Wearable Computing Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 95.40 Billion |

| Market Size (2031) | USD 201.92 Billion |

| Growth Rate (2026 - 2031) | 16.18% CAGR |

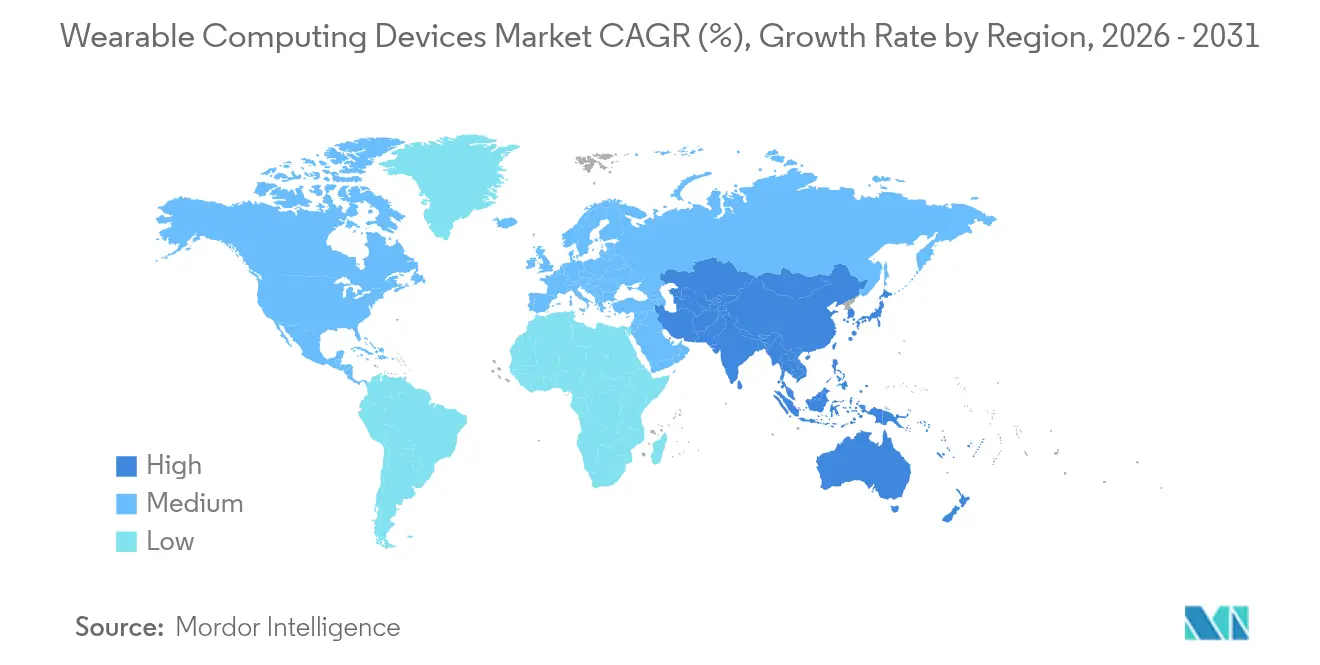

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

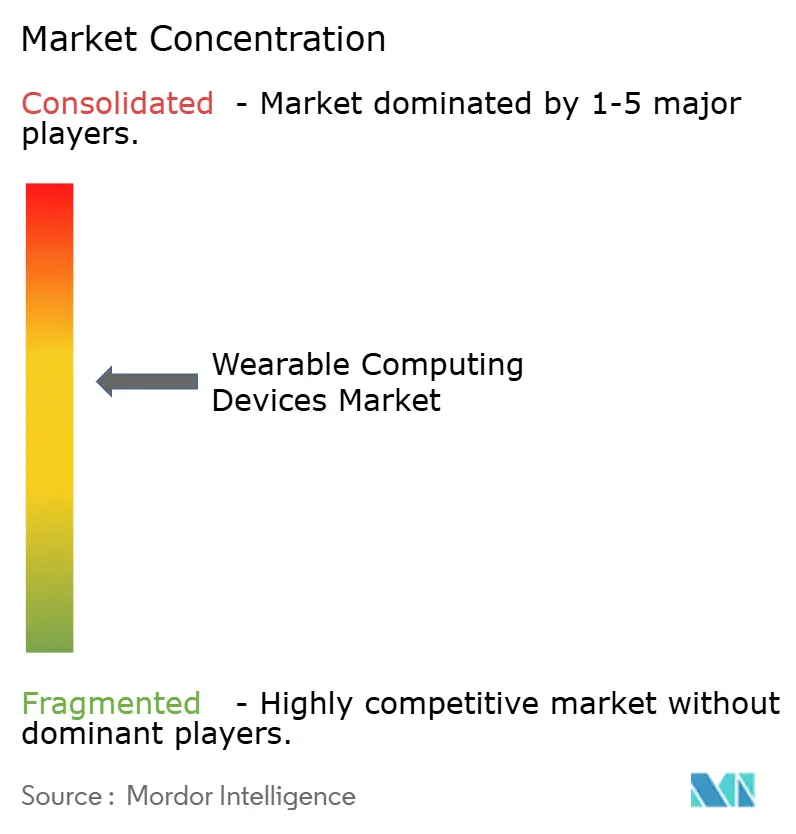

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wearable Computing Devices Market Analysis by Mordor Intelligence

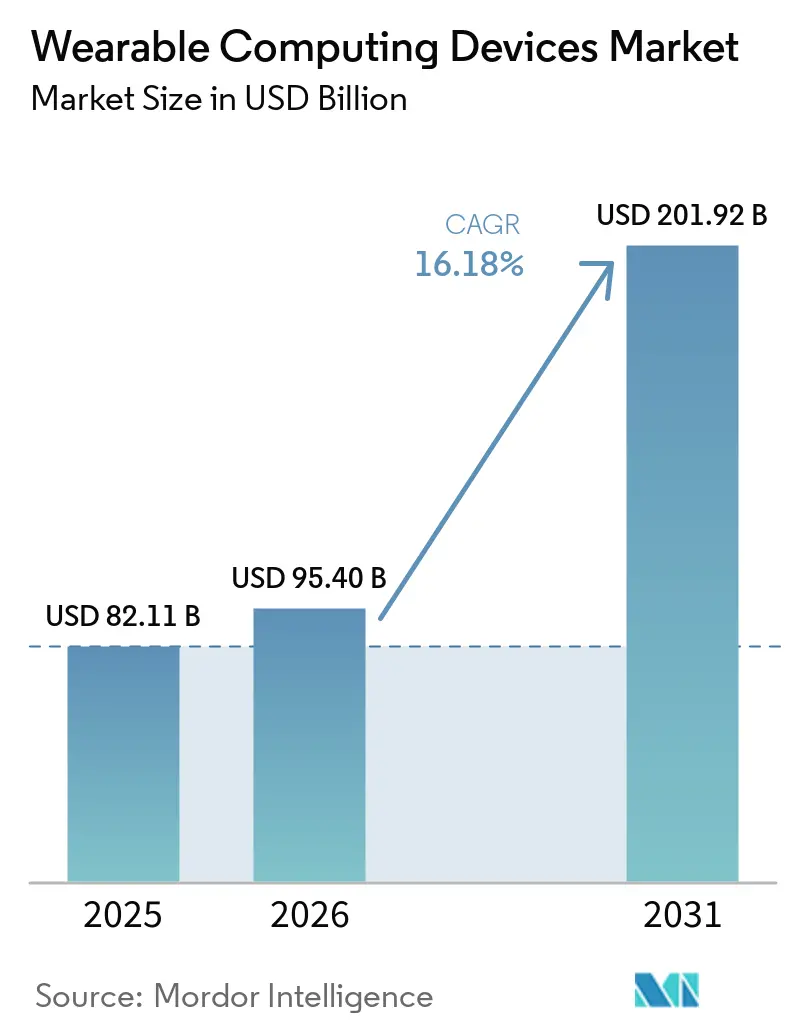

Wearable Computing Devices Market size in 2026 is estimated at USD 95.4 billion, growing from 2025 value of USD 82.11 billion with 2031 projections showing USD 201.92 billion, growing at 16.18% CAGR over 2026-2031.

Sensor miniaturization breakthroughs, battery-efficient chipsets, and closer integration with smartphone ecosystems are widening both consumer and enterprise appeal. Non-invasive metabolic monitoring and FDA alignment with ISO 13485:2016 are improving the regulatory path for medical-grade products, while precise location capabilities built on ultra-wideband are expanding industrial safety use cases. Supply-chain resilience, especially around micro-LED components, remains a strategic requirement, and privacy-focused design is moving to the foreground as data sharing rules tighten. Collectively, these factors keep competitive pressure high and encourage ecosystem-centric strategies that blend hardware, software, and health-service subscriptions.

Key Report Takeaways

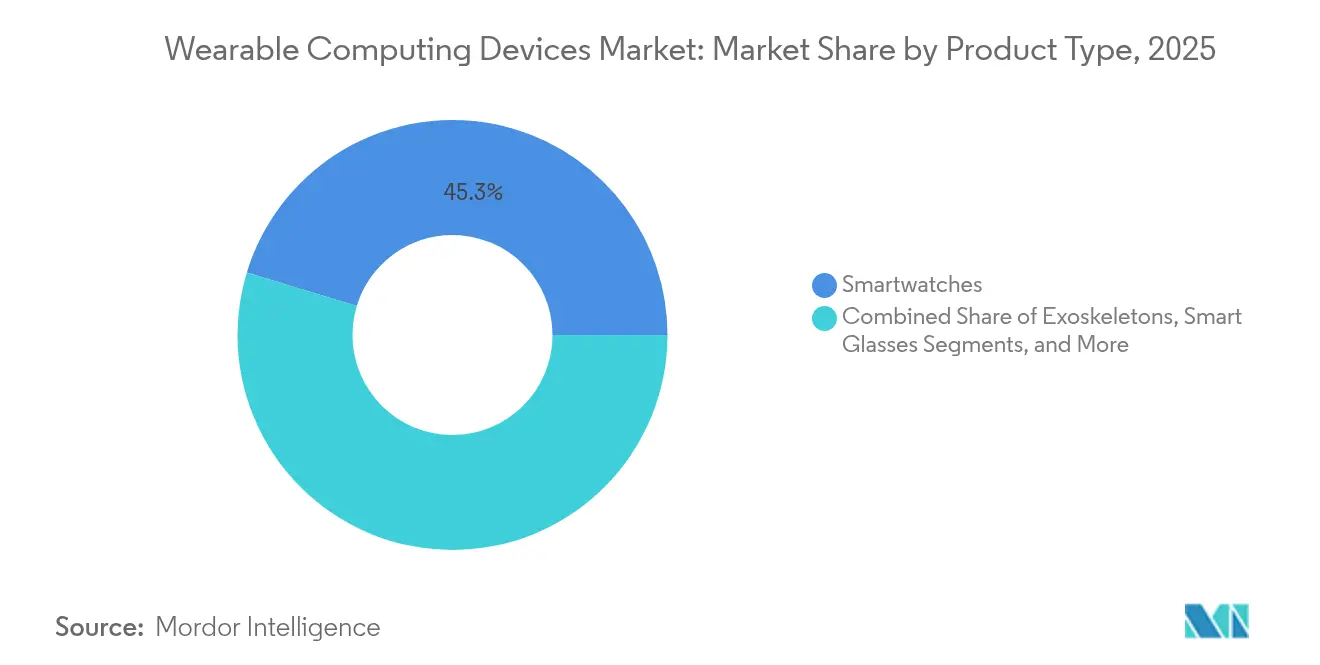

- By product type, smartwatches led with 45.30% of wearable computing devices market share in 2025, while ear-worn devices are forecast to expand at an 18.02% CAGR through 2031.

- By end user, the fitness and wellness segment accounted for 38.40% share of the wearable computing devices market size in 2025, whereas medical and healthcare applications are advancing at a 18.7% CAGR to 2031.

- By operating system, watchOS commanded 38.55% revenue share in 2025, while HarmonyOS records the highest projected CAGR at 16.6% through 2031.

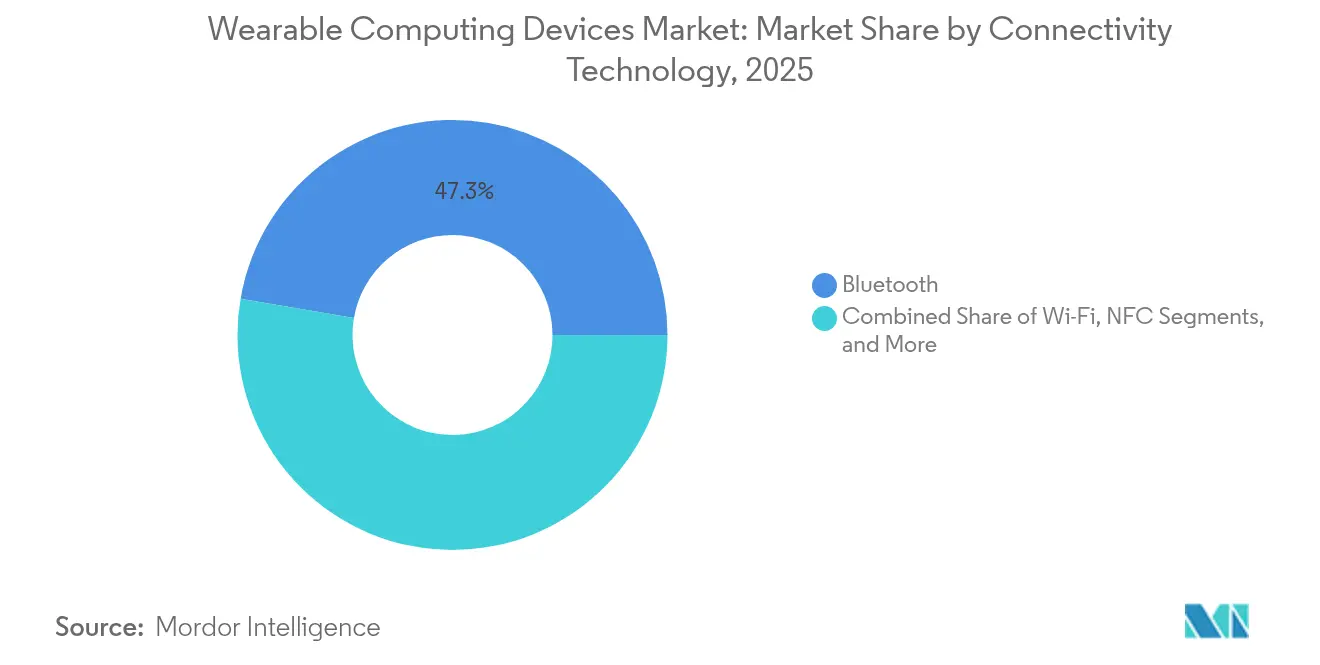

- By connectivity technology, Bluetooth held 47.30% of the wearable computing devices market share in 2025, while ultra-wideband is projected to grow at a 19.2% CAGR through 2031.

- By geography, North America retained a 34.10% share of the wearable computing devices market in 2025, whereas Asia Pacific is projected to grow at a 16.25% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wearable Computing Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sensor miniaturization and battery-efficient chipsets | +3.2% | Taiwan and South Korea semiconductor hubs lead; global benefit | Medium term (2-4 years) |

| Rising consumer health-monitoring culture | +2.8% | North America and EU lead; APAC demand accelerates | Short term (≤ 2 years) |

| Smartphone-ecosystem integration and super-apps | +2.1% | China and India mobile-first markets show stronger influence | Medium term (2-4 years) |

| Insurance tele-wellness incentives | +1.9% | North America primary; EU emerging | Long term (≥ 4 years) |

| Hands-free AR wearables for frontline workforce safety | +1.4% | Industrial regions: Germany, Japan, US manufacturing corridors | Long term (≥ 4 years) |

| Breakthrough non-invasive metabolic monitoring | +2.3% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sensor Miniaturization and Battery-Efficient Chipsets

Solid-state batteries from TDK achieve 1,000 Wh/l energy density, cutting size while extending run-time for hearables and watches.[2]TDK Corporation, “TDK Develops Next-Generation Solid-State Battery for Wearables,” global.tdk.com Chip packaging advances allow multiple sensors on one substrate, and Apple patents show dynamic power and thermal adjustment based on user context, boosting efficiency without thicker casings. Aqueous ammonium-ion micro batteries developed at Tsinghua University demonstrate safer and flexible chemistry suitable for skin-contact devices. These leaps enable always-on health metrics plus vivid micro-LED displays that draw minimal power. The outcome is a broader acceptance of continuous monitoring in everyday accessories.

Rising Consumer Health-Monitoring Culture

Wearables increasingly detect clinical-grade events, highlighted when a consumer's watch flagged cardiac abnormalities later diagnosed as takotsubo cardiomyopathy. Galaxy AI now delivers “Energy Score” insights that contextualize sleep, stress, and activity for personal coaching.[3]Samsung Electronics, “Galaxy AI Delivers New Energy Score,” news.samsung.com In-sensor computing prototypes from the University of Hong Kong process bio-signals locally, lowering latency and reducing exposure of sensitive data online. Evidence from the MOTIVATE-T2D study shows enhanced adherence to exercise regimens among diabetes patients equipped with trackers, supporting quantifiable health gains. These developments deepen consumer trust and normalize proactive self-care.

Smartphone-Ecosystem Integration and Super-Apps

Xiaomi shipments grew 44% in Q1 2025 after HyperOS unified phones, wearables, and smart-home devices, converting sporadic hardware sales into recurring digital-service engagement. Apple retains stickiness through tight Watch-iPhone-Health integration that concentrates personal data in one interface. In Asia, super-apps merge payments, transport, and wellness, and watches act as authentication tokens, cementing daily use. Samsung’s Galaxy Watch now controls SmartThings devices and leverages on-device AI for context-based suggestions, extending relevance beyond fitness. The strategic direction moves revenue from one-off sales to multi-year service bundles.

Breakthrough Non-Invasive Metabolic Monitoring

Samsung patents outline optical sensing and AI models that predict hypoglycemia without skin puncture, targeting accuracy thresholds demanded by regulators. A Nature paper documents polarization-based optics reaching 95% clinical accuracy with 0.24 MARD, closing the gap with invasive strips. Multilevel near-infrared algorithms report 9.98% MARD and sustain daily monitoring needs. FDA updates to Quality Management System Regulations streamline approval, giving manufacturers clearer pathways for integrated glucose solutions. Commercial introduction within five years would open new chronic-care revenue streams for the wearable computing devices market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and cybersecurity concerns | -2.4% | Stricter EU rules; US frameworks evolving | Short term (≤ 2 years) |

| Battery life and thermal-design limits | -1.8% | Hardware constraint worldwide | Medium term (2-4 years) |

| Regulatory ambiguity for medical-grade claims | -1.6% | FDA and EU MDR | Long term (≥ 4 years) |

| Advanced component supply bottlenecks | -1.3% | Taiwan and South Korea fabs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cybersecurity Concerns

A study shows 92% of users lack clarity on how wearable data is shared, fueling hesitation about sharing sensitive metrics.[4]National Institutes of Health, “Consumer Perceptions of Wearable Data Privacy,” nih.gov HIPAA exclusions for consumer devices leave enforcement gaps, and healthcare breaches rose 55% over five years, underlining exposure. The Australian Human Rights Commission warns of heightened neural-data risk in child-oriented wearables, prompting calls for privacy law modernization. Blockchain prototypes reduce unauthorized access by 45% and cut detection time to under 10 days, but cost and scalability remain barriers. Market momentum hinges on transparent consent flows and security-by-design architectures.

Battery Life and Thermal-Design Limits

Consumer expectations for multi-day endurance conflict with heavier processing needed for AI, multi-band radios and bright micro-LEDs. Piezoelectric harvesters from DGIST generate 280-fold higher output than prior designs, hinting at supplemental power from body motion. Nonetheless, commercial readiness is several cycles away, and developers continue to juggle feature richness with heat dissipation. Apple patent filings describe context-aware power allocation that scales CPU loads based on activity, moderating skin-surface temperature. Until energy density improves further, component trade-offs will curb aggressive sensor roll-outs in the wearable computing devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smartwatches Maintain Lead While Hearables Surge

Smartwatches accounted for 45.30% of wearable computing devices market share in 2025, anchored by comprehensive health dashboards and extensive third-party app ecosystems that secure daily relevance. The wearable computing devices market size attributed to smartwatches is poised to grow steadily as BioActive and other multi-modal sensors enable metabolic readings beyond heart rate. Ear-worn devices, advancing at 18.02% CAGR to 2031, benefit from discreet form factors and the addition of temperature, heart-rate and voice command functions. Industrial head-mounted displays gain ground in shipbuilding and field service by overlaying digital instructions, driving measurable productivity gains. Smart clothing remains nascent, though flexible printed circuits and textile-embedded electrodes from e-skin prototypes advance rehabilitation use cases. Fitness trackers feel price pressure from entry-level watches that bundle similar metrics at little premium.

The wearable computing devices industry sees body-worn cameras and exoskeletons serving specialist verticals such as public safety and manufacturing fatigue mitigation. Market entrants emphasize open APIs so video streams and biomechanical data feed into employer dashboards. Smart glasses pivot to warehouse and healthcare workflows, cutting manual scanning time and error rates. Vendors invest in ultra-low-power chipsets so prescription-lens variants meet optical clarity and battery objectives. Overall, product diversification expands the total addressable base without eroding smartwatch primacy, supporting layered growth across the wearable computing devices market.

By End User: Medical Uptake Accelerates Beyond Fitness Roots

Fitness and wellness accounted for 38.40% of the wearable computing devices market size in 2025, held up by broad consumer interest in step counts, sleep staging, and on-watch coaching. Integration with subscription fitness content strengthens retention. Medical and healthcare applications, forecast to grow 18.7% CAGR, transition devices from wellness accessories to reimbursable clinical tools as remote patient monitoring programs reimburse continuous vitals capture. Chronic-disease cohorts such as Type 2 diabetes show measurable blood-glucose control improvements when guided by wearable-generated alerts and tele-consultation prompts. Hospitals adopt patch-based sensors for post-operative care, reducing bedside checks and freeing staff time.

Infotainment keeps momentum through immersive audio, while industrial firms deploy environmental monitors to cut exposure incidents in hazardous zones. Defense uses include biometric authentication and situational awareness overlays. The wearable computing devices industry also touches education, where attention-tracking headsets inform adaptive curricula. Demand convergence pushes suppliers to meet both IEC medical safety norms and ruggedized ingress ratings, further professionalizing design and quality assurance obligations.

By Operating System: HarmonyOS Challenges watchOS Supremacy

watchOS held 38.55% revenue share in 2025, showing strong synergy with iPhone and HealthKit that simplifies onboarding and data consolidation. The wearable computing devices market size tied to watchOS grows through premium pricing, even as unit growth eases. HarmonyOS, expected to post a 16.6% CAGR to 2031, rides Huawei phone loyalty in markets without Google Services and secures regional service partners for health cloud storage. Android-based Wear OS competes on breadth but still contends with irregular update cadence among OEMs, diluting the uniform experience.

Real-time operating systems address deterministic latency in medical pumps and industrial alarms, favoring verified code bases over expansive app stores. Proprietary stacks endure where single-purpose focus or ultra-long battery life outweighs ecosystem breadth. Cross-device orchestration is the next battleground: leading brands expose APIs that let tablets, TVs, and vehicles retrieve wearable biometrics, creating network effects in the wearable computing devices market.

By Connectivity Technology: Ultra-Wideband Augments Bluetooth Dominance

Bluetooth managed a 47.30% share in 2025, enabled by low-energy profiles and near-ubiquitous phone support. The wearable computing devices market relies on Bluetooth for most notification and audio pathways. Ultra-wideband adoption, growing 19.2% CAGR, brings centimeter-level ranging that improves asset tracking, fall detection in elder-care, and secure car entry. LTE and 5G modules free devices from phone tethers, vital for lone-worker safety and adventure sports, though battery drain and cellular subscription costs limit mass adoption. Wi-Fi powers high bandwidth transfers like firmware updates, whereas NFC sustains contactless payments with minimal energy draw.

Multi-protocol chipsets allow dynamic selection based on range, power, and data-rate needs. Regulatory bodies already set exposure guidelines under specific absorption rate limits, influencing antenna design and payload scheduling. Developers optimise stacks to enter deep-sleep between bursts, keeping thermal load within comfort limits even as data payloads grow.

Geography Analysis

North America retained 34.10% share of the wearable computing devices market in 2025 as insurers integrated devices into wellness incentives and clinicians embraced remote monitoring enrolment. Apple, Samsung and rising health-tech specialists benefit from reimbursement codes that cover continuous vitals capture, reinforcing consumer willingness to pay out-of-pocket premiums. Heightened scrutiny of data collection pushes vendors to adopt US-based HIPAA-aligned clouds and transparent consent flows. Health-system pilots demonstrate lower readmissions among cardiac patients equipped with connected patches, amplifying hospital procurement interest.

Asia Pacific is the fastest-growing region at 16.25% CAGR to 2031. Local brands in India offer sub-USD 30 smartwatches that still package blood-oxygen and heart-rate alerts, expanding addressable consumer segments. China pursues integrated health-digitization polices that reimburse remote monitoring for chronic diseases, encouraging hospital procurement of medical-grade wristbands. Japan showcases cooling wearables for workforce comfort in humid environments, while South Korea’s component supply clusters underpin global production scalability. Import tariffs push OEMs to diversify assembly into Vietnam and Indonesia, mitigating cost swings. Europe posts steady growth under a more cautious adoption curve. GDPR alignment delivers user trust yet adds documentation overhead. National health systems pilot device subsidies for chronic-care populations, but reimbursement schedules differ widely between member states. Middle East and Africa see potential in affluent Gulf markets where connected fitness is a status symbol, contrasted by infrastructure hurdles in sub-Saharan regions. Latin America records pockets of demand in Brazil and Mexico as gym culture and smartphone penetration improve. Across regions, the wearable computing devices market continues to be shaped by healthcare policy, disposable income and telecom infrastructure maturity.

Competitive Landscape

The market remains moderately concentrated. Apple, Samsung and Xiaomi headline shipments, while Oura and other specialists capture valuation upside through focused propositions. Apple experienced unit softness in 2024 but leverages its patent pipeline—including liquid-filled blood-pressure sensors—to sustain premium differentiation. Samsung expanded volume and revenue after embedding Galaxy AI, which contextualizes diagnostics on-device and offloads fewer packets to the cloud, preserving user privacy. Xiaomi’s volume leadership in Q1 2025 reflects aggressive sub-USD 50 bands tied to HyperOS benefits that lock users into wider home-device ecosystems.

Strategy pivots from hardware features to service moats. Subscription tiers bundle guided workouts, sleep coaching, and metabolic analytics, smoothing revenue and reinforcing data feedback loops. Suppliers race to secure micro-LED, haptic drivers, and battery materials ahead of mass production timetables. White-space entrants target industrial safety niches with rugged smart glasses certified against impact and dust, while med-tech firms explore FDA fast-track pathways for pediatric arrhythmia detection patches. Component scarcity in Taiwan and South Korea highlights geopolitical risk and encourages dual-sourcing or near-shoring. The competitive theatre ultimately rewards ecosystem stickiness, regulatory foresight and resilient supply footprints across the wearable computing devices market.

Wearable Computing Devices Industry Leaders

Apple Inc.

Samsung Electronics Co. Ltd

Garmin Ltd.

Fitbit Inc.

Huawei Technologies Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: FDA issued final Quality Management System Regulation amendments aligning with ISO 13485:2016, providing clearer pathways for medical-grade wearable device approval and enhancing regulatory framework for health monitoring applications FDA.

- October 2024: Essence Healthcare announced Oura Ring distribution to Medicare Advantage Plan members at no additional cost, expanding wearable health monitoring access to senior populations Essence Healthcare.

- August 2024: Sony published Sustainability Report 2024 highlighting R&D investments in sensing, AI and digital virtual spaces through Sony Research Inc., including development of IMX500 intelligent vision sensor for wearable applications Sony Group Corporation.

Global Wearable Computing Devices Market Report Scope

Wearable computing devices are like portable computers that a user can wear on the body. This technological device is capable of storing and processing data using the internet. The rising popularity of the Internet of Things and the growing adoption of smartwatches, head-mounted display, body-worn camera, and exoskeleton are some factors fueling the market growth in various end-user segments, such as medical and healthcare and infotainment.

The Wearable Computing Devices Market is Segmented by Product Type (Smart Watches, Head Mounted Displays, Smart Clothing, Ear Worn, Fitness Trackers, Body Worn Camera, and Exoskeleton), End User (Fitness and Wellness, Medical and Healthcare, Infotainment, Industrial, and Defense), and Geography. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Smartwatches |

| Head-Mounted Displays |

| Smart Clothing |

| Ear-worn (Hearables) |

| Fitness Trackers |

| Body-worn Cameras |

| Exoskeletons |

| Smart Glasses |

| Fitness and Wellness |

| Medical and Healthcare |

| Infotainment |

| Industrial and Defense |

| Others |

| watchOS |

| Android / Wear OS |

| HarmonyOS |

| RTOS |

| Proprietary / Other |

| Bluetooth |

| Cellular (LTE, 5G) |

| Wi-Fi |

| NFC |

| Ultra-Wideband |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| APAC | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| South-East Asia | ||

| Rest of Asa-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Product Type | Smartwatches | ||

| Head-Mounted Displays | |||

| Smart Clothing | |||

| Ear-worn (Hearables) | |||

| Fitness Trackers | |||

| Body-worn Cameras | |||

| Exoskeletons | |||

| Smart Glasses | |||

| By End User | Fitness and Wellness | ||

| Medical and Healthcare | |||

| Infotainment | |||

| Industrial and Defense | |||

| Others | |||

| By Operating System | watchOS | ||

| Android / Wear OS | |||

| HarmonyOS | |||

| RTOS | |||

| Proprietary / Other | |||

| By Connectivity Technology | Bluetooth | ||

| Cellular (LTE, 5G) | |||

| Wi-Fi | |||

| NFC | |||

| Ultra-Wideband | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| APAC | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| South-East Asia | |||

| Rest of Asa-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the wearable computing devices market?

The wearable computing devices market is valued at USD 95.4 billion in 2026 and is on track to reach USD 201.92 billion by 2031.

Which product category leads the wearable computing devices market?

Smartwatches lead with 45.30% market share as of 2025 because they combine health dashboards with robust app ecosystems.

Which region is growing fastest in the wearable computing devices market?

Asia Pacific is expanding at 16.25% CAGR to 2031, driven by affordable local brands and strong smartphone integration.

How are medical applications influencing market growth?

Medical and healthcare applications are growing at 18.7% CAGR as regulatory clarity and non-invasive monitoring technologies move devices into reimbursable clinical roles.

What is the key restraint for wider adoption of wearables?

Data privacy and cybersecurity concerns, coupled with fragmented regulations, exert the largest negative impact on the growth trajectory.

Which connectivity technology is emerging as a disruptor?

Ultra-wideband is the fastest-growing connectivity option at 19.2% CAGR thanks to its precise location tracking and enhanced security features.

Page last updated on: