Ballistic Composites Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

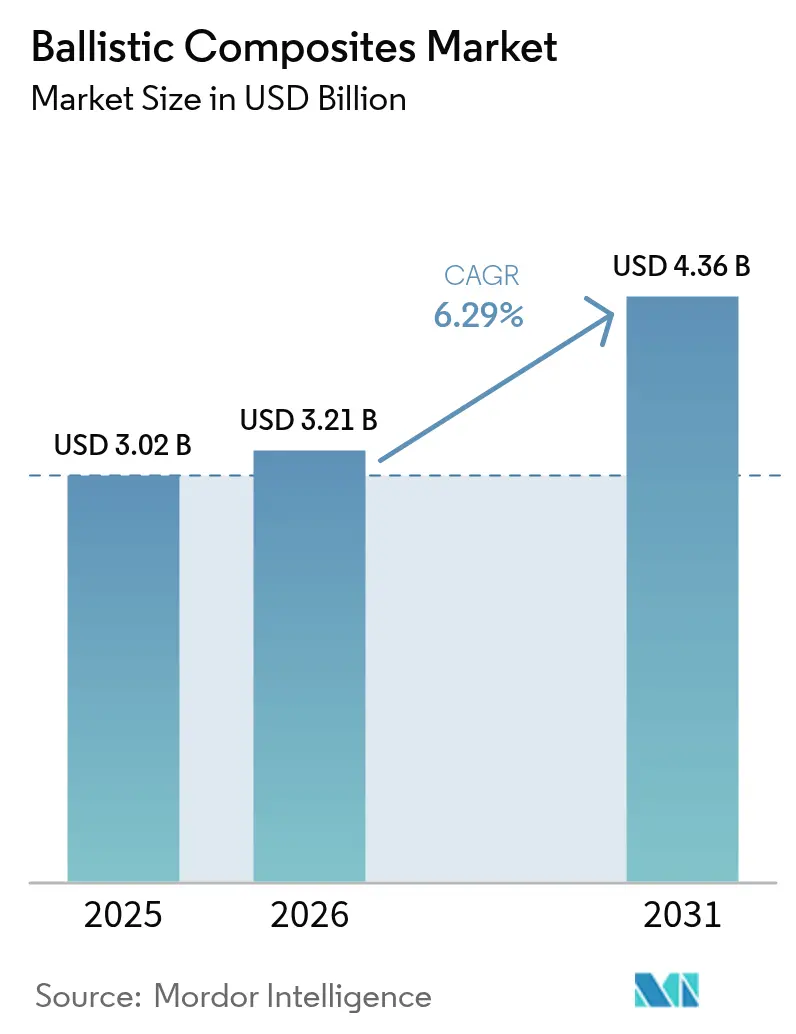

| Market Size (2026) | USD 3.21 Billion |

| Market Size (2031) | USD 4.36 Billion |

| Growth Rate (2026 - 2031) | 6.29% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ballistic Composites Market Analysis by Mordor Intelligence

Ballistic Composites Market size in 2026 is estimated at USD 3.21 billion, growing from 2025 value of USD 3.02 billion with 2031 projections showing USD 4.36 billion, growing at 6.29% CAGR over 2026-2031. Steady gains come from defense modernization, autonomous vehicle shielding, and the aerospace sector’s persistent drive to trim airframe mass without sacrificing crew safety. Demand growth concentrates on lighter yet tougher laminate configurations, wider adoption of hybrid fiber lay-ups, and the migration of advanced composite tooling from the aerospace supply chain into armor production lines. Aramid fibers reinforce much of today’s armor solutions, while polymer matrices enable manufacturers to balance multi-hit performance with processing flexibility. North America retains its pole position thanks to the United States Army’s high-budget soldier modernisation programs and next-generation vehicle platforms that rely on sophisticated armor architectures. Meanwhile, Asia-Pacific commands attention with accelerated procurement of personal protection gear for large infantry forces. Technology launches such as DuPont’s Kevlar EXO, which delivers 30% higher tensile strength than standard aramid, showcase the innovation pace that underpins the ballistic composites market.

Key Report Takeaways

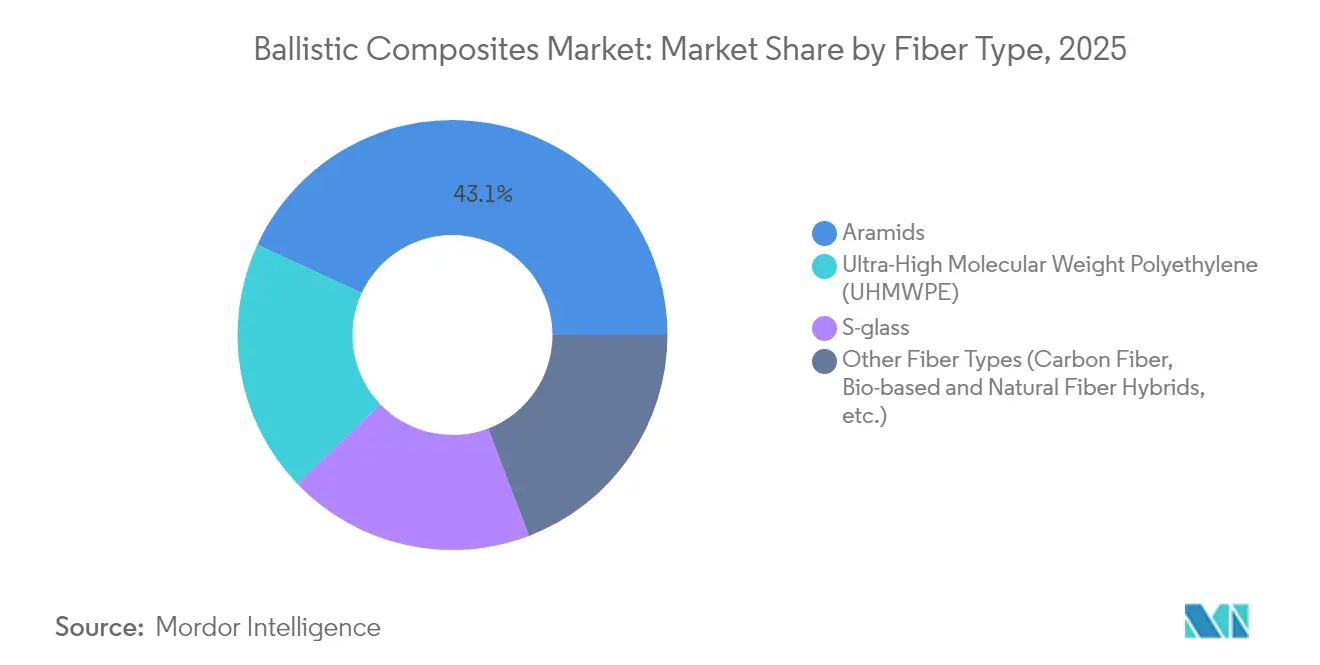

- By fiber type, aramid captured 43.10% of ballistic composites market share in 2025, while ultra-high molecular weight polyethylene (UHMWPE) posted the fastest 6.36% CAGR between 2026 and 2031.

- By matrix type, polymer systems accounted for 52.10% of ballistic composites market share in 2025 and are advancing at a 6.30% CAGR through the forecast window.

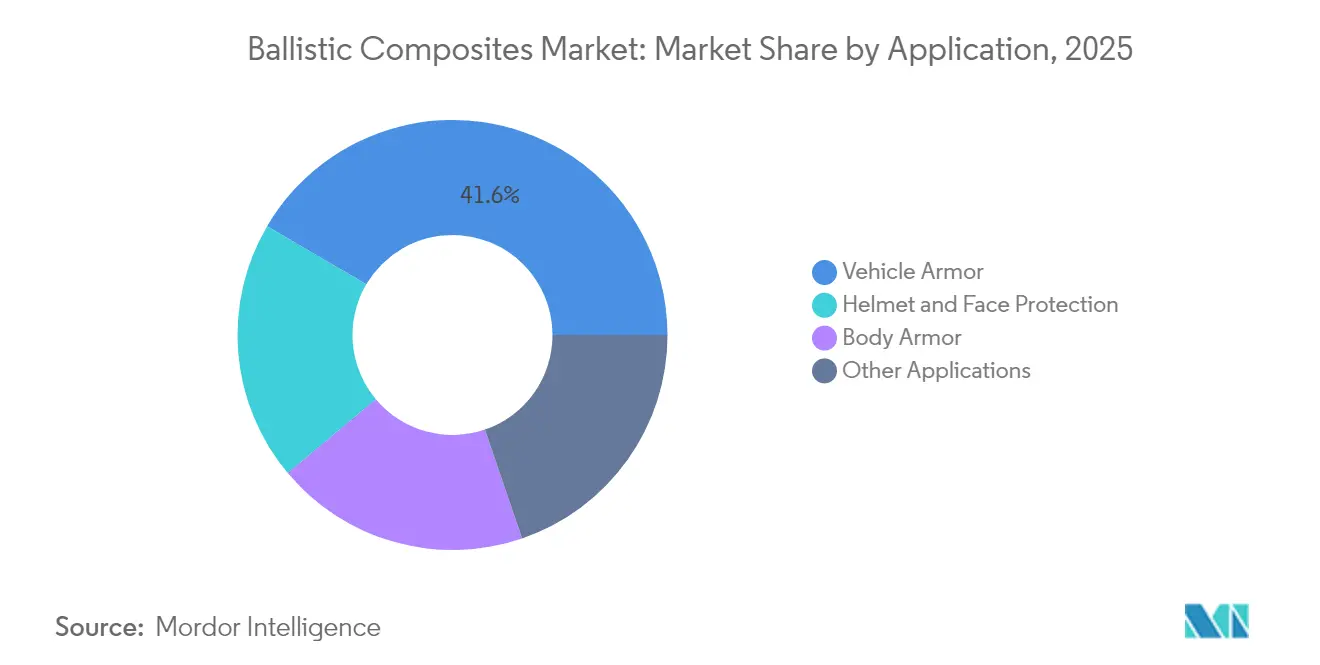

- By application, vehicle armor held 41.55% share of ballistic composites market size in 2025, whereas helmet and face protection is projected to expand at a 6.45% CAGR to 2031.

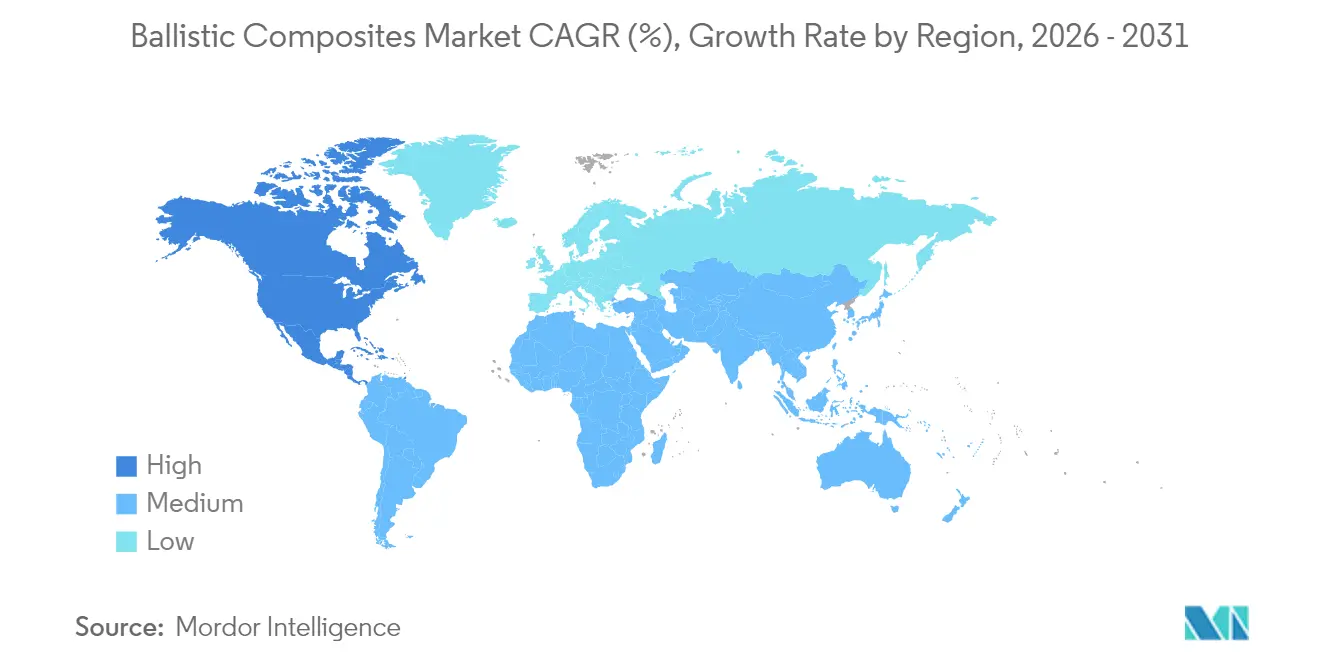

- By geography, North America dominated with 42.80% revenue share in 2025, and the region also records the highest 6.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ballistic Composites Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in Global Defence Expenditure | +1.8% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Lightweighting Push in Aerospace and Defence Platforms | +1.2% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rapid Soldier-modernisation Programmes in Emerging Economies | +1.0% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Development of Terrain Motor Vehicles With Ballistic Protection | +0.8% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Growing Demand for Multi-hit Hybrid Armour for Autonomous Ground Vehicles | +0.6% | North America and Europe, pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Global Defence Expenditure

Defense spending escalation across major economies fundamentally reshapes ballistic composites demand patterns, shifting procurement priorities toward advanced materials that deliver superior protection-to-weight ratios. The United States Army's Ground X-Vehicle Technologies program exemplifies this trend, targeting 50% weight reduction while maintaining survivability through innovative composite armor systems rather than traditional steel plating. This strategic pivot reflects military planners' recognition that future combat effectiveness depends on mobility and agility rather than passive armor thickness. Asian defense markets are experiencing parallel modernization drives, with countries like India integrating advanced ballistic helmets into standard infantry equipment, as demonstrated by MKU Limited's delivery of Kavro Doma 360 helmets to the Indian Army in 2025. The procurement shift toward composite materials creates sustained demand growth that transcends traditional cyclical defense spending patterns.

Lightweighting Push in Aerospace and Defence Platforms

Aerospace and defense manufacturers are pursuing aggressive weight reduction strategies that position ballistic composites as critical enablers of next-generation platform performance. Carbon fiber composites in missile applications demonstrate 40-50% weight reductions compared to aluminum alternatives, enabling extended operational ranges and enhanced payload capacities that directly translate to tactical advantages [1]AddComposites, “Weight savings in missile casings,” addcomposites.com. The trend extends to extreme-temperature hypersonic systems. In 2025, Canopy Aerospace secured a USD 2.8 million U.S. Air Force contract for reusable thermal-protection tiles that withstand ballistic impact during re-entry. Cross-pollination of thermal and ballistic requirements gives the ballistic composites market new growth vectors.

Rapid Soldier-Modernisation Programmes in Emerging Economies

Emerging economies are implementing comprehensive soldier modernization programs, prioritizing individual protection systems over traditional heavy armor platforms, creating substantial demand for personal ballistic composites. These programs reflect a strategic shift toward asymmetric warfare capabilities where soldier survivability and mobility take precedence over conventional force projection. The emphasis on personal protection systems drives innovation in helmet and body armor technologies, with manufacturers developing lighter, more comfortable solutions that maintain or enhance ballistic performance. Advanced materials like UHMWPE are gaining traction due to their superior strength-to-weight ratios compared to traditional aramid fibers, enabling extended wear periods without compromising protection levels. This trend is particularly pronounced in Asia-Pacific markets where rapid military modernization coincides with domestic manufacturing capability development, creating opportunities for international suppliers and local composite manufacturers.

Development of Terrain Motor Vehicles With Ballistic Protection

Military vehicle manufacturers are integrating ballistic protection as a fundamental design requirement rather than an aftermarket addition, driving demand for structural composite materials that combine load-bearing and protective functions. The International Armored Group's expansion into advanced Infantry Fighting Vehicles demonstrates how ballistic composites are becoming integral to vehicle architecture, with the Rila 6x6 and 8x8 platforms engineered to meet STANAG 4596 protection levels while maintaining tactical mobility. This integration approach reduces overall vehicle weight compared to traditional add-on armor solutions while providing superior protection against evolving threat profiles. The development of autonomous ground vehicles is accelerating this trend, as unmanned platforms can accommodate higher protection levels without crew comfort constraints, enabling more aggressive use of advanced composite materials in critical areas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Processing and Qualification Costs | -1.4% | Global, with higher impact in cost-sensitive emerging markets | Medium term (2-4 years) |

| Volatile Aramid and Ultra-high Molecular Weight Polyethylene (UHMWPE) Precursor Supply | -0.9% | Global, with supply concentration in Asia-Pacific | Short term (≤ 2 years) |

| Perfluoroalkyl and Polyfluoroalkyl Substances (PFAS)-related Environmental Regulations on Aramid Finishing | -0.7% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Processing and Qualification Costs

The ballistic composites industry faces substantial barriers from complex processing requirements and extensive qualification protocols that significantly inflate production costs and market entry thresholds. NIJ Standard 0101.07, implemented in 2024, introduces more rigorous testing methodologies for ballistic-resistant body armor, requiring manufacturers to invest in advanced testing facilities and extended qualification timelines [2]National Institute of Justice, “NIJ Standard 0101.07,” nij.ojp.gov. Military standards such as STANAG 4569 add further complexity with multi-angle, multi-velocity shot matrices that only a handful of laboratories can deliver. Investment in controlled-atmosphere hot presses, fibre tension rigs, and computerised drape forming lines inflates entry costs, favouring incumbents within the ballistic composites market.

Volatile Aramid and Ultra-high Molecular Weight Polyethylene (UHMWPE) Precursor Supply

Raw material supply chain volatility represents a critical constraint on ballistic composites market growth, with aramid and Ultra-high Molecular Weight Polyethylene (UHMWPE) precursor availability subject to concentrated supplier bases and complex chemical processing requirements. Aramid fiber production relies on specialized chemical precursors that require sophisticated polymerization processes, making supply chains vulnerable to disruptions from environmental regulations, plant maintenance, or geopolitical tensions. Ultra-high Molecular Weight Polyethylene (UHMWPE) production depends on specialist Ziegler-type catalysts that only a few Asian suppliers master. Teijin Aramid trimmed its workforce in 2024 as pricing pressure mounted, reflecting how feedstock swings unsettle capacity planning. Such volatility prompts armour producers to carry larger safety stocks, adding working-capital strain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber Type: Aramids Dominate Through Innovation

Aramid fibre held 43.10% share of ballistic composites market size in 2025 and is forecast to expand at a 6.18% CAGR. The latest Kevlar EXO fibre improves tensile strength by 30% while maintaining flame resistance, enabling thinner armour panels and improved soldier mobility. UHMWPE is narrowing the gap, appealing to customers that prioritise weight reduction and moisture resistance. S-glass remains prominent in vehicular armour where high-temperature exposure is common. Competitive tension is intensifying as research laboratories demonstrate carbon-nanotube yarns with dynamic strength above 14 GPa, a level that could redefine the ballistic composites market.

Aramid suppliers defend their position through improved surface treatments that enhance matrix adhesion and through partnerships with fabric weavers that can tailor multiaxial lay-ups for multi-hit scenarios. UHMWPE producers are expanding capacity in Asia to stabilise lead times and costs. Hybrid laminates that blend aramid, UHMWPE, and carbon fibres balance tensile strength, delamination resistance, and thermal robustness. Bio-based fibre initiatives, though still niche, attract defence agencies focused on sustainability targets, signalling the long-term diversification path within the ballistic composites market.

By Matrix Type: Polymer Systems Enable Versatility

Polymer matrices commanded 52.10% of ballistic composites market share in 2025 and lead growth with a 6.30% CAGR to 2031. Thermoset epoxies and high-toughness phenolics provide predictable viscosity windows for vacuum-assisted resin transfer moulding. Thermoplastic tapes based on poly-propylene and poly-amide allow thermoforming into complex helmet shells with short cycle times. Ceramic-rich polymer hybrids answer the multi-hit need in advanced land vehicles, integrating boron carbide tiles bonded to energy-absorbing backers. Titanium-based metal matrix systems attract aerospace primes that tolerate higher costs for unmatched temperature endurance.

Process routes diversify. Out-of-autoclave consolidation lowers factory energy bills, while induction welding gives field repairability. Milliken & Company’s Tegris fabric demonstrates how polypropylene tapes fused into rigid sheets yield fragment resistance equal to glass laminates at half the weight. Matrix producers respond to PFAS restrictions by introducing water-based dispersion chemistries that retain ballistic efficiency.

By Application: Vehicle Armor Leads, Helmets Accelerate

Vehicle armour accounted for 41.55% of ballistic composites market share in 2025. Infantry Fighting Vehicles such as the Bradley M2A2 ODS-SA employ layered steel and aluminium augmented by reactive tiles to defeat tandem warheads, while new variants integrate composite hull sections to trim mass and enhance payloads. Technological demonstrations of composite metal foams show promise for future vehicles because the foam dissipates three times the impact energy of solid armour plate at one-third the weight, broadening the addressable opportunity for the ballistic composites market.

Helmet and face protection is the fastest-advancing sub-market, projected at a 6.45% CAGR. Next-generation combat helmets fuse UHMWPE shells, aramid layers, and impact-absorbing liners, while integrated visors apply graded transparency ceramics for full facial coverage. Liquid armour concepts using shear-thickening fluids lock instantly under impact, delivering flexibility during routine wear.

Geography Analysis

North America led the ballistic composites market with 42.80% revenue share in 2025 and is expected to grow at a 6.46% CAGR through 2031. The Future Long-Range Assault Aircraft program relies on Integris Composites armour fitted into the Bell V-280 Valor airframe, a clear sign of sustained demand. Robust federal defense budgets, resilient supply chains, and university-backed testing infrastructure underpin regional dominance.

Asia-Pacific is the fastest-scaling region outside North America. China, India, Japan, and South Korea invest in lighter individual protection equipment and domestically produced vehicle armour. India’s Light Combat Vehicle program specifies composite appliqué kits to reduce curb weight, reflecting a shift from steel-only hulls. South Korea integrates fibre-metal laminates in K2 Black Panther tanks to improve mine resistance without weight penalties.

Europe revives timid defence budgets amid heightened security concerns. Manufacturers such as International Armored Group operate an expanded vehicle plant in Bulgaria, ensuring shorter lead times for NATO contracts. Germany tests the Leopard 2 ARC 3.0 with an active protection suite and modular composite skirts, pushing demand for interchangeable composite modules across allied fleets.

Regulatory Landscape

Ballistic composites used in body armor are shaped by performance standards and test methodologies that affect material selection, laminate architecture, and qualification costs. In the United States, the National Institute of Justice (NIJ) Standard 0101.07 (implemented in 2024) tightened ballistic-resistance requirements for law-enforcement body armor, and it relies on ASTM-aligned laboratory procedures. This increases the need for consistent control of fiber, resin, and lay-up across production lots.

During 2025, NIJ continued to refine the compliance framework, including publication of NIJ Standard 0123.00 (Specification for NIJ Ballistic Protection Levels and Associated Test Threats) and addenda updates to NIJ 0101.07 (including Addendum 2 in July 2025 and Addendum 3 in November 2025). For internationally traded ballistic materials and finished armor, export controls also remain a gating factor, with classification-dependent requirements under U.S. ITAR (Department of State) and EAR (Department of Commerce) influencing supplier qualification, customer eligibility, and cross-border technology transfer for advanced fibers and armor system designs.

Value Chain Analysis

The ballistic composites value chain begins with chemical feedstocks and specialty precursors, then moves into fiber production (aramids and UHMWPE), fabric formation and unidirectional tape or ply manufacturing, prepreg and panel consolidation, and, finally, integration by armor OEMs into body armor, helmets, and vehicle appliques. Upstream inputs include aramid polymer precursors, ethylene-based UHMWPE resins (and catalysts), and specialty resin systems (epoxy, phenolic, and thermoplastic) that influence consolidation temperature, cycle time, and multi-hit performance.

Midstream converters and composite fabricators translate fibers into woven, multiaxial, and UD formats, then produce consolidated sheets and laminates. Armor OEMs assemble finished systems and run NIJ and STANAG test programs. Bottlenecks tend to cluster around high-performance fiber availability and qualification throughput, and logistics can also disrupt ceramic and precursor deliveries, with congestion at major European ports such as Hamburg and Rotterdam cited as a friction point for hard-armor inputs. Capacity changes upstream can shift lead times and allocation dynamics, including Solstice Advanced Materials initiating a USD 220 million expansion for Spectra Shield ballistic fiber production (announced January 2026), which supports a broader push toward more secure, domestically anchored supply for critical fibers.

Competitive Landscape

The Ballistic Composites Market exhibits moderate consolidation with the presence of major players, such as DuPont, Avient Corporation, Honeywell International Inc., Teijin Limited, and BAE Systems. These companies own proprietary fibre chemistries, mature finishing lines, and multi-decade ties to procurement agencies. DuPont’s consideration of divesting Kevlar and Nomex in 2025, valued at nearly USD 2 billion, signals portfolio optimisation yet underlines the attractiveness of high-margin defence fibres. Portfolio refresh is accelerating. Avient acquired DSM Protective Materials for USD 2 billion in 2025, inheriting Dyneema UHMWPE and gaining a platform to expand in personal armour.

Ballistic Composites Industry Leaders

DuPont

Teijin Limited

Honeywell International Inc.

Avient Corporation

BAE Systems

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear opportunity emerges where tighter performance standards (NIJ 0101.07 in the United States and STANAG-driven procurement for military programs) intersect with the industry push toward lighter, multi-hit solutions for helmets, hard plates, and vehicle kits. Manufacturers that internalize more testing capability, standardize repeatable lay-ups, and pair fibers with qualified resin systems can shorten revalidation cycles when standards and threat matrices update, which has been reinforced by NIJ revisions to 0101.07 via addenda during 2025.

Technical whitespace remains in hybridization and interfacial engineering that improves energy absorption without adding mass. Peer-reviewed 2026 research reports point to multiple pathways, including UHMWPE hybrid ballistic panels combined with boron carbide (B4C), which achieve substantial weight reductions versus steel references while meeting STANAG 4569 Level 3 requirements, and functionalized carbon nanotube (CNT) film approaches that increase dynamic impact energy absorption in UHMWPE composite systems. On the supply side, upstream investments that expand qualified fiber output provide room for armor OEMs and converters to pursue dual-sourcing and faster delivery cycles, supported by Solstice Advanced Materials announcing a USD 220 million Spectra and Spectra Shield manufacturing expansion in Virginia (January 2026).

Recent Industry Developments

- January 2026: Solstice Advanced Materials announced a USD 220 million investment to expand Spectra and Spectra Shield ballistic fiber manufacturing in Chesterfield County, Virginia. The expansion strengthens domestic supply availability for UHMWPE-based ballistic composite architectures used in hard and soft armor. This upstream capacity action can improve lead times and reduce allocation risk for armor OEMs qualifying to NIJ and STANAG requirements.

- December 2025: DuPont launched Kevlar EXO for hard armor applications, positioning the fiber for use in helmets and ballistic plate inserts where protection-to-weight performance is critical. The launch adds another commercially available aramid option for hybrid lay-ups that balance multi-hit durability with manufacturability. It also signals ongoing product refresh in a market where qualification cycles can lock in material choices for multi-year contracts.

- January 2024: Atomic-6 raised USD 9.2 million in mixed funding to advance rapid-cure composite armor manufacturing technologies supporting U.S. Air Force programs. The work targets faster processing routes that can shorten production cycles and reduce cost barriers tied to qualification and throughput. If scaled, rapid-cure processing can expand capacity at converters and armor integrators without proportional increases in press time and energy use.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the ballistic composites market covers composite materials engineered to stop or reduce the impact of ballistic threats, and used in protection products and platforms where weight and mobility matter.

Scope exclusions: We exclude basic metals and non-composite armor materials sold as standalone protection, and we also exclude services such as testing, installation, and maintenance.

Segmentation Overview

- By Fiber Type

- Aramids

- Ultra-High Molecular Weight Polyethylene (UHMWPE)

- S-glass

- Other Fiber Types (Carbon Fiber, Bio-based and Natural Fiber Hybrids, etc.)

- By Matrix Type

- Polymer

- Polymer-Ceramic

- Metal

- By Application

- Vehicle Armor

- Body Armor

- Helmet and Face Protection

- Other Applications (Aircraft and Marine Protection, High-performance Sporting Goods, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the structure of the model and to anchor it to measurable defense and safety demand signals. We reviewed public sources such as defense procurement and budget documents, customs and trade statistics, and standards references related to ballistic performance and protective equipment.

To keep assumptions realistic, we also cross-checked adoption and material trends using sources such as the US Census Bureau trade data, UN Comtrade, World Bank macro indicators, NATO and national defense ministry releases, and peer-reviewed materials science journals that cover aramid, UHMWPE, and composite laminates. Supplier websites, investor presentations, and annual reports were used to understand product positioning and end-use exposure, while paid subscriptions for company financials, patent searches, and shipment-level trade helped fill gaps where public data was thin. These examples are illustrative only, and there were many other sources also referred to for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what portion of composite demand is truly ballistic-grade, and how buying cycles shift by end user and region. We spoke with a mix of material suppliers, fabricators, and downstream users to confirm typical use cases (body armor, vehicle armor, and helmet and face protection), and to sanity-check pricing movements, qualification timelines, and substitution between fibers and hybrid layups across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 37% |

| Mid tier: 55% | Functional/Unit leaders: 33% | EMEA: 37% |

| Smaller Players: 14% | Managers: 55% | Americas: 26% |

Market-Sizing & Forecasting

Sizing started with a top-down build where defense and security demand pools were reconstructed using procurement direction, protective equipment issuance patterns, and platform-level armor needs, which were then translated into composite material value. Once this path was set, we ran selective bottom-up checks using sampled volume by application multiplied by typical composite content and average selling prices, then adjusted when the two views showed a persistent gap.

Key inputs used in the model included the mix shift between aramid and UHMWPE, the share of hard armor versus soft armor use, replacement and refurbishment timing for vests and plates, vehicle armor retrofit activity, and the pricing trend for high-performance fibers and resin systems. Forecasts were built using scenario analysis, where base, conservative, and accelerated procurement cases were discussed with experts, and then the final path was chosen after it matched near-term contract signals and capacity commentary. Where direct volume signals were not available for a country or niche application, proxy indicators were used (such as defense spending direction and trade flows of relevant protective equipment) and were later normalized through interview feedback.

Data Validation & Update Cycle

Outputs were checked against independent signals such as defense budget shifts, known procurement programs, and observed price movements for key fibers and composite forms. When a country result looked unusual, the assumptions were re-opened, and follow-up calls were triggered to confirm whether the change was driven by timing, currency, or a genuine demand step-up.

Before sign-off, the model and the written logic go through a multi-step analyst review so calculation errors and inconsistent definitions are removed. The report is refreshed annually, and interim updates are completed when material events occur, such as major contract awards or sharp raw material price changes. Right before delivery, a final pass is performed so the numbers align with the latest available public releases.

Mordor Intelligence's Ballistic Composites Market Estimate Compared With Other Published Estimates

Published market sizes for ballistic composites can look far apart even when everyone is talking about similar protective needs. The differences usually come from what gets counted as ballistic-grade material, which applications are included, and how price and currency timing are treated in the base year.

In this market, the biggest gap drivers tend to be whether adjacent non-ballistic composites are blended in, whether spending is modeled from defense procurement signals or from broad materials revenue, and whether the current-year value is anchored to a specific application mix across body armor, vehicle armor, and helmet and face protection. Some estimates also start from an earlier base year and then apply a single growth rate, which can miss short-term spikes from procurement cycles and qualification delays.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.21 B (2026) | |

| Industry Research Publisher A | USD 1.91 B (2024) | Uses an earlier base year and appears to anchor sizing to broad ballistic protection demand, which can undercount platform and replacement-cycle effects that lift material value in later years. |

| Industry Research Publisher B | USD 2.09 B (2025) | Provides limited clarity on what qualifies as ballistic-grade composites versus adjacent composites, and the longer forecast horizon can amplify growth assumptions if procurement timing is not explicitly modeled. |

The benchmark table shows a spread that is largely explained by base-year selection and what gets filtered into the definition, and in Mordor Intelligence's model the 2026 value is tied to application-level demand (body armor, vehicle armor, and helmet and face protection) and then validated with pricing and mix checks rather than a single blended growth path. When the scope, timing, and pricing logic are made explicit, the final number becomes easier to trace and to update as procurement cycles change.

Key Questions Answered in the Report

What is the current value of the ballistic composites market?

The ballistic composites market size stands at USD 3.21 billion in 2026, with a projection to reach USD 4.36 billion by 2031.

Which fibre type dominates sales?

Aramid fibres lead with 43.10% market share in 2025 and continue to grow at a 6.18% CAGR.

Why are polymer matrices preferred in armour panels?

Polymer systems account for 52.10% market share because they combine processing flexibility with high energy absorption, supporting multi-hit capability.

Which region grows the fastest?

North America not only holds 42.80% share but also posts the highest 6.46% CAGR, propelled by U.S. soldier modernisation and vehicle armour programs.

What regulations could impede growth?

Perfluoroalkyl and Polyfluoroalkyl Substances (PFAS) restrictions on aramid finishing, adopted in states like California and New York, require reformulated coatings and re-qualification of armour products.

Page last updated on: