Germany Bathroom Furniture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.20 Billion |

| Market Size (2026) | USD 4.42 Billion |

| Market Size (2031) | USD 5.74 Billion |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Bathroom Furniture Market Analysis by Mordor Intelligence

Germany's bathroom furniture market size in 2026 is estimated at USD 4.42 billion, growing from 2025 value of USD 4.20 billion with 2031 projections showing USD 5.74 billion, growing at 5.33% CAGR over 2026-2031. Momentum is anchored in premiumization, sustainability, and technology, even as the broader construction sector wrestles with permitting delays and a 7.4% revenue dip at the start of 2024. Bath vanities remain the largest product category, while the commercial end-user segment outpaces residential growth due to hospitality refurbishments. Certified wood and recycled composites reinforce green credentials, and IoT-enabled mirrors or drawers recalibrate what constitutes “furniture,” keeping average selling prices resilient. Established brands such as Hansgrohe, Duravit, and Villeroy & Boch leverage design heritage and international distribution to defend their share, yet digital-first challengers chip away online, forcing incumbents to sharpen direct-to-consumer strategies.

Key Report Takeaways

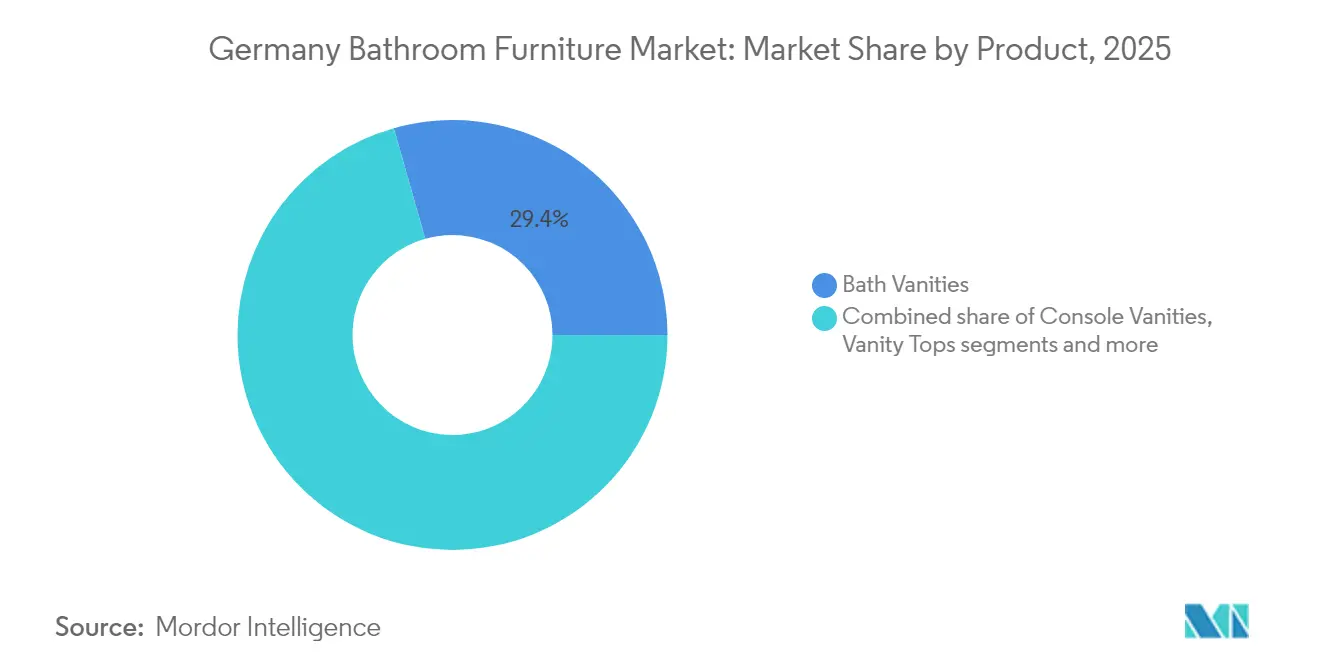

- By product, bath vanities led with 29.40% of Germany bathroom furniture market share in 2025; storage furniture & accessories are projected to grow at a 6.07% CAGR between 2026-2031.

- By material, wood captured 31.30% of Germany bathroom furniture market size in 2025; plastics and polymers are tracking a 5.72% CAGR through 2031.

- By price range, the mid-range tier represented 39.20% of Germany bathroom furniture market size in 2025, whereas premium lines expanded at a 6.24% CAGR.

- By end user, residential controlled 74.20% of Germany's bathroom furniture market size in 2025, while the commercial sector posts a 6.61% CAGR through 2031.

- By distribution, B2C/retail retained 59.10% value in 2025; direct B2B channels record the highest 6.14% CAGR on stronger manufacturer–specifier ties.

- By geography, North Rhine-Westphalia commanded 29.50% value in 2025, and Bavaria is the fastest-growing region with a 5.86% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Bathroom Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing housing stock renovations backed by federal subsidies | +1.8% | National; urban focal points | Medium term (2-4 years) |

| Adoption of smart IoT-enabled bathroom furniture with integrated lighting | +1.2% | Metropolitan areas first | Long term (≥4 years) |

| Premium sustainable design preference & eco certification influence | +1.0% | Affluent regions | Medium term (2-4 years) |

| Urban multifamily construction fueling compact modular solutions | +0.7% | Berlin, Munich, Hamburg | Medium term (2-4 years) |

| Rising e-commerce penetration enhancing product accessibility | +0.6% | Nationwide | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Ageing Housing Stock Renovations Backed by German Federal Subsidies

Federal housing programs allotting EUR 8 billion between 2018 and 2024 stimulate demand for retrofit-friendly vanities and storage kits that blend accessibility with aesthetics.[1]European Commission, “Supporting housing renovation in Germany,” ec.europa.eu Roughly one-quarter of Germany’s citizens are 60 +; yet only 2% of homes offer age-appropriate bathrooms, driving suppliers such as Duravit and Burgbad to pioneer grab-free drawer profiles and height-adjustable mirrors. Product specs increasingly match barrier-free guidelines without evoking institutional styling, supporting willingness to pay in the premium tier. Municipal subsidy portals further shorten payback periods for homeowners, keeping renovation pipelines active despite labor shortages.

Adoption of Smart IoT-Enabled Bathroom Furniture with Integrated Lighting

Voice- or app-controlled mirrors, LED-framed cabinets, and motion-triggered drawers reposition bathrooms as wellness hubs rather than functional volumes. Early uptake clusters in Berlin loft conversions, where tech-savvy professionals demand personalization and remote diagnostics. Manufacturers interlink faucets, lighting, and vanities to gather water-consumption data, aligning with ESG targets of hotel operators. Brand ecosystems—Duravit’s D-Neo platform, Hansgrohe’s RainTunes lighting sync—lock customers into upgrade paths and help defend margin dilution from commodity imports.

Premium Sustainable Design Preference & Eco Certification Influence

PEFC-certified oak, water-based lacquers, and take-back schemes now decide brand choice for Gen-Y buyers who equate durability with environmental stewardship. Duravit’s cradle-to-cradle DuraCeram washbasins and Hansgrohe’s 98% raw-material recycling pilot testify to industry’s shift from compliance to proactive leadership.

Urban Multifamily Construction Fueling Compact Modular Solutions

Urban apartment construction is stretching every square meter, especially in cities such as Berlin and Hamburg, where housing shortages remain acute. Builders and renovators now favor wall-mounted vanities, slim storage towers, and other modular pieces that keep the floor clear and visually enlarge tight bathrooms while still offering generous shelving. Although Germany completed only about 270,000 of its 400,000-unit annual housing goal in 2024, the ongoing pipeline keeps demand high for furniture that packs multiple functions into a single body—think vanity bases that conceal a washer-dryer or mirror cabinets with discreet ventilation fans to cut down on steam [2]FIEC. "Germany - FIEC Statistical Report." fiec-statistical-report.eu/germany..

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labour shortages & long permitting delaying renovation cycles | -0.9% | More acute in rural zones | Medium term (2-4 years) |

| Escalating raw-material costs compressing manufacturer margins | -0.7% | Nationwide | Short term (≤2 years) |

| Price pressure from DIY chains on branded furniture vendors | -0.5% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Labour Shortages & Long Permitting Delaying Renovation Cycles

Planning permissions for new homes slumped by 24.2% year-over-year in May 2024, extending project lead times and inflating subcontractor rates. Multitrade coordination—plumbers, tilers, electricians—makes bathrooms especially vulnerable, pushing some consumers to defer upgrades. Industry responds with prefab panel systems and tool-free fittings that shave labor hours, yet cannot fully offset structural shortages.

Escalating Raw-Material Costs Compressing Manufacturer Margins

Rising raw material costs are squeezing profit margins across the bathroom furniture value chain, forcing manufacturers to choose between absorbing costs or risking market share through price increases. After a 7.4% jump in 2023, construction inputs moderated to a 2.6% rise in 2024 but still squeeze mid-tier makers lacking brand-led price power. Proprietary composites such as Duravit’s DuroCast allow partial substitution of costlier resins, while group purchasing with faucet divisions hedges steel contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Smart Integration Drives Storage Growth

Storage furniture is forecasted to climb at a 6.07% CAGR, outstripping the overall category pace. Wi-Fi-enabled drawers that log cosmetics expiry dates and humidity-resistant shelving target compact urban bathrooms. Bath vanities retained a commanding 29.40% German bathroom furniture market share in 2025 and anchor renovation budgets because countertop and basin selection set the aesthetic tone. Console variants and mirrors adopt LED backlighting, defogging films, and Bluetooth speakers, weaving technology into traditional silhouettes. Competition pivots from raw volume to software interoperability that locks users into brand ecosystems.

Demand for modular storage also benefits from demographic aging: slide-out laundry hampers mitigate bending, while adjustable shelving adapts to children's growth. Premium lines such as Duravit’s Aurena collection introduce porcelain-clad dividers that merge hygienic surfaces with high-design cues. As adoption broadens, suppliers experiment with subscription-based filter replacements for mirror-integrated air purifiers, crystallizing annuity revenue.

By Material: Sustainability Reshapes Material Choices

Wood’s warm tactility and carbon-sink narrative underpin its 31.30% share of Germany bathroom furniture market size in 2025. FSC- or PEFC-certified oak and walnut remain hero finishes, yet veneer thicknesses shrink to reduce material intensity without visual compromise. Cross-laminated panels with bio-based adhesives improve moisture resilience, extending warranty periods. Plastics and advanced polymers trail but clock the highest 5.72% CAGR. WPC blends, commercialized by the LIMOWOOD consortium, divert landfill waste while achieving Class B fire ratings, attracting hospitality specifiers. Hybrid assemblies—oak drawer fronts on recycled-PET carcasses carry aesthetics with resource efficiency and facilitate easier disassembly at the end of life.

Metal frames re-emerge as accents, allowing thinner carcass walls and floating effects. Powder-coated aluminum in matte pastel tones answers pastel design trends forecasted for 2026 interiors. Ceramic or solid-surface tops integrate overflow-free drains to reduce water use, echoing broader German plumbing codes.

By Price Range: Premium Segment Defies Economic Headwinds

Premium models hold niche volume but deliver disproportionate profit, growing at 6.24% CAGR. Partnerships with global design icons—e.g., Philippe Starck for Duravit—elevate brand stories, enabling average gross margins beyond 40%. Mid-range units represent the workhorse 39.20% share of the German bathroom furniture market. Economy SKUs cater to do-it-yourself remodeling but face stagnation as inflation hits discretionary spending.

Product mix is tilting toward “affordable luxury,” where mid-tier carcasses pair with premium handles or smart mirrors offered as upsell modules. Such micro-segmenting lets brands defend price ladders without alienating value hunters.

By End User: Commercial Sector Accelerates Modernization

Corporate wellness programs and hotel pipeline refurbishments propel the commercial tier at 6.61% CAGR, versus modest residential expansion. Occupancy-driven ROI models prioritize durable laminates, anti-fingerprint coatings, and IoT sensors that count traffic for cleaning schedules. Public restrooms in airports integrate vanities with concealed paper-towel bins and maintenance alerts, trimming facility costs. Residential buyers, still 74.20% of volume, oscillate between minimalistic Scandinavian influences and maximalist color blocking. Aging-in-place retrofits introduce grab bars disguised as towel rails and vanities with knee clearance for seated use, blurring disability and mainstream design language.

By Distribution Channel: Digital Transformation Reshapes Buying Journey

B2B/direct sales outpace at 6.14% CAGR as architects request factory-configured sets and BIM files directly from manufacturers’ portals. Project dashboards synchronize logistics for multi-floor hotel rollouts, compressing lead times. Conversely, B2C/retail retains 59.10% share by virtue of foot-traffic visibility and hands-on evaluation. Omnichannel is no longer optional: QR codes on showroom tags open AR overlays showing color variants, then route to e-cart checkout. Returns logistics, once a deterrent, now mirror apparel industry efficiency, further lifting online penetration.

Geography Analysis

North Rhine-Westphalia commands a 29.50% value share thanks to dense urban demand from Cologne, Düsseldorf, and Dortmund. A sizeable ageing housing stock intersects with high disposable income, supporting uptake of premium, accessibility-friendly vanities. Concentration of showrooms and logistics hubs shortens delivery lead times, enticing consumers toward larger, customized solutions.

Bavaria earns fastest-growing status at a 5.86% CAGR as Munich and Nuremberg sustain robust construction pipelines. Tourism inflow prompts hotel bathroom refurbishments that ripple to residential aspirations, particularly for eco-labelled furniture, given Bavarian environmental sensibilities. Regional proximity to Baden-Württemberg manufacturing clusters streamlines supply chains and facilitates showroom inventory rotation.

Eastern Länder retrofit Soviet-era flats, favoring budget-aware mid-range lines, while Hamburg’s micro-apartments push ultra-compact modular vanities. National targets of 400,000 new homes annually, though under-delivered, still buoy region-wide demand for space-efficient and sustainable furniture .

Competitive Landscape

Germany bathroom furniture market features a moderately concentrated structure. Duravit sustains brand equity through frequent collaborations and its climate-neutral pledge targeting Scope 1 & 2 emissions by 2045. Hansgrohe expands beyond brassware by releasing vanity lines co-designed with Phoenix Design, seeking to cross-sell into its faucet install base. Villeroy & Boch leverages its ceramics heritage to market integrated countertop-basin slabs that dovetail with its tile business.

Nimble entrants like VALLONE differentiate through direct-to-architect models and mass-customization, while DIY private labels nibble low-end volume. Innovation races beyond materials toward service layers: augmented-reality apps, five-day custom color lead times, and post-purchase maintenance analytics. Sustainability remains a showdown arena; Hansgrohe’s zero-plastic packaging pledge by 2025 and Duravit’s post-consumer take-back program set benchmarks competitors must meet or exceed. Strategy convergence around full-suite bathroom solutions intensifies, with faucet, lighting, and furniture bundles promoting upselling synergies and supply-chain leverage.

Germany Bathroom Furniture Industry Leaders

-

Burgbad

-

Duravit AG

-

IKEA

-

Villeroy & Boch AG

-

Geberit AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: At ISH 2025, Laufen unveiled its forward-thinking "Bathroom of 2025" collection, featuring innovative smart ceramics, water-efficient technologies, and versatile bathroom furniture. This new lineup emphasizes sustainability and contemporary living, reshaping wellness spaces with its focus on integrated design, circular materials, and flexible storage options.

- October 2024: Kaldewei partnered with e15 and Stefan Diez on oak-based bathroom furniture reflecting circularity goals.

- May 2024: Hansgrohe Group committed to eliminating plastic from German product packaging by 2025, targeting an annual reduction of 312 tons.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Germany bathroom furniture market as all purpose-built vanities, cabinets, mirrored units, shelving, and auxiliary storage items that are factory-finished and sold for permanent installation in residential or commercial washrooms. Products can be freestanding or wall-mounted and are valued at transaction prices expressed in USD.

Scope Exclusion: Plumbing fixtures (sinks, faucets, toilets), decorative hardware, and loose accessories are not assessed.

Segmentation Overview

-

By Product

- Bath Vanities

- Console Vanities

- Vanity Tops

- Bathroom Mirrors

- Storage Furniture & Accessories

-

By Material

- Wood

- Metal

- Plastic & Polymer

- Other Material

-

By Price Range

- Economy

- Mid-range

- Premium / Luxury

-

By End User

- Residential

- Commercial

-

By Distribution Channel

-

B2C/Retail

- Home Centers

- Specialty Furniture Stores (including exclusive brand outlets)

- Online

- Other Distribution Channels (includes hypermarkets, supermarkets, teleshopping, warehouse clubs, departmental stores, etc.)

- B2B/Directly from Manufacturers

-

B2C/Retail

-

By Geography

- Bavaria

- Baden-Württemberg

- North Rhine-Westphalia

- Lower Saxony

- Hesse

- Rest of Germany

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed German joinery specialists, DIY-store buyers, e-commerce merchandisers, hotel fit-out contractors, and real-estate developers across Bavaria, NRW, and Berlin. These conversations validate penetration rates, replacement cycles, and realistic average selling prices; they close gaps left by fragmented secondary statistics.

Desk Research

We begin with national statistics from Destatis, Eurostat trade codes for HS 9403 sub-categories, building-permit data from the Federal Ministry for Housing, and consumer-spend series from the German Retail Federation. Trade association insights (Arbeitsgemeinschaft Die Moderne Badgestaltung), patent trends via Questel, and company filings enrich supply cues. Annual reports and investor decks of listed bath-furniture producers further anchor pricing bands and capacity shifts. Subscription datasets such as D&B Hoovers for company revenues and Dow Jones Factiva for deal flow give us longitudinal evidence on consolidation and channel expansion. The sources cited above illustrate our desk work; many additional public and paid references are consulted throughout the project.

Market-Sizing & Forecasting

A top-down build starts from total bathroom-related renovation and new-build spend, which is then apportioned using bathroom size norms, furniture take-rates, and unit ASPs. Supplier roll-ups and channel checks offer bottom-up cross-verification. Key variables include housing completions, hotel room pipeline, disposable-income growth, import value of HS 940360, the wood-based furniture price index, and furniture replacement intervals. Multivariate regression, stress-tested through scenario analysis, projects demand to 2030; any bottom-up gaps are interpolated with mean ASP trends derived from sampled retail audits.

Data Validation & Update Cycle

Outputs pass three-layer analyst review; variance flags trigger source re-checks, and abnormal swings are re-vetted with at least one fresh expert call. Reports refresh yearly and are mid-cycle updated if raw-material shocks, regulatory shifts, or large M&A events materially move the baseline.

Why Mordor's Germany Bathroom Furniture Baseline Commands Reliability

Published numbers differ widely because firms diverge on scope, currency treatment, and refresh cadence. Some inflate totals by folding modular kitchen cabinets or global revenues into the German bucket; others upscale list prices without discount calibration.

Key gap drivers versus our view include broader product baskets, aggressive mark-ups, and lighter validation of import-export offsets. Mordor's estimate rests on Germany-only transaction values, calibrated discounts, and yearly model renewal.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.20 Bn (2025) | Mordor Intelligence | - |

| USD 7.90 Bn (2024) | Global Consultancy A | Includes modular storage and applies list ASP; Germany share inferred from global ratios |

| USD 7.86 Bn (2024) | Industry Databook B | Uses revenue of top vendors without netting exports; model updated biennially |

Taken together, the comparison shows that once non-bath products, unadjusted price lists, and dated inputs are stripped out, Mordor delivers a balanced, transparent figure that users can reproduce with clear variables and repeatable steps.

Key Questions Answered in the Report

How big is the Germany bathroom furniture market in 2026?

Germany bathroom furniture market stands at USD 4.42 billion in 2026, with a projected CAGR of 5.33% to 2031.

Which product segment leads the Germany bathroom furniture market?

Bath vanities lead with 29.40% market share in 2025, while storage furniture shows the strongest 6.07% CAGR outlook.

What role does sustainability play in purchasing decisions?

Eco-certified materials and circular design now rank among the primary purchase criteria, lifting premium products that offer PEFC-certified wood or recycled composites.

Why is the commercial end-user segment growing faster than residential?

Hospitality renovations and corporate wellness investments push commercial demand to a 6.61% CAGR, outpacing residential upgrades.

How are manufacturers mitigating raw-material cost inflation?

They innovate with proprietary composites, expand vertical integration, and pass through selective price increases, especially in premium tiers.

Which sales channel is expanding most rapidly?

Direct B2B relationships with developers and architects are rising at 6.14% CAGR, supported by digital configurators and BIM integration.

Page last updated on: