B2B Enterprise And Industrial Wearables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

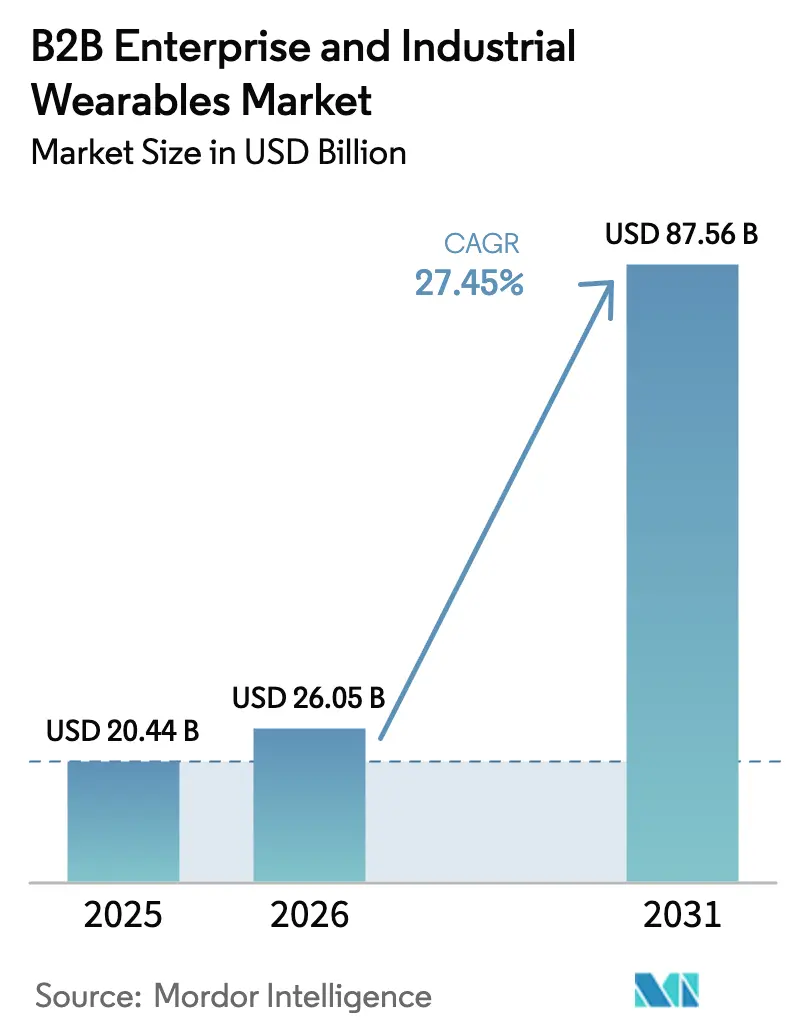

| Market Size (2026) | USD 26.05 Billion |

| Market Size (2031) | USD 87.56 Billion |

| Growth Rate (2026 - 2031) | 27.45% CAGR |

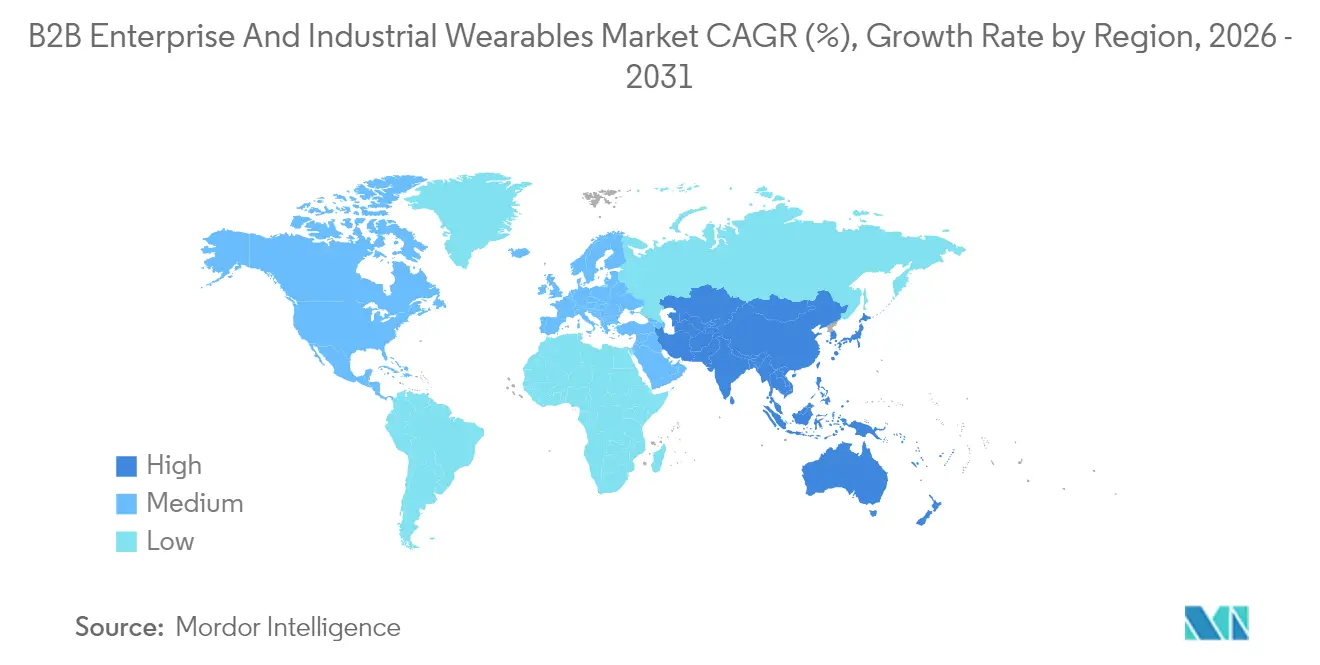

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

B2B Enterprise And Industrial Wearables Market Analysis by Mordor Intelligence

The B2B enterprise and industrial wearables market size was valued at USD 20.44 billion in 2025 and estimated to grow from USD 26.05 billion in 2026 to reach USD 87.56 billion by 2031, at a CAGR of 27.45% during the forecast period (2026-2031). The continued migration of compute power toward the edge, regulatory pressure for real-time worker safety, and private 5G rollouts are the primary catalysts driving this expansion. Industrial buyers now place greater emphasis on deterministic latency, data sovereignty, and battery-efficient AI inference than on headline display specifications. Early deployments in manufacturing, logistics, and healthcare are providing proof points that shorten purchase cycles, even as labor unions demand privacy controls that keep biometric data local. Component advances, such as 15 TOPS edge AI chipsets operating under 5 watts, are enabling all-day smart glasses and sensor-rich safety vests that occupants forget they are wearing. As software ecosystems mature, enterprises can deploy out-of-the-box AR workflows that integrate with ERP and CMMS platforms in weeks rather than quarters. Together, these forces push the B2B enterprise and industrial wearables market toward mainstream procurement budgets rather than discretionary innovation funds.

Key Report Takeaways

- By device type, smart glass led with a 31.02% revenue share in 2025, while smart clothing and body sensors are projected to post a 28.74% CAGR through 2031.

- By end-user industry, manufacturing held 27.95% of the 2025 base, whereas healthcare is forecast to expand at a 29.86% CAGR to 2031.

- By component, sensors accounted for 34.35% of 2025 revenue, and the segment is expected to grow at a 29.05% CAGR over the forecast period.

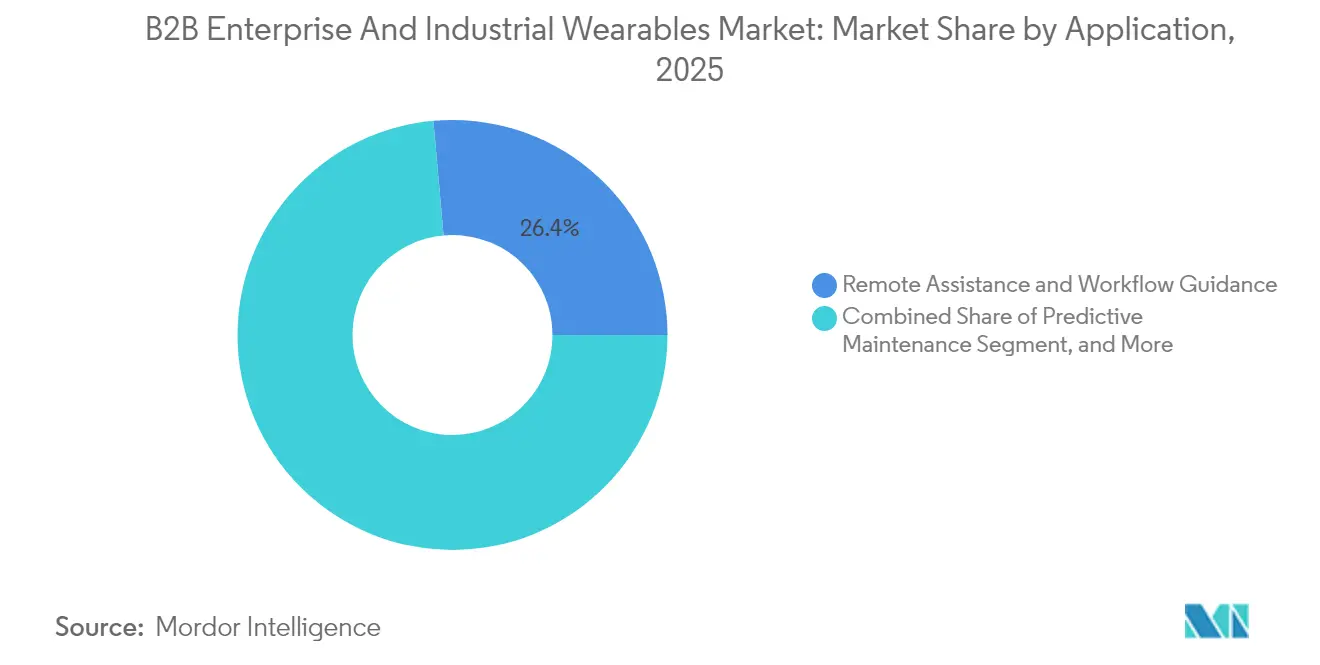

- By application, remote assistance and workflow guidance captured 26.42% of 2025 revenue, while predictive maintenance is anticipated to rise at a 30.10% CAGR through 2031.

- By connectivity technology, Bluetooth and BLE contributed 42.10% of 2025 revenue, with 5G and 5G RedCap projected to advance at a 30.25% CAGR.

- By geography, North America commanded a 39.65% share in 2025, whereas Asia-Pacific is set to post a 30.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global B2B Enterprise And Industrial Wearables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing App Ecosystem Fuels Enterprise Adoption | +4.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Demand for Smart Factory Set-Ups | +5.2% | Asia-Pacific core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Rapid Gains in 5G Stand-Alone and Private Networks | +4.5% | North America and Europe early, Asia-Pacific scaling | Medium term (2-4 years) |

| Edge AI Chips Reduce Latency and Power Budget | +3.9% | Global | Short term (≤ 2 years) |

| Regulatory Push for Workforce Safety Compliance | +3.6% | North America and Europe, emerging in Middle East | Short term (≤ 2 years) |

| Mainstreaming of Digital Twins in Heavy Industry | +3.4% | Global, with early gains in Germany, United States, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing App Ecosystem Fuels Enterprise Adoption

Enterprises increasingly judge wearables by how well the software stack integrates with existing ERP, MES, and CMMS workflows, rather than by display resolution or battery longevity. PTC’s Vuforia Studio now ships with over 200 modular AR workflows that can be deployed without custom code, shrinking pilot phases from months to weeks. Siemens’ Industrial Edge Marketplace extends similar plug-and-play logic to manufacturing execution environments, allowing plants to run the same workflow in parallel lines with minimal IT investment. At Boeing, AR guidance reduced wiring-harness assembly time by 25% and errors by 90%, providing the ROI clarity that finance groups require before funding fleetwide rollouts. [1]The Boeing Company, “AR-Guided Assembly Reduces Production Time,” boeing.com This pivot from bespoke development to API-first modules lowers switching costs, accelerates user onboarding, and solidifies the B2B enterprise and industrial wearables market as a line item in formal capital budgets, rather than an R&D curiosity.

Demand for Smart Factory Set-Ups

National programs such as China’s Made in China 2025 and India’s Production-Linked Incentive schemes earmark billions for automated production lines that rely on wearable-equipped technicians for exception handling and quality inspection. BMW’s Regensburg logistics team reported a 15% reduction in picking errors after smart-glass deployment, while Bosch feeds wearable sensor streams into its ConnectedWorld IoT platform to trigger predictive maintenance work orders. These use cases validate the thesis that wearables serve as the human-machine interface of Industry 4.0, linking physical assets to digital twins that simulate process changes before plant managers pull the trigger. As factories become data factories, demand for head-mounted displays, smart gloves, and biometric vests scales in lockstep.

Rapid Gains in 5G Stand-Alone and Private Networks

Ericsson cites sub-10 ms latency and four-nines uplink reliability in private 5G proofs of concept for automotive paint shops and chemical refineries. GSMA Intelligence reported a 40% increase in private 5G installations in 2024, with manufacturing and logistics accounting for 60% of that growth. [2]GSMA, “Private Network Deployments Grow 40% in 2024,” gsma.comUnlike Wi-Fi, which struggles with RF interference in metal-dense halls, 5G RedCap offers deterministic performance at lower BOM costs, making it viable for sensor-rich wearables. Network slicing enables safety alerts to preempt video traffic, thereby satisfying OSHA mandates for real-time arc-flash detection. [3]U.S. Occupational Safety and Health Administration, “Updated Electrical Safety Standards,” osha.govThe result is a connectivity backbone that elevates the B2B enterprise and industrial wearables market from pilot-scale to plant-wide roll-outs.

Edge AI Chips Reduce Latency and Power Budget

Qualcomm’s QCS6490 delivers 15 TOPS at under 5 watts, allowing smart glasses to execute computer-vision models on device and still last an entire shift. Bosch Sensortec’s BHI385 enables AI inference directly within the sensor hub, filtering out noise locally and transmitting only actionable events. On-premises processing sidesteps GDPR restrictions that complicate uploading biometric data to cloud endpoints. Lower latency and longer battery life translate into greater user satisfaction, addressing the wear fatigue complaints that doomed prior generation trials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Business-Grade Applications | -3.2% | Global | Medium term (2-4 years) |

| Data Security and Legacy IT Integration Issues | -2.8% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| High Up-Front TCO and Uncertain ROI | -2.5% | Global | Short term (≤ 2 years) |

| Worker Privacy and Wear Fatigue Concerns | -1.9% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Business-Grade Applications

Many AR and workflow guidance suites remain pilot-grade, lacking essential features such as ISO 9001 audit trails, role-based access controls, or FDA 510(k) validations required for continuous vital-sign telemetry. Hospitals are often forced to rely on consumer-grade wearables that do not meet EHR interoperability requirements, leaving clinical staff to manually reconcile data. Fragmentation across Android, proprietary RTOS, and iOS platforms obliges IT to maintain parallel code bases, inflating ownership costs. EU-OSHA has warned that opaque data flows heighten psychosocial risks, a red flag for worker councils. Until software catches up with enterprise governance standards, adoption will lag hardware readiness.

Data Security and Legacy IT Integration Issues

CISA’s 2024 advisory cataloged multiple CVE vulnerabilities tied to wearable gateways in industrial control systems. The FDA now requires a software bill of materials for connected medical devices, adding months to product certification cycles. In brownfield factories, SCADA stacks predating Ethernet struggle to ingest wearable data, forcing middleware hacks that undermine reliability. The GDPR and the forthcoming EU AI Act necessitate data localization, which undermines cloud-centric architectures. Combined, these frictions slow procurement and temper the otherwise meteoric growth of the B2B enterprise and industrial wearables market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type – Smart Glass Dominates as Smart Clothing Surges

Smart glass delivered 31.02% of 2025 revenue, underscoring its maturity in hands-free inspection and remote expert workflows. RealWear and Vuzix units meet IP67 ingress ratings and pair voice control with high-brightness micro-OLED optics, letting automotive line workers navigate manuals without removing gloves. The B2B enterprise and industrial wearables market size for smart glass is projected to expand at a healthy clip as next-generation optics lighten form factors and extend field of view. Yet, smart clothing and body sensors are poised for a 28.74% CAGR, reflecting regulatory moves to monitor heat stress and hazardous gas exposure in real-time. Honeywell’s biometric safety vest, which embeds PPG, accelerometer, and CO2 sensors, fulfills OSHA heat illness prevention guidance without adding bulky gear, positioning textile-integrated wearables as the breakout form factor of the decade.

The widening adoption spectrum now includes wrist wear for two-factor authentication and notification pings, HMDs for VR training in confined-space rescue, and wearable cameras for capturing law enforcement evidence. Sony’s 4K, 1-inch micro-OLED display enables glasses that resemble prescription frames yet deliver industrial brightness, erasing the cultural stigma once associated with head-mounted computers. Pancake optics and waveguide patents promise further weight reductions, translating to full-shift comfort and accelerating replacement of rugged tablets in maintenance work orders.

By End-User Industry – Manufacturing Leads, Healthcare Accelerates

Manufacturing accounted for 27.95% of the 2025 spend, primarily driven by predictive maintenance and assembly guidance. The B2B enterprise and industrial wearables market share for the sector stems from high labor costs and strict defect-per-million targets that justify automation outlays. BMW and Bosch demonstrate that reducing rework yields immediate payback, even before accounting for fewer safety incidents. Healthcare is the fastest-growing sector, with a 29.86% CAGR, as the Centers for Medicare and Medicaid Services reimburse remote patient monitoring codes and the FDA clears clinical-grade biosensors. Continuous telemetry reduces hospital stays, allowing providers to shift risk in value-based contracts.

IT and telecom field crews utilize AR overlays to reduce truck rolls and first-time-fix errors, while retail warehouses deploy glove scanners to shave seconds off of pick cycles. Transportation fleets issue smart watches that double as driver safety monitors, collecting heart-rate variability alongside telematics to predict fatigue. Utilities and oil and gas firms equip inspectors with ATEX-certified smart glasses, replacing paper logs with voice-captured inspection records.

By Component – Sensors Anchor Value, Software Shapes Differentiation

Sensors captured 34.35% of the 2025 value and continue to be the backbone of data collection. Multi-modal IMUs, PPGs, and environmental detectors are embedded in a single flex board, reducing BOM and calibration costs. Artificial intelligence embedded in sensor hubs means fewer data packets traverse congested networks, easing compliance with data minimization rules. The B2B enterprise and industrial wearables market size for sensors is projected to grow at a 29.05% CAGR as integrated packages replace discrete parts.

Displays and optics chase weight and brightness targets, while processor roadmaps push 45 TOPS per watt by mid-forecast, unlocking on-device natural language processing for voice-only UIs. Connectivity modules must juggle Bluetooth, Wi-Fi 7, and 5G RedCap in a postage-stamp footprint. Ultimately, software and services dictate stickiness: ThingWorx and MindSphere ecosystems provide drag-and-drop dashboards that convert raw sensor streams into KPI alerts, reinforcing the shift from hardware sales to recurring SaaS revenue.

By Application – Remote Assistance Dominates, Predictive Maintenance Surges

Remote assistance and workflow guidance delivered 26.42% of 2025 revenue. Field engineers wearing smart glasses stream high-definition video to HQ experts, who overlay AR annotations, eliminating the need for costly second visits. In a complex wiring harness assembly, this approach reduced errors by 90% at Boeing, demonstrating its economic benefits. Predictive maintenance is racing ahead with a 30.10% CAGR, as vibration and thermal anomalies captured by wearables feed asset-health algorithms. The B2B enterprise and industrial wearables market size is tied to the benefits of predictive maintenance, which can lead to deferred capital spending on replacement equipment.

Training and simulation see growing VR adoption for confined-space entry drills, while worker health monitoring extends beyond pulse checks to include gas exposure thresholds and posture analytics. Inventory management leverages glove-integrated RFID to automate stock counts, and quality inspection workflows pair computer vision with voice tags to archive audit trails for ISO compliance.

By Connectivity Technology – Bluetooth Leads, 5G Gains Momentum

Bluetooth and BLE secured 42.10% of 2025 revenue, thriving on the ubiquity of smartphones and sub-100 mW power draws. Wi-Fi 6E fills high-bandwidth indoor tasks, and Wi-Fi 7 targets sub-5 ms latency. 4G LTE remains indispensable for field crews beyond factory fences, though LTE-M and NB-IoT serve low-throughput sensors.

Private 5G and 5G RedCap, however, are forecast to leap forward at a 30.25% CAGR as enterprises seek deterministic latency for safety alerts and real-time video. Ultra-wideband offers centimeter-level positioning, enabling collision-avoidance systems for forklifts inside warehouses once plagued by blind corners.

Geography Analysis

North America generated 39.65% of 2025 revenue. Stringent OSHA standards and early adoption of AR by logistics behemoths laid the groundwork for widespread uptake. U.S. aerospace, automotive, and oil majors continue to layer wearables on top of digital-twin roadmaps, driving the B2B enterprise and industrial wearables market toward established annual budgets. Canada utilizes rugged smart glass in remote mining and forestry operations, where fly-in-fly-out crews require off-grid diagnostics. Mexico’s maquiladora plants adopt wearables to satisfy zero-defect mandates from North American OEMs.

Asia-Pacific is poised for a 30.90% CAGR through 2031. Beijing’s Made in China 2025 agenda finances automated factories in the Yangtze River Delta, embedding wearable feeds into real-time MES dashboards. India’s Production-Linked Incentive outlays fund smart clothing pilots for the pharmaceutical and automotive sectors, addressing labor-skill gaps. Japan’s Society 5.0 vision positions wearables as the interface between an aging workforce and robotic co-workers, with smart exoskeletons and biometric sleeves helping to ease musculoskeletal strain. South Korea’s semiconductor fabs deploy UWB-enabled badges to enforce cleanroom zoning, while Australia’s mines adopt fatigue-detection vests to mitigate accident risks.

Europe shows robust yet regulated growth. Germany leverages Industrie 4.0 subsidies and CE-marking expertise to export turnkey wearable-enabled production lines. GDPR compels on-premises inference, putting the spotlight on edge AI chipmakers. France and Italy face slower roll-outs as worker councils debate surveillance optics, though automotive clusters in Turin and Modena pilot smart glasses for torque-wrench calibration. The United Kingdom’s divergent post-Brexit standards add compliance complexity but also open fast-track routes for innovative suppliers. Elsewhere, the Middle East invests in smart-city megaprojects that include wearable safety mandates on construction sites, while South America pilots edge-AI-enabled wearables in Brazil’s open-pit mines.

Competitive Landscape

Competition remains moderately fragmented. Platform incumbents such as Meta, Microsoft, and Apple utilize existing collaboration suites and digital twin backends to secure accounts. RealWear, Vuzix, and ProGlove carve out niches with ATEX-rated smart glasses and glove scanners that withstand dust and vibration.

Patent runs highlight strategic moats: Sony owns micro-OLED roadmaps, Kopin holds waveguide optics, and Qualcomm bundles 5G RedCap with 45 TOPS AI compute in a single SoC. Bosch Sensortec’s sensor-hub-with-AI models consolidate IMU, PPG, and gas detection on one die, attracting OEMs that want to shrink PCBs and extend battery life.

End-to-end software integration trumps raw hardware specs. Meta’s Quest platform pre-loads Zoom and Teams connectors, minimizing IT effort. Microsoft ships Azure Digital Twin APIs that feed directly into Dynamics maintenance tickets. Apple courts field technicians by merging Vision Pro spatial menus with SAP and Salesforce extensions, prioritizing usability over warehouse-grade ruggedness. Regulatory hurdles favor large players: Honeywell’s FDA 510(k) clearance for biometric vests and RealWear’s ATEX/IECEx certifications erect barriers that newcomers struggle to cross.

B2B Enterprise And Industrial Wearables Industry Leaders

Alphabet Inc.

Samsung Electronics Co. Ltd.

Sony Corporation

HTC Corporation

Apple Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Meta Platforms partnered with Accenture and PwC to deploy Quest 3 headsets for enterprise training, bundling Microsoft Teams and Zoom integrations out of the box.

- January 2025: Apple expanded Vision Pro enterprise programs alongside SAP and Salesforce connectors, targeting utilities and field maintenance technicians.

- November 2024: RealWear introduced the Navigator Z1, an ATEX-certified smart glass with thermal imaging and UWB positioning for oil and gas sites.

- October 2024: Qualcomm unveiled the QCS8550G processor, combining 45 TOPS AI performance with an embedded 5G RedCap modem and Wi-Fi 7 radio.

Global B2B Enterprise And Industrial Wearables Market Report Scope

Wearable technology consists of devices that utilize wearable sensors to track data related to self-monitoring, personal responsibility, and creating awareness about the operating environment of an employee. Industrial wearable devices are designed to enhance workplace productivity, safety, and efficiency in sectors such as manufacturing, logistics, and mining. These devices collect data in real-time, track activities, provide alerts, and offer customized experiences tailored to the needs of users and organizational objectives. They are designed for specific situations or industry verticals, as opposed to consumer wearables, which are often general in function.

The B2B Enterprise and Industrial Wearables Market Report is Segmented by Device Type (HMDs, Wrist Wears, Smart Glass, Smart Clothing and Body Sensors, Wearable Cameras, Other Device Types), End-User Industry (IT and Telecom, Healthcare, Retail and E-Commerce, Insurance and Financial Services, Manufacturing, Transportation and Logistics, Other End-User Industries), Component (Sensors, Displays and Optics, Processors and Memory, Connectivity Modules, Power and Battery, Software and Services), Application (Remote Assistance and Workflow Guidance, Worker Safety and Health Monitoring, Training and Simulation, Predictive Maintenance, Inventory and Asset Management, Quality Inspection and Documentation), Connectivity Technology (Bluetooth/BLE, Wi-Fi/Wi-Fi 6/6E, 4G LTE/LTE-M/NB-IoT, 5G and 5G RedCap, UWB and Short-Range RF), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| HMDs |

| Wrist Wears |

| Smart Glass |

| Smart Clothing and Body Sensors |

| Wearable Cameras |

| Other Device Types |

| IT and Telecom |

| Healthcare |

| Retail and E-Commerce |

| Insurance and Financial Services |

| Manufacturing |

| Transportation and Logistics |

| Other End-User Industries |

| Sensors |

| Displays and Optics |

| Processors and Memory |

| Connectivity Modules |

| Power and Battery |

| Software and Services |

| Remote Assistance and Workflow Guidance |

| Worker Safety and Health Monitoring |

| Training and Simulation |

| Predictive Maintenance |

| Inventory and Asset Management |

| Quality Inspection and Documentation |

| Bluetooth / BLE |

| Wi-Fi / Wi-Fi 6 / 6E |

| 4G LTE / LTE-M / NB-IoT |

| 5G and 5G RedCap |

| UWB and Short-Range RF |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Device Type | HMDs | ||

| Wrist Wears | |||

| Smart Glass | |||

| Smart Clothing and Body Sensors | |||

| Wearable Cameras | |||

| Other Device Types | |||

| By End-User Industry | IT and Telecom | ||

| Healthcare | |||

| Retail and E-Commerce | |||

| Insurance and Financial Services | |||

| Manufacturing | |||

| Transportation and Logistics | |||

| Other End-User Industries | |||

| By Component | Sensors | ||

| Displays and Optics | |||

| Processors and Memory | |||

| Connectivity Modules | |||

| Power and Battery | |||

| Software and Services | |||

| By Application | Remote Assistance and Workflow Guidance | ||

| Worker Safety and Health Monitoring | |||

| Training and Simulation | |||

| Predictive Maintenance | |||

| Inventory and Asset Management | |||

| Quality Inspection and Documentation | |||

| By Connectivity Technology | Bluetooth / BLE | ||

| Wi-Fi / Wi-Fi 6 / 6E | |||

| 4G LTE / LTE-M / NB-IoT | |||

| 5G and 5G RedCap | |||

| UWB and Short-Range RF | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is spending on enterprise wearables growing in manufacturing?

Manufacturing spend in the B2B enterprise and industrial wearables market is growing alongside a 27.45% overall CAGR and held 27.95% share of 2025 revenue.

Which connectivity option is gaining the most momentum for industrial wearables?

Private 5G and 5G RedCap connections are the fastest-growing, projected at a 30.25% CAGR through 2031 on the back of deterministic latency and reliability.

Why are smart clothing and body sensors attracting fresh investment?

Regulatory pressure for real-time worker safety monitoring and advancements in washable textile-integrated sensors support a 28.74% CAGR for smart clothing and body sensors.

What is the biggest adoption barrier for enterprise AR devices?

The lack of business-grade applications with enterprise security certifications and deep ERP integration remains the leading bottleneck.

How does edge AI improve wearable performance?

Chipsets delivering up to 15 TOPS under 5 watts enable on-device inference, cutting latency and complying with data-localization rules without sacrificing battery life.

Page last updated on: