Beer Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.71 Billion |

| Market Size (2031) | USD 30.27 Billion |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

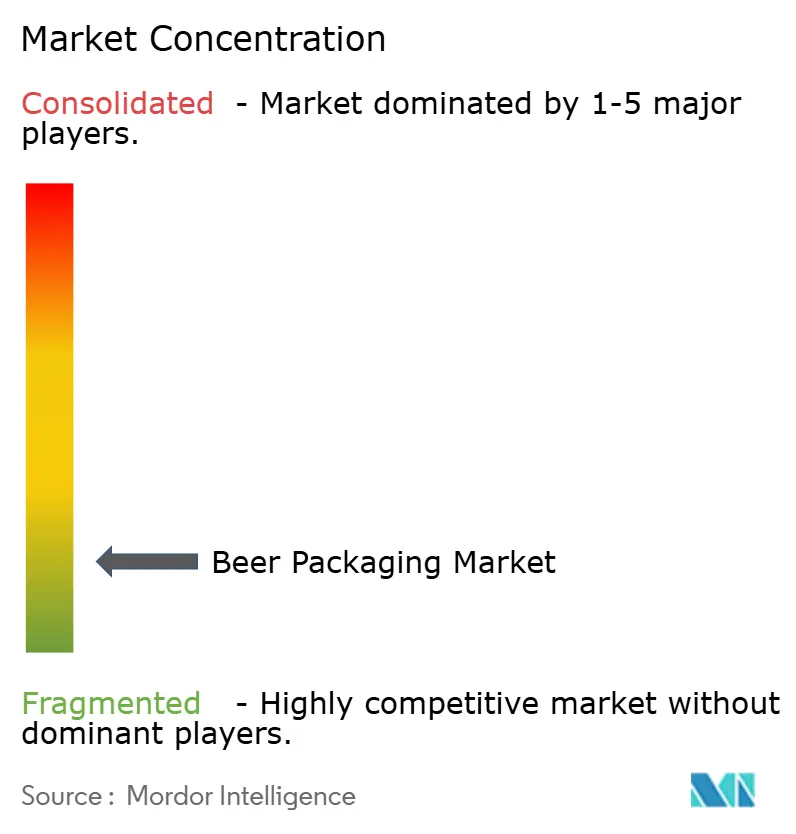

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Beer Packaging Market Analysis by Mordor Intelligence

Beer packaging market size in 2026 is estimated at USD 25.71 billion, growing from 2025 value of USD 24.88 billion with 2031 projections showing USD 30.27 billion, growing at 3.32% CAGR over 2026-2031. This growth reflects rising demand for sustainable materials, the acceleration of premium formats, and ongoing shifts in consumption channels. Aluminum’s share continues to expand as recyclability and logistics efficiency attract large and small brewers alike, while PET gains traction where cold-chain quality assurance is improving. Glass holds a clear lead in volume but now contends with cost pressures from energy-intensive production and heavier freight loads. Regional opportunities cluster in Asia-Pacific, where urbanization lifts packaged beer sales, and in North America, where craft breweries seek differentiated, eco-friendly formats that match retail shelf dynamics. Supply-side investments by leading can makers, glass producers, and flexible-pack specialists underline an industry pivot toward high-speed, low-waste technologies that cut material inputs and boost brand agility.

Key Report Takeaways

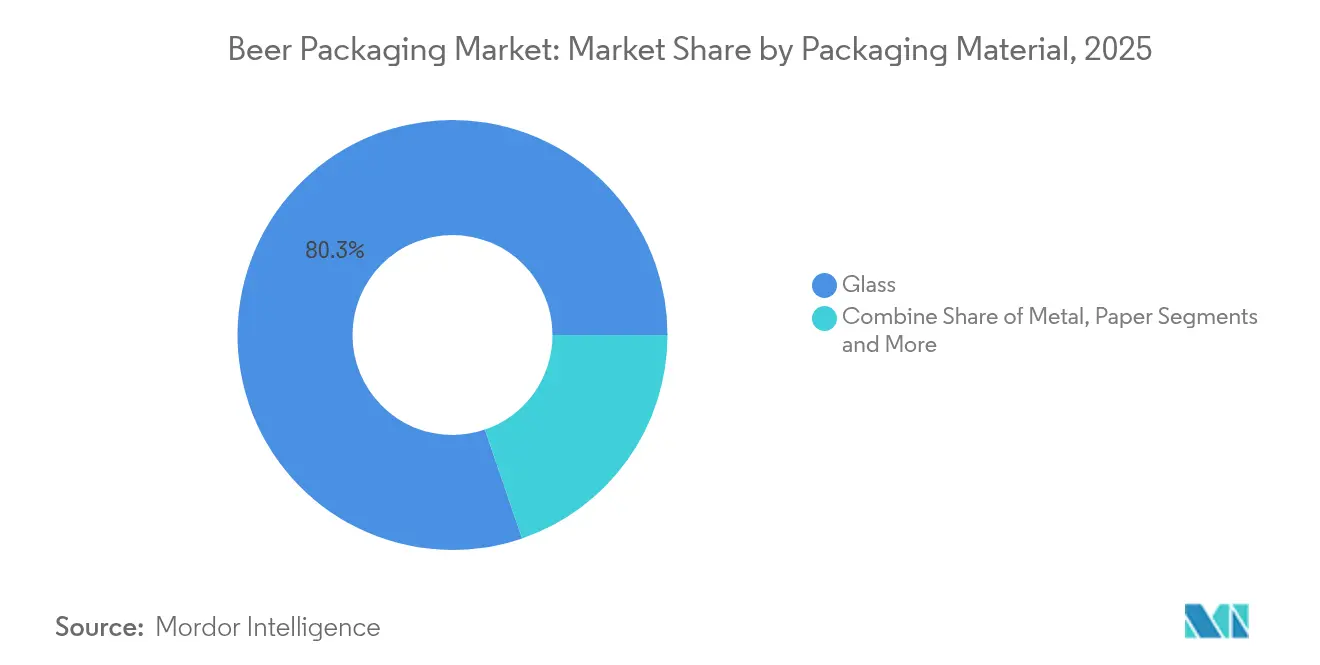

- By packaging material, glass commanded 80.25% of Beer packaging market share in 2025, while PET is projected to expand at a 5.52% CAGR through 2031.

- By packaging type, bottles led with a 74.64% share in 2025; cans are the fastest-growing at a 6.38% CAGR to 2031.

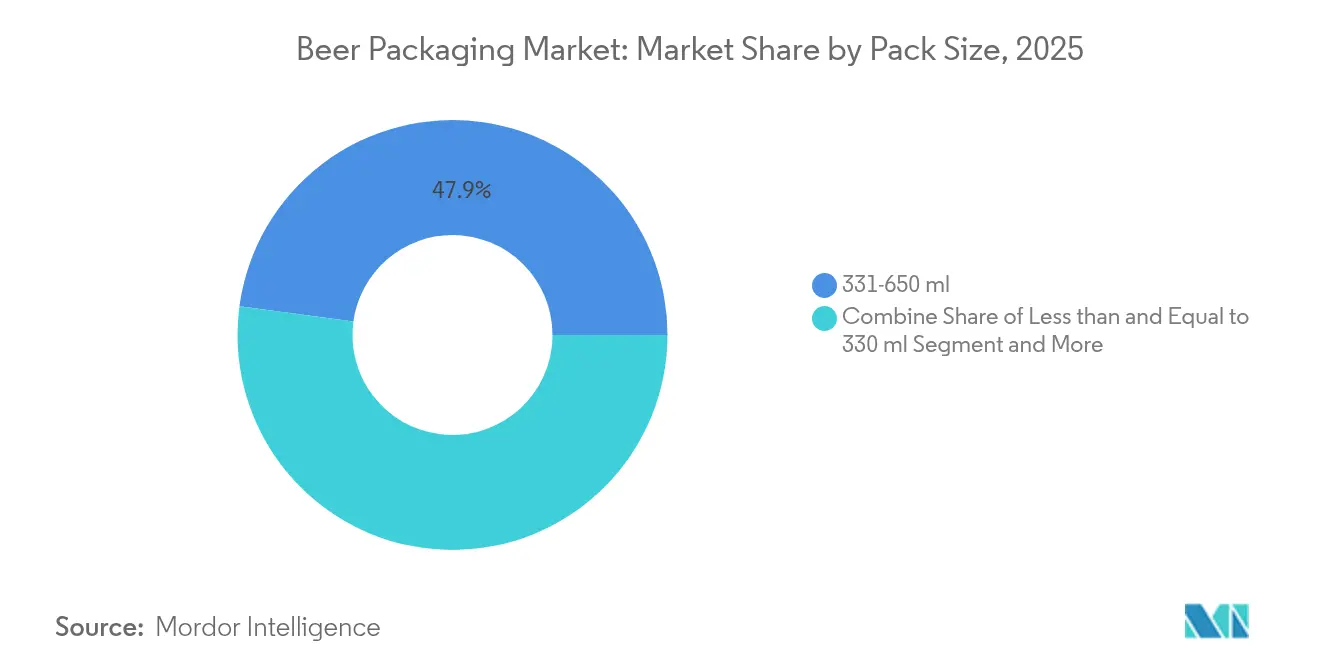

- By pack size, the 331–650 ml range accounted for 47.86% of Beer packaging market size in 2025, whereas formats above 650 ml are forecast to rise at a 4.89% CAGR.

- By distribution channel, direct sales captured 56.21% share in 2025, but indirect channels are advancing at a 4.31% CAGR.

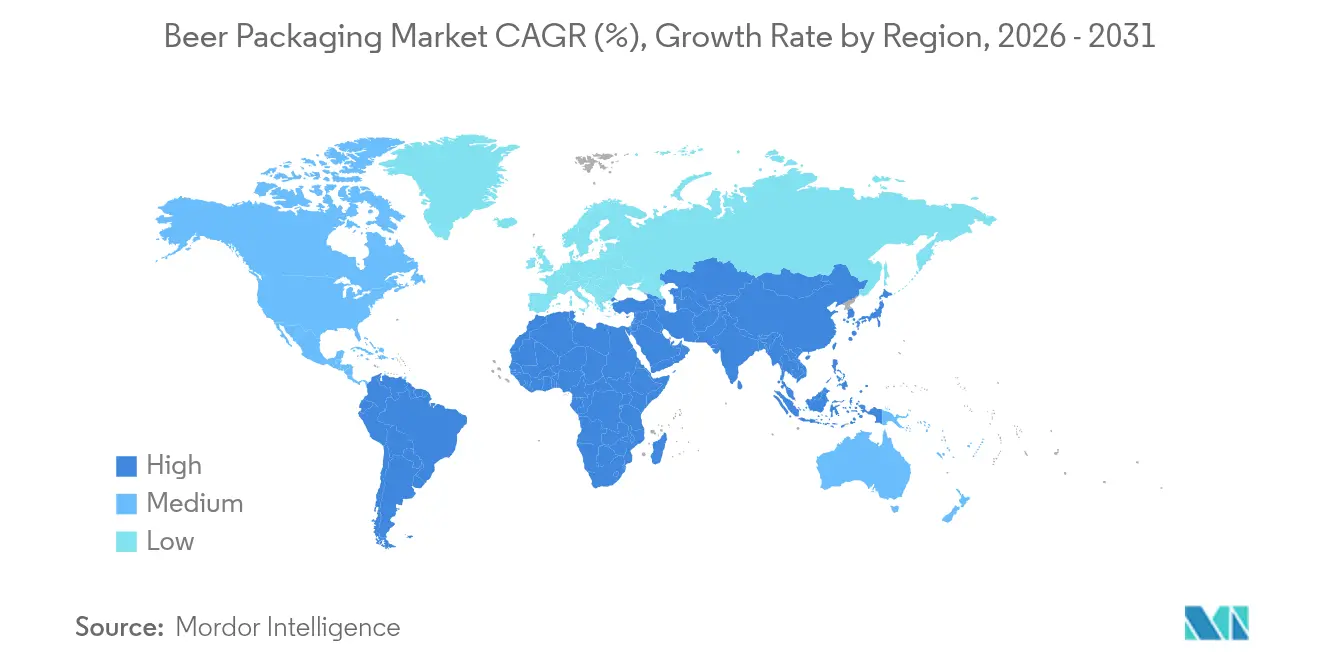

- By geography, Asia-Pacific held 38.05% share in 2025; North America posts the strongest CAGR at 6.08% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Beer Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in craft breweries driving short-run can designs in North America | +0.8% | North America, expansion to Europe | Medium term (2–4 years) |

| Rising adoption of lightweight returnable glass bottles backed by EU deposit-return schemes | +0.6% | Europe, notably Germany and France | Long term (≥ 4 years) |

| Rapid cold-chain expansion enabling PET penetration in Asian beer | +0.5% | Asia-Pacific, Southeast Asia focus | Medium term (2–4 years) |

| Brand premiumization fueling embossed specialty bottles among German breweries | +0.4% | Europe, premium segments | Long term (≥ 4 years) |

| Aluminum tariff cuts triggering can conversions in South America | +0.3% | South America, Brazil and Argentina | Short term (≤ 2 years) |

| E-commerce multipacks accelerating corrugated secondary packaging demand in the UK | +0.2% | Global, early adoption in the UK and North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surge in Craft Breweries Driving Short-Run Can Designs in North America

Craft brewery growth reshapes packaging economics as digital printing such as Ball’s Dynamark Advanced Pro lets multiple graphics run on one pallet, eliminating historic minimum-order barriers. [1]Ball Corporation, “Ball Introduces New Era of its Dynamark Printing Technology in EMEA,” ball.comFlexible can lines help brewers manage inventory, pilot new SKUs, and execute seasonal launches without excess glass bottle purchases. Though digital print premiums approach 300% over offset, the cost is offset by faster sell-through rates and stronger shelf appeal at more than 9,000 breweries across the region.

Rising Adoption of Lightweight Returnable Glass Bottles Backed by EU Deposit-Return Schemes

Mandated deposit systems achieve 98% return rates in Germany, prompting innovations like Vetropack’s Echovai tempered bottle that is 30% lighter yet rugged across multiple cycles.[2]Vetropack, “Echovai,” vetropack.com France’s rollout adds centralized washing hubs capable of 60 million bottles per year, shifting cost structures from one-way disposal toward circular asset management.

Rapid Cold-Chain Expansion Enabling PET Penetration in Asian Beer

Plasma-assisted chemical vapor deposition boosts oxygen-barrier performance by over 1,000-fold, letting PET maintain carbonation for extended shipping. Vietnam’s domestic converters scale capacity as island supply routes and urban on-the-go demand favor lighter bottles that cut freight costs by 70% versus glass.

Brand Premiumization Fueling Embossed Specialty Bottles Among German Breweries

Krombacher’s USD 107 million bottling revamp installs smart sorters and variable molds supporting artisanal embossing, while Veltins’ new lines hit 130,000 bottles per hour. Embossed glass pairs tactile cues with heritage designs to justify higher price points during premiumization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legislative bans on single-use plastics curtailing PET in Europe | -0.9% | Europe, potential wider adoption | Medium term (2–4 years) |

| Tight U.S. aluminum slab supply elevating can costs for craft brewers | -0.7% | North America, global aluminum effects | Short term (≤ 2 years) |

| Consumer shift to hard seltzers reducing glass volumes in Australia | -0.4% | Australia, regional spillover | Medium term (2–4 years) |

| High cap-ex for keg refurbishment limiting returnability in emerging markets | -0.3% | Emerging markets, infrastructure gap | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legislative Bans on Single-Use Plastics Curtailing PET in Europe

The EU Packaging and Packaging Waste Regulation enforces 30% recycled content by 2030 and phases out targeted formats from 2025. [3]European Parliament, “New EU rules to reduce, reuse and recycle packaging,” europarl.europa.euExtended Producer Responsibility fees raise PET costs relative to infinitely recyclable aluminum, prompting portfolio shifts toward metal and lightweight returnable glass.

Tight U.S. Aluminum Slab Supply Elevating Can Costs for Craft Brewers

Only five domestic smelters remain, and a 25% tariff imposed in 2025 worsens input shortages. Craft brewers, buying via distributors, pay mark-ups that threaten seasonal release timing and force reconsideration of glass despite higher freight expenses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Material: Aluminum and PET Erode Long-Held Glass Advantage

Glass preserved an 80.25% share in 2025 due to sensory neutrality and entrenched consumer associations. Yet aluminum’s recyclability edge and transportation savings peel away volume, aided by policy targets for 100% recyclable packaging by 2030. PET, advancing at 5.52% CAGR, draws on barrier-coated bottles that now satisfy beer’s carbonation needs, while paper remains confined to secondary packs.

Rising energy costs and carbon levies widen aluminum’s total-cost edge over furnace-fired glass. Meanwhile, innovations like bio-paraxylene PET from used cooking oil improve brand credentials and foreshadow broader polymer adoption. Brewers keep niche glass SKUs for premium variants, but the Beer packaging market increasingly redirects new capacity toward lighter substrates.

By Packaging Type: Bottle Legacy Versus Can Momentum

Bottles supplied 74.64% of global volume in 2025. Still, cans are accelerating at a 6.38% CAGR as dynamism in craft beer, convenience shopping, and outdoor consumption tips formats in favor of metal. Keg growth remains muted by cleaning-system cap-ex in emerging regions, and pouches stay marginal.

Digital printing lets small brewers match multinational packaging quality, increasing SKU churn without wasteful overruns. Investment in regional can lines, as seen in Brazil, further scales economies that shrink per-unit costs and enhance availability.

Glass manufacturers counter with embossing and tapered profiles that lift perceived value on-premise.

By Pack Size: Mid-Range Stability with Upsized Premium Plays

The 331–650 ml range represented 47.86% of Beer packaging market size in 2025, offering price-per-sip balance across mainstream retail. Larger bottles above 650 ml rise at 4.89% CAGR, leveraged by craft brewers who position 750 ml formats as shareable, gift-ready experiences. Small cans and stubbies retain a role in regulated portion markets but face cost-of-goods pressure where packaging weight represents a bigger cost share.

Capacity upgrades that hit six-figure bottle-per-hour rates allow simultaneous runs of multiple sizes, reducing changeover time and supporting seasonal mixed-pack strategies. Logistics efficiencies favor bigger units for export corridors, while convenience stores prioritize mid-sizes that fit limited shelf footprints.

By Distribution Channel: Direct Dominates Yet Omnichannel Gains

Direct brewery-to-retail pathways held 56.21% share in 2025, driven by on-premise keg and bottle return loops. However, indirect channels grow faster at 4.31% CAGR as supermarkets, convenience stores, and e-commerce enlarge their beer aisles. Corrugated shippers designed for doorstep delivery reshape secondary packaging, embedding QR codes that guide consumers to brand content.

Contract brewing agreements, like Pabst’s 2025 switch to Anheuser-Busch InBev plants, demonstrate hybrid models that blend scale efficiency with brand autonomy. Breweries diversify route-to-market choices to buffer against demand shocks and tariff-driven margin swings.

Geography Analysis

Asia-Pacific led with 38.05% share in 2025, underpinned by population scale, climbing incomes, and rapid urbanization that favor packaged formats. Cold-chain expansion in Vietnam and Indonesia supports PET penetration, while China’s craft segment grew to CNY 33.1 billion in 2024, fostering boutique can designs and gift-oriented glass bottles alike.

North America posts the fastest 6.08% CAGR through 2031. More than 9,000 craft breweries generate steady demand for short-run cans, though tariff and slab shortages inflate costs. Investments such as Ball’s Florida acquisition streamline supply networks and add sustainable capacity, reinforcing aluminum’s role as the region’s growth engine.

Europe remains a premium stronghold but confronts flat per-capita beer intake. The EU’s recyclability mandate triggers capital shifts into tempered, returnable glass and high-recycled-content cans. German breweries showcase premium packaging by installing embossed lines that hit industrial speeds while meeting circular-economy KPIs.

Regulatory Landscape

Packaging rules are tightening around recyclability, labeling, and recycled-content verification, which directly affects beer packaging material and format choices. In the European Union, Regulation (EU) 2025/40 (Packaging and Packaging Waste Regulation) applies from 12 August 2026, raising compliance requirements for packaging sustainability and labeling. It also reinforces the shift toward highly recyclable substrates and reuse systems that can work under deposit-return schemes.

Verification is being standardized as well. The EU adopted Commission Implementing Decision (EU) 2026/1425 on 30 June 2026, setting calculation and verification rules for recycled plastic content in single-use beverage bottles, which affects how PET packaging claims are substantiated. Outside Europe, China issued GB/T 45318-2025 for PET beer bottles on 28 February 2025 (effective 1 September 2025), while India issued the Cookware, Utensils and Cans for Foods and Beverages (Quality Control) Order, 2026 on 15 January 2026 (DPIIT), mandating BIS certification for aluminum cans under IS 14407:2023, with staged implementation deadlines starting 1 October 2026 for large enterprises.

Competitive Landscape

The Beer packaging market is fragmented, with strategic moves centered on sustainability, scale, and digital workflow. Crown Holdings operates 195 plants across 39 nations, deriving 67% of revenue from beverage cans and expanding high-speed South American lines. Ball ships roughly 48 billion aluminum containers annually in North America, owns 34% regional share, and has set a 55% greenhouse-gas cut target for 2030.

M&A furthers material science reach: Ball bought Spain-based Alucan in 2024 to broaden extruded packaging, while Amcor’s USD 8.43 billion union with Berry Global aims for USD 650 million synergies and stronger bio-based polymer R&D. Glass suppliers answer with tempered, light-weight tech and high-speed digital decoration that preserve heritage aesthetics while lowering carbon.

Digital print, barrier coatings, and smart QR labels form the next battleground. Dynamark’s pallet-level art variation democratizes limited-edition releases, while PET coatings extend shelf life to unlock regions where cold storage was once a constraint. Leading suppliers channel R&D toward these value-added areas to defend share against agile newcomers.

Beer Packaging Industry Leaders

Amcor Limited

Crown Holdings Incorporated

Ball Corporation

Tetra Laval International SA

O-I Glass Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Reuse and return models are creating whitespace in durable primary packs, and track-and-trace enablement that can operate at retail scale. This is paired with the secondary packaging needed for reverse logistics. LIONs June 2026 Steinlager pilot in 48 Auckland stores introduced a returnable crate and bottle system that replaces traditional deposits with digital tracking, highlighting practical demand for standardized returnable glass footprints, retailer-friendly handling, and packaging components that maintain performance across multiple washing cycles.

Capacity and flexibility investments by brewers and can makers are also opening near-term opportunities for suppliers that can shorten lead times and support SKU proliferation, particularly as cans gain share. Carlsberg India commissioned a new canning line in Mysuru in January 2026 (22,000 cans per hour, INR 100 crore), and Heinekens Passos, Brazil brewery reported reaching 1 million hectoliters (about 300 million cans) within four months of its November 2025 inauguration, reflecting an operational focus on scalable can availability. On the technology side, reusable PET designed to run on conventional glass bottling and washing infrastructure (for example, Petainers May 2026 launch) and lightweighting initiatives in aluminum packaging create openings for material suppliers and converters that can balance downgauging, recycled content, and line compatibility under evolving recycled-content verification and labeling requirements.

Recent Industry Developments

- April 2026: Crown Holdings announced plans to build a two-line beverage can manufacturing facility in Northern India, supported by a partnership with United Breweries Limited. The project targets operations in the second half of 2027 and is positioned to supply both alcoholic and non-alcoholic customers. The expansion increases regional can supply in a high-growth market and reduces dependence on long-haul can shipments.

- April 2025: Amcor completed an all-stock combination with Berry Global. The transaction strengthens Amcor's scale across rigid and flexible packaging formats and broadens its R&D and manufacturing footprint relevant to beverage packaging. Consolidation at this level can reshape supplier bargaining power and accelerate the rollout of recyclable and reusable packaging solutions across global beer value chains.

- July 2024: Ball Corporation acquired Alucan in Spain to broaden its extruded aluminum packaging portfolio. The acquisition extends Ball's capabilities beyond standard beverage cans into specialty aluminum formats and components. It also supports a wider offering for premium and differentiated beer packs where shape, durability, and lightweighting are used to improve shelf impact and logistics efficiency.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the beer packaging market covers the value of packs and containers used to store, transport, and sell beer, across common materials and formats used by brewers and filling partners in global trade.

Scope exclusions: We exclude brewing ingredients and beer production equipment, and we also exclude non-beer beverage packaging unless it is explicitly used for beer.

Segmentation Overview

- By Packaging Material

- Glass

- Metal

- PET

- Paper

- By Packaging Type

- Bottle

- Can

- Keg

- Pouches

- By Pack Size

- Less than 330 ml

- 331-650 ml

- More than 650 ml

- By Distribution Channel

- Direct Sales

- Indirect Sales

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic demand map for beer packaging and to set realistic bounds on volumes and pricing. We relied on public series such as national statistics on beer production and consumption, customs and trade data for glass containers and aluminum cans, and packaging waste and recycling datasets published by environment agencies.

To make the model more practical, we reviewed sources such as brewer and packaging company annual reports, investor presentations, and releases from packaging and beverage associations. We also used peer-reviewed papers on material shifts and lightweighting. For cross-checking company footprints and recent capacity moves, we used paid subscriptions that provide company financials and intelligence, plus a patent database to track packaging innovation activity. The sources listed here are illustrative, and additional public and paid references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating the split between bottles, cans, and kegs, and on understanding how pricing moves with can sheet costs, cullet availability, and freight. We spoke with packaging converters, can and glass supply chain participants, and commercial teams close to brewery procurement, then applied regional inputs to keep the global view balanced across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 12% | APAC: 53% |

| Mid tier: 50% | Functional/Unit leaders: 39% | EMEA: 29% |

| Smaller Players: 17% | Managers: 49% | Americas: 18% |

Market-Sizing & Forecasting

The sizing started from a top-down build where beer production and consumption by region were translated into packaging demand pools using pack mix indicators, refillable versus one-way tendencies, and on-trade versus off-trade shifts. Once the demand pools were established, the value layer was added using region specific price ranges for bottles, cans, and kegs, and then adjusted for pack size patterns (such as 330 ml versus larger formats) that change material use per unit.

To keep totals realistic, we corroborated the outputs with selective bottom-up checks, such as sampled supplier revenue exposure to beer packaging, channel checks on can line utilization, and simple ASP times volume approximations for major formats. Key inputs we tracked included aluminum can adoption, glass bottle reuse rates where relevant, keg circulation in on-premise channels, recycling and deposit scheme intensity, and freight and energy cost pressure that changes packaging conversion pricing.

For forecasting, scenario analysis was used because packaging mix shifts can change quickly when metal prices move or when sustainability rules tighten. The forward view was anchored on expected beer volume trends, packaging material substitution rates, and price pass-through timing, and gaps were handled by applying conservative ranges and then re-testing them through expert feedback before finalizing totals.

Data Validation & Update Cycle

Outputs were checked against independent signals such as beer volume trends, packaging material trade flows, and public capacity announcements, and then reviewed for unexpected jumps by region or format. When variances were large, assumptions on pack mix, reuse intensity, or pricing were revisited, followed by re-contact with select primary respondents to confirm what changed.

A multi-step review was followed before sign-off, including internal checks on math integrity, unit consistency, and year-over-year movement reasonableness. Reports refresh annually, and interim updates are triggered when a material event occurs, such as major input cost swings, regulation changes affecting packaging waste, or capacity disruptions. Before delivery, a fresh analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's Beer Packaging Market Estimate Compared With Other Published Estimates

Published market sizes for beer packaging do not always match because each publisher draws the boundary differently and also uses different timing for prices and currency conversion. The differences usually show up in what is counted as packaging (primary only versus primary plus secondary), how kegs are treated, and whether pricing is built from observable material and conversion signals.

Beer production and consumption direction by region, along with format mix checks from primary calls and trade-linked material signals, are the evidence points that keep Mordor Intelligence's 2026 estimate tied to packaging actually used for beer filling and distribution. When those signals are not used consistently, totals can drift due to broader packaging scope, more aggressive price progression, or less frequent refreshes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 25.71 B (2026) | |

| Global Consultancy A | USD 25.66 B (2024) | Uses a different base year and growth window, and the definition appears to mix end-use channel lenses that can shift what is counted as packaging revenue in beer. |

| Industry Publisher B | USD 26.00 B (2025) | Often includes a broader packaging scope (frequently blending primary and secondary packaging) and applies longer-horizon price growth assumptions, which can lift totals even if beer volumes are steady. |

The table shows that the spread is mostly explained by boundary choices and timing, not by a dispute on beer volumes. By keeping packaging scope tied to beer formats, using observable mix and pricing inputs, and then pressure-testing totals with selective supplier and channel checks, the estimate stays traceable to repeatable steps that a buyer can follow year to year.

Key Questions Answered in the Report

What is the projected CAGR for the Beer packaging market from 2026 to 2031?

The market is forecast to expand at a 3.32% CAGR over the period.

Which packaging material is growing fastest in the Beer packaging industry?

PET shows the highest growth, advancing at a 5.52% CAGR through 2031 after recent barrier-coating breakthroughs.

Why are aluminum cans gaining share against glass bottles?

Aluminum offers lighter weight, infinite recyclability, and now benefits from digital printing that lowers minimum runs, helping breweries meet sustainability and convenience demands.

Which region will post the quickest Beer packaging market growth?

North America leads growth with a 6.08% CAGR, driven by craft brewery expansion and preference for recyclable cans.

How are EU regulations affecting packaging choices?

New rules require 100% recyclable formats by 2030 and higher recycled content, pushing brewers toward aluminum and lightweight returnable glass while restricting certain single-use plastics.

What role does e-commerce play in Beer packaging trends?

Online sales stimulate demand for robust corrugated secondary packs that protect products in transit and deliver a branded unboxing experience aligned with sustainability targets.

Page last updated on: