Market Overview

| Study Period | 2021 - 2031 |

|---|---|

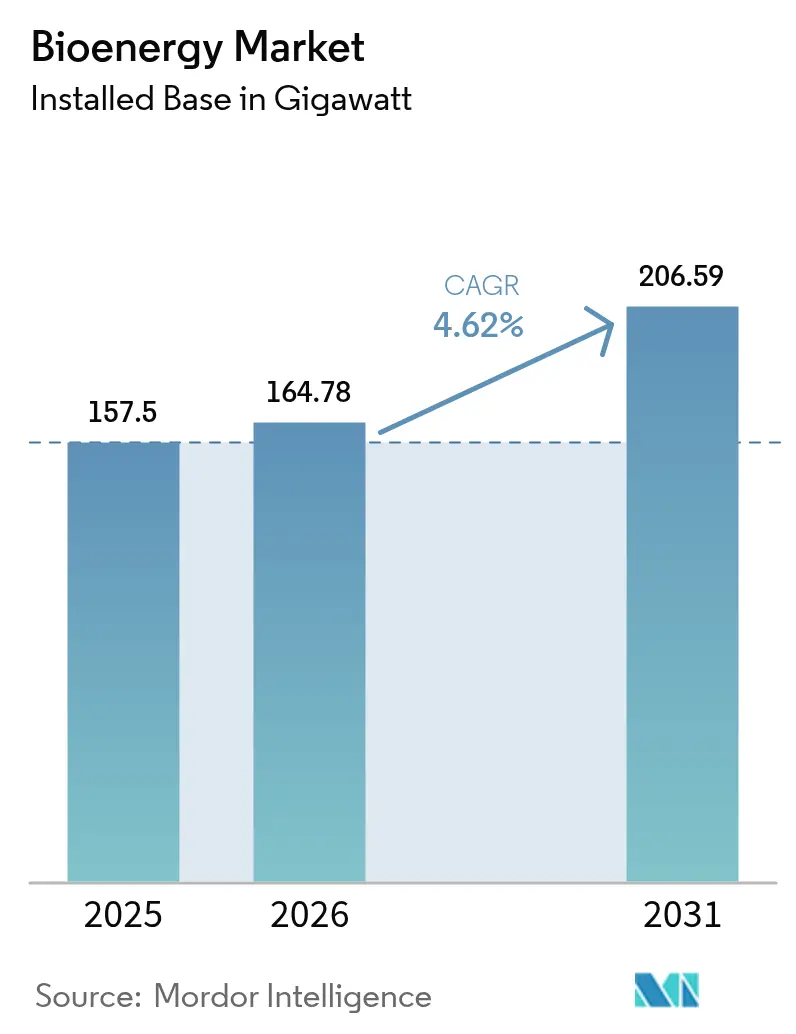

| Market Volume (2026) | 164.78 gigawatt |

| Market Volume (2031) | 206.59 gigawatt |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

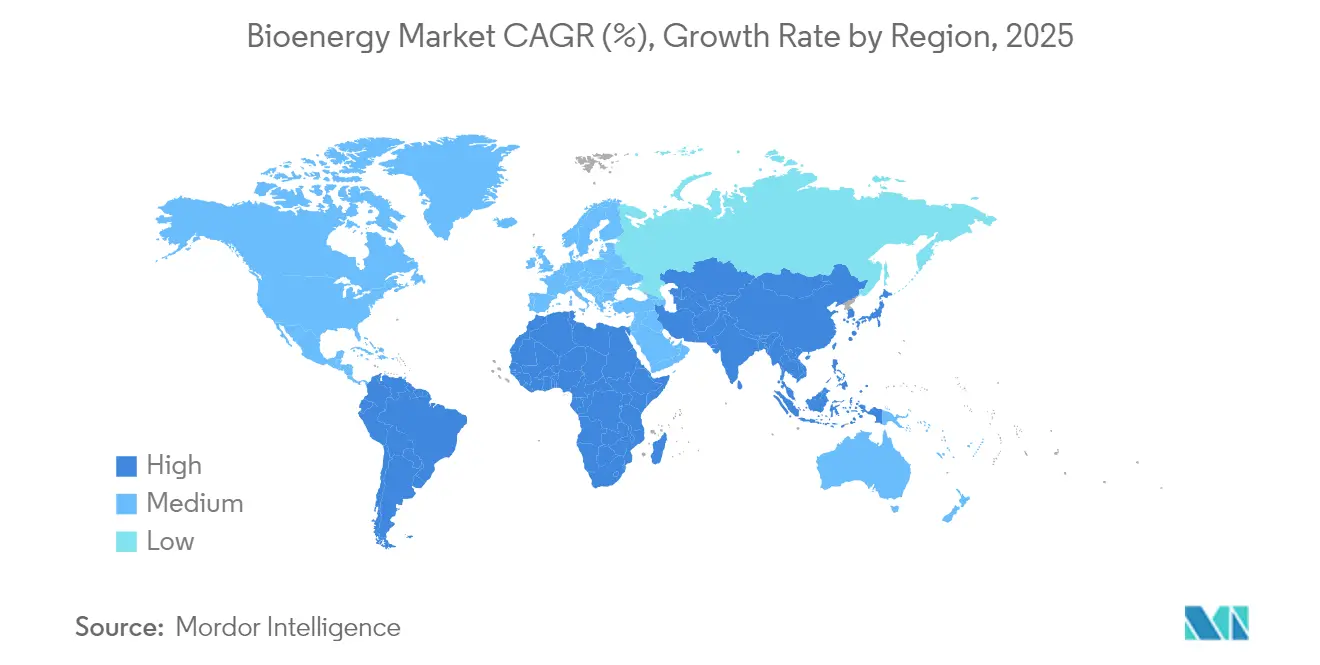

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioenergy Market Analysis by Mordor Intelligence

Bioenergy market size in 2026 is estimated at 164.78 gigawatt, growing from 2025 value of 157.5 gigawatt with 2031 projections showing 206.59 gigawatt, growing at 4.62% CAGR over 2026-2031.

Net-zero mandates, ample low-cost residues, and steady technology-driven declines in the levelized cost of electricity underpin expansion. Dispatchable generation capacity and the prospect of negative emissions through bioenergy with carbon capture and storage (BECCS) reinforce sector resilience even as variable renewables widen their footprint across power grids. Aggressive aviation and road-fuel blending rules, rising demand for firm industrial heat, and improved access to carbon markets further tighten the demand outlook. Financing barriers persist, yet project economics continue to improve as advanced gasification, pyrolysis, and anaerobic digestion plants scale faster than predicted only a few years ago. Policy alignment across electricity, fuels, and heavy-industry applications gives the bioenergy market a visibility horizon that still eludes several other renewable segments.

Key Report Takeaways

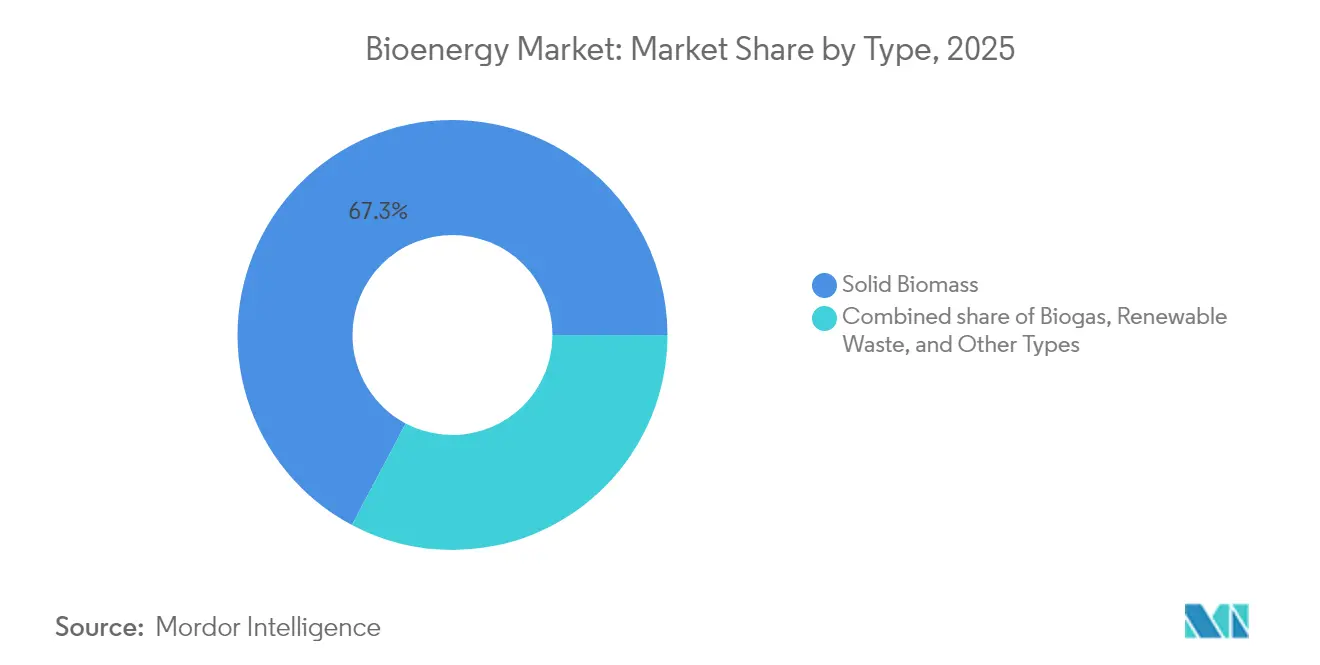

- By type, solid biomass held 67.25% of the bioenergy market share in 2025; biogas is the fastest-growing sub-segment at a 10.1% CAGR through 2031.

- By feedstock, forestry residues accounted for 39.70% of the bioenergy market size in 2025, and agricultural residues advanced at an 8.55% CAGR to 2031.

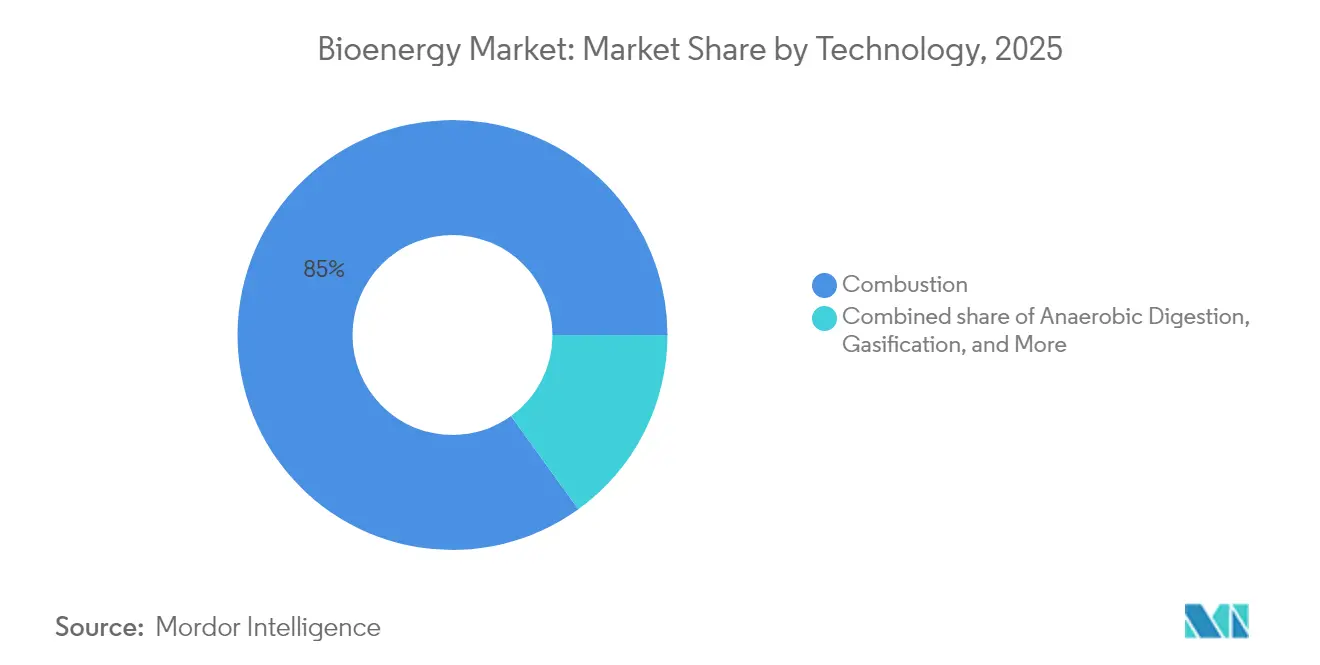

- By technology, combustion commanded 84.95% of 2025 capacity, but anaerobic digestion is projected to grow at a 11.7% CAGR through 2031.

- By application, heat generation retained 57.85% of the bioenergy market size in 2025, whereas transportation fuels exhibit the highest CAGR at 9.35% through 2031.

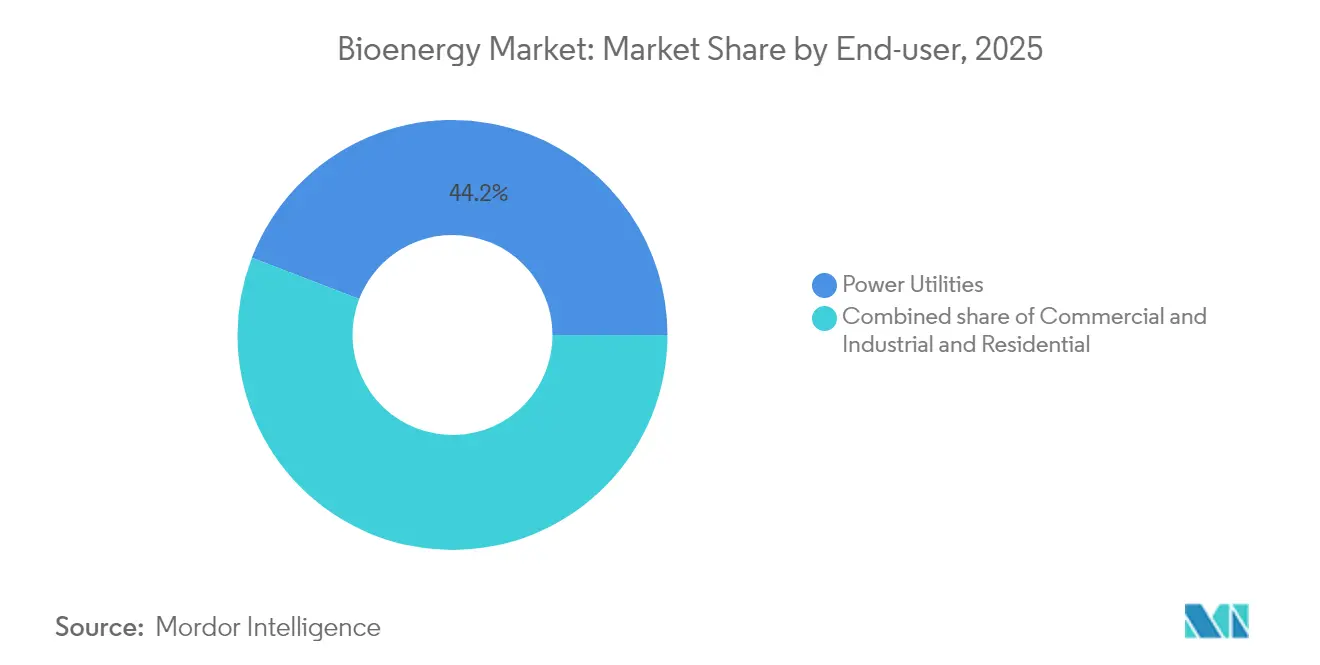

- By end-user, power utilities held a 44.15% share of the bioenergy market size in 2025, while commercial and industrial demand is projected to advance at a 8.75% CAGR between 2026-2031.

- By geography, Asia-Pacific led with a 43.30% revenue share in 2025 and is also forecast to expand at a 5.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bioenergy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Net-zero targets & renewable energy mandates | 1.2% | Global, with EU, US, and APAC leading implementation | Medium term (2-4 years) |

| Abundant low-cost agricultural & forestry residues | 0.9% | Global, concentrated in APAC, North America, and South America | Long term (≥ 4 years) |

| Technology-driven LCOE decline for advanced bioenergy | 0.8% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| BECCS incentives & negative-emissions revenue streams | 0.6% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

| Industrial off-take demand for dispatchable green heat/power | 0.5% | Europe, North America, and industrial APAC regions | Short term (≤ 2 years) |

| Monetisation of biogenic-CO₂ credits | 0.3% | Europe and North America primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Net-zero targets & renewable-energy mandates

Mandatory carbon-neutrality trajectories now cover more than 80% of global GDP, with the EU’s 90% net-emissions-reduction goal for 2040, the US Inflation Reduction Act’s funding tranches for advanced fuels, and India’s 20% ethanol blending target converging to lift long-term demand. Broad-based mandates extend to ReFuelEU’s 70% sustainable aviation fuel requirement by 2050 and the UK’s 2% sustainable aviation fuel obligation from 2025. The resulting multi-sector pull allows the bioenergy market to tap into electricity, heating, and transport segments simultaneously. Strong offtake visibility enables developers to structure 15- to 20-year contracts and improve debt tenors. The cross-industry appeal remains a clear competitive edge where intermittent renewable sources struggle to shoulder firm-capacity obligations.[1]European Commission, “Proposal for a 2040 Climate Target,” ec.europa.eu

Abundant low-cost agricultural & forestry residues

The US Department of Energy’s latest Billion-Ton Report shows that sustainable feedstock potential exceeds 1 billion t annually, dwarfing current consumption. India alone produces 180 million t of residues each year, with projected feedstock demand growth of 50% by 2030.[2]International Energy Agency, “World Energy Outlook 2024,” iea.org Evolving geopolitics underline resource-risk asymmetry: Europe’s wood-chip supply tightened after sanctions on Russian and Belarusian products, sending benchmark prices to multi-year highs. Consequently, proximity between feedstock clusters and processing hubs now dictates a meaningful share of total project cost. Companies licensing next-generation preprocessing systems to convert corn stover, rice straw, and palm residues into drop-in fuels illustrate how logistics‐driven value creation often outranks absolute resource abundance.

Technology-driven LCOE decline for advanced bioenergy

Hybrid solar-assisted pyrolysis reduces bio-oil production costs to EUR 18.68 per GJ and increases carbon efficiency to 90.7%, underscoring substantial cost savings compared to conventional thermal treatment. Direct biomass gasification plants reach 62% energy efficiency and outperform indirect bio-oil routes by 9 percentage points. Chemical-looping reforming increases hydrogen yields while reducing CO₂ intensity, and an optimized three-reactor configuration enables negative emissions profiles without compromising throughput. Such performance gains drop the bioenergy market’s mid-scale LCOE below combined-cycle natural-gas peaker tariffs in select regions. Technology convergence also supports modular deployment, enabling smaller developers to close funding rounds that were previously only accessible to utility-scale sponsors.

BECCS incentives & negative-emissions revenue streams

Formal recognition of greenhouse-gas removals reshapes the revenue stack. The UK is integrating BECCS credits into its domestic emissions-trading system, guaranteeing an offtake floor price for captured carbon. Corporate buyers such as Microsoft have signed multi-year removal contracts that now account for the bulk of verified BECCS credit sales in Scandinavia. A single BECCS-enabled plant is poised to remove up to 8 million t CO₂ annually while supplying baseload power. With the International Energy Agency estimating a requirement of 190 million t CO₂ removals by 2030 versus fewer than 2 million t today, early movers can lock in premium pricing and scale advantages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital intensity & financing hurdles | -0.8% | Global, particularly affecting emerging markets and smaller developers | Short term (≤ 2 years) |

| Fragmented feed-stock logistics & costs | -0.7% | Global, with acute challenges in developing regions and remote areas | Medium term (2-4 years) |

| Stricter ILUC & sustainability criteria | -0.5% | Global, with EU leading regulatory implementation | Medium term (2-4 years) |

| Competing low-cost battery storage eroding baseload value | -0.4% | Global, with faster impact in markets with high renewable penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capital intensity & financing hurdles

A single advanced biorefinery can require more than USD 2 billion in equity and debt, making pre-FID capital stacking a multiyear process. Although long-term offtake agreements mitigate merchant-price risks, nascent credit-enhancement frameworks in many developing economies still restrict local-currency debt. Investment costs for combined heat-and-power biomass plants range between EUR 3,410 and EUR 5,970 per kW, significantly higher than those for gas-fired alternatives. Therefore, sponsors increasingly syndicate risk through joint ventures with utilities, EPCs, and feedstock aggregators. Large corporates now anchor equity rounds, but smaller developers continue to face sizable hurdles, especially when carbon-credit revenue is not yet bankable.

Fragmented feedstock logistics & costs

Solid biomass accounts for up to 50% of the delivered energy cost in distributed projects. Seasonality, competing industrial uses, and evolving trade flows alter supply security. Sanctions-driven wood-chip shortages in Northern Europe illustrate how geopolitics can disrupt cost projections within quarters. Transport premiums for low-density residues can add USD 15-25 per t when delivery radii exceed 70 km, eroding margins for mid-scale power plants. Co-location near existing refineries and ports, investment in pelletization hubs, and vertically integrated sourcing models emerge as the favored mitigation pathways. However, the fragmented nature of agricultural residues in Asia and Africa still leaves smaller players exposed to volumetric and price volatility.[3]Cluster Collaboration, “Investment Cost Estimates for Biomass CHP,” clustercollaboration.eu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Solid Biomass Leads, but Biogas Is Catching Up

Solid biomass still does most of the heavy lifting, supplying 67.25% of global bioenergy in 2025 thanks to decades of investments in pellet mills, residue-handling equipment, and dependable combustion plants. A mature supply chain, from forestry by-products to purpose-grown crops, keeps fuel flowing in every major region. Yet the fastest mover right now is biogas. Backed by better anaerobic-digestion technology and tough new waste-recycling rules, biogas output is set to grow 10.1% a year through 2031. Germany’s latest biomass program even singles out flexible biogas units so they can keep supporting the grid once their first subsidies expire. Municipal solid-waste gasification and landfill-gas capture add more momentum, while early-stage options, such as algae fuels, remain in the lab for now. Together, these shifts show the market tilting from simple burn-and-boil systems toward cleaner, higher-value processes that squeeze more out of every ton of organic material.

By Feedstock: Forestry Waste Still Rules, but Farm Residues Are Rising Fast

Wood chips and sawmill scraps dominate feedstock supply, giving forestry residues a 39.70% share in 2025. Long-standing harvest routines and pellet logistics make this stream reliable and price-competitive. Farm residues, however, are gaining ground the quickest, expanding at an annual rate of 8.55% as policies favor turning crop waste into energy rather than leaving it to rot or burn in the field. The U.S. Billion-Ton Report points to more than 1 billion tons of untapped biomass, much of it corn stalks, wheat straw, and rice husks, waiting to be collected. Dedicated energy crops and sorted municipal waste add diversity, though Europe’s recent wood-chip shortage shows how geopolitics can rattle even well-established supply chains. That reality is pushing producers toward stricter certification and full traceability so buyers can trust both the origin and the sustainability of every load.

By Technology: Combustion Is Big, Anaerobic Digestion Is Booming

Traditional boilers still account for 84.95% of installed capacity because they are simple, proven, and quick to hook up to existing power or heat networks. But anaerobic digestion, the process behind most biogas plants, is growing at 11.7% a year. It turns household scraps, farm manure, and other organic waste into energy while also producing a fertilizer-rich digestate, giving operators two revenue lines instead of one. Gasification, fast pyrolysis, and fermentation are carving out niches in advanced fuels and chemicals, helped by breakthroughs like solar-assisted pyrolysis that cuts bio-oil costs below EUR 19 per gigajoule. The overall trend is clear: newer technologies aim to deliver more flexible products and stronger environmental performance than straight combustion plants ever could.

By Application: Heat Still Dominates, but Fuel Demand Is Surging

Supplying industrial and district heat remains bioenergy’s largest job, accounting for 57.85% of use in 2025. Many factories and city heating grids simply swap coal or oil burners for biomass and keep running with minimal fuss, an attractive option in regions with pricey fossil gas or high carbon fees. The headline growth, though, is in transportation fuels. Sustainable aviation fuel (SAF) and renewable diesel are on track to grow nearly 9.35% a year, spurred by airline and trucking mandates plus premium prices for low-carbon fuels. Electricity generation still commands a sizable slice, while combined-heat-and-power plants squeeze up to 90% total efficiency by recycling waste heat, an appealing proposition for energy-hungry industries.

By End User: Utilities on Top, Commercial Buyers Gaining Pace

Electric utilities took 44.15% of bioenergy in 2025, mainly through co-firing and dedicated biomass plants that help them hit renewable-portfolio targets without sacrificing grid stability. Corporate and industrial users are the fastest-growing customer base, expanding 8.75% a year as carbon prices climb and firms chase net-zero pledges. Pellet stoves are spreading in rural homes short on natural-gas access, while transport operators, from airlines to city bus fleets, are locking in long-term biofuel contracts; Southwest Airlines’ 20-year deal with USA BioEnergy is a recent example.

Geography Analysis

The Asia-Pacific region not only holds the largest regional share of 43.30% in 2025, but is also the fastest-growing, at a rate of 5.95% per year. India plans to triple biofuel use by the mid-2020s, backed by a vast pool of crop residues and clear government targets. China is rolling out full-suite biomass projects covering power, gas, and liquid fuels. Japan and South Korea rely more heavily on imports and advanced technologies, whereas Southeast Asia utilizes palm and rice waste for both domestic use and exports. The common thread is energy security: turning local waste into local energy while reducing the oil import bill.

Europe maintained a commanding 29.70% share of the bioenergy market in 2025, thanks to a decades-long alignment between climate ambition, feed-in tariffs, and sustainability criteria. Germany’s new biomass package, France’s capacity auctions, and the Netherlands’ incoming BECCS subsidy exemplify cohesive policy frameworks that maintain investment momentum. Yet growth is moderating as land-use constraints take effect, wood-chip imports become more stringent, and competing ecological priorities challenge further large-scale forest harvesting. Market participants, therefore, pivot toward higher-value niches, including negative-emission power and industrial heat projects that optimize limited feedstock through high-efficiency conversion systems.

North America holds third place in terms of capacity, yet leads in advanced biofuel innovation. The United States accounts for the lion’s share of global ethanol and renewable-diesel volumes, leveraging its corn and soy supply chains alongside federal production and blending credits. A growing pipeline of SAF projects positions the country to remain at the forefront of aviation-fuel decarbonization. Canada leverages vast forestry resources and provincial clean-fuel standards to attract large-scale gasification and RNG facilities, often in partnership with First Nations. Mexico’s emerging mandates create opportunities for retrofitting sugarcane mills with bagasse cogeneration, although policy clarity will determine near-term pace.

Competitive Landscape

The bioenergy market remains moderately concentrated, with no single player holding a global share exceeding 10%. Incumbent utilities and oil majors integrate upstream feedstock assets, proprietary conversion technologies, and long-term distribution channels to capture scale synergies. Strategic moves include Copenhagen Infrastructure Partners’ joint venture to build Danish biogas plants and BP’s USD 1.4 billion acquisition to secure full ownership of Brazil’s largest biofuels producer. Developers that lock in dedicated biomass supply gain cost predictability and resilience against price shocks, a decisive differentiator as feedstock markets tighten.

Technology leadership is another axis of competition. Firms advancing modular gasification, chemical looping, and solar-assisted pyrolysis attract venture and strategic capital. Kvasir Technologies’ lignocellulose-to-marine-fuel pathway, for example, secured multi-million-euro backing to scale pilot output. Large equipment vendors, such as Mitsubishi Heavy Industries, embed carbon-capture add-ons in boiler packages, enabling customers to future-proof their assets against stricter emissions rules. Mid-tier players rely on regional specialization—such as wood-pellet exports from the Southeastern United States or rice-husk CHP units in South Asia—to defend their margins.

Partnership models are proliferating. Airlines guarantee minimum bio-jet purchases, heavy-industry offtakers co-invest in on-site plants, and municipalities allocate waste streams under long-term concessions. Such vertically aligned contracts shorten payback periods and mitigate demand risk. On the financing front, green bonds and sustainability-linked loans are now common, provided borrowers commit to verifiable emissions cuts and feedstock traceability. Competition increasingly hinges on proving end-to-end sustainability and securing revenue diversification across power, fuels, heat, and carbon credits.

Bioenergy Industry Leaders

Orsted A/S

Drax Group plc

Fortum Oyj

Enviva Inc.

Mitsubishi Heavy Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: U.S. Department of Energy allocates USD 12 million to scale integrated biorefinery technologies aimed at producing sustainable aviation fuels and biochemicals.

- April 2025: Energy and environmental agencies direct USD 6 million from the Inflation Reduction Act to three advanced biofuel pilots, including a biogenic-CO₂-to-jet-fuel pathway.

- February 2025: Comstock Fuels extends licensing to Malaysia for Bioleum refineries expected to yield 280 million gal y of renewable fuels from lignocellulosic biomass.

- January 2025: Emerging Fuels Technology and Highbury Energy sign a master license for a wood-waste-to-fuel project in Ontario targeting 20 million L y production.

Global Bioenergy Market Report Scope

Bioenergy is a source of energy from the organic material that drives up plants, known as biomass. Biomass contains carbon absorbed by plants through photosynthesis. It is a form of renewable energy derived from recently living organic materials known as biomass, which can be utilized to deliver transportation fuels, heat, electricity, and products.

The bioenergy market is segmented by type, application, and geography. By type, the market is segmented as Biodiesel, Bioethanol, and Biogas. By application, the market is segmented as Power Generation, District Heating, Transportation, Industrial Applications, and other applications. The report also covers the market size and forecasts across major regions. For each segment, the market size and forecasts have been done based on installed capacity.

By Type

| Solid Biomass |

| Biogas |

| Renewable Waste |

| Other Types |

By Feedstock

| Agricultural Residues |

| Forestry Residues |

| Energy Crops |

| Municipal Solid Waste |

By Technology

| Combustion |

| Gasification |

| Fast Pyrolysis |

| Anaerobic Digestion |

| Fermentation |

| Other Technologies |

By Application

| Electricity Generation |

| Heat Generation |

| Transportation Fuel |

| Combined Heat & Power (CHP) |

By End-user

| Power Utilities |

| Commercial and Industrial |

| Residential |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Sweden | |

| Finland | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Chile | |

| Colombia | |

| Uruguay | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Ethiopia | |

| Sudan | |

| Rest of Middle East and Africa |

| By Type | Solid Biomass | |

| Biogas | ||

| Renewable Waste | ||

| Other Types | ||

| By Feedstock | Agricultural Residues | |

| Forestry Residues | ||

| Energy Crops | ||

| Municipal Solid Waste | ||

| By Technology | Combustion | |

| Gasification | ||

| Fast Pyrolysis | ||

| Anaerobic Digestion | ||

| Fermentation | ||

| Other Technologies | ||

| By Application | Electricity Generation | |

| Heat Generation | ||

| Transportation Fuel | ||

| Combined Heat & Power (CHP) | ||

| By End-user | Power Utilities | |

| Commercial and Industrial | ||

| Residential | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Sweden | ||

| Finland | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Chile | ||

| Colombia | ||

| Uruguay | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Ethiopia | ||

| Sudan | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global bioenergy market?

The bioenergy market reached 164.78 GW in 2026 and is projected to hit 206.59 GW by 2031.

Which region is growing fastest in the bioenergy market?

Asia-Pacific shows the highest growth, with a 5.95% CAGR forecast through 2031 owing to strong biofuel mandates and expanding biomass infrastructure.

Which feedstock category holds the largest bioenergy market share?

Forestry residues account for 39.70% of capacity in 2025, supported by robust collection networks and sustainability policies.

Why is BECCS important for the bioenergy industry?

BECCS enables negative emissions, unlocking carbon-credit revenue and supporting net-zero trajectories while delivering dispatchable renewable energy.

What are the main challenges facing new bioenergy projects?

High capital intensity and fragmented feedstock logistics create financing and supply-chain hurdles, particularly in emerging markets.

Which application segment is expanding fastest?

Transportation fuels, particularly sustainable aviation fuel and renewable diesel, are advancing at a 9.35% CAGR due to strict blending mandates and corporate decarbonization goals.

Page last updated on: