Business-to-Business (B2B) Courier, Express, And Parcel (CEP) Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

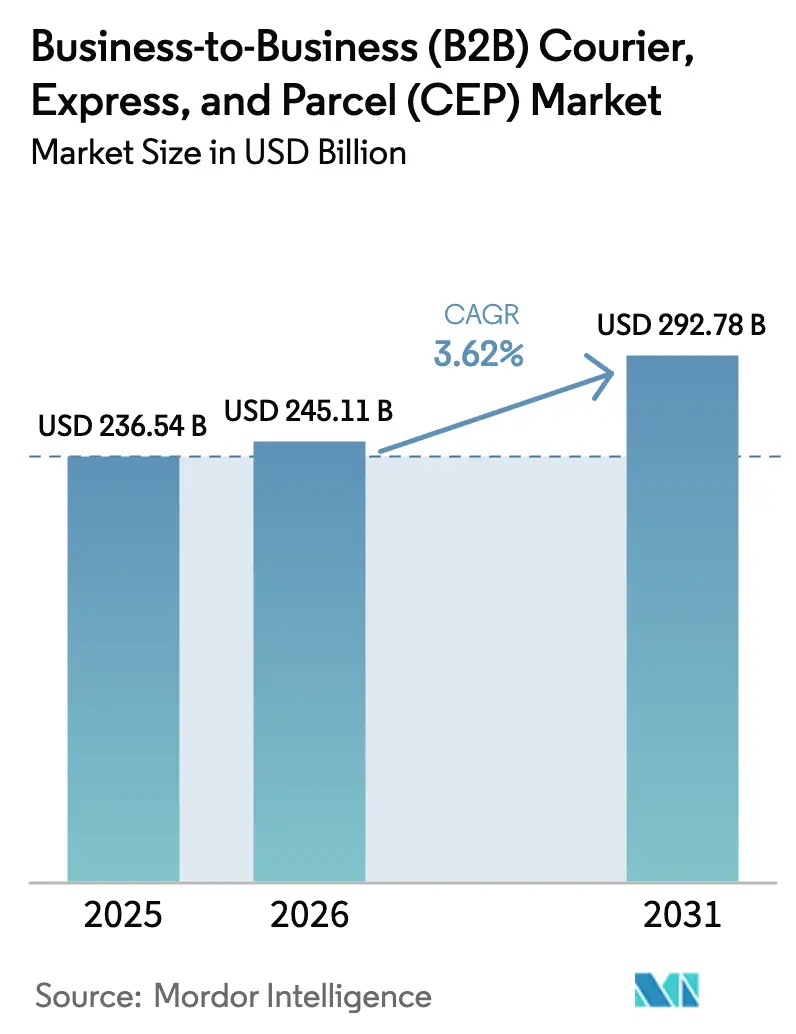

| Market Size (2026) | USD 245.11 Billion |

| Market Size (2031) | USD 292.78 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

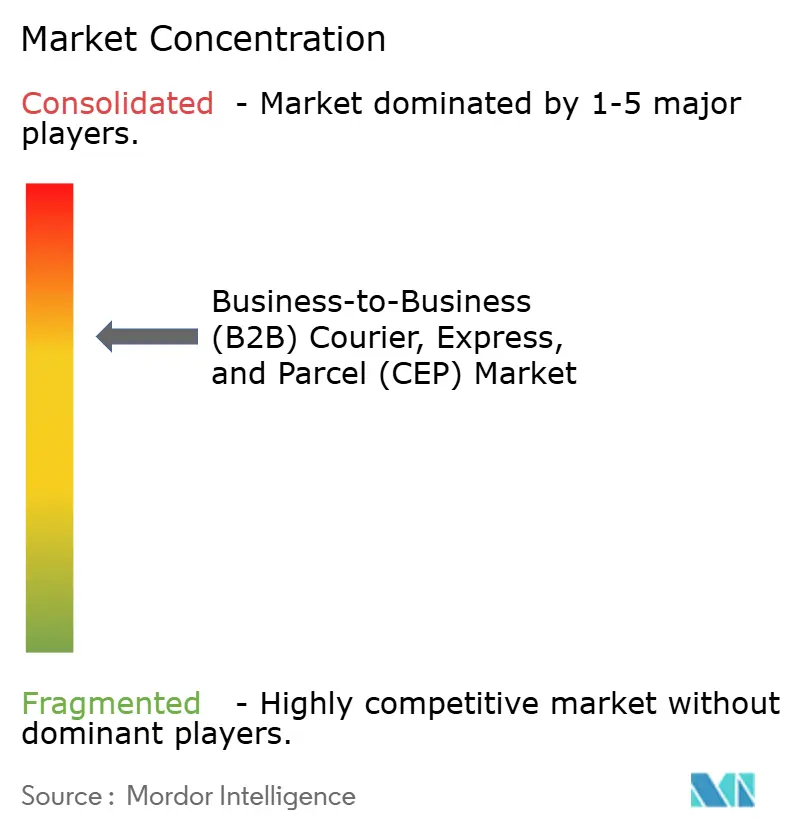

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Business-to-Business (B2B) Courier, Express, And Parcel (CEP) Market Analysis by Mordor Intelligence

The business-to-business (B2B) courier, express, and parcel (CEP) market size is expected to grow from USD 236.54 billion in 2025 to USD 245.11 billion in 2026 and is forecast to reach USD 292.78 billion by 2031 at 3.62% CAGR over 2026-2031. Heightened digital integration, automation, and near-shoring are reinforcing demand despite supply-chain volatility. North America continues to anchor revenue on account of network maturity, while Asia-Pacific registers the quickest expansion as manufacturers relocate capacity and cross-border e-commerce flourishes. Domestic deliveries dominate volumes, yet international lanes outpace them in growth as trade pacts compress customs friction. Express services attract premium pricing because B2B buyers now rank speed above cost, and operators with smart hubs and route optimization capture this shift. Consolidation, exemplified by DSV’s EUR 14.3 billion (USD 15.78 billion) acquisition of DB Schenker, signals the scramble for scale, technology, and specialized vertical capabilities.

Key Report Takeaways

- By destination, domestic shipments held 67.45% of the business-to-business (B2B) courier, express, and parcel (CEP) market share in 2025, whereas international shipments are expected to advance at a 4.42% CAGR between 2026-2031.

- By speed of delivery, non-express services accounted for 63.20% of the revenue share in 2025, while express segments are on track for a 4.41% CAGR between 2026-2031.

- By shipment weight, lightweight packages accounted for 62.95% of the business-to-business (B2B) courier, express, and parcel (CEP) market size in 2025, and medium-weight parcels are expected to grow at a 4.05% CAGR between 2026-2031.

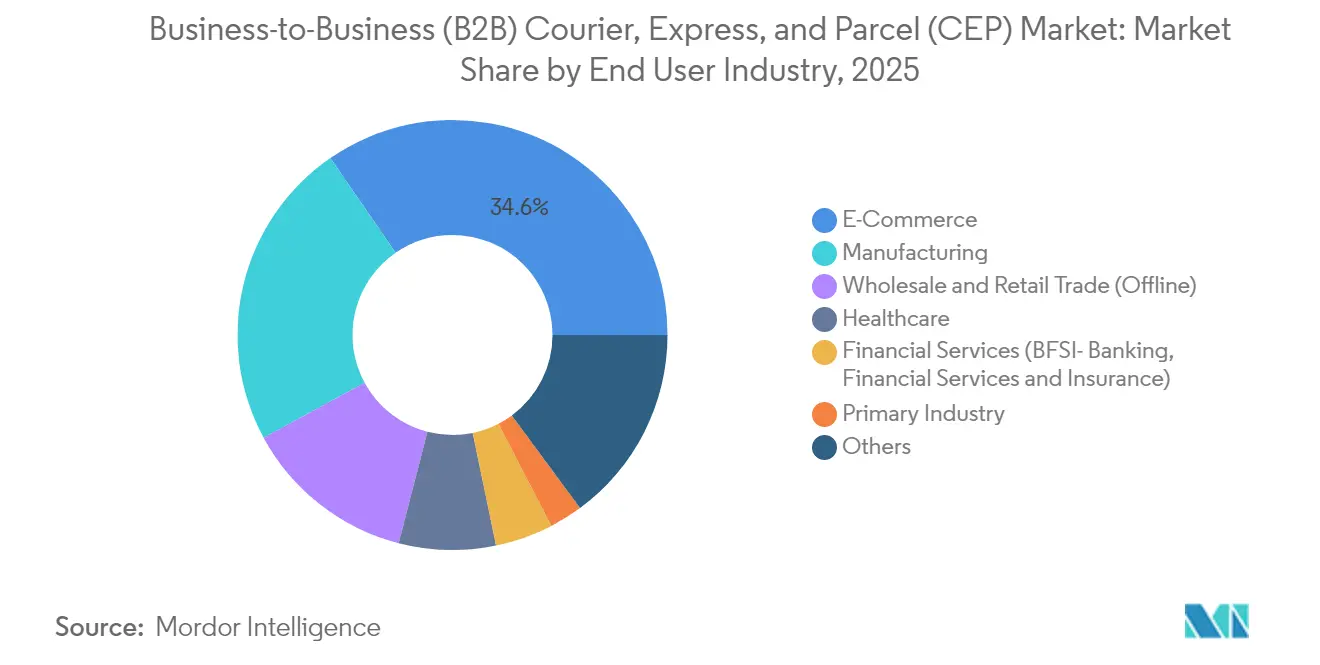

- By end user industry, e-commerce led with 34.62% revenue share in 2025; healthcare is forecast to grow at a 4.08% CAGR between 2026-2031.

- By mode of transport, road transport commanded 47.10% of revenue in 2025, whereas air transport is expected to rise at a 4.39% CAGR between 2026-2031.

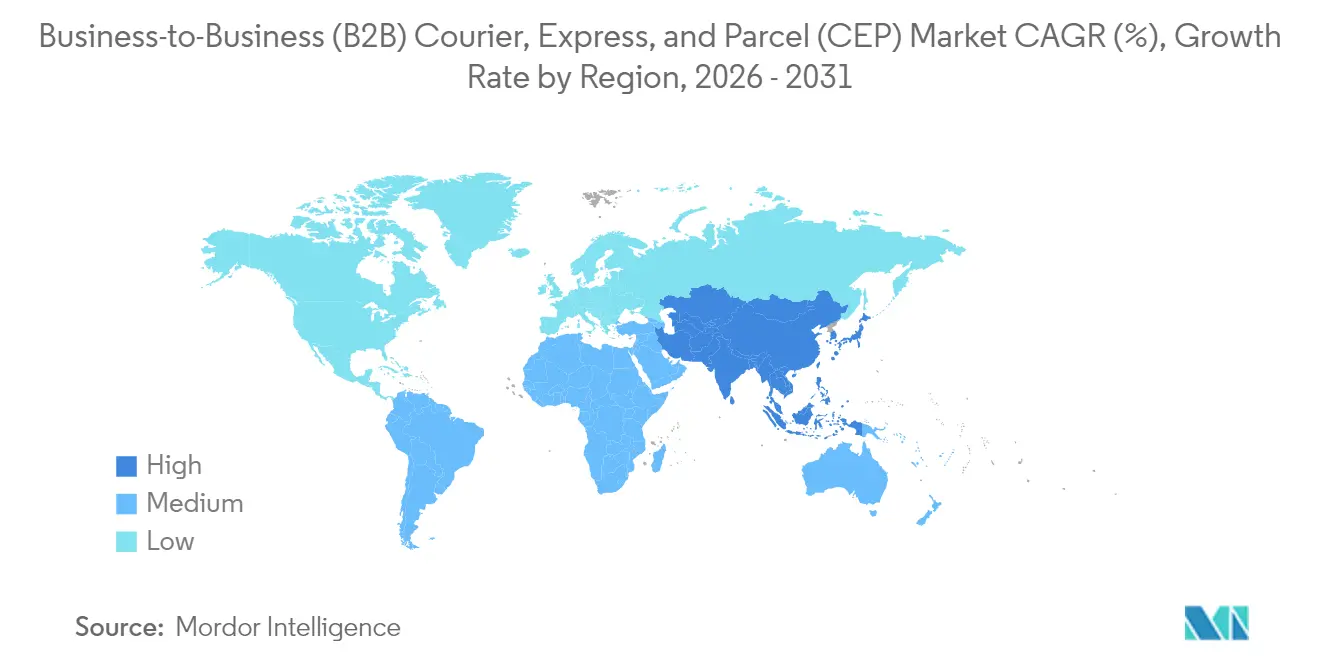

- By geography, North America commanded a 35.98% share in 2025, whereas Asia-Pacific is poised for the strongest regional up-trend at a 5.12% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Business-to-Business (B2B) Courier, Express, And Parcel (CEP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital trade growth among SMEs and suppliers fuels parcel demand | +1.2% | North America, Europe | Medium term (2-4 years) |

| Same‑day and next‑day deliveries rapidly becoming industry standard | +0.8% | North America, EU, APAC | Short term (≤ 2 years) |

| Trade pacts create fresh momentum for cross‑border shipping growth | +0.6% | APAC, Americas | Long term (≥ 4 years) |

| Automation and robotics transform warehouses into smarter hubs | +0.7% | Global | Medium term (2-4 years) |

| Near‑shoring and micro‑fulfilment support faster, on‑demand production | +0.5% | North America, Mexico, APAC | Medium term (2-4 years) |

| Rising carbon costs drive stronger focus on shipment consolidation | +0.4% | EU, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Digital Trade Adoption by SMEs and Industrial Suppliers

Small and mid-sized exporters now regard online channels as their principal growth lever, with DHL reporting that 65% of SMEs expect international e-commerce volumes to rise and 78% prioritize shorter transit times over discounts. Platform integration forces carriers to provide ERP connectivity and live tracking, shifting demand toward premium services that guarantee visibility and reliability. Industrial distributors mirror this behavior as they digitalize procurement, accelerating shipment frequencies and enlarging the addressable base for the business-to-business (B2B) courier, express, and parcel (CEP) market.

Tightening Delivery Windows – Same-Day and Next-Day as the Norm

Consumer shopping habits influence business purchasing, making one-day fulfillment a standard requirement in metropolitan areas. Quick-commerce operators that originally served consumers now target factories, hospitals, and repair shops, compelling legacy integrators to deploy urban micro-hubs, dynamic routing, and electric vans. Higher service levels widen the gap between scale players and smaller couriers that cannot match network reach.

New Cross-Border Opportunities From Trade Pacts

The RCEP accord, covering 15 Asia-Pacific members, slashes tariffs and streamlines procedures, opening new lanes for manufacturers and mid-market exporters[1]"RCEP fuels regional growth amid economic recovery, challenges," The State Council of the People’s Republic of China, gov.cn. In North America, USMCA provisions spur near-shoring, boosting cross-border volumes between the United States, Mexico, and Canada. Providers with customs-clearance expertise exploit first-mover advantage, cementing partnerships with regional SMEs that seek turnkey door-to-door options.

Smarter Warehouses and Hubs through Automation

Robotic sorters, AI-driven load-balancing, and autonomous guided vehicles raise throughput while easing labor shortages, a pain point highlighted by rising vacancy rates for warehouse technicians. Automation enables 24/7 cut-off windows and error-free handling of temperature-controlled consignments, making it indispensable for healthcare and high-tech verticals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| City restrictions worsen congestion and last‑mile delivery bottlenecks | -0.4% | Global cities | Short term (≤ 2 years) |

| Complex regulations and duties create barriers to seamless shipping | -0.3% | Global cross-border lanes | Medium term (2-4 years) |

| Retailers and marketplaces expand by owning delivery capabilities | -0.2% | North America, EU, APAC | Medium term (2-4 years) |

| Shortage of skilled technicians slows adoption of automation systems | -0.3% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urban Delivery Restrictions and Last-Mile Bottlenecks

Cities from Paris to New York roll out zero-emission zones, congestion charges, and time-window limits that inflate cost structures and hinder route densification[2]"Urban Vehicle Access Regulations," European Commission, europa.eu. Operators must invest in electric fleets and secure micro-depots within city limits, eroding margins for high-frequency small-parcel rounds.

Complex Patchwork of Regulations, Duties, and Compliance Rules

Mandatory pre-arrival cargo filings under the EU’s Import Control System 2 elevate documentation burdens and add delay risk for non-compliant shippers[3]“Import Control System 2,” European Commission, europa.eu. Similar schemes worldwide require multi-country compliance expertise and specialized IT platforms, raising entry barriers for smaller couriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: E-Commerce Dominance, Healthcare Upside

E-commerce captured 34.62% of 2025 revenue, as corporate buyers migrate catalogs online and expect consumer-grade fulfillment. API integration, real-time milestone alerts, and flexible billing terms underpin stickiness with platforms such as Amazon Business. Healthcare, expected to be the quickest riser at a 4.08% CAGR (2026-2031), depends on validated cold-chain, chain-of-custody scans, and regulatory documentation.

Manufacturing maintains robust baseline volumes through inbound parts flow and outbound finished-goods distribution, anchoring long-term network density. Financial and extractive industries persist as high-margin niches that reward compliance expertise, rounding out end-market diversification in the business-to-business (B2B) courier, express, and parcel (CEP) industry.

By Destination: Domestic Dominance Meets International Momentum

Domestic parcels contributed 67.45% of revenue in 2025 and remain the backbone of the business-to-business (B2B) courier, express, and parcel (CEP) market. As companies reshore parts sourcing, local capacity utilization stays high. Yet international consignments, though only 32.55% in 2025, are expected to post a 4.42% CAGR between 2026-2031, benefiting from trade-pact tailwinds. The resulting diversification balances cyclical risks and lifts network yields.

Cross-border growth hinges on customs digitization and SME adoption of online marketplaces that simplify foreign ordering. Routes within RCEP already report mid-teen volume jumps, especially on China-ASEAN corridors. Providers that pre-integrate regulatory data and duty calculations into booking portals strengthen loyalty among emerging exporters, expanding the business-to-business (B2B) courier, express, and parcel (CEP) market footprint.

By Speed of Delivery: Express Services Accelerate

Although non-express held a 63.20% revenue share in 2025, express options claim superior momentum with a projected 4.41% CAGR (2026-2031). Faster cycles allow buyers to cut safety stocks and free working capital, resonating with just-in-time manufacturing and hospital supply chains. The premium equips carriers to justify capital outlays for high-density sortation assets and aircraft.

Price-sensitive segments still rely on standard services for bulk replenishment, yet rising on-demand requirements foster dual-tier contract models, pairing express for critical parts with deferred for routine loads. This hybrid approach widens share-of-wallet opportunities in the business-to-business (B2B) courier, express, and parcel (CEP) market.

By Shipment Weight: Light Weight Parcels Drive Frequency, Medium Weight Parcels Drive Yield

Light-weight parcels generated 62.95% of consignments in 2025 owing to component-level sourcing and small-package B2B e-commerce. Automation elevates their processing efficiency, aligning with 24-hour dispatch promises. Medium-weight parcels are forecast to grow at a 4.05% CAGR (2026-2031), striking a sweet spot between revenue per piece and express sortation compatibility.

Heavy-weight parcels remain niche, constrained by handling requirements and modal competition from LTL trucking. Nonetheless, specialized integrators monetize them by bundling installation and return-logistics services for industrial equipment, maintaining relevance within the broader business-to-business (B2B) courier, express, and parcel (CEP) market.

By Mode of Transport: Road Transport Remains Essential, Air Transport Gains Altitude

Road transport held a 47.10% share in 2025 owing to ubiquitous highway reach and final-mile flexibility. Even under sustainability mandates, electric vans and alternative fuels keep road relevant. Air transport, expanding at a 4.39% CAGR (2026-2031), channels express and international urgency, bolstered by main-deck capacity additions and e-AWB adoption.

Rail and sea retain roles in heavy or non-urgent consignments but confront transit-time penalties incompatible with tightening service-level agreements. Multimodal bundling that pairs ocean outbound with air expedited returns emerges as a margin enhancer, supporting integrated solutions within the business-to-business (B2B) courier, express, and parcel (CEP) market.

Geography Analysis

North America controlled 35.98% of global revenue in 2025, underpinned by sophisticated fulfillment infrastructure and USMCA-enabled cross-border flows. Same-day coverage across the contiguous United States provides a benchmark for service elsewhere, and automation offsets elevated labor costs. Regulatory challenges, however, surface in cross-border security filings and divergent state-level carbon policies, nudging carriers toward unified compliance platforms.

Asia-Pacific is expected to be the fastest-growing arena at 5.12% CAGR (2026-2031). China’s manufacturing gravity anchors long-haul exports, yet Southeast Asia rises on supply-chain diversification. The RCEP framework trims customs latency, amplifying intra-regional parcel density. India contributes double-digit growth in domestic B2B dispatches as SME sellers exploit nationwide e-commerce penetration. Local couriers climb the value curve by investing in temperature-controlled fleets, courting healthcare and electronics clients.

Europe offers mature infrastructure and standardized security under ICS2, but macro-economic headwinds temper short-term expansion. Germany and France function as continental gateways, while the Nordics champion zero-emission last-mile pilots. Post-Brexit Britain negotiates new data-sharing protocols, injecting complexity yet spawning advisory opportunities for customs-savvy carriers. Urban access fees and emission zones accelerate the transition to electric fleets, potentially lifting cost-per-stop but protecting network sustainability in the business-to-business (B2B) courier, express, and parcel (CEP) market.

Competitive Landscape

The arena remains moderately fragmented, with the top four providers accounting minor share of the global turnover. Yet headline deals illustrate mounting consolidation pressure. DSV’s EUR 14.3 billion (USD 15.78 billion) purchase of DB Schenker in 2025 vaults it into second-place revenue ranks behind DHL. Scale amalgamates contract logistics, airfreight allotments, and IT investments, reinforcing defensive moats.

Technology differentiation shapes strategy: DHL deploys AI-based route orchestration, FedEx beta-tests autonomous tugs, and UPS invests in healthcare-dedicated GMP hubs. Regionals counter by specializing—Aramex leverages Middle-East customs fluency, while SF Holding pairs China’s domestic girth with European last-mile via its GLS alliance. Venture-backed platforms furnish API gateways, letting micro-couriers plug into global track-and-trace ecosystems without bearing capex burdens.

Vertical expertise gains prominence. GDP certificates unlock pharma revenue, ISO 13485 supports medical devices, and bonded-warehouse capabilities attract high-tech exporters. Environmental credentials such as Science-Based Targets compliance differentiate bids amid customer carbon-audit demands. Price wars recede in favor of total cost-of-ownership arguments, repositioning the business-to-business (B2B) courier, express, and parcel (CEP) market as a value-driven, service-differentiated landscape.

Business-to-Business (B2B) Courier, Express, And Parcel (CEP) Industry Leaders

-

DHL Group

-

United Parcel Service of America, Inc. (UPS)

-

FedEx

-

SF Holding Co., Ltd. (Including KEX-SF)

-

La Poste Group (Including DPD Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ADQ (Abu Dhabi Developmental Holding Company) completed a USD 1.1 billion acquisition of Aramex PJSC, injecting capital for Middle East network upgrades.

- March 2025: Cainiao opened its largest ASEAN fulfillment center in Vietnam, pledging 30% faster cross-border e-commerce delivery.

- October 2024: SF Holding partnered with GLS Group to strengthen European last-mile capacity for Asia-origin parcels.

- May 2024: Japan Post Holdings launched its JP Vision 2025+ strategic plan, committing JPY 1 trillion (USD 7.09 billion) in technology investments and international expansion initiatives.

Global Business-to-Business (B2B) Courier, Express, And Parcel (CEP) Market Report Scope

The B2B courier express parcel market refers to the business-to-business courier express parcel market. It involves the transportation and delivery of packages, documents, and goods between businesses. These services are designed to be fast, reliable, and efficient, meeting the specific needs of businesses when it comes to sending and receiving shipments.

The B2B courier express parcel market is segmented by destination (domestic and international), end user (BFSI (banking, financial services, and insurance), wholesale and retail trade, manufacturing, construction, and utilities, and primary industries (agriculture and other natural resources)) and geography (North America, Europe, Asia-Pacific, and LAMEA. The report offers market sizes and forecasts in terms of value (USD) for all the above segments.

| Domestic |

| International |

| Express |

| Non-Express |

| Heavy Weight Shipments |

| Light Weight Shipments |

| Medium Weight Shipments |

| E-Commerce |

| Financial Services (BFSI) |

| Healthcare |

| Manufacturing |

| Primary Industry |

| Wholesale and Retail Trade (Offline) |

| Others |

| Road |

| Air |

| Others |

| Asia-Pacific | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| Philippines | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Europe | France |

| Germany | |

| Italy | |

| Netherlands | |

| Spain | |

| United Kingdom | |

| Nordics | |

| Central and Eastern Europe (CEE) | |

| Rest of Europe | |

| Middle East and Africa | Qatar |

| Saudi Arabia | |

| United Arab Emirates | |

| Egypt | |

| Nigeria | |

| South Africa | |

| Rest of Middle East and Africa | |

| North America | Canada |

| Mexico | |

| United States | |

| Rest of North America | |

| South America | Argentina |

| Brazil | |

| Chile | |

| Rest of South America |

| Destination | Domestic | |

| International | ||

| Speed of Delivery | Express | |

| Non-Express | ||

| Shipment Weight | Heavy Weight Shipments | |

| Light Weight Shipments | ||

| Medium Weight Shipments | ||

| End User Industry | E-Commerce | |

| Financial Services (BFSI) | ||

| Healthcare | ||

| Manufacturing | ||

| Primary Industry | ||

| Wholesale and Retail Trade (Offline) | ||

| Others | ||

| Mode of Transport | Road | |

| Air | ||

| Others | ||

| Geography | Asia-Pacific | Australia |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Malaysia | ||

| Philippines | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Europe | France | |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Spain | ||

| United Kingdom | ||

| Nordics | ||

| Central and Eastern Europe (CEE) | ||

| Rest of Europe | ||

| Middle East and Africa | Qatar | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Egypt | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

| North America | Canada | |

| Mexico | ||

| United States | ||

| Rest of North America | ||

| South America | Argentina | |

| Brazil | ||

| Chile | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the business-to-business (B2B) courier, express, and parcel (CEP) market in 2026?

The segment is valued at USD 245.11 billion in 2026, with a forecast to reach USD 292.78 billion by 2031.

Which region grows fastest between 2026 and 2031?

Asia-Pacific leads with a projected 5.12% CAGR (2026-2031) thanks to RCEP trade facilitation and manufacturing migration.

What is the main growth driver through 2031?

Rising SME participation in cross-border digital trade adds an estimated +1.2 percentage points to CAGR.

Which end-user sector shows the highest growth momentum?

Healthcare, propelled by stringent cold-chain needs, is expanding at a 4.08% CAGR between 2026-2031.

How is consolidation reshaping competition?

Mega-deals like DSV-DB Schenker enhance scale economies, automation funding, and global lane coverage, compressing smaller rivals’ margins.

What impact will urban low-emission zones have on carriers?

Carriers must electrify fleets and deploy parcel lockers to retain city access, raising capital requirements but lowering future emission penalties.

Page last updated on: