Market Overview

| Study Period | 2020 - 2031 |

|---|---|

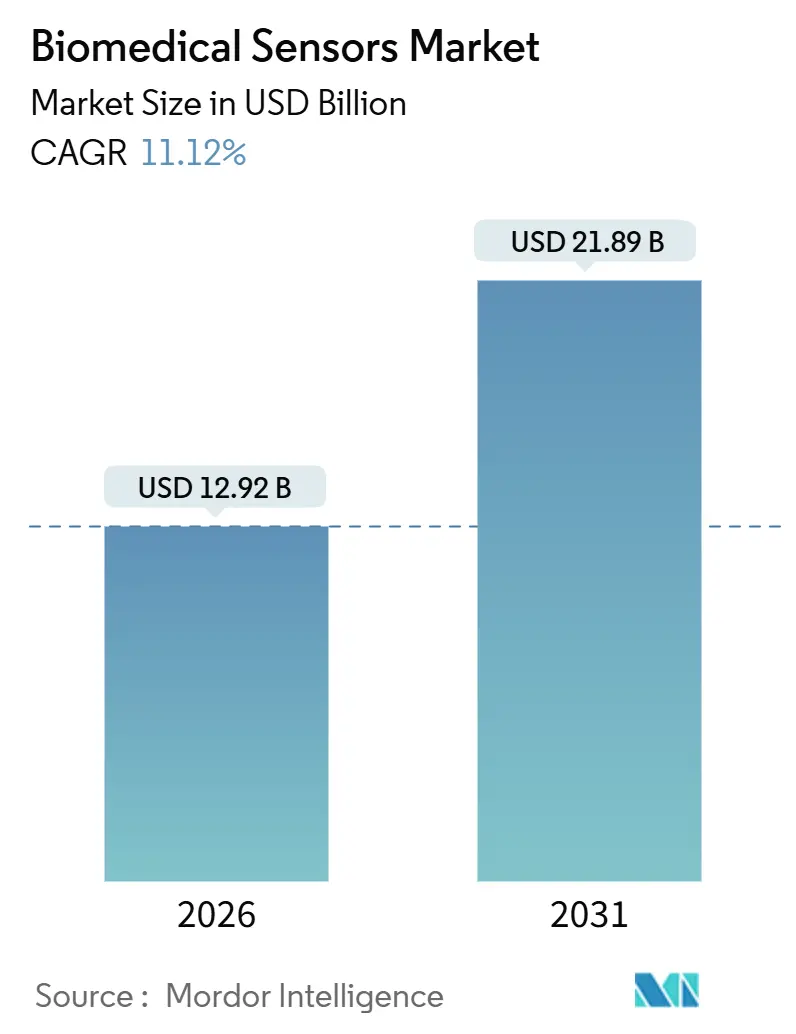

| Market Size (2026) | USD 12.92 Billion |

| Market Size (2031) | USD 21.89 Billion |

| Growth Rate (2026 - 2031) | 11.12% CAGR |

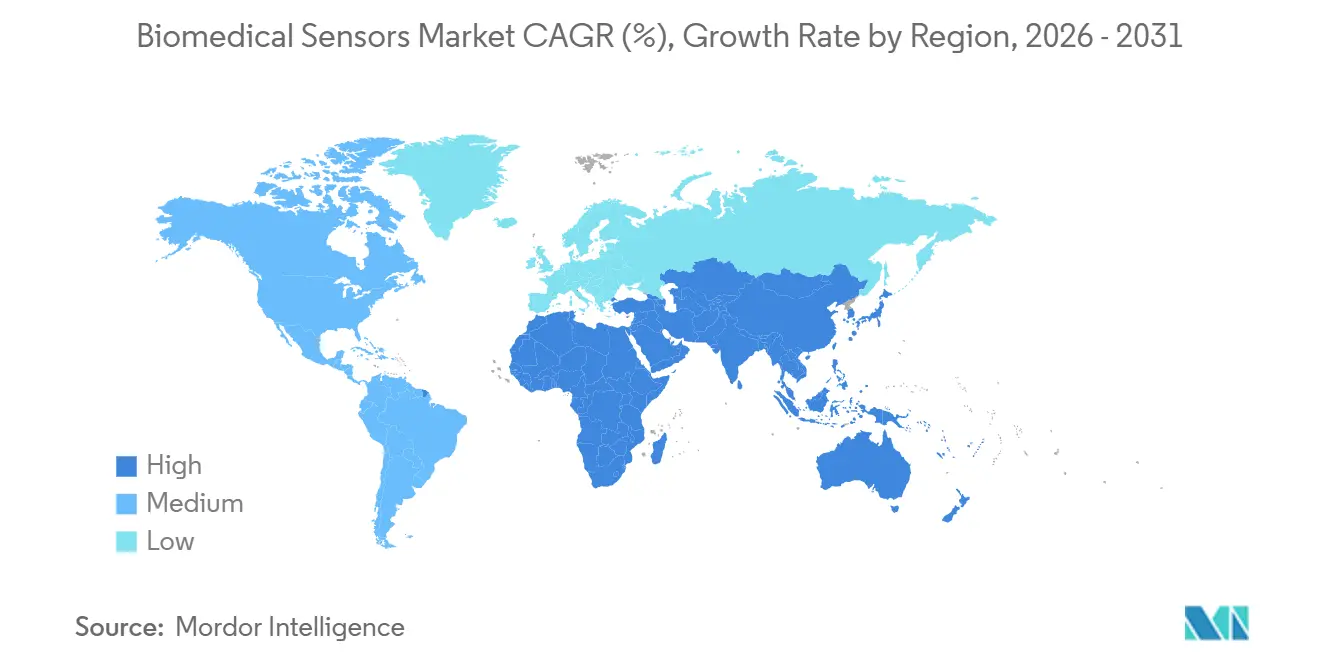

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biomedical Sensors Market Analysis by Mordor Intelligence

The biomedical sensors market size stood at USD 12.92 billion in 2026 and is forecast to advance at an 11.12% CAGR to reach USD 21.89 billion by 2031. Growth stems from rising wireless deployments, expanded reimbursement for remote patient monitoring, and form-factor innovation that embeds multiple modalities on millimeter-scale dies. Device makers are prioritizing Bluetooth Low Energy and near-field communication to bypass clinic-centric networks, a shift that gives payers real-time visibility into outcomes and strengthens value-based contracting. Continuous analyte tracking is expanding beyond diabetes to include lactate, ketone, and chemotherapy metabolite monitoring, thereby broadening the clinical addressable base. Semiconductor incumbents utilize advanced packaging to integrate pressure, temperature, and biochemical sensing onto a single chip, while software-first entrants leverage predictive analytics to wrap around commoditized hardware, capturing recurring revenue. Asia-Pacific governments are rapidly implementing digital health mandates that favor remote screening, and regulators on all continents now support iterative software updates, thereby shortening innovation cycles.

Key Report Takeaways

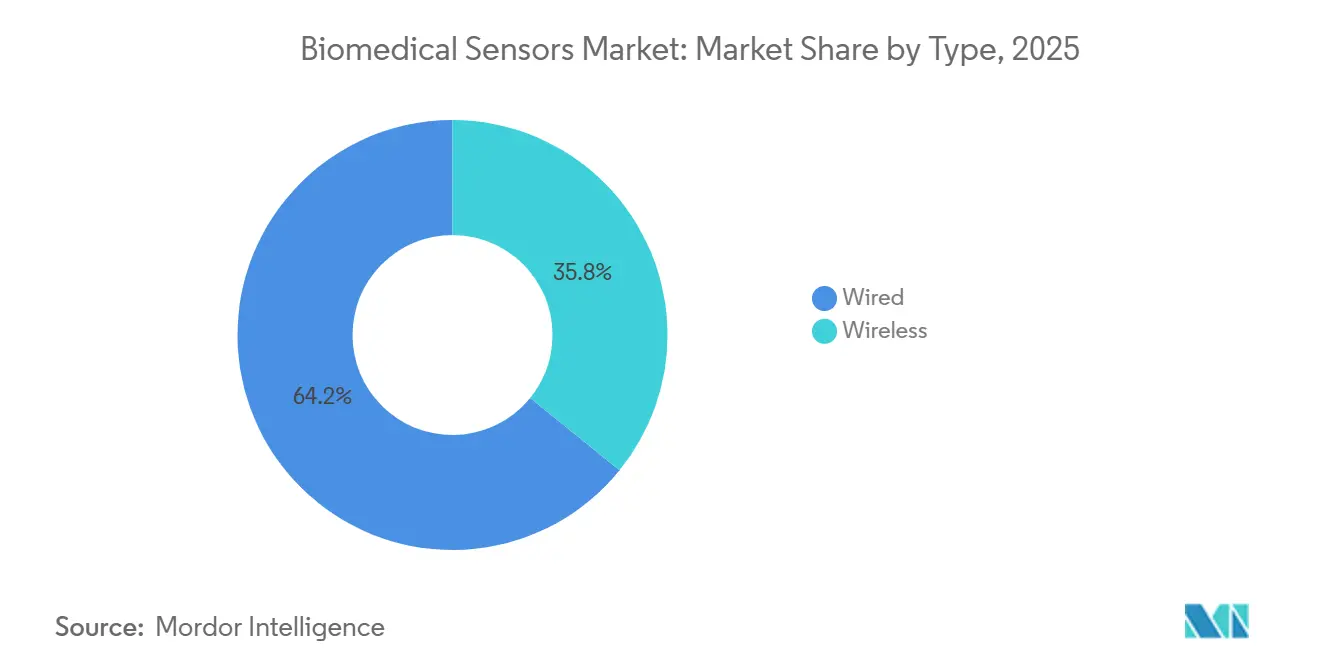

- By type, wireless architectures captured 64.17% of the biomedical sensors market share in 2025; the same segment is projected to register an 11.57% CAGR through 2031.

- By sensor type, temperature sensors held 29.73% of the biomedical sensors market share in 2025, while biochemical sensors are forecast to expand at a 12.73% CAGR through 2031.

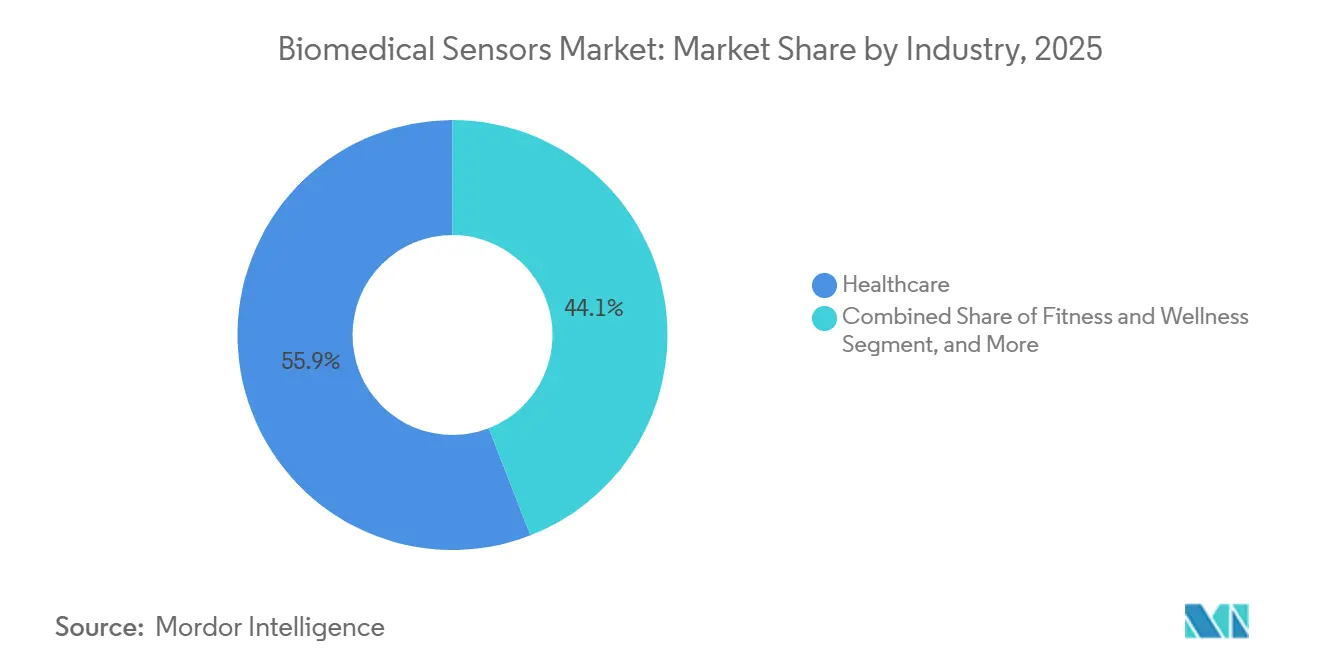

- By industry, healthcare institutions accounted for 55.91% of demand in 2025; fitness and wellness channels are projected to advance at a 12.03% CAGR through 2031.

- By application, monitoring accounted for a 46.72% share in 2025, whereas therapeutics platforms are poised for a 12.38% CAGR during the forecast period.

- By geography, North America dominated with a 39.12% revenue share in 2025, while the Asia-Pacific region is projected to deliver a 12.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biomedical Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for wearable health-monitoring devices | +2.3% | Global, early focus in North America and Western Europe | Short term (≤ 2 years) |

| Proliferation of remote patient monitoring programs | +2.1% | North America and EU core, expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| Miniaturization of MEMS and flexible electronics | +1.8% | Global, led by Taiwan, South Korea, Japan | Medium term (2-4 years) |

| Integration of AI-enabled predictive analytics into sensors | +1.6% | North America and China, spill-over to India and Southeast Asia | Long term (≥ 4 years) |

| Government incentives for tele-health and home care | +1.4% | Asia-Pacific, North America, EU | Short term (≤ 2 years) |

| Adoption of passive, battery-free architectures | +1.2% | Global, R&D concentration in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Wearable Health-Monitoring Devices

Consumer electronics brands have demonstrated that wrist, patch, and ring form factors can achieve clinical-grade sensitivity and specificity, as shown by studies on Apple Watch atrial fibrillation detection. Medicare added remote physiologic monitoring codes in 2024, creating a reimbursable pathway that accelerated the use of primary-care prescriptions. The Bluetooth 5.2 specification quadrupled range and doubled throughput, enabling stable links during vigorous activity. Two-week wearable electrocardiogram patches now replace 24-hour Holter monitors, capturing episodic arrhythmias that would otherwise be missed.[1]U.S. Food and Drug Administration, “Digital Health Center of Excellence – 2024 Annual Report,” FDA.gov

Proliferation of Remote Patient Monitoring Programs

The U.S. Department of Veterans Affairs enrolled more than 120,000 veterans in home telehealth programs, resulting in a 25% reduction in hospital bed days. European health ministries earmarked EUR 1.2 billion (USD 1.28 billion) in 2024 to subsidize remote-monitoring infrastructure for chronic disease cohorts. Private payers in the United States tie shared-savings bonuses to real-time sensor visibility for high-risk members, embedding monitoring mandates into value-based contracts.[2]Centers for Medicare and Medicaid Services, “CY 2024 Physician Fee Schedule Final Rule – Remote Physiologic Monitoring,” CMS.gov The ONC-endorsed FHIR standard enables sensor data to be directly integrated into electronic health records, eliminating the need for manual transcription and enhancing data integrity.

Miniaturization of MEMS and Flexible Electronics

MEMS fabrication on 200 mm and 300 mm wafers has reduced the unit costs of pressure and accelerometer dies to below USD 2. Polyimide flex circuits now bend to a 1 mm radius without electrical failure, enabling comfortable skin-conforming patches. STMicroelectronics has launched a 1.2 mm × 1.2 mm inertial measurement unit that integrates six degrees of freedom, plus temperature sensing, on a single die, representing a 40% footprint reduction compared to prior generations. IEC 60601-1-11:2024 clarified safety rules for home-health devices, accelerating market entry for flexible sensors. Silver-nanowire stretchable inks maintain conductivity under 30% strain, preserving signal quality during patient movement.

Integration of AI-Enabled Predictive Analytics Into Sensors

Abbott’s FreeStyle Libre 3 continuous glucose monitor performs on-device trend analysis that predicts hypoglycemia 20 minutes ahead of threshold crossings. Draft FDA guidance on predetermined change-control plans allows machine-learning algorithms to be updated post-market without requiring a new 510(k) submission, provided the performance remains within an agreed-upon envelope. Federated-learning architectures train local models on the device, thereby mitigating privacy concerns by eliminating the need for raw-data transfers. Neural-network quantization reduces model size by 75%, enabling inference to run within coin-cell power budgets for multi-year implantables.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High unit cost of advanced implantable sensors | -1.8% | Global, acute in emerging markets | Medium term (2-4 years) |

| Stringent multi-region regulatory approval cycles | -1.5% | Global, complex across North America, EU, China | Long term (≥ 4 years) |

| Data-privacy and cyber-security vulnerabilities | -1.2% | Global, heightened in EU under GDPR and in U.S. under HIPAA | Short term (≤ 2 years) |

| Packaging-related drift in long-term implants | -0.9% | Global, critical for neurostimulation and cardiac monitoring | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Unit Cost of Advanced Implantable Sensors

Factory-calibrated continuous glucose monitors, plus yearly transmitter and sensor replacements, cost USD 3,000–5,000, exceeding the savings modeled in most value-based contracts. Cardiac loop recorders cost nearly USD 8,000, while Medicare covers only the implantation fee, leaving hospitals to absorb the device expense. Manufacturing yields for hermetically sealed implantable packages remain below 85% because laser-welded feedthroughs are prone to microcracks, which necessitate costly rework. Emerging markets often lack reimbursement codes for implantables, resulting in limited adoption, which is primarily confined to self-pay urban segments in Southeast Asia and Latin America.

Stringent Multi-Region Regulatory Approval Cycles

The European Medical Device Regulation demands prospective clinical evidence even for devices previously cleared under equivalence routes, adding up to 24 months to launch timelines.[3]European Union, “Medical Device Regulation (EU) 2017/745 – Implementation Status 2024,” EUR-Lex.Europa.eu China’s National Medical Products Administration now requires Mandarin labeling and domestic clinical data for Class III medical devices, favoring local partners and potentially delaying the entry of multinationals. The U.S. De Novo pathway averaged 14 months from submission to decision in 2024, which is longer than typical consumer electronics refresh cycles. Limited harmonization means that firms must run parallel trials to satisfy divergent statistical significance thresholds across key markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Wireless Architectures Dominate Deployment

Wireless configurations accounted for 64.17% of the biomedical sensors market share in 2025, and this segment is projected to grow at an 11.57% CAGR through 2031. Standards-based Bluetooth, Wi-Fi 6E, and IEEE 802.15.6 protocols allow hospitals to network dozens of devices per room without retrenching cabling or risking infection from tethers. The biomedical sensors market size for wireless platforms is projected to reach USD 14.8 billion by 2031 as disposable patches become routine on surgical wards. Wired systems endure where electromagnetic interference tolerance or sub-millisecond latency is essential, but commoditized radio chipsets have cut wireless bills-of-materials by 40% since 2022, tipping the cost-benefit equation in favor of general wards and home care. Regulatory cybersecurity clauses in ISO 13485 have standardized update mechanisms, alleviating payer concerns about data breaches.

Second-generation wireless nodes can run for a full year on coin-cell power, easing the caregiver burden in elder-care environments. In intensive care, wired sensors still dominate closed-loop anesthesia because latency under 10 ms remains unattainable over the shared spectrum. Yet firms are trialing ultra-wideband to meet this threshold, hinting at full-wireless theaters within the forecast horizon. Disposable, peel-and-stick patches eliminate sterilization logistics, freeing nursing hours and reducing capital cycles for hospitals that previously invested in durable wired probes.

By Sensor Type: Biochemical Sensors Lead Growth

Temperature sensors captured a 29.73% share in 2025, thanks to ubiquitous fever screening; however, biochemical sensors are pacing the field at a 12.73% CAGR. The biomedical sensors market size for biochemical modalities is expected to exceed USD 4.7 billion by 2031, driven by the adoption of continuous glucose, lactate, and ketone monitors. Electrochemical platforms have achieved a mean absolute relative difference of less than 9%, unlocking Medicare and Japan’s national coverage for insulin-treated Type 2 diabetes. Sports physiology now demands real-time lactate thresholds, driving the integration of biochemical sensors into athletic wearables.

Pressure sensors face gross margin compression as mature MEMS lines push unit costs under USD 3. Image sensors incorporate on-chip processing to stream 4K endoscopy over legacy networks, while inertial sensors enter neurology with gait analytics that flag Parkinson’s disease progression months earlier than clinical observation. Dry-electrode electrocardiogram patches permit 30-day recordings, capturing paroxysmal arrhythmias that short-duration Holters miss. Contactless time-of-flight motion arrays are replacing chest belts in neonatal wards, improving comfort and lowering false alarms.

By Industry: Fitness and Wellness Accelerates

Healthcare institutions accounted for 55.91% of revenue in 2025, driven by bedside monitors and surgical navigation; however, consumer channels are advancing at a 12.03% CAGR. Direct-to-consumer continuous glucose monitors, positioned as metabolic optimization tools, topped USD 200 million in 2024 sales, indicating a willingness to self-fund data that guides nutrition and training. Professional cycling, triathlon, and CrossFit coaches now standardize glucose and lactate telemetry, broadcasting use cases that influence amateur adoption.

Pharmaceutical sponsors deploy sensors in decentralized trials to reduce the need for on-site visits, while research institutes collect longitudinal biosignals for exposome studies. The biomedical sensors industry is increasingly overlapping with consumer electronics; retailers are demanding ISO 13485 compliance even for wellness devices, thereby forcing quality regimes that previously applied only to medical devices. This blurring allows manufacturers to cross-subsidize R&D, but also attracts big-tech entrants that compete on user experience rather than hardware margins.

By Application: Therapeutics Applications Surge

Monitoring represented 46.72% of revenue in 2025, but therapeutics systems integrating sensors with actuators are growing at a rate of 12.38% annually. Closed-loop insulin delivery now meets pediatric glycemic targets that were previously unattainable by manual titration, and responsive neurostimulation has reduced seizure frequency by 75% in long-term data. The biomedical sensors market size for therapeutics platforms is expected to exceed USD 6.2 billion by 2031, driven by expanding reimbursement.

Diagnostics remains stable amid bundled payments, while imaging benefits from augmented reality overlays that fuse sensor data with pre-operative scans. Research and development use rises as digital biomarkers move from exploratory to surrogate endpoints in oncology and rare disease trials. Veterinary and industrial hygiene niches repurpose human sensor designs, illustrating the leverage of volume across adjacent domains.

Geography Analysis

North America accounted for 39.12% of global revenue in 2025, driven by Medicare CPT codes that reimburse device setup and monthly review. Provincial programs in Canada fully subsidize continuous glucose monitors for insulin users, while Mexico’s social-security pilots have demonstrated a 30% reduction in emergency department visits, validating the economics of rural telehealth. A deep venture ecosystem and flexible FDA software update policies maintain innovation velocity.

Asia-Pacific is forecast to have a 12.19% CAGR through 2031. China’s electronic-record mandate compels hospitals to integrate remote data, driving procurement of wireless vital-sign patches. Japan reimburses continuous glucose monitors for insulin-treated Type 2 patients, tripling its addressable base. India’s digital health mission assigns every citizen a unified identifier, allowing sensor data to follow patients across facilities and powering state-level analytics. Korean semiconductor giants expanded MEMS capacity by 40% in 2025, lowering component costs worldwide and reinforcing the region’s manufacturing dominance.

Europe grows unevenly as reimbursement and Medical Device Regulation demands diverge by country. Germany links payment to demonstrated reductions in hospitalization, nudging vendors toward predictive analytics. The United Kingdom secured volume discounts that slash unit prices by 35%, broadening access. France’s health-technology assessments emphasize the use of real-world evidence, thereby incentivizing post-market registries. Middle East investments in smart hospitals and South American insurer pilots extend adoption, though inconsistent payer policies keep those regions trailing headline growth leaders.

Regulatory Landscape

Biomedical sensors used for diagnosis, monitoring, and therapeutics are regulated as medical devices in major markets, which requires multi-region compliance planning across the United States (FDA), Europe (EU MDR/IVDR), and China (NMPA). In the United States, the FDA device framework (including 510(k) and De Novo pathways) affects time-to-market for connected wearables and implantables, while cybersecurity and software lifecycle expectations increasingly shape clearance strategies for wireless sensors used in remote patient monitoring programs.

Key regulatory anchors affecting product design and post-market obligations include the FDA Quality Management System Regulation (QMSR) amendment to CGMP taking effect on February 2, 2026, and Europe making EUDAMED database-related transparency obligations mandatory on May 28, 2026 for MDR/IVDR compliance. Standards updates also continue to tighten safety and performance baselines for home and remote use, including ISO 80601-2-61:2026 for pulse oximeter basic safety and essential performance, alongside broader home healthcare safety expectations referenced in IEC 60601-1-11:2024 for devices used in non-clinical environments.

Value Chain Analysis

The biomedical sensors value chain starts with upstream materials and components, including semiconductor wafers for MEMS, polymers for flexible substrates, and electrodes and enzymes or reagents for biochemical sensing. It then moves through sensor design, wafer fabrication, and specialized packaging. For implantable and long-wear devices, outsourced semiconductor assembly and test (OSAT) capacity for biocompatible and hermetic packaging acts as a gating step, followed by calibration, sterilization where applicable, and quality-system release under ISO 13485-aligned processes.

Downstream, device OEMs integrate sensing modules with radios (Bluetooth Low Energy, NFC, Wi-Fi) and firmware, then connect data to clinical and payer workflows through interoperable standards such as FHIR for EHR integration. Deployment typically goes through hospital procurement, remote patient monitoring program operators, and consumer retail channels for wellness-oriented wearables. Recent ecosystem signals also point to distribution of integrated wearable biosensor modules, such as Mouser stocking STMicroelectronics biosensor components in January 2025, and university-to-industry technology transfer that feeds next-generation biochemical interfaces, such as IPLEXMEDs graphene-based biosensor commercialization agreement with the University of Minho and INL in November 2025; in both cases, qualification, packaging, and regulatory documentation remain recurring bottlenecks.

Competitive Landscape

Roughly 55% of 2025 revenue accrued to the top ten suppliers, signifying moderate concentration yet fierce competition. Medtronic and Abbott leverage proprietary clinical datasets and vertically integrated manufacturing to defend provider channels. Texas Instruments and STMicroelectronics compete on die cost and power efficiency, feeding a long tail of original equipment manufacturers. Patent filings for flexible, stretchable substrates increased by 34% in 2024, indicating a shift from performance specifications to form-factor differentiation that favors materials science over legacy electromechanical expertise.

White space exists in closed-loop therapy, where diagnostic and intervention merge, creating regulatory moats. Niche entrants target intracranial and intraocular pressure, where calibration drift hobbles incumbents, using focused trials to prove superiority. Revenue models migrate toward SaaS dashboards that monetize data rather than hardware, favoring companies that can stand up cybersecurity-hardened cloud stacks. Compliance with ISO 14971 risk management and IEC 62304 software lifecycle now influences hospital tenders as much as price.

Biomedical Sensors Industry Leaders

Abbott Laboratories

Analog Devices Inc.

First Sensor AG

GE Healthcare

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary opportunity area is multi-analyte biochemical sensing that extends continuous monitoring beyond glucose into ketones, lactate, and other markers, supported by commercial moves toward dual-parameter products and partnerships in automated insulin delivery ecosystems. In May 2026, Abbott secured CE Mark for Libre Duo and Libre Duo 10 Day dual glucose-ketone sensing, and in June 2026 MiniMed announced an expanded agreement to commercialize dual glucose-ketone sensors made by Abbott for integration with MiniMed smart dosing systems. These actions support whitespace for suppliers that can combine biochemical sensing with low-power wireless, robust calibration, and manufacturable packaging for long-wear patches and closed-loop therapeutics.

A second opportunity area is the intersection of form-factor innovation and data integration, where multimodal sensing reduces device count and improves patient adherence in home and remote settings. Academic and open-hardware platforms published in 2026, such as the Biocoin wearable framework with multiplexed sensor inputs and cross-modal epidermal sensor research that fuses biopotential and biomechanical signals into a single channel, point to ways to reduce footprint and power while increasing signal richness. For vendors and OEMs, this supports product roadmaps that pair sensor miniaturization with interoperability, including FHIR-aligned data pipelines, and cybersecurity-ready update mechanisms aligned with payer-driven remote monitoring workflows and the broader wellness-to-medical continuum in wearables.

Recent Industry Developments

- June 2026: MiniMed announced an expanded agreement to commercialize integrated dual glucose-ketone sensors made by Abbott for exclusive integration with MiniMed smart dosing systems. The agreement supports broader multi-analyte sensing adoption inside automated insulin delivery workflows, while also raising the requirements for sensor accuracy, wear time, and interoperability within closed-loop therapeutics.

- May 2026: Abbott received CE Mark for Libre Duo and Libre Duo 10 Day, positioned as the first dual glucose-ketone continuous sensing technology for people with diabetes. The approval expands the product class for continuous biochemical monitoring in Europe and adds momentum toward multi-analyte sensor platforms rather than single-parameter CGM.

- March 2024: Analog Devices received US FDA 510(k) clearance and commercially launched the Sensinel Cardiopulmonary Management (CPM) System for remote chronic disease monitoring. This introduced an end-to-end wearable monitoring system from a semiconductor incumbent, reinforcing the shift from component supply toward integrated remote patient monitoring solutions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the biomedical sensors market is defined as revenue generated from sensors used to detect, measure, and convert physiological or biochemical signals into usable outputs for medical monitoring, diagnosis support, imaging, and therapy support across care settings.

Scope exclusions: We exclude general industrial sensors and lab-only analytical instruments that are not intended for medical or patient-related sensing use.

Segmentation Overview

- By Type

- Wired

- Wireless

- By Sensor Type

- Temperature

- Pressure

- Image Sensors

- Biochemical

- Inertial Sensors

- Motion Sensors

- Electrocardiogram (ECG)

- Other Sensor Types

- By Industry

- Pharmaceutical

- Healthcare

- Research Institutions

- Fitness and Wellness

- By Application

- Diagnostics

- Monitoring

- Therapeutics

- Imaging

- Research and Development

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand pool and the supply chain, so the assumptions stay grounded in what can be measured. We leaned on public sources such as US FDA device clearance databases, World Health Organization health statistics, US CDC health indicators, OECD health data, and publications indexed on PubMed to track clinical adoption and sensor performance trends.

Next, we used company annual reports, investor decks, and reputable press to understand product positioning, pricing moves, and route-to-market patterns. In parallel, patent databases and an approved paid subscription for company financials and intelligence helped confirm active development areas and the revenue mix signals that can be tied back to sensor content. These desk sources are illustrative, and we also used other public references for cross-checking, gap filling, and clarifying definitions.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions that usually drive size differences, including which sensors are counted as biomedical versus adjacent medical components, and how pricing changes by end use. We spoke with manufacturers, component specialists, device integrators, and downstream buyers across major regions, so adoption rates, average selling prices, and shipment patterns could be adjusted to reflect real purchasing behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 44% |

| Mid tier: 47% | Functional/Unit leaders: 40% | EMEA: 32% |

| Smaller Players: 14% | Managers: 48% | Americas: 24% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand reconstruction that starts from medical device and monitoring adoption signals, then narrows to sensor content that is used per device class. Once that anchor was set, the totals were corroborated with selective bottom-up checks, including sampled supplier revenue splits, typical sensor ASP bands by type, and volume logic tied to unit deployments in monitoring and diagnostics.

Key model inputs included wearable and remote patient monitoring penetration, chronic disease prevalence indicators that drive monitoring needs, procedure and imaging volumes where sensor content is consistent, device replacement cycles that affect annual unit flow, and pricing movement by sensor type as miniaturization increases. Forecasting used scenario analysis, where these variables were projected with expert consensus and then combined into base, conservative, and expansion cases. Where bottom-up evidence was missing for smaller countries or niche sensor categories, we used proxy adoption rates from comparable markets and then validated the implied per-capita spend against interview feedback.

Data Validation & Update Cycle

Validation is done through multiple passes, so the final number is not dependent on a single assumption. Outputs are checked against independent signals such as device shipment momentum, reimbursement direction for monitoring, and regional healthcare spending patterns, and any large variance triggers a review of pricing and adoption levers.

Before sign-off, the model goes through analyst-to-analyst checks, and respondents are re-contacted when a key input moves materially or when a new regulation changes device usage. The report is refreshed annually, and we also apply interim updates when major events shift demand, supply availability, or pricing. Right before delivery, a final review is completed so clients receive the most current view available at that time.

Mordor Intelligence's Biomedical Sensors Market Size Compared Against Other Published Estimates

It is normal to see different market sizes for biomedical sensors because sources may not count the same product set, may use different timing for currency conversion, or may apply different pricing curves when wearables grow faster than hospital systems.

Some published estimates widen the scope by bundling a broader set of medical sensors and device components. In Mordor Intelligence, the value is counted only when the sensor is used for biomedical signal sensing in defined medical and patient monitoring uses, and adjacent non-sensing device content is kept out, which changes the total even before forecasting assumptions are applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.92 B (2026) | |

| Global Consultancy A | USD 10.79 B (2024) | Uses a different base year and typically reports a wider definition of biomedical sensing that can pull in adjacent device components, which can shift both the starting value and the growth path. |

| Industry Publisher B | USD 10.70 B (2024) | Centers the estimate on a 2024 base with a different category mix and price progression approach, and the published number can vary if connectivity and end-use bundles are counted inside the sensor value. |

Taken together, the spread is mainly explained by scope choices, base-year selection, and how ASP changes are handled as wearables scale. Our approach keeps the model tied to observable adoption and unit signals, and the same steps can be repeated each refresh to keep the number stable and easy to audit.

Key Questions Answered in the Report

How large is the biomedical sensors market in 2026?

The biomedical sensors market size reached USD 12.92 billion in 2026 and is projected to hit USD 21.89 billion by 2031.

Which sensor category is growing fastest?

Biochemical sensors, led by continuous glucose and lactate monitors, are expected to expand at a 12.73% CAGR through 2031.

What share of revenue comes from wireless architectures?

Wireless configurations captured 64.17% of the biomedical sensors market share in 2025 and continue to outpace wired systems.

Which region will post the highest growth?

Asia-Pacific is forecast to register a 12.19% CAGR through 2031, propelled by government digitization mandates and local manufacturing scale.

How are reimbursement changes influencing adoption?

New CPT codes in the United States and expanded coverage in Canada and Japan offset device costs, making remote monitoring financially viable for providers.

What is driving competitive differentiation?

Flexible substrates, passive energy harvesting, and AI-enabled edge analytics are key innovation fronts shaping future product roadmaps.

Page last updated on: