Ball Clay Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

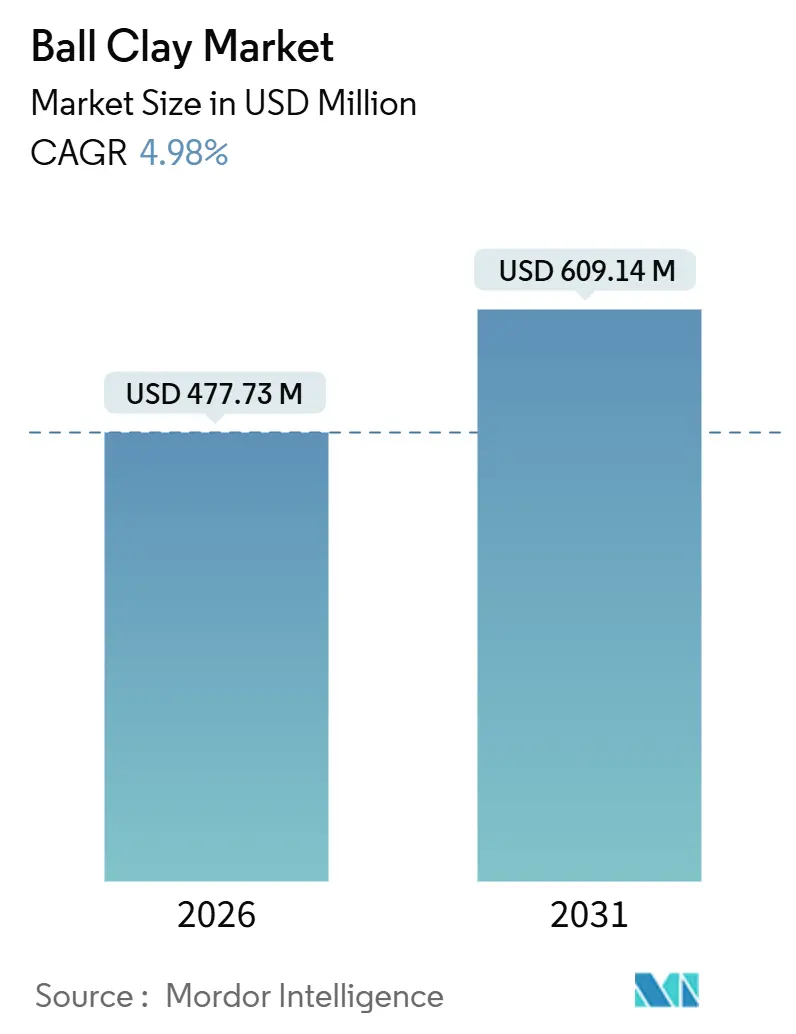

| Market Size (2026) | USD 477.73 Million |

| Market Size (2031) | USD 609.14 Million |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

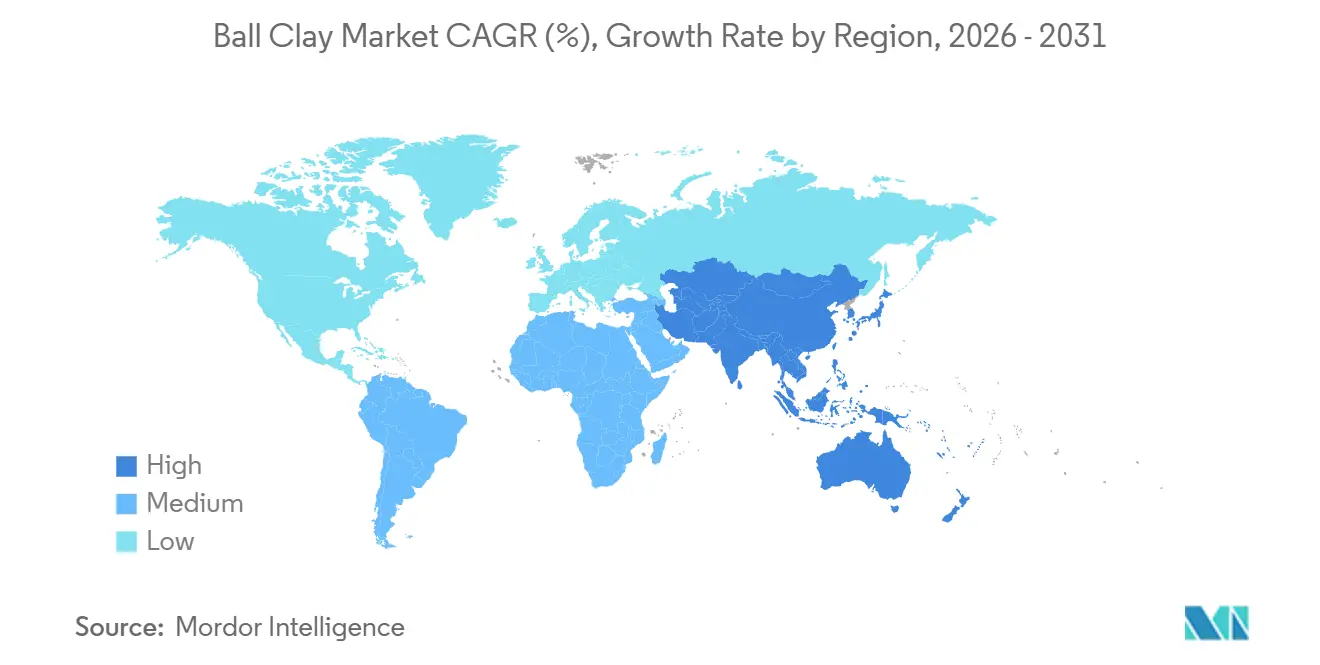

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

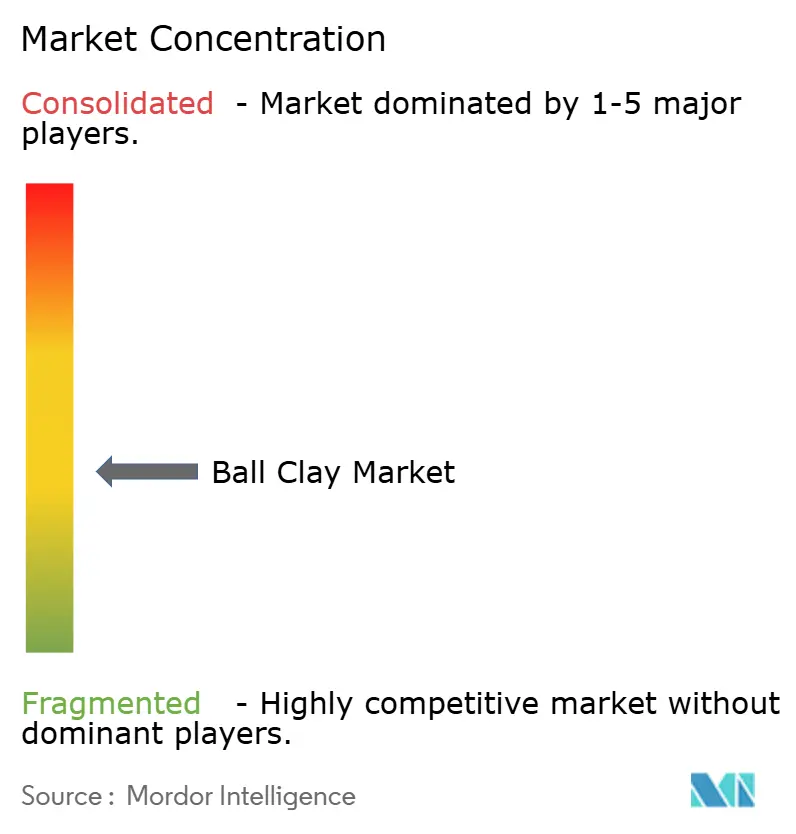

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ball Clay Market Analysis by Mordor Intelligence

The Ball Clay Market size is estimated at USD 477.73 million in 2026, and is expected to reach USD 609.14 million by 2031, at a CAGR of 4.98% during the forecast period (2026-2031). This trajectory stems from ball clay’s entrenched role in sanitaryware, wall and floor tiles, and tableware, where its ultra-plasticity and fine particle distribution are difficult to replicate synthetically. Ceramic applications commanded 93.19% of 2025 demand, reflecting the material’s irreplaceable status in thin-wall vitreous bodies. Asia-Pacific accounted for 38.06% of global consumption in 2025 and is on course for a 5.14% CAGR through 2031, leveraging large-scale residential construction in China and India. Capacity expansions in Morbi, Gujarat, together with ASEAN’s resurgent tile output, are pulling in imports from the United Kingdom and Germany despite freight volatility. On the supply side, Ukraine’s 2022 output collapse disrupted European supply chains, redirecting buyers to UK and German producers and lifting spot prices.

Key Report Takeaways

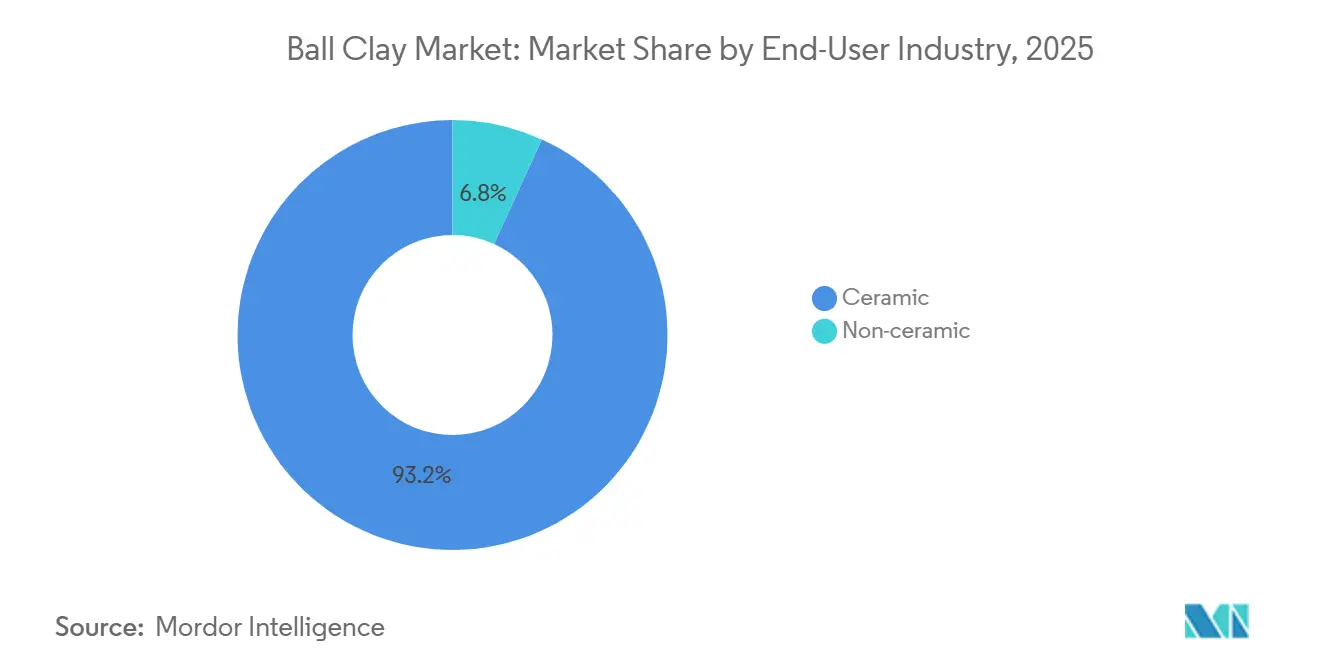

- By end-user industry, ceramics held 93.19% of the ball clay market share in 2025, and are poised for the fastest 4.98% CAGR through 2031.

- By geography, Asia-Pacific captured 38.06% of the ball clay market share in 2025 and is forecast to register the highest 5.14% regional CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ball Clay Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in sanitary-ware installations across Asia-Pacific high-rise housing | +1.8% | Asia-Pacific core, spill-over to Middle-East | Medium term (2-4 years) |

| Expansion of ceramic tile capacity in India and ASEAN | +1.5% | India, Vietnam, Thailand, Indonesia | Short term (≤ 2 years) |

| Rebound in North-American residential remodeling | +0.7% | United States, Canada | Short term (≤ 2 years) |

| Tightening specifications in European Union food-contact tableware | +0.6% | Europe, with indirect influence on exporters in Asia | Long term (≥ 4 years) |

| 3-D-printed advanced ceramics requiring ultra-plastic blends | +0.4% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Sanitary-Ware Installations Across Asia-Pacific High-Rise Housing

As urbanization accelerates in China and India, the demand for sanitary ware has transitioned from mere replacements to initial installations. Developers are now equipping multi-story towers with vitreous china fixtures, which leverage the plasticity of ball clay for their thin-wall casting. India's ceramic tile industry is witnessing significant growth. Concurrently, the output of sanitary ware is on the rise, driven by building codes that mandate separate wet areas in apartments exceeding 600 square feet. Thailand's market for sanitary fixtures is largely dominated by key players, who collectively source substantial volumes of UK ball clay. Developers are now pre-ordering fixtures months prior to project handovers, securing their ball clay demand earlier in the construction timeline. Over half of the world's vitreous china sanitary ware is produced using UK ball clay. This specific clay, with its unique kaolinite-mica-quartz balance, allows for lower-water slip casting and boasts a firing shrinkage of under 8%. The region's affinity for thin, glossy white surfaces heightens the demand for premium, low-iron grades.

Expansion of Ceramic Tile Capacity in India and ASEAN

In 2023, India claimed the title of the world's lowest-cost tile producer, buoyed by a surge in activity at Morbi-based factories, which ramped up their utilization. Meanwhile, Vietnam, with its plants boasting significant capacity, managed to produce less than its potential in 2024. This shortfall presents a significant opportunity for increased ball clay orders, especially as exports begin to pick up. In Indonesia, producers face a challenge: logistics for raw materials. Imports from Australia and Malaysia inflate landed prices compared to locally sourced kaolin. Furthermore, rising kaolin costs are prompting formulators to pivot towards blended bodies. These blends incorporate lower-grade ball clay, but only where the whiteness tolerances permit. In a move underscoring the region's growing demand, Kajaria is constructing its eighth plant in Nepal, projecting an additional need for ball clay, further bolstering import demand across South Asia.

Rebound in North-American Residential Remodeling

In 2024, U.S. ball clay production reached significant levels. Notably, a substantial portion of this output catered to wall and floor tile manufacturers. Deposits in Tennessee, boasting high plasticity indices, are pivotal for producing large-format porcelain tiles, a favored choice in open-plan remodels. Exports saw a resurgence, primarily driven by inventory replenishments from Canadian and Mexican buyers. While housing-start fluctuations can lead to uneven demand, the trend of larger master bathrooms is boosting tile usage per home, providing a buffer against potential market downturns.

Tightening Specifications in European Union Food-Contact Tableware

In response to EU Directive 84/500/EEC, which limits lead and cadmium migration, tableware manufacturers are reformulating their clay blends, now favoring low-iron ball clay grades. Acetic-acid leach tests have been standardized by Commission Regulation 333/2007. Meanwhile, the EU's anti-dumping regulation, 2025/1981, establishes a benchmark to deter imports priced below this threshold. Adhering to these regulations increases production costs, leading many producers to source ISO 17025-certified materials predominantly from the UK and Germany. Chinese exporters are now redirecting a portion of their ceramics exports toward the domestic market due to the tightening of EU regulations.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of substitutes (kaolin, synthetic binders) | -0.9% | Global, most acute in cost-sensitive segments in Asia and South America | Short term (≤ 2 years) |

| Environmental-impact permitting delays at open-pit mines | -0.5% | United Kingdom, Germany, North America | Medium term (2-4 years) |

| Concentration of Tier-1 deposits in politically sensitive belts | -0.4% | Europe (primary), with spillover to global supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Substitutes (Kaolin, Synthetic Binders)

Low-plasticity products, including construction bricks and economy tiles, benefit from cost savings when using kaolin and synthetic binders. Between 2020 and 2024, Indian tile plants reduced their ball clay content, opting for locally sourced kaolin that costs less. China's vast kaolin reserves allow for compositions with a higher proportion of kaolin and a lower proportion of ball clay. While binders such as polyvinyl alcohol enhance green strength, they fall short of ball clay in firing-shrinkage predictability, restricting their use in vitreous ceramics. This limitation impacts the market growth rate.

Environmental-Impact Permitting Delays at Open-Pit Mines

In the UK’s Bovey Basin, permitted reserves sit idle, constrained by operations nestled within Areas of Outstanding Natural Beauty. This has led to Environmental Impact Assessments (EIAs) taking longer to clear compared to 2015. In Germany, a reclamation bond requirement set at a high percentage of restoration costs translates to a substantial upfront addition[1]German Federal Ministry for Economic Affairs and Climate Action, “Federal Mining Act,” bmwk.de. Meanwhile, Michigan’s 2024 leasing framework, which mandates DNR-approved Mining and Reclamation Plans, has inadvertently extended timelines[2]Michigan Department of Natural Resources, “Nonmetallic Minerals Leasing Framework,” michigan.gov . Such regulatory hurdles have tightened supply elasticity, resulting in notable spikes in spot prices during demand surges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Ceramics Continue to Dominate While Niche Non-Ceramic Uses Gain Traction

Ceramic applications held 93.19% of the ball clay market share in 2025 and should mirror the overall 4.98% CAGR to 2031. Asia-Pacific's construction boom, particularly in high-rises, is driving the sanitaryware market, with vitreous china output now incorporating blends sourced from the UK. Wall and floor tiles dominate U.S. consumption, and large-format porcelain tiles are now requiring higher plasticity indices. In Europe, tableware is consolidating, influenced by stringent EU migration rules that favor premium, low-iron grades. As the industry shifts towards kaolin, bricks and other construction ceramics are losing market share. This shift is evident as Indian brick manufacturers have reduced their ball clay content. While the ball clay market for non-ceramic applications is currently modest, it shows potential for growth. Formulators of adhesives and sealants are turning to surface-treated products like Amlok 321 for improved sag resistance. Meanwhile, compounders in rubber and plastics are incorporating ball clay to ensure dimensional stability. Although fertilizer and pesticide carriers occupy a small portion of the market, their growth is hampered by competition from higher-CEC clays. The real growth potential lies in 3D-printed technical ceramics, where ultra-plastic blends can meet stringent particle specifications, a feat standard kaolin struggles to achieve.

These trends are further bolstered by secondary effects. Producers of sanitaryware in China and India are now forward-contracting their supplies in advance, leading to tighter spot volumes. In Germany and Italy, tableware manufacturers are diversifying their sourcing strategies to mitigate risks from disruptions in Ukraine, consequently boosting the demand for certified UK grades. In the U.S., infrastructure spending is driving the adhesive sector's growth, especially with state-level “Buy American” clauses promoting domestically mined inputs. Furthermore, the intersection of additive manufacturing and biomedical research is unveiling a fresh opportunity, which is poised to grow significantly in the coming years.

Geography Analysis

Asia-Pacific retained 38.06% of the ball clay market share in 2025 and is set for a 5.14% CAGR, the fastest worldwide. Morbi, India, with a significant tile capacity, consumes a substantial amount annually and is ramping up imports from the UK and Thailand. In China, producers are adjusting ball clay ratios to ensure plasticity as feldspar costs rise. Meanwhile, Vietnam's under-utilized plants hint at untapped demand. In Thailand, eight leading sanitaryware manufacturers are turning to the UK for premium glazing, underscoring the latter's significance.

By 2025, North America is poised to capture a notable market share. The U.S. caters to both its domestic market and exports. Tennessee stands out, providing high-plasticity grades crucial for large-format tiles. While housing-start cycles introduce demand fluctuations, trends like larger bathroom spaces and remodeling choices ensure steady growth. Manufacturers in Canada and Mexico are sourcing from U.S. mines, capitalizing on freight savings that bolster regional specialization.

Europe faces challenges post-Ukraine's output decline. To fill the gap, UK basins, especially Bovey and Petrockstowe, are dispatching significant reserves to clients across the continent. Germany's Stephan Schmidt KG is meeting EU standards by offering certified low-iron grades for tableware. Spain and Italy, once dependent on Ukrainian kaolin, have shifted their reliance to imports from the UK and Germany, making their supply chains more vulnerable to political and regulatory changes.

South America and the combined regions of the Middle-East and Africa hold a modest share in the market but show promise for medium-term growth. Brazil, standing as a leading tile producer, is leveraging deposits from São Paulo and Paraná, with Argentine imports filling any supply voids. In Saudi Arabia, a construction surge is driving a rise in sanitaryware imports. South Africa is curating its offerings, sourcing premium materials from Europe for upscale sanitaryware, while using local kaolin for more basic brick production.

Value Chain Analysis

Ball clay value creation starts with reserve access and permitting for open-pit mining in geologically constrained basins, notably the UK and parts of continental Europe and North America. After drilling and selective overburden removal, producers run wet or dry beneficiation to control particle-size distribution, iron/titania impurities, and rheology for slip casting. The material is then dewatered, filter-pressed, dried, and milled to customer specifications.

Product is sold as bulk/palletized powder or slurry and shipped mainly by truck, rail, and sea. Freight volatility and port and rail availability can affect landed costs for ceramic clusters such as Morbi (India) and ASEAN tile hubs, particularly when they import premium grades from the United Kingdom and Germany to cover gaps in local blends on whiteness and plasticity. Ceramics remain the dominant downstream use, with sanitaryware, wall and floor tiles, and tableware relying on ball clay for ultra-plasticity and predictable firing shrinkage that kaolin and synthetic binders struggle to replicate in vitreous bodies. Distribution typically combines direct contracts from miners, often with quality certification for regulated applications such as EU food-contact tableware, and regional mineral distributors that warehouse multiple grades and manage blending. Bottlenecks concentrate around supply and geopolitics, including European supply re-routing after the Ukraine disruption, alongside planning and environmental constraints that can extend approvals in sensitive landscapes such as the UK Bovey Basin, tightening spot availability during demand surges.

Competitive Landscape

The ball clay market is moderately fragmented. Regional specialists leverage logistics and customization. Technological differentiation is sharpening. White-space innovation centers on 3D printing. UK and German premium grades naturally achieve ±2 µm distributions without costly micronizing, positioning incumbents as preferred suppliers for aerospace and biomedical prototypes.

Ball Clay Industry Leaders

Sibelco

Imerys

ASHAPURA GROUP OF INDUSTRIES

Old Hickory Clay Company

Stephan Schmidt KG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

On the supply side, the main whitespace is securing long-duration reserves and planning permissions in premium basins, especially after European buyers re-routed sourcing following Ukraine-related supply disruption. Recent UK planning activity highlights how continuity depends on approvals tied to traffic management, restoration, and biodiversity conditions. Public reporting points to Sibelco planning discussions for the Zitherixon quarry expansion in Devon, targeting 5 million tonnes over a 50-year horizon, and Imerys-related planning actions around the Povington Pit cover both sand and continued access to ball clay grades used in ceramics and fine china. These permitting-led projects create room for contractors, rail and truck logistics providers, and processors that can deliver consistent, low-iron, narrow-size-distribution material aligned with tableware and sanitaryware specifications.

Demand-side opportunity is more concentrated in tighter specifications and higher-value formulations than broad substitution. EU food-contact tableware requirements, including Directive 84/500/EEC and standardized leach testing under Commission Regulation 333/2007, are pushing manufacturers toward certified low-iron inputs and favoring suppliers that can support documentation and traceability from mine to shipment. At the same time, the report’s identified innovation white space in 3D-printed technical ceramics rewards ultra-plastic blends with controlled particle distribution, including premium UK and German grades that naturally achieve tight distributions. This supports more differentiated offerings for prototype and specialty ceramic applications where standard kaolin cannot meet forming and shrinkage predictability requirements.

Recent Industry Developments

- May 2026: Imerys received local permission linked to operations at the Povington Pit in Dorset, supporting continued extraction of mineral products that include distinctive ball clay grades used in ceramics and fine china. The decision reinforces the role of planning approvals, traffic conditions, and restoration commitments in maintaining supply from premium UK basins. For ceramic manufacturers dependent on white-firing, high-plasticity inputs, such approvals help sustain availability amid broader European supply tightness.

- October 2025: Public reporting highlighted Sibelco planning discussions for a long-term expansion at the Zitherixon quarry in Devon, with an extraction plan cited at 5 million tonnes over 50 years. The scale and duration signal the strategic importance of reserve replacement and long-cycle permitting for ball clay producers operating in environmentally sensitive regions. It also indicates where future supply assurances for European ceramic clusters are being built through multi-decade resource planning rather than short-term spot procurement.

- July 2024: Imerys applied to extend operations at the Povington ball clay pit, with the submission referencing the release of around 275,000 tonnes over a 7 to 9 year period. The move shows how mature deposits are being managed through staged extensions to maintain feedstock for ceramic customers while meeting local planning requirements. Such extensions influence contract security and blending strategies for tile, sanitaryware, and tableware manufacturers that rely on consistent UK-origin ball clay.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market is defined as the value of ball clay sold for industrial use, where demand is tied to ceramic body formulations and other consuming industries that use ball clay for plasticity and binding.

Scope exclusions: We exclude internal mine-to-mine transfers, on-site captive consumption that is not priced, and unrelated kaolin or bentonite products sold outside ball clay specifications.

Segmentation Overview

- By End-User Industry

- Ceramic

- Sanitary Ware

- Wall and Floor Tiles

- Tableware

- Bricks

- Other Ceramics (Construction Ceramics and Refractories)

- Non-ceramic

- Adhesives and Sealants

- Rubbers and Plastics

- Fertilizers and Insecticides

- Other Non-ceramics

- Ceramic

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map how ball clay is produced, traded, and consumed, and then to set realistic bounds for volumes and pricing. We referred to public mining and minerals statistics, such as USGS mineral summaries, national geological survey releases, and select state mining department publications where clay reporting is available.

To understand demand pull, we also reviewed ceramics and construction indicators from sources such as UN Comtrade for trade flows, the World Bank for macro and construction signals, and trade association publications that discuss ceramic tiles and sanitaryware output trends. Company annual reports, investor presentations, and reputable industry press were used to cross-check capacity additions, mine expansions, and plant utilization commentary. In a few cases, paid subscriptions for company financials and an import-export shipment-level database helped validate major trade corridors and supplier presence. The desk sources listed here are illustrative only, and many other public documents were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was run to validate what desk sources cannot fully show, which is the practical split between ceramic and non-ceramic consumption and the typical price realization by grade and destination. We spoke with a mix of miners, processors, distributors, and large end users across APAC, EMEA, and the Americas, and then used those checks to adjust utilization, trade assumptions, and the timing of demand recovery where needed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 21% | APAC: 48% |

| Mid tier: 40% | Functional/Unit leaders: 26% | EMEA: 30% |

| Smaller Players: 22% | Managers: 53% | Americas: 22% |

Market-Sizing & Forecasting

Our core model uses a top-down approach where ceramic production signals and construction-linked demand are reconstructed by region, and then converted into ball clay demand using typical inclusion rates and material recipes shared during interviews. To keep the totals realistic, results are corroborated with selective bottom-up approximations, such as sampled supplier volumes, channel checks in key importing countries, and average selling price bands applied to estimated tonnage.

Key inputs that shaped the model include ceramic tile and sanitaryware output trends, building activity indicators, ball clay import and export movements, mine and processing capacity changes, and region-wise price realization differences driven by quality and logistics. We also watched substitution pressure from adjacent clays in non-ceramic uses, since that can shift demand without any visible change in construction output.

For forecasting, scenario analysis was used to reflect different paths for housing and renovation cycles, ceramic capacity utilization, and trade normalization in major corridors. Where bottom-up inputs had gaps (for example, private suppliers with limited disclosure), we filled them using peer benchmarks and then rechecked the implied per-country consumption against trade flows and end-use output levels.

Data Validation & Update Cycle

Validation was handled through multiple checks so the final number stays aligned with real-world signals. We compared modeled demand with independent indicators like ceramic production trends, trade intensity, and known capacity ramps, and then reviewed any large variances region by region before sign-off.

If an assumption created an unrealistic jump in implied consumption or pricing, the driver was isolated and tested again using interview feedback and alternate data cuts. The report is refreshed annually, and interim updates are triggered when material events occur, such as new mine capacity, policy changes affecting mining, or sharp freight and energy shifts that alter delivered pricing. Before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Ball Clay Market Size Compared Against Other Published Estimates

Published market sizes for ball clay often differ because each publisher draws the boundary in a slightly different way and then uses its own mix of production, trade, and price assumptions. Differences also show up when a study focuses mostly on ceramics versus counting a wider set of non-ceramic uses, and when the base year is anchored to a high or low point in the cycle.

By tracking ceramic output proxies, trade flows, and delivered price bands, Mordor Intelligence keeps the 2026 market value tied to a defined demand pool, while some estimates lean more on broad price ladders or a different product scope that inflates totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.48 B (2026) | |

| Global Consultancy A | USD 0.60 B (2024) | Uses an earlier base year and may apply a broader average pricing assumption across forms, which can lift value even if implied tonnage is similar. |

| Industry Publisher B | USD 0.97 B (2025) | Appears to include a wider clay scope and higher base-year valuation, and the longer forecast window can mix demand beyond core ceramic and verified non-ceramic applications. |

The spread in values is mainly explained by what gets counted as ball clay, which base year anchors pricing, and how tightly demand is linked back to ceramics and trade signals. Our approach stays repeatable because each regional total is built from observable indicators and then checked against supplier and importer feedback before finalizing the market value.

Key Questions Answered in the Report

How large is the ball clay market today, and how fast is it growing?

The ball clay market size was USD 477.73 million in 2026 and is forecast to reach USD 609.14 million by 2031, expanding at a 4.98% CAGR.

Which end-use segment consumes the most ball clay?

Ceramic applications, particularly sanitaryware, wall and floor tiles, and tableware, captured 93.19% of 2025 demand.

Which region leads global ball clay consumption?

Asia-Pacific held 38.06% of global demand in 2025 and is projected to post a 5.14% CAGR through 2031, driven by India, China, and ASEAN nations.

What are the major growth opportunities in ball clay?

Growth prospects include premium grades for EU-compliant tableware and ultra-plastic blends for 3D-printed technical ceramics, which demand particle-size distributions tighter than ±2 µm.

Page last updated on: