Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

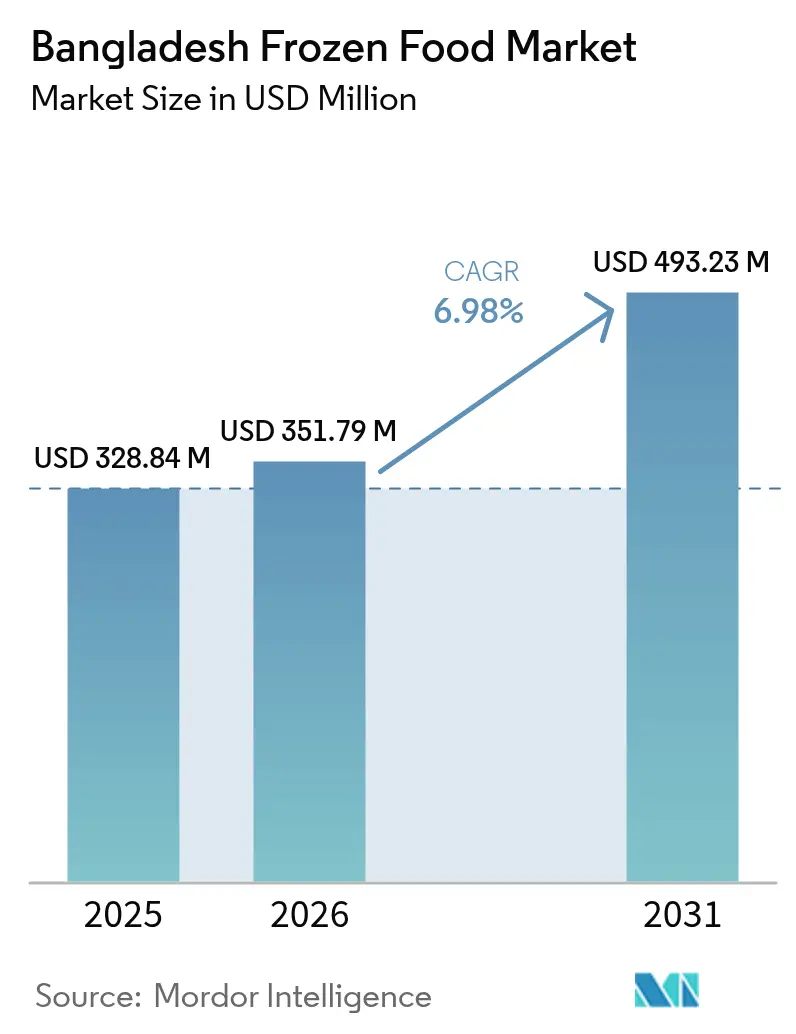

| Base Year Market Size (2025) | USD 328.84 Million |

| Market Size (2026) | USD 351.79 Million |

| Market Size (2031) | USD 493.23 Million |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

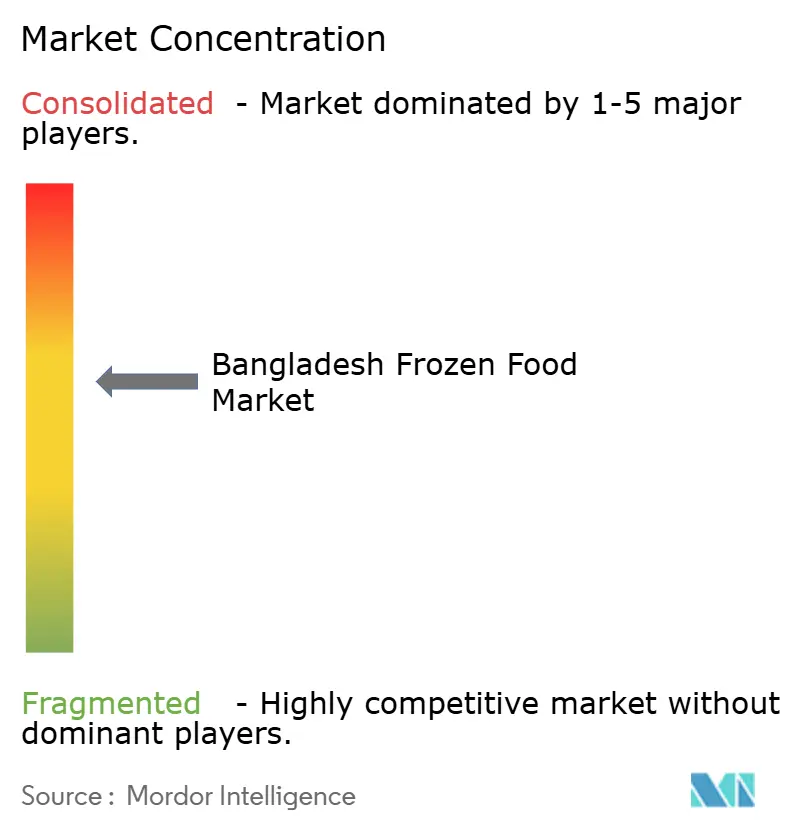

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bangladesh Frozen Food Market Analysis by Mordor Intelligence

The Bangladesh frozen food market size is expected to grow from USD 328.84 million in 2025 to USD 351.79 million in 2026 and is forecast to reach USD 493.23 million by 2031 at 6.98% CAGR over 2026-2031. According to The International Finance Corporation (IFC), rapid urbanization, a burgeoning middle class with increasing disposable income, and infrastructure projects like the Bay Terminal are driving a consistent demand for convenient, long-shelf-life meal solutions. The growth of Bangladesh's frozen food market is further bolstered by rising export earnings from frozen seafood and government incentives for agro-processing. Meanwhile, the adoption of technology in cold-chain operations and HACCP-compliant processing plants is reducing quality-related losses. Additionally, modern retail formats are enhancing product visibility in urban centers. However, challenges remain: high import tariffs on certain ingredients and persistent consumer skepticism towards processed items in rural areas are moderating volume growth.

Key Report Takeaways

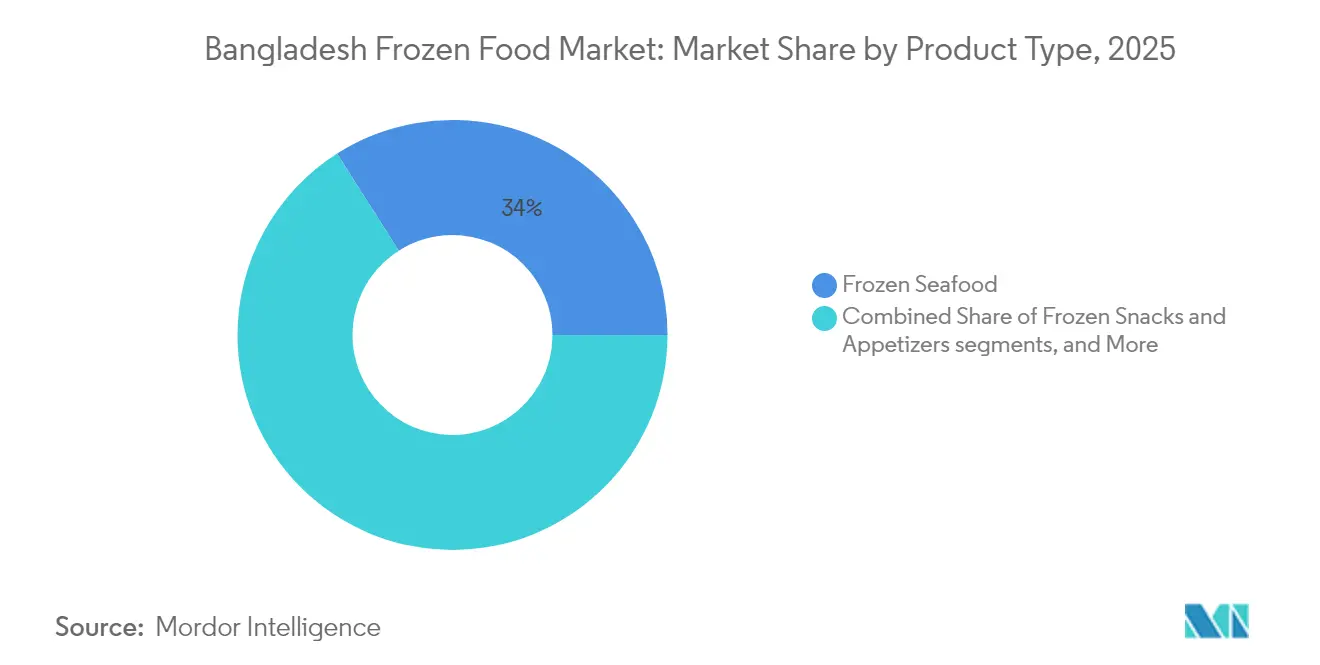

- By product type, frozen seafood led with a 34.02% share of the Bangladesh frozen food market in 2025, while frozen snacks and appetisers are projected to record a 9.08% CAGR through 2031.

- By product category, ready-to-cook formats commanded 41.05% of the Bangladesh frozen food market size in 2025, whereas ready-to-eat items exhibit the fastest trajectory at an 8.81% CAGR to 2031.

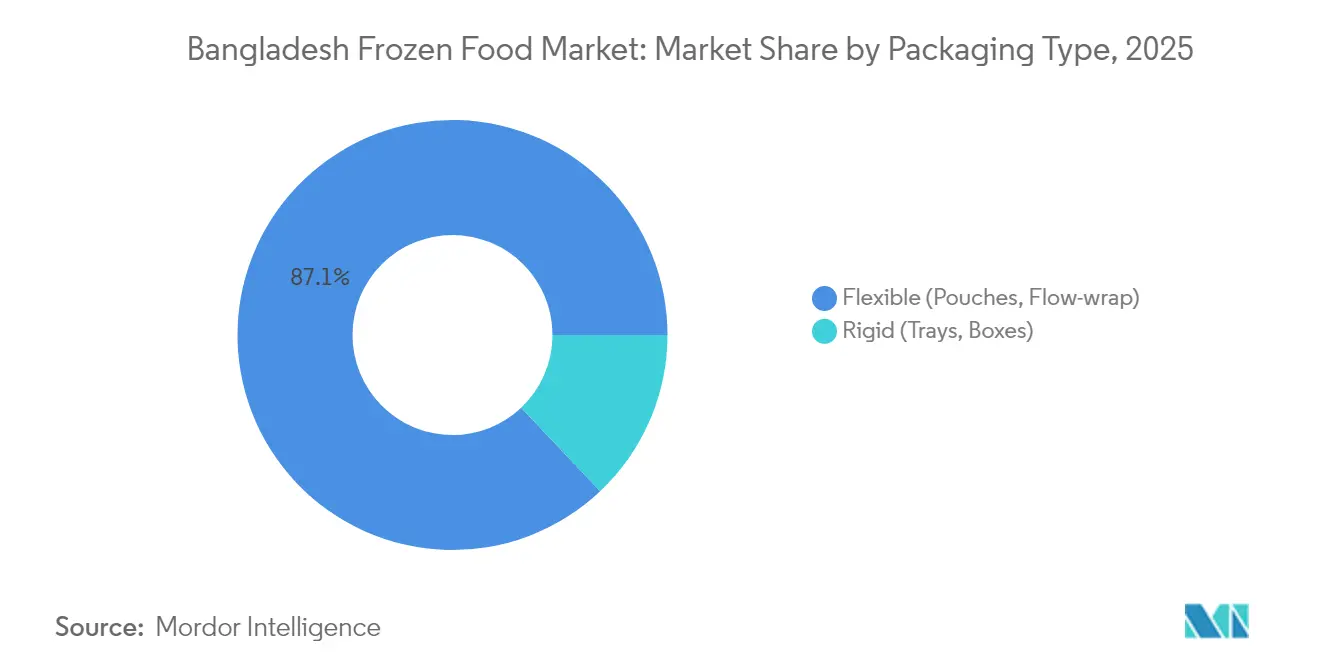

- By packaging type, flexible formats accounted for 87.05% of the Bangladesh frozen food market size in 2025, while rigid packs are advancing at a 7.58% CAGR on the back of premium product positioning.

- By distribution channel, off-trade outlets controlled 74.10% of the Bangladesh frozen food market share in 2025; on-trade sales are widening at an 8.29% CAGR as foodservice operators rely on frozen inputs to streamline operations.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bangladesh Frozen Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements in food processing | +1.2% | Dhaka and Chittagong industrial zones | Medium term (2-4 years) |

| Rising urban middle-class demand for convenience | +0.8% | Dhaka, Chittagong, Sylhet, Khulna urban clusters | Short term (≤ 2 years) |

| Government incentives for agro-processing | +1.1% | National, export-oriented zones | Long term (≥ 4 years) |

| Expansion of cold-chain infrastructure | +0.9% | Nationwide with urban–rural corridors | Medium term (2-4 years) |

| Halal-certified frozen export opportunities | +0.7% | National; outward to Middle East, Southeast Asia, Europe | Long term (≥ 4 years) |

| ASC-certified shrimp cluster farming momentum | +0.6% | Cox’s Bazar, Khulna, Barisal coastal belts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological advancements in food processing

In 2024, Bangladesh's food processing sector is witnessing a technological transformation. IoT-enabled monitoring systems and automated cold-chain solutions are enhancing efficiency throughout the value chain. The government has greenlit pilot farms for vannamei shrimp, harnessing smart aquaculture technologies. These advancements, as highlighted by research from Bangladesh Agricultural University, facilitate real-time monitoring of water quality and optimized feeding. Hermetic storage systems address quality control challenges by maintaining moisture variation at approximately 0.5% over 125 days, in contrast to the significant degradation typically observed with traditional methods. Processing facilities, drawing on the lessons learned from the 1997 EU ban, are increasingly adopting HACCP-compliant systems. Following the 1997 EU ban, market access was restored within 18 months, accompanied by systematic quality improvements. Furthermore, the adoption of AI-driven forecasting models, akin to those used by global cold-chain operators, is revolutionizing capacity planning. This shift not only slashes storage costs by up to 15% but also boosts inventory turnover rates.

Rising urban middle-class demand for convenience

In urban areas of Bangladesh, the growing middle class is reshaping food consumption habits. Although people have traditionally preferred freshly prepared meals, convenience foods are steadily gaining popularity. Modern retail outlets are expanding rapidly, with approximately 211 major supermarket branches now making a notable contribution to the national economy. This retail growth is strengthening the supply chain and helping frozen foods reach more city markets. In cities like Dhaka and Chittagong, busy professionals are increasingly opting for quick meal solutions, driving up demand for ready-to-eat products across the Bangladesh foodservice market and retail channels. However, concerns about food adulteration continue to deter some consumers. Many remain cautious about the safety of processed foods, creating a potential market for premium brands that emphasize quality, transparency, and proper certification.

Government incentives for agro-processing

Bangladesh's government is strategically promoting agro-processing industrialization, offering significant financial incentives that favor frozen food manufacturers and exporters. Under the latest budget, export-oriented agro-processing facilities are granted a 10% cash incentive on their export earnings. Additionally, there's a 15% VAT exemption on machinery imports, specifically for cold storage and processing equipment. Highlighting the importance of these measures, the World Bank Group's Bangladesh Country Private Sector Diagnostic emphasizes the need for reforms, such as digitizing customs classifications and expediting import clearances [1]Source: International Finance Corporation, “World Bank Group Report Unveils Pathways for Bangladesh's Economic Expansion,” ifc.org. Such changes promise to reduce input costs for frozen food processors, especially those that rely on imported packaging and cold-chain equipment. Further bolstering these initiatives, the government has approved the Tk 13,525 crore Bay Terminal project[2]Source: Planning Commission, Government of Bangladesh, “ECNEC Approves Bay Terminal Project,” planningcommission.gov.bd. This endeavor aims to enhance port efficiency and reduce the current 17.48-day container dwell time, a significant barrier to export competitiveness.

Expansion of cold chain infrastructure

Private sector investments are rapidly bolstering cold-chain infrastructure, as evidenced by Nippon Express's acquisition of a 20% stake in Cold Chain Bangladesh Limited, which indicates rising international interest in the market[3]Source: Nippon Express, “Strategic Equity Participation in Cold Chain Bangladesh Limited,” nipponexpress.com. This strategic move aims to rectify significant infrastructure gaps, which currently result in postharvest losses of vegetables, such as cucumbers, and fruits, including mangoes, at the farm level. In its infrastructure development blueprint, the government is enhancing rural connectivity. This initiative aims to expand cold-chain access, moving beyond urban locales where limited refrigeration has hindered market growth. Cutting-edge cold-chain facilities are now harnessing AI-driven capacity planning systems. These innovations not only optimize storage but also curtail operational costs. Such technological advancements empower exporters to adhere to stringent international quality standards, all while minimizing waste that has been a drain on profitability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inadequate cold-chain outside urban centres | -0.9% | Rural and semi-urban districts nationwide | Medium term (2-4 years) |

| High import tariffs and VAT on ingredients | -0.7% | Countrywide | Short term (≤ 2 years) |

| Supply chain inefficiencies | -0.6% | Ports and transport hubs | Medium term (2-4 years) |

| Consumer perception barriers | -0.4% | All regions, intensity varies by demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply chain inefficiencies

Bangladesh’s frozen food industry is struggling to reach its full potential due to persistent inefficiencies in the country’s food supply chain. These weaknesses drive up storage costs and increase the risk of quality loss, especially for products that require strict temperature control. The situation is made worse by poor transportation infrastructure, particularly the shortage of refrigerated trucks, which forces producers to rely on less efficient transportation methods. As a result, handling risks rises and deliveries take longer. The agricultural supply chain is also highly fragmented, with multiple middlemen involved in the movement of fruits and vegetables. This creates information gaps and frequent price fluctuations, making it difficult for frozen food processors to plan their raw material purchases. Export-focused producers are hit hardest, as delays and inconsistent product quality can result in financial penalties and lost contracts abroad. Together, these challenges limit the expansion of the frozen food sector and weaken Bangladesh’s ability to compete in global markets.

Inadequate cold-chain outside urban centers

The lack of cold-chain infrastructure in rural and semi-urban regions of Bangladesh is limiting the reach of frozen food producers and driving up their distribution expenses. While major cities like Dhaka benefit from advanced cold storage facilities, rural areas continue to struggle with inadequate refrigerated transportation. This forces manufacturers to concentrate their operations in urban centers, reducing their overall market coverage and increasing per-unit delivery costs. To meet sporadic demand from rural areas, companies often have to maintain larger inventories in city warehouses, which adds further strain to logistics and storage management. The weak cold-chain network also affects export performance; inconsistent temperature control from production sites to ports can compromise product quality, leading to rejected shipments and damaging the reputation of Bangladeshi brands in international markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Seafood Dominance Drives Export Growth

In 2025, frozen seafood accounted for the largest share of Bangladesh’s frozen food market, at 34.02%, benefiting from the country’s extensive coastline and robust aquaculture sector. That same year, the government approved pilot projects for farming vannamei shrimp, a move toward higher-value species that reflects growing global demand for sustainably sourced seafood. Frozen snacks and appetizers are experiencing rapid growth, with a projected annual growth rate of 9.08% through 2031. This rise is driven by increasing urbanization and the changing lifestyles of city professionals who prefer convenient meal options.

Frozen fruits and vegetables are also experiencing growth, supported by government initiatives aimed at reducing postharvest losses. However, the lack of reliable cold-chain facilities in rural areas continues to hinder smooth sourcing and distribution. The frozen meat and poultry segments are seeing stable growth, boosted by a rising appetite for protein among middle-income households. Meanwhile, frozen desserts and ice creams are thriving as disposable incomes increase and Western food habits become more popular. The expansion of modern retail, particularly supermarket chains with specialized frozen sections, is strengthening distribution networks and supporting growth across all categories. Ready meals and pre-cooked items are also gaining ground, as restaurants and food service businesses increasingly turn to frozen products for consistent quality and faster preparation.

By Product Category: Ready-to-Cook Leads Market Evolution

In 2025, ready-to-cook foods make up 41.05% of Bangladesh’s frozen food market, reflecting consumers’ desire for convenient meal options that still allow for some home cooking. This category has gained popularity because it aligns well with local traditions, allowing people to save time without compromising the satisfaction of preparing a meal themselves. Ready-to-eat products, though currently a smaller segment, are expanding rapidly with an annual growth rate of 8.81% expected through 2031. The trend is primarily driven by busy urban professionals who prefer quick, no-fuss meal solutions that fit their fast-paced lifestyles.

However, the rise of ready-to-eat foods faces some resistance, as many consumers remain cautious about the safety and quality of processed products. Even so, premium brands are addressing these concerns by emphasizing quality control, certification, and transparency in their ingredients. This approach resonates with educated city dwellers who value both convenience and assurance of safety, and are willing to pay extra for it. As consumer awareness grows and eating habits become more diverse, new opportunities are emerging in niche categories, such as specialized diets and ethnic frozen dishes. Overall, ready-to-cook products continue to appeal to consumers in transition between traditional and modern lifestyles, while ready-to-eat foods are becoming the choice of fully urbanized buyers seeking maximum convenience.

By Packaging Type: Flexible Solutions Drive Cost Efficiency

In 2025, flexible packaging, including pouches and flow wraps, leads the frozen food market with an 87.05% share. Its popularity stems from being cost-effective, easy to store, and well-suited for consumers seeking convenience, particularly in price-sensitive markets. These lightweight formats make efficient use of space in both retail and home settings while providing strong protection for frozen products at a lower material cost than rigid packaging. Rigid packaging, such as trays and boxes, is also gaining momentum, with a projected growth rate of 7.58% annually through 2031. This segment’s growth is largely driven by wealthier urban consumers who perceive rigid packaging as more premium and reflective of higher product quality.

The shift in packaging preferences highlights the growing maturity of Bangladesh’s frozen food market. Premium brands are turning to rigid formats to distinguish themselves and justify higher prices, while mass-market brands continue to rely on flexible options to remain affordable. At the same time, growing environmental awareness and stricter export requirements are steering the industry toward more sustainable packaging solutions. Innovations such as advanced barrier films and modified atmosphere packaging are helping extend shelf life, maintain product quality, and strengthen export competitiveness, especially for products traveling through longer distribution chains. Additionally, regulations around food safety labeling and export standards are increasingly influencing packaging choices, prompting greater investment in high-performance, globally compliant materials.

By Distribution Channel: Off-Trade Dominance with On-Trade Growth

In 2025, off-trade channels, including supermarkets, hypermarkets, convenience stores, and online platforms, lead Bangladesh’s frozen food market with a 74.10% share, serving both urban and rural customers. Major supermarket chains, such as Shwapno, with their extensive network of outlets, are strengthening their distribution in cities and gradually expanding into semi-urban areas. Although on-trade channels currently hold a smaller portion of the market, they are expected to grow rapidly at an annual rate of 8.29% through 2031. This rise is being driven by restaurants, hotels, and institutional foodservice providers that increasingly rely on frozen ingredients to improve efficiency, control costs, and maintain consistency.

The expansion of the on-trade segment reflects the growing professionalism of Bangladesh’s foodservice industry. Frozen ingredients help ensure uniform quality, simplify portioning, reduce labor needs, and minimize food waste. Meanwhile, online retail platforms are emerging as a significant sales channel, particularly for premium frozen products that appeal to urban consumers seeking convenience and variety. Convenience stores, though often underappreciated, are also becoming key players by catering to impulse buyers and offering small-pack options ideal for single households and busy city dwellers. Overall, the country’s distribution network for frozen foods is becoming more sophisticated, with modern retail formats emphasizing both accessibility and the need to maintain a reliable cold chain across diverse regions.

Geography Analysis

In Bangladesh, urban centers dominate the frozen food market, with the Dhaka metropolitan area leading the charge. Dhaka boasts the highest concentration of middle-class households, all of which have a penchant for convenience foods. Bolstered by a sophisticated retail landscape, featuring modern supermarkets and cold storage facilities, Dhaka adeptly caters to a diverse range of consumer segments. Chittagong, the nation's primary commercial port and industrial hub, ranks as the second-largest market. Here, export-driven food processing facilities not only bolster production but also fuel local demand for frozen goods. Chittagong's strategic positioning ensures smooth distribution to the southeastern rural areas and opens doors to international trade, introducing local consumers to global food trends.

Regional demand patterns highlight distinct product preferences. Coastal regions, steeped in a traditional fishing culture, show a pronounced affinity for frozen seafood. Meanwhile, Sylhet and Khulna, with their burgeoning middle-class populations, are embracing convenience foods, a shift driven by urbanization and evolving lifestyles. Investments in cold-chain infrastructure, such as Nippon Express's stake in Cold Chain Bangladesh Limited, are enhancing distribution efficiency in these secondary cities. While rural areas remain largely untapped due to limited refrigeration and traditional cooking methods, government efforts to bolster rural connectivity and cold storage access are slowly broadening the market's reach.

Frozen food companies are now setting their sights on tier-2 cities and semi-urban locales, where rising incomes and evolving lifestyles present fresh opportunities, moving away from the crowded metropolitan markets. Coastal regions, especially around Cox's Bazar and Khulna, are becoming hotspots for export-oriented production. Their closeness to raw materials and port facilities not only slashes logistics costs but also ensures adherence to global quality benchmarks. The government's ambitious Tk 13,525 crore Bay Terminal project promises to improve Bangladesh's global trade competitiveness and reduce import and export costs by increasing port operational efficiency and mobilizing private investment. As infrastructure improves and incomes rise, the frozen food market is gradually spreading its wings, reaching beyond its traditional urban confines.

Competitive Landscape

In the Bangladesh frozen food market, established players engage in fierce competition, often employing vertical integration strategies. Meanwhile, emerging specialists carve out their niches, focusing on specific segments and seizing export opportunities. Golden Harvest Agro Industries and PRAN-RFL Group, with their vast distribution networks and strong brand recognition, dominate the market. In contrast, companies like Apex Foods, with their expertise in seafood processing, are adeptly capturing premium prices in the export market.

Technology adoption is becoming a focal point in the competitive landscape. Companies are channeling investments into IoT-enabled cold-chain monitoring and AI-driven demand forecasting, aiming to streamline inventory management and cut operational costs. These moves align with the best practices observed in global cold-chain operations. Larger players are broadening their horizons, expanding horizontally across diverse product categories. On the other hand, smaller firms are honing in on vertical specialization, targeting lucrative segments such as halal-certified exports and premium ready-to-eat products. This market structure paves the way for tech-savvy disruptors. These newcomers can tackle ongoing supply chain challenges, especially in rural distribution and export logistics, areas where established players grapple with infrastructure constraints.

Oversight by the Bangladesh Food Safety Authority and various government entities enforces regulatory compliance. While these regulations act as barriers to entry, favoring established firms with robust quality systems, they may inadvertently stifle innovation from smaller newcomers. As the competitive landscape shifts, there's a palpable sense of potential consolidation. Infrastructure investments and the push for export market growth demand significant capital. Such financial requirements might outstrip the capabilities of smaller players, setting the stage for strategic partnerships or acquisitions that could redefine market dynamics.

Bangladesh Frozen Food Industry Leaders

Golden Harvest Agro Industries Ltd

Pran-Rfl Group Ltd

McCain Foods

AG Agro Foods Limited

Kazi Farms Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Nippon Express Holdings has taken a significant step by acquiring a 20% stake in Cold Chain Bangladesh Limited (CCBL). This move aims to bolster Nippon's domestic logistics operations while tapping into CCBL's established network in Bangladesh. With this partnership, Nippon Express is poised to deliver holistic, end-to-end logistics solutions across Bangladesh.

- October 2024: Sharika Foods and Amandala Limited, a subsidiary of Taufika Foods, alongside Lovello Ice Cream PLC, a publicly traded entity in the food and allied sector, entered the frozen foods market. Their product lineup will include Paratha, Roti, Chicken Nuggets, Meatballs, Fishballs, Aaloo Puri, Dal Puri, Spring Rolls, Samosas, Singara, and a range of processed items such as chicken, beef, mutton, vegetables, and various types of fish.

Bangladesh Frozen Food Market Report Scope

Frozen food is food that has been preserved at low temperatures and used over a long period of time. The Bangladesh Frozen Food Market is segmented by product category, type, and distribution channel. On the basis of product category, the market is segmented into ready-to-eat, ready-to-cook, ready-to-drink, and other frozen food types. By product type, the market is segmented into frozen fruits and vegetables, frozen meat and fish, frozen-cooked ready meals, frozen desserts, frozen snacks, and other applications. By distribution channel, the market is segmented into supermarkets and hypermarkets, convenience stores, online channels, and others. The report offers market size and forecasts in value (USD million) for the above segments.

By Product Type

| Frozen Fruits and Vegetables |

| Frozen Meat and Poultry |

| Frozen Seafood |

| Frozen-Cooked Ready Meals |

| Frozen Snacks and Appetisers |

| Frozen Desserts and Ice-cream |

| Other Product Types |

By Product Category

| Ready-to-Eat |

| Ready-to-Cook |

| Other Categories |

By Packaging Type

| Flexible (Pouches, Flow-wrap) |

| Rigid (Trays, Boxes) |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets / Hypermarkets |

| Convenience Stores | |

| Online Stores | |

| Other Channels |

| By Product Type | Frozen Fruits and Vegetables | |

| Frozen Meat and Poultry | ||

| Frozen Seafood | ||

| Frozen-Cooked Ready Meals | ||

| Frozen Snacks and Appetisers | ||

| Frozen Desserts and Ice-cream | ||

| Other Product Types | ||

| By Product Category | Ready-to-Eat | |

| Ready-to-Cook | ||

| Other Categories | ||

| By Packaging Type | Flexible (Pouches, Flow-wrap) | |

| Rigid (Trays, Boxes) | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Online Stores | ||

| Other Channels | ||

Key Questions Answered in the Report

How large is the Bangladesh frozen food market in 2026?

It is valued at USD 351.79 million and is projected to grow to USD 493.23 million by 2031.

Which segment contributes the most sales?

Frozen seafood leads with a 34.02% share, buoyed by established aquaculture and rising exports.

What is the fastest growing category?

Ready-to-eat products are forecast to expand at an 8.81% CAGR as urban professionals demand quick meals.

Which channel dominates distribution?

Off-trade outlets such as supermarkets and e-commerce together hold 74.10% of nationwide volume.

What infrastructure project will impact exports most?

The Bay Terminal at Chittagong port, once operational, will shorten container dwell times and cut logistics costs.

Page last updated on: