Size and Share of Big Data Market In Automotive Industry

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

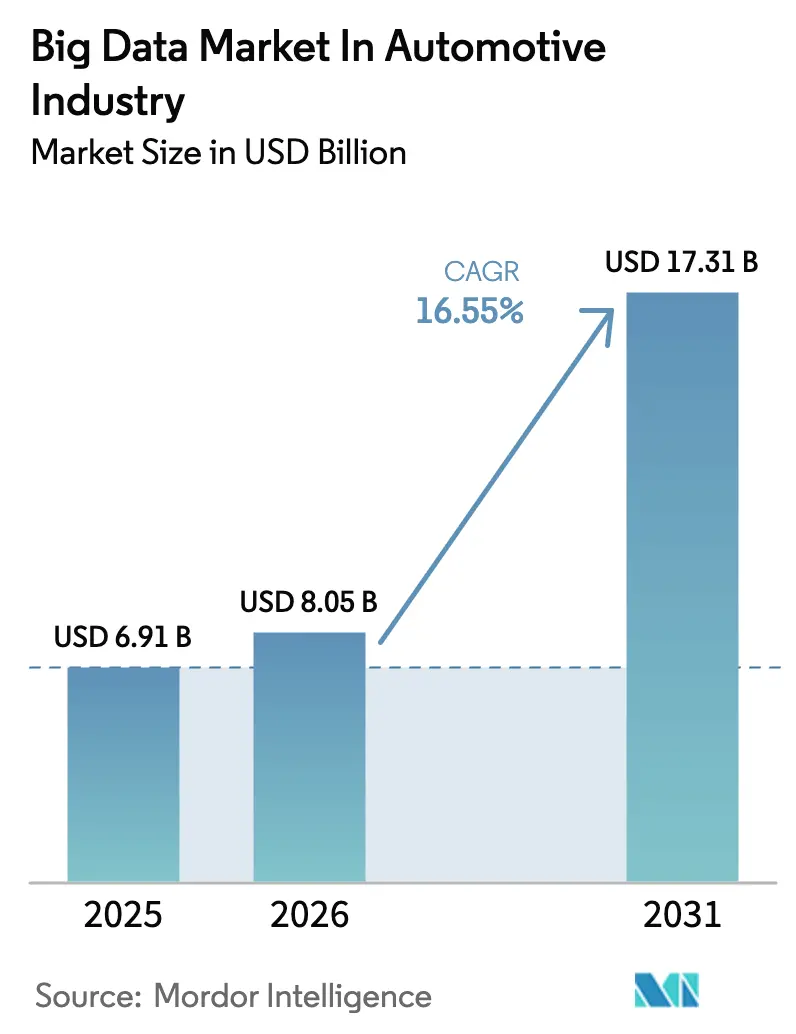

| Market Size (2026) | USD 8.05 Billion |

| Market Size (2031) | USD 17.31 Billion |

| Growth Rate (2026 - 2031) | 16.55% CAGR |

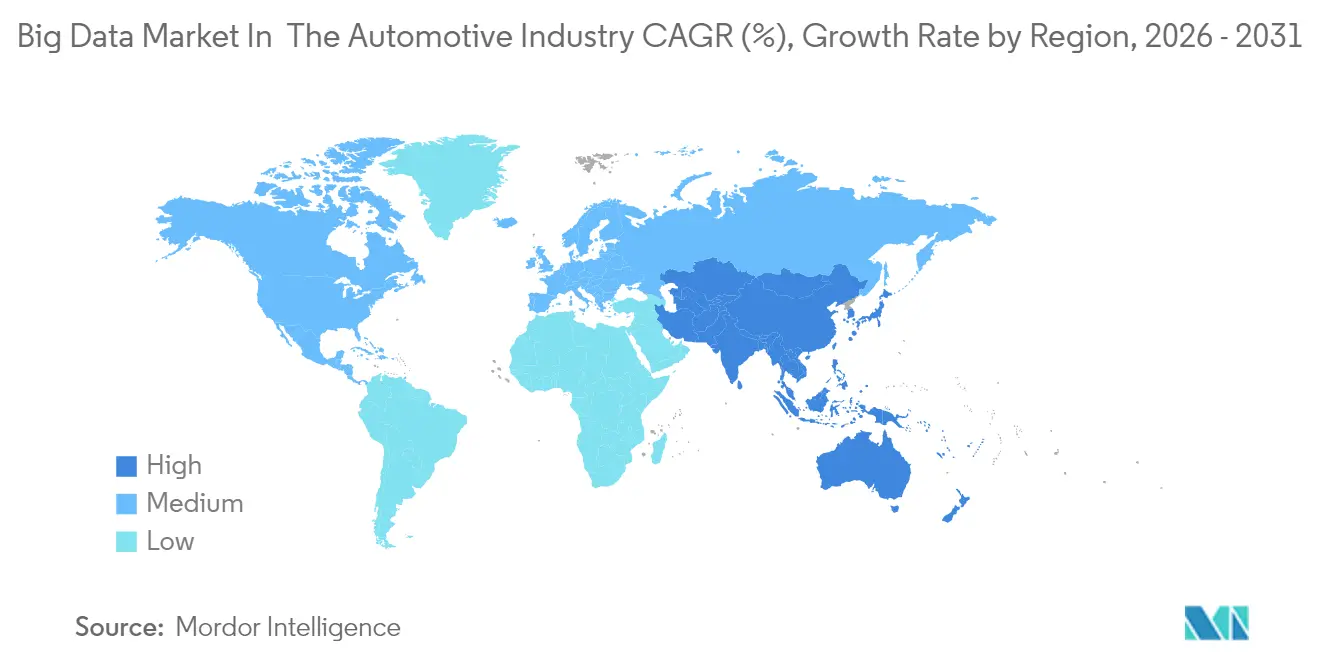

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Big Data Market In Automotive Industry by Mordor Intelligence

The Big Data Market size in the Automotive Industry market size in 2026 is estimated at USD 8.05 billion, growing from 2025 value of USD 6.91 billion with 2031 projections showing USD 17.31 billion, growing at 16.55% CAGR over 2026-2031.

The semiconductor content per vehicle is on track to double to USD 1,200 by 2030, underscoring the growing linkage between data-intensive applications and expensive processing hardware. Automakers now treat software as the core differentiator, with connected vehicles generating nearly 25 GB of data every hour.[1]Salesforce Staff Writers, “Connected Cars and Data,” salesforce.comStrategic alliances with cloud and chip leaders are proliferating as original equipment manufacturers (OEMs) strive to leverage this data for real-time analytics. North America still commands the largest regional foothold, yet Asia Pacific is scaling faster on the back of expansive electric- and autonomous-vehicle policies.

Key Report Takeaways

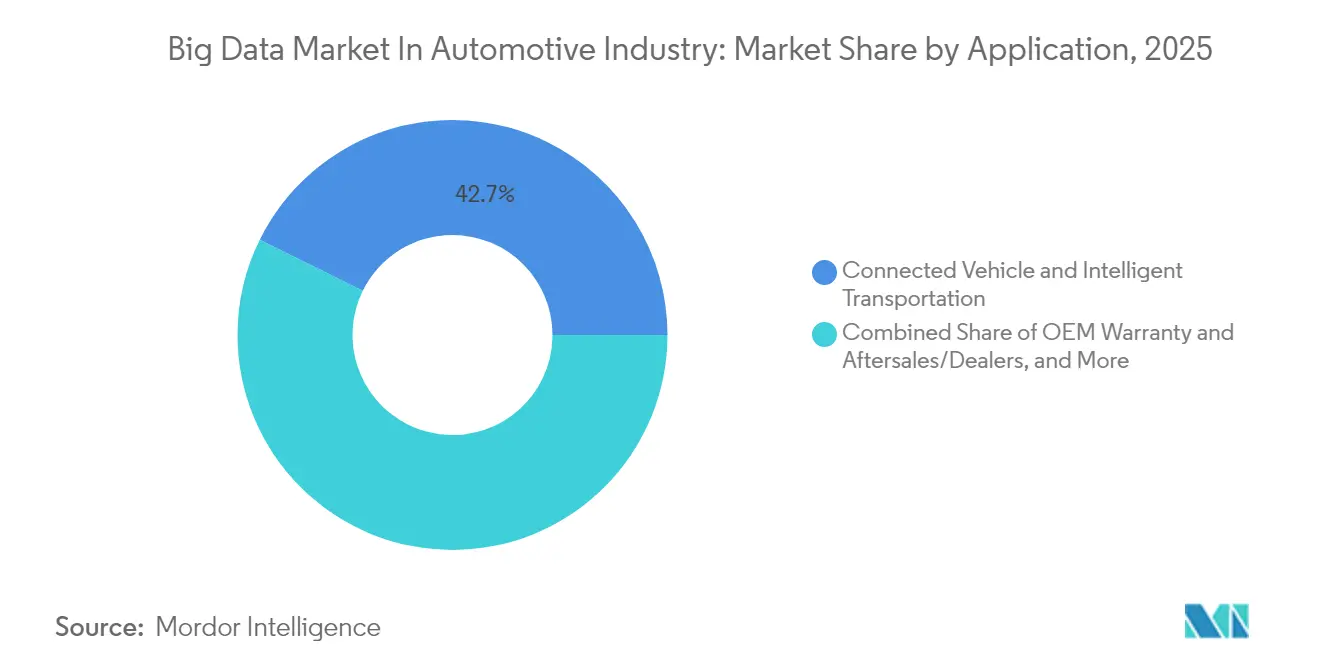

- By application, Connected Vehicle and Intelligent Transportation captured 42.70% of Big Data market share in the automotive industry in 2025, while the segment is expanding at a 16.95% CAGR to 2031.

- By data source, ADAS/Autonomous Sensor Data held 36.85% of Big Data market share in the automotive industry in 2025; it also logs the highest 17.72% CAGR through 2031.

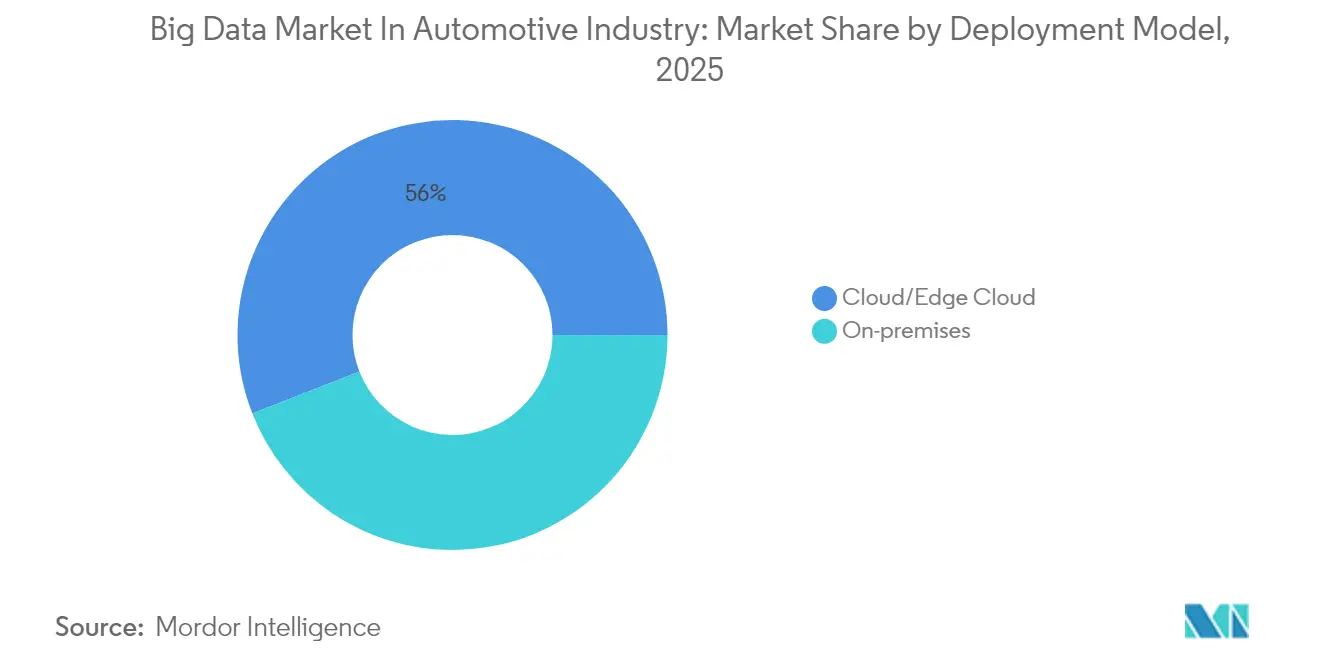

- By deployment model, Cloud/Edge Cloud accounted for 55.95% of Big Data market share in the automotive industry in 2025 and is growing at a 17.35% CAGR.

- By end user, OEMs led with 48.35% revenue share in 2025, while Fleet Operators and Mobility Service Providers posted the swiftest 16.74% CAGR.

- By geography, North America retained a 34.10% share in 2025; Asia Pacific is the fastest-growing region at 18.08% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Big Data Market In Automotive Industry

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing efforts by ecosystem players to monetise vehicle-generated data | 3.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Growing installed base of connected and software-defined vehicles | 4.1% | Global, led by APAC and North America | Long term (≥ 4 years) |

| Regulatory mandates spurring telematics data availability | 2.8% | EU core, expanding to APAC markets | Short term (≤ 2 years) |

| Emergence of edge-cloud analytics loops for autonomous-driving model training | 3.5% | North America & China, spill-over to EU | Long term (≥ 4 years) |

| OEM-led vehicle-data marketplaces unlocking new recurring-revenue streams | 2.1% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Real-time ADAS log offload to hyperscale clouds reducing time-to-validation | 1.9% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing efforts to monetize vehicle-generated data

Automakers are redirecting revenue models toward digital subscriptions that ride on telematics feeds. Ford Pro recorded USD 2.6 billion EBIT on USD 17 billion revenue in Q2 2024, propelled by 600,000 paid software subscriptions that leverage fleet data for uptime optimization. Subscription services could generate as much as USD 310 per connected vehicle each year by 2030, bolstering margins. Marketplace platforms now let OEMs license data sets to insurers, municipalities, and energy providers. The Big Data market in the automotive industry, therefore, pivots on analytics engines that convert raw sensor logs into saleable insights. Scalability hinges on hyperscale partnerships that can ingest terabytes without latency.

Growing installed base of connected and software-defined vehicles

Global connected-vehicle stock is projected to hit 367 million units in 2027, a 91% leap over 2023. Japan is clearing 25 public roads for driverless cars and targets 100% electric-vehicle sales by 2035. Such regulations expand the addressable fleet for real-time data services. Software-centric architectures also allow continuous over-the-air feature upgrades, sharpening recurring revenue. Suppliers that master vehicle operating systems stand to capture the lion’s share of emerging value pools. The Big Data market in the automotive industry relies on this hardware-agnostic shift to amplify data volume and quality.

Regulatory mandates spurring telematics data availability

The EU Data Act grants vehicle owners control over in-car data and is expected to lift availability to 30 TB per vehicle per day by 2025, fostering usage-based insurance and mobility apps. China’s automotive data rules enforce localization, driving OEMs to deploy domestic clouds. India’s Digital Personal Data Protection Act of 2023 introduces explicit consent and localization, shaping global data-flow strategies[2]CyberPeace Foundation, “India’s Data Protection Act Explained,” cyberpeace.org. Harmonized telematics protocols promoted by COVESA are emerging to ease compliance while preserving security. Overall, regulation is simultaneously opening new service lanes and raising governance costs for the Big Data market in the automotive industry.

Emergence of edge-cloud analytics loops for autonomous-driving model training

The emergence of edge-cloud analytics loops is becoming a major driver for big data in the automotive industry. Autonomous vehicles generate large volumes of sensor, camera, radar, and telematics data that must be processed close to the vehicle and then refined in the cloud. This loop allows automakers to train models faster by combining real-world driving data with centralized analytics and continuous model improvement. It also helps reduce latency, improve decision-making, and make autonomy systems more adaptive to changing road conditions. As vehicles become more software-defined, the need to capture, move, and analyze data continuously is increasing. This is pushing demand for scalable big data platforms that can support both edge processing and cloud-based training. Overall, the trend is strengthening the role of data as the core fuel for autonomous-driving development.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Privacy and Data-Sovereignty Regulations (GDPR, CPRA, China PIPL) | -2.80% | Europe, North America, Asia-Pacific | Medium term (2–4 years) |

| Lack of Industry-Wide Standard Schemas for Automotive Data Sets | -2.10% | Global | Medium term (2–4 years) |

| High TCO of Petabyte-Scale, Low-Latency Analytics Infrastructure | -2.50% | Global | Short term (≤ 2 years) |

| OEM Reluctance to Share Proprietary Driving-Scenario IP | -1.70% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter privacy and data-sovereignty regulations

A web of statutes, including GDPR, California’s CPRA, and China’s PIPL, forces OEMs to invest heavily in governance. India’s draft 2025 rules add a mandatory breach notice within 72 hours and annual impact assessments. Chinese localization clauses oblige global brands to build parallel infrastructure behind the firewall. Non-compliance risks fines, reputational harm, and service lockdowns, trimming the near-term expansion tempo of the Big Data market in the automotive industry. Vendors are responding with privacy-enhancing technologies such as federated learning to keep raw data in-country while sharing model weights.

Lack of industry-wide standard schemas for automotive data sets

Despite initiatives like the Common Vehicle Information Model, data silos persist. Fragmentation leads to expensive custom interfaces between OEM back ends and third-party applications. The MOBI Connected Mobility Data Marketplace standard sets governance frameworks for identity and permissions, yet adoption varies. Japanese automakers are piloting ASIL-D-certified middleware to harmonize message formats. Until common ontologies mature, analytics scalability will suffer, delaying full value extraction from the Big Data market in the automotive industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Connected Vehicle Systems Drive Innovation

Connected Vehicle and Intelligent Transportation logged the largest slice of Big Data market share in the automotive industry at 42.70% in 2025 and is advancing at a 16.95% CAGR. This growth rests on 5G build-outs, mandated ADAS functions, and rising consumer appetite for seamless infotainment. Real-time congestion rerouting, battery-health monitoring, and dynamic tolling are examples of revenue-generating use cases. Policy moves such as mandatory emergency braking systems in Europe further boost data volumes. OEM Warranty and Aftersales units mine service histories to predict parts demand, cutting downtime. Sales and marketing arms rely on behavioral analytics to tailor offers that lift conversion rates. Traffic optimization algorithms powered by generative AI now flag incidents with high precision, enhancing public-sector appeal. As these applications scale, the Big Data market in the automotive industry cements its role as a cross-sector data orchestrator.

Product Development, Supply Chain, and Manufacturing analytics add another layer of value. Stellantis employs its Mobilisights platform to refine fleet efficiency across Europe. Predictive maintenance models shave unplanned line stoppages, while digital twins of factories cut ramp-up time for new models. Telematics-driven service scheduling improves customer satisfaction scores. Marketing teams leverage usage patterns to craft subscription bundles, translating into steadier revenue streams. Together, these trends reinforce a feedback loop where data-centric services finance further investment in the Big Data market in the automotive industry.

By Data Source: ADAS Sensors Dominate Processing

ADAS and autonomous sensors commanded 36.85% of the Big Data market share in the automotive industry in 2025 and carry the fastest 17.72% CAGR. Vision, lidar, and radar units output high-resolution streams that underpin safety features such as lane keeping and collision avoidance. Regulatory edicts in the EU require autonomous emergency braking in all new models, ensuring sensor proliferation. Edge AI chips compress and classify feeds before forwarding summaries to the cloud for model retraining. In-car infotainment and HMI logs capture user preferences, feeding personalized content engines. Power-train and CAN-bus data flow into health-score algorithms that alert owners ahead of faults, cutting warranty costs.

Fleet and insurance databases round out the source mix. Cambridge Mobile Telematics shows that engaged telematics users reduce distracted driving by 20%. Usage-based insurance leverages those inputs to adjust premiums in near real time. As sensor fidelity improves, object-detection accuracy rises, enhancing autonomy. Suppliers like Aptiv have unveiled Gen 6 platforms with over-the-air upgrade paths. Each leap feeds back into the Big Data market in the automotive industry, enriching predictive power and monetization options.

By Deployment Model: Cloud Infrastructure Accelerates

Cloud and edge-cloud solutions represented 55.95% of Big Data market share in the automotive industry in 2025 and are expanding at 17.35% CAGR. Hyperscale operators offer elastic storage and GPU fleets that lower entry barriers for algorithm training. Microsoft’s Autonomous Vehicle Operations blueprint illustrates how Azure pipelines ingest, curate, and analyze petabyte-scale driving logs. OEMs can iterate perception models weekly instead of quarterly, accelerating feature rollout. Data residency rules push some workloads to regional clouds, spurring investments in sovereign instances.

On-premises environments persist where deterministic latency is vital, such as airbag deployment analytics. Hybrid frameworks route safety-critical loops to edge gateways while archiving long-tail data centrally. Hyundai Motor Group’s alliance with NVIDIA integrates AI across design, production, and robotics, underscoring platform convergence. Ultimately, cloud economies of scale provide free resources for differentiated cockpit experiences, reinforcing the flywheel effect for the Big Data market in the automotive industry.

By End User: OEMs Lead While Fleets Accelerate

OEMs controlled 48.35% of 2025 revenue thanks to embedded analytics in product design and quality loops. Digital twins validate engineering changes before physical builds, saving time and material. Vehicle-as-a-Platform strategies let brands bundle navigation, charging, and infotainment under subscription umbrellas. Fleet Operators and Mobility Service Providers, however, post the fastest 16.74% CAGR as shared-mobility models expand. Targa Telematics monitors half a million connected assets worldwide, underscoring data’s role in uptime and routing.

Tier-1 suppliers deploy analytics for inventory planning and predictive maintenance, while insurers integrate real-time scores into claim adjudication, shortening payout cycles. Dealers tap data to stage proactive service campaigns, lifting customer retention. This diverse demand mosaic safeguards momentum for the Big Data market in the automotive industry, even if any single cohort slows.

Geography Analysis

North America retained 34.10% of the Big Data market share in the automotive industry in 2025. Deep OEM–supplier linkages, favorable data-sharing regulations, and cross-border trade between the United States and Canada sustain scale advantages. U.S. automakers dispatched USD 17.2 billion worth of vehicles to Canada in 2022, reflecting integrated supply chains. Federal incentives for domestic chip fabrication and the USD 52 billion CHIPS Act underpin the compute supply for analytics workloads. General Motors is implementing NVIDIA Omniverse for plant simulation and DRIVE AGX for in-vehicle AI, highlighting regional leadership in data-driven manufacturing.

Asia Pacific, the fastest-growing territory at 18.08% CAGR, benefits from China’s USD 500 billion autonomous-vehicle roadmap and Japan’s goal to capture 30% global share in next-generation models. Japan has opened 25 public roads to driverless testing, accelerating data accrual. India’s automotive vision targets USD 300 billion output by 2030, backed by a USD 500 million EV production policy and a ₹10,300 crore AI mission that funds national GPU clusters. Smartphone penetration and low-cost connectivity prime the region for telematics adoption, feeding the Big Data market in the automotive industry with high-velocity inputs.

Europe shows steady expansion underpinned by rigorous privacy safeguards. The EU Data Act could surface 30 TB of data per vehicle daily by 2025, enabling insurers to craft real-time policies while safeguarding consumer rights. Stellantis launched fleet, insurance, and EV-charging data packages through its Mobilisights arm in 2024, operating under consent-first principles. Sustainability targets and charging-infrastructure rollouts drive EV penetration, further enriching datasets. To comply with localization clauses, OEMs deploy regional clouds and privacy-enhancing encryption, supporting measured yet resilient growth in the Big Data market in the automotive industry.

Competitive Landscape

Competition is intensifying as cloud hyperscalers, chipmakers, and traditional automotive suppliers converge around data platforms. IBM, Microsoft, and Amazon Web Services leverage global cloud footprints to host petabyte-scale pipelines. Continental, Bosch, and HERE combine domain know-how with real-time mapping and sensor-fusion engines. NVIDIA is expanding from GPUs into complete AI stacks, partnering with General Motors for factory digitization and Hyundai on software-defined vehicle programs.

OEMs are acquiring or allying with software specialists to accelerate capability build-up. Volkswagen’s USD 5.8 billion investment in Rivian focuses on electrical architecture and over-the-air software rather than manufacturing footprint. Data-marketplace providers such as Otonomo and Caruso enable secure vehicle-data monetization, carving a niche between OEMs and service players. Pony AI’s pact with Tencent Cloud illustrates how autonomous-vehicle startups leverage hyperscale infrastructure to shorten time-to-market. Standardization and interoperability solutions remain a white space, with MOBI developing blockchain-based frameworks that could reduce onboarding friction.

Mid-tier contenders differentiate through specialized analytics, from battery-health scoring to environmental conditioning for lidar systems. Startups tackling edge-AI compression attract funding as bandwidth limits surface. The Big Data market in the automotive industry is, therefore, characterized by a fluid mix of collaboration and competition, with data-control strategies often dictating deal rationale.

Leaders of Big Data Market In Automotive Industry

IBM Corporation

Microsoft Corporation

SAP SE

SAS Institute Inc

Reply SpA (Data Reply)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: General Motors and NVIDIA announced a comprehensive collaboration to enhance next-generation vehicles and manufacturing through AI and accelerated computing, implementing NVIDIA Omniverse for factory planning and DRIVE AGX for ADAS.

- March 2025: Magna and NVIDIA partnered to integrate the NVIDIA DRIVE AGX platform into next-generation technologies, targeting L2+ to L4 safety solutions with demos slated for Q4 2025.

- January 2025: Hyundai Motor Group teamed with NVIDIA to accelerate AI deployment across software-defined vehicles, robotics, and mobility services.

- November 2024: Rivian and Volkswagen Group raised their joint-venture commitment to USD 5.8 billion, aiming to embed Rivian software into VW models by 2027.

Scope of Report on Big Data Market In Automotive Industry

Big data deals with a collection of data that is huge in volume and growing exponentially with time. Such data is so large and complex that no traditional data management tools can store it or process it efficiently. Big data solutions help analyze and systematically extract information from or otherwise deal with data sets that are too large or complex to be handled by traditional data-processing application software.

The big data market in the automotive industry is segmented by application (product development, supply chain, and manufacturing, OEM warranty and aftersales/dealers, connected vehicle and intelligent transportation, and sales, marketing, and other applications) and geography (North America, Europe, Aisa-Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Product Development, Supply Chain and Manufacturing |

| OEM Warranty and Aftersales/Dealers |

| Connected Vehicle and Intelligent Transportation |

| Sales, Marketing and Other Applications |

| Power-train and CAN-bus Logs |

| ADAS/Autonomous Sensor Data |

| In-car Infotainment and HMI Data |

| Fleet Operations and Usage-based Insurance Data |

| On-premises |

| Cloud/Edge Cloud |

| OEMs |

| Tier-1 Suppliers |

| Fleet Operators and Mobility Service Providers |

| Insurance and Finance Companies |

| Aftermarket and Dealer Networks |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Application | Product Development, Supply Chain and Manufacturing | |

| OEM Warranty and Aftersales/Dealers | ||

| Connected Vehicle and Intelligent Transportation | ||

| Sales, Marketing and Other Applications | ||

| By Data Source | Power-train and CAN-bus Logs | |

| ADAS/Autonomous Sensor Data | ||

| In-car Infotainment and HMI Data | ||

| Fleet Operations and Usage-based Insurance Data | ||

| By Deployment Model | On-premises | |

| Cloud/Edge Cloud | ||

| By End User | OEMs | |

| Tier-1 Suppliers | ||

| Fleet Operators and Mobility Service Providers | ||

| Insurance and Finance Companies | ||

| Aftermarket and Dealer Networks | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Big Data market in the automotive industry?

The market is worth USD 8.05 billion in 2026 and is projected to grow to USD 17.31 billion by 2031.

Which application segment holds the largest share?

Connected Vehicle & Intelligent Transportation leads with a 42.70% share in 2025 and remains the fastest-growing segment at 16.95% CAGR.

Why is Asia Pacific growing faster than other regions?

Aggressive autonomous-vehicle targets in China, supportive driverless-testing policies in Japan, and India’s sizable EV and AI investments propel an 18.08% regional CAGR.

How are OEMs monetizing vehicle data today?

Automakers sell subscription services, operate data marketplaces, and license telematics feeds to insurers and municipalities, generating recurring revenue per vehicle.

What role does edge computing play in automotive Big Data?

Edge nodes process sensor streams locally to meet millisecond latency needs for safety functions while synchronizing with cloud platforms for long-term model training.

How do privacy regulations impact market growth?

GDPR, CPRA, PIPL, and emerging Indian rules impose consent and localization requirements that raise compliance costs and can slow short-term expansion, yet they also foster consumer trust essential for data-driven services.

Page last updated on: