Medical Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.37 Billion |

| Market Size (2031) | USD 14.84 Billion |

| Growth Rate (2026 - 2031) | 9.62% CAGR |

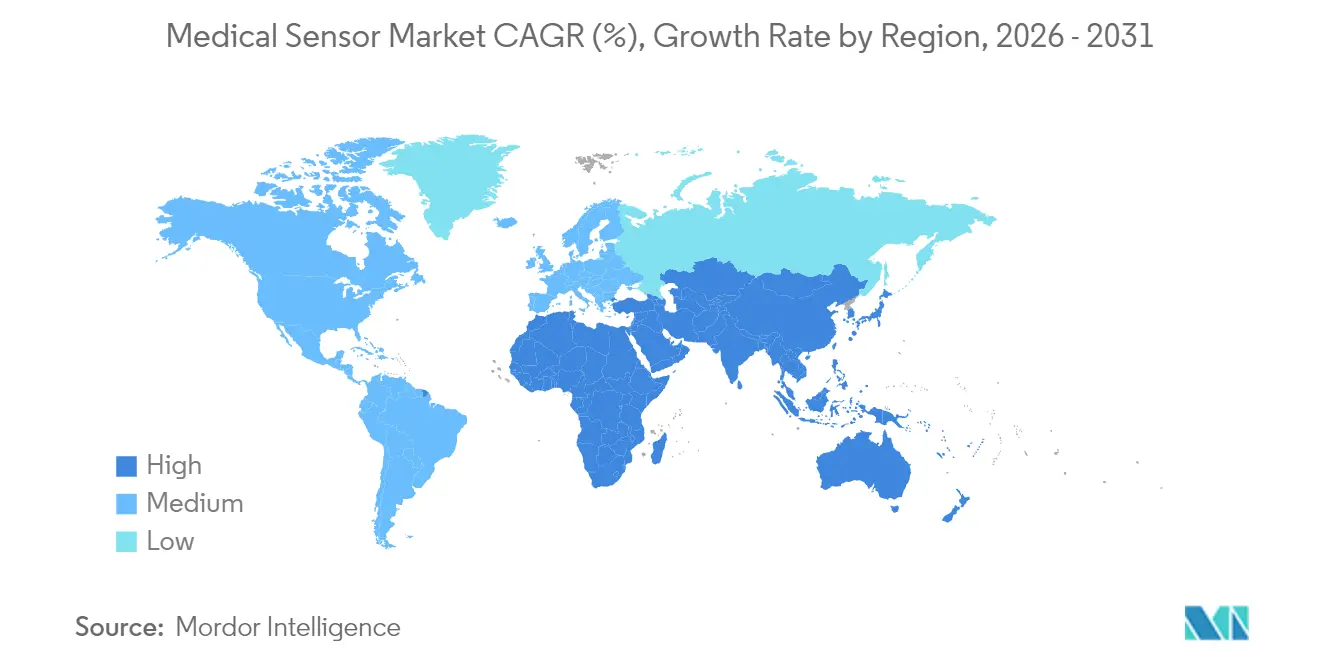

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

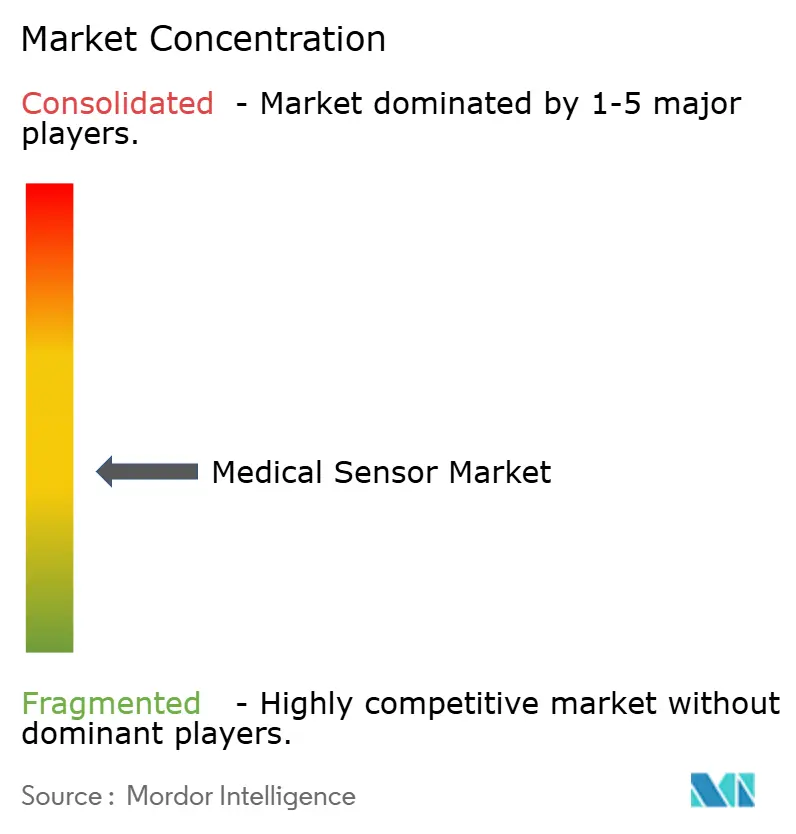

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Sensor Market Analysis by Mordor Intelligence

The medical sensors market size was valued at USD 8.55 billion in 2025 and estimated to grow from USD 9.37 billion in 2026 to reach USD 14.84 billion by 2031, at a CAGR of 9.62% during the forecast period (2026-2031). Rapid semiconductor miniaturization, AI-enabled analytics, and supportive regulatory pathways are accelerating the commercialization of medical devices across clinical and consumer settings. Biosensors retain demand leadership as glucose monitoring shifts from episodic testing to real-time feedback. Optical and image sensors gain momentum through high-resolution, non-invasive diagnostics that complement traditional modalities. Domestic fabrication incentives under the U.S. CHIPS Act, combined with national procurement programs in China, continue to shape supply chains and regional competitive advantages. Strategic partnerships between device firms and technology companies are shortening development cycles and broadening ecosystem integration to unlock new revenue pools across the medical sensors market.

Key Report Takeaways

- By sensor type, biosensors led with 43.35% medical sensors market share in 2025; optical/image sensors are forecast to expand at a 14.12% CAGR through 2031.

- By technology, MEMS devices captured 51.90% of the medical sensors market size in 2025, while nano/graphene sensors are projected to grow at 14.55% CAGR.

- By mode of deployment, wearable sensors accounted for 38.25% of the medical sensors market size in 2025; implantable sensors are advancing at a 13.05% CAGR to 2031.

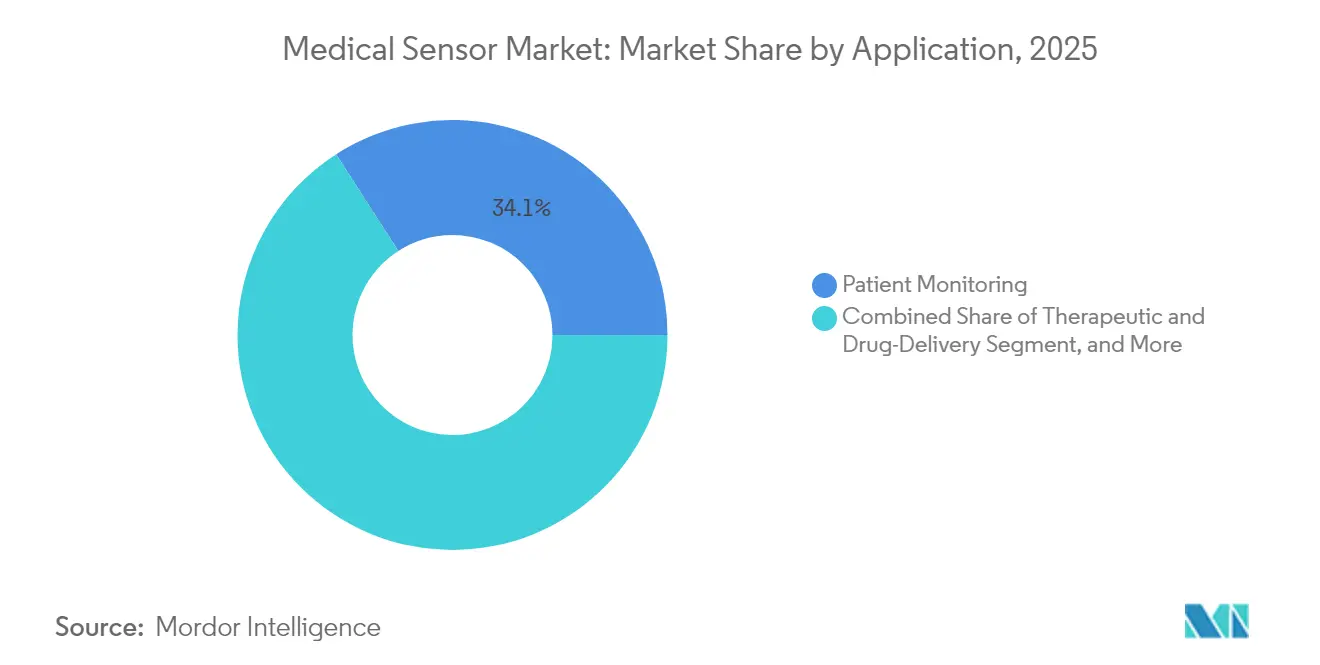

- By application, patient monitoring held 34.10% medical sensors market share in 2025; therapeutic and drug-delivery applications are growing at 13.22% CAGR.

- By end-user, hospitals controlled 63.30% of the medical sensors market size in 2025, whereas home-care settings show a 13.74% CAGR outlook.

- By geography, North America represented 34.20% medical sensors market share in 2025; Asia-Pacific exhibits the fastest regional CAGR at 13.92% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-enabled Continuous Glucose Monitoring Adoption in North America | +2.1% | North America, spill-over to EU | Medium term (2-4 years) |

| EU MDR–Driven Shift to Traceable Disposable Sensors | +1.8% | Europe, regulatory influence in Asia-Pacific | Long term (≥ 4 years) |

| China NHSA Procurement of Home-use SpO₂ Wearables | +1.5% | China, influence across Asia-Pacific | Short term (≤ 2 years) |

| Demand for Sterilizable Sensors in Robotic-Assisted Surgery (Japan) | +1.2% | Japan, adoption in developed markets | Medium term (2-4 years) |

| U.S. CHIPS-Act MEMS Fabs for Medical Sensors | +1.0% | North America, supply chain resilience globally | Long term (≥ 4 years) |

| 3D-Printed Microfluidic Wound Sensors in German Hospitals | +0.9% | Germany, EU adoption, clinical validation globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-enabled continuous glucose monitoring adoption

Roche secured CE Mark for its Accu-Chek SmartGuide system in 2024, integrating predictive algorithms that anticipate hypoglycemia events hours in advance. The FDA expanded automated insulin dosing clearance to Type 2 diabetes patients the same year, validating a path for closed-loop therapies. Dexcom’s USD 75 million investment in Oura underscores convergence between metabolic sensing and holistic wellness tracking. Collaboration between Abbott and Medtronic is accelerating interoperable platforms that link CGM data to pump algorithms in near real time. IBM and Roche advanced this trajectory in 2025 by adding lifestyle-based predictive models to sensor dashboards.[1]Roche, “Roche Receives CE Mark for Its AI-Enabled Continuous Glucose Monitoring Solution,” roche.com

EU MDR–driven shift to traceable disposable sensors

Medical Device Regulation enforcement obliges full life-cycle traceability through unique device identifiers embedded in even single-use products, pushing manufacturers to integrate digital tracking into disposables shipped to European clinics. German hospitals now pilot 3D-printed microfluidic wound sensors that log batch data at the point of care, creating feedback loops that support both reimbursement and post-market surveillance. Global firms increasingly adopt MDR-compliant design across all facilities to avoid dual inventories, elevating quality baselines in Asia-Pacific contract lines that supply European orders.

China NHSA procurement of home-use SpO₂ wearables

China’s National Healthcare Security Administration deployed millions of AI-equipped pulse-oximeters through public hospitals in 2024. Interoperability mandates ensure these devices feed national electronic health records, enabling epidemiological insights that strengthen chronic disease prevention. Vendors tailor firmware to meet local data-sovereignty rules while sustaining ISO-13485 certification, generating a bifurcated feature set that differentiates China-bound inventory from export models.

Demand for sterilizable sensors in robotic-assisted surgery

Japanese surgical centers require pressure and optical sensors capable of repeated autoclave exposure without drift. Soft optical blood sensors used in colonoscopy trials reached 96% detection performance while enduring high-pressure steam cycles. Material science programs focus on high-temperature polymers and hermetic glass encapsulation to extend sensor lifetimes through dozens of procedures, creating a premium segment that commands higher average selling prices in the medical sensors market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Divergent Cyber-Security Labeling (FDA RTA-V vs EU MDCG 2024-12) | -1.4% | Global, with acute impact in North America and EU | Short term (≤ 2 years) |

| Medical-grade Semiconductor Wafer Shortage (APAC) | -1.1% | Asia-Pacific manufacturing, global supply chain impact | Medium term (2-4 years) |

| EU WEEE/RoHS 2024 Cost Impact on Single-use Sensors | -0.8% | Europe, influence on global manufacturing standards | Long term (≥ 4 years) |

| Clinician Workflow Overload with Multi-param Wearables (UK NHS) | -0.6% | UK, broader adoption challenges in public health systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Divergent cyber-security labeling

Mismatch between the FDA’s real-time threat assessment framework and the EU’s pre-market security dossier rulebook requires dual validation pipelines. Development timelines lengthen by up to 20% and smaller entrants frequently limit launches to a single region, constraining competitive diversity and slowing global diffusion of innovations.

Medical-grade semiconductor wafer shortage

Foundries across Taiwan, South Korea, and China prioritize consumer electronics orders, leaving specialized image-sensor and analog lines under-allocated for medical demand. Lead times on advanced nodes exceed 12 months, pushing device makers to explore domestic wafer capacity expansions supported by the U.S. CHIPS Act funding mechanisms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Biosensors sustain clinical versatility

Biosensors captured 43.35% of the medical sensors market in 2025, anchored by glucose, cardiac, and infectious disease assays that display strong reimbursement support. Blood-glucose modules dominate subsegment revenues as continuous sensing replaces fingerstick diagnostics. Electrochemical platforms integrate AI filters that flag anomalous readings and reduce false alarms, boosting clinician trust. Pressure sensors remain critical in ventilators and hemodynamic monitors, while temperature elements now feature in multiparameter wearables that track fever progression. Flow sensors support respiratory therapy devices whose volumes rose following pandemic surges. Optical and image sensors hold the fastest growth path with a 14.12% CAGR as terahertz and hyperspectral modalities enable non-invasive tissue characterization. Accelerometers advance rehabilitation tools for stroke survivors, and niche graphene biosensors demonstrate sub-picomolar detection thresholds that anticipate future commercial uptake.

The competitive mix within biosensors is widening as research centers patent carbon nanotube arrays targeting hormonal biomarkers, adding depth to the medical sensors industry pipeline. Market leaders co-develop sensor-analytics bundles that merge raw signals with predictive dashboards. This services layer raises switching costs and broadens profit pools beyond the hardware sale. Given these trends, biosensors will preserve their dominant role while ceding relative percentage share to image-centric modalities that address oncology and dermatology needs within the medical sensors market.

By Technology: MEMS leadership meets nano-scale disruption

MEMS platforms provided 51.90% of the medical sensors market size in 2025 due to matured fabrication ecosystems and established reliability metrics. They underpin pressure, inertial, and flow devices across ICU monitors and ambulatory pumps. CMOS fabrication supports high-resolution image sensors and multifunctional system-on-chip solutions that house photodiodes, amplifiers, and radio interfaces. Fiber-optic sensors penetrate MRI suites and burn units where electromagnetic immunity is mandatory, supported by advances in flexible glass fibers that survive tensile strain.

Nano and graphene devices, though only a fraction of shipments, will post a 14.55% CAGR through 2031. Graphene metasurface biosensors demonstrated single-molecule viral detection in laboratory trial. Universities also produced sound-wave graphene sensors that achieve chemical fingerprinting, underscoring ultra-high sensitivity possibilities. Parallel progress in 3D-printed organic electronics opens design freedom for custom geometries that conventional lithography cannot deliver. As production yields improve, nano-scale architectures will increasingly displace MEMS in niche, high-sensitivity use cases across the medical sensors market.

By Mode of Deployment: Wearables dominate consumer entry

Wearable devices represented 38.25% of 2025 revenue, supported by smartphone connectivity and cloud analytics that translate sensor feeds into user-friendly dashboards. Fitness-oriented form factors use optical, inertial, and temperature elements to deliver sleep and activity insights, while clinical-grade patches collect ECG and SpO₂ data under regulated programs. Non-invasive designs reduce adherence barriers and expand sampling frequency, thus enhancing longitudinal datasets critical for preventive care algorithms.

Implantable platforms are growing at 13.05% CAGR as wireless power and miniaturized batteries lengthen dwell time. Early vascular health sensors already monitor pressure and flow to guide therapy adjustments. Disposable sensors answer infection control needs and meet traceability regulations by embedding low-cost memory tags that store batch identifiers. Their adoption surged during the pandemic when isolation protocols limited device reuse, a trend that remains sticky across the medical sensors market.

By Application: Patient monitoring anchors adoption

Patient monitoring retained 34.10% of the medical sensors market in 2025, reflecting broad integration into vitals stations, telehealth kits, and chronic disease dashboards. Remote models lower readmission risk and enable value-based reimbursement structures. Diagnostic imaging sensors deliver sharper resolution at lower radiation doses, aided by iterative reconstruction algorithms. Surgical guidance sensors provide real-time tissue oxygen feedback, elevating precision in minimally invasive procedures.

Therapeutic and drug-delivery systems hold the strongest growth at 13.22% CAGR as patch pumps and electronic bandages embed flow and pH sensors that titrate dosing in response to physiological cues. Wellness and fitness applications extend sensor footprints into consumer routines, creating hybrid datasets that bridge clinical and lifestyle domains. AI analytics extract early warning signals, positioning predictive care as a cornerstone of the medical sensors market.

By End-user: Hospitals retain scale but home care accelerates

Hospitals accounted for 63.30% of 2025 revenue by combining procurement power with clinical validation frameworks. Critical care floors rely on invasive pressure and hemodynamic sensors that interface with centralized monitoring stations. Ambulatory surgical centers embrace single-use optical elements that expedite turnover and minimize infection risk. Specialty clinics pilot niche devices such as sweat-resistant electromyography arrays that facilitate post-stroke rehabilitation.

Home-care settings record a 13.74% CAGR as reimbursement codes for remote patient monitoring expand coverage across chronic conditions. AI-driven dashboards translate multivariate sensor outputs into actionable home alerts. Smart textiles with embedded fiber-optic networks track mobility in elderly populations and deliver 100% activity classification accuracy during pilot studies. This distributed approach alleviates hospital capacity pressures and reshapes the care continuum within the medical sensors market.

Geography Analysis

North America maintained 34.20% revenue share in 2025 owing to large installed bases of connected diabetes and cardiac devices. The CHIPS Act earmarks USD 52 billion for semiconductor capacity that prioritizes medical allocations, reducing import reliance. FDA cybersecurity guidance promotes secure-by-design principles, granting compliant vendors first-mover position. Strategic alliances, such as the Dexcom-Oura partnership, spotlight a region where consumer wearables and regulated devices increasingly overlap. Canada leverages a single-payer model to pilot community-scale remote monitoring, while Mexico attracts nearshored sensor component production under US-Mexico-Canada free trade provisions.

Asia-Pacific presents the fastest expansion at a 13.92% CAGR through 2031. China’s NHSA mass procurement funnels millions of SpO₂ wearables into primary care, creating the largest longitudinal oximetry dataset worldwide. Japan’s aging society and high adoption of robotic surgery fuel demand for autoclave-resistant sensors. India scales low-cost glucometers under national non-communicable disease programs. South Korea’s foundries enable co-location of design and fabrication, shortening cycle times for next-generation pressure and image sensors. Semiconductor wafer shortages remain a headwind, yet government incentives encourage local capacity build-out, maintaining momentum across the medical sensors market.

Europe benefits from harmonized MDR regulations that elevate traceability standards and spur adoption of smart disposable sensors. Germany pilots 3D-printed wound sensors that offer embedded UDI codes for post-market surveillance. The United Kingdom’s National Health Service trials multi-parameter wearables under digital ward models, though clinician workload concerns moderate rollout speed. France and Italy adapt cybersecurity conformity assessments ahead of EU deadlines, supporting cross-border device portability. Data privacy mandates drive encryption and edge-processing innovations, shaping global design templates for secure medical sensors market deployments.

Competitive Landscape

The medical sensors market shows moderate fragmentation. Powerhouses such as Medtronic, Abbott, and Dexcom utilize their regulatory track records and extensive portfolios to maintain channel dominance. Semiconductor specialists, including STMicroelectronics and NXP, serve as critical upstream partners, ensuring supply continuity and providing reference design support. Consumer-electronics entrants capitalize on volume manufacturing and UX expertise to fast-track FDA submissions for wellness devices that straddle regulated and non-regulated categories.

Partnerships define competitive strategy. Volta Medical partnered with GE HealthCare to integrate AI electrophysiology algorithms with advanced mapping sensors, accelerating cath lab adoption. Dexcom and Abbott pursue ecosystem plays that link CGM data to consumer sleep and activity metrics, broadening longitudinal insight. Emerging startups focus on nano-material breakthroughs that promise order-of-magnitude sensitivity gains, positioning them as potential acquisition targets once manufacturability hurdles are cleared.

Competitive intensity heightens as policymakers tie reimbursement to outcome evidence that sensors uniquely provide. Firms integrate analytics subscriptions and cloud dashboards to elevate recurring revenue share. Those able to secure domestic wafer supply, achieve MDR cybersecurity conformity, and build AI stewardship credentials will strengthen standing in the medical sensors market over the forecast horizon.

Medical Sensor Industry Leaders

Medtronic plc

TE Connectivity Ltd.

Honeywell International Inc.

GE Healthcare Technologies Inc.

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Roche and IBM announced a collaboration to develop predictive AI technology for continuous glucose monitoring systems, leveraging machine learning algorithms to anticipate glucose fluctuations based on lifestyle and physiological patterns, representing a significant advancement in personalized diabetes management.

- April 2025: California Institute of Technology unveiled the iCares smart bandage featuring microfluidic components that sample wound fluid to provide real-time biomarker analysis, with machine-learning algorithms predicting healing times with expert-level accuracy, potentially revolutionizing chronic wound care.

- March 2025: University of Turku researchers achieved a breakthrough in carbon nanotube sensors that can detect low levels of female hormones, addressing the challenge of separating nanotubes based on chirality to improve sensor accuracy and sensitivity for continuous health monitoring applications.

- May 2024: Sensirion has launched the SLD3x series, a compact digital liquid flow sensor platform designed for precise dosing and enhanced patient safety in subcutaneous drug delivery. The sensors cater to diverse therapies and provide features like bubble detection, occlusion alerts, and pump malfunction identification.

Global Medical Sensor Market Report Scope

Medical sensors are sophisticated sensors that create a monitoring system and have a higher significance value. They decrease human errors, respond to physical stimuli, and find application in various forms, like checking/monitoring alcohol levels in the blood, biomechanics, blood analysis, breath analysis, eye parameters, and many others. The use of sensors is not only limited to patient care but it can also be used to track the movement of medicines and other patient-related testing materials.

The medical sensor market is segmented by type (flow sensor, biosensor, temperature sensor, pressure sensor, other types), application (clinical application and consumer application), and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Pressure Sensors |

| Temperature Sensors |

| Biosensors |

| Blood-Glucose Sensors |

| Flow / Airflow Sensors |

| Optical / Image Sensors |

| Accelerometers and Motion Sensors |

| Other Sensor Types |

| MEMS |

| CMOS |

| Fiber-optic |

| Nano / Graphene |

| 3D-Printed |

| Sensor Fusion Modules |

| Wearable |

| Implantable |

| Invasive (Catheter-based) |

| Non-invasive |

| Disposable / Single-use |

| Patient Monitoring (Vital Signs, RPM) |

| Diagnostic Imaging and In-vitro Diagnostics |

| Therapeutic and Drug-Delivery |

| Surgical and Minimally-Invasive Procedures |

| Wellness and Fitness |

| Hospitals and Large Health Systems |

| Ambulatory Surgical Centers |

| Home-care Settings |

| Specialty Clinics and Diagnostic Labs |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Sensor Type | Pressure Sensors | ||

| Temperature Sensors | |||

| Biosensors | |||

| Blood-Glucose Sensors | |||

| Flow / Airflow Sensors | |||

| Optical / Image Sensors | |||

| Accelerometers and Motion Sensors | |||

| Other Sensor Types | |||

| By Technology | MEMS | ||

| CMOS | |||

| Fiber-optic | |||

| Nano / Graphene | |||

| 3D-Printed | |||

| Sensor Fusion Modules | |||

| By Mode of Deployment | Wearable | ||

| Implantable | |||

| Invasive (Catheter-based) | |||

| Non-invasive | |||

| Disposable / Single-use | |||

| By Application | Patient Monitoring (Vital Signs, RPM) | ||

| Diagnostic Imaging and In-vitro Diagnostics | |||

| Therapeutic and Drug-Delivery | |||

| Surgical and Minimally-Invasive Procedures | |||

| Wellness and Fitness | |||

| By End-user | Hospitals and Large Health Systems | ||

| Ambulatory Surgical Centers | |||

| Home-care Settings | |||

| Specialty Clinics and Diagnostic Labs | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the medical sensors market today?

The market stands at USD 9.37 billion in 2026 and is set to reach USD 14.84 billion by 2031, registering a 9.62% CAGR.

Which sensor type generates the highest revenue?

Biosensors lead with 43.35% share, supported by continuous glucose monitoring and cardiac diagnostics growth.

What is the fastest-growing deployment mode?

Implantable sensors exhibit a 13.05% CAGR as wireless power and biocompatible materials mature.

Why is Asia-Pacific the fastest-growing region for medical sensors?

National procurement of home-use SpO₂ wearables in China and advanced sterilizable sensor demand in Japan drive a 13.92% regional CAGR.

How are regulations shaping product design in Europe?

The EU Medical Device Regulation mandates full traceability, prompting manufacturers to embed digital identifiers even in disposable sensors.

What competitive strategies are market leaders adopting?

Firms pursue partnerships that merge sensor hardware with AI analytics platforms, creating integrated ecosystems that improve patient outcomes and generate recurring revenues.

Page last updated on: