Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

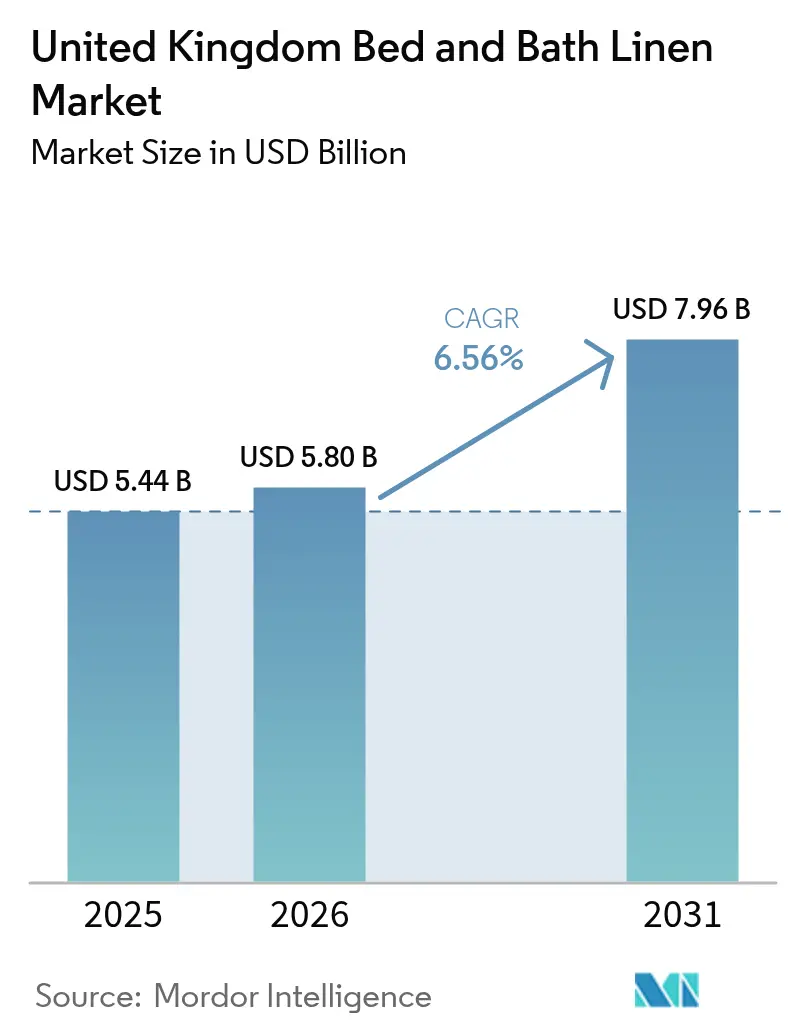

| Base Year Market Size (2025) | USD 5.44 Billion |

| Market Size (2026) | USD 5.8 Billion |

| Market Size (2031) | USD 7.96 Billion |

| Growth Rate (2026 - 2031) | 6.56% CAGR |

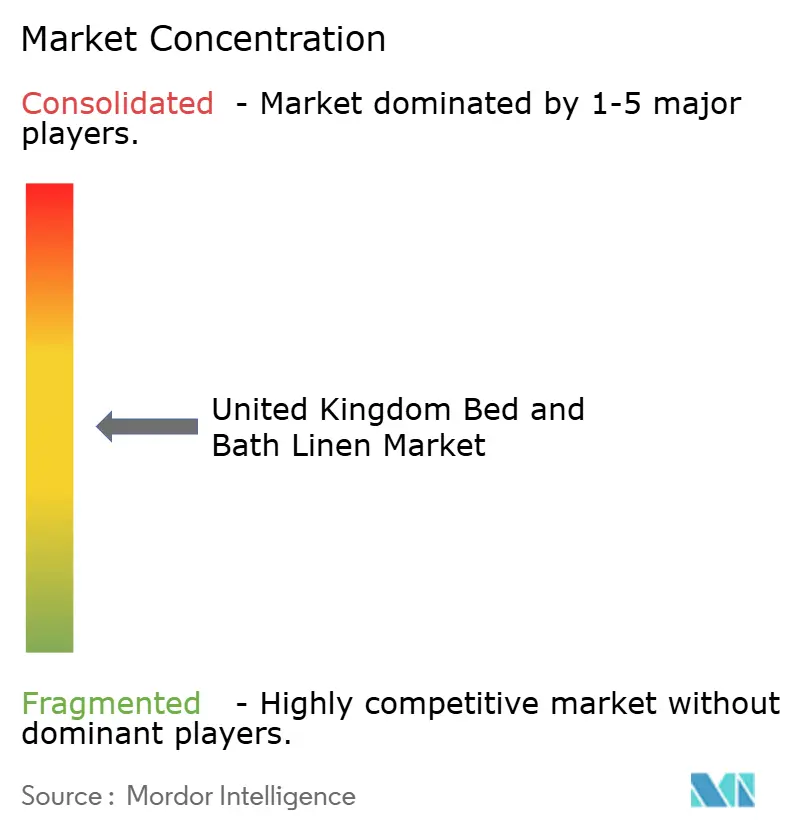

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Bed And Bath Linen Market Analysis by Mordor Intelligence

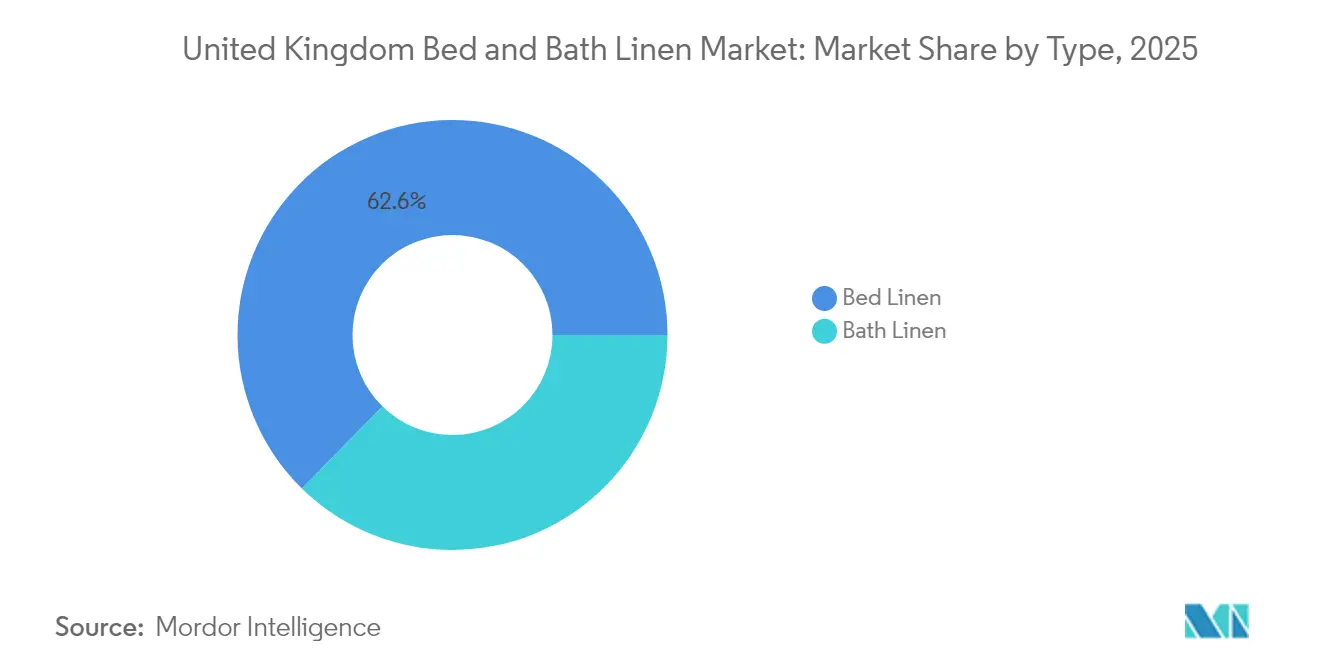

United Kingdom bed and bath linen market size in 2026 is estimated at USD 5.8 billion, growing from 2025 value of USD 5.44 billion with 2031 projections showing USD 7.96 billion, growing at 6.56% CAGR over 2026-2031. Rising home‐improvement spending, luxury hotel pipeline additions, and a marked consumer preference for sustainable fabrics underpin this steady outlook. England accounts for 79.48% of national revenue, while Scotland records the quickest regional expansion at a 6.13% CAGR on the back of tourism-led hospitality demand. Bed linen commands 63.27% of product sales because households replace sheets and pillowcases more frequently than other textile categories, yet bath linen is set to outpace it with a 7.28% CAGR as commercial sectors refresh towels to meet stricter hygiene standards. Amid this growth, the competitive landscape remains moderately fragmented: the top five suppliers hold a combined 45.2% share, making scale advantages valuable but leaving headroom for niche and private-label challengers.

Key Report Takeaways

- By product type, bed linen led with 62.65% of the United Kingdom Bed and Bath Linen Market share in 2025, bath linen is forecast to expand at a 7.18% CAGR through 2031.

- By end users, the residential segment captured 67.60% of the United Kingdom Bed and Bath Linen Market share in 2025; the commercial segment is projected to advance at a 6.10% CAGR between 2026 and 2031.

- By distribution channel, hypermarkets and supermarkets contributed 37.75% of the United Kingdom Bed and Bath Linen Market share in 2025, and sales, e-commerce are expected to accelerate at a 10.15% CAGR in the same period.

- By geography, England accounted for 78.90% ofthe UnitedKingdom'sm Bed and Bath Linen Market share in 2025,and Scotland is set to grow fastest with a 6.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Bed And Bath Linen Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic home renovation boom | 1.0% | National, with higher impact in England and Wales | Medium term (2-4 years) |

| Expansion ofUnited Kingdomluxury hotel pipeline | 0.8% | National, concentrated in England and Scotland | Medium term (2-4 years) |

| E-commerce share gains in home textiles | 1.2% | National, with stronger adoption in urban areas | Long term (≥ 4 years) |

| Consumer shift to sustainable & organic fabrics | 0.7% | National, led by England and Scotland | Long term (≥ 4 years) |

| NHS infection-control protocols for healthcare linens | 0.5% | National, concentrated in England | Short term (≤ 2 years) |

| Early adoption of smart bedding technology | 0.4% | England and Scotland, limited Wales/Northern Ireland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic Home Renovation Boom

Households continue to funnel discretionary income into home upgrades that include higher-quality sheets, duvets, and towels as lifestyles remain more home-centric. Retail footfall data show that linen categories sustained mid-single-digit volume growth in 2024 even after lockdowns ended[2]Dunelm Group plc, “Preliminary Results FY24,” dunelm.com.. Consumers who initially purchased budget bedding during supply constraints are now trading up to organic cotton and premium thread counts, driving average selling prices. Big-box chains leverage bundled bedroom sets to capture this upgrade cycle, while specialty e-tailers rely on customizable design tools to convert browsers into repeat buyers. The trend is most pronounced among owners of recently renovated properties, where coordinated linens become finishing touches that elevate interior aesthetics. Ongoing DIY activity, therefore, acts as a reliable spur to replacement demand across both value and premium segments.

Expansion of United Kingdom Luxury Hotel Pipeline

Hospitality operators have announced or opened thousands of high-end rooms that require premium linen specifications, supporting a stable base of institutional demand. IHG alone added more than 900 United Kingdom and Ireland rooms in 2024 and specified higher thread counts to boost guest satisfaction metrics[3]IHG Hotels & Resorts, “Strong Q3 2024 Results,” ihg.com.. Hoteliers now see linens as a cost-effective differentiator for revenue per available room, prompting supply contracts with strict durability and sustainability clauses. Forward bookings for heritage properties under renovation signal continued appetite for upscale accommodation, especially in London and Edinburgh. As each luxury bed set typically includes multiple sheets, duvet covers, and pillow protectors, procurement volumes compound quickly, benefiting suppliers able to meet stringent delivery windows. The pipeline expansion therefore provides a predictable offtake that helps manufacturers smooth volatility in consumer channels.

E-commerce Share Gains in Home Textiles

Digital migration reshapes purchasing habits as improved imagery, same-day delivery in major cities, and no-quibble return policies overcome the traditional need to feel fabrics in-store. Online linen sales rose to 37% of Dunelm’s revenue in fiscal 2024, doubling their share from 2020. Artificial-intelligence search tools and augmented-reality visualization help customers match colors to bedroom décor, lifting conversion rates. Marketplaces and direct-to-consumer brands exploit lower overhead to undercut brick-and-mortar pricing without sacrificing margins. For rural consumers, e-commerce extends the range of styles beyond what local retailers carry, further accelerating digital uptake. Logistics partners expand capacity ahead of bank-holiday promotions, ensuring that delivery speed remains a differentiator as channels converge.

Consumer Shift to Sustainable & Organic Fabrics

Eco-conscious shoppers scrutinize origin certificates and water usage, pushing organic cotton and recycled blends into mainstream assortments. Royal College of Art research shows circular design could halve textile sector emissions by 2030 if widely adopted[4]Textiles Circularity Centre, “Circular Textiles Research,” textilescircularity.rca.ac.uk. . Retailers respond with in-aisle QR codes that trace farm-to-shelf supply chains, boosting transparency. Pricing premiums for organic bedding remained resilient despite cost-of-living headwinds, indicating strong value attribution to environmental attributes. Brands launching linen take-back schemes find improved customer loyalty and incremental sales upon voucher redemption for returned goods. This green pivot pressures conventional manufacturers to invest in water-saving dyeing and renewable energy usage to keep pace with evolving buyer expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in global cotton and flax prices | -0.8% | National, affecting all regions | Short term (≤ 2 years) |

| Influx of low-cost Asian imports driving price wars | -0.5% | National, concentrated in England | Medium term (2-4 years) |

| Post-Brexit customs documentation delays | -0.3% | National, with higher impact on importers | Short term (≤ 2 years) |

| Skilled-labour shortages United Kingdom textile mills | -0.3% | England and Wales, limited Scotland/Northern Ireland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Global Cotton and Flax Prices

Cotton futures swung between USD 0.70 and USD 0.80 per pound in 2024 because of weather shocks and trade disruptions, compressing margins for import-reliant United Kingdom mills. Spot price uncertainty deters long production runs, forcing retailers to hold higher safety stock or hedge with synthetic substitutes. Currency fluctuations since Brexit amplify raw-material cost swings when converting invoices denominated in USD or EUR. Some suppliers pivot to recycled fibers to mitigate exposure, yet supply volumes remain insufficient for wide-scale substitution. Retailers, therefore, use dynamic pricing engines, passing part of the spike to consumers but risking demand elasticity in value tiers. Abrupt input cost reversals also create inventory valuation risks, complicating promotional planning.

Influx of Low-Cost Asian Imports Driving Price Wars

Asian manufacturers leverage scale and wage advantages to supply entry-level linens at price points domestic producers cannot match. Value-tier retailers intensify promotional frequency, eroding margins across the chain. Quality-conscious consumers sometimes report premature wear and dye bleed on imported items, handing opportunities to local brands that highlight British craftsmanship. Yet tariffs remain low, so import penetration holds above 65% in volume terms. Domestic mills focus on quick-turn and bespoke production to avoid direct price competition, but capacity limitations restrict market share recapture. Sustained pressure from imports thus restrains average selling price growth even as premium sub-segments expand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Bed Linen Dominance Faces Bath Linen Acceleration

Bed linen accounts for 62.65% of 2025 revenue, underlining the category’s entrenched role in household refresh cycles that align with seasonal promotions and gifting peaks. The United Kingdom bed and bath linen market share concentration in bed sheets is reinforced by robust private-label programs at grocery chains, which entice shoppers seeking one-stop convenience. However, the United Kingdom bed and bath linen market is witnessing faster unit growth for bath towels and robes as hospitality buyers replace stock more frequently to meet infection-control standards. Commercial purchase orders often stipulate higher GSM weights and antimicrobial finishes, raising value per unit and supporting supplier margins. At the premium end, spa-like towel sets marketed through social media influencers stimulate cross-selling opportunities for coordinated floor mats and shower curtains. Conversely, bed linen innovation focuses on thermoregulation and moisture wicking, as seen in temperature-controlled mattress covers that command triple the average price of conventional bedding.

The United Kingdom bed and bath linen market size for bath linen is projected to swell at a 7.18% CAGR, exceeding the 6.03% pace forecast for bed linen, evidence that product diversification is reshaping strategic portfolios. Hospitality refurbishment cycles amplify bath linen volumes because each guest room requires multiple towel sizes, hand towels, and bathmats. Manufacturers able to pre-treat towels for chlorine resistance gain a competitive edge among institutional laundries that cycle items hundreds of times. Meanwhile, retailers harness color-story merchandising to upsell complete bathroom makeovers, bundling towels with matching shower curtains and accessories to lift basket value. Supply chain investments in low-liquor-ratio dyeing reduce water use, aligning with sustainability messaging and lowering operational costs. Overall, the dual-speed trajectory between bed and bath segments demands agile inventory management and tailored marketing to avoid overstocks in slower-moving SKUs.

By End Users: Residential Leadership Amid Commercial Acceleration

Residential customers captured 67.60% of 2025 turnover thanks to lingering home-centric lifestyles and a millennial cohort entering peak household-formation years. The United Kingdom bed and bath linen market benefits from consumers viewing bedding as both a functional necessity and a décor statement, raising willingness to pay for organic cotton and higher thread counts. Yet commercial institutions—from luxury hotels to NHS facilities—are set to outpace households with a 6.10% CAGR by 2031 as hospitality occupancy climbs toward pre-pandemic norms. Institutional contracts often include multi-year replenishment clauses, offering predictable volumes that help mills optimize capacity. However, price concessions demanded by public procurement frameworks pressure margins unless suppliers differentiate on performance features. Residential channels, by contrast, allow richer storytelling around wellness and sustainability, cushioning against discounting cycles.

The United Kingdom bed and bath linen market size allocated to commercial buyers rests on repeat purchase frequency rather than initial order magnitude, so supplier responsiveness and compliance credentials often trump brand recognition. Healthcare providers demand detailed laundering instructions and product-life certifications, tightening the tendering gate. Hotel groups, meanwhile, embed linen quality into brand standards, making supplier switches less common once approved. For residential shoppers, impulse buys in grocery aisles and online flash sales create volatile demand spikes that test fulfillment agility. Consequently, companies with dual-channel strategies hedge cyclical swings, cross-leveraging production runs to serve both consumer and institutional specifications with minimal changeovers. This balanced exposure supports stable EBITDA despite sectoral shocks.

By Distribution Channel: Traditional Retail Resilience Amid Digital Disruption

Hypermarkets and supermarkets preserved a 37.75% share in 2025 due to high shopper frequency and attractive price points, confirming brick-and-mortar relevance in linens. The United Kingdom bed and bath linen market nonetheless tilts increasingly toward clicks as e-commerce records a 10.15% CAGR, winning younger demographics who rely on reviews and next-day delivery. Grocery chains respond by integrating QR-based virtual shelves that extend assortments beyond on-site space constraints, thereby defending share. Specialty stores differentiate through curated ranges and tactile experiences, but footfall recovery remains uneven, especially outside prime high-street locations. At the same time, marketplace operators weaponize data analytics to personalize offers and compress search costs, raising conversion and average order value. Return-rate management—critical in texture-sensitive items—improves through easy-wash product descriptors and 360-degree imagery.

The United Kingdom bed and bath linen market share captured by brick-and-mortar retailers could erode if digital payment adoption accelerates further among older cohorts, yet physical outlets still play a pivotal role in omnichannel fulfillment. Click-and-collect services accounted for one-third of online linen orders in 2024 at leading homeware chains. This hybrid model lowers last-mile costs and drives incremental in-store purchases. Hypermarkets invest in in-aisle digital kiosks that let shoppers browse extended catalogs without leaving the store, blending convenience with instant gratification. E-tailers experiment with subscription models supplying fresh towels every quarter, smoothing revenue and reinforcing customer loyalty. Overall, channel boundaries blur as retailers chase seamless customer journeys while mitigating logistical spend.

Geography Analysis

England contributed 78.90% of the 2025 value owing to dense population centers, higher disposable incomes, and a concentration of luxury hotels that demand premium linens. The United Kingdom bed and bath linen market size in England benefits from integrated supply networks centered around the Midlands logistics corridor, enabling next-day delivery across most postcodes. London’s design-savvy consumers drive premiumization trends that ripple out to regional cities via social media influence. Scotland, though smaller, delivers the fastest growth at a 6.05% CAGR on tourism revival and public-sector infrastructure projects that boost hospitality linen demand. Wales and Northern Ireland experience steadier but modest advances tied to demographic changes and value positioning among retailers.

Regional disparities in household income shape SKU mix: Southeast England leans toward organic Egyptian cotton, while parts of Wales favor polyester-cotton blends that meet price thresholds. Transport costs increase toward peripheral regions, encouraging retailers to site micro-fulfillment hubs to maintain service levels. Scottish textile mills tap governmental innovation grants to modernize looms, enabling faster turnaround and bespoke tartan designs that resonate with local heritage initiatives. Northern Ireland leverages unfettered intra-UK trade routes to mitigate Brexit customs friction, steadying import flows of raw fabrics. The United Kingdom bed and bath linen market share for England is expected to settle slightly lower by 2031 as faster-growing regions nibble at its dominance, yet absolute gains remain largest there because of scale.

Competitive Landscape

The United Kingdom bed and bath linen market is moderately fragmented, with the top five companies collectively holding a significant portion of the market. This creates opportunities for both large-scale growth and specialized niche strategies. Dunelm stands out as the market leader, demonstrating the strength of its omnichannel approach and focus on value. At the higher end of the market, The White Company has established a strong presence by emphasizing luxury and direct-to-consumer sales. Together, these players illustrate the diverse ways brands can succeed in a competitive landscape. Competitive dynamics are increasingly shaped by supply chain resilience and sustainable sourcing, as consumers demand ethical manufacturing and environmentally responsible practices.

Post-Brexit customs complexities are providing an edge to domestic players and seasoned importers with robust logistics and compliance infrastructure. These changes create barriers for smaller international entrants who lack documentation proficiency and customs experience. Strategic efforts across the industry focus on vertical integration, with Dunelm moving into made-to-measure window treatment manufacturing. This shift aims to capture higher-margin custom orders and reduce reliance on external suppliers. As a result, businesses are better positioned to control quality, costs, and customer experience.

Technology is rapidly transforming the sector through innovations such as AI-powered search, augmented reality tools, and smart inventory systems. These solutions enhance the customer journey and improve operational efficiency by boosting conversion rates and lowering working capital needs. Circular economy initiatives are gaining traction, with Dunelm and The Salvation Army piloting textile takeback schemes. These programs not only promote sustainable end-of-life solutions but also enhance customer loyalty through environmental responsibility. Upcoming Extended Producer Responsibility (EPR) legislation is expected to benefit larger companies with mature reverse logistics, while increasing compliance costs could challenge smaller, less-resourced competitors.

United Kingdom Bed And Bath Linen Industry Leaders

Dunelm Group plc

John Lewis Partnership plc

Marks & Spencer Group plc

IKEA Ltd (UK)

The White Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Pottery Barn, an American homeware brand, has launched in the UK. The debut includes a dedicated website offering furniture, bedding, and accessories. The brand targets style-focused consumers with curated collections. It marks a key step in Williams-Sonoma’s global expansion strategy.

- July 2024: Dunelm and The Salvation Army launched a trial home textile takeback scheme through ACT UK, piloting circular economy initiatives that could reshape industry end-of-life management. This program addresses anticipated Extended Producer Responsibility legislation while creating customer engagement opportunities around sustainability positioning.

- October 2024: Bank of England maintained elevated interest rates at 4.75%, affecting consumer financing costs for discretionary purchases, including premium bedding and bath textiles, while supporting currency stability for import-dependent suppliers.

- May 2024: Project Reclaim joint venture between the Salvation Army and Project Plan B, began operations in Kettering, Northamptonshire, processing polyester textiles into granules for new yarn production. The facility expects to recycle 2,500 tonnes in its first year, doubling capacity in 2025 while working with major United Kingdom retailers, including John Lewis.

United Kingdom Bed And Bath Linen Market Report Scope

The United Kingdom Bed and Bath Linen Market is one of the fastest-growing Bed and Bath Linen Industries as businesses and people prefer the naturally sustainable and luxurious bed and bath linen products for which the United Kingdom is one of the largest markets. A complete background analysis of the United Kingdom Bed and Bath Linen Market, which includes an assessment of the economy, market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles, is covered in the report. The United Kingdom Bed and Bath Linen Market is Segmented by Type ((Bed Linen (Sheets, Pillow Case, Duvet Case, and Other Bed Linen), Bath Linen (Towels, Bath Robes, and Other Bath Linen)), Distribution Channel (Hypermarkets/Supermarkets, Specialty Stores, e-Commerce, and Other Distribution Channels), End Users (Residential and Commercial). The report offers market size and forecasts in value (USD) for all the above segments.

By Type

| Bed Linen |

| Bath Linen |

By End Users

| Residential |

| Commercial |

By Distribution Channel

| Hypermarkets & Supermarkets |

| Specialty Stores |

| E-Commerce |

| Other Distribution Channels |

By Geography

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Type | Bed Linen |

| Bath Linen | |

| By End Users | Residential |

| Commercial | |

| By Distribution Channel | Hypermarkets & Supermarkets |

| Specialty Stores | |

| E-Commerce | |

| Other Distribution Channels | |

| By Geography | England |

| Scotland | |

| Wales | |

| Northern Ireland |

Key Questions Answered in the Report

How large is the United Kingdom bed and bath linen market in 2026?

It totals USD 5.8 billion and is expected to reach USD 7.96 billion by 2031, growing at a 6.56% CAGR.

Which product category leads sales?

Bed linen accounts for 62.65% of 2025 revenue, dominating due to frequent replacement cycles and premiumization.

What channel is expanding fastest?

E-commerce is advancing at a 10.15% CAGR as consumers embrace digital convenience and broader assortments.

Why is Scotland viewed as a growth hotspot?

Tourism recovery and new hotel projects push regional demand, lifting Scotland’s forecast CAGR to 6.05%.

Page last updated on: