Market Overview

| Study Period | 2020 - 2030 |

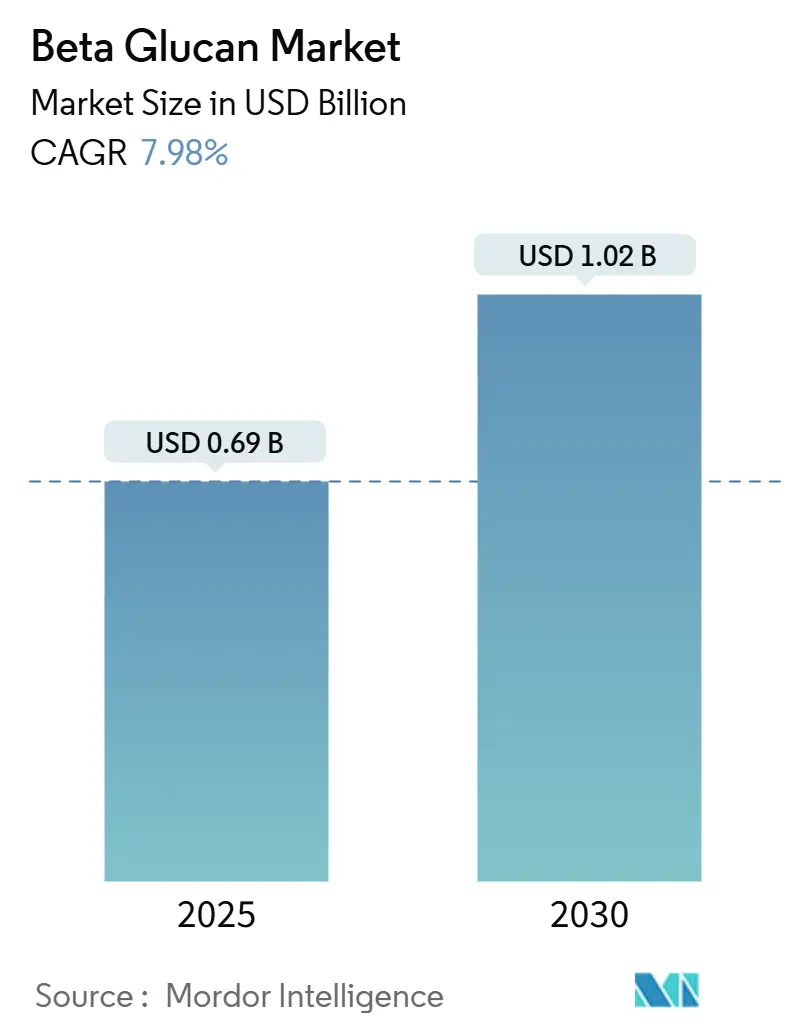

| Market Size (2025) | USD 0.69 Billion |

| Market Size (2030) | USD 1.02 Billion |

| Growth Rate (2025 - 2030) | 7.98% CAGR |

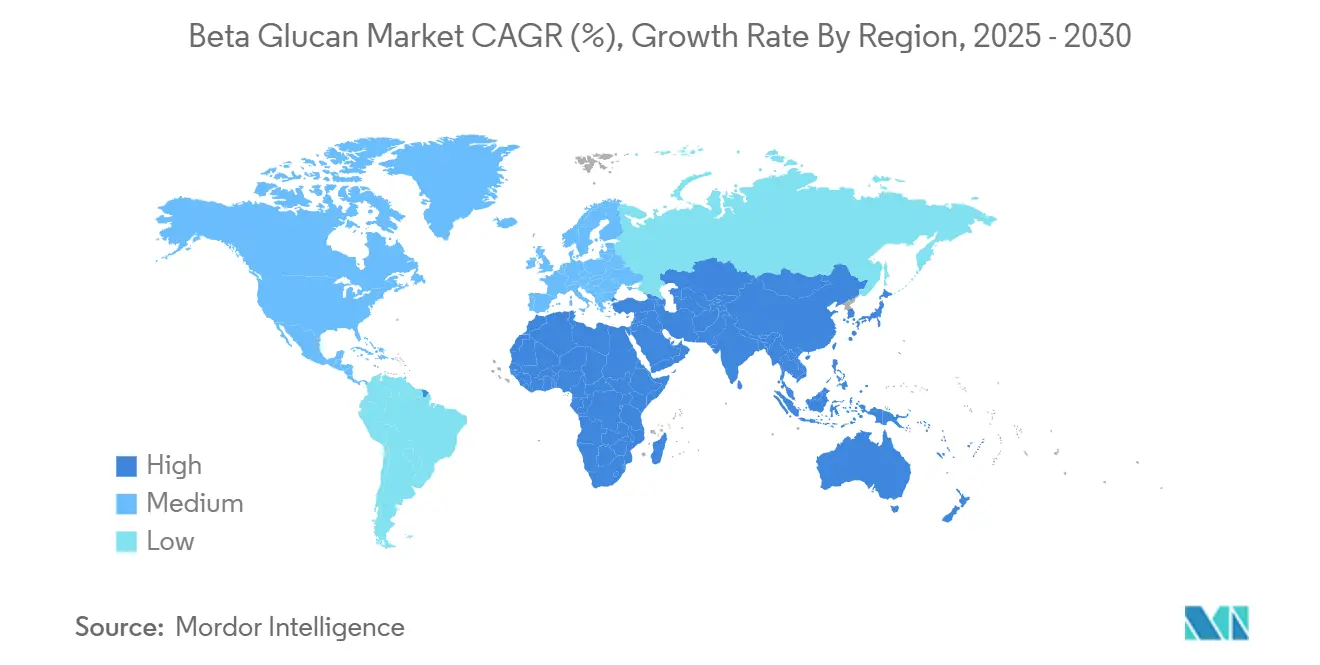

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

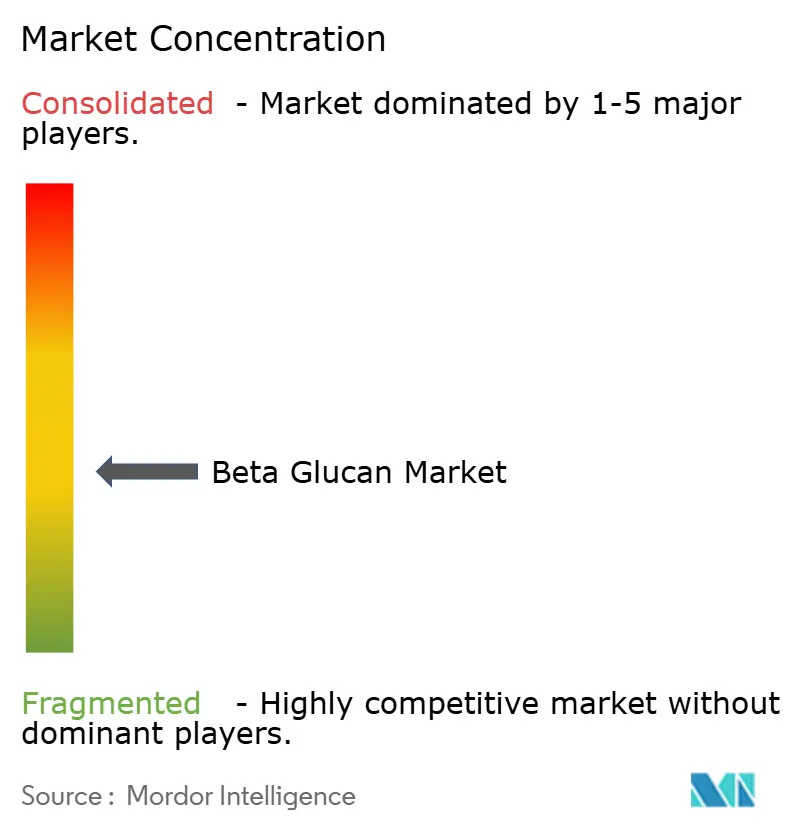

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Beta Glucan Market Analysis by Mordor Intelligence

The beta glucan market size is estimated at USD 0.69 billion in 2025, and is expected to reach USD 1.02 billion by 2030, at a CAGR of 7.98% during the forecast period (2025-2030). Rising scientific consensus around cholesterol reduction, immune modulation, and gut-health benefits continues to elevate beta-glucan’s profile in functional food, pharmaceutical, and personal-care lines. The U.S. Food and Drug Administration (FDA) recognizes oat beta-glucan’s cholesterol-lowering efficacy, enabling on-pack health claims that accelerate product launches. Investments in precision fermentation and advanced extraction are expanding supply options while reducing production cost volatilities. Solid regulatory backing from bodies such as the European Food Safety Authority (EFSA) and clear labeling rules are further encouraging brand owners to champion beta-glucan-forward formulations

Key Report Takeaways

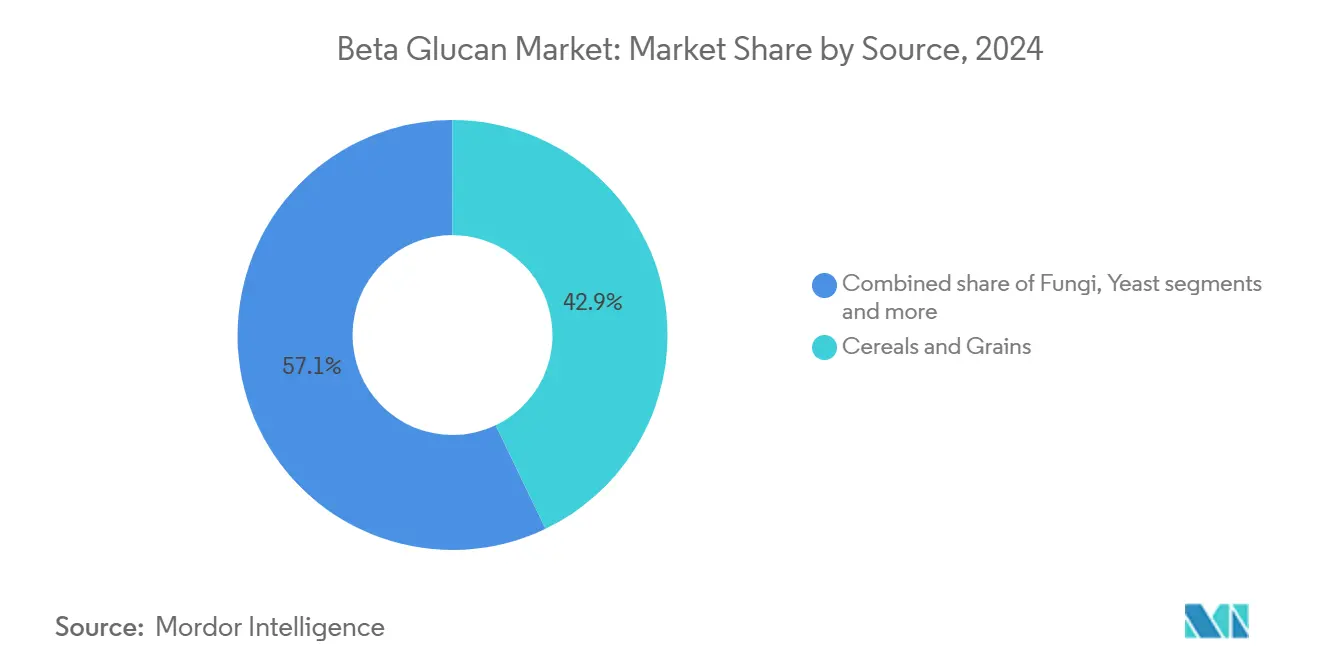

- By source, cereals and grains led with 42.88% revenue share in 2024; fungi-derived formats are projected to expand at 8.75% CAGR through 2030.

- By category, soluble forms commanded 72.47% of the beta-glucan market share in 2024, while insoluble types are poised to grow at 9.04% CAGR to 2030.

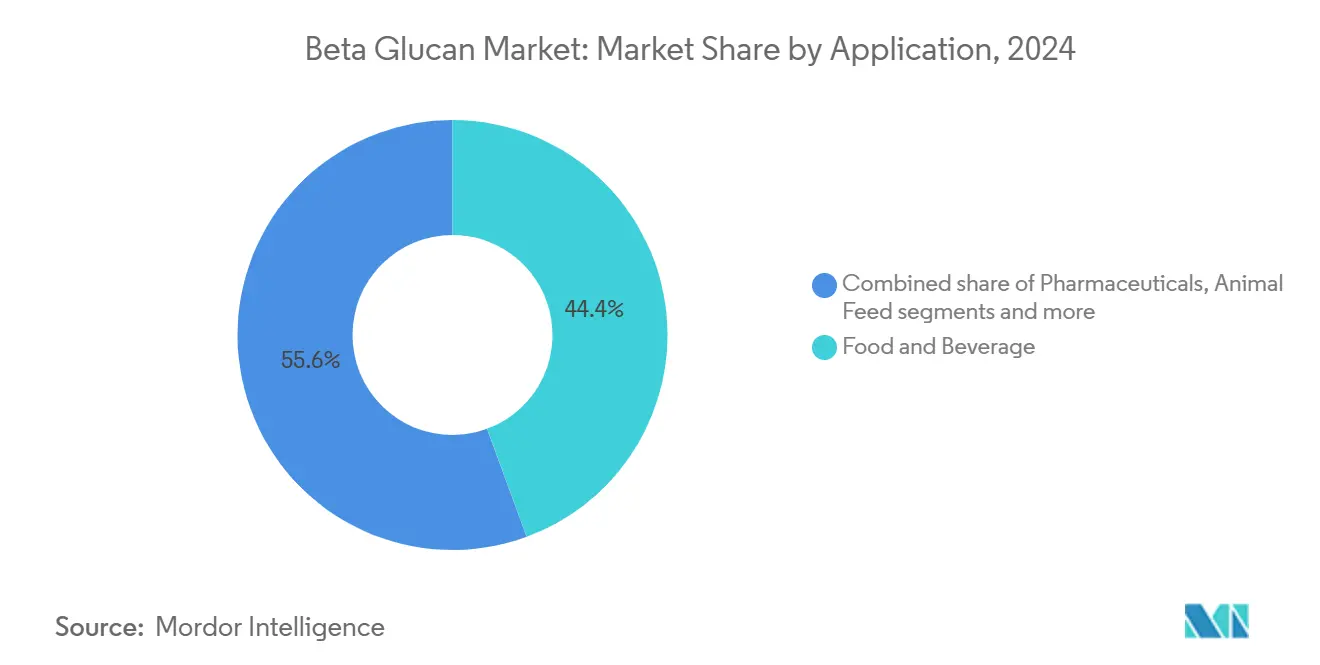

- By application, food and beverage accounted for 44.38% of the beta-glucan market size in 2024; personal care and cosmetics are advancing at 8.86% CAGR between 2025-2030.

- By geography, Europe held a 33.44% share of the beta-glucan market in 2024, whereas Asia-Pacific is on track for a 9.07% CAGR up to 2030.

Global Beta Glucan Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for immune-boosting ingredients in functional foods | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing popularity of plant based ingredients | +1.2% | Global, led by Asia-Pacific and Europe | Long term (≥ 4 years) |

| Increasing popularity in gut health and prebiotic products | +1.5% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growth in vegan and gluten-free product launches | +0.9% | North America and Europe primarily | Short term (≤ 2 years) |

| Expansion of fungi- and yeast-based beta-glucans in pharmaceuticals | +1.1% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Rising research and development investment for enhanced solubility and bioavailability | +0.7% | North America and Europe | Long term (≥ 4 years) |

Source: Mordor Intelligence

Understand The Key Trends Shaping This Market

Download PDF

Rising Demand for Immune-Boosting Ingredients in Functional Foods

Post-pandemic health consciousness has fundamentally shifted consumer priorities toward immune-supporting ingredients, with consumers actively seeking products that support immune health, according to the Kerry Group report. Beta-glucan's scientifically validated immunomodulatory effects position it as a preferred ingredient in functional beverages, with 60% of Asia-Pacific, Middle East, and Africa (APMEA) region consumers expressing interest in immune health beverages. The FDA's GRAS approval for beta-glucans from Antrodia cinnamomea at levels up to 150 mg per serving demonstrates regulatory confidence in safety profiles. Clinical studies indicate that beta-glucan consumption enhances immune response in patients with compromised immune systems, as demonstrated in myelodysplastic syndrome trials. This immune-centric positioning drives premium pricing strategies and enables market penetration across previously untapped demographic segments. The convergence of scientific validation and consumer demand creates sustainable competitive advantages for beta-glucan suppliers with robust clinical data portfolios.

Growing Popularity of Plant Based Ingredients

According to the Smart Protein Project, in 2023, 49% of survey respondents in Italy prioritized health benefits, while 26% focused on environmental and climate impact when purchasing plant-based or vegan food products [1]Source: Smart Protein Project, “Evolving Appetites: An In-depth Look At European Attitudes Towards Plant-based Eating”, smartproteinproject.eu. Consumer preferences directly influence purchasing patterns in the plant-based food segment, with demand increasing for clean-label products that deliver health advantages and environmental sustainability. This trend indicates a fundamental shift in the food market, where health and environmental considerations drive product selection. Plant-based positioning enables manufacturers to implement premium pricing strategies and meet sustainability requirements from major food companies. This approach not only satisfies consumer preferences but also aligns with corporate sustainability goals and regulatory requirements. The combination of plant-based trends and functional health benefits creates distinct value propositions that generate higher margins compared to standard beta-glucan products. This convergence of health functionality and sustainability presents significant opportunities for manufacturers to develop innovative products that capture premium market segments.

Increasing Popularity in Gut Health and Prebiotic Products

Gut health awareness drives sophisticated consumer understanding of prebiotic mechanisms, with beta-glucan's ability to modulate beneficial gut bacteria gaining scientific validation. The mechanistic understanding of beta-glucan's interaction with gut microbiota enables targeted product development for specific health outcomes, moving beyond generic fiber positioning. Clinical evidence supporting beta-glucan's role in maintaining healthy cholesterol levels through gut-mediated mechanisms strengthens regulatory health claim substantiation across multiple jurisdictions. This scientific foundation enables premium positioning in the expanding gut health category, where consumers demonstrate a willingness to pay higher prices for proven efficacy. The convergence of microbiome science and beta-glucan functionality creates opportunities for personalized nutrition applications and targeted therapeutic interventions.

Growth in Vegan and Gluten-Free Product Launches

According to The Vegan Society survey, approximately two million people in Great Britain, representing 3% of the population, follow a vegan or plant-based diet [2]Source: The Vegan Society, “Nationwide Trends Highlight Growing Shift Toward Plant-based Diets”, vegansociety.com. This increase indicates a market transition from medical necessity to lifestyle preferences in dietary choices. Beta-glucan, being naturally gluten-free and plant-based, meets the market requirements for vegan and gluten-free products while delivering functional health benefits. Comprehensive research studies demonstrate that beta-glucans derived from Pleurotus ostreatus significantly enhance both the nutritional profile and sensory characteristics of gluten-free bread, effectively addressing a persistent challenge in gluten-free product development. The European Commission's approval of (1-3)(1-6)-β-glucans from mushroom sources as food ingredients has substantially expanded the potential applications across various specialty dietary products. This strategic market positioning enables manufacturers to effectively serve multiple dietary preference segments while maintaining premium price points for their specialized product formulations in both vegan and gluten-free categories.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low consumer awareness in developing markets | -1.3% | Asia-Pacific developing markets, Latin America, Middle East and Africa | Medium term (2-4 years) |

| Variability in functional efficacy across sources | -0.8% | Global, particularly affecting new entrants | Short term (≤ 2 years) |

| Supply chain disruption in raw material sourcing | -1.1% | Global, with acute impact in North America and Europe | Short term (≤ 2 years) |

| Lack of standardization in product quality | -0.6% | Global, with regulatory focus in developed markets | Long term (≥ 4 years) |

Source: Mordor Intelligence

Low Consumer Awareness in Developing Markets

Consumer education gaps in emerging markets constrain beta-glucan adoption despite growing health consciousness and disposable income. Scientific substantiation requirements vary significantly across developing markets, creating compliance complexities that favor established multinational players over local manufacturers. The disconnect between traditional dietary practices and modern functional food concepts requires substantial consumer education investments that many beta-glucan suppliers cannot justify given uncertain return timelines. Regulatory frameworks in developing markets often lack specific guidelines for beta-glucan health claims, creating market entry barriers and limiting promotional messaging effectiveness. This awareness deficit particularly impacts premium-priced beta-glucan products where consumer understanding of functional benefits directly correlates with purchase intent and willingness to pay price premiums.

Variability in Functional Efficacy Across Sources

Source-dependent efficacy variations create quality consistency challenges that undermine consumer confidence and complicate regulatory approval processes. Beta-glucan molecular weight, structural configuration, and extraction methods significantly influence bioactivity, with studies showing that molecular weight variations affect prebiotic efficacy and immune response modulation. The FDA's requirement for comprehensive safety evaluations and toxicological studies for each beta-glucan source, as demonstrated in GRAS notices for Antrodia and white button mushroom extracts, creates regulatory complexity and market entry barriers. Extraction method variations, including enzymatic, alkaline, and subcritical water techniques, produce beta-glucan products with different physicochemical properties and biological activities, complicating standardization efforts. This variability particularly challenges smaller manufacturers lacking resources for comprehensive characterization and clinical validation studies. The resulting market fragmentation limits economies of scale and creates consumer confusion regarding product selection and expected health outcomes.

Segment Analysis

By Source: Cereals Anchor Market While Fungi Accelerate

Cereals and grains command 42.88% market share in 2024, reflecting established supply chains and regulatory acceptance for oat and barley-derived beta-glucans. The FDA's recognition of oat beta-glucan's cholesterol-lowering properties at a 3-gram daily intake supports market positioning, while Tate & Lyle's PromOat demonstrates commercial viability in organic food formulations. However, fungi-derived beta-glucans surge ahead with 8.75% CAGR through 2030, driven by superior bioactivity profiles and novel extraction opportunities. Seaweed and microalgae sources face regulatory hurdles, particularly in Europe, where EFSA novel foods approval requirements create market entry barriers despite promising bioactivity profiles.

The competitive landscape reveals strategic positioning differences across source categories, with cereal-based suppliers emphasizing cost efficiency and regulatory compliance while fungi-based producers focus on premium bioactivity and novel applications. Bacterial beta-glucan production through lactic acid bacteria fermentation offers in-situ enrichment opportunities for sourdough applications, addressing clean-label demands while enhancing nutritional profiles. This source diversification strategy enables risk mitigation against supply chain disruptions while capturing premium pricing for specialized applications.

Note: Segment shares of all individual segments available upon report purchase

By Category: Soluble Dominance Meets Insoluble Innovation

Soluble beta-glucans maintain a 72.47% market share in 2024, supported by established health claims and proven functionality in food applications. The European Food Safety Authority's approval of health claims for soluble beta-glucans reinforces market positioning, particularly for cholesterol reduction and glycemic response modulation. This category differentiation enables premium pricing strategies for specialized applications while addressing unmet needs in pharmaceutical and cosmetic formulations, where soluble forms prove inadequate.

Insoluble beta-glucans accelerate with a 9.04% CAGR through 2030, driven by emerging applications in personal care and specialized pharmaceutical formulations. The structural properties of insoluble forms enable unique delivery mechanisms, particularly in topical applications where sustained release and barrier function enhancement provide competitive advantages. Additionally, beta-glucans that were insoluble stimulated immune response through macrophage activation and strengthening of the gut barrier. These compounds also improved digestive health by increasing fecal volume and maintaining regular bowel movements, making them essential components in immunity and digestive health supplements.

By Application: Food Dominance Challenged by Personal Care Surge

Food and beverage applications secure 44.38% market share in 2024, anchored by established regulatory pathways and consumer acceptance of functional foods. General Mills' whole grain portfolio, with 86% of cereals providing at least 8 grams of whole grain per serving, demonstrates a major manufacturer's commitment to beta-glucan incorporation, according to the General Mills sustainability report 2024. Bakery and confectionery segments benefit from beta-glucan's functional properties as thickeners and stabilizers, while beverage applications leverage immune health positioning.

Personal care and cosmetics applications surge with 8.86% CAGR through 2030, reflecting beauty-from-within trends and scientific validation of topical benefits. Beta-glucan's wound healing, antioxidant, and anti-inflammatory properties enable premium positioning in skincare formulations, with research demonstrating efficacy in cosmetic applications. According to the Office for National Statistics data from 2024, consumer spending on personal care in the United Kingdom was GBP 41.9 billion [3]Source: Office for National Statistics, "Consumer Trends October to December 2024", ons.gov.uk. Pharmaceutical applications benefit from beta-glucan's immunomodulatory effects and drug delivery capabilities, with GRAS approvals expanding formulation possibilities. Animal feed applications leverage beta-glucan's immune enhancement properties, reducing antibiotic dependency while improving livestock health outcomes. This application diversification reduces dependence on traditional food markets while capturing higher margins in specialized segments.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Europe's market leadership stems from comprehensive regulatory frameworks and established consumer acceptance of functional foods, with the European Food Safety Authority's health claims database providing market clarity for beta-glucan applications. The region's 33.44% market share in 2024 reflects mature supply chains and sophisticated consumer understanding of functional benefits. The KELP -EU project's EUR 6 million investment in sustainable seaweed biorefinery demonstrates European commitment to source diversification while addressing environmental sustainability mandates. Brexit implications continue affecting supply chain logistics and regulatory harmonization, creating opportunities for domestic production expansion.

Asia-Pacific's 9.07% CAGR through 2030 reflects accelerating health consciousness and expanding nutraceutical markets across diverse economies. India's expanding middle class and growing awareness of preventive healthcare drive demand for functional ingredients, while regulatory harmonization across ASEAN markets facilitates regional expansion strategies. The region's diverse dietary traditions create opportunities for culturally adapted beta-glucan formulations.

North America benefits from established oat production infrastructure and regulatory clarity through FDA GRAS approvals, enabling efficient market entry for beta-glucan products. The region's mature functional foods market and sophisticated consumer base support premium positioning strategies, while vertical integration opportunities in agriculture and processing create competitive advantages. Supply chain vulnerabilities in grain sourcing, highlighted by Colorado's local grain supply chain challenges, create opportunities for regional diversification strategies. South America and Middle East and Africa represent emerging opportunities with growing health consciousness and expanding middle-class populations, though regulatory frameworks remain underdeveloped compared to established markets.

Competitive Landscape

The beta-glucan market exhibits moderate fragmentation, with major companies including Kerry Group, DSM-Firmenich, and Angel Yeast Co. Ltd. These companies maintain market positions through strategic initiatives. These companies have prioritized product innovation, particularly in developing specialized beta-glucan formulations for diverse applications ranging from food and beverages to pharmaceuticals and personal care products.

The industry has witnessed a significant focus on research and development activities, with companies investing in new extraction technologies and improved production processes to enhance product quality and efficiency. Strategic partnerships, especially with research institutions and distribution networks, have emerged as a key trend to expand market reach and technological capabilities. Companies are also actively pursuing geographical expansion through new manufacturing facilities and distribution centers, particularly in emerging markets, while simultaneously strengthening their presence in established regions through acquisitions and collaborations.

Technology adoption patterns reveal divergent strategies, with established players emphasizing process optimization and cost efficiency while newcomers pursue premium positioning through advanced extraction technologies and novel source materials. White-space opportunities emerge in personalized nutrition applications and targeted therapeutic interventions, where beta-glucan's immunomodulatory properties enable precision health solutions.

Beta Glucan Industry Leaders

-

Kerry Group

-

DSM-Firmenich

-

Tate & Lyle Plc

-

Lesaffre International

-

Angel Yeast Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Layn Natural Ingredients developed Galacan, a beta-glucan ingredient manufactured through precision fermentation, at its expanded biotechnology facility. The ingredient demonstrated improved bioavailability and water solubility. The company designed Galacan for applications in gut health, inflammatory response modulation, and personal care, while pursuing FDA GRAS certification.

- November 2024: Alchemy Agencies partnered with Super Beta Glucan to distribute organic mushroom extract products containing high concentrations of beta-glucans for health and wellness applications. Beta-glucans derived from mushroom extracts were increasingly recognized for their potential health benefits, including improved cognitive function, increased energy levels, enhanced immune response, and better skin health.

- July 2023: BENEO launched Orafti β-Fit, its first barley beta-glucans ingredient. The natural wholegrain barley flour contains 20% beta-glucans and provides health benefits for heart function and blood sugar regulation.

Global Beta Glucan Market Report Scope

Beta-glucans are biologically active fibers derived from the cell wall of various natural sources, including yeast, mushroom, oats, barley, and others, with the proven benefits for health and medical significance. The beta-glucan market is segmented by category into soluble and insoluble and by application into food and beverage, healthcare and dietary supplements, and other applications. The food and beverage segment is further bifurcated into dairy, snacks, beverages, confectionery, baked goods, and other products, and the healthcare and dietary supplements into infant nutrition and other dietary and supplements. By source, the market is segmented into cereals, yeast, mushroom, and other sources. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasting have been done in value terms of USD million.

| By Source | Cereals and Grains | ||

| Fungi | |||

| Yeast | |||

| Seaweed and Microalgae | |||

| Others | |||

| By Category | Soluble | ||

| Insoluble | |||

| By Application | Food and Beverage | Bakery and Confectionary | |

| Beverage | |||

| Snacks | |||

| Dairy and Dairy Products | |||

| Others | |||

| Personal Care and Cosmetics | |||

| Pharmaceuticals | |||

| Animal Feed | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | United Kingdom | ||

| Germany | |||

| Spain | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

By Source

| Cereals and Grains |

| Fungi |

| Yeast |

| Seaweed and Microalgae |

| Others |

By Category

| Soluble |

| Insoluble |

By Application

| Food and Beverage | Bakery and Confectionary |

| Beverage | |

| Snacks | |

| Dairy and Dairy Products | |

| Others | |

| Personal Care and Cosmetics | |

| Pharmaceuticals | |

| Animal Feed | |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current global value of the beta-glucan market?

The beta glucan market was valued at USD 0.69 billion in 2025 and is projected to climb to USD 1.02 billion by 2030.

Which region holds the largest share of beta glucan sales?

Europe leads with 33.44% share, benefiting from harmonized EFSA health-claim rules and consumer familiarity with functional foods.

Which source is growing fastest within the beta glucan market?

Fungi-derived beta glucans are expanding at 8.75% CAGR thanks to superior bioactivity and precision-fermentation capacities.

What is driving beta-glucan adoption in personal care?

Clinical evidence of skin-repair and anti-inflammatory benefits, combined with rising “beauty-from-within” trends, is fueling 8.86% CAGR in cosmetic applications.

Page last updated on: July 9, 2025