Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

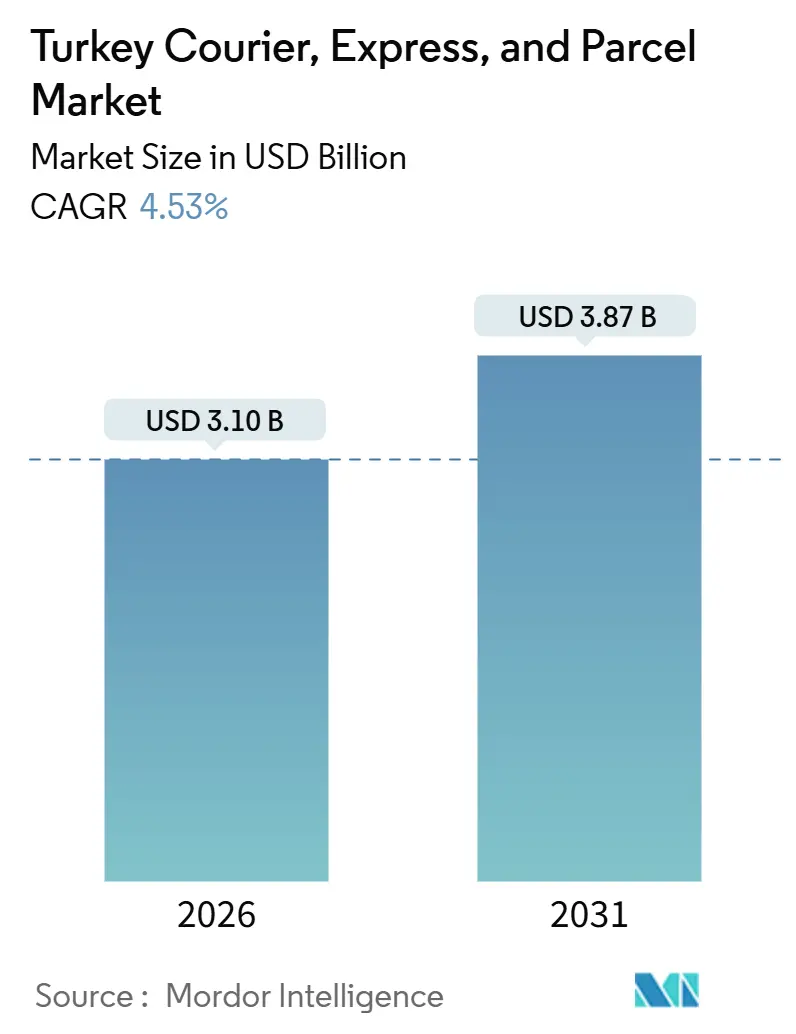

| Market Size (2026) | USD 3.10 Billion |

| Market Size (2031) | USD 3.87 Billion |

| Growth Rate (2026 - 2031) | 4.53% CAGR |

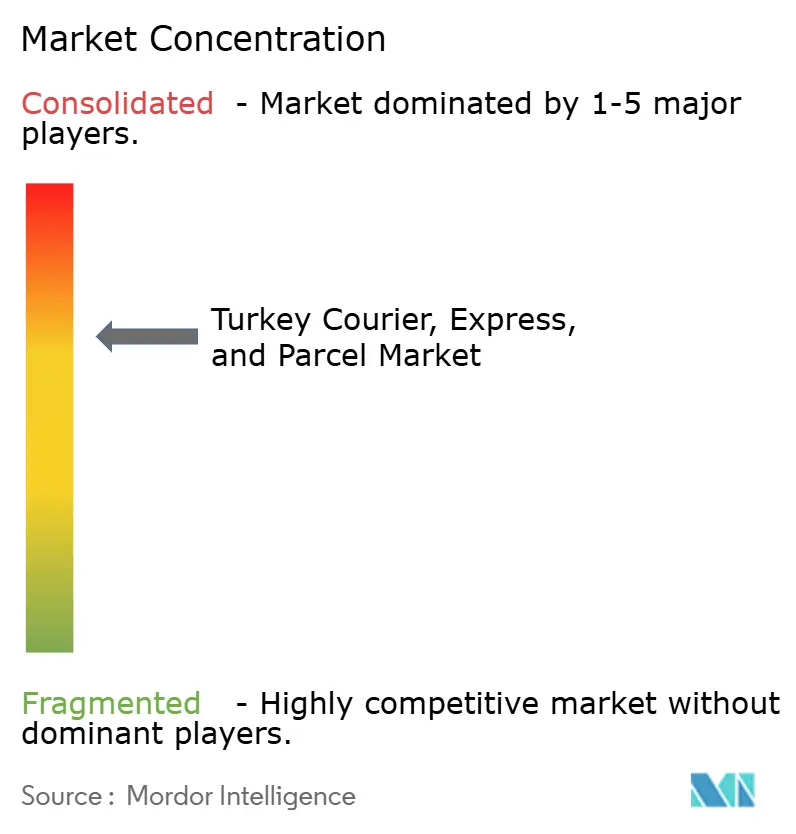

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Courier, Express, And Parcel Market Analysis by Mordor Intelligence

The Turkey courier, express, and parcel market size is estimated at USD 3.10 billion in 2026, and is expected to reach USD 3.87 billion by 2031, at a CAGR of 4.53% during the forecast period (2026-2031). The trajectory reflects a powerful mix of doubling e-commerce volumes, Istanbul Airport’s emergence as Europe’s busiest cargo hub, and rising demand for same-day services in densely populated metros. Domestic deliveries dominate current volumes, yet international flows are expanding faster as customs processes go digital and near-shoring tightens links with European buyers. Operators are investing in automated hubs, electric fleets, and route-optimization software to offset fuel inflation, lira depreciation, and urban congestion. These dynamics are sharpening competition between global integrators, cash-rich incumbents, and technology-first entrants across the Turkey courier express and parcel market.

Key Report Takeaways

- By destination, domestic shipments held 76.53% of the Turkey courier express and parcel market share in 2025, while international flows are forecast to grow at a 4.82% CAGR between 2026-2031.

- By speed of delivery, non-express services led with 83.31% revenue share in 2025; express offerings are projected to advance at a 5.64% CAGR between 2026-2031.

- By business model, B2C accounted for 53.44% of the Turkey courier express and parcel market size in 2025 and is projected to expand at a 5.91% CAGR between 2026-2031.

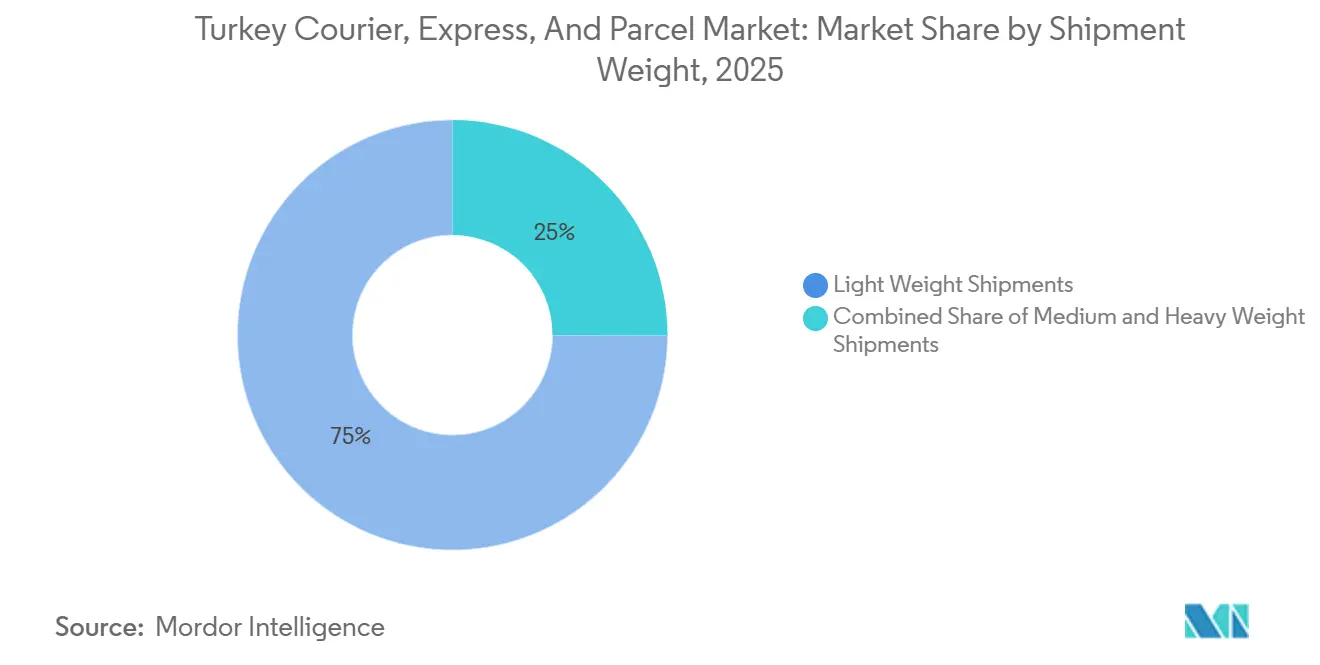

- By shipment weight, light weight parcels under 5 kg commanded a 74.96% share in 2025 and are expected to grow at a 4.99% CAGR between 2026-2031.

- By mode, road transport retained a 69.10% share in 2025, whereas multimodal alternatives are expected to rise at a 5.67% CAGR between 2026-2031.

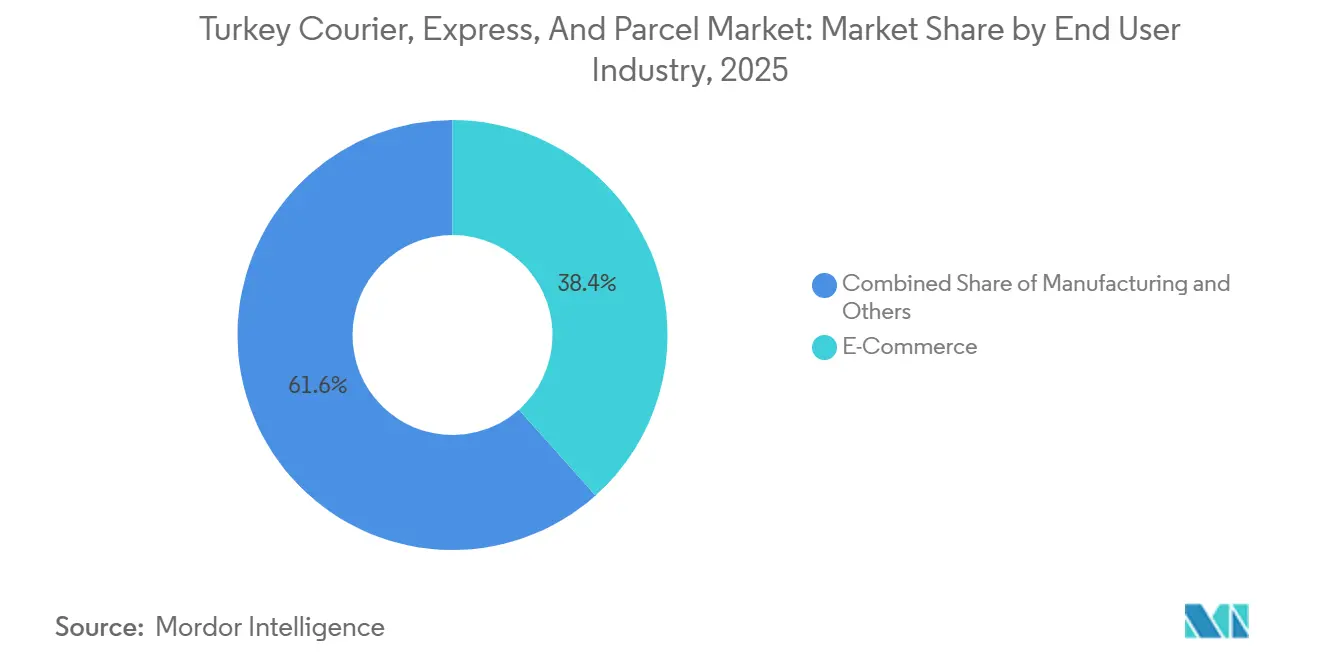

- By end user industry, e-commerce generated 38.42% revenue share in 2025 and is advancing at a 4.95% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Turkey Courier, Express, And Parcel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce volume surge | +1.2% | National, with concentration in Istanbul, Ankara, Izmir metropolitan areas | Short term (≤ 2 years) |

| Istanbul Airport as regional hub | +0.7% | National for domestic consolidation; international for cross-border flows to EU, Central Asia, Middle East | Medium term (2-4 years) |

| Customs-process digitalization | +0.5% | National, with spillover to cross-border corridors (EU, Georgia, Azerbaijan) | Medium term (2-4 years) |

| Near-shoring driven B2B flows | +0.4% | National, with early gains in Marmara, Aegean industrial zones | Long term (≥ 4 years) |

| Same-day/on-demand delivery demand | +0.6% | Urban cores (Istanbul, Ankara, Izmir, Bursa) | Short term (≤ 2 years) |

| Cross-border e-commerce initiatives | +0.5% | National, with emphasis on Istanbul Airport gateway and land corridors to EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Volume Surge

Turkey’s online spending doubled to TRY 1.85 trillion (USD 52.38 billion) in 2023 and climbed to TRY 3.16 trillion (USD 89.47 billion) in 2024, generating 476 million parcels in 4Q 2024 alone. Mobile commerce captured 50% of transactions, favoring lightweight, high-frequency orders. Roughly 220,000 e-commerce firms operate in Istanbul, concentrating last-mile demand where couriers execute 50-80 stops per day. Quick-commerce grocery sales reached TRY 126 billion (USD 3.56 billion) in 2023, further slicing delivery windows. Micro-fulfillment centers and automated hubs are proliferating as operators seek to compress cycle times without proportional labor. These forces underpin the growth premium visible across the Turkey courier express and parcel market[1]“E-Commerce Statistics 2024,” Turkish Statistical Institute, TURKSTAT.GOV.TR.

Istanbul Airport as Regional Hub

The airport handled 1.97 million tons of cargo in 2024, up 39.6% year-on-year, vaulting it to the top of the European rankings. FedEx opened a 25,300 m² hub in September 2025 capable of 7,000 packages per hour. UPS, DHL, and Turkish Cargo anchor additional flights that stitch Istanbul into overnight networks touching Cologne, Paris, and Dubai. Planned rail-highway corridors to the Persian Gulf will further consolidate flows. As a result, international parcels are set to outpace domestic growth within the Turkey courier express and parcel market.

Customs-Process Digitalization

A reduction in simplified-clearance thresholds from EUR 1,500 (USD 1,562.34) to EUR 30 (USD 31.24) in August 2024 sped electronic pre-clearance, even while adding duty costs for many inbound parcels. The Single Window platform links 22 agencies, cutting border dwell times by roughly 20%. Turkey also signed the eTIR roadmap with neighboring states, digitizing transit guarantees and trimming road-freight delays by 30%. Together, these reforms add velocity to cross-border flows and boost the competitiveness of the Turkey courier express and parcel market[2]“E-Commerce Merchant Registry 2024,” Turkish Ministry of Trade, TRADE.GOV.TR.

Same-Day/On-Demand Delivery Demand

Penetration of sub-24-hour delivery in Istanbul, Ankara, and Izmir is escalating as platforms promise groceries in under 30 minutes and general merchandise in 2-4 hours. Getir’s strategic retreat to its home market underlines the focus on rapid fulfillment. HepsiJet’s patented route-optimization cut fleet kilometers by 8% in 2024 and pairs with a growing electric-vehicle fleet to serve dense urban routes. Congestion, however, remains acute, pressing firms to invest in micro-depots within 5 km of demand clusters, an approach dominating capital plans across the Turkey courier express and parcel market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile fuel costs | -0.8% | National, with acute impact on long-haul road operators serving eastern provinces | Short term (≤ 2 years) |

| Urban congestion and delivery windows | -0.5% | Istanbul, Ankara, Izmir, Bursa metropolitan areas | Medium term (2-4 years) |

| Lira depreciation vs imported assets | -0.6% | National, affecting operators reliant on imported vehicles, sorting equipment, IT systems | Medium term (2-4 years) |

| Driver-workforce shortage | -0.4% | National, with concentration in urban cores where turnover exceeds 40% annually | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Fuel Costs

Diesel prices surged 44% in 2024, lifting transport costs by up to 35% for road-based carriers. With road still at 69.10% modal share, any 10% hike in diesel raises per-parcel costs 3-4% for operators lacking hedges. Investments in rail-road intermodal routes and initial deployments of electric vans are tactical shields, yet high upfront capital and sparse charging infrastructure hinder rapid scaling[3]“eTIR Implementation Roadmap 2024,” International Road Transport Union, IRU.ORG .

Urban Congestion and Delivery Windows

Istanbul ranks second globally for traffic, costing residents 105 lost hours a year. Off-peak vehicle restrictions in historic districts push delivery activity into costly night shifts. Although a 31-km North Marmara bypass is due by 2027, capacity relief will not arrive soon enough to ease the near-term margin squeeze within the Turkey courier express and parcel market[4]“Fuel Price Index 2024,” Turkish Energy Market Regulatory Authority, EPDK.GOV.TR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: E-Commerce Leads, Manufacturing Rises

E-commerce contributed 38.42% of total revenue generated in 2025 and is expected to grow at a 4.95% CAGR (2026-2031). Manufacturing follows as automotive output hit 1.4 million units in 2024, requiring just-in-time spares for EU plants.

Pharmaceuticals and banking add niche demand for temperature-controlled and secure document services, offering margin diversification for operators willing to invest in specialized capabilities.

By Destination: International Volumes Outrun a Large Domestic Base

Domestic shipments delivered 76.53% of parcels in 2025, reflecting Turkey’s 85 million population and dense e-commerce activity in western metros. Still, international parcels are forecast to rise at a 4.82% CAGR between 2026-2031 as Istanbul Airport accelerates cross-border sortation and A.TR automation streamlines EU-bound exports. The Turkey courier express and parcel market size for international flows is projected to capture a growing slice of total revenue as outbound sellers tap European and Central Asian demand. Longer-haul yields cushion operators against same-day cost pressures felt on domestic routes, underscoring the strategic pivot toward cross-border capacity.

The EU attracts 55% of outbound parcels, while the eTIR framework cuts clearance frictions on east-bound corridors. Truck-to-rail conversion in Eastern Anatolia promises margin uplift once freight capacity scales. Conversely, inbound B2C parcels cool after the new EUR 30 (USD 31.24) threshold imposed duties of 30%-60%, encouraging shoppers to favor local platforms.

By Speed of Delivery: Express Accelerates on Time-Critical Demand

Non-express services held 83.31% 2025 share, yet express is on track for a 5.64% CAGR (2026-2031), the fastest of any segment. Istanbul residents expect 2-4-hour fulfillment, pushing merchants to pay premiums for time-definite capacity. FedEx’s USD 130 million hub and UPS’s daily Cologne flight underline the rush to enlarge express capacity. Higher margins from spare parts and fabric-sample traffic also lift express economics inside the Turkey courier express and parcel market.

Despite elevated fuel and labor costs, algorithmic routing and parcel-locker rollouts anchor productivity gains. Standard three-day services remain vital for price-sensitive merchants, but their growth lags as consumer expectations shift.

By Shipment Weight: Light Parcels Dominate the Mix

Light parcels under 5 kg captured 74.96% of revenue generated in 2025, mirroring fashion, electronics, and cosmetics baskets favored online. The Turkey courier, express, and parcel market size for this weight band is projected to increase at a 4.99% CAGR (2026-2031), supported by mobile-first buying patterns and locker networks optimized for small cartons.

Medium and heavy parcels, tied to white-goods and furniture deliveries, grow more slowly due to narrow streets and congestion hurdles in old city centers.

By Mode of Transport: Road Still Rules, but Multimodal Gains Traction

Road transport retained a 69.10% revenue share in 2025, but rail-linked corridors are growing at a 5.67% CAGR (2026-2031) as diesel inflation bites. The Eastern Turkey middle-corridor railway will elevate capacity twenty-six-fold by 2028, tilting bulk B2B parcels toward intermodal services.

Air freight underpins express expansion, with Istanbul Airport adding rapid-sort capacity that feeds premium lanes across the Turkey courier express and parcel market.

By Model: B2C Sustains Growth Leadership

B2C accounted for 53.44% of the Turkey courier express and parcel market share in 2025 and is advancing at a 5.91% CAGR between 2026-2031, propelled by mobile-commerce sales now equal to half of all online purchases. Quick-commerce volumes augment parcel density and keep van fill rates high. B2B traffic, led by automotive and textile exporters, yields superior per-parcel revenue yet expands more slowly. C2C remains the smallest niche but benefits from Turkey’s young, digitally savvy consumers trading via marketplaces.

Technology investments such as HepsiJet’s route-optimization engine are critical for B2C players juggling thin margins and stringent delivery windows. Platforms betting on algorithmic efficiency are set to capture incremental share within the Turkey courier express and parcel market.

Geography Analysis

Marmara, Aegean, and Central Anatolia regions together generated roughly 60% of 2025 domestic volumes, buoyed by Istanbul’s 220,000 e-commerce firms and Ankara’s strategic distribution location. The North Marmara Highway, due by 2027, will shave an estimated 20% off rush-hour delays, improving delivery predictability within the Turkey courier express and parcel market.

Aegean’s textile clusters spur rapid B2B turnaround, while Eastern Anatolia benefits from a USD 1.615 billion railway upgrade that multiplies freight capacity to 20 million t by 2028. Mediterranean ports enable Ro-Ro and coastal shipping, relieving pressure on long-haul trucks after diesel rose 44% in 2024.

Internationally, the EU captures 55% of outbound parcels thanks to A.TR duty advantages, Central Asia absorbs up to 20% on the back of eTIR digitalization, and the Middle East holds 25% aided by geographic proximity. The forthcoming Development Road to the Gulf will funnel additional B2B flows and reinforce Turkey’s bridge status between three continents.

Competitive Landscape

Competition is moderately consolidated, with the top three domestic firms plus four global integrators accounting for about 75-80% of handled parcels. FedEx’s USD 130 million hub, DHL’s takeover of MNG Kargo, and Austrian Post’s investment in Aras Kargo highlight a capital-intensive race to automate and densify networks.

Technology-centric entrants like HepsiJet and Kolay Gelsin chase niche gains through electric fleets and AI-based routing, trimming fleet kilometers and fuel spend.

Regulation remains permissive, yet labor volatility and lira depreciation widen performance gaps between cash-rich multinationals and lira-denominated local operators. Parcel-locker ecosystems and healthcare cold-chain projects are emerging battlegrounds poised to reshape share distribution inside the Turkey courier express and parcel market.

Turkey Courier, Express, And Parcel Industry Leaders

Aras Kargo

PTT Kargo

Yurtici Kargo

DHL Group

United Parcel Service of America, Inc. (UPS)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: FedEx opened a 25,300 m² express hub at Istanbul Airport, backed by USD 130 million, with 7,000-parcel-per-hour throughput.

- June 2025: Austrian Post confirmed its 80% stake in Aras Kargo after TRY 1.5 billion (USD 44.2 million) of cumulative investment, boosting capacity to 300,000 parcels per hour.

- October 2024: UPS expanded to 18 Turkish hubs, supporting a daily Istanbul-Cologne flight network.

- May 2024: PTT Kargo enhanced its mobile app with live tracking and Kargomat locker integration.

Turkey Courier, Express, And Parcel Market Report Scope

CEP stands as an abbreviation for courier, express, and parcel services that offer logistic services in areas. The services offered differ in the speed, weight, and volume of the packages and the way of carrying out the shipment of the goods. Especially, the regulations regarding weight and volume allow for vital standardization and great potential for automating the service. The report offers a complete background analysis of the Turkish courier, express, and parcel (CEP) market, including the market overview, market size estimation for critical segments, emerging trends by segment, and market dynamics. The report also offers the impact of COVID-19 on the market.

Turkey's courier, express, and parcel (CEP) market is segmented by business (B2B (business-to-business), and B2C (business-to-consumer)), destination (domestic and international), and end-user industry (services (BFSI (banking, financial services, and insurance), etc.), wholesale and retail trade (e-commerce), life sciences/healthcare, industrial manufacturing, and other end-user industries. The report offers market size and forecast values in USD billion for all the above segments.

Destination

| Domestic |

| International |

Speed of Delivery

| Express |

| Non-Express |

Model

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Consumer-to-Consumer (C2C) |

Shipment Weight

| Heavy Weight Shipments |

| Light Weight Shipments |

| Medium Weight Shipments |

Mode of Transport

| Air |

| Road |

| Others |

End User Industry

| E-Commerce |

| Financial Services (BFSI) |

| Healthcare |

| Manufacturing |

| Primary Industry |

| Wholesale and Retail Trade (Offline) |

| Others |

| Destination | Domestic |

| International | |

| Speed of Delivery | Express |

| Non-Express | |

| Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Consumer-to-Consumer (C2C) | |

| Shipment Weight | Heavy Weight Shipments |

| Light Weight Shipments | |

| Medium Weight Shipments | |

| Mode of Transport | Air |

| Road | |

| Others | |

| End User Industry | E-Commerce |

| Financial Services (BFSI) | |

| Healthcare | |

| Manufacturing | |

| Primary Industry | |

| Wholesale and Retail Trade (Offline) | |

| Others |

Key Questions Answered in the Report

How large is the Turkey courier express and parcel market in 2026?

The Turkey courier express and parcel market size stands at USD 3.10 billion in 2026.

What is the expected growth rate through 2031?

What is the expected growth rate through 2031?

Which delivery speed segment is growing fastest?

Which delivery speed segment is growing fastest?

How dominant are domestic deliveries?

How dominant are domestic deliveries?

Which region contributes most parcel traffic?

Which region contributes most parcel traffic?

Who are the leading players?

Aras Kargo, Yurtici Kargo, PTT Kargo, DHL, FedEx, and UPS are among the leading operators by handled volume.

Page last updated on: