Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

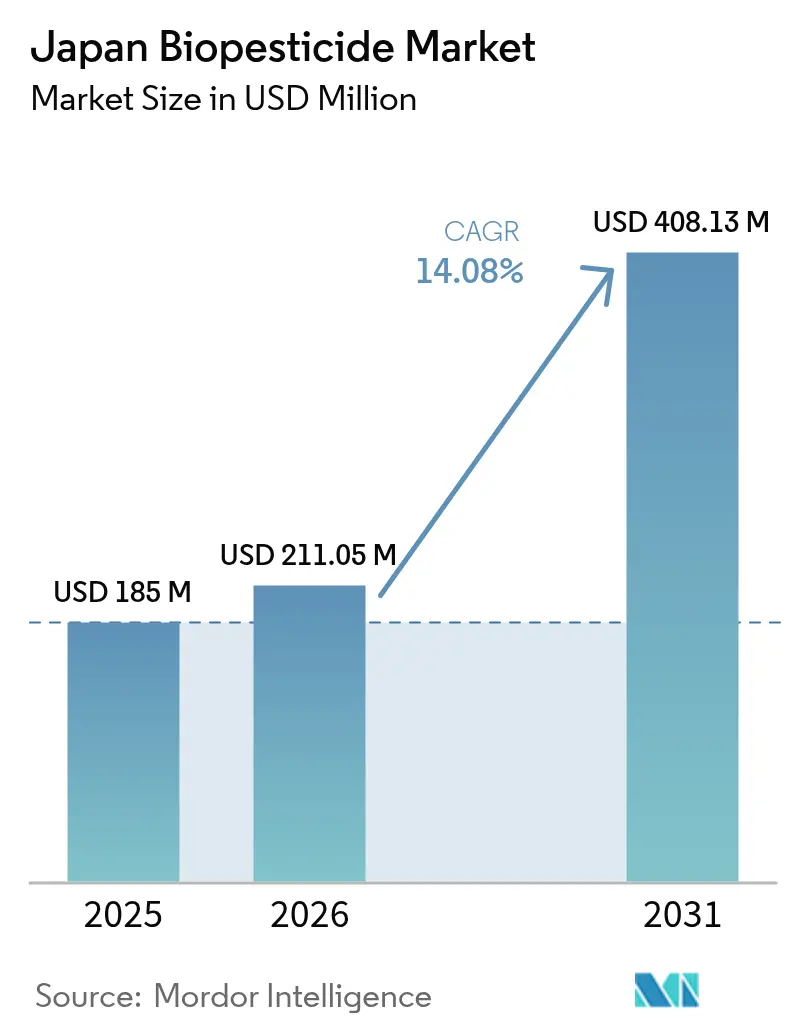

| Base Year Market Size (2025) | USD 185 Million |

| Market Size (2026) | USD 211.05 Million |

| Market Size (2031) | USD 408.13 Million |

| Growth Rate (2026 - 2031) | 14.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Biopesticide Market Analysis by Mordor Intelligence

The Japan biopesticide market size was valued at USD 185 million in 2025 and estimated to grow from USD 211.05 million in 2026 to reach USD 408.13 million by 2031, at a CAGR of 14.08% during the forecast period (2026-2031). This growth is supported by the Ministry of Agriculture, Forestry, and Fisheries' MIDORI Strategy, which aims to reduce chemical pesticide risk by 10% by 2030 and 50% by 2050, providing a policy-driven boost to the biopesticides market. Bioinsecticides currently lead in revenue as growers transition away from pyrethroids, which have become less effective against pests such as planthoppers and fall armyworm. Additionally, the demand for biochemical biopesticides is increasing in turf and ornamental grass applications, where residue-free aesthetics command premium pricing. The Green Food System Law, which includes subsidies amounting to USD 200 million for integrated pest management, shortens grower payback periods and encourages smallholders to adopt biological pest control programs. Export-focused fruit and vegetable supply chains, which enforce stringent residue limits, further position biopesticides as a critical tool for maintaining access to European and North American markets. Leading companies leverage rapid-registration processes, local fermentation facilities, and combined synthetic-biological product offerings to strengthen their market presence.

Key Report Takeaways

- By product type, bioinsecticides captured 37.40% of the Japane biopesticide market size in 2025, while biochemical biopesticides are advancing at a 14.95% CAGR toward 2031.

- By application, fruits and vegetables accounted for 41.00% of the Japan biopesticide market size in 2025, while turf and ornamental grass is forecast to expand at a 13.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Biopesticide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for organic farming and produce | +3.2% | National, strongest in Kanto, Kansai, Kyushu | Medium term (2–4 years) |

| Regulatory support for sustainable agriculture | +2.8% | Nationwide, MAFF-led | Long term (≥ 4 years) |

| Environmental and health concerns | +2.5% | Urban markets Tokyo, Osaka, Nagoya | Short term (≤ 2 years) |

| Government subsidies for integrated pest management | +2.1% | Smallholders in Tohoku, Hokuriku | Medium term (2–4 years) |

| Increasing chemical-pesticide resistance in target pests | +1.9% | Kyushu, Kanto greenhouses | Short term (≤ 2 years) |

| Carbon-credit programs favoring biologically derived inputs | +1.2% | Early pilots in Hokkaido, Tohoku | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Organic Farming and Produce

Japan's organic retail sales expanded, driven by consumer willingness to pay a 26 to 29% premium for pesticide-free produce, yet this premium often fails to cover the 1.35 to 1.6 times higher production costs that organic growers face. The MIDORI Strategy's target of 1 million hectares of organic farmland by 2050 represents a tenfold increase from current levels, creating a structural demand pull for biopesticides that can bridge the transition period when fields are converting from conventional to certified organic status [1]Source: Ministry of Agriculture, Forestry and Fisheries, “Green Food System Strategy,” maff.go.jp. Retailers such as Aeon and Seven and i Holdings are expanding organic private-label lines, leveraging traceability systems that highlight reduced chemical residue as a point of differentiation in saturated fresh produce categories. This dynamic is most pronounced in Kanto's peri-urban vegetable belts, where proximity to Tokyo's affluent consumer base justifies the higher input costs and logistical complexity of organic production systems.

Regulatory Support for Sustainable Agriculture

The Ministry of Agriculture, Fisheries and Food (MAFF) introduced a fast-track approval pathway for biopesticides under the revised Agricultural Chemicals Regulation Law, reducing registration timelines from 36 months to 24 months for microbial actives with established safety profiles, thereby lowering market entry barriers for biocontrol innovators. The Green Food System Law, enacted in 2024, designated over 17,000 certified producers eligible for direct payments and technical assistance, creating a cohort of early adopters who serve as demonstration sites for biological pest management practices. These policy instruments collectively de-risk biopesticide adoption by socializing transition costs and compressing the payback period for growers who invest in new application equipment and training.

Environmental and Health Concerns

Consumer backlash against chemical residue has intensified following multiple high-profile detections of neonicotinoid and pyrethroid residues in domestically grown produce, prompting major retailers to impose supplier standards that exceed the Ministry of Agriculture, Fisheries and Food (MAFF) maximum residue limits (MRLs). apan's positive list system, which sets a default MRL of 0.01 parts per million for unregistered pesticide-active ingredient combinations, creates a compliance minefield for exporters and domestic suppliers alike, driving demand for biopesticides that leave minimal detectable residues. The Food Safety Commission of Japan (FSCJ) applies safety factors up to 1,000 times when setting acceptable daily intakes (ADIs) for synthetic pesticides, a precautionary stance that raises the regulatory bar for chemical approvals and tilts the competitive playing field in favor of biological alternatives with inherently lower toxicity profiles. This consumer-driven pressure is amplified by social media campaigns that spotlight pesticide detections, creating reputational risks for growers and retailers that accelerate the shift toward biological crop protection solutions.

Government Subsidies for Integrated Pest Management

The 2024 Green Food System fund earmarked USD 200 million for integrated pest management adopters, with subsidy rates covering up to 50 percent of biopesticide input costs and 75 percent of precision application equipment investments for certified smallholders. These subsidies are geographically targeted, prioritizing Tohoku and Hokuriku rice-producing regions where aging farmer demographics and small plot sizes create structural barriers to technology adoption. Ministry of Agriculture, Fisheries and Food (MAFF) extension service network conducts over 5,000 annual training sessions on microbial application protocols, addressing the knowledge gap that has historically constrained biopesticide uptake among growers accustomed to synthetic chemistries with broader efficacy windows and simpler application requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited farmer awareness and technical know-how | -1.8% | Nationwide, most acute in Tohoku, Hokuriku, Shikoku | Short term (≤ 2 years) |

| Higher cost and scalability challenges versus synthetics | -1.5% | National, stark in low-margin rice and grain systems | Medium term (2–4 years) |

| Ultra-strict residue limits for microbial actives on exports | -0.9% | Shizuoka tea, Aomori apples, Kyushu citrus | Long term (≥ 4 years) |

| Dependence on imported patented microbial strains | -0.7% | All formulation segments | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Limited Farmer Awareness and Technical Know-How

Only 28% of Japanese smallholders have received training in microbial application protocols, a knowledge deficit that manifests in suboptimal timing, dosing errors, and inadequate storage practices that degrade biopesticide efficacy and erode grower confidence in biological solutions. The aging farmer demographic, with over 70% of operators older than 65 years, creates resistance to adopting new technologies that require modified spray schedules, specialized equipment, and real-time pest monitoring to achieve performance parity with synthetic chemistries. The technical complexity of matching biopesticide modes of action to specific pest life stages and environmental conditions requires a level of agronomic sophistication that many growers lack, creating a performance gap that undermines market expansion beyond early-adopter cohorts.

Higher Cost and Scalability Challenges Versus Synthetics

Biofungicides are priced at approximately 1.6 times the cost of synthetic equivalents per hectare, a cost premium that compresses profit margins in low-value crops such as rice and wheat, where growers operate on thin returns and prioritize input cost minimization over environmental performance. Organic production systems incur 1.35 to 1.6 times higher total costs compared to conventional farming, driven by elevated labor requirements for manual weeding, increased pest monitoring intensity, and yield penalties during the 3- to 5-year transition period before soil biology stabilizes [2]Source: Ministry of Agriculture, Forestry and Fisheries, “Green Food System Strategy,” maff.go.jp. The scalability challenge is most acute in extensive rice systems, where large treatment areas and narrow application windows favor synthetic pesticides that offer longer residual activity and simpler logistics, limiting biopesticide penetration to high-value crops where premium pricing justifies the incremental complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bioinsecticides Lead Amid Resistance Pressures

Bioinsecticides held a 37.40% share of the Japanese biopesticide market in 2025, reflecting their established efficacy against lepidopteran pests in rice, vegetables, and fruit crops, where pyrethroid resistance has eroded the performance of conventional chemistries. Bacillus thuringiensis formulations such as DiPel and Agree dominate this segment, leveraging MAFF registrations that span over 50 crop-pest combinations and distribution networks anchored by Sumitomo Chemical's agricultural cooperative partnerships. Spinosad products, derived from the soil bacterium Saccharopolyspora spinosa, captured a share in greenhouse vegetable systems where their translaminar activity and short pre-harvest intervals align with intensive cropping schedules and export residue requirements.

Biochemical biopesticides are advancing at a 14.95% CAGR toward 2031, this acceleration is driven by turf and ornamental grass managers who prioritize residue-free solutions that preserve aesthetic quality and minimize applicator exposure risks, particularly in high-traffic areas such as golf courses and urban parks. Pheromone-based mating disruption systems are gaining adoption in apple orchards in Aomori and pear orchards in Tottori, where they provide season-long control of codling moth and Oriental fruit moth without the spray frequency and resistance risks associated with insecticides.

By Application: Fruits and Vegetables Capture Premium Value

Fruits and vegetables commanded a 41.00% share of the Japan biopesticide market Size in 2025, driven by their high per-hectare value, intensive pest pressure, and exposure to strict export residue standards that favor biopesticides with minimal detectable residues. Greenhouse tomato and cucumber production in Kanto and Kansai regions exhibits the highest biopesticide adoption rates, reflecting controlled environments that reduce efficacy variability and justify premium input costs. Apple orchards in Aomori and citrus groves in Kyushu are transitioning to integrated pest management programs that incorporate pheromone mating disruption and Bacillus thuringiensis sprays, driven by export market access requirements and domestic consumer preferences for reduced-residue fruit.

Turf and ornamental grass applications are forecast to expand at a 13.55% CAGR through 2031, the fastest growth rate among application segments, driven by golf course managers and urban park operators who prioritize residue-free solutions that minimize applicator exposure and protect water quality in high-visibility settings. Japan's 2,300 golf courses, primarily located in Chiba, Hyogo, and Shizuoka prefectures, are adopting biological fungicides and insect growth regulators to manage turf diseases and pests while complying with municipal water quality regulations that restrict the use of synthetic pesticides near drinking water sources .

Geography Analysis

Kanto region dominates Japan's biopesticide market in 2025, driven by its concentration of greenhouse vegetable production, proximity to Tokyo's affluent consumer base, and dense network of agricultural research institutions that serve as early-adoption demonstration sites. The region's peri-urban vegetable belts in Chiba, Saitama, and Ibaraki prefectures supply fresh produce to metropolitan markets where retailers demand reduced-residue products, creating a direct line of sight between consumer preferences and grower input decisions. Kansai region, anchored by Osaka and Kyoto's vegetable production and Hyogo's fruit orchards, exhibits moderate growth as growers balance premium pricing opportunities against the higher input costs and technical complexity of biological pest management.

Hokkaido's potato, wheat, and dairy systems exhibit a more cautious adoption profile, constrained by shorter growing seasons that limit the window for slower-acting biopesticides to deliver economic returns, as well as the region's lower pest pressure compared to subtropical zones. The region's large-scale farm operations, which average over 20 hectares compared to the national average of 2 hectares, create opportunities for precision agriculture integration that could accelerate the adoption of biopesticides if manufacturers develop formulations optimized for Hokkaido's cool-temperate climate. The rice-dominated landscape of the Tohoku region is experiencing a gradual shift, driven by government subsidies for integrated pest management and by planthopper resistance that is eroding the efficacy of neonicotinoid seed treatments.

The Chubu region, spanning both industrial and agricultural zones, exhibits bifurcated adoption patterns, where Shizuoka's tea plantations and Nagano's fruit orchards lead in biopesticide use, while lowland rice systems lag due to cost sensitivity. Chugoku and Shikoku regions, characterized by mountainous terrain and aging farmer demographics, face structural barriers to adoption, including limited access to technical training and higher logistics costs for biopesticide distribution, yet pockets of organic production in these regions create niche demand for biological inputs that meet certification requirements.

Regulatory Landscape

Biopesticides in Japan are regulated as agricultural chemicals under the Agricultural Chemicals Regulation Act (Act No. 82 of 1948). Registration with the Minister of Agriculture, Forestry and Fisheries is required before manufacturing, processing, or import. The Food and Agricultural Materials Inspection Center (FAMIC) acts as the core technical body for application intake and dossier evaluation, covering efficacy, phytotoxicity, human and animal toxicity, and environmental residue data. Overseas applicants must appoint a Japan-resident custodian to manage registration and compliance.

The regulatory regime continues to change through guidance updates for biological categories. MAFF issued revised data requirement guidelines for microbial pesticides and natural enemy pesticides effective April 1, 2024, and FAMIC has continued publishing updated notifications and associated documents, including guideline document updates reflected in July 2026 materials. In parallel, MAFF finalized separate biostimulant labeling and handling guidelines in May 2025 after public consultation, which supports clearer boundary-setting between agricultural chemicals and other agricultural inputs that sit outside pesticide registration.

Competitive Landscape

The Japan biopesticides market exhibits a moderate concentration, with the top players, including Valent BioSciences LLC, Bayer CropScience AG, BASF SE, Koppert B.V., and UPL Limited are commanding a significant combined share in 2024, reflecting the dominance of multinational agrochemical firms that leverage global R&D pipelines, established distribution networks, and regulatory expertise to maintain market leadership. The competitive landscape is also shaped by intellectual property dynamics, where microbial strain patents create barriers to entry that favor established players with extensive patent portfolios, yet also create licensing opportunities for Japanese formulation companies seeking to access proprietary genetics.

Competitive strategies center on portfolio integration, where incumbents bundle biological and synthetic products to reduce grower complexity and defend their share against specialized biocontrol entrants, such as Koppert Biological Systems. This company has captured a significant market share by focusing on high-value greenhouse crops and the release of beneficial insects. Opportunities exist in rice systems, where biopesticide penetration remains less despite documented insecticide resistance, and in turf and ornamental applications, where residue-free positioning aligns with municipal procurement preferences for reduced environmental impact.

Emerging disruptors are leveraging digital agriculture platforms to enhance biopesticide efficacy and simplify application complexity, utilizing precision scouting tools and weather-based spray advisories that optimize timing and dosing for biological agents with narrower efficacy windows compared to synthetic chemistries. UPL's ProNutiva biological line and Certis Biologicals' expansion into foliar spray formulations signal a strategic pivot toward integrated chemical-biological offerings that improve field performance consistency and reduce the technical barriers that have historically constrained biopesticide adoption among mainstream growers.

Japan Biopesticide Industry Leaders

Valent BioSciences LLC

Bayer CropScience AG

BASF SE

Koppert B.V.

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Policy-driven integrated pest management creates room for microbial and natural enemy solutions that can replace or reduce conventional spray programs. MAFFs MIDORI Strategy anchors this shift with targets including a 10% reduction in chemical pesticide use by 2030 and a 50% reduction in risk-weighted chemical pesticide use by 2050, while the Green Food System Law supports adoption through IPM-linked subsidies that lower friction for smaller farms. With fruits and vegetables already the largest application segment by value (41.00% share in 2025), opportunities are most concentrated in export-linked supply chains and intensive greenhouse systems, where residue management and shorter pre-harvest intervals favor biopesticides.

A second opportunity area involves performance-consistent IPM packages that pair biologicals with scouting and timing discipline, addressing the efficacy variability and know-how restraints highlighted for growers. MAFF-backed field evidence for greenhouse tomatoes indicates that natural enemy-based biological control can reduce chemical pesticide spraying frequency by 62.5% and active ingredient counts by 75%, supporting broader commercialization of compatible biocontrol agents and application protocols. On the supply side, domestic capacity and localization also stand out as commercialization levers, reinforced by Sumitomo Chemicals investment to expand Bacillus thuringiensis fermentation output at its Oita facility. More broadly, multinational R&D pipelines increasingly target next-generation bioinsecticides for sap-sucking pests in high-value fruit and vegetable crops.

Recent Industry Developments

- June 2026: Bayer and Aphea.Bio announced a strategic research partnership to develop a new generation of bioinsecticides targeting sap-sucking pests such as aphids and thrips for use across crops including pome and stone fruits, citrus, and grapes. The collaboration strengthens pipelines aimed at resistance-management needs in high-value horticulture, where residue constraints and IPM practices support biological uptake.

- May 2026: Kumiai Chemical and Bayer CropScience entered a new sales agreement to transfer distribution rights for 12 Bayer agrochemical products to Kumiai, with commercial sales under the new arrangement scheduled to begin on December 1, 2026. The portfolio realignment reinforces the role of Japanese distributors in shaping go-to-market execution and stewardship, which can influence how growers adopt integrated chemical-biological programs.

- March 2025: BASF expanded its Serifel biofungicide registration in Japan to include additional greenhouse vegetable crops, with MAFF approval for use on eggplant and bell peppers. The label expansion widens addressable acreage in Kantos intensive protected-cropping systems, where growers prioritize residue management for domestic retail standards and export channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of biopesticide products sold for crop protection use in Japan, including microbial, botanical, and beneficial organism based solutions that are applied to control pests and diseases in crops.

Scope exclusions: We exclude synthetic chemical pesticides and non-crop pest control uses such as household, structural, and public health applications.

Segmentation Overview

- By Product Type

- Bioherbicides

- Bioinsecticides

- Biofungicides

- Others

- By Application

- Food Crop

- Grains and cereals

- Oilseeds

- Fruits and vegetables

- Non-food Crop

- Turf and ornamental grass

- Others

- Food Crop

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the Japan crop protection context and then narrowing it to biopesticides, so the model sits on traceable and public reference points. We typically review official sources such as Japan MAFF releases, FAOSTAT crop and area series, OECD agri statistics, and UN Comtrade trade codes to understand crop mix, planted area shifts, and import patterns that can affect product demand.

To translate those signals into realistic market values, we also use sources like peer reviewed agronomy journals, pesticide registration and active ingredient listings from relevant regulators, and association publications that describe adoption drivers and constraints. Company annual reports, investor presentations, and credible press are used to sense-check product launches, channel structure, and pricing direction. Where needed, a paid subscription database is referenced for company financials, patent activity, and import-export shipment views at a high level. These desk research sources are illustrative, and we also checked other public materials to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary discussions are used to convert the desk view into Japan-specific buying reality, especially around which crops are actively using biopesticides and how often applications happen across the season. We spoke with a mix of manufacturers, formulators, distributors, advisors, and large farm or grower-cooperative stakeholders across Japan to validate penetration, pricing bands, and near-term demand drivers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 17% | APAC: 38% |

| Mid tier: 43% | Functional/Unit leaders: 34% | EMEA: 37% |

| Smaller Players: 20% | Managers: 49% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build using Japan crop area and cropping intensity, which are then mapped to typical biopesticide treatment patterns by crop type and pest pressure. From there, value is reconstructed using a practical set of inputs, such as hectares under key food crops, frequency of spray or application per season, share of acreage using biological solutions, and average price per hectare by product category.

We then run selective bottom-up checks so the totals do not drift away from what suppliers and channels can reasonably deliver. These checks include sampled price quotes from distributors, a roll-up of observable supplier revenues tied to Japan crop protection portfolios, and channel feedback on mix shifts between microbial and botanical solutions. For forecasting, we use scenario analysis supported by expert views, where adoption rate, regulatory acceptance of biological actives, and crop profitability are adjusted together. Where product-level details are limited, gaps are handled through conservative mix assumptions that we re-test in interviews.

Data Validation & Update Cycle

Outputs are validated through multiple passes so one unusual input does not set the market total. We compare the modeled values against independent signals such as crop protection spending direction, changes in registered biological products, and trade or supply cues that suggest constraints or surges, and then review outliers before sign-off.

If a major variance is found, the assumptions behind application rate, penetration, or pricing are revisited, and follow-up calls are triggered with the most relevant respondents. Reports are refreshed annually, and interim updates are made when material events occur, such as regulation changes or abrupt demand shocks. Before delivery, an analyst performs a final update sweep so clients receive the latest view aligned to the base year and forecast frame.

Mordor Intelligence's Japanese Biopesticides Market Estimate Compared With Other Published Estimates

Published market sizes for Japan biopesticides can look far apart, even when the growth story sounds similar, because each publisher draws the market box in a different way and then applies different pricing and adoption assumptions. Differences also come from base year choice, currency timing, and how quickly estimates are refreshed after new registrations or demand shifts.

Some published figures fold biopesticides into a wider bio-based crop input bucket, or they include non-crop pest control uses that inflate the spending pool. In Mordor Intelligence sizing, only biopesticide products used for crop protection in Japan are counted, and the value is anchored to crop-area driven demand with interview-validated application rates and price per hectare ranges.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 185.00 M (2025) | |

| Global Consultancy A | USD 300.00 M (2024) | Uses a different base year and tends to apply higher average pricing without making the crop-area and application rate logic transparent, which can push the value up when adoption is still uneven by crop. |

| Trade Journal B | USD 242.00 M (2025) | Often blends broader biological crop input spending and relies on simplified growth curves, which can overstate demand if non-food crop uses or adjacent bio-solutions are included. |

The spread across sources is mainly explained by what gets included around the core biopesticide definition and by how price and adoption are carried forward year to year. By tying the estimate to observable crop and usage drivers, and then checking those assumptions with local channel feedback, the final number stays easier to audit and repeat when the market is updated.

Key Questions Answered in the Report

What is the current value of the Japan biopesticides market?

The market is valued at USD 211.05 million in 2026 and is projected to reach USD 408.13 million by 2031.

What is the market's expected growth rate?

It is projected to expand at a 14.08% CAGR through 2031.

Which segment holds the largest share?

Bioinsecticides lead with a 37.40% share, driven by the need for control of pyrethroid-resistant pests.

Who are the top market players?

Valent Biosciences, Bayer Crop Science, BASF, Koppert Biological Systems, and UPL are the leading companies in current sales.

Page last updated on: