization is vital to curb calcium-oxalate precipitation that can blunt adsorption.

Vapour-Phase adoption is escalating in pharmaceutical-oil and cosmetic bases where trace metals must stay below parts-per-million limits. Plants installing vapour-acid reactors report 15-20% lower clay consumption thanks to higher activity, though capex remains a barrier. Suppliers leveraging proprietary oxalic vapour techniques position themselves for differentiated margin capture while meeting upcoming EU waste-water norms. Consequently, the Activated Bleaching Earth market continues to bifurcate into high-performance vapour-phase niches and cost-driven wet-process volumes, with technology selection dictated by feedstock quality and compliance pressures.

By Application: Edible Oil Refining Anchors Demand, Mineral-Oil Segment Accelerates

Edible oil and fats represented 79.10% of 2025 demand, supported by 200 million t global vegetable-oil consumption. Palm-oil’s higher carotenoid burden keeps dosage in the 1.0-3.0% band, whereas soybean and rapeseed oils use 0.5-1.5%. Dosage compression strategies—silica-hydrogel pretreatment and ultrasound-assisted bleaching—are lowering volume growth, but unit prices for premium clay grades are inching upward. EU limits on 3-MCPD are prompting refiners to favor natural or mildly activated clays, a shift that caps dosage yet drives up per-kilogram value. The Activated Bleaching Earth market share for edible-oil grades is likely to edge down as non-food niches expand, yet absolute tonnage will remain anchored here.

Mineral oil and lubricants, while smaller, are expanding at 5.33% CAGR through 2031. API Group III refiners require ultra-clean base oils, prompting 0.1-0.5% clay dosages with 30-50% price premiums. This segment stabilizes supplier revenues during agricultural downturns. Other applications—cosmetics, pharmaceuticals, wastewater—offer bespoke opportunities but demand consistent regulatory compliance and tighter particle-size control. Suppliers that can deliver traceability and technical support capture higher margins even at lower volumes.

Geography Analysis

Asia-Pacific maintained a 60.12% Activated Bleaching Earth market share in 2025, driven by 80 million t refining capacity across China, India, Indonesia, and Malaysia. Indonesia refined 47.5 million t of palm oil in 2024 and consumed 11.96 million t for B35 biodiesel, supporting twin demand streams. Export levy structures favor domestic refining, sustaining clay offtake. India’s pivot to crude palm oil imports, now 99.7% of palm group volumes, will spur local refining capex as duty gaps persist. China’s stricter mining rules are raising feedstock costs, opening import windows for Turkey and Brazil. Japan and South Korea continue to buy premium clays for pharmaceutical-oil and synthetic-lube segments, offering suppliers higher margins despite smaller volumes.

South America is the fastest-growing region at 4.96% CAGR, underpinned by Brazil’s B15 rollout and Argentina’s soybean-oil expansions. Brazilian biodiesel used 5-6 million t soybean oil in 2024, with B20 targeted by 2030, locking in clay demand for degumming and ester polishing. While enzymatic degumming trims dosage, refiners still require high-activity clay for low-phosphorus targets. Chile and Colombia are expanding edible-oil plants under import-substitution policies, contributing incremental volumes.

North America and Europe display mature trajectories. In the United States, renewable-diesel and sustainable-aviation-fuel plants provide pockets of growth, though Q3 2025 supplier comments pointed to policy-driven volume swings. Europe’s strict 3-MCPD caps are shifting consumption toward natural clays, while ILUC rules curb palm-based biodiesel imports and promote rapeseed refining. The Middle East and Africa, though smaller, are scaling refining under food-security mandates in Saudi Arabia, Egypt, and Nigeria, creating new clay demand coupled with technical-service needs.

Competitive Landscape

The Activated Bleaching Earth market is moderately concentrated. Clariant, Imerys, Oil-Dri, Musim Mas, and Taiko together hold roughly 40-45% share, leaving substantial space for regional suppliers. Clariant’s 60 bentonite mines across five continents provide feedstock security and support transfer-cost advantages. Imerys’ EUR 50 million January 2025 acquisition of Chemviron’s diatomite and perlite assets broadens its filtration portfolio and signals ongoing consolidation. Product differentiation is shifting toward ultrasound-ready clays and oxalic-acid activation, both promising lower effluent toxicity and higher activity.

Asia-Pacific hosts the fiercest price competition, with small-scale Chinese and Indian producers undercutting multinationals. Clariant’s Q3 2025 results highlighted negative pricing in Asia-Pacific despite double-digit volume growth, evidencing the focus on dosage efficiency over premium grades. New entrants investing in vapour-phase reactors aim at pharmaceutical and cosmetic niches that demand uniform particle distribution and regulatory certifications. Technology services—real-time dosage monitoring, predictive maintenance of bleaching vessels—are emerging differentiators. Suppliers offering integrated clay plus analytics bundles gain stickiness and protect volumes even as per-tonne usage declines.

Spent-clay valorization is the next competitive frontier. Roughly 2 million t of spent bleaching earth containing 20-40% residual oil accumulate yearly. Pilot projects converting this residue into biodiesel or recovering fatty acids via pyrolysis are underway in Malaysia and Spain, with suppliers partnering refiners in take-back schemes. Companies that master waste-to-value pathways may capture new revenue streams while easing disposal liabilities for customers, tightening client relationships in the process.

Activated Bleaching Earth Industry Leaders

CLARIANT

Taiko Group of Companies

Oil-Dri Corporation of America

Ashapura Perfoclay Limited (APL)

Musim Mas Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Imerys completed the EUR 50 million acquisition of Chemviron’s European diatomite and perlite operations, incorporating three mines located in France and Italy into its filtration portfolio. This acquisition is expected to strengthen Imerys' position in the activated bleaching earth market by enhancing its raw material supply for filtration applications.

- October 2024: The USDA has confirmed Indonesia's crude palm oil production for 2024 at 47.5 million tons, with biodiesel feedstock usage projected at 11.96 million tons. This supports the region's structural clay demand, which is a key component in the activated bleaching earth market used for refining palm oil.

Global Activated Bleaching Earth Market Report Scope

Activated bleaching earth is utilized in the refining, purification, and discoloration of edible and non-edible oils and fats. It is also referred to as wash clay. Activated bleaching earth is generally composed of clay minerals such as bentonite and attapulgite.

The activated bleaching earth market is segmented by technology, application and geography. By technology, the market is segmented into wet process, dry process, and vapour-phase process. By application, the market is segmented into edible oil and fats, mineral oil and lubricants, and other applications. The report also covers the market size and forecasts in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Wet Process |

| Dry Process |

| Vapour-Phase Process |

| Edible Oil and Fats |

| Mineral Oil and Lubricants |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Technology | Wet Process | |

| Dry Process | ||

| Vapour-Phase Process | ||

| By Application | Edible Oil and Fats | |

| Mineral Oil and Lubricants | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Activated Bleaching Earth market?

The Activated Bleaching Earth market size stood at USD 4.26 billion in 2026.

Which technology dominates Activated Bleaching Earth demand?

Wet Process technology led with a 54.38% share in 2025 due to its cost efficiency.

Why is South America the fastest-growing region?

Brazil’s B15 biodiesel mandate and Argentina’s soybean-oil expansions push regional growth at a 4.96% CAGR.

How are dosage-reduction trends affecting suppliers?

Enzymatic degumming and ultrasound-assisted bleaching are lowering per-tonne clay use, pressuring suppliers to deliver higher-activity grades.

Page last updated on: