Belarus Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

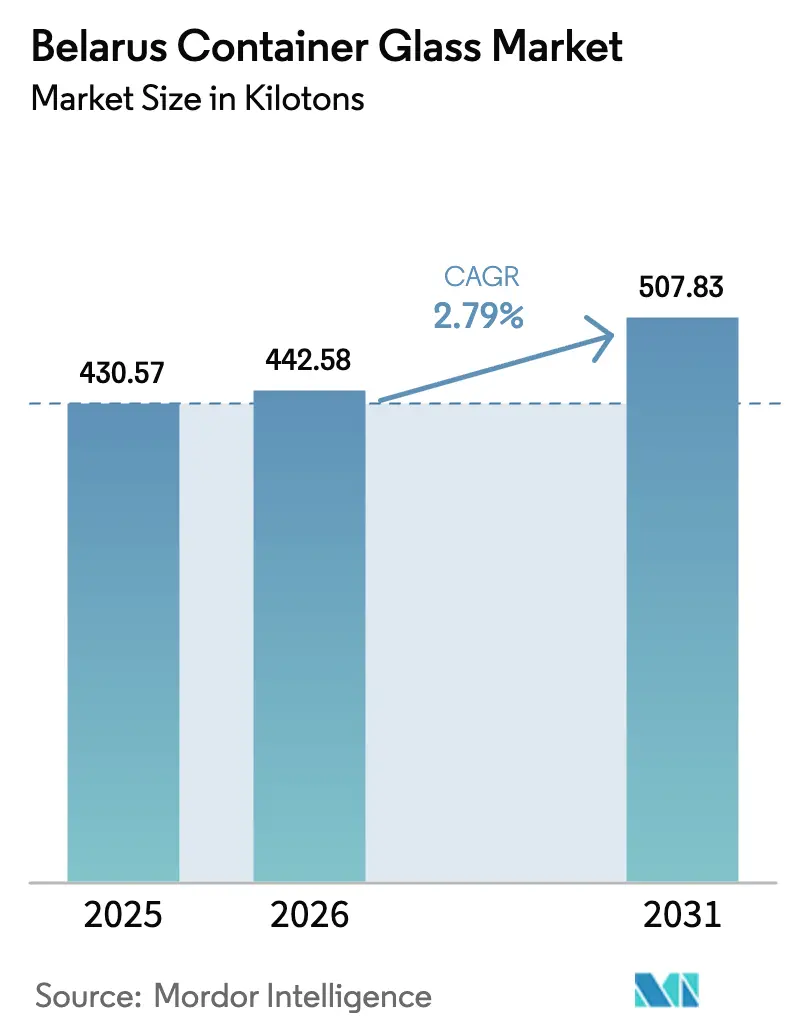

| Base Year Market Size (2025) | 430.57 kilotons |

| Market Volume (2026) | 442.58 kilotons |

| Market Volume (2031) | 507.83 kilotons |

| Growth Rate (2026 - 2031) | 2.79% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Belarus Container Glass Market Analysis by Mordor Intelligence

Belarus container glass market size in 2026 is estimated at 442.58 kilotons, growing from 2025 value of 430.57 kilotons with 2031 projections showing 507.83 kilotons, growing at 2.79% CAGR over 2026-2031. Stable demand from beverage fillers, regulatory tailwinds for recyclable packaging, and the country’s advantageous position along the China-Europe rail corridor underpin this growth. Rising craft-beer bottling volumes, the EU’s carbon border adjustment mechanism, which favors glass, and amber glass requirements for serialized pharmaceuticals collectively strengthen order books. At the same time, cost pressures from volatile natural gas prices and competition from low-priced PET imports restrain margins, prompting manufacturers to adopt lightweight press-and-blow technology and increase cullet use to manage fuel intensity. Strategic investments in furnace upgrades and logistics optimization are therefore emerging as key differentiators for producers seeking to defend or expand their market share in Belarus' container glass market.

Key Report Takeaways

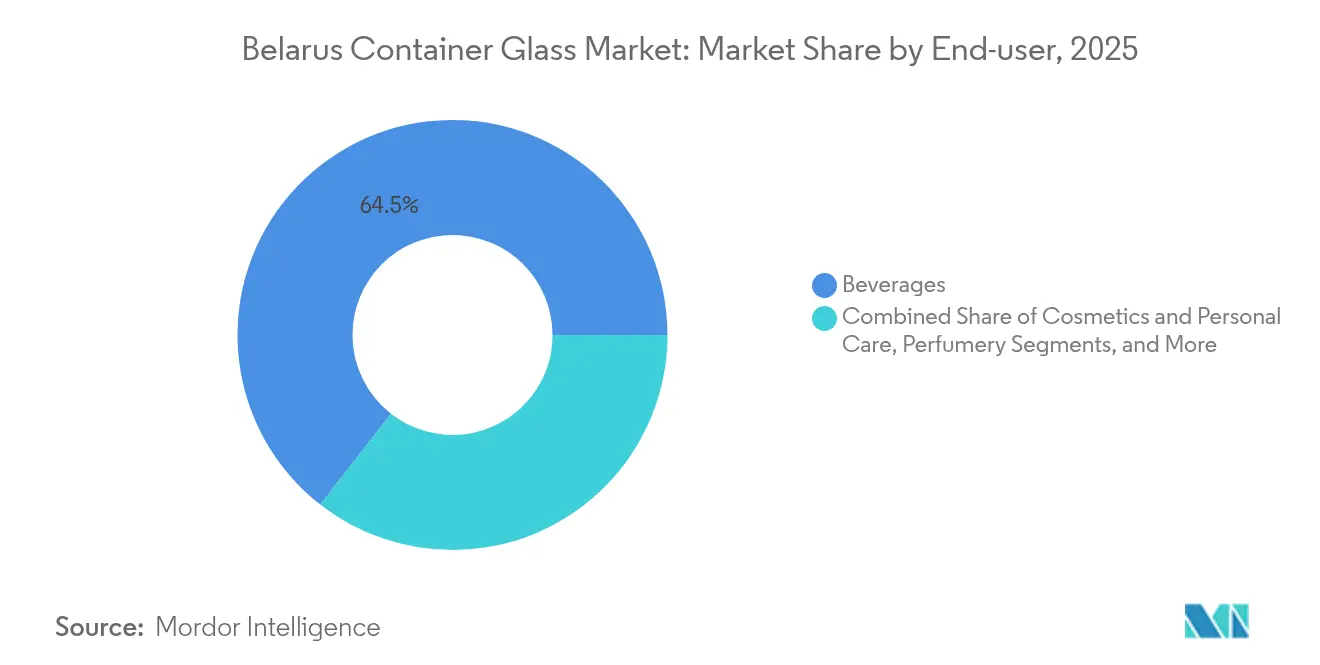

- By application, beverages captured 64.45% of the Belarus container glass market share in 2025.

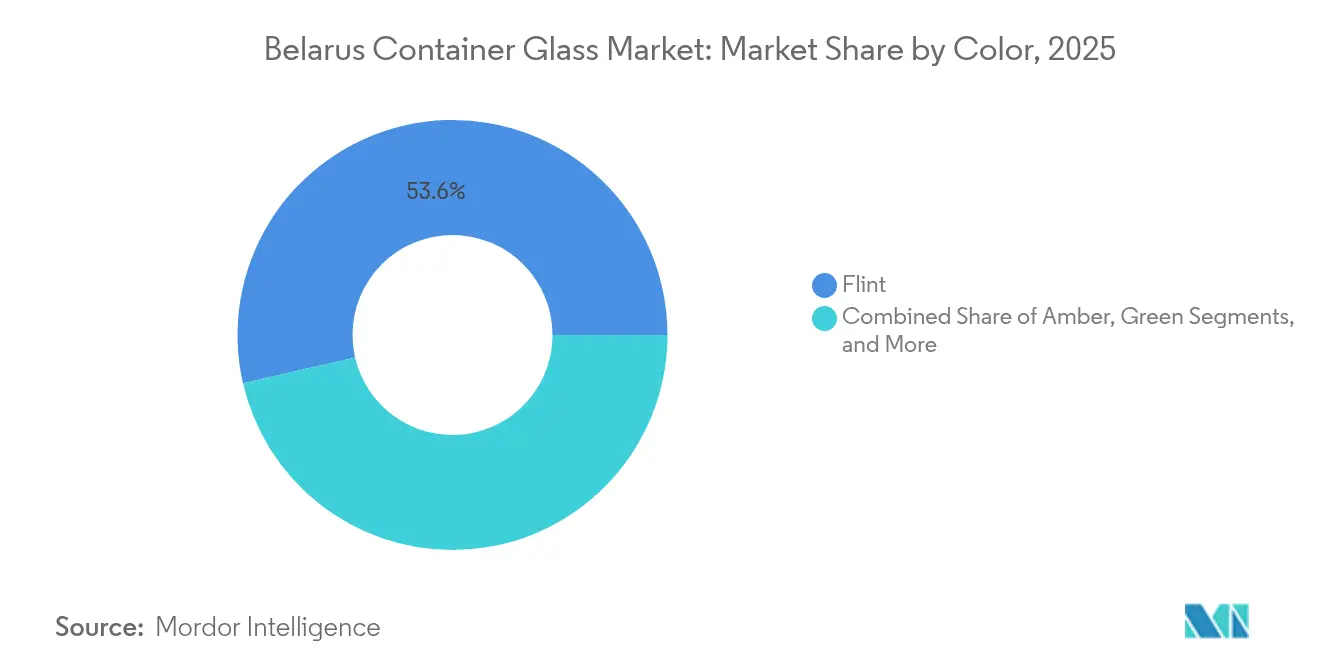

- By color, the Belarus container glass market size for the amber glass segment is projected to grow at a 4.55% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Belarus Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in local craft-beer bottling demand | +0.8% | National, Minsk, and regional centers | Medium term (2-4 years) |

| EU carbon border tax favors glass recyclability | +0.6% | Export-oriented plants serving the EU | Long term (≥ 4 years) |

| Pharmaceutical serialization is pushing amber glass | +0.4% | Nationwide, spillover to CIS | Short term (≤ 2 years) |

| Belarus–China rail corridor boosting export orders | +0.3% | Rail-linked industrial hubs | Medium term (2-4 years) |

| Rising adoption of lightweight press-and-blow technology | +0.2% | Major factories countrywide | Long term (≥ 4 years) |

| State subsidy for cullet logistics networks | +0.1% | Urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Local Craft-Beer Bottling Demand

Local breweries are scaling up their output and favoring premium, often embossed, amber or flint bottles to convey their artisanal quality. Many contracts are structured around shorter production runs, allowing producers to charge higher unit prices while maintaining high line utilization. Nationwide craft-beer volume has grown by more than 25% annually since 2022, and this momentum is expected to continue as licensing reforms simplify market entry for microbreweries.[1]Brewers Association, “Craft Beer Packaging Trends,” brewersassociation.org Bottle suppliers capable of delivering flexible molds and rapid color changeovers are capturing the bulk of these incremental orders.

EU Carbon Border Tax Favoring Glass Recyclability

The Carbon Border Adjustment Mechanism phases in full charges on embedded emissions from 2026, sharply raising delivered costs for higher-carbon PET and aluminum packaging imported to the bloc.[2]European Medicines Agency, “Falsified Medicines Directive,” ema.europa.eu Belarus glass exporters, already integrated into cullet collection networks, face lower tariffs because recycled glass requires up to 30% less energy than virgin feed. Forward contracts signed with EU beverage and cosmetics brands increasingly specify glass in place of PET, consolidating a long-term order pipeline for Belarus container glass market producers.

Pharmaceutical Serialization Pushing Amber Glass

The Falsified Medicines Directive now mandates tamper-evident, traceable packaging, and amber glass is preferred for light-sensitive active ingredients. Belarus drug-fillers intent on exporting to the EU have therefore ramped up purchase commitments for amber containers, boosting furnace utilization rates dedicated to this color. Because amber runs involve lower output volumes and longer batch changeovers, producers secure a price premium and raise blended operating margins.

Belarus-China Rail Corridor Boosting Export Orders

Regular freight services on the Belt and Road corridor cut transit times to inland Chinese hubs by around 30% compared with maritime routes. Spirits and pharmaceutical companies in China are now sourcing specialty bottles from Belarus at competitive landed costs. The corridor’s reliability, combined with export-credit insurance backed by state banks, reduces payment risk and encourages manufacturers to commit extra furnace capacity for Asian call-offs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cheap PET imports from Russia and Ukraine | -0.5% | Nationwide beverages and food | Short term (≤ 2 years) |

| Natural-gas price volatility is impacting furnace OPEX | -0.4% | Energy-intensive plants | Medium term (2-4 years) |

| Skilled-labor migration to EU neighbors | -0.3% | Border regions | Long term (≥ 4 years) |

| Limited domestic soda-ash supply | -0.2% | All glassworks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cheap PET Imports from Russia and Ukraine

Russian PET producers, contending with sanctions-related oversupply, are pricing aggressively into Belarus, undercutting glass for mainstream soft drinks and bottled water by up to 40%.[3]Reuters, “Russia's Petrochemical Sector Adapts to Sanctions,” reuters.com Beverage fillers prioritizing cost over premium brand cues are switching formats, denting baseline order volume for flint bottles. Glass manufacturers are responding by emphasizing superior recyclability and developing lightweight designs to narrow the delivered-cost gap.

Natural-Gas Price Volatility Impacting Furnace OPEX

Natural gas supplies 62.8% of Belarus' industrial energy, and spot price swings directly impact furnace costs, which can account for 30% of ex-works bottle prices. Because hot-end shutdowns jeopardize refractory life, producers have limited flexibility to throttle output. This cost unpredictability deters some smaller firms from investing in new capacity and drives collective interest in higher cullet ratios, electric boosting, and waste-heat recovery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Beverages Sustain Scale while Cosmetics Accelerate

The beverages segment accounted for 64.45% of the Belarus container glass market size in 2025, reflecting a strong preference for glass bottles among domestic beer, wine, and spirits producers. Demand persists as premiumization trends encourage heavier embossing, unique shapes, and limited-edition packaging, driving the market forward. Craft brewers in Minsk are placing frequent small-batch orders, supporting niche mold development and shortening payback periods for digital decoration lines. Non-alcoholic fillers, although experimenting with aluminum cans, still reserve glass for flagship SKUs that target upscale retail channels. Over the forecast period, incremental consumption gains are expected from craft and low-alcohol beverages, maintaining the beverage share at a broadly stable level despite the substitution of PET in economy segments.

Cosmetics and personal care, although with a smaller base, are outpacing other uses at a 3.12% CAGR. Regional beauty brands are adding glass jars for high-end creams and serums, citing perceived premium positioning and recyclability. Contract packers are collaborating with Belarus mold shops to localize distinctive silhouettes previously imported from Western Europe, reducing lead times and currency exposure. In parallel, global cosmetics groups sourcing from Belarus plants are adding serialized QR codes onto bottle shoulders, linking consumers to ingredient traceability platforms and further differentiating glass from plastic alternatives.

By Color: Flint Holds Scale Advantage while Amber Commands Premiums

Flint bottles accounted for 53.60% of the Belarus container glass market share in 2025, driven by beverage lines that prioritize product visibility and utilize mature cold-end inspection technology. High pulling rates and standard neck finishes deliver cost leadership, enabling Flint to defend share even as PET prices fluctuate. Producers continue to shave weight by 15-20% using the press-and-blow method, partly offsetting energy-related cost escalations.

Amber glass, which is expanding at a 4.55% CAGR, is benefiting from growing pharmaceutical serialization and demand for craft beer. Amber furnaces, often segregated from flint to avoid color contamination, run shorter campaigns and incur higher unit costs. However, buyers pay premiums of 8-12% for light protection and regulatory compliance, lifting contribution margins. Investments in dual-stack forehearths enable faster color changes, opening the door to mid-scale craft beer orders without dedicating entire furnaces.

Geography Analysis

Domestic consumption remains anchored in urban corridors stretching from Minsk to Grodno, where beverage bottlers and pharmaceutical fillers cluster near rail nodes. Within these clusters, vertically integrated plants secure cullet from municipal recovery programs, keeping freight expenses minimal and improving lifecycle carbon scores. Annual recycling rates have climbed above 55% since 2024, narrowing the differential between Belarus' container glass market size growth and primary energy use.

On the export front, Western corridors into Poland and Lithuania support just-in-time deliveries to EU beverage fillers, which benefit from shorter lead times compared to suppliers in Asia or Latin America. The EU carbon border adjustment mechanism further enhances the competitiveness of Belarusian containers in these markets by imposing lower carbon levies relative to PET and virgin aluminum alternatives.

Eastbound, the Belt and Road rail corridor channels bottles toward Chongqing and Chengdu in as little as 14 days, opening Chinese niches for premium spirits and serialized APIs that demand glass packaging. Exporters favor full-train block consignments to secure volume discounts, while logistics partners offer repositioning services for empty pallets, thereby mitigating backhaul costs.

Geopolitical uncertainties, notably dependence on Russian natural gas transmitted via trans-border pipelines, pose locational risk. Manufacturers are hedging their risks by negotiating flexible take-or-pay clauses and exploring partial electrification options. Nonetheless, the geographic midpoint between EU markets and Central Asia remains a strategic asset, enabling producers to adjust shipments as demand fluctuates.

Competitive Landscape

The Belarusian container glass industry exhibits moderate concentration, with state-linked Belstekloprom and private OJSC Grodno Glass Factory leading the installed capacity. Together with three mid-tier producers, the top five operators account for roughly 65% of national output, fostering competition on technology upgrades rather than price alone. Vetropack, Gerresheimer, and Ardagh maintain commercial ties or minority stakes, channeling process know-how and compliance systems into local facilities.

Technology adoption is the principal arena of rivalry. Grodno’s 2024 furnace retrofit reduced gas consumption by 25% and increased cullet ratios to 60%, thereby reducing carbon intensity compared to EU benchmarks. Belstekloprom’s USD 10 million amber line, focusing on pharma bottles, aims to capitalize on the rising demand for serialization. Foreign groups are leveraging local wage advantages to run labor-intensive decoration or short-campaign specialty lines previously housed in Western Europe.

Supplier relationships are increasingly centered on multi-year volume commitments, coupled with joint sustainability targets. Beverage brand owners stipulate cullet content thresholds and impose scorecards on supplier energy mixes. This dynamic favors players with credible roadmaps to electric boosting and internal cullet processing, leaving laggards exposed to contract attrition.

Belarus Container Glass Industry Leaders

Belstekloprom JSC

Vedatranzit Glass Factory LLC

Premium Glass LLC

OJSC Grodno Glass Factory

OJSC Glassworks “Neman”

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Vetropack Holding AG invested EUR 15 million (USD 16.4 million) in lightweight glass technology upgrades across Eastern Europe, including prospective Belarus capacity.

- August 2024: Gerresheimer AG secured a USD 12 million multi-year amber-glass supply agreement with Belarus pharmaceutical firms.

- July 2024: OJSC Grodno Glass Factory completed a USD 8 million furnace modernization, cutting gas use by 25%.

- June 2024: Ardagh Group SA partnered with Belarus rail operators to accelerate China-bound shipments by 30%.

Belarus Container Glass Market Report Scope

Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents. It is often chosen for products where purity, safety, and environmental sustainability are paramount concerns.

The Belarus container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, and by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What will be the size of the Belarusian container glass market by 2031?

It is projected to reach 507.83 kilotons by 2031, up from 442.58 kilotons in 2026.

Which application drives the most volume?

Beverages remain dominant, accounting for 64.45% of 2025 shipments, and benefit from the expansion of craft beer.

Why is amber glass demand rising?

EU pharmaceutical serialization rules and the need for light-sensitive drug formulations are driving manufacturers to use amber bottles, resulting in increased amber volumes at a 4.55% CAGR.

How does the carbon border tax affect Belarus' glass exports?

Glass incurs lower carbon levies than PET or aluminum, making Belarus bottles more price-competitive in the EU.

What technologies improve cost competitiveness?

Lightweight press-and-blow, higher cullet ratios, and furnace electric boosting lower fuel intensity and production costs.

What is the main risk to supply stability?

Volatile natural-gas prices, given that gas supplies nearly two-thirds of industrial energy in Belarus.

Page last updated on: