Global Solvent Evaporation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

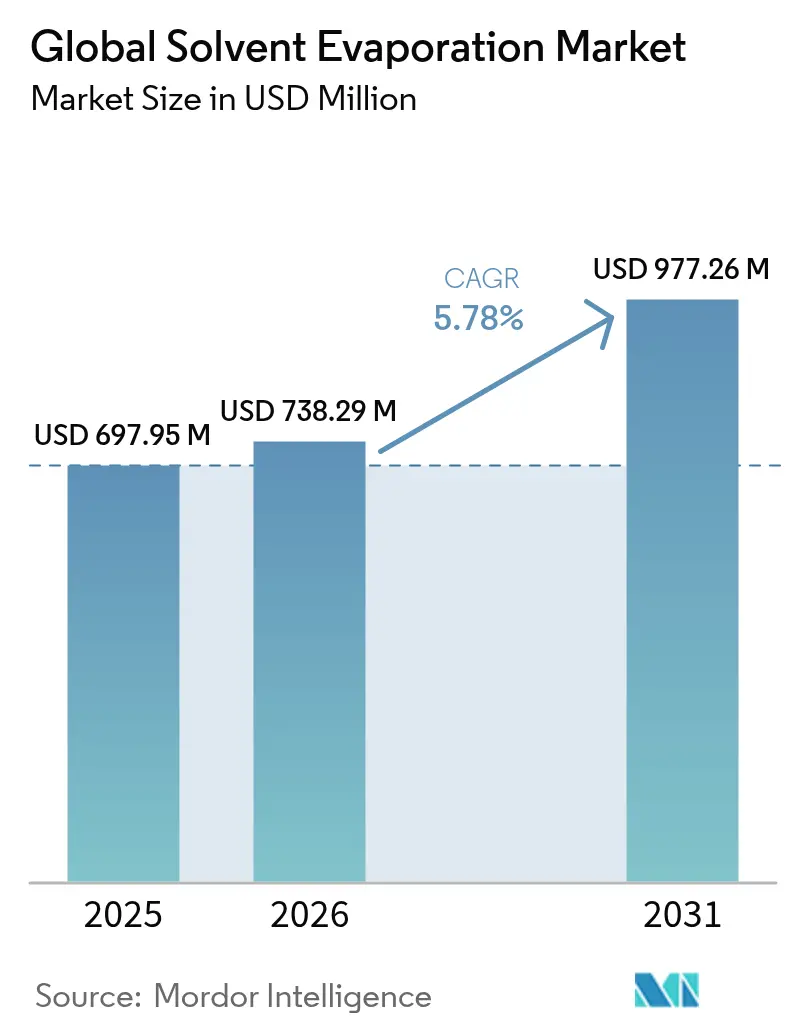

| Market Size (2026) | USD 738.29 Million |

| Market Size (2031) | USD 977.26 Million |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

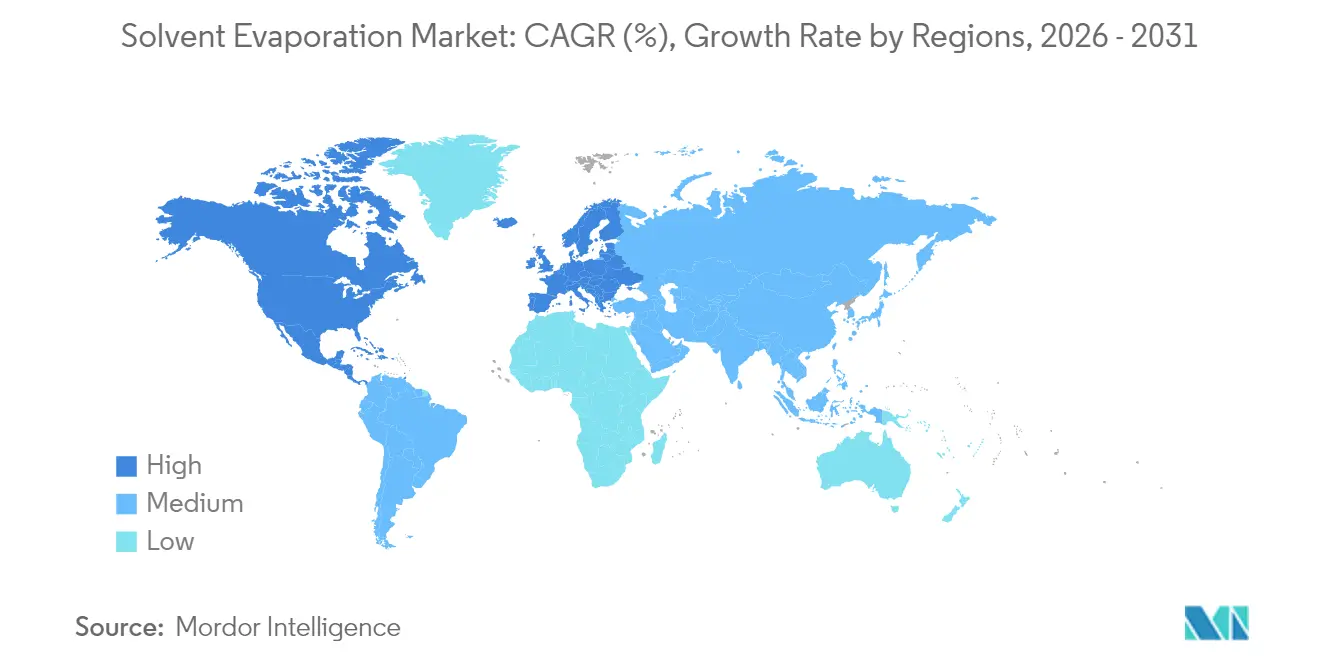

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

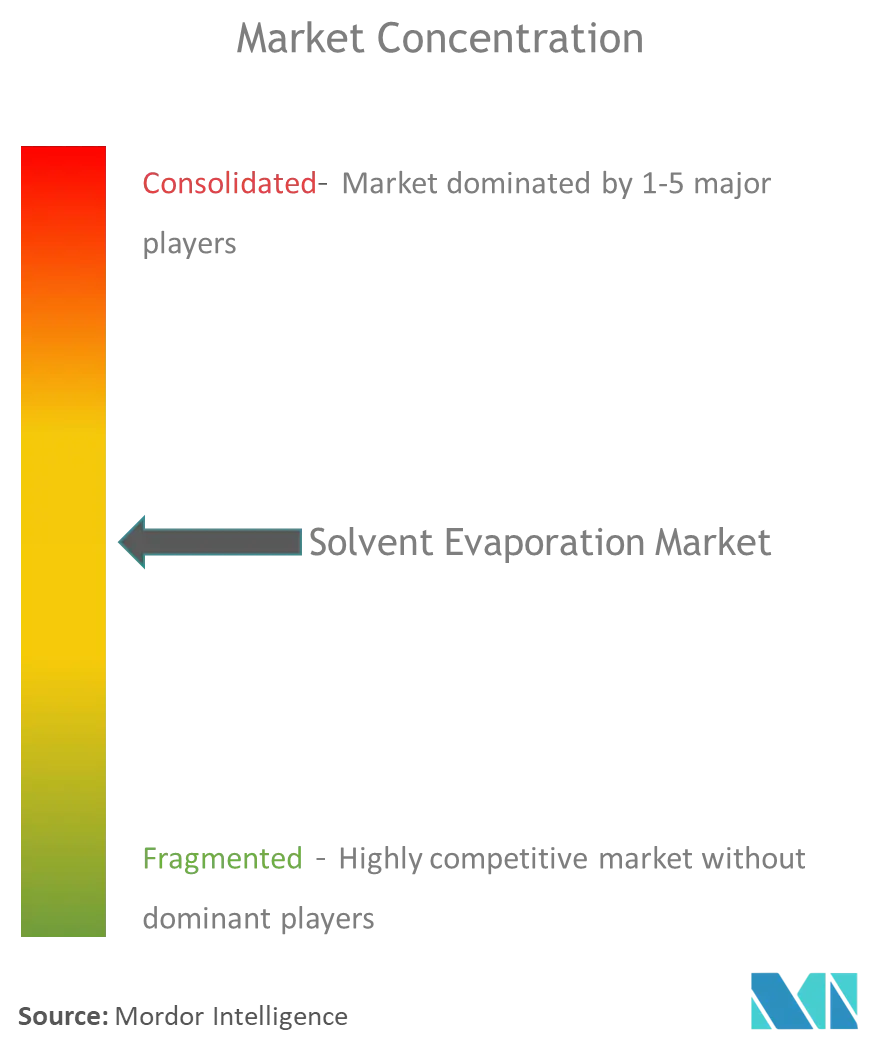

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Solvent Evaporation Market Analysis by Mordor Intelligence

solvent evaporation market size in 2026 is estimated at USD 738.29 million, growing from 2025 value of USD 697.95 million with 2031 projections showing USD 977.26 million, growing at 5.78% CAGR over 2026-2031. This trajectory mirrors sustained capital allocation by pharmaceutical developers eager to streamline drug-discovery workflows, where solvent evaporation steps often define the overall cadence of synthesis and analytical testing. Rising demand for large-molecule biologics is reshaping equipment specifications toward gentler temperature-vacuum profiles, while closed-loop recovery designs gain favor amid tightening volatile-organic-compound (VOC) regulations. High-throughput screening protocols are reinforcing the need for automated parallel processing, and laboratories across North America rapidly upgrade infrastructure under recent National Institutes of Health (NIH) instrumentation grants that cover up to USD 350,000 per facility. Environmental, social, and governance (ESG) frameworks are pushing end users to prefer systems that document solvent recovery rates above 95% and integrate real-time monitoring features for audit readiness.

Key Report Takeaways

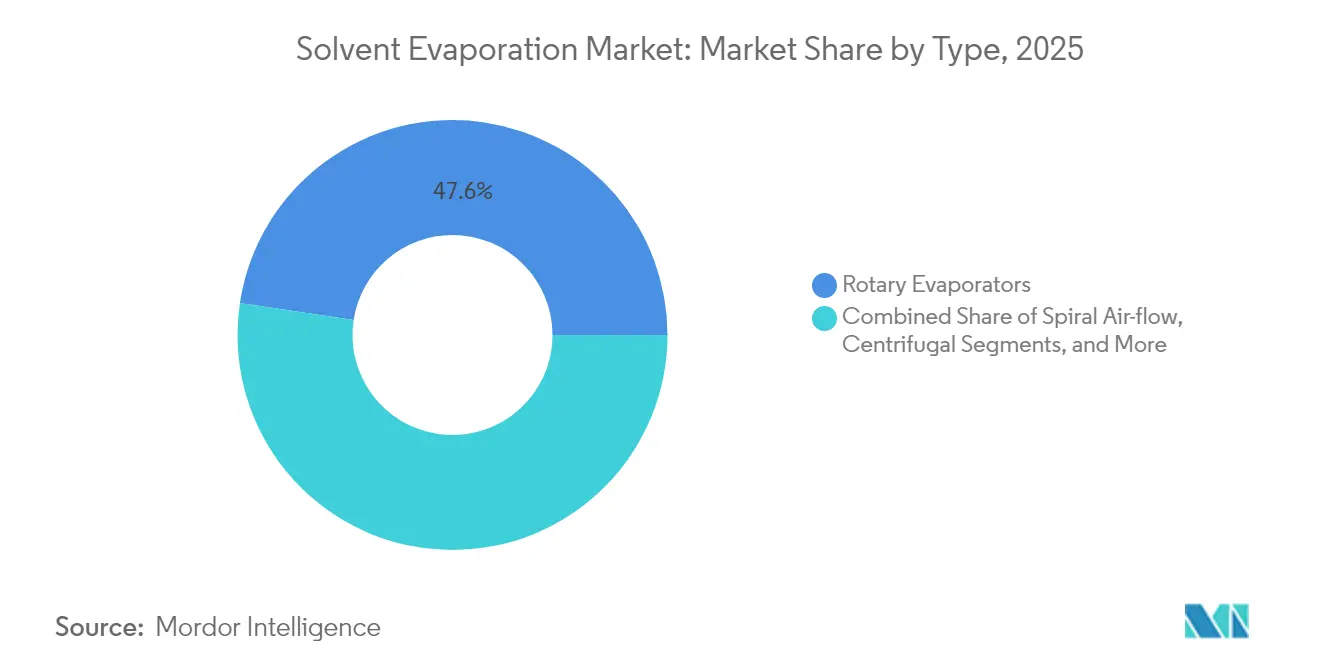

- By product type, rotary evaporators led with 47.62% of solvent evaporation market share in 2025, whereas centrifugal and vacuum-centrifugal systems are forecast to accelerate at a 6.03% CAGR through 2031.

- By end user, the pharmaceutical and biopharmaceutical segment accounted for 58.15% of the solvent evaporation market size in 2025, while diagnostic and clinical laboratories are poised to grow at a 6.41% CAGR to 2031.

- By geography, North America commanded 43.30% revenue share of the solvent evaporation market in 2025, yet Asia-Pacific is projected to register the fastest 6.74% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Solvent Evaporation Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding pharmaceutical & biotech R&D budgets | +1.2% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Shift toward large-molecule biologics requiring gentle evaporation | +0.9% | Global, led by North America & Asia-Pacific | Long term (≥ 4 years) |

| Stringent purity standards in analytical laboratories | +0.8% | Global, stricter in North America & Europe | Short term (≤ 2 years) |

| High-throughput screening boosting demand for parallel evaporation | +0.7% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Closed-loop solvent recovery adoption for ESG compliance | +0.6% | Global, regulatory-driven in developed markets | Long term (≥ 4 years) |

| Rapid growth of cannabis extraction laboratories | +0.4% | North America, selective European markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Pharmaceutical & Biotech R&D Budgets

Federal stimulus programs and record private financing have intensified the pace of laboratory modernization, making automated solvent removal modules a centerpiece of next-generation synthesis cells. Continuous-manufacturing lines at Pfizer and Eli Lilly now depend on intelligent rotary platforms that sustain unattended operation for several shifts, shortening time to regulatory submission. Process-analytical-technology (PAT) sensors embedded in condensers automatically adjust pressure and bath temperature, boosting reproducibility and cutting operator intervention. Demand is also supported by reshoring incentives that encourage U.S. and European plants to rely less on overseas intermediates, which further elevates equipment purchase volumes. Manufacturers reporting PAT-enabled evaporators cite up to 30% fewer batch failures, translating directly into cost-avoidance returns that strengthen purchasing rationales. As NIH and European Research Council grants continue to prioritize scalable automation, solvent evaporation market demand is set to remain firmly positive through the forecast horizon.

Shift Toward Large-Molecule Biologics Requiring Gentle Evaporation

Monoclonal antibody pipelines require evaporation temperatures below 40 °C to prevent protein denaturation, driving adoption of low-pressure chambers paired with precise condenser cooling loops. Spray-drying formats that handle viscous biologic feeds already demonstrate powder yields above 90%, providing an alternative to traditional freeze-drying without compromising stability. Single-use evaporation bags integrated with sterile connectors minimize cleaning validation effort, a benefit that aligns with biologics’ stringent sterility expectations. Biotage’s V-10 Touch unit reaches evaporation rates of 0.5 mL/min for dimethyl sulfoxide while maintaining batch-to-batch temperature deviations within ±1 °C. Demand is further amplified by the surge in high-concentration subcutaneous formulations that tolerate only narrow moisture windows, necessitating sensors that verify endpoints in real time. Collectively, these requirements underpin the solvent evaporation market’s migration toward vacuum centrifugal and parallel platforms optimized for thermally fragile macromolecules.

Stringent Purity Standards in Analytical Laboratories

Updated Environmental Protection Agency (EPA) rules now cap permissible methylene chloride exposure at an 8-hour-time-weighted average of 2 ppm, compelling laboratories to install advanced containment and condensation arrays [1]United States Environmental Protection Agency, “Risk Management Rule for Methylene Chloride,” epa.gov. Cannabis testing facilities in states like Colorado must validate residual solvent levels under United States Pharmacopeia <467>, raising throughput demands for nitrogen blow-down systems able to handle diverse matrices while limiting cross-contamination. Automated workstations that couple evaporation with liquid-handling robotics efficiently achieve sub-ppm detection limits and generate electronic logs that satisfy accreditation bodies. Laboratory directors also emphasize that closed-cupboard designs reduce operator solvent exposure, supporting Occupational Safety and Health Administration (OSHA) goals for safer workplace environments. Adoption has accelerated since 2024, with vendors documenting double-digit growth in North American shipments of fully enclosed evaporators equipped with integrated recovery flasks. Pure-grade outputs enable consistent chromatographic baselines, cutting retest rates and supporting tighter batch-release timelines across pharmaceutical quality-control labs.

High-Throughput Screening Boosting Demand for Parallel Evaporation

Quantitative screening initiatives routinely test millions of concentration-response curves, a throughput that manual solvent removal cannot match. The NIH Chemical Genomics Center now combines 384-well plates with parallel evaporators able to finish solvent exchange within 8 minutes per microplate, upholding compound integrity for downstream assays [2]National Institutes of Health, “Instrument Upgrade Funding Opportunity,” nih.gov. Vendors such as Labconco offer 96-position centrifugal units that maintain sample-to-sample temperature deviations below 2 °C, ensuring reliable IC50 values. In practice, automated evaporators shorten medicinal-chemistry cycle times by 60%, freeing bench scientists for design-make-test analytics and boosting overall productivity. Scheduling algorithms built into control software optimize order of execution based on boiling point and volume, smoothing energy demand inside busy screening suites. As more big-pharma campuses retrofit legacy buildings, demand for modular racks capable of future channel expansion continues to strengthen the solvent evaporation market outlook.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operating cost of advanced systems | -0.8% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Tightening VOC-emission regulations & certification costs | -0.6% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Supply-chain volatility in vacuum-pump components | -0.5% | Global, acute in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Shortage of skilled operators in emerging regions | -0.4% | Asia-Pacific & Middle East, selective African markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Operating Cost of Advanced Systems

State-of-the-art rotary stations outfitted with analytics, remote monitoring, and vacuum-pump redundancy often surpass USD 100,000 per unit, while high-throughput automated banks can breach USD 250,000, impeding access for smaller institutions. Annual service contracts covering calibration, pump oil, and membrane replacements absorb 15-20% of a laboratory’s equipment budget. Energy-efficient mechanical-vapor-recompression modules promise 30% savings but require steeper upfront fees, complicating cost-benefit calculations. Facilities that lease instead of purchase report higher five-year spending, owing to bundled service premiums and restrictive upgrade clauses. Training costs also mount; operators need specialized instruction in vacuum control, solvent-specific temperature mapping, and software validation, lengthening the payback period. Consequently, capital-constrained buyers in emerging markets gravitate toward tier-two suppliers that deliver essential functionality without premium automation, tempering solvent evaporation market penetration rates in price-sensitive geographies.

Tightening VOC-Emission Regulations & Certification Costs

EPA leak-detection rules for synthetic-organic-chemical facilities require quarterly monitoring and rapid repair protocols, adding USD 50,000–100,000 to annual compliance outlays for mid-size laboratories. New York now limits cleaning solutions to ≤ 25 g/L VOC content, forcing users to retrofit or replace evaporators that cannot isolate vapors effectively. Certification demands span third-party emissions testing, process-safety management documentation, and continuous monitoring hardware, often consuming 5–10% of operational budgets. Global producers face overlapping jurisdictional rules, meaning a single site sometimes subjects the same evaporator to multiple audits, each with unique paperwork trails. Compliance consultants report that environmental-impact statements now take twice as long to complete compared with 2023, underscoring the escalating administrative burden. While these measures enhance sustainability, they slow equipment-adoption cycles and raise cost barriers, dampening near-term solvent evaporation market expansion despite strong underlying demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Rotary Systems Dominate Despite Centrifugal Innovation

Rotary evaporators captured 47.62% of solvent evaporation market share in 2025, anchored by their ability to process everything from milligrams of synthesis intermediates to liters of botanical extracts. Their enduring popularity stems from straightforward flask rotation, dependable mechanical seals, and broad solvent compatibility. Premium models now offer automatic bath refilling, condenser-chiller synchronization, and intuitive touchscreens, making them attractive even within high-throughput production suites that traditionally relied on centrifugal formats. The nitrogen blow-down subsegment holds favor among food-safety and environmental laboratories that require gentle heating profiles, while spiral air-flow designs serve specialized medicinal-chemistry workflows demanding near-zero cross-contamination. Centrifugal and vacuum-centrifugal systems are nevertheless the fastest-growing subsegment, recording a 6.03% CAGR, because they evaporate multiple microplates in parallel, an essential requirement for combinatorial chemistry and fragment-based lead discovery. Vendors focus heavily on reducing footprint and noise, two operational factors that matter in dense laboratory clusters. Looking forward, microfluidic evaporation chips capable of on-line solvent exchange could blur traditional boundaries between preparative evaporation and analytical injection, opening fresh revenue lanes inside the solvent evaporation market.

Second-generation centrifugal platforms increasingly incorporate real-time infrared sensors that halt cycles once residual-volume targets are met, minimizing over-drying risk and preserving analyte integrity. High-viscosity biologic feeds also benefit from programmable acceleration ramps that prevent foaming—an issue historically associated with rotary units at low pressures. Industry feedback points to maintenance as a purchasing criterion; magnetic-bearing vacuum pumps reduce oil change frequency, cutting downtime and improving total cost of ownership. Competitive differentiation has thus migrated from pure throughput metrics to holistic workflow integration, with suppliers offering software development kits that allow seamless data transfer into electronic lab notebooks. These enhancements collectively reinforce centrifugal equipment’s trajectory toward broader adoption, yet rotary platforms are expected to retain the largest absolute revenue pool through 2031 because of their entrenched installed base within academia and pilot-scale production.

By End User: Pharmaceuticals Lead While Diagnostics Accelerate

The pharmaceutical and biopharmaceutical sector accounted for 58.15% of the solvent evaporation market size in 2025, underpinned by vertically integrated discovery-to-manufacturing pipelines that rely heavily on solvent removal at each stage. Continuous-manufacturing sites equip production lines with automated rotary stations connected to process-control historians, enabling real-time deviation tracking and facilitating faster release of finished batches. Bioprocess engineers highlight that improvements in condenser surface area and compressor efficiency have cut cycle times by 20%, freeing capacity for pipeline expansion. Academic spin-offs also use benchtop evaporators to shorten medicinal-chemistry loops, often scaling from sub-gram outputs to pilot quantities without changing core technology.

Diagnostic and clinical laboratories represent the fastest-rising customer group, posting a projected 6.41% CAGR to 2031. Growth derives from mass-spectrometry-based assays that demand stringent sample-pretreatment, where automated blow-down or centrifugal units guarantee reproducible evaporation endpoints across diverse biological matrices. Companion-diagnostic programs blur the line between pharma and diagnostics, requiring instruments that satisfy both Good Manufacturing Practice (GMP) and Clinical Laboratory Improvement Amendments (CLIA) documentation. Cannabis-testing laboratories add an additional demand spike, as state regulations impose sub-ppm residual-solvent thresholds necessitating precise evaporation control. Laboratories now favor units featuring bar-code tracking and audit-trail logging to satisfy accreditation bodies and meet chain-of-custody requirements, strengthening the solvent evaporation market’s long-term demand profile.

Geography Analysis

North America retained 43.30% of global revenue in 2025, with spending bolstered by NIH infrastructure grants that reimburse up to USD 350,000 for laboratory upgrades aimed at accelerating public-health innovation. Early adoption of continuous production lines by Pfizer and Eli Lilly created demonstration sites that validated cost and regulatory advantages, encouraging smaller firms to replicate similar configurations. The region’s robust cannabis-testing sector demands closed-loop evaporation systems that can reclaim ≥ 95% solvent, ensuring both regulatory compliance and cost savings. Stringent VOC rules issued by the EPA make enclosed condensers and activated-carbon scrubbing a default specification across new installations, even though compliance escalates annual operating budgets by USD 50,000-100,000.

Europe remains an influential contributor, supported by long-standing pharmaceutical clusters in Germany, Switzerland, and Ireland that maintain high capital-expenditure on laboratory innovation. Stringent climate legislation and circular-economy commitments spur adoption of solvent recycling centers capable of pervaporation, fractionation, and distillation, reinforcing market pull for high-efficiency evaporation modules. Academic-industry consortia fund pilot plants dedicated to continuous crystallization, driving interest in evaporators capable of seamless integration with downstream aqueous quench and drying units. Although budget restraint in selected economies moderates premium equipment uptake, collective adherence to EU Green Deal objectives ensures ongoing refurbishment cycles emphasizing lower energy footprints.

Asia-Pacific exhibits the fastest anticipated 6.74% CAGR, driven by China’s and India’s initiatives to achieve GMP parity with Western peers and amplify biologics output. Chinese developers allocate substantial capital toward single-use evaporation skids designed for sterile operations, mirroring their strategy to reach global monoclonal-antibody markets within the decade. Indian contract-development and manufacturing organizations (CDMOs) expand pilot suites for mRNA and viral-vector platforms, relying on vacuum-centrifugal evaporators that mitigate thermal degradation. Supply-chain disruptions sparked by geopolitical tensions motivate regional manufacturers to localize component sourcing, encouraging joint ventures with pump and chiller specialists to secure capacity. Despite legal complexities introduced by China’s Anti-Espionage Law, multinational suppliers still view Asia-Pacific as a growth engine for the solvent evaporation market because of strong domestic demand and export ambitions.

Competitive Landscape

The solvent evaporation market shows moderate fragmentation, with competition balancing between established conglomerates and nimble specialist firms. Thermo Fisher Scientific’s USD 4.1 billion acquisition of Solventum’s purification and filtration division in 2025 broadens its bioprocess hardware portfolio and is projected to yield USD 125 million in adjusted operating income by year five [3]Thermo Fisher Scientific, “Thermo Fisher to Acquire Solventum’s Purification and Filtration Business,” thermofisher.com. The move highlights a wider consolidation trend in which scale enables suppliers to bundle evaporators with downstream filtration, chromatography, and fill-finish skids, offering customers integrated procurement pathways.

Innovation focus has shifted to sustainability features such as magnetic-bearing vacuum pumps, hydrophobic condenser coatings, and advanced heat-pump chillers that collectively slash energy usage. Biotage, for instance, markets phase-separation technology that handles high-boiling solvents, cutting post-process waste by 40% and delivering measurable ESG metrics attractive to publicly traded pharmaceutical customers. Intellectual-property filings reveal heightened activity in sensor fusion, where infrared moisture probes interface with predictive algorithms to prevent over-drying. Suppliers also develop software development kits to ensure instrument data flow into electronic lab notebooks and quality-management systems, features increasingly decisive in procurement scored under laboratory digitalization strategies.

White-space opportunities emerge around continuous crystallization lines, advanced biologic unit operations, and microfluidic diagnostic cartridges—all of which require fine-tuned evaporation modules. Component OEMs specializing in perfluoroelastomer seals, corrosion-resistant vacuum pumps, or low-global-warming-potential refrigerants position themselves as indispensable partners to system integrators. Competitive intensity remains highest in North America and Europe, where regulatory scrutiny and buyer sophistication encourage premium solutions. In emerging regions, price-optimized models from regional brands co-exist alongside imported high-specification units, reflecting varied purchasing power yet collectively advancing solvent evaporation market penetration.

Global Solvent Evaporation Industry Leaders

Biotage

Buchi Labortechnik AG

Heidolph Instruments GmbH & CO. KG

Labconco

Yamato Scientific Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thermo Fisher Scientific reached a definitive agreement to acquire Solventum’s purification and filtration business for USD 4.1 billion, expanding its bioproduction equipment portfolio.

- February 2023: ATS Automation Tooling Systems Inc. entered a definitive agreement to acquire SP Industries, Inc., a designer and manufacturer of biopharma processing and life-science laboratory equipment.

- June 2022: BÜCHI Labortechnik launched the Mini Spray Dryer S-300, featuring fully automated operation and enhanced safety for handling organic solvents.

- February 2022: Biotage introduced the TurboVap 96 Dual well-plate evaporator, offering two independently controlled evaporation compartments for high-throughput workflows.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the solvent evaporation market as revenues generated from laboratory-grade instruments that remove volatile solvents from small to medium liquid samples through rotary, centrifugal, nitrogen blow-down, spiral airflow, or automated workstation configurations, plus their directly attached glassware and condensers. According to Mordor Intelligence, demand is tracked at the point of original equipment sale to research, diagnostic, and production labs worldwide.

Scope exclusion: Industrial multi-effect or falling-film evaporators used for food, wastewater, or bulk chemical processing lie outside this definition.

Segmentation Overview

- By Type

- Nitrogen Blow-down Evaporators

- Rotary Evaporators

- Centrifugal / Vacuum Centrifugal Evaporators

- Spiral Air-flow / Parallel Evaporators

- Intelligent Automated Evaporation Workstations

- By End User

- Pharmaceutical & Biopharmaceutical Industry

- Research & Academic Institutes

- Diagnostic & Clinical Laboratories

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with application scientists at pharmaceutical firms, procurement managers in North America, Europe, and Asia-Pacific, and service engineers at leading instrument distributors. These conversations validated duty-cycle assumptions, regional price spreads, and emerging automation preferences that secondary data could not fully capture.

Desk Research

We began with open datasets from regulators and trade bodies, US FDA 510(k) listings, European Medicines Agency device submissions, and UN Comtrade HS 841940 export flows, which reveal installed bases and shipment trends. ScienceDirect and PubMed articles showed throughput norms for drug-discovery sample prep, while annual reports from listed lab-equipment makers clarified average selling prices. Our team also pulled company financials via D&B Hoovers and cross-checked news on capacity expansions through Dow Jones Factiva. These sources build the foundational demand pool; however, they are illustrative, not exhaustive, of the wider desk research consulted.

Market-Sizing & Forecasting

A top-down reconstruction from production and trade data established the 2025 baseline, which is then sense-checked with selective bottom-up inputs such as sampled ASP multiplied by installed units for rotary and centrifugal systems. Key variables like R&D spending by pharma, biotech patent filings, instrument replacement cycles, laboratory automation adoption rates, and regional CAPEX indices feed the model. Forecasts rely on multivariate regression blended with scenario analysis to reflect funding swings in drug-discovery pipelines; gaps in bottom-up estimates are bridged by price-volume proxies from dealer channel checks.

Data Validation & Update Cycle

Outputs pass through variance screening against independent shipment tallies and previously published market signals. An analyst peer review precedes sign-off, and the model is refreshed every twelve months, with interim updates if major recalls, regulation, or macro disruptions occur.

Why Our Solvent Evaporation Baseline Commands Confidence

Published figures often differ because firms choose dissimilar base years, bundle accessories inconsistently, or project growth from unverified uptake rates. By anchoring scope to laboratory-scale instruments only and overlaying real shipment data with verified price corridors, Mordor delivers a balanced, repeatable baseline that decision-makers can trust.

Taken together, the comparison shows that while external estimates swing widely, our disciplined scope setting, mixed-method modeling, and annual refresh cadence yield a dependable reference point for planning investments in solvent evaporation technologies.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 697.95 M (2025) | Mordor Intelligence | - |

| USD 694 M (2024) | Regional Consultancy A | Older base year and excludes intelligent workstations, which compresses future value |

| USD 588.45 M (2022) | Industry Association B | Uses conservative ASPs and omits service-kit revenues, understating size |

| USD 628.37 M (2023) | Trade Journal C | Reports global shipments but applies uniform currency conversion without inflation adjustment |

Taken together, the comparison shows that while external estimates swing widely, our disciplined scope setting, mixed-method modeling, and annual refresh cadence yield a dependable reference point for planning investments in solvent evaporation technologies.

Key Questions Answered in the Report

What is the current Global Solvent Evaporation Market size?

The solvent evaporation market stands at USD 738.29 million in 2026 and is forecast to reach USD 977.26 million by 2031 at a 5.78% CAGR.

Who are the key players in Global Solvent Evaporation Market?

Biotage, Buchi Labortechnik AG, Heidolph Instruments GmbH & CO. KG, Labconco and Yamato Scientific Co. are the major companies operating in the Global Solvent Evaporation Market.

Which is the fastest growing region in Global Solvent Evaporation Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which product type holds the largest share?

Rotary evaporators command 47.62% of revenue, driven by broad solvent compatibility and entrenched use across synthesis and extraction workflows.

Page last updated on: