Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

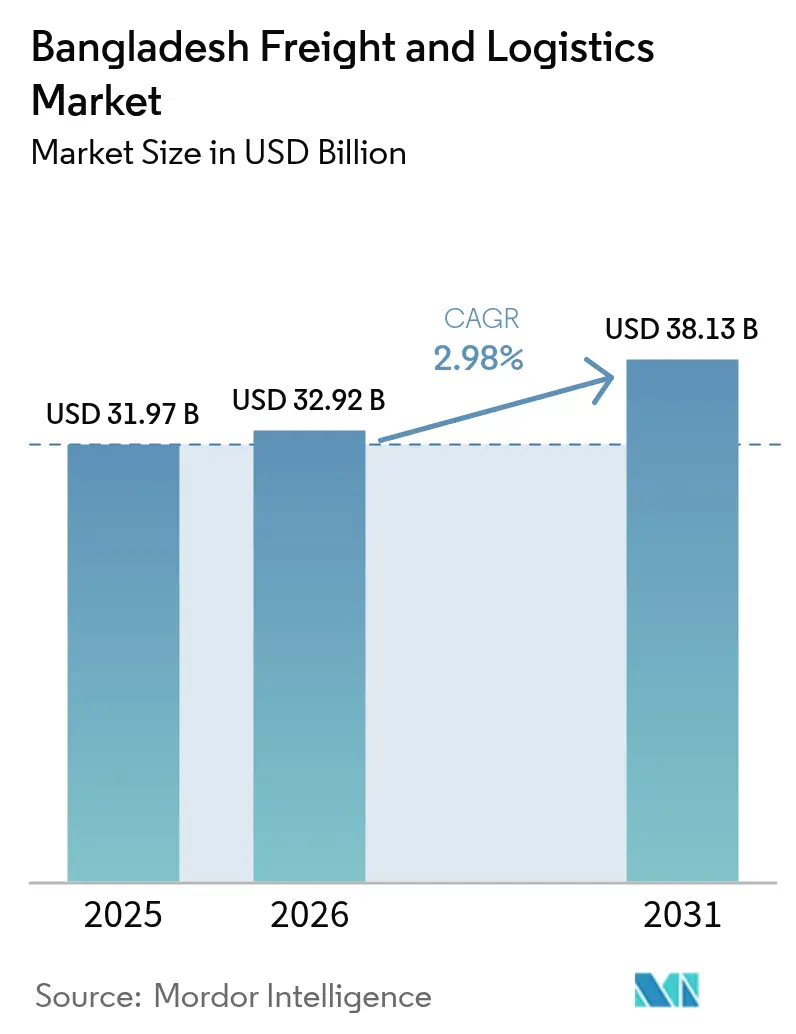

| Base Year Market Size (2025) | USD 31.97 Billion |

| Market Size (2026) | USD 32.92 Billion |

| Market Size (2031) | USD 38.13 Billion |

| Growth Rate (2026 - 2031) | 2.98% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bangladesh Freight And Logistics Market Analysis by Mordor Intelligence

The Bangladesh freight and logistics market size in 2026 is estimated at USD 32.92 billion, growing from 2025 value of USD 31.97 billion with 2031 projections showing USD 38.13 billion, growing at 2.98% CAGR over 2026-2031. Expansion rests on resilient export momentum, led by ready-made garments, rising e-commerce volumes, and incremental progress on road, bridge, and port projects. Demand for value-added services is broadening as shippers seek reliability, visibility, and compliance across supply chains. Digital customs reforms are trimming clearance times, while public–private investment in deep-sea capacity signals a gradual modal shift toward larger vessels. Nonetheless, chronic road congestion, shallow port drafts, and limited rail capacity keep average logistics costs high and temper the growth trajectory of the Bangladesh freight and logistics market.

Key Report Takeaways

- By end user industry, manufacturing captured 35.20% of the Bangladesh freight and logistics market size in 2025; wholesale and retail trade is set to grow at a 3.27% CAGR between 2026-2031.

- By logistics function, freight transport led with 53.10% of the Bangladesh freight and logistics market share in 2025, while Courier, Express, and Parcel is projected to expand at a 3.47% CAGR between 2026-2031.

- By freight transport mode, road freight transport accounted for 68.75% revenue share in 2025; air freight transport is poised for the fastest 3.54% CAGR between 2026-2031.

- By warehousing type, non-temperature-controlled facilities held 91.55% revenue share in 2025, whereas the temperature-controlled segment is set to advance at a 3.40% CAGR between 2026-2031.

- By CEP segment, domestic services commanded a 63.80% revenue share 2025; international CEP shows the fastest projected 3.59% CAGR between 2026-2031.

- By freight forwarding mode, sea freight forwarding dominated with 75.20% revenue share in 2025; air freight forwarding is forecast to climb at a 3.61% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bangladesh Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth of RMG and emerging non-RMG exports fuelling time-sensitive logistics | +1.6% | National, with concentration in Dhaka and Chattogram | Medium term (2-4 years) |

| Government megaprojects Padma Bridge, Matarbari Port unlocking multimodal corridors | +1.3% | National, with emphasis on Southwest and Southeast regions | Long term (≥ 4 years) |

| Bilateral and regional transit pacts BBIN, BIMSTEC enabling cross-border through-flows | +0.9% | National, with concentration on border regions with India, Nepal, and Bhutan | Medium term (2-4 years) |

| Digitization push national single window and port community systems slashing dwell times | +0.8% | National, with initial impact at major ports and border crossings | Medium term (2-4 years) |

| Rising demand for temperature-controlled logistics for pharma and seafood exports | +0.6% | National, with concentration in major production and export hubs | Short term (≤ 2 years) |

| Foreign direct investment in logistics infrastructure driving capacity expansion | +0.5% | National, with focus on major economic zones and port cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of RMG and Emerging Non-RMG Exports Fueling Time-Sensitive Logistics

Ready-made garment exports reached USD 38.48 billion in 2024 and continue climbing, while non-traditional destinations added USD 6.33 billion in 2024. Knitwear and woven apparel shipments are rising in double digits, creating heavier demand for predictable transit times and compliant documentation[1]“RMG Exports Cross USD 38 Billion Mark,” Md Saifuddin, tbsnews.net . Buyers in Japan, Australia, and Latin America require stricter labelling and shorter replenishment cycles, spurring investments in bonded trucking, value-added warehousing, and parcel-level tracking. As order sizes shrink and frequency rises, the Bangladesh freight and logistics market is shifting from bulk movement toward agile, time-definite services that protect margin and reputation.

Government Megaprojects (Padma Bridge, Matarbari Port) Unlocking Multimodal Corridors

Padma Bridge has halved travel times between Dhaka and the southwest, opening routes once bypassed by exporters[2]“Padma Bridge Operations Company Gets Green Light,” Tapan Biswas, tbsnews.net . Policy makers expect up to 4 million new jobs over the next decade, intensifying intra-country freight flows. Matarbari deep-sea port, scheduled for 2027, will receive 100,000-plus DWT vessels, removing feeder legs that currently add extra expense to shipping costs. The link between Padma Bridge, Mongla Port, and Matarbari will gradually forge a triangle of road, rail, and maritime options, encouraging carriers to redesign networks and helping the Bangladesh freight and logistics market capture transit traffic from northeast India and Bhutan.

Bilateral and Regional Transit Pacts (BBIN, BIMSTEC) Enabling Cross-Border Through-Flows

The BBIN Motor Vehicles Agreement, supported by SASEC financing, has introduced electronic cargo tracking, integrated check posts, and streamlined documentation[3]“Bangladesh SASEC Road Connectivity Report,” Asian Development Bank, adb.org. Corridor 2 now handles 65% of India-Bangladesh road trade, and a trial run using ECTS cut border dwell to three hours. Transit cargo through Chattogram and Mongla ports for Indian importers is becoming routine, positioning the country as a coastal gateway for Himalayan economies. These developments diversify revenue streams and raise service benchmarks across the Bangladesh freight and logistics market.

Digitization Push, National Single Window and Port Community Systems Slashing Dwell Times

The Customs Strategic Plan 2024-2028 targets full Single Window coverage by 2027 and end-to-end automation of declarations by 2026. Pilot implementations cut release time for compliant consignments at Chattogram to 48 hours, down from 104. AI-driven risk engines are separating low-risk shipments, while mandatory Maritime Single Window protocols introduced in 2024 harmonize data across shipping lines, agents, and terminals. Faster processing improves vessel utilization, lowers inventory buffers, and strengthens the competitiveness of the Bangladesh freight and logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic congestion on Dhaka-Chattogram highway increasing transit times | -1.3% | National, with acute impact on Dhaka-Chattogram corridor | Short term (≤ 2 years) |

| Shallow draft at Chattogram port creating feeder dependence and higher trans-shipment cost | -0.9% | National, with primary impact on international trade flows | Medium term (2-4 years) |

| Skills gap in cold-chain and DG handling limiting service quality for high-value cargo | -0.8% | National, with concentration in major logistics hubs | Medium term (2-4 years) |

| Limited rail freight capacity and lack of ICD connectivity | -0.6% | National, with emphasis on major economic corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Congestion on Dhaka-Chattogram Highway Increasing Transit Times

The 240 km long Dhaka-Chattogram Highway corridor handles more than 90% of external trade yet offers average speeds of 19-22 km/h. Frequent lane closures, dense mixed traffic, and limited bypasses undermine schedule reliability. As 61.65% of the load picked (tons) travels by road, long queues translate into stock-outs, overtime costs, and missed vessel connections. Expressway upgrades are planned, but land acquisition and funding gaps delay completion, constricting the medium-term growth of the Bangladesh freight and logistics market.

Shallow Draft at Chattogram Port Creating Feeder Dependence and Higher Trans-shipment Cost

Handling 3.26 million TEUs in 2024, Chattogram Port cannot berth container ships above 9.5 m draft, forcing cargo onto feeder services via Colombo or Singapore. Additional handling pushes ocean freight up by 15-25% and extends voyage time by 4-6 days. While the Bay Terminal and Matarbari projects promise relief, financing, dredging, and road linkage works must converge before direct mainline calls become routine. Until then, the Bangladesh freight and logistics market absorbs higher costs and faces eroding margins, especially for low-value garments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Manufacturing Centrality Reflects Export Orientation

Manufacturing accounted for 35.20% of the revenue share of the Bangladesh freight and logistics market. RMG requirements dominate but are becoming more sophisticated, ranging from vendor-managed inventory to carton-level barcoding. The sector’s logistics bill is set to grow with integrated warehouse-transport bundles replacing spot trucking.

Wholesale and retail trade is poised for rapid growth. Digital marketplaces doubled order counts in two years, driving parcel density and reverse-logistics needs. This vertical will outpace others at 3.27% CAGR (2026-2031) as omnichannel chains open fulfillment centers near Dhaka and Chattogram. Construction and agriculture, though smaller, still require bulk inland movement of cement, steel, seeds, and perishables, demanding improved multimodal transfers and cold chain nodes.

By Logistics Function: CEP Segment Accelerates on E-commerce Surge

The freight transport segment contributed 53.10% of the Bangladesh freight and logistics market share. Moderate expansion reflects incremental highway upgrades and steady export flows. Road haulage represents 68.75% of the freight transport segment value because shippers continue to rely on trucking between cluster factories and ports. Manufacturing alone generates a significant share of road freight spending, underscoring how garments anchor domestic line-haul demand.

The Courier, Express, and Parcel segment is projected to grow at a CAGR of 3.47% from 2026 to 2031. Domestic parcels dominate as of 2025, but a faster 3.59% CAGR (2026-2031) in international traffic is reshaping service design. E-commerce accounted for 41.73% of CEP turnover in 2024, compelling operators to improve last-mile address accuracy, real-time status alerts, and pick-up lockers. As digital buyers expect two-day delivery to Tokyo or Toronto, the Bangladesh freight and logistics market is pushing CEP providers to integrate customs data feeds, bonded warehouses, and airside trucking for seamless export fulfilment.

By Courier, Express, and Parcel: International Segment Outpaces Domestic Growth

Domestic CEP services yielded a 63.80% revenue share in 2025. Operators battle inconsistent address formats and traffic bottlenecks that slow last-mile runs. Initiatives such as geo-coded digital postcodes and two-wheeler electric fleets are improving hit rates and lowering delivery windows, making city logistics a critical differentiator within the Bangladesh freight and logistics market.

International CEP is forecasted to grow at a CAGR of 3.59% between 2026-2031. Direct air links to Guangzhou, Dubai, and Istanbul now allow garments, leather goods, and handicrafts to reach consumers sooner. Global integrators provide trade compliance dashboards, while local partners offer doorstep pick-ups. Customs automation, electronic advance data, and electronic duty-merchandise systems together shorten export parcel clearance, bolstering the competitive edge of Bangladesh-based sellers.

By Warehousing and Storage: Temperature-Controlled Segment Gains Momentum

Non-temperature-controlled warehouses accounted for 91.55% of warehousing value inside the Bangladesh freight and logistics market. Most structures remain single-story sheds with manual handling and basic inventory systems. The wholesale and retail trade sector consumed half of this space, given the country’s growing grocery and fashion networks, while the manufacturing sector taking significant space to stage exports.

The temperature-controlled niche is gathering pace as pharmaceutical exports rise and seafood players target frozen value. The segment is forecasted to expand at a 3.40% CAGR (2026-2031), yet unmet demand persists, especially beyond major urban clusters. New public-private cold hubs, supported by USTDA financing, plan pallet racking, solar backup, and tele-monitoring to shrink the post-harvest loss rate.

By Freight Transport: Road Dominance Persists Amid Modal Shift Efforts

Road transport generated a 68.75% revenue share in the freight transport segment. Despite wide usage, load efficiency is low, with trucks carrying 61.65% of the load picked (tons) but covering only 33.34% of the load moved (ton-km) in 2024, evidence of short, congested hauls. Manufacturers and retailers were significant contributors to the segment. Regulators are piloting weigh-in-motion, axle bans, and GPS-based tolling to lift productivity and curb overloading.

Sea and inland waterways, with 60.57% of the load moved (ton-km) while only 21.05% of the load picked (tons), confirmed their efficiency. The segment will likely grow by 2030 as Matarbari and Bay Terminal add berth capacity. Rail freight transport held a minimal market share in 2024 but offers scale economies once gauge conversion and ICD links mature. Air freight transport posted the quickest 3.54% CAGR (2026-2031) outlook, buoyed by pharmaceuticals and premium knitwear. Together, these trends signal a gradual diversification of the Bangladesh freight and logistics market away from an over-road dependence.

By Freight Forwarding: Air Segment Grows on High-Value Cargo Demand

Sea and Inland Waterways freight forwarding amassed 75.20% of forwarding activity in the Bangladesh freight and logistics market in 2025. Box volumes grew 6.8% despite vessel draft limits at Chattogram. Forwarders invest in feeder slot agreements and inland water trans-loading barges to stabilize schedules and mitigate tide restrictions.

Air freight forwarding is expected to enjoy a 3.61% CAGR (2026-2031) outlook. Pharmaceuticals, technical textiles, and sample shipments need temperature logging, chain-of-custody, and warranty services unavailable in general cargo lanes. Forwarders are adding GDP-compliant containers, cool dollies, and data loggers to command premium yields. Land-road-rail forwarding under “others” benefits from BBIN transit rights that reduce border formalities on the Dhaka–Siliguri–Kathmandu lanes.

Geography Analysis

The Dhaka-Chattogram axis forms the backbone of the Bangladesh freight and logistics market, hosting the densest warehouse clusters, freight terminals, and CEP sorting centers. Yet it also carries the country’s worst congestion, with peak-hour speeds barely 20 km/h, forcing shippers to build larger safety stocks. Bridge toll reforms, weigh-in-motion scales, and completion of the Dhaka Elevated Expressway are expected to ease bottlenecks, but short-term relief is limited.

To the southwest, Padma Bridge has rerouted cargo previously ferried across the river, cutting Dhaka-Khulna transit from nine to three hours. The link is attracting garment factories, agro processors, and logistics parks that can bypass metropolitan traffic. The government plans to connect Mongla Port by dual-gauge rail and four-lane road will further diversify gateways, gradually rebalancing freight flows across the Bangladesh freight and logistics market.

The southeast anchors the ocean trade. Chattogram handled 3.26 million TEUs in 2024, but vessel-size restrictions and urban sprawl force truck queues on approach roads. Matarbari deep-sea port, plus the Bay Terminal reclamation, aims to double capacity and accommodate Panamax ships, giving the Bangladesh freight and logistics market a chance to become a regional trans-shipment option for northeast India, Bhutan, and Nepal. Border districts are also modernizing, with integrated check posts at Benapole and Tamabil linking customs, immigration, and quarantine under one roof, shortening document processing and encouraging road-rail multimodal solutions.

Competitive Landscape

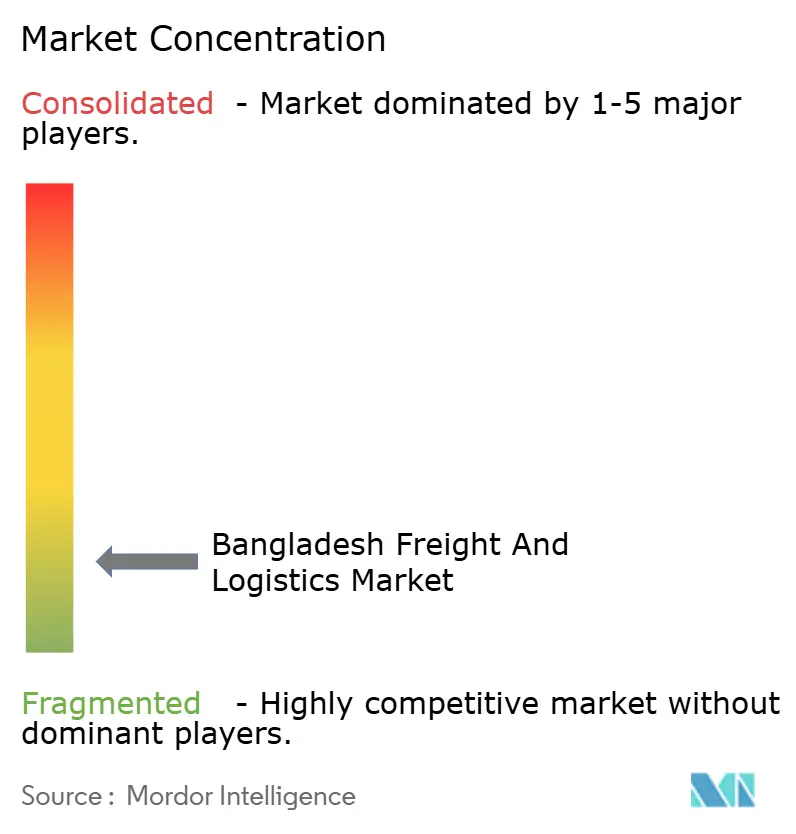

Competition remains fragmented, as no single operator controls a dominant national share across modes. Global multinationals command international forwarding, express, and container terminal concessions, leveraging technology, global contracts, and risk management standards. Domestic fleets dominate short-haul trucking and general warehousing, often using family-owned fleets that offer agility and deep local knowledge. The Bangladesh freight and logistics market is witnessing gradual consolidation, with mid-sized firms merging to meet minimum fleet requirements, quality audits, and IT investments set by large exporters and the National Logistics Policy 2024.

Strategic investment is a critical differentiator. A.P. Moller-Maersk’s USD 800 million stake in Laldia Container Terminal will add three deep berths and advanced gate automation, enhancing throughput and linking seamlessly to the company’s inland depots. DHL’s EUR 26 million (USD 28.16 million) facility in north Dhaka doubles parcel sort capacity and incorporates sustainable aviation fuel modularity to lower Scope 3 emissions. Toll Group’s new forwarding branch, backed by Japan Post, brings healthcare GMP competencies and alternative-fuel vehicle trials, broadening choices for pharmaceutical shippers.

Digital adoption has become the frontline of competitive positioning inside the Bangladesh freight and logistics market. Global players deploy AI route optimization, blockchain bill-of-lading, and IoT sensor networks, while leading local carriers partner with fintechs for cashless collections. Smaller operators risk being crowded out unless they pool resources for shared visibility platforms. The forthcoming ICD at Dhirasram and rail gauge conversions present new opportunities for asset-right forwarders to plug into port-to-factory shuttles, re-shaping rivalry based on multimodal reliability rather than solely on price.

Bangladesh Freight And Logistics Industry Leaders

DHL Group

DSV A/S (including DB Schenker)

A.P. Moller - Maersk

Kuehne + Nagel

FedEx

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Toll Group announced a new Global Forwarding branch in Bangladesh with an emphasis on decarbonized fleets and healthcare logistics.

- January 2025: A.P. Moller-Maersk confirmed a USD 800 million investment for the Laldia Container Terminal at Chattogram Port, structured under a build-operate-transfer model.

- December 2024: FedEx introduced a direct Guangzhou-Bengaluru flight that improves air-cargo connectivity for Bangladeshi exporters.

- September 2024: DHL Express revealed a EUR 26 million (USD 28.69 million) Dhaka facility spanning 10,000 m² and integrating SAF-enabled GoGreen Plus services.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Bangladesh freight and logistics market as the total annual revenue earned inside the country from moving, storing, and handling physical goods across road, rail, air, inland waterway, and sea links, along with related forwarding, courier-express-parcel, and warehousing services. The definition therefore captures both domestic flows and international movements that originate in, terminate in, or transit through Bangladesh.

Scope exclusion: Pipeline services, postal money transfers, passenger transport, and purely digital fulfillment platforms are kept outside the market boundary to maintain clear comparability.

Segmentation Overview

- End User Industry

- Agriculture, Fishing, and Forestry

- Construction

- Manufacturing

- Oil and Gas, Mining and Quarrying

- Wholesale and Retail Trade

- Others

- Logistics Function

- Courier, Express, and Parcel (CEP)

- By Destination Type

- Domestic

- International

- By Destination Type

- Freight Forwarding

- By Mode of Transport

- Air

- Sea and Inland Waterways

- Others

- By Mode of Transport

- Freight Transport

- By Mode of Transport

- Air

- Pipelines

- Rail

- Road

- Sea and Inland Waterways

- By Mode of Transport

- Warehousing and Storage

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Temperature Control

- Other Services

- Courier, Express, and Parcel (CEP)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed freight forwarders, trucking fleet owners, garment exporters, e-commerce parcel aggregators, and port officials across Dhaka, Chattogram, and Khulna. Discussions tested volume growth estimates, typical haul rates, mode preference shifts, and the practical impact of new infrastructure, thereby filling data gaps and validating secondary findings.

Desk Research

We began by screening authoritative, freely available material such as Bangladesh Bureau of Statistics transport tables, National Board of Revenue customs releases, Bangladesh Bank trade data, and planning documents from the Roads and Highways Department. Sector-specific publications from the World Bank, UNCTAD, and the Bangladesh Freight Forwarders Association added mode-level insights. Company filings, investor decks, reputable press coverage, and select modules from D&B Hoovers and Dow Jones Factiva helped us gauge operator revenues and contract pipelines. Numerous other secondary sources supported cross-checks; the list above is illustrative rather than exhaustive.

A second sweep focused on infrastructure capacity, tariff revisions, and regulatory milestones (for example, Padma Bridge opening, National Single Window roll-out) that reshape cost curves and throughput. These signals fed into our baseline demand and price assumptions.

Market-Sizing & Forecasting

A top-down construct starts with historical merchandise trade, industrial output, and household consumption to estimate freight demand pools, which are then split by mode using observed share trends. Results are referenced against selective bottom-up checks such as sampled average selling price × tonnage for garment exports, container throughput roll-ups, and warehouse floor-space occupancy to refine totals. Key input fingerprints include ready-made garment export value, annual container lifts at Chattogram, e-commerce parcel counts, diesel price movements, and road freight tariff indices; each variable influences either volume or yield. Multivariate regression of these drivers under a base-case macro scenario generates our 2025-2030 forecast, while scenario analysis stresses the model for port-capacity delays or global demand shocks. Where bottom-up evidence is thin, conservative gap factors cushion the estimate.

Data Validation & Update Cycle

Outputs pass automated variance screens, peer review, and a senior analyst sign-off. We compare model figures with external indicators such as import tonnage and truck registration growth; anomalies trigger re-checks with respondents. Reports refresh each year, and mid-cycle updates occur when material events, such as currency shifts, policy changes, and major infrastructure commissioning, arise.

Why Mordor's Bangladesh Freight And Logistics Baseline Stand Firm

Published market values often differ because firms pick varied service baskets, pricing bases, and forecast cadences. Our disciplined scope, variable set, and annual refresh limit such drift.

Key gap drivers include whether domestic courier revenues are folded into total logistics, the choice of nominal versus real growth, and the aggressiveness of long-run GDP elasticity. Our study reports a balanced base case, while others may embed uniform 7% CAGRs or rely solely on historic trade curves without validating domestic freight flows.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 31.97 B (2025) | Mordor Intelligence | |

| USD 32.9 B (2024) | Global Consultancy A | Broader service basket and a single 7% CAGR applied across all modes |

| USD 28.7 B (2022) | Research Publication B | Earlier base year and exclusion of courier and contract logistics revenues |

| USD 5.7 B (2023) | Industry Portal C | Focus limited to warehousing; transport and forwarding segments omitted |

The comparison shows that figures swing with scope and assumptions. Mordor's stepwise top-down build, cross-checked with selective bottom-up tests and refreshed each year, offers decision-makers a dependable, transparent baseline for Bangladesh's freight and logistics outlook.

Key Questions Answered in the Report

What is the current value of the Bangladesh freight and logistics market?

The market is worth USD 32.92 billion in 2026 and is projected to grow to USD 38.13 billion by 2031.

Which logistics function holds the largest share?

Freight transport leads with 53.10% of Bangladesh freight and logistics market share in 2025.

Which segment is expanding the fastest?

The Courier, Express, and Parcel (CEP) segment shows the quickest 3.47% CAGR (2026-2031), spurred by e-commerce growth.

How will Padma Bridge affect freight flows?

Padma Bridge has already cut Dhaka-Khulna travel times, creating new southwest corridors and diversifying gateways away from the congested Dhaka-Chattogram axis.

Why is shallow draft at Chattogram Port a constraint?

Limited draft forces reliance on feeder vessels, adding 15-25% to freight costs and extending ocean transit by several days.

What technology initiatives are improving customs efficiency?

Implementation of the Bangladesh Single Window and AI-based risk assessments is lowering clearance times, making border crossings more predictable for shippers.

Page last updated on: