Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

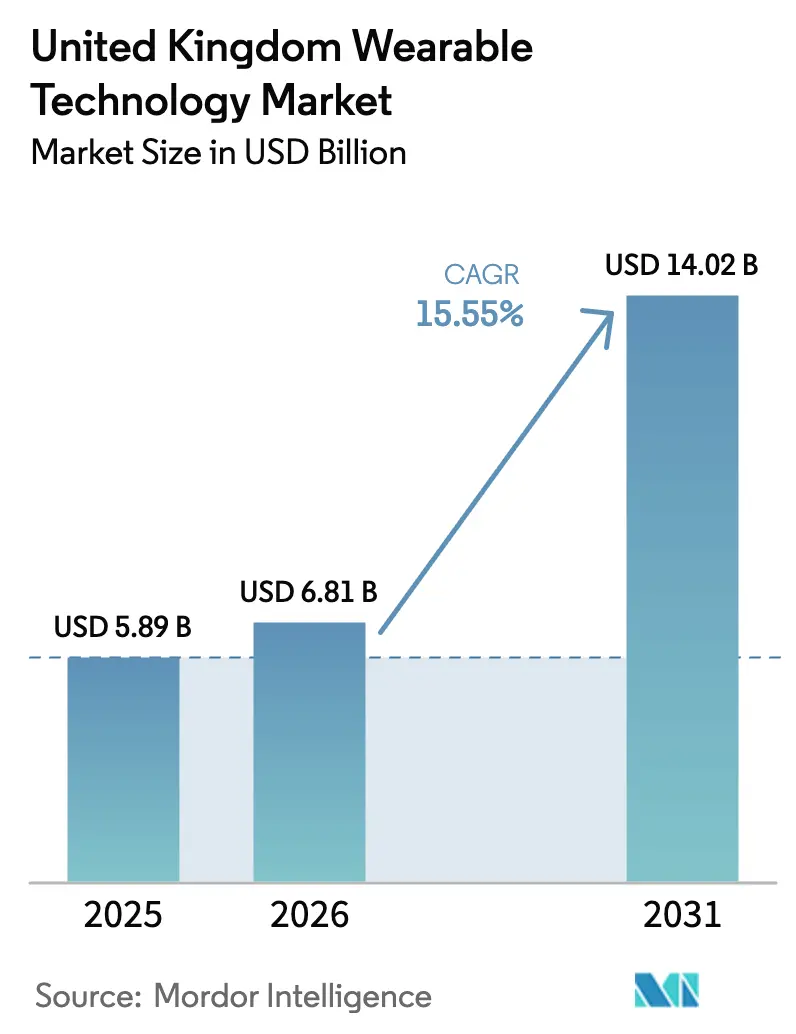

| Base Year Market Size (2025) | USD 5.89 Billion |

| Market Size (2026) | USD 6.81 Billion |

| Market Size (2031) | USD 14.02 Billion |

| Growth Rate (2026 - 2031) | 15.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Wearable Technology Market Analysis by Mordor Intelligence

The UK wearable technology market size is expected to grow from USD 5.89 billion in 2025 to USD 6.81 billion in 2026 and is forecast to reach USD 14.02 billion by 2031 at 15.55% CAGR over 2026-2031. Ongoing NHS virtual ward rollouts, rapid 5G coverage expansion, and fintech-linked health-insurance incentives combine to accelerate device demand across England, Scotland, Wales, and Northern Ireland. Smart watches strengthen clinical credibility after Apple secured FDA clearance for hypertension monitoring, while ear-wearables grow fastest as Meta’s Ray-Ban Display and Apple’s biosignal-enabled AirPods push the frontier of discreet sensing. Ultra-Wideband adoption gains pace despite Bluetooth’s dominance, giving manufacturers sub-centimeter indoor positioning that meets emerging hospital asset-tracking and logistics needs. Simultaneously, online direct-to-consumer retail leads distribution, aided by bundled subscription services that deliver continuous software and analytics upgrades. Competitive intensity stays moderate, yet regulatory compliance costs under WEEE battery rules and possible VAT reclassification continue to pressure smaller entrants.

Key Report Takeaways

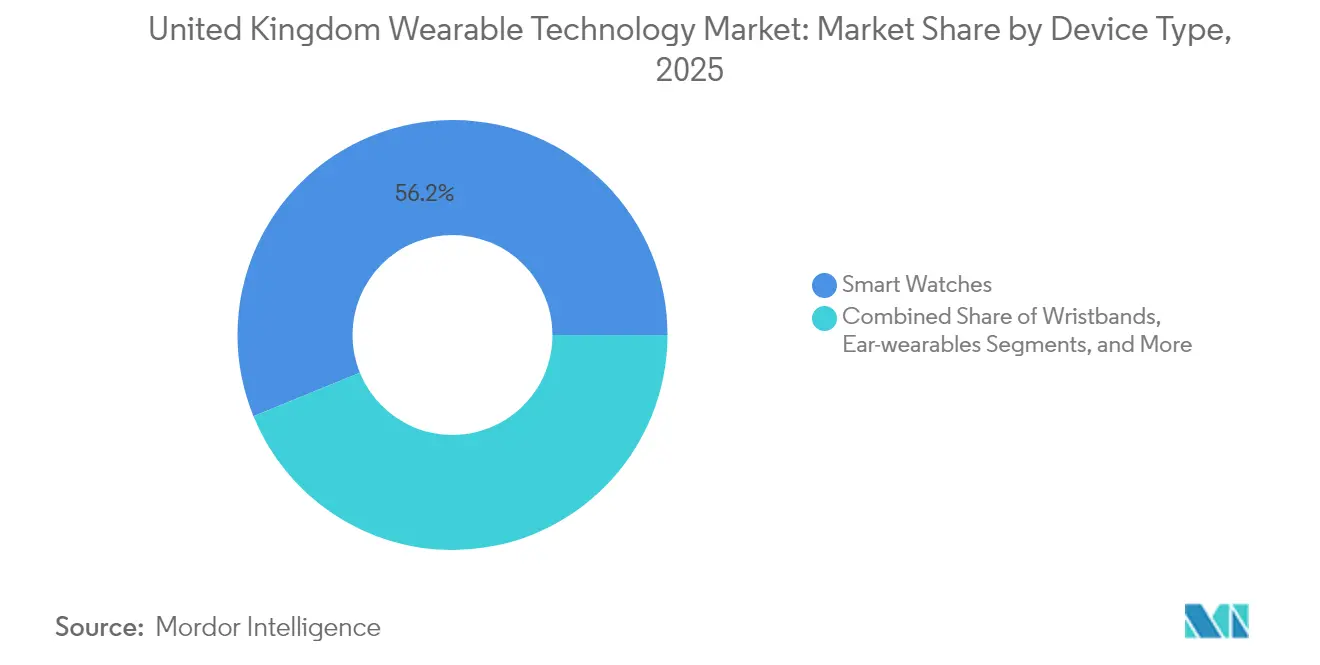

- By device type, smart watches led with 56.16% of UK wearable technology market share in 2025, while ear-wearables advanced at the highest 16.11% CAGR to 2031.

- By connectivity, Bluetooth retained 65.95% share of the UK wearable technology market size in 2025, whereas Ultra-Wideband is expanding at 16.80% CAGR.

- By operating system, watchOS captured 47.52% market share in 2025 and Wear OS is progressing at 15.83% CAGR.

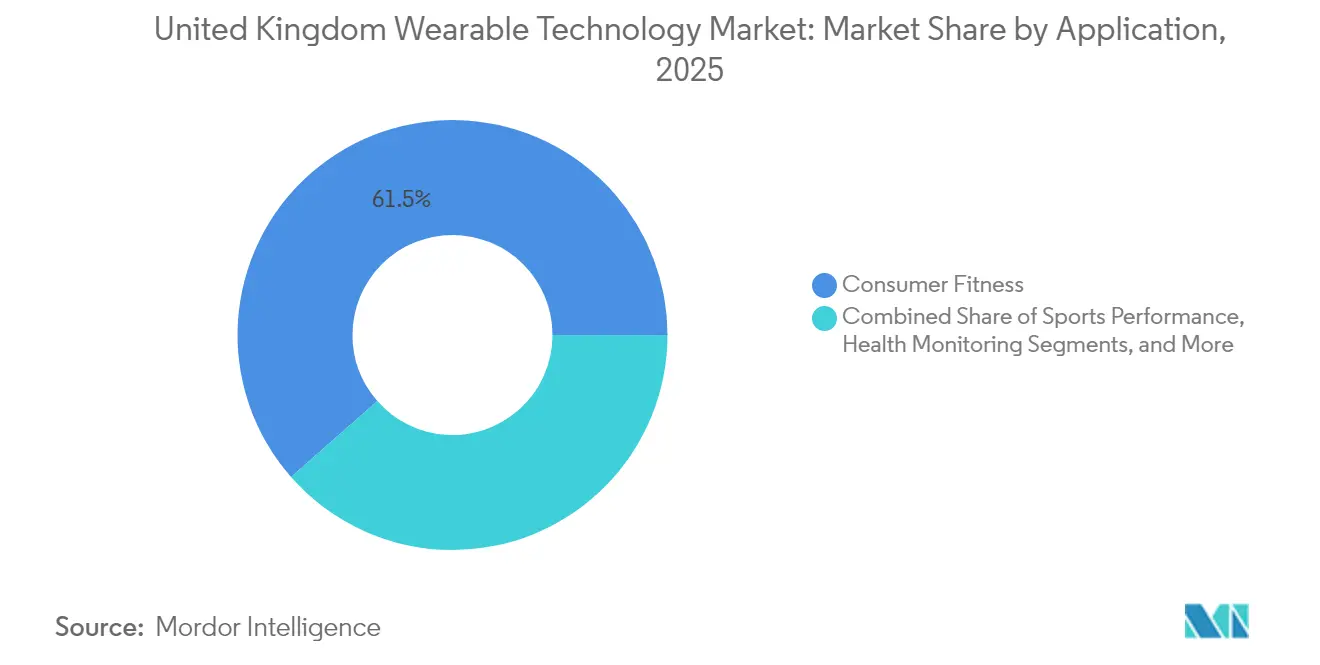

- By application, consumer fitness held 61.48% share of the UK wearable technology market size in 2025 and remote patient monitoring is moving ahead at 16.05% CAGR.

- By geography, England accounted for 83.58% of 2025 revenue, with Wales registering the fastest 15.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Wearable Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of NHS Digital Health Initiatives | +2.8% | England, Scotland, Wales, Northern Ireland | Medium term (2-4 years) |

| Integration of Wearables with UK Fintech Ecosystem for Health Insurance Incentives | +2.1% | England core, spillover to Scotland and Wales | Short term (≤ 2 years) |

| Adoption of AI-Powered Predictive Health Analytics in Consumer Wearables | +3.2% | Global with UK early adoption | Long term (≥ 4 years) |

| Rise of Workplace Wellness Regulations in the UK | +1.9% | England, Scotland, Wales, Northern Ireland | Medium term (2-4 years) |

| Expansion of 5G and IoT Infrastructure Across the UK | +2.4% | England, Scotland, Wales, Northern Ireland | Short term (≤ 2 years) |

| Growing Demand for Remote Patient Monitoring in Ageing Population | +3.1% | England, Scotland, Wales, Northern Ireland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of NHS Digital Health Initiatives

Virtual wards supported 4 million UK patients in 2024 and integrated care boards across West Yorkshire, Humber and North Yorkshire, and Cambridge and Peterborough plan broader coverage. Unified procurement frameworks shorten the path from clinical validation to national rollout, so device vendors with MHRA-cleared biosensors receive preferential consideration. Scotland and Wales mirror England’s model, evidencing nation-wide adoption of remote patient monitoring that underpins steady demand for validated wearables. NHS targets prioritize chronic respiratory and cardiovascular programs, aligning with smart-watch blood-pressure and pulse-ox features. Predictive analytics platforms further amplify device utility by translating raw data into actionable care-team alerts.

Integration of Wearables with UK Fintech Ecosystem for Health-Insurance Incentives

Fintech insurers link step counts, heart-rate variability, and sleep scores to dynamic premium discounts, spurring usage across younger, digitally native groups. Open banking standards and FCA oversight ensure secure data exchange between wearable apps and financial dashboards, improving adoption confidence. Employers deploy the same data flows to trigger wellness bonuses that lower group health-cover costs. Device makers benefit from recurring revenue when insurers subsidize hardware in exchange for long-term data access. Cross-platform APIs reduce user friction, reinforcing ecosystem stickiness and keeping churn low.

Adoption of AI-Powered Predictive Health Analytics in Consumer Wearables

Machine-learning models analyze multimodal signals to forecast arrhythmia events, stress spikes, or sleep-apnea risk, transforming devices from passive trackers to preventive companions. Apple’s 2025 software update delivers on-device hypertension prediction while Google’s Fitbit Labs pilots conversational AI that nudges users toward behavioral change.[1]Apple Inc., “Apple introduces groundbreaking health features to support conditions impacting billions of people,” Apple Newsroom, apple.com Research institutions partner with manufacturers to derive digital biomarkers that can replace invasive screening for diabetes or COPD. MHRA’s software-as-a-medical-device pathway provides regulatory clarity, accelerating approvals for AI modules integrated into consumer hardware. Continuous upgrades via cloud APIs extend product life cycles and strengthen subscription economics.

Rise of Workplace Wellness Regulations in the UK

Health and Safety Executive guidance increasingly promotes proactive monitoring of fatigue, ergonomics, and mental well-being. Large employers equip staff with wristbands and smart rings that flag cumulative strain, helping them document compliance and negotiate liability insurance discounts. Aggregate anonymized data informs organizational health benchmarks and resource allocation. Tax relief on qualifying wellness expenditures amplifies corporate uptake, particularly in logistics, construction, and financial services where productivity gains outweigh device outlays. Suppliers that deliver privacy-preserving analytics capture an edge because unions and staff councils demand strict data governance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter UK Data Privacy Enforcement Post-GDPR | -1.8% | England, Scotland, Wales, Northern Ireland | Short term (≤ 2 years) |

| Wearable Device VAT Reclassification Risk | -1.2% | England, Scotland, Wales, Northern Ireland | Medium term (2-4 years) |

| Battery Waste Regulations Increasing Compliance Cost | -0.9% | England, Scotland, Wales, Northern Ireland | Long term (≥ 4 years) |

| Consumer Skepticism on Long-Term Accuracy of Biosensors | -2.1% | Global with UK market impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter UK Data Privacy Enforcement Post-GDPR

The Information Commissioner’s Office intensifies audits of health-data processors and levies heavy fines for consent mis-steps, so smaller brands divert scarce funds into compliance or retreat from the UK. Mandatory data-protection-impact assessments slow new-feature rollouts, stretching time-to-market. Cross-border transfers to U.S. cloud servers trigger additional contractual safeguards that elevate operating expense. Established vendors capitalize on their mature privacy infrastructures, yet even they redesign user flows to gain granular consent without hurting engagement. Clear privacy victory messages on packaging now influence purchasing almost as strongly as battery life or waterproof ratings.

Consumer Skepticism on Long-Term Accuracy of Biosensors

Independent studies reveal variance in calorie-expenditure and sleep depth accuracy across mainstream wearables, fueling doubt among health-conscious buyers. Disappointment with overstated claims pushes some users to abandon devices within months, eroding retention metrics that underpin subscription revenue. Brands respond by publishing peer-reviewed validation, opening APIs for academic scrutiny, and seeking FDA or MHRA clearances. Nevertheless, high expectations make audiences quick to flag inconsistencies on social channels, so marketing narratives shift toward transparency and explainability rather than perfection.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Smart watches solidify leadership while ear-wearables accelerate

Smart watches accounted for 56.16% of UK wearable technology market share in 2025 and generated the highest revenue as Apple Watch’s hypertension clearance validated clinical utility. Ear-wearables lead growth at 16.11% CAGR, propelled by Meta’s AR audio glasses and Apple’s sensor-rich AirPods that discreetly record EEG and EMG signals.

Demand diversifies into smart rings and textile-embedded smart clothing. Oura doubled 2025 ring shipments, demonstrating appetite for minimalist form factors that deliver continuous monitoring without screen fatigue. Smart clothing pilots in elder-care homes record fall risk and hydration data through washable fibers, pointing to future convergence between fashion, medical monitoring, and ESG-compliant materials.

By Connectivity Technology: Bluetooth dominance meets Ultra-Wideband precision

Bluetooth covered 65.95% of connections in 2025, but Ultra-Wideband adoption is rising 16.80% annually as hospitals and warehouses seek centimeter-level indoor location. 5G modems appear in cellular wristbands targeted at high-risk patients who require uninterrupted remote patient monitoring.

Mesh networking firmware lets smart rings relay data to a watch, then to a phone, cutting power draw while maintaining real-time transmission. Ofcom spectrum allocations guarantee coexistence, and device makers design dual-radio chipsets that switch automatically based on bandwidth needs and battery status.

By Operating System: watchOS retains lead yet Wear OS narrows the gap

watchOS commanded 47.52% share in 2025 because of Apple’s tight hardware-software integration and NHS pilot deployments. Wear OS is growing 15.83% CAGR after Masimo and Google launched a reference platform bundling validated pulse-ox and ECG sensors.

Linux-based systems find traction where open-source customization is critical, like industrial safety helmets that combine gas sensing and head-impact detection. Samsung’s cross-platform Galaxy Ring strategy underscores a broader pivot toward ecosystem-agnostic accessories that reduce switching friction for non-iPhone users.

By Application: Fitness still dominates but healthcare monitoring gains momentum

Consumer fitness applications delivered 61.48% revenue in 2025, reinforced by pandemic-era exercise habits. The NHS virtual ward roadmap accelerates remote patient monitoring at a 16.05% CAGR, directly lifting demand for clinically validated sensors that transmit vitals into electronic patient records.

Corporate wellness programs integrate stress and posture analytics to comply with HSE guidelines and curb absenteeism. Sports performance analytics filter down from elite clubs to amateur leagues through subscription-based dashboards. Meanwhile, pregnancy-outcome studies from Garmin illustrate how large-scale consumer datasets now inform clinical research with minimal incremental cost.

By Distribution Channel: Online retail preserves the edge

Online platforms captured 57.86% revenue in 2025 and continue at 15.62% CAGR as brands exploit shoppable livestreams and AI chatbots to personalize bundles. Direct webstores pair devices with cloud analytics subscriptions, boosting lifetime value and shielding margins from retailer fees.

Brick-and-mortar consumer electronics chains remain relevant for high-ticket AR glasses where in-person demos clarify value. Pharmacies add clinically approved watches next to blood-pressure cuffs, aligning with their expanding frontline-care responsibilities. Insurance-sponsored distribution gains ground, with underwriters offering subsidized rings or bands in exchange for health-data sharing consent.

Geography Analysis

England contributed 83.58% of 2025 revenue in the UK wearable technology market after NHS England prioritized virtual wards across integrated care systems. London’s role as a fintech hub accelerates insurer-wearable tie-ins that scale nationally through digital channels. Continuous 5G coverage by the four major operators underpins low-latency remote monitoring and AR use cases in hospitals and logistics centers.

Wales posts the fastest 15.88% CAGR because targeted 5G grants modernize connectivity in rural zones and the Welsh government funds digital health pilots for aging-in-place services. University-led incubators in Cardiff and Swansea supply local start-ups that adapt wearables for bilingual interfaces and region-specific public-health programs.

Scotland maintains stable uptake through NHS Scotland’s COPD and heart-failure remote monitoring, while Northern Ireland benefits from cross-border EU regulatory alignment and shared clinical trials. Regional procurement frameworks emphasize interoperability so vendors must support shared FHIR data standards regardless of deployment area.

Competitive Landscape

Market concentration is moderate, with Apple, Samsung, and Fitbit controlling mainstream channels, while Oura, Garmin, and Polar specialize in rings and sports wearables. Dexcom invested USD 75 million in Oura to merge continuous glucose data with ring-based sleep and readiness scores, creating a holistic metabolic platform.[4]Dexcom Inc., “Strategic investment in Oura,” dexcom.com Apple’s hypertension clearance elevates clinical stakes, pressing rivals to secure similar approvals.

Component suppliers such as TDK entered the hardware stack by acquiring SoftEye to gain AR optics technology and deepen value-chain control.[5]TDK Corporation, “Acquisition of SoftEye,” tdk.com AI start-ups provide algorithms that device vendors license to speed time-to-market for new sensing modalities. The cost of MHRA certifications and WEEE compliance triggers partnership models where smaller innovators license IP to larger firms rather than pursue full product launches.

White-space opportunities persist in mental health and occupational safety. XPANCEO’s smart-contact-lens prototypes reveal potential to bypass form-factor constraints for in-eye glucose sensing. Venture and corporate investors channel funds toward battery chemistry breakthroughs and flexible electronics that promise multi-day wear without trade-offs in comfort or accuracy.

United Kingdom Wearable Technology Industry Leaders

Huawei Technologies Co., Ltd.

Samsung Electronics Co. Ltd.

Fitbit LLC

Xiaomi Inc.

Apple Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Meta released Ray-Ban Display smart glasses with EMG wristband at USD 799 for UK launch in early 2026.

- September 2025: Apple unveiled new health features across Apple Watch and iPhone targeting chronic conditions.

- September 2025: Garmin initiated a 60,000-participant pregnancy outcome study using smart watches.

- July 2025: iFIT partnered with Samsung Health to embed personalized fitness content across Galaxy devices.

United Kingdom Wearable Technology Market Report Scope

Wearable technology is an electronic device that can be worn as an accessory (e.g., as a watch). These devices often comes equipped with processing and communication capabilities. The United Kingdom Wearable Technology Market is Segmented by type of device including Smart Watches, Head-mounted Displays, Wristbands, and Ear-wearables. The report offers a comprehensive analysis of the past and future trends along with future opportunities. The report also offers an analysis of the impact of COVID-19 on the studied market.

By Device Type

| Smart Watches |

| Head-mounted Displays |

| Wristbands |

| Ear-wearables |

| Smart Clothing |

| Smart Rings |

| Other Device Types |

By Connectivity Technology

| Bluetooth |

| Wi-Fi |

| Cellular |

| NFC |

| Ultra-Wideband |

| 5G |

| Other Connectivity Technologies |

By Operating System

| watchOS |

| Wear OS |

| Proprietary OS |

| RTOS |

| Linux |

| Other Operating Systems |

By Application

| Consumer Fitness |

| Healthcare Monitoring |

| Remote Patient Monitoring |

| Corporate Wellness |

| Sports Performance |

| Medical Diagnostics |

| Other Applications |

By Distribution Channel

| Online Retail |

| Offline Consumer Electronics |

| Specialist Health Stores |

| Pharmacies |

| Department Stores |

| Other Distribution Channels |

By Geography

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Device Type | Smart Watches |

| Head-mounted Displays | |

| Wristbands | |

| Ear-wearables | |

| Smart Clothing | |

| Smart Rings | |

| Other Device Types | |

| By Connectivity Technology | Bluetooth |

| Wi-Fi | |

| Cellular | |

| NFC | |

| Ultra-Wideband | |

| 5G | |

| Other Connectivity Technologies | |

| By Operating System | watchOS |

| Wear OS | |

| Proprietary OS | |

| RTOS | |

| Linux | |

| Other Operating Systems | |

| By Application | Consumer Fitness |

| Healthcare Monitoring | |

| Remote Patient Monitoring | |

| Corporate Wellness | |

| Sports Performance | |

| Medical Diagnostics | |

| Other Applications | |

| By Distribution Channel | Online Retail |

| Offline Consumer Electronics | |

| Specialist Health Stores | |

| Pharmacies | |

| Department Stores | |

| Other Distribution Channels | |

| By Geography | England |

| Scotland | |

| Wales | |

| Northern Ireland |

Key Questions Answered in the Report

How much revenue will the UK wearable technology sector generate by 2031?

The segment is forecast to reach USD 14.02 billion in 2031, up from USD 6.81 billion in 2026.

Which device type is expanding at the quickest pace across the country?

Ear-wearables are advancing at a 16.11% CAGR, the highest among all product categories.

In what ways are NHS virtual wards shaping demand for connected devices?

The virtual-ward model relies on continuous remote monitoring, so hospitals are procuring clinically validated smart watches and rings that stream real-time vitals into electronic patient records, accelerating adoption in both acute and chronic-care pathways.

What benefits does Ultra-Wideband deliver to future UK wearables?

Ultra-Wideband offers centimeter-level indoor positioning that supports asset tracking in hospitals, hands-free device unlocking, and precise proximity alerts, driving a 16.80% CAGR for this connectivity option.

Why do UK data-privacy rules present a hurdle for smaller wearable vendors?

Post-GDPR enforcement demands strict consent workflows, regular audits, and secure cross-border data transfers, adding compliance costs that weigh more heavily on resource-constrained start-ups than on established brands with mature privacy infrastructures.

Which UK region is recording the fastest growth in wearable adoption?

Wales leads regional expansion with a 15.88% CAGR, supported by targeted digital-health funding and nationwide 5G rollout initiatives.

Page last updated on: