Tanzania Fruits And Vegetables Market Analysis by Mordor Intelligence

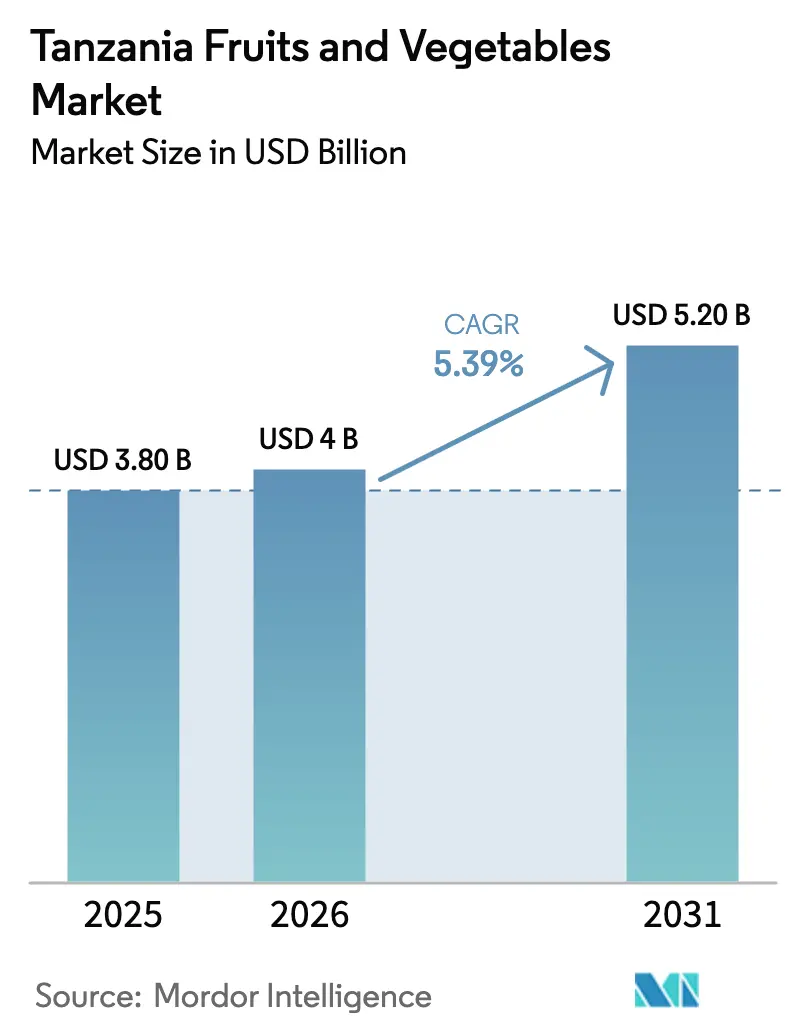

The Tanzania fruits and vegetables market size was valued at USD 3.8 billion in 2025 and estimated to grow from USD 4.0 billion in 2026 to reach USD 5.2 billion by 2031, at a CAGR of 5.39% during the forecast period (2026-2031). Port upgrades, third-party cold-chain investments, and a government push to reach USD 2 billion in annual horticultural exports are accelerating trade flows. Vegetables still anchor domestic consumption, yet the fruits segment is expanding faster as Hass avocado orchards mature and new Chinese market access diversifies export destinations. Modern, GlobalG.A.P–certified packhouses integrate smallholders, while digital agronomy services raise yields and narrow knowledge gaps. Persistent bottlenecks, especially inland refrigerated trucking shortages and post-harvest losses exceeding 30%, remain the primary hindrance to supply-chain efficiency.

Key Report Takeaways

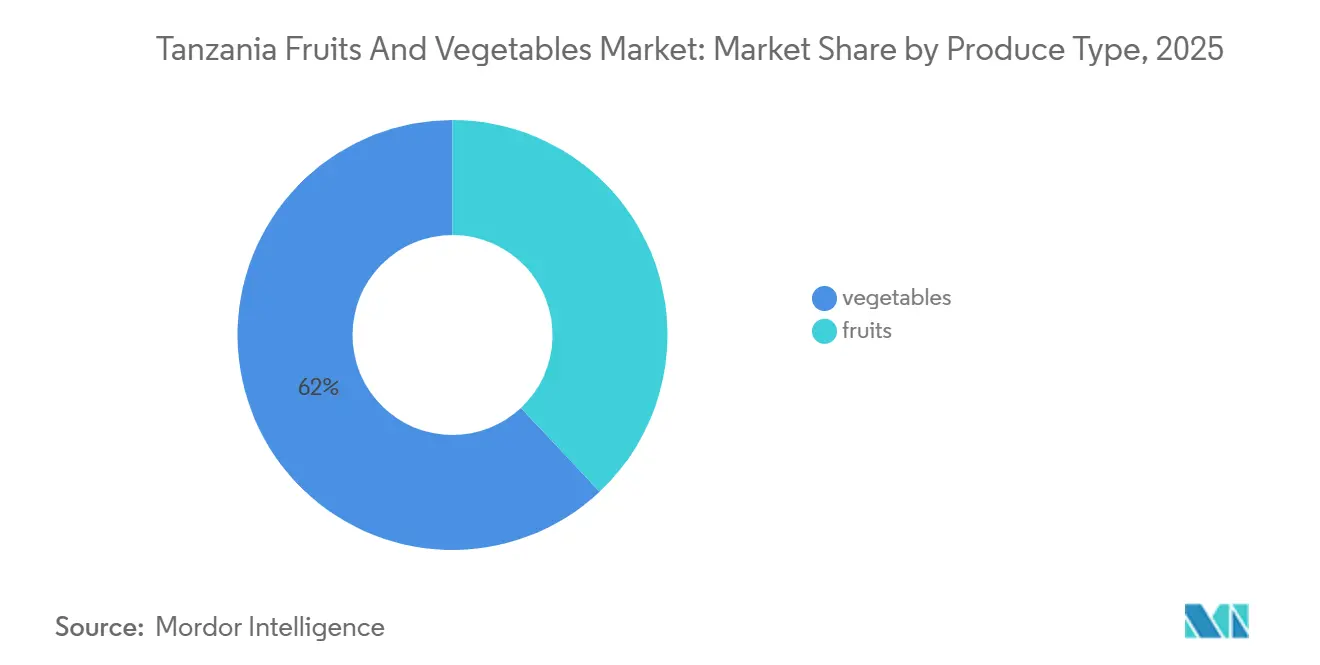

- By produce type, vegetables led with 62% of Tanzania's fruit and Vegetable market value in 2025, while fruits are poised for a 7.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Tanzania Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding horticultural export corridors | +0.9% | Coastal, Northern, and Southern zones | Medium term (2–4 years) |

| Cold-chain investments by third-party logistics specialists | +0.8% | Coastal, Northern, and Southern zones | Medium term (2–4 years) |

| Growing domestic demand for ready-to-cook produce | +0.7% | Coastal, Northern, and Lake zones | Short term (≤ 2 years) |

| Contract-farming programs by large supermarket chains | +0.6% | Northern, Coastal, and Lake zones | Short term (≤ 2 years) |

| Digitized extension services (SMS agronomy alerts) | +0.5% | National | Medium term (2–4 years) |

| Rapid growth of avocado orchards in Southern Highlands | +0.8% | Southern and Northern Highlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Horticultural Export Corridors

Port upgrades in Dar es Salaam and Tanga cut export lead times to the European Union by three days, preserving shelf life and enhancing price realization. The Dar es Salaam Maritime Gateway Project trimmed vessel turnaround from 5.2 days in 2023 to 3.8 days in 2025. Tanga’s USD 12 million rehabilitation added a cold-storage terminal that ships directly to Middle Eastern buyers. The Ministry of Agriculture attributes 15% of the targeted USD 2 billion horticultural exports for 2030 to these corridor efficiencies. Faster clearance also lowers demurrage fees, improving exporter cash flow and encouraging reinvestment in orchard expansion. Importantly, shorter transit times reduce rejection rates at European distribution centers, strengthening Tanzania’s reputation for reliability.

Cold-Chain Investments by Third-Party Logistics Specialists

ARCH Cold Chain Fund committed USD 18 million in 2024 to four regional hubs, each with a 3,000-ton capacity. The Food and Agriculture Organization's (FAO) 24 solar cold rooms in Njombe and Mbeya reduced losses from 40% to below 15% [1]Source: Food and Agriculture Organization of the United Nations, “Official Website,” Food and Agriculture Organization, fao.org. Africado’s Kilimanjaro facility integrates training for 2,290 farmers, demonstrating how infrastructure facilitates the inclusion of smallholders. Access to reliable cooling is especially critical because harvests must travel up to 600 kilometers to port. Cold-chain access also enables diversification into higher-value berries and fresh-cut products that demand strict temperature control. As third-party specialists scale, service fees are falling, making chilled logistics accessible to mid-tier aggregators.

Growing Domestic Demand for Ready-to-Cook Produce

Dar es Salaam, now home to 7.4 million residents, is driving demand for pre-washed and chopped vegetables sold by Quality Center and Shoppers Plaza supermarkets. TBS introduced 14 produce quality standards to support retail packaging [2]Source: Tanzania Bureau of Standards, “Official Website,” Tanzania Bureau of Standards, tbs.go.tz. Zanzibar hotels source 63% of produce locally, signaling a rising food-service channel. Margins widen for processors who extend shelf life compared with raw produce wholesalers. Ready-to-cook packs reduce household meal-prep time, a key benefit for dual-income urban families. Processors earn higher margins per kilogram by selling convenience rather than raw bulk produce. Steady domestic demand cushions exporters against international market fluctuations, enhancing revenue stability.

Contract-farming Programs by Large Supermarket Chains

The EAT Fresh partnership guarantees off-take for 4,000 smallholders, reducing weekly price swings of up to 40%. Rikolto’s project enrolled more than 14,000 farmers and launched 489 demo plots to boost export-grade vegetable supply [3]Source: Rikolto, “Official Website,” Rikolto, rikolto.org. Quality Center advances seed and provides extension support in exchange for exclusive supply. Stable contracts incentivize growers to adopt improved seed and irrigation, lifting yields and quality. Supermarkets gain year-round volumes that meet traceability requirements, cutting reliance on volatile spot procurement. The model also fosters youth engagement by offering predictable income streams in horticulture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-harvest loss rates exceeding 30 percent | -1.2% | National | Short term (≤ 2 years) |

| Limited refrigerated trucking capacity inland | -0.9% | Southern, Central, and Lake zones | Medium term (2–4 years) |

| Volatile farm-gate pricing due to informal middlemen | -0.7% | National | Short term (≤ 2 years) |

| Outbreaks of Tuta absoluta and fruit flies | -0.6% | Southern and Northern Highlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Post-Harvest Loss Rates Above 30 Percent

Tomato losses range from 20% to 40% under normal conditions and can spike to 50% during pest outbreaks. The United States Agency for International Development (USAID) Tuhifadhi Chakula project aims to reduce food waste to 5% by 2030 through training and the development of cooling structures. High loss rates erode farmer incomes and undermine supply reliability for exporters. Wastage inflates consumer prices in urban centers, cutting affordability for low-income households. Excess organic waste also contributes to methane emissions, an emerging sustainability concern for global buyers.

Limited Refrigerated Trucking Capacity Inland

Only 180 certified reefer trucks serve the entire country. The 600-kilometer Mbeya to Dar es Salaam haul often takes 10 hours in 30-degree heat, causing crops to wilt. Some exporters route cargo via Kenya, incurring an additional USD 0.15 per kilogram in costs. Financing hurdles and high diesel prices slow fleet expansion. Limited backhaul opportunities raise per-trip costs, deterring private investment. Without reliable trucking, the economic case for up-country cold rooms weakens, perpetuating the storage deficit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Produce Type: Vegetables Anchor Domestic Demand, Fruits Lead Export Upside

Vegetables accounted for 62% of Tanzania's fruit and vegetable market value in 2025, reflecting staple status for tomatoes, onions, and leafy greens. Tomatoes alone represented more than half of the production tonnage. However, Tuta absoluta and high loss rates hindered the development of an effective, marketable supply. Onions and cabbages thrive under Central Zone irrigation, while French beans and snow peas earn premium export revenue through GlobalG.A.P. pack houses.

The fruits segment is projected to grow at a 7.5% CAGR through 2031, outpacing the vegetables segment, driven by the expansion of avocado orchards and new market access in China. Mangoes face 25 to 40% on-farm losses, yet investments in pack houses and pest management aim to unlock Middle East demand. Passion fruit and citrus remain domestically focused but benefit from tourism-led fresh-cut demand in Zanzibar.

Geography Analysis

The Northern Highlands controlled the majority of Tanzania's fruit and vegetable market share in 2025, propelled by volcanic soils, reliable rainfall, and proximity to Kilimanjaro International Airport. Exporters ship more than 8,000 metric tons of French beans and snow peas annually. Long-standing input suppliers and freight forwarders keep transaction costs low. Land scarcity and rising costs, however, are prompting new investments to move southward.

The Southern Highlands are forecast to post the fastest CAGR from 2026 to 2031, led by 4,500 hectares of new Hass avocado plantations. TAHA’s five collection centers and Nundu pack house bind more than 2,000 farmers into export supply chains. Altitudes of 1,800 to 2,400 meters also support Irish potatoes and carrots that supply Dar es Salaam. Nonetheless, only 180 refrigerated trucks nationwide create cooling gaps on the 600-kilometer route to port.

The Coastal Zone revolves around Dar es Salaam, Pwani, and Tanga, serving both domestic distribution and export logistics. The Dar es Salaam Maritime Gateway Project reduced vessel turnaround time to 3.8 days by 2025, thereby enhancing corridor competitiveness. Tanga Port’s new cold terminal enables direct shipments to the Middle East, cutting logistics costs by 20%. Supermarket demand for ready-to-cook packs is rising in Dar es Salaam’s 7.4 million urban market. The Lake and Central zones remain domestically oriented and are subject to volatile pricing due to broker dominance.

Competitive Landscape

The Tanzania fruits and vegetables market is characterized by the involvement of key players overseeing GlobalG.A.P.-certified packing houses, refrigerated transportation fleets, and phytosanitary compliance systems regulated by the Tanzania Plant Health Inspectorate. These leaders grow revenue at roughly the market's CAGR because vertical integration lets them capture margins 15% to 20% higher than spot-market traders without cold-chain access. Export-focused firms are diversifying beyond the European Union by building supply programs for China and Middle Eastern buyers that prioritize counter-seasonal volumes. Their networks span thousands of contracted smallholders, reducing price volatility and raising on-farm quality through seed advances and agronomic support.

Leading exporters are focusing on key priorities to protect and expand their market share. Investments in the development of regional cold-storage hubs have reduced post-harvest losses from 40% to below 15%. The implementation of digital traceability systems, which integrate farm records, grading data, and temperature logs, has enabled these exporters to secure price premiums of 8% to 10% from buyers who emphasize food safety. Geographic diversification into the Southern Highlands avocado belt allows exporters to capitalize on counter-seasonal export opportunities to Europe while positioning themselves to meet China’s annual avocado demand growth of 18%. Additionally, contract-farming programs are being scaled to include up to 5,000 growers, incorporating soil testing, irrigation system installation, and integrated pest management training, which collectively increase yields by over 10%.

Mid-tier and emerging participants pursue alternative growth paths. Mobile aggregation platforms bypass traditional brokers, connecting farmers with urban retailers and hotels, cutting intermediary margins by up to 30%, and giving growers next-day payment visibility. Domestic processors are launching ready-to-cook packs, dried fruit lines, and frozen formats that target Dar es Salaam’s growing middle class and Zanzibar’s tourism sector, where local sourcing already exceeds 60%. Niche players secure organic and fair-trade certifications to reach premium European Union buyers willing to pay mark-ups of 15% to 20% despite certification costs that must be amortized over multiyear contracts. Cooperative models such as public–private partnerships demonstrate that organized farmer groups can raise farm-gate prices by more than 18% through pooled volumes and stronger negotiating power.

Recent Industry Developments

- October 2025: Government officials unveiled a digital export-expansion program that combines e-certification, mobile quality inspection apps, and blockchain traceability to streamline compliance for smallholder exporters. Pilot tests demonstrated a 40% reduction in document-processing time, which helped participating firms secure faster payments from overseas buyers.

- October 2025: The Tanzania Horticultural Association announced the launch of HortiTanzania Expo, a new annual trade show in Arusha that will showcase seeds, greenhouse technologies, pack-house equipment, and cold-chain solutions. Organizers expect more than 150 exhibitors and 4,000 visitors, positioning the event as a regional hub for East African buyers and technology providers.

- August 2025: Tanzania unveiled an export promotion campaign at Asia Fruit Logistica 2025 aimed at capturing a share of China’s USD 19.4 billion fresh fruit import market. The initiative prioritizes Hass avocados and mangoes and includes in-store tastings, digital marketing, and fast-track phytosanitary clearance for pre-approved orchards.

Tanzania Fruits And Vegetables Market Report Scope

A fruit develops from the flower of a plant and contains seeds. Vegetables are a culinary classification that includes edible plant parts, such as roots, stems, leaves, and flowers, that are typically not sweet. Culinary usage often distinguishes fruits as sweet or tart foods used in desserts or snacks, while vegetables are commonly savory and served as part of main or side dishes. The Tanzania Fruits and Vegetables market is analyzed by production (volume), consumption (volume and value), imports (volume and value), exports (volume and value), wholesale price trends, and more. The report provides market sizes and forecasts for all the above segments, expressed in value (USD) and volume (Metric Tons).

By Produce Type

| Vegetables | Tomatoes | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | ||

| Key Supplying Markets | ||||

| Export Market Analysis | Export Value and Volume | |||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Onions | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Cabbage | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Beans | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Chilies and Peppers | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Fruits | Mangoes | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Watermelons | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Oranges | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Pineapples | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Avocado | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| By Produce Type | Vegetables | Tomatoes | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |||

| Key Supplying Markets | |||||

| Export Market Analysis | Export Value and Volume | ||||

| Key Destinations Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Onions | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destinations Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Cabbage | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destinations Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Beans | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destinations Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Chilies and Peppers | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destinations Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Fruits | Mangoes | Production Analysis | Production Volume | ||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destinations Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Watermelons | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destinations Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Oranges | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destinations Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Pineapples | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destinations Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Avocado | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destinations Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

Key Questions Answered in the Report

What is the current size of the Tanzania fruits and vegetables market?

The market was valued at USD 4.0 billion in 2026.

Which product category is growing fastest?

Fruits, led by Hass avocado, are forecast to advance at a 7.5% CAGR through 2031.

What is the main logistical constraint for exporters?

Limited inland refrigerated trucking, with only 180 certified reefer trucks nationwide, raises spoilage risk and costs.

How significant are post-harvest losses?

Losses exceed 30% nationally, reaching 40% for some crops, but targeted cold-chain investments aim to reduce them below 15%.

Page last updated on: