Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Microbolometer Market Report is Segmented by Material (Vanadium Oxide, Amorphous Silicon, and More), Pixel Pitch (≤10 Μm, 12 Μm, and More), Resolution Format (≤320×240, and More), Application (Security and Surveillance, and More), End-Use Industry (Aerospace and Defense, Automotive, Industrial Manufacturing, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

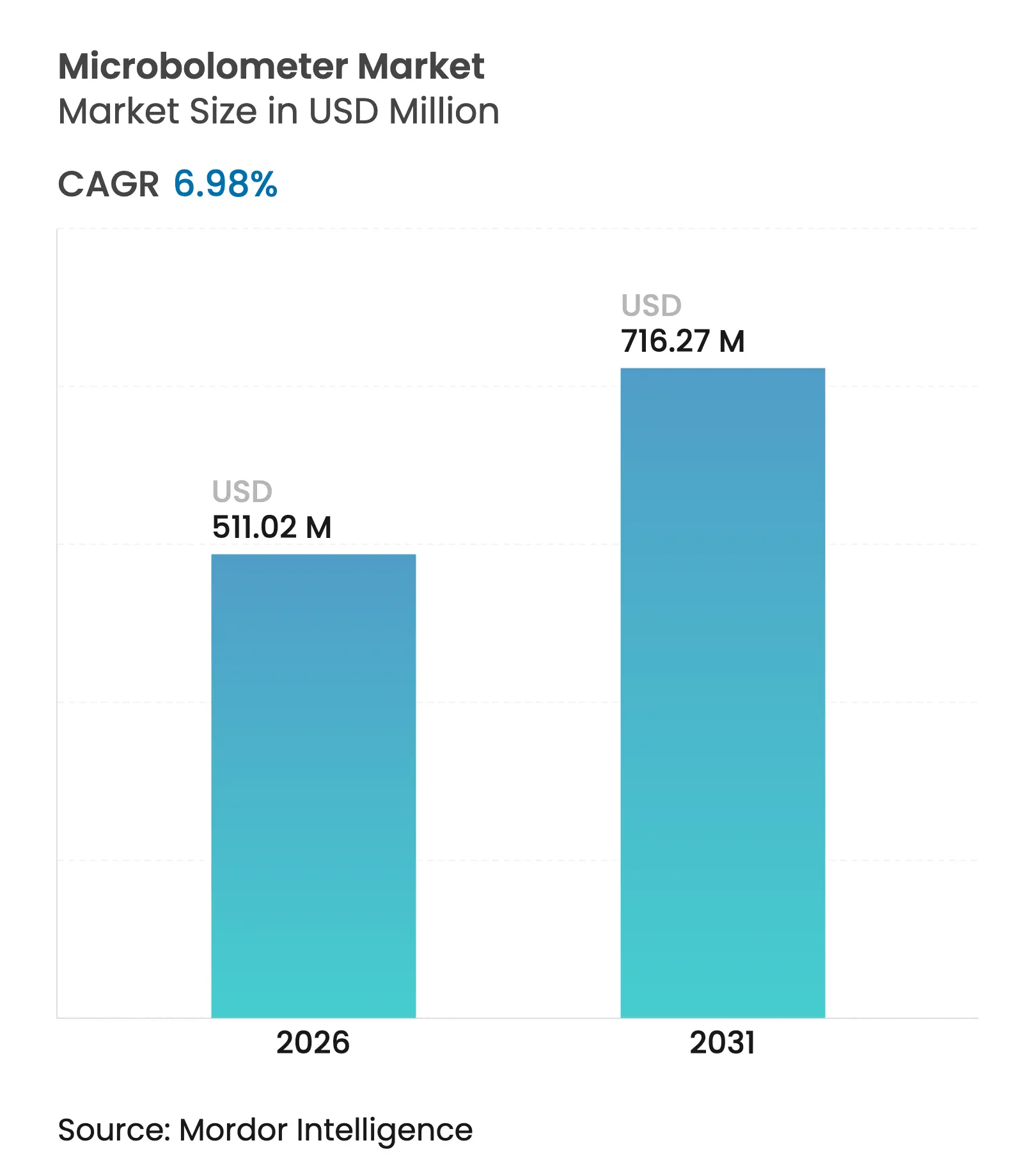

| Market Size (2026) | USD 511.02 Million |

| Market Size (2031) | USD 716.27 Million |

| Growth Rate (2026 - 2031) | 6.98 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Microbolometer market size in 2026 is estimated at USD 511.02 million, growing from 2025 value of USD 477.7 million with 2031 projections showing USD 716.27 million, growing at 6.98% CAGR over 2026-2031. The microbolometer market size reflects steady expansion as the technology moves from defense programs into mainstream commercial systems. Unit prices declined after wafer-level packaging reached high-volume production, and regulators relaxed export rules for sub-15 µm detectors, widening the customer base. Automotive advanced driver assistance systems have become a pivotal demand source, because thermal cameras extend pedestrian detection well beyond headlight range. Manufacturers also benefitted from stronger defense outlays and broader industrial IoT deployments that embed thermal nodes in factory assets for predictive maintenance.

Market participants focused on scale and vertical integration to protect margins in an environment where competition from silicon-based sensors is increasing. Clean-room investments, led by Lynred, doubled vanadium-oxide output capacity in Europe, while Asian entrants pursued cost-competitive CMOS routes. The microbolometer market is therefore at an inflection point: leaders must balance capacity expansion with in-house ROIC design talent to sustain performance advantages, even as alternative technologies such as short-wave infrared arrays chase the same budget-sensitive applications.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Regulatory easing of <15 µm export controls

Regulatory easing of <15 µm export controls

| +1.2% | Global, with primary benefits to North America and EU manufacturers | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global, with primary benefits to North America and EU

manufacturers

|

Impact Timeline

:

Medium term (2-4 years)

|

Cost decline via wafer-level packaging and 12 µm migration

Cost decline via wafer-level packaging and 12 µm migration

| +1.8% | Global, led by Asia-Pacific manufacturing hubs | Short term (≤ 2 years) | |||

ADAS-led automotive uptake

ADAS-led automotive uptake

| +2.1% | Global, concentrated in automotive manufacturing regions | Medium term (2-4 years) | |||

Industrial IoT - predictive maintenance thermal nodes

Industrial IoT - predictive maintenance thermal nodes

| +0.9% | APAC core, spill-over to North America and EU | Long term (≥ 4 years) | |||

Consumer AR/VR wearables with thermal sensing

Consumer AR/VR wearables with thermal sensing

| +0.6% | Global, early adoption in North America and Asia-Pacific | Long term (≥ 4 years) | |||

Defense and border-security modernization budgets

Defense and border-security modernization budgets

| +1.1% | North America, EU, Middle East | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Cost Decline via Wafer-Level Packaging and 12 µm Migration

Lynred doubled clean-room capacity in Grenoble in 2025, raising annual detector output by 50% and signalling industry commitment to scaled VOx production. Meridian Innovation attracted USD 12.5 million in funding to refine silicon CMOS-compatible wafer-level vacuum packaging, drawing venture interest toward low-cost detectors.[1]SPIE Europe Ltd., “Meridian Lands $12.5M for Low-Cost Thermal Sensors,” Optics.org, optics.org Shrinking from 17 µm to 12 µm reduced die area about 40%, cutting material cost per unit. Yet smaller pixels demanded tighter optical tolerances that lifted lens complexity, partly offsetting savings. Producers that mastered both packaging and optics therefore captured the bulk of cost benefits and secured design wins in industrial and consumer programs.

ADAS-Led Automotive Uptake

The U.S. National Highway Traffic Safety Administration mandated pedestrian automatic emergency braking for all new passenger vehicles from 2029. Magna’s thermal system, already deployed on 1.2 million cars, showed detection ranges four times farther than headlights. Sensor-fusion designs coupling thermal cameras with radar lowered false alarms while securing functional-safety certification. Teledyne FLIR and Valeo released the first ASIL B-rated automotive thermal camera, resolving readiness concerns for series production. These regulatory and technical milestones converted thermal imaging from a premium feature into a volume safety component, broadening the microbolometer market in the automotive value chain.

Industrial IoT – Predictive Maintenance Thermal Nodes

Factories adopted embedded thermal nodes to curb unplanned downtime. TDK’s i3 Micro Module combined thermal detection with edge AI, allowing real-time anomaly alerts while minimising network bandwidth. Exertherm offered self-powered IR sensors for medium-voltage switchgear that enabled continuous busbar monitoring without external energy sources . The microbolometer market gained a recurring revenue stream because service contracts for analytics complemented hardware sales. Adoption cycles remained lengthy, since plants insisted on multi-year reliability tests before linewide deployment, pushing the bulk of volume gains into the long-term horizon.

Defense and Border-Security Modernization Budgets

Leonardo DRS secured a USD 94 million order in June 2025 for advanced sniper sights that blended micro-cooled mid-wave and uncooled long-wave detectors. The program underlined continued preference for compact uncooled modules where low power and silent operation are paramount. Leonardo DRS also unveiled a rugged AI processor that pairs with thermal sensors to deliver on-board target recognition for ground forces. Border agencies specified microbolometer payloads for fixed and mobile towers, because LWIR performance stayed consistent through fog or dust.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High-resolution optics cost premium

High-resolution optics cost premium

| -0.8% | Global, particularly affecting cost-sensitive applications | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.8%

|

Geographic Relevance

:

Global, particularly affecting cost-sensitive applications

|

Impact Timeline

:

Short term (≤ 2 years)

|

Competition from SWIR/InGaAs and thermopile arrays

Competition from SWIR/InGaAs and thermopile arrays

| -1.1% | Global, concentrated in industrial and automotive segments | Medium term (2-4 years) | |||

Vanadium-oxide sputtering equipment bottlenecks

Vanadium-oxide sputtering equipment bottlenecks

| -0.6% | Global, affecting manufacturing scale-up | Short term (≤ 2 years) | |||

ROIC design-engineering talent shortage

ROIC design-engineering talent shortage

| -0.4% | North America and EU, limited impact in Asia-Pacific | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Competition from SWIR/InGaAs and Thermopile Arrays

System designers compared microbolometers with short-wave InGaAs and cost-oriented thermopile arrays. Lynred marketed all three detector families, acknowledging that no single technology fits every scenario. InGaAs excelled in high-temperature or gas-sensing roles, while thermopile grids undercut pricing for entry-level thermometers. Automotive Tier 1 suppliers evaluated hybrid modules that combine SWIR and LWIR for all-weather imaging, creating head-to-head bidding situations. Unless microbolometer vendors continue to cut cost per pixel, they risk displacement from price-sensitive platforms.

Vanadium-Oxide Sputtering Equipment Bottlenecks

VOx deposition relied on specialised physical vapor deposition tools, and the small supplier pool extended lead times when demand spiked.[2]Dalrada, “What Is PVD in Semiconductors?” Deposition Technology, deptec.com Expansion projects therefore faced long procurement cycles, capping near-term output. Some manufacturers investigated amorphous silicon or SiGe films to bypass VOx lines, but those alternatives required fresh process tuning and did not always match VOx sensitivity. Firms mitigated risk by pre-ordering spare chambers and dual-sourcing key components, yet supply resilience remained a drag on projected shipment acceleration.

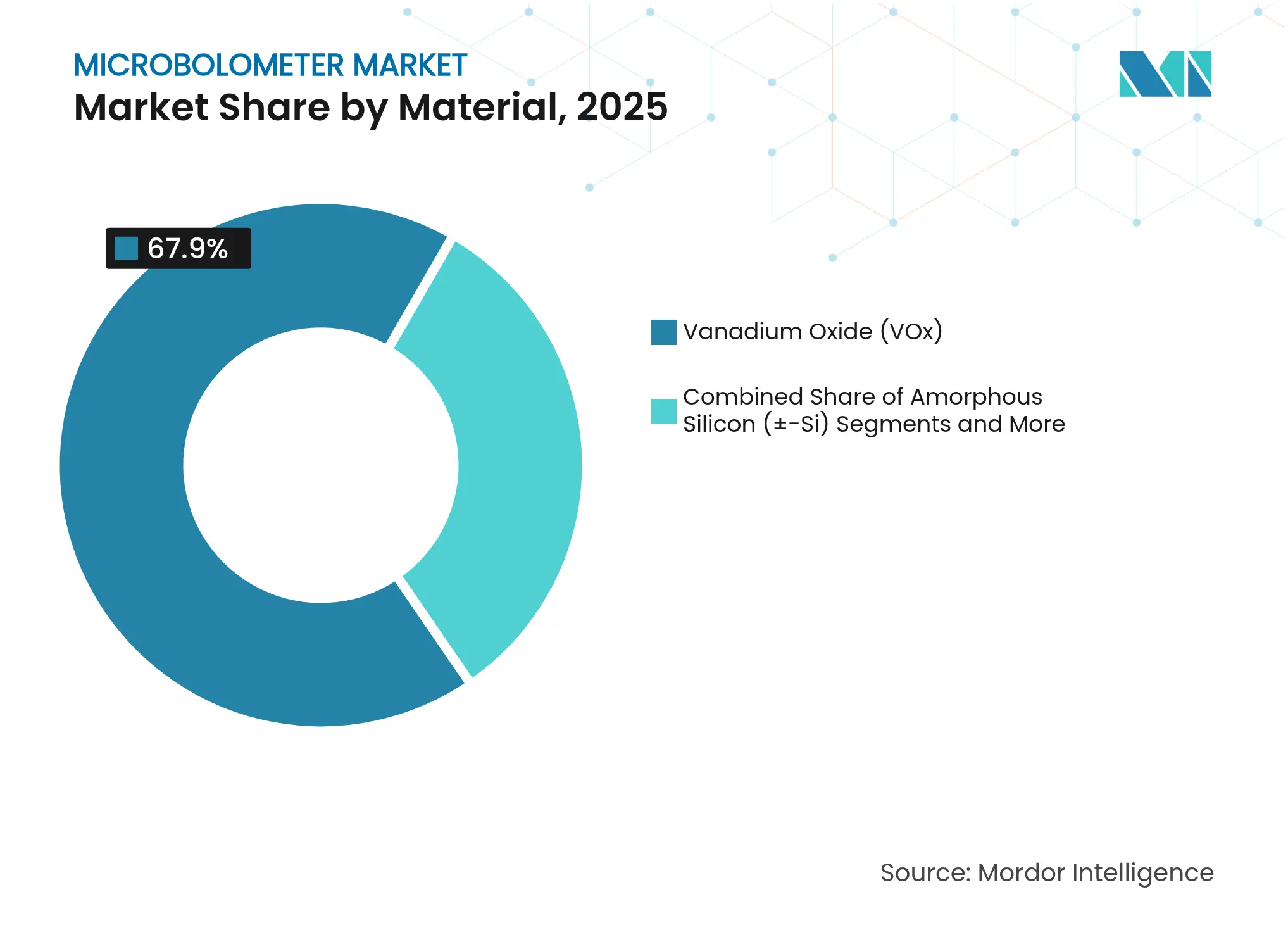

By Material: VOx Dominance Faces Silicon Challenge

Vanadium-oxide sensors retained 67.90% revenue in 2025. Lynred’s additional VOx capacity, completed in 2025, reinforced dominance despite silicon’s rise. The microbolometer market continued rewarding VOx for its low noise-equivalent temperature difference in defense optics. In parallel, amorphous silicon lines posted a 9.42% CAGR outlook, because CMOS-friendly processing lowered production cost for consumer and IoT modules. Emerging films such as amorphous Ge-Si or poly-SiGe targeted niche spectroscopic uses where coefficient-of-resistance tuning outweighed cost premiums.

Second-generation fabs co-located VOx and Si deposition to hedge demand swings across segments. Defense integrators still specified VOx to meet stringent sensitivity targets, while appliance makers preferred silicon for mass market price points. As a result, the microbolometer market saw dual-material roadmaps rather than a binary shift, ensuring supply resilience.

Note: Segment shares of all individual segments available upon report purchase

By Pixel Pitch: Miniaturization Drives Innovation

The 12 µm class delivered 53.85% value in 2025, recognised as the sweet spot between sensitivity and array size. Moving toward ≤10 µm pixels unlocked 15.45% CAGR through 2031, essential for smartphones and compact wearables. However, SPIE’s 2025 review indicated diminishing returns once diffraction-limited optics dominated system noise. The microbolometer market size for 17 µm parts remained resilient in price-driven thermography, because lens sets were cheaper and assembly yields higher.

Tool makers upgraded lithography steppers and wafer bonders to handle tighter tolerances. Design teams balanced quantum efficiency against reduced fill factors to prevent sensitivity loss. Consequently, product portfolios spanned three pitch classes to serve cost, performance, and miniaturization trade-offs.

By Resolution Format: VGA Stability Amid XGA Growth

The 640 × 480 VGA standard held 46.75% of 2025 shipments. OEMs favoured its mature software ecosystem and modest data rates that eased processor load. Resolutions above 1024 × 768 are tracking a 13.02% CAGR, propelled by defence panorama cameras and industrial robots that need digital zoom. In contrast, ≤320 × 240 arrays powered entry-level building monitors where thermal pattern detection over absolute accuracy sufficed.

Sensor makers incorporated on-chip image enhancement so that legacy VGA devices deliver near-HD perception at lower bandwidth. Market analysts expect the microbolometer market to sustain dual trajectories: VGA for utility devices and XGA-plus for vision-analytics stacks.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

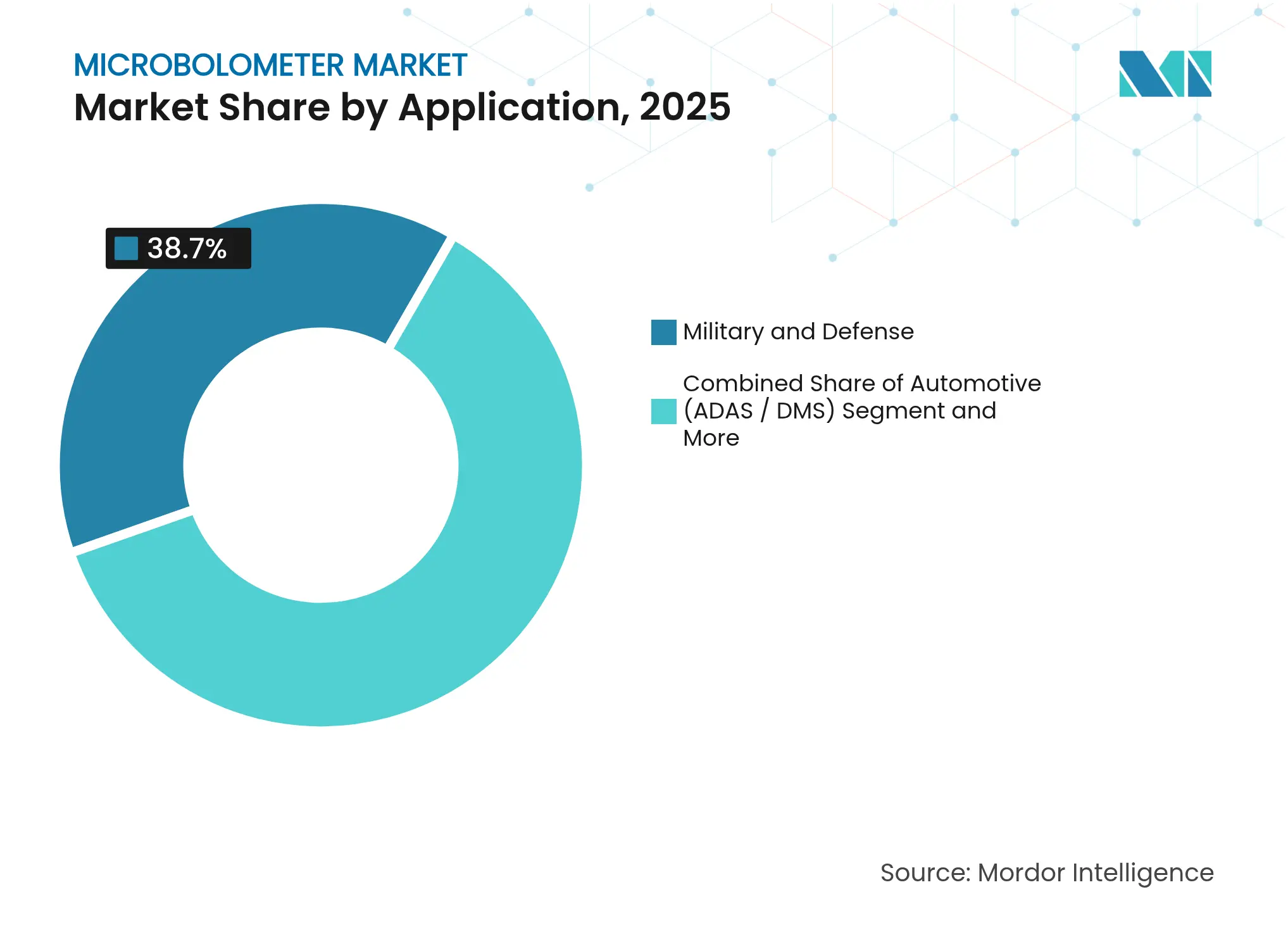

By Application: Military Leadership Yields to Automotive Growth

Military contracts generated 38.70% revenue in 2025. Program orders for weapon sights and situational-awareness gimbals locked in baseline volume. Automotive ADAS now posts the fastest 14.12% CAGR, because regulatory deadlines fix a clear uptake path. Security, thermography, medical screening, and personal vision each added incremental demand, rounding out the diversified funnel.

OEM procurement teams tailors specifications nased on the use case applications that may vary from long-range optics for border security, small pixel cameras for windscreen integration, and rugged cores for fire-rescue helmets. The microbolometer market therefore evolved from one dominant end-user to a multiprong structure that dampens cyclical risk.

Note: Segment shares of all individual segments available upon report purchase

By End-Use Industry: Aerospace Dominance Faces Automotive Challenge

Aerospace and defense kept 35.80% share in 2025, buoyed by sovereign upgrade programs. The automotive segment is expected to clock 13.32% CAGR to 2031, overtaking industrial manufacturing by the end of the forecast. Healthcare adopted non-contact thermography for triage, while public safety agencies employed helmet-mounted cams to improve visibility in smoke or darkness.

Tier-1 suppliers embedded thermal cameras into forward-looking sensor suites, and chip vendors offered reference boards that bundle IR cores with AI accelerators. This cross-industry tool-chain integration signals that the microbolometer industry is shifting from bespoke modules to platform solutions.

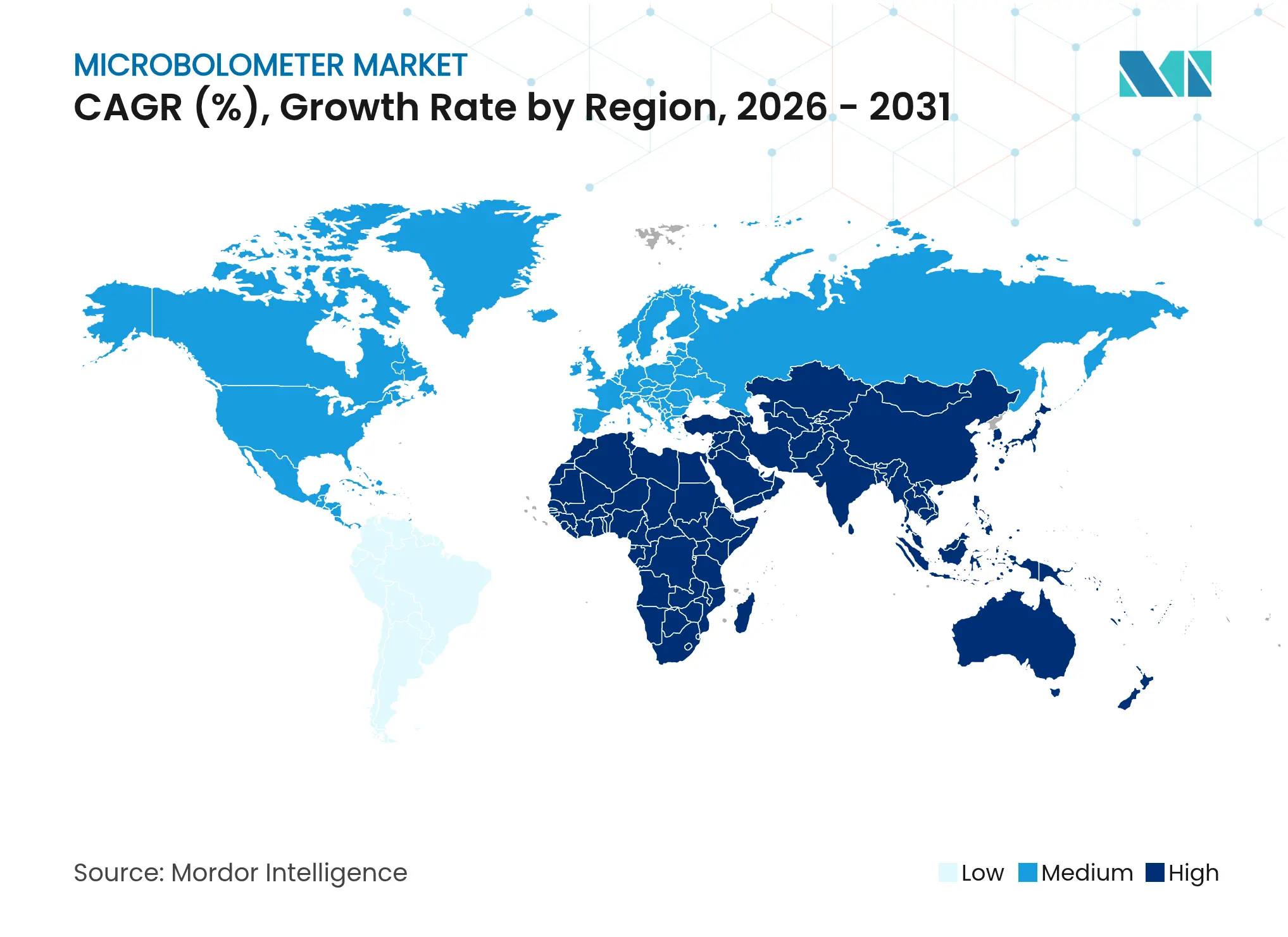

North America held 31.85% of 2025 turnover, anchored by U.S. defense contracts and early automotive pilots. Leonardo DRS’s USD 94 million sniper-sight award exemplified sustained military appetite Automakers adopted thermal cameras to comply with upcoming safety rules, and Mexican assembly plants integrated the sensors on high-volume lines. The region also featured strong academic-industry collaboration that nurtured ROIC design talent.

Asia-Pacific recorded the highest 9.98% CAGR outlook, driven by Chinese fabs such as Wuhan Global Sensor Technology producing cost-competitive VOx arrays. Japanese and South Korean automakers embedded thermal cameras in premium models, while factories across ASEAN rolled out IoT monitoring kits. The microbolometer market size in Asia-Pacific is projected to pass North America by 2031 as production clusters scale.

Europe remained influential owing to Lynred’s production upgrade and Germany’s automotive demand. European industrial firms adopted thermal imaging for energy-efficiency audits and machine monitoring. Middle East modernization and African infrastructure projects opened new procurement channels, though volumes stayed comparatively modest.

Market Concentration

The market showed moderate concentration. Teledyne Technologies, Lynred, and Leonardo DRS controlled detector design, ROIC fabrication, and end-user modules, enabling cost leverage and proprietary algorithms. Teledyne FLIR partnered with Valeo to embed ASIL-rated cameras into series-production cars, broadening reach beyond defense. Lynred’s EUR 85 million capacity build strengthened its supply security for both terrestrial and space missions, including the Meteosat Third Generation payload delivered in late 2024.

Asian challengers emphasised wafer-level CMOS routes. Meridian Innovation bet on silicon to undercut VOx pricing, while Wuhan GST leveraged domestic supply contracts. Leonardo DRS invested in AI-enabled processing that fuses thermal frames with contextual data, aiming to lock customers into software ecosystems. Niche players such as Seek Thermal targeted the consumer tier, releasing a USD 149 plug-and-play smartphone camera in mid-2024.[3]Seek Thermal Inc., “Introducing Seek Nano,” thermal.com

Competitive tactics ranged from long-term supply agreements with lens houses to royalty-free SDKs that accelerate developer adoption. Intellectual-property cross-licensing remained common, reducing litigation risk but reinforcing incumbent advantages.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Microbolometers, a specific kind of infrared sensor, play a pivotal role in thermal imaging cameras. They detect infrared radiation, or heat, and translate it into electronic signals. Notably, microbolometers are integral to uncooled infrared detectors, allowing them to operate without the need for extreme cooling, a requirement for certain other infrared detector types.

The study tracks the revenue accrued through the sale of microbolometers by various players across the globe. it also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The microbolometer market is segmented by type (vanadium oxide, amorphous silicon, and others), application (military, aerospace and defense, automotive, medical, others), and geography (North America, Europe, Asia Pacific, Middle East and Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.